The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 700+ that read this report daily, below!

Fundamental

The U.S. Treasury upped its borrowing estimate by $262 billion as federal revenue projections shifted.

Here’s why this matters.

Per Damped Spring’s Andy Constan, on an “overwhelming high issuance in Q1,” markets sold, and on “light issuance, once QT start[ed], plus some crazy tax receipts in Q3,” markets rallied.

With the Treasury’s debt managers seeking to borrow more than $400 billion through September, compared to the original estimate of $180 billion or so, anticipated is added borrowing through new marketable debt issuances.

“This is the reason I dumped my long equities after 3:00 when the news hit,” Constan added.

Overall, this news is important because it has an impact on the money available for circulation.

To explain, after the Federal Reserve (Fed) bean upping the size of its balance sheet (BS) in an unprecedented way in 2020, the deployment of this money – liquidity – boosted risk-asset prices and the cost of living.

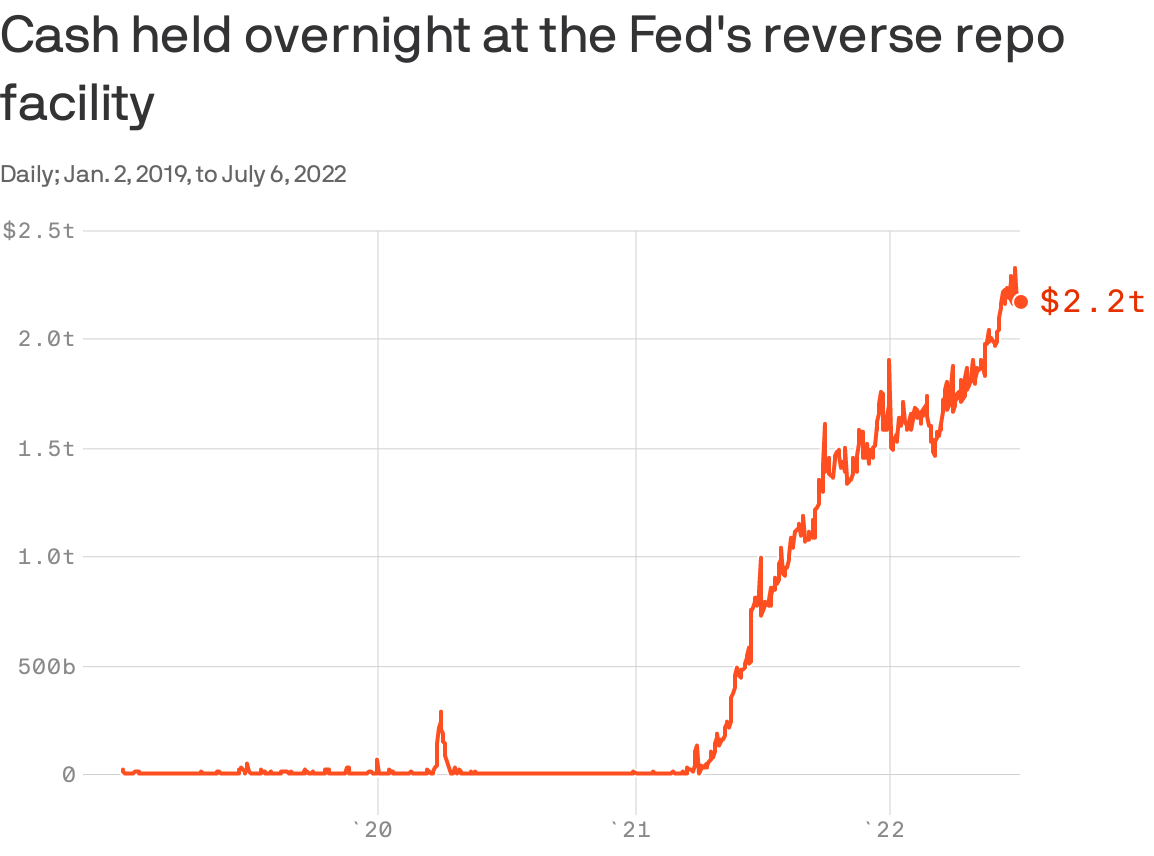

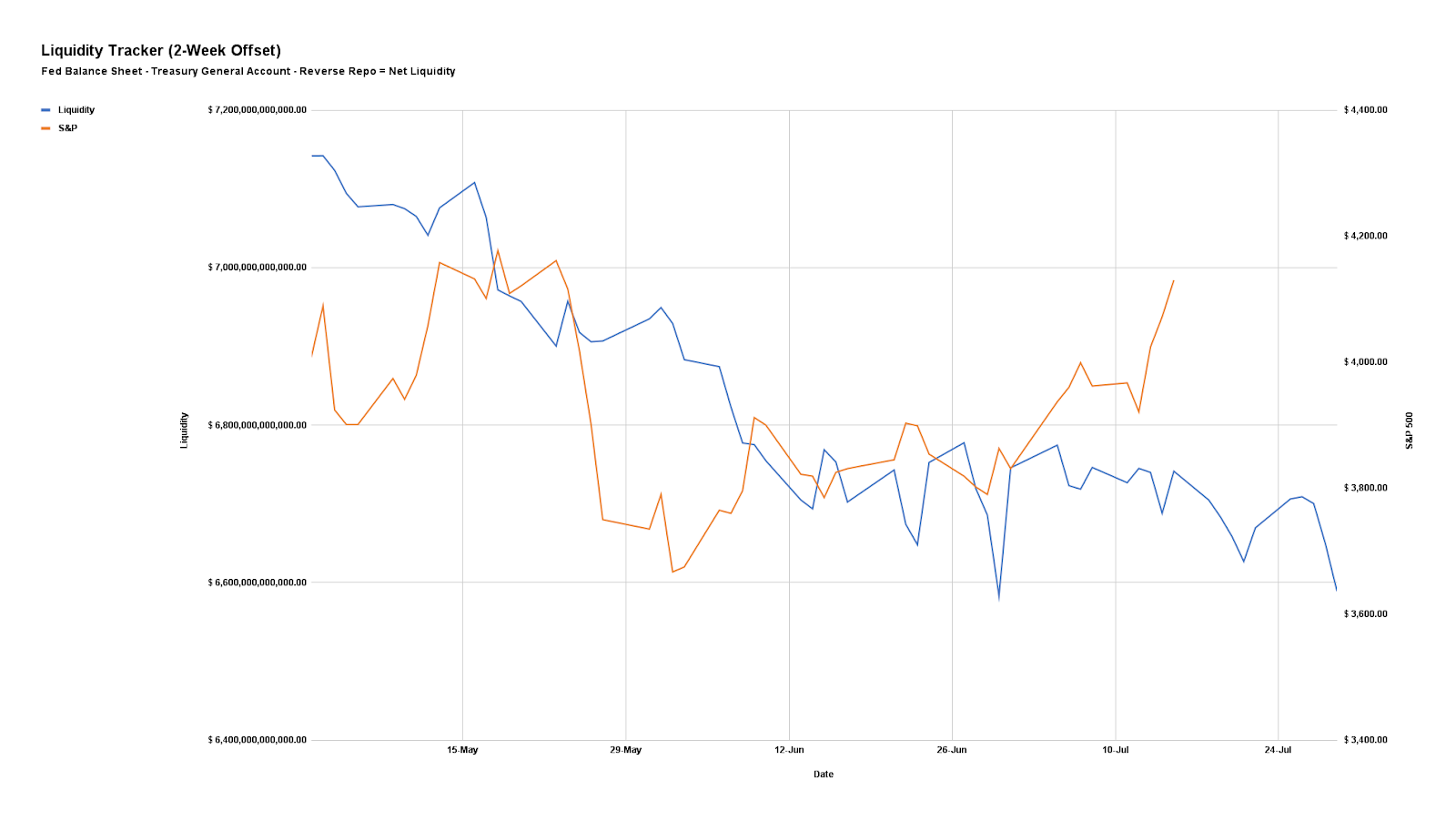

We can measure the availability of this liquidity, as well showcased by Max Anderson, online.

So, what’s going on, now?

To rein inflation, and undo some of its intervention, the Treasury issued fewer short-dated T-bills, and the Fed raised rates on Reverso Repo (RRP), “the next best low-duration-risk alternative.”

This has sucked over $2 trillion out of the economy, “six times more than ever done before.”

That said, unlike in the past, however, “relative changes in [the] Treasury General Account (TGA) and RRP” are way bigger than changes in the size of the BS.

As a result, the game changes.

The “changes in TGA and RRP have taken over as the primary drivers [of] Net Liquidity,” the money available to circulate in the economy. “[S]ince 2020, the Treasury and Reverse Repo [control] that. Not the size of Fed’s balance sheet.”

That’s per the tight correlation between Net Liquidity and the S&P 500. Offsetting the two by two weeks (i.e., using the path of Net Liquidity to forecast the path of the S&P 500 by two weeks in advance) reveals a tight correlation.

As Anderson puts it, “when there’s a change in Liquidity, it takes two weeks to propagate out into the economy and impact asset prices. And that change in Liquidity predicts next two week’s change in asset prices with 95% correlation.”

See a file containing the data and charts, here. We’ll work to improve the charts in subsequent letters.

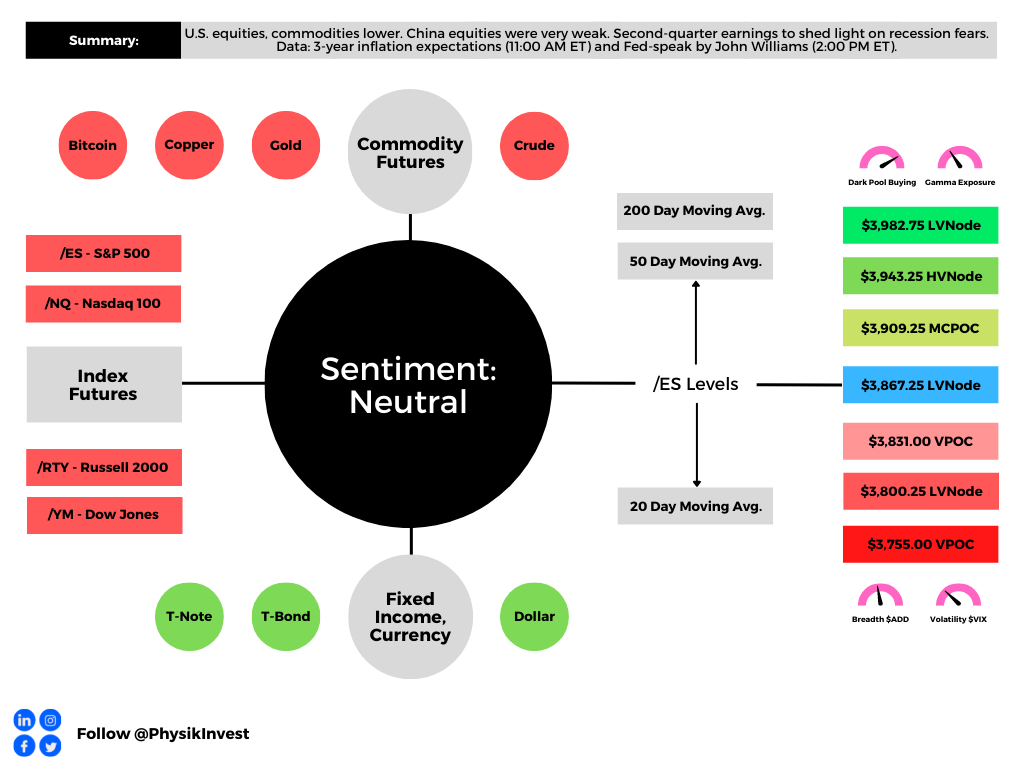

Positioning

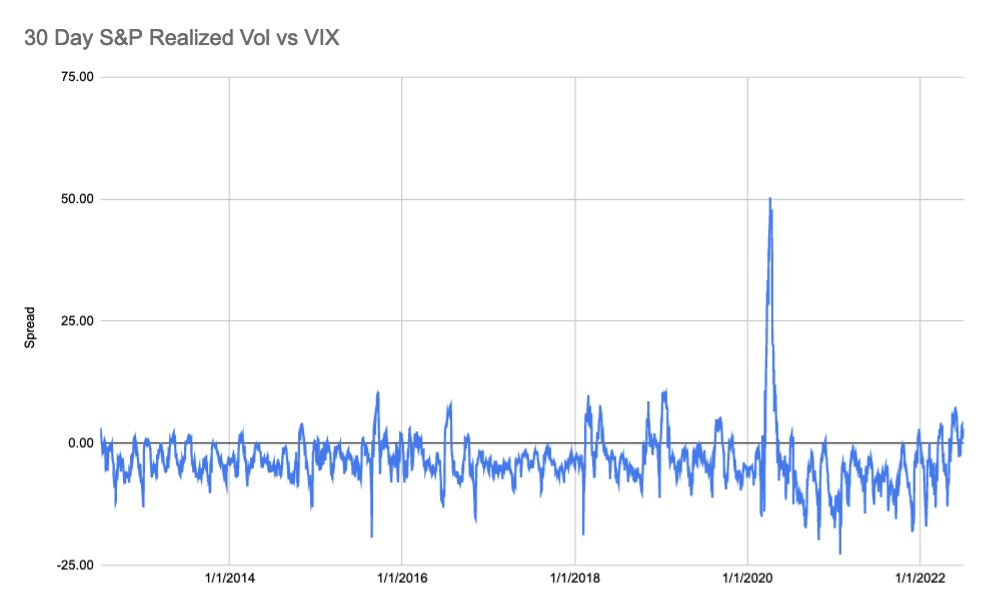

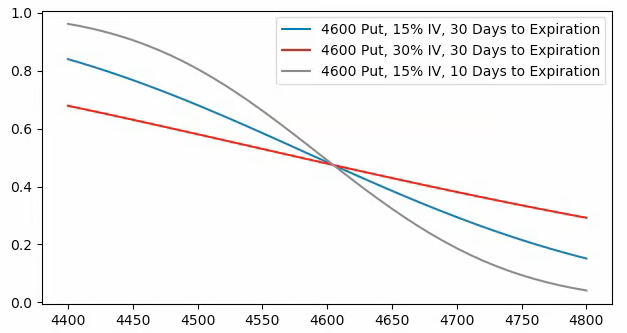

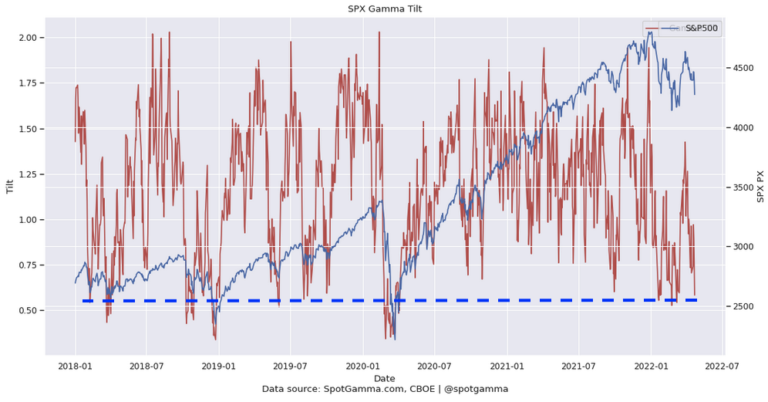

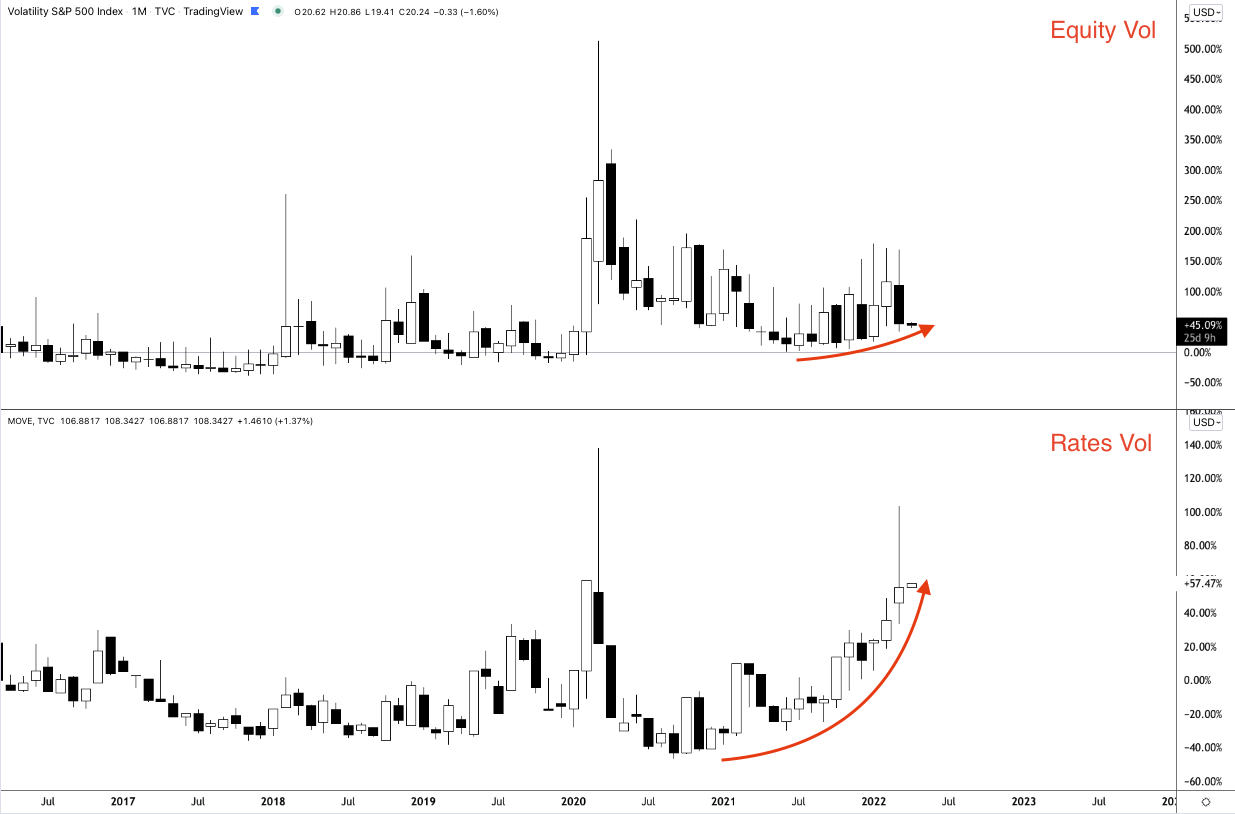

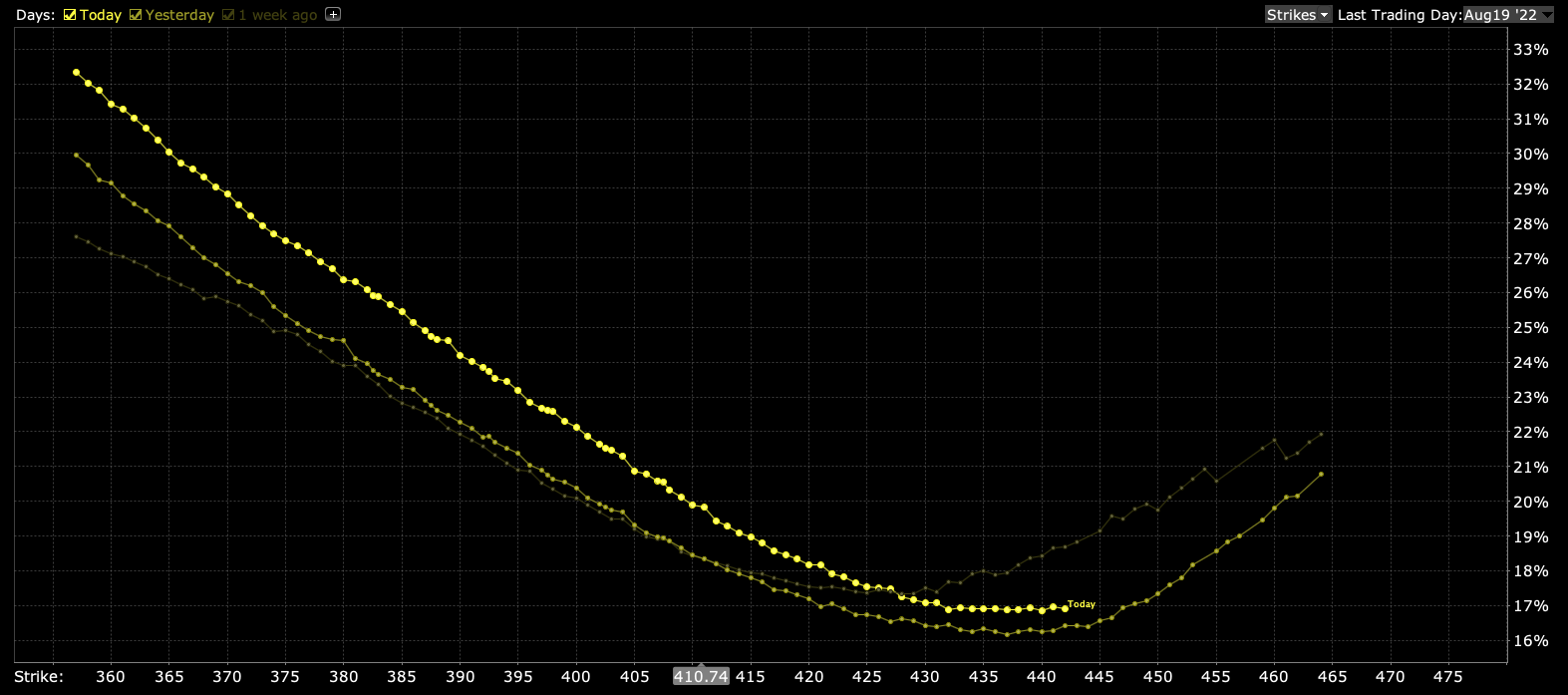

As of 6:30 AM ET, Tuesday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.29%. Net gamma exposures increasing may promote tighter ranges.

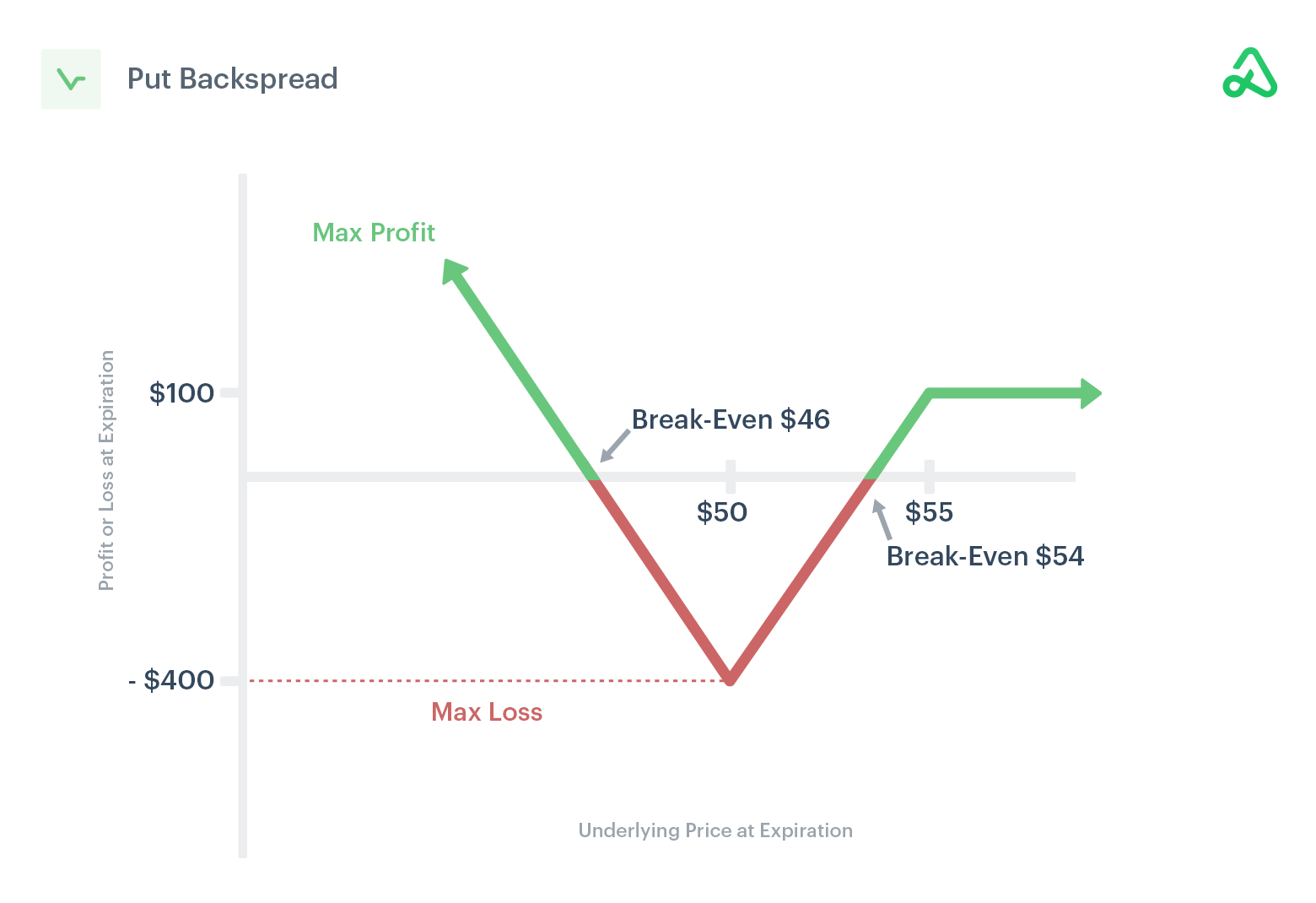

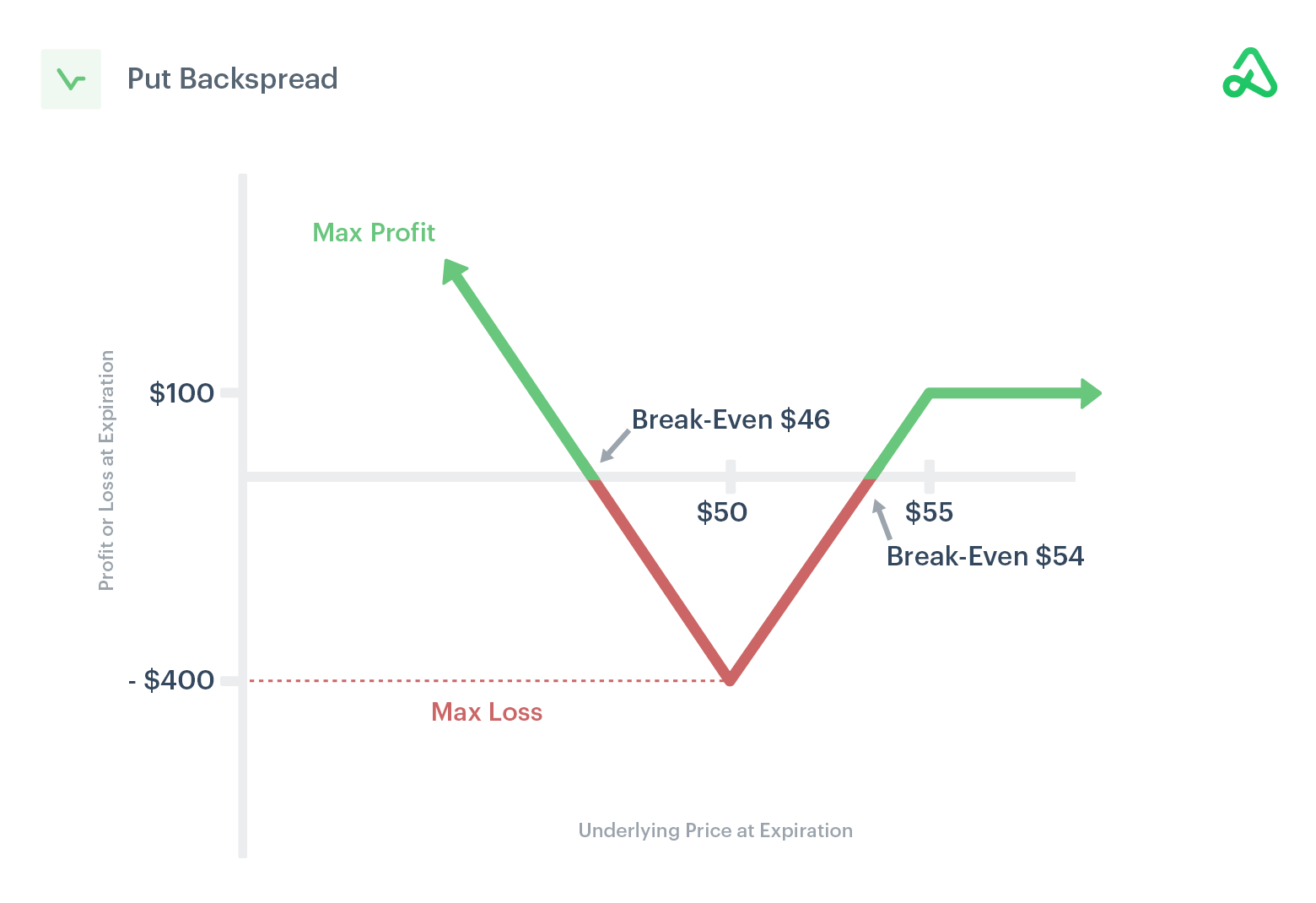

Given where realized (RVOL) and implied (IVOL) volatility measures are, as well as skew, it is beneficial to be a buyer of complex options structures (e.g., back spreads).

The reason why?

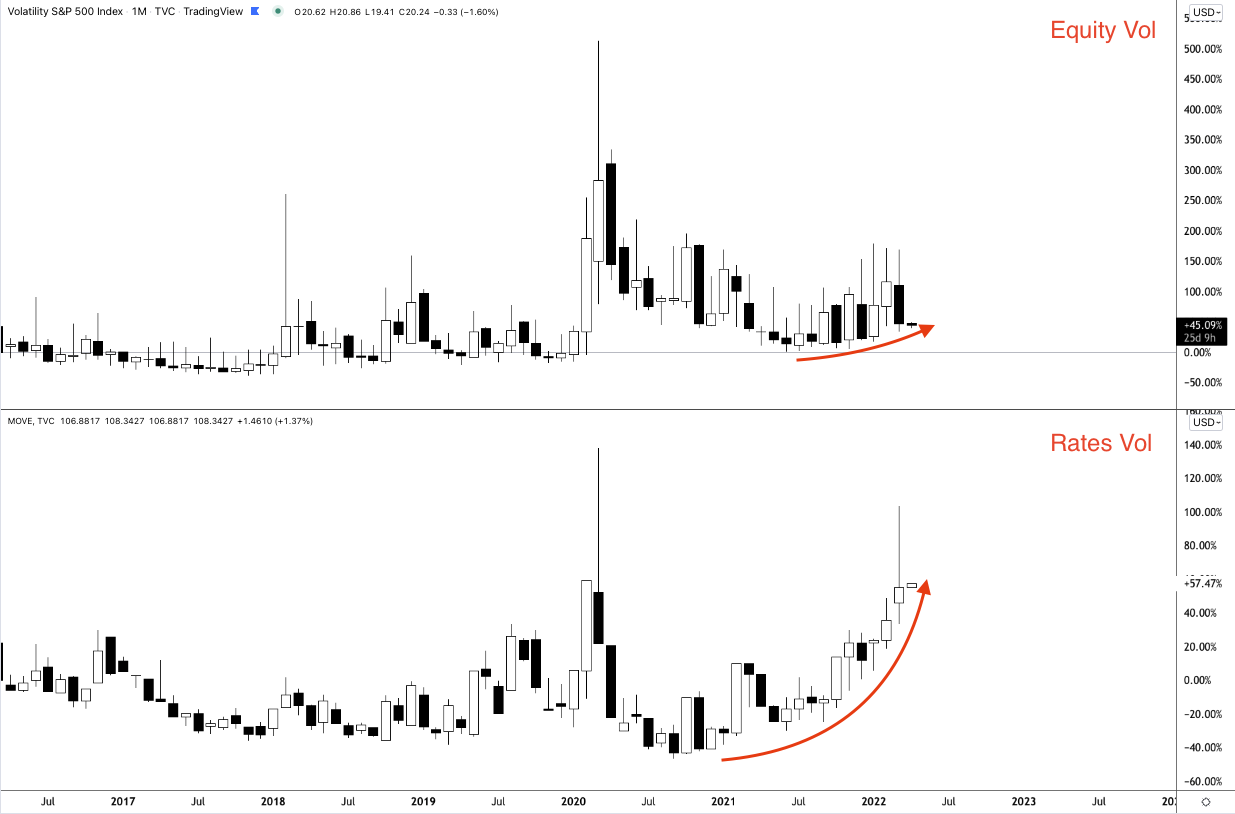

Pursuant to our comments on monetary policymakers ditching forward guidance, which, per the Macro Compass’ Alfonso Peccatiello leaves “no anchor for bond markets, … and higher volatility,” bolsters risk premia “everywhere else.”

As stated Monday, this does more to support our recent positioning analyses and the case for an “untethering” in equity IVOL, “one of the most supportive things into the decline,” per statements by Kai Volatility’s Cem Karsan.

Here’s some context.

As well explained in the Daily Brief for July 21, 2022, heading into the 2022 decline, institutions repositioned and hedged, even allocating to “commodity trend following,” per our Daily Brief for July 15, 2022, which worked well the first two quarters.

The monetization and counterparty hedging of existing customer hedges, as well as the sale of short-dated volatility, particularly in some of the single names where there was “rich” volatility, into the fall, lent to lackluster performance in IVOL and index mean reversion.

This trend is coming to an end as entities are squeezed out of trades that aren’t working (i.e., participants rotate out of volatility and commodities).

Per Karsan, as “volatility itself, on the equity side, becomes less and less hedged on the customer level, … [the] market can really begin to respond to the core macro factors.”

Should markets experience a shock (e.g., China and U.S. tensions escalate), the new demand for hedges may result in an “untethering” in IVOL, which was “one of the most supportive things into the decline,” Karsan said, adding that now is the best time to rotate into call options which are outperforming “their delta to the upside.”

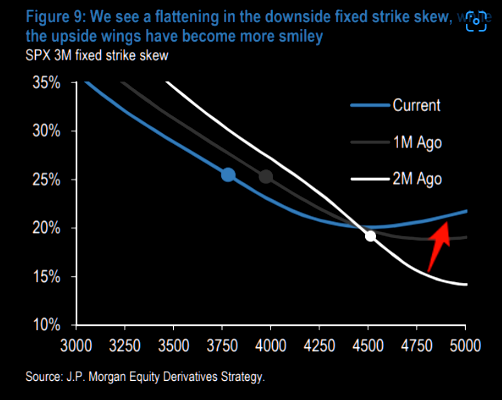

Accordingly, given the macro risk, IVOL is likely at a lower bound (as validated by the S&P 500 trading higher and downside skew holding a bid) and, per The Ambrus Group’s Kris Sidial, “if you wanted to go out and hedge, the opportunity is still there in the equity space.”

Through downside protection (e.g., butterfly and back spreads) you can position yourself to monetize on the sort-of non-linear repricing in volatility we’re alluding there is potential for. The bid in skew is helping those structures maintain their value better, essentially.

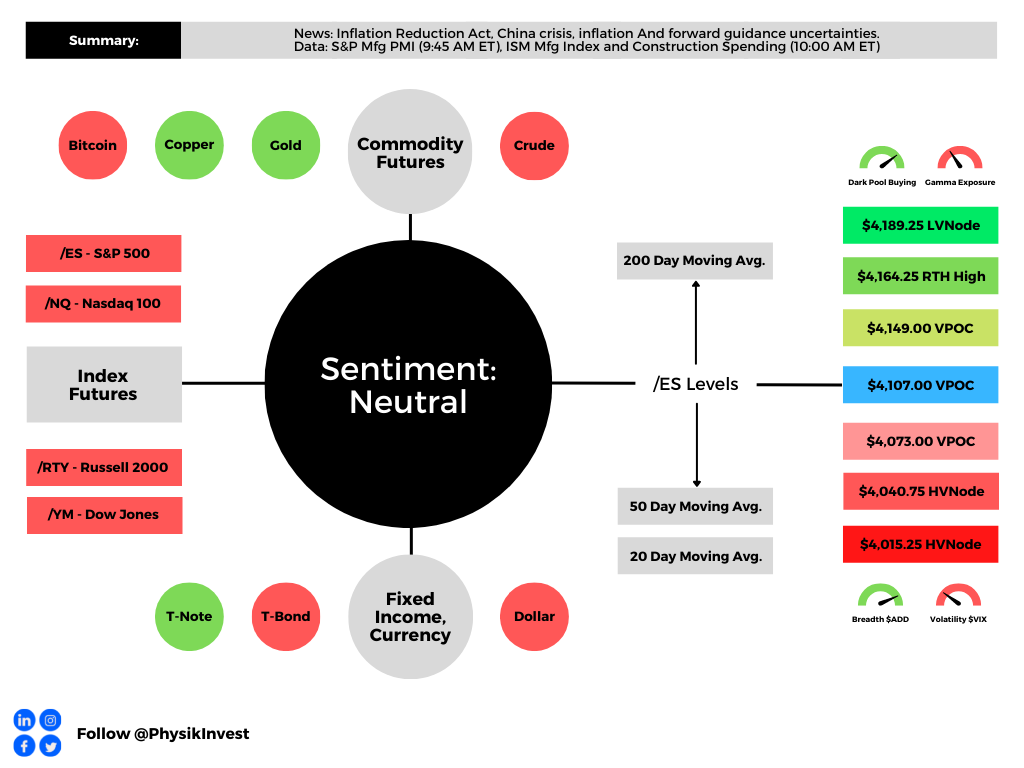

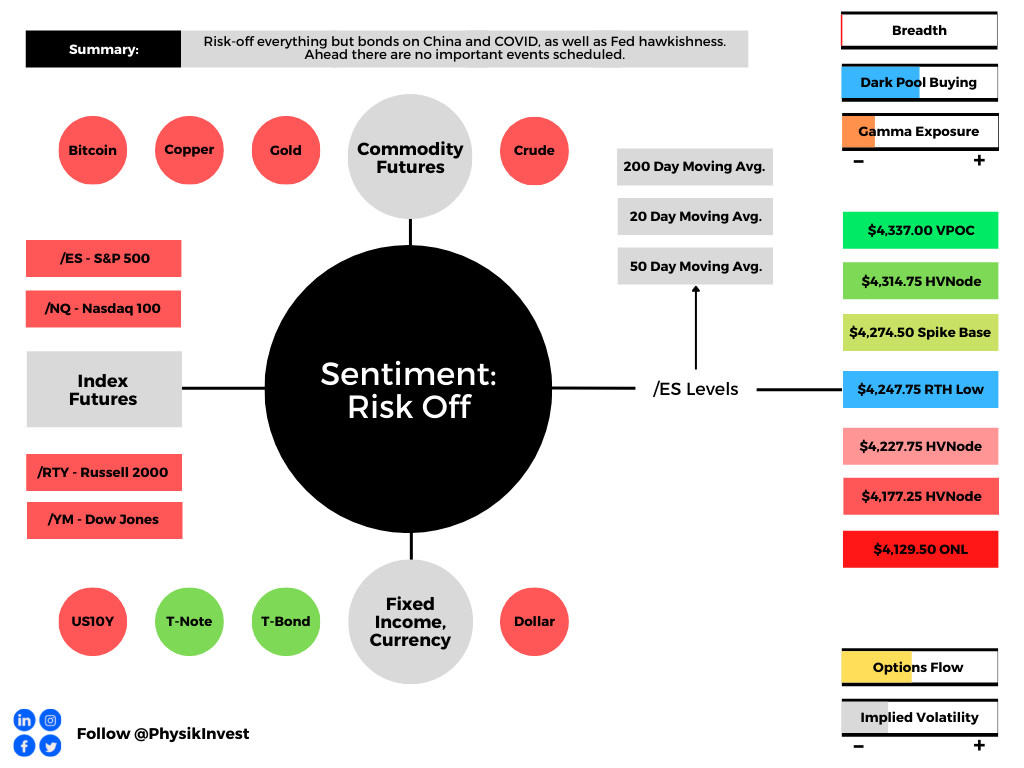

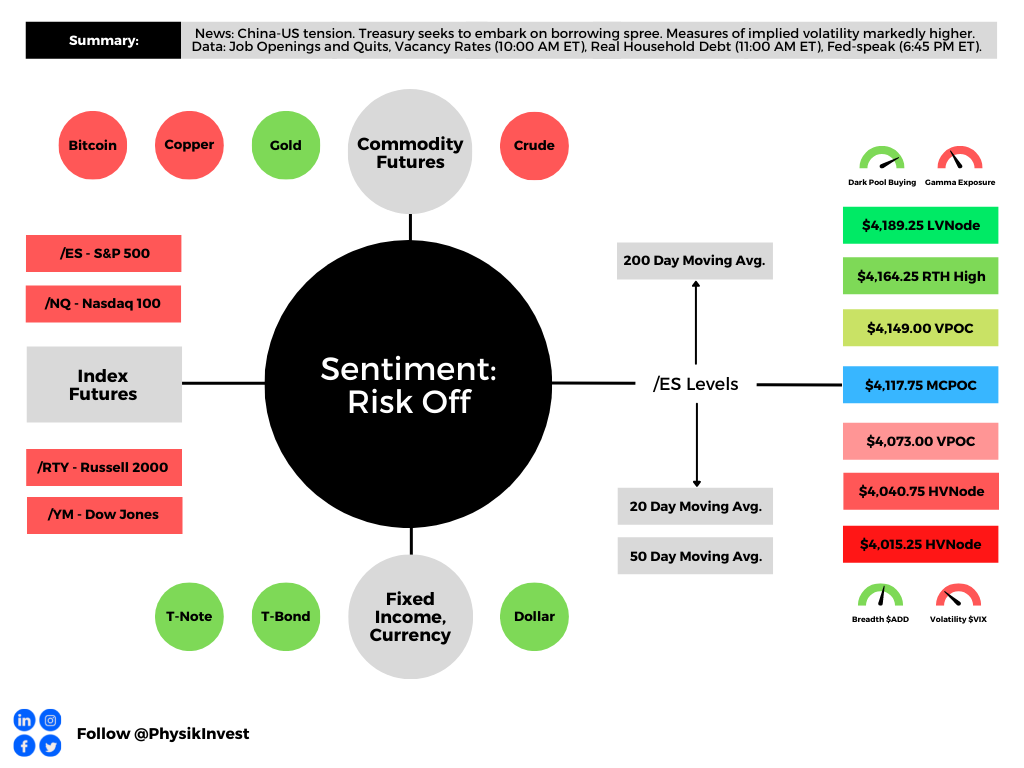

Technical

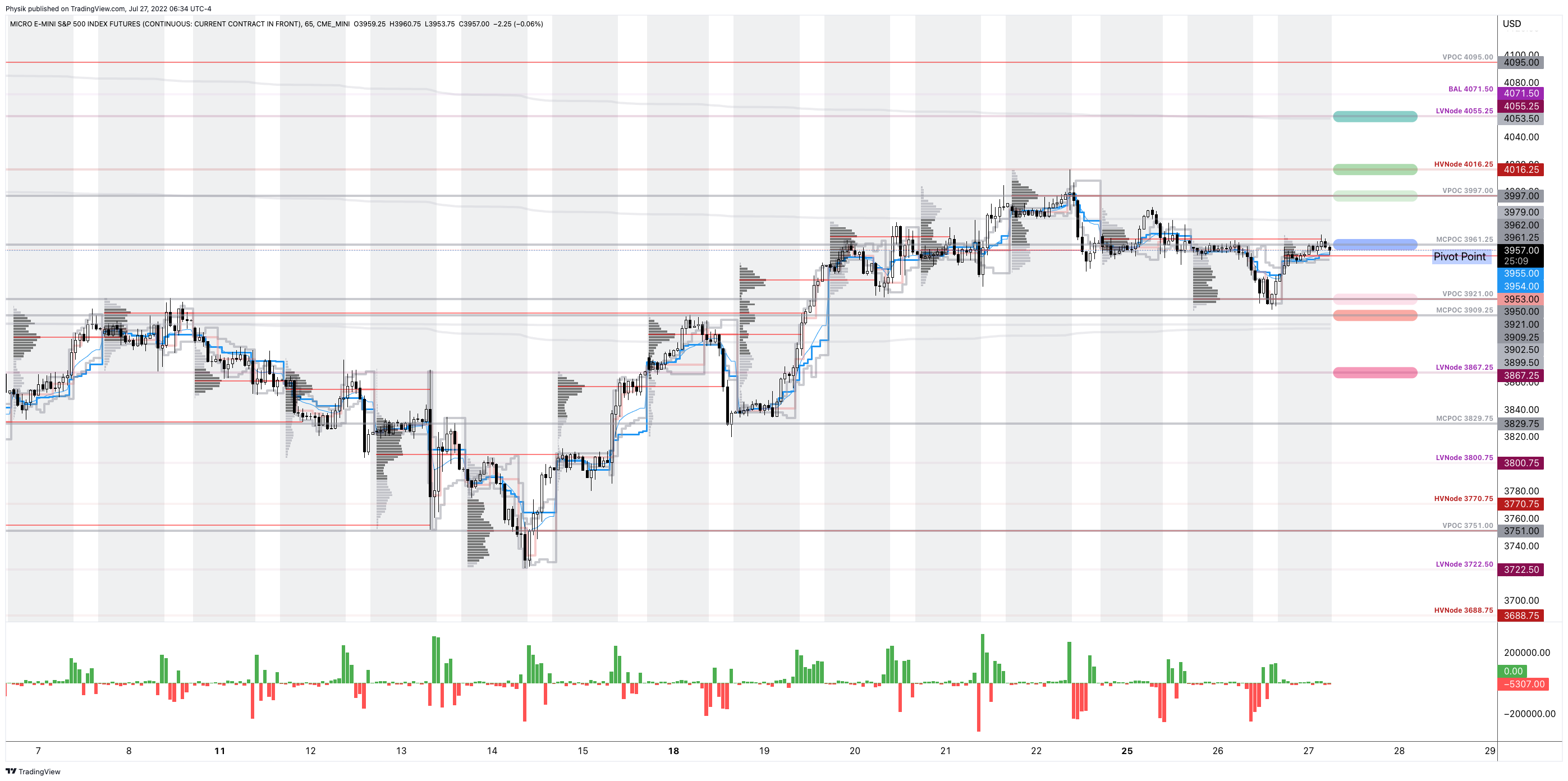

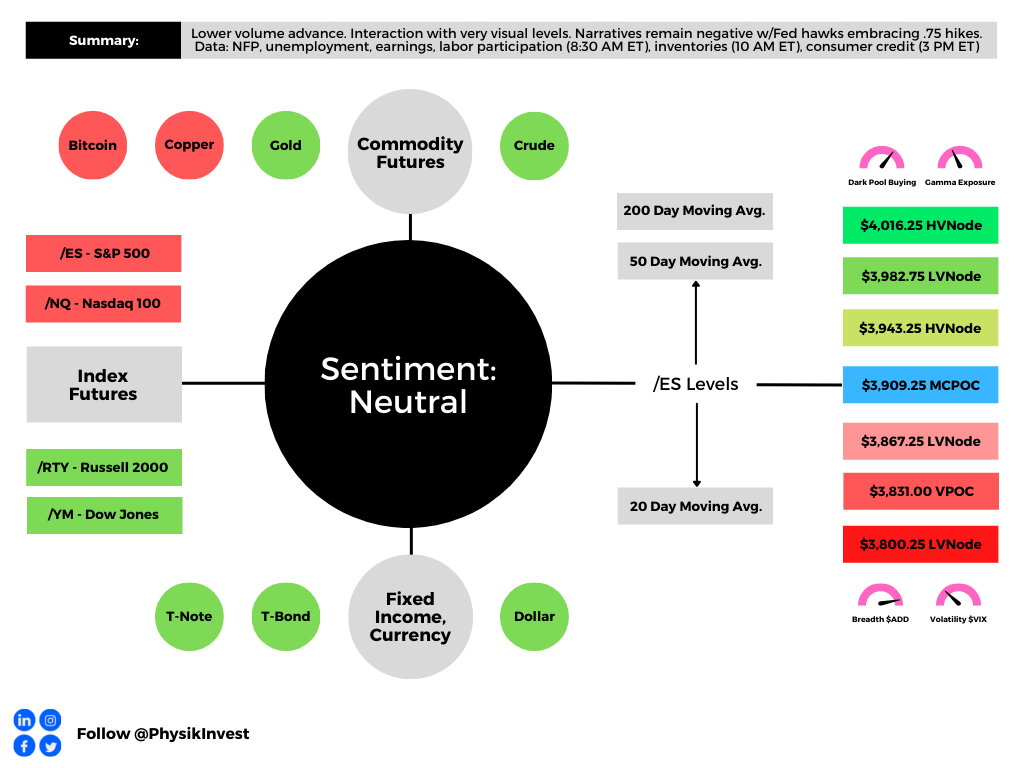

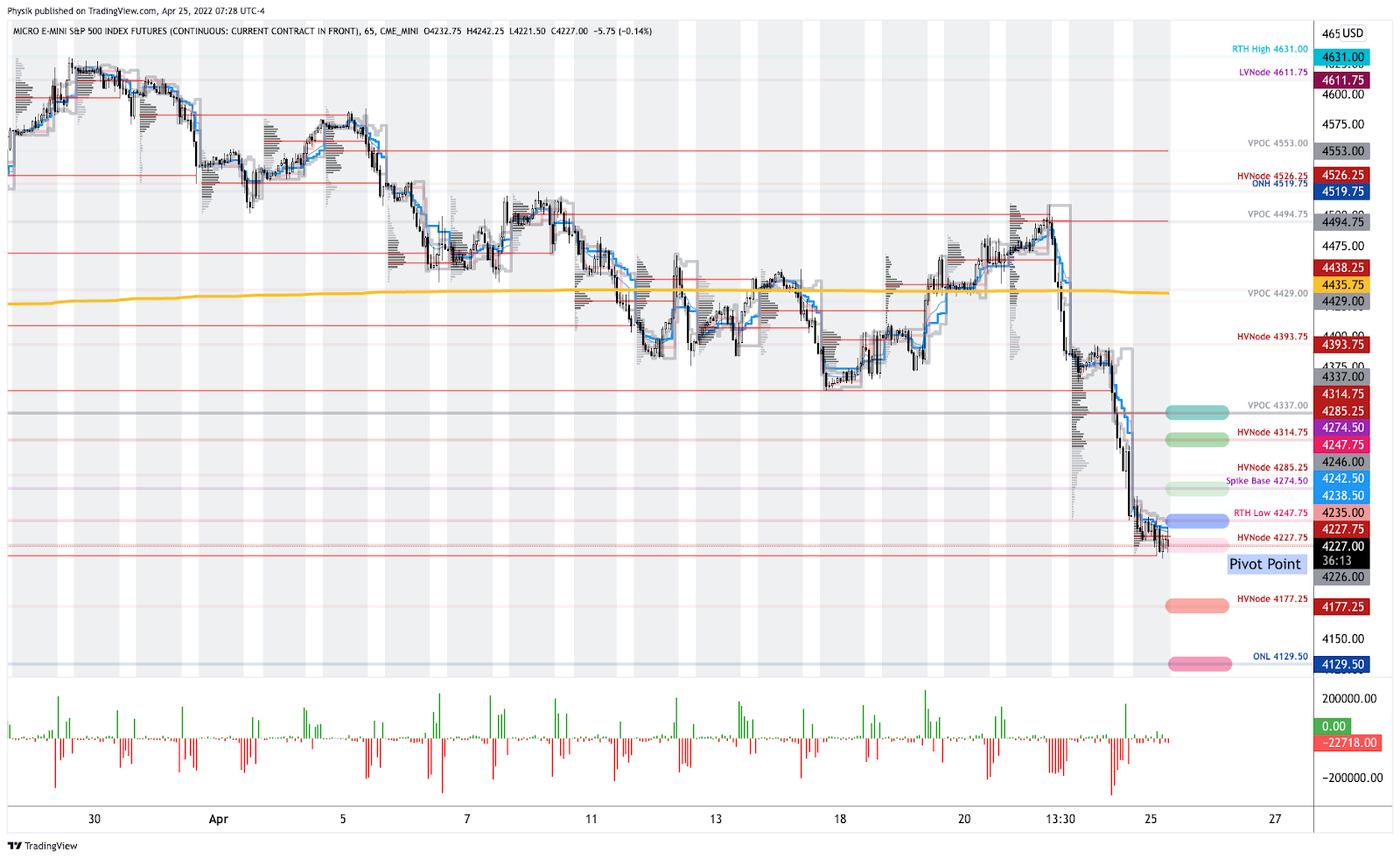

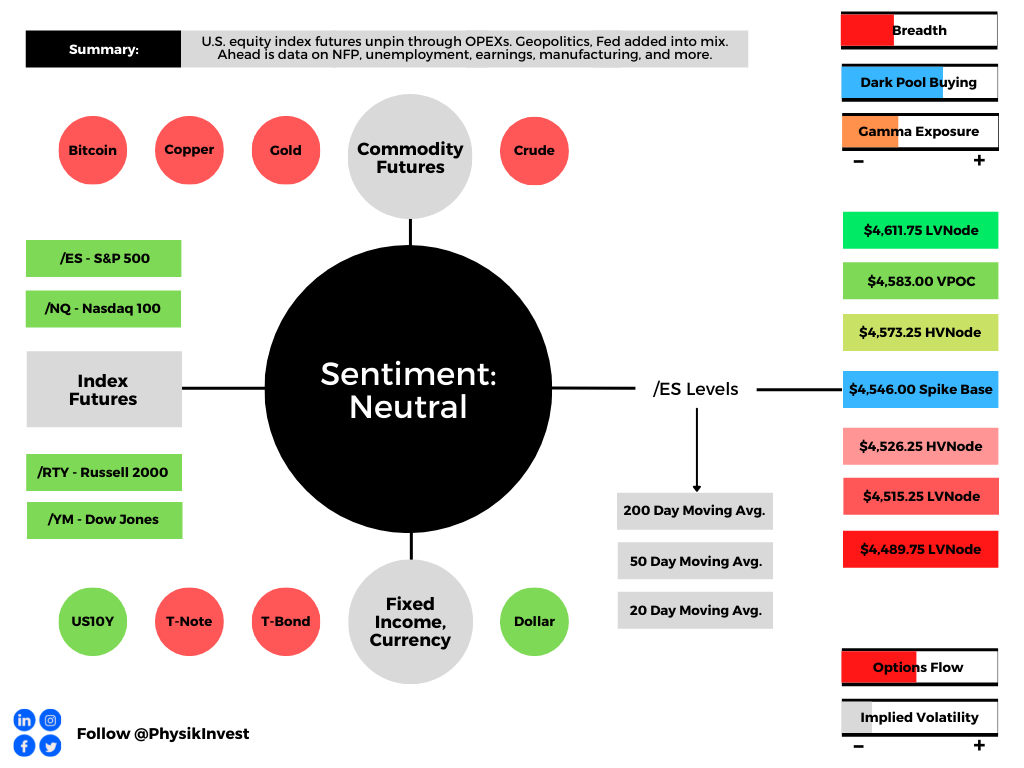

As of 6:30 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $4,117.75 MCPOC puts into play the $4,149.00 VPOC. Initiative trade beyond the VPOC could reach as high as the $4,164.25 RTH High and $4,189.25 LVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $4,117.75 MCPOC puts into play the $4,073.00 VPOC. Initiative trade beyond the VPOC could reach as low as the $4,040.75 and $4,015.25 HVNodes, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.