Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Positioning

In The Second Leg Down: Strategies For Profiting After A Market Sell-Off, there is one passage on the inaccuracy of normal distributions in markets and serial correlation, as well as the underpricing of rare events. In that same passage, Nassim Nicholas Taleb is credited for his advocacy on portfolio allocations to safe short-term government bonds and high-risk speculative bets through which “you could lose no more than your initial investment.”

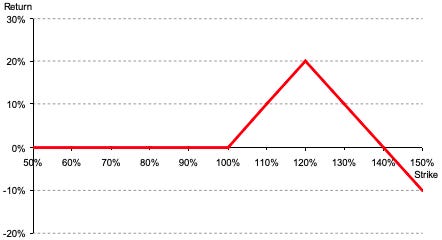

Naturally, this leads to Exotic Options and Hybrids. Structured notes, to quote chapter two, are “composed of a non-risky asset providing a percentage of protected capital and a risky asset offering leverage potential.”

The structure, as a whole, is not risky in the absence of defaults. The bond, which is bought at a discount, increases in value until maturity. The difference between the initial value to allocate (100% of notional) and the bond purchase price is allocated to the leverage (e.g., options) component of the structure.

This type of capital-protected structure is particularly attractive right now, given the interest rate environment. That’s because high-interest rates decrease the initial value of the bond. This means we can allocate more to leveraged bets, for example.

During the life of the structured note, the value of the non-risky part increases when interest rates decrease. At maturity, the value of the bond component is equal to 100% of the notional while the value of the riskier part of the note is “non-linear and fluctuates depending on many market parameters such as the underlying’s spot, interest rates, borrowing costs, dividend yield or volatility.”

Last week, IPS Strategic Capital’s Pat Hennessy wrote a thread on how to apply this information.

Basically, with interest rates near 5% at the front of the yield curve, and traditional portfolio constructions performing poorly, defined-outcome investing is attractive.

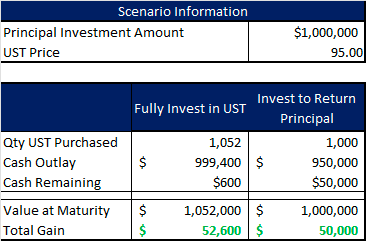

With $1,000,000 to invest and rates at ~5% (i.e., $50,000 is 5% of $1,000,000), one could “purchase 1000 USTs [or S&P 500 (INDEX: SPX) Box Spreads] which will have a value of $1 million at maturity for the price of $950,000.”

With $50,000 left in cash, one can use options for leveraged exposure to an asset of their choosing, Hennessy explained. Should these options expire worthless, the $50,000 gain from USTs, at maturity, provides “a full return of principal.”

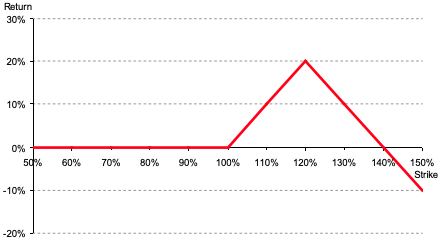

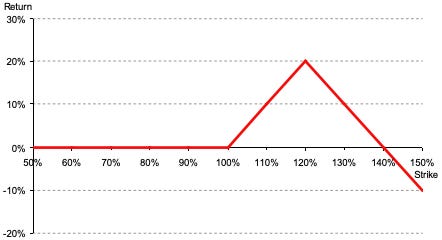

In an example, Hennessy presented a structure providing 60% of the upside gain of the S&P 500 with full principal protection should markets fall. Though “you may initially scoff at 60%, [] keep in mind that historically 60/40 has captured between 60-70% of the upside of equities.”

If you’re bearish or unopinionated, Hennessy presented capital-protected structures that make money if the market moves lower (e.g., instead of buying a call option on the SPX, buy put options or a put options spread) or sideways (e.g., sell defined-risk option condor structures).

Markets have a tendency to move big and continue moving big in the same direction, over the very short term, hence the “fat tails in the distribution over short horizons,” to quote The Second Leg Down. Given this, your letter writer can use his analyses to capitalize big on underpricing and participate in upside or downside through a series of short-dated options bets (e.g., butterflies, broken-wing butterflies, ratio spreads, back spreads, and beyond) that, in time, may return in excess of ~10 times the initial investment. Should nothing happen, then he walks away with his principal. That’s trading made less stressful.

Have a great day. If you enjoyed today’s letter, consider sharing it with your friends!

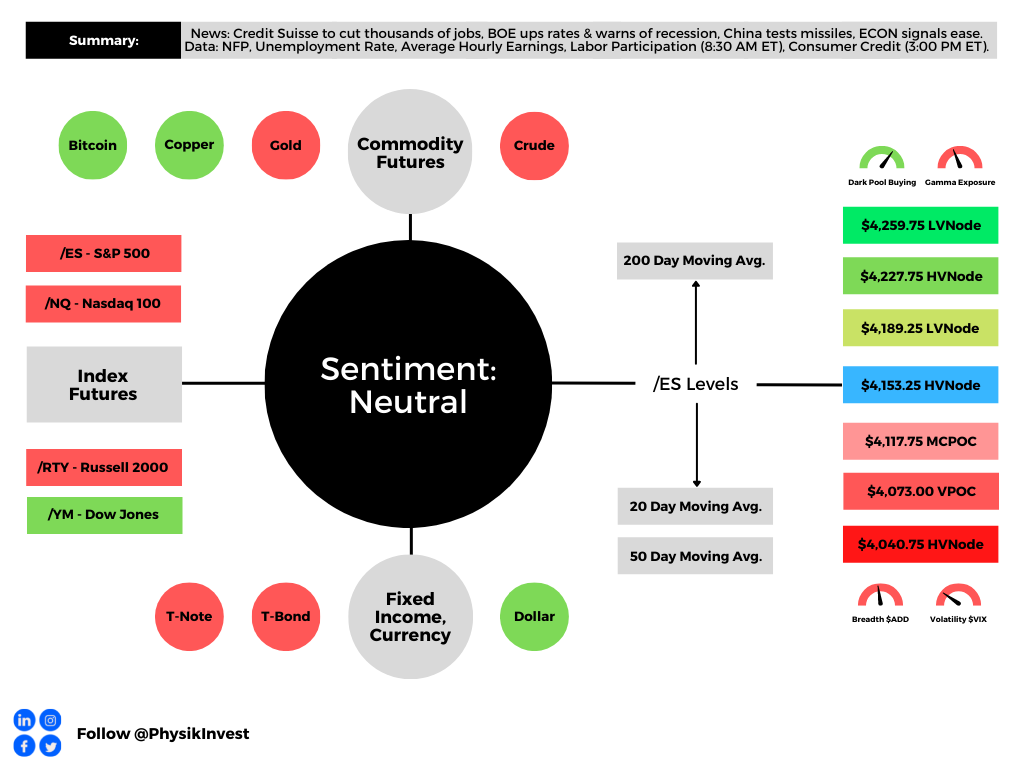

Technical

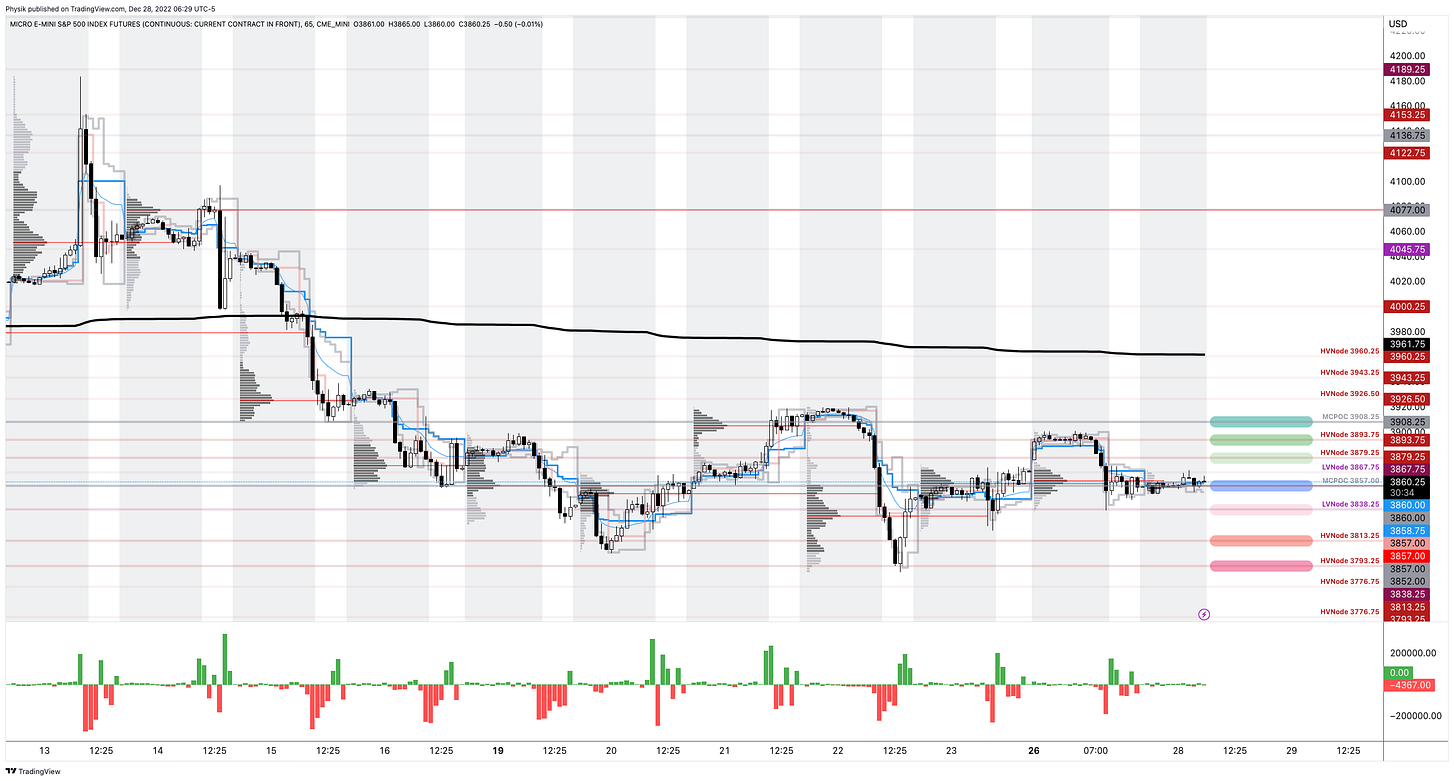

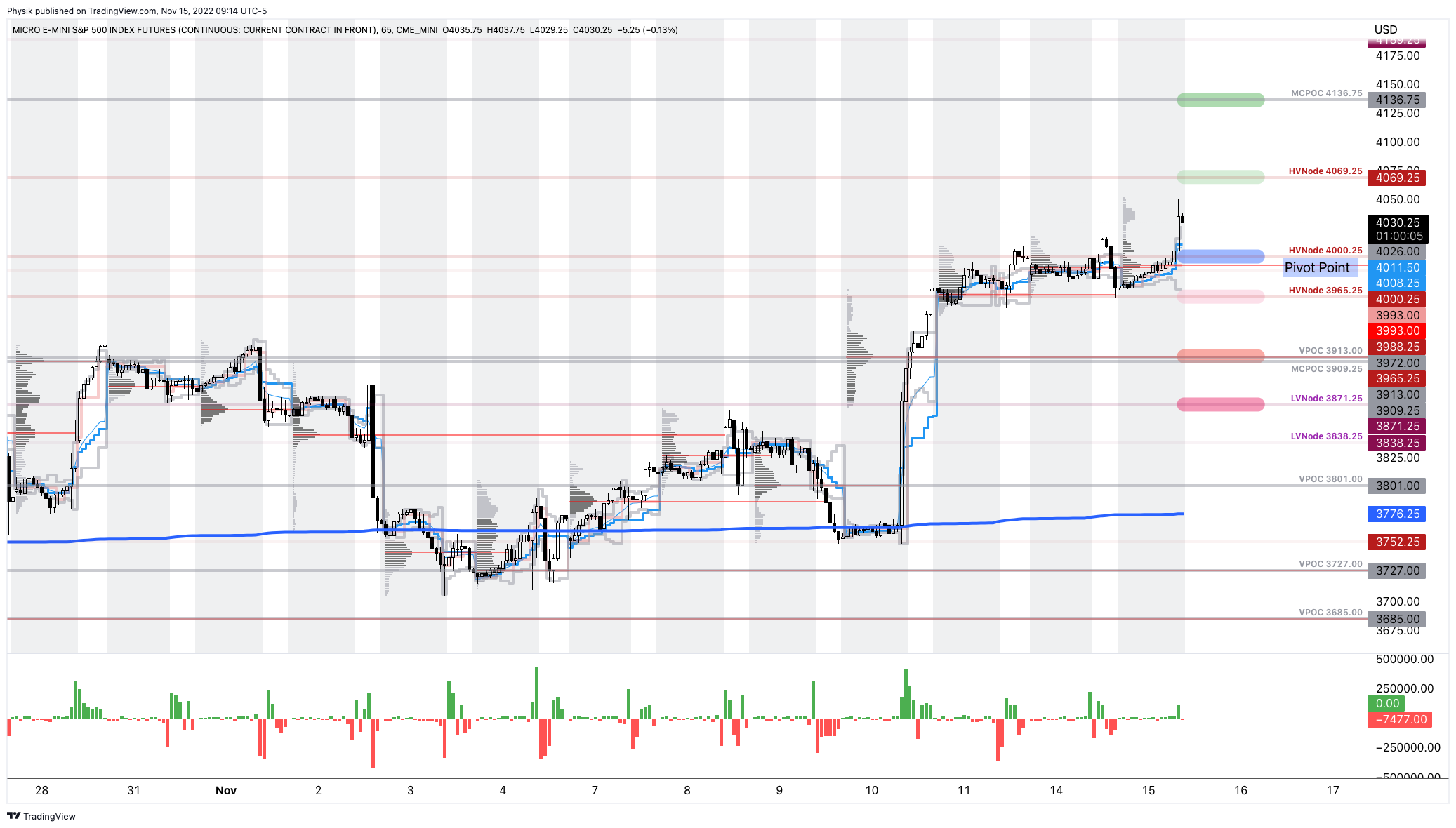

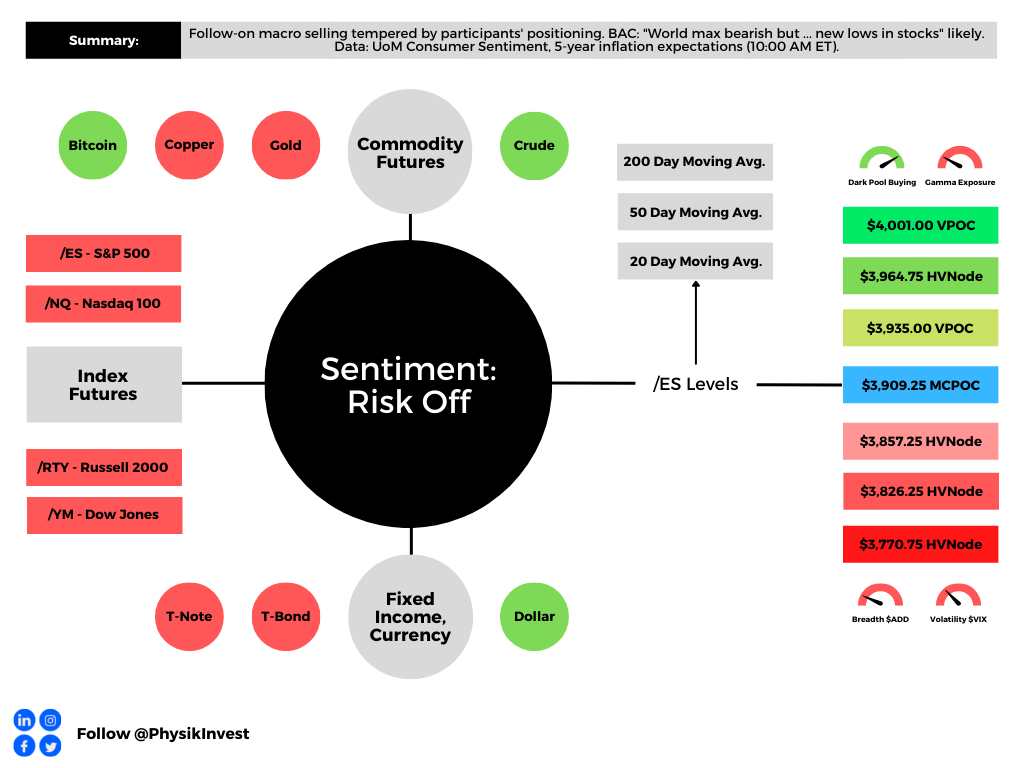

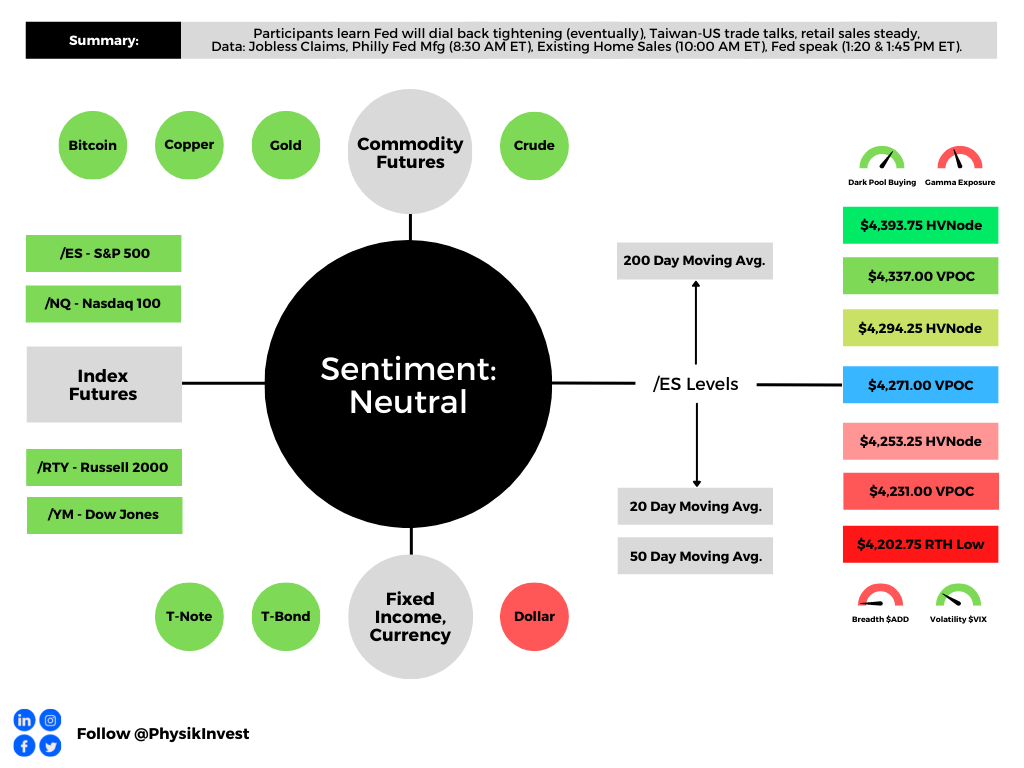

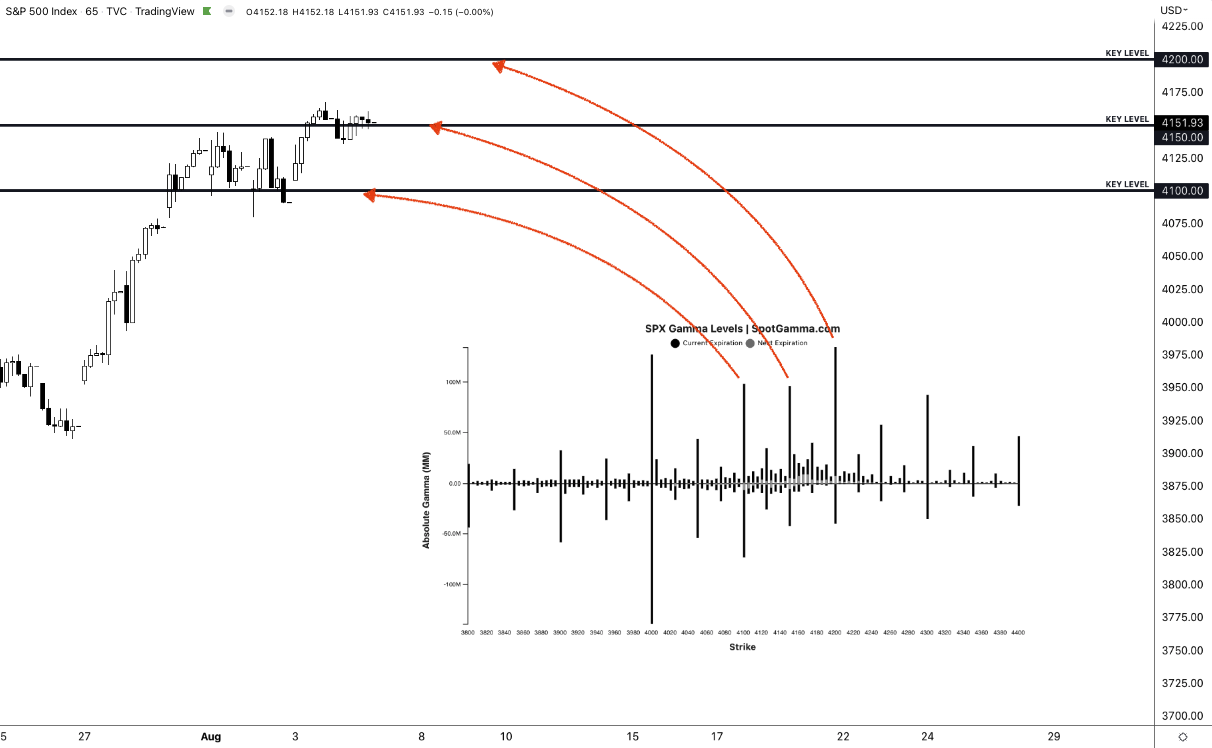

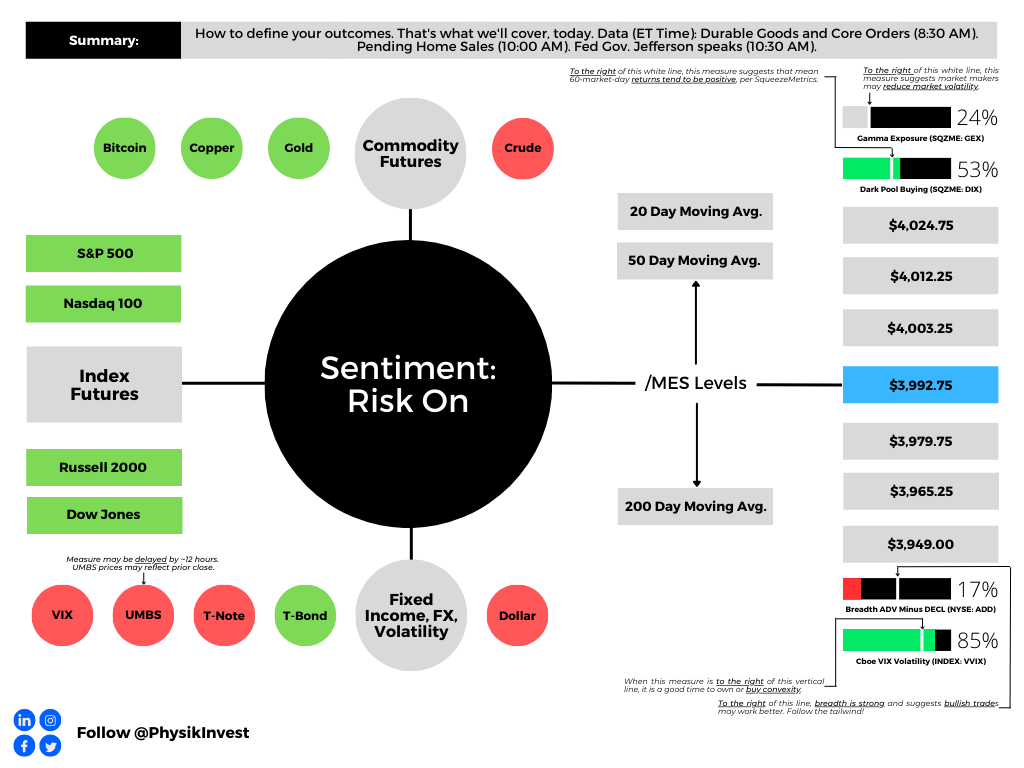

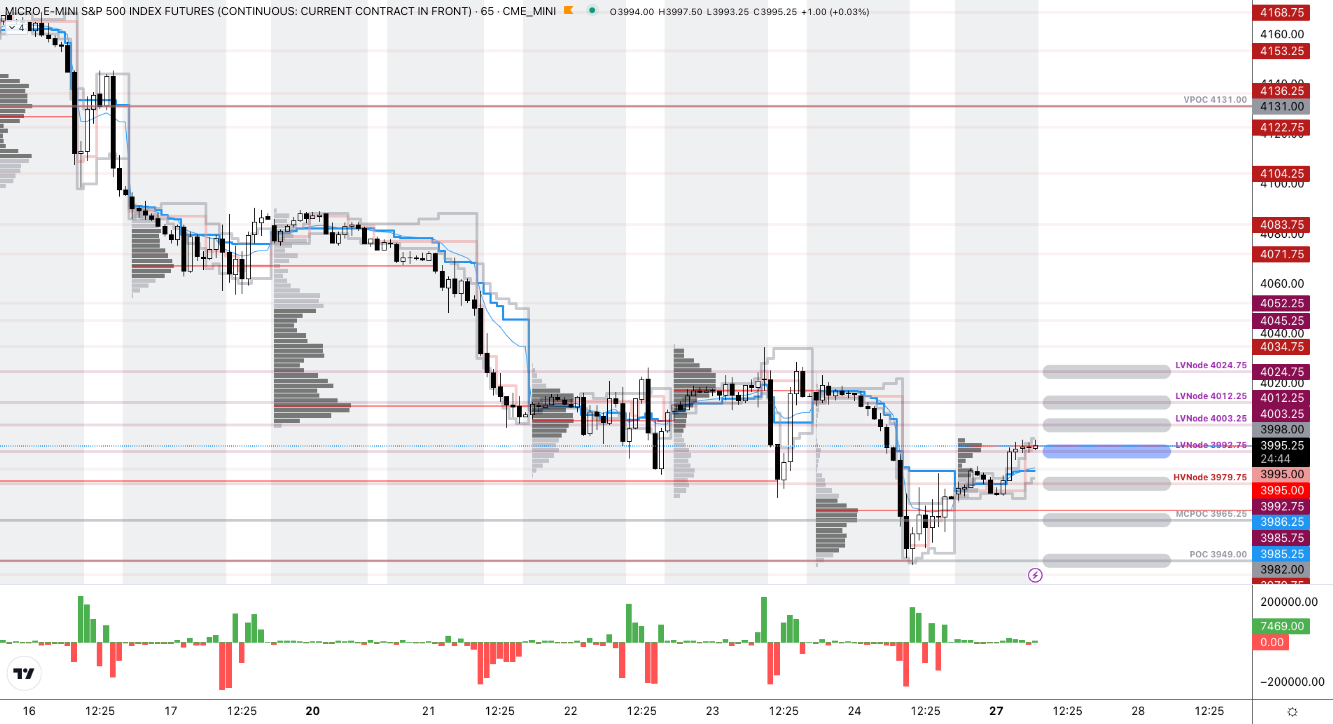

As of 7:40 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, outside of the prior day’s range, suggesting a potential for immediate directional opportunity.

The S&P 500 pivot for today is $3,992.75.

Key levels to the upside include $4,003.25, $4,012.25, and $4,024.75.

Key levels to the downside include $3,979.75, $3,965.25, and $3,949.00.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Definitions

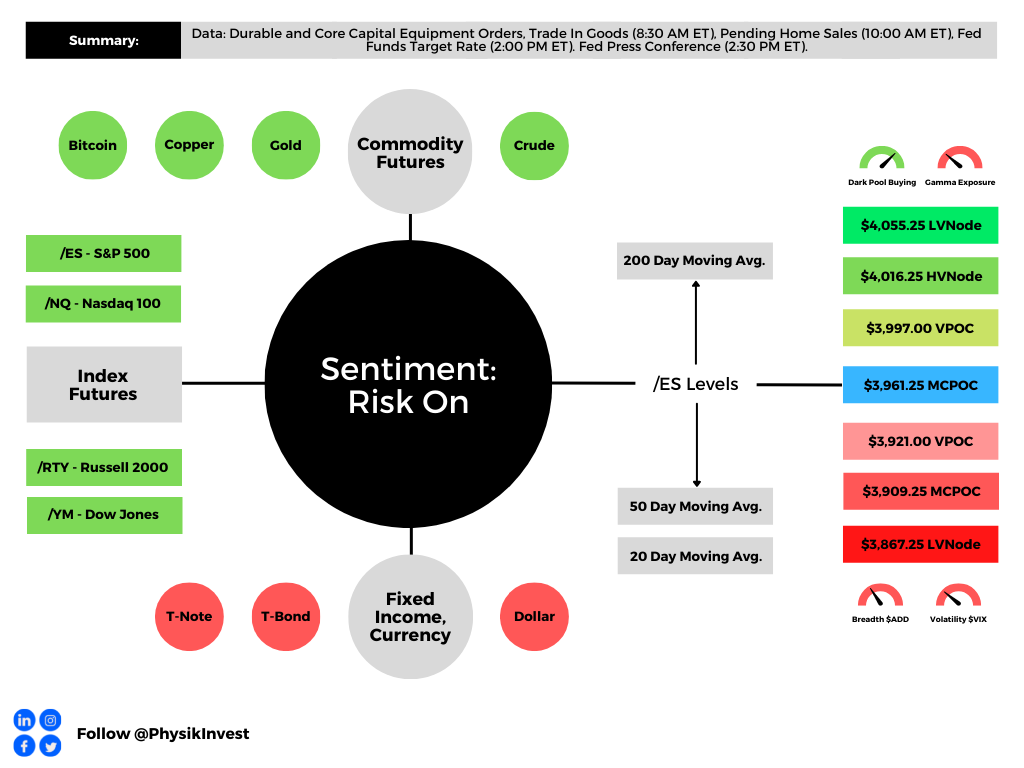

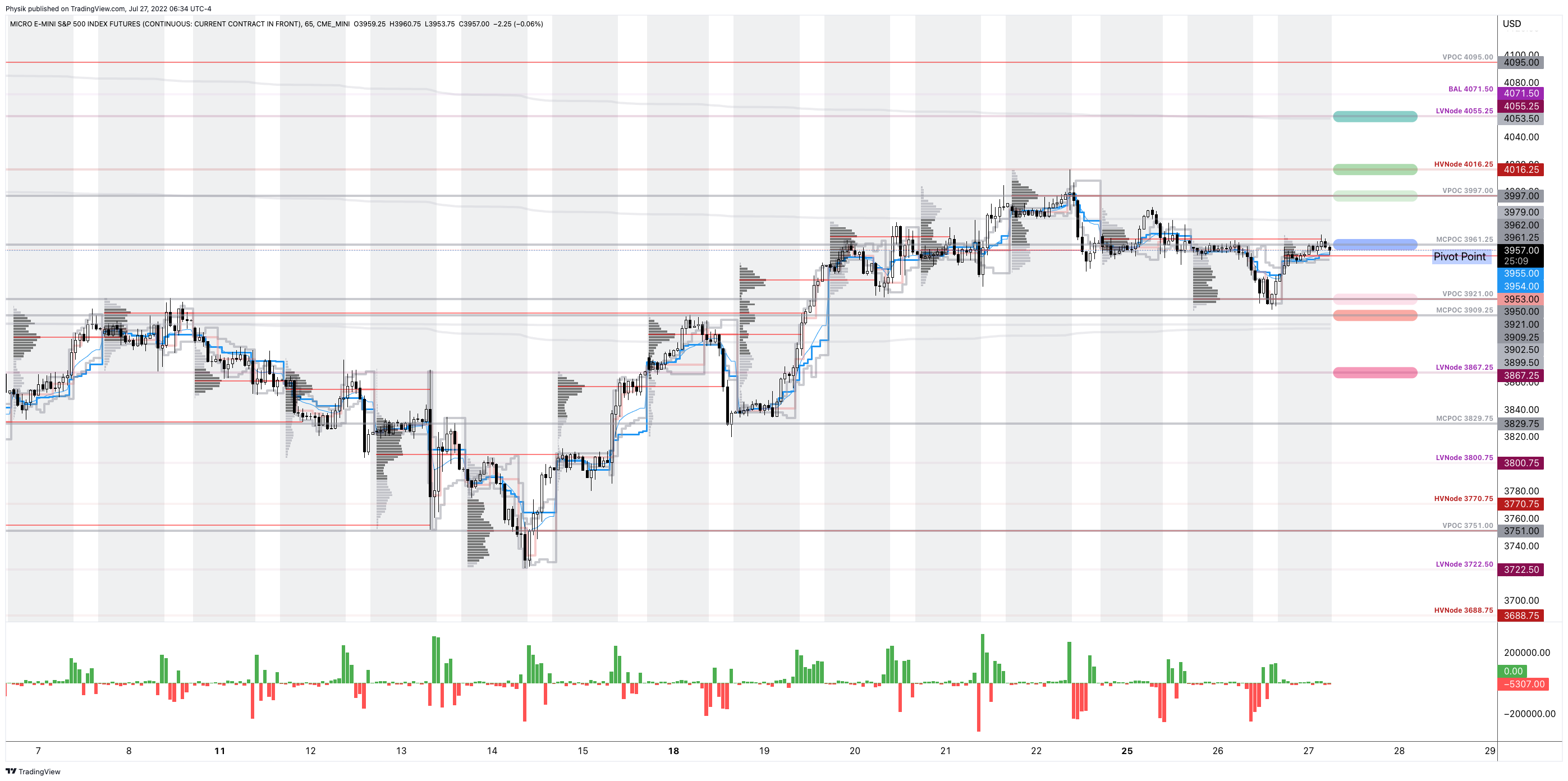

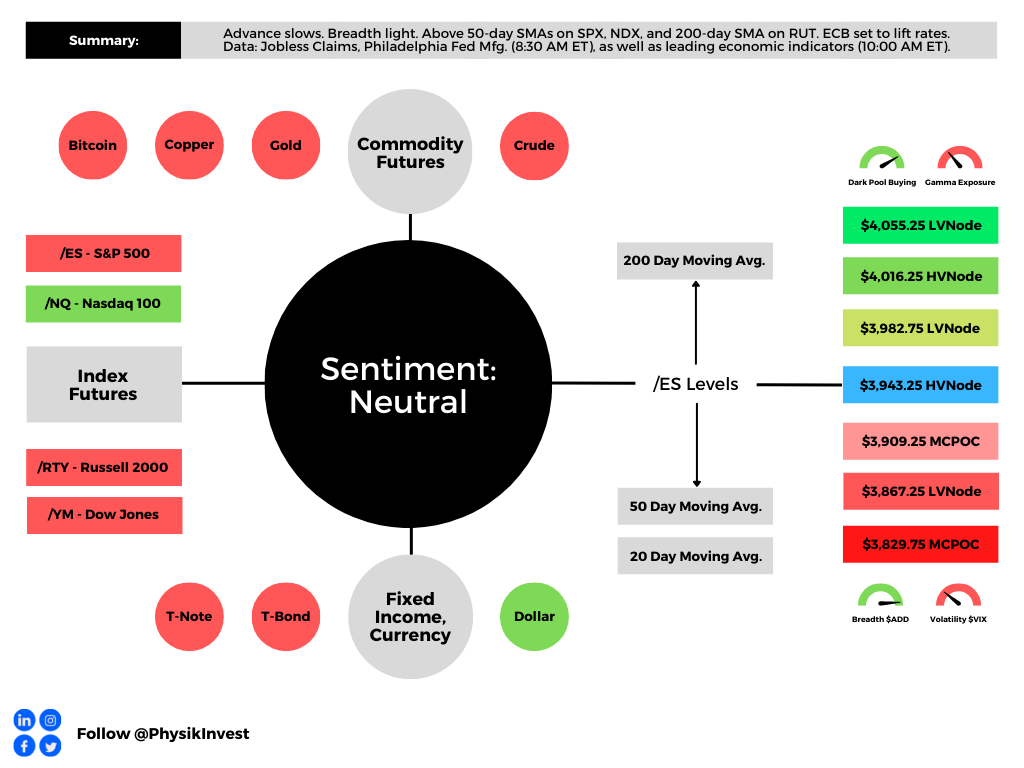

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

The author, Renato Leonard Capelj, works in finance and journalism.

Capelj spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market. Separately, Capelj is an options analyst at SpotGamma and an accredited journalist.

Capelj’s past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, North Dakota Governor Doug Burgum, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Connect

Direct queries to renato@physikinvest.com. Find Physik Invest on Twitter, LinkedIn, Facebook, and Instagram. Find Capelj on Twitter, LinkedIn, and Instagram. Only follow the verified profiles.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.