Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Administrative

Sorry for the delay. Please read through the positioning section. Have a great Monday!

As always, if there are holes or unclear language. We will fix this in the next letters.

Fundamental

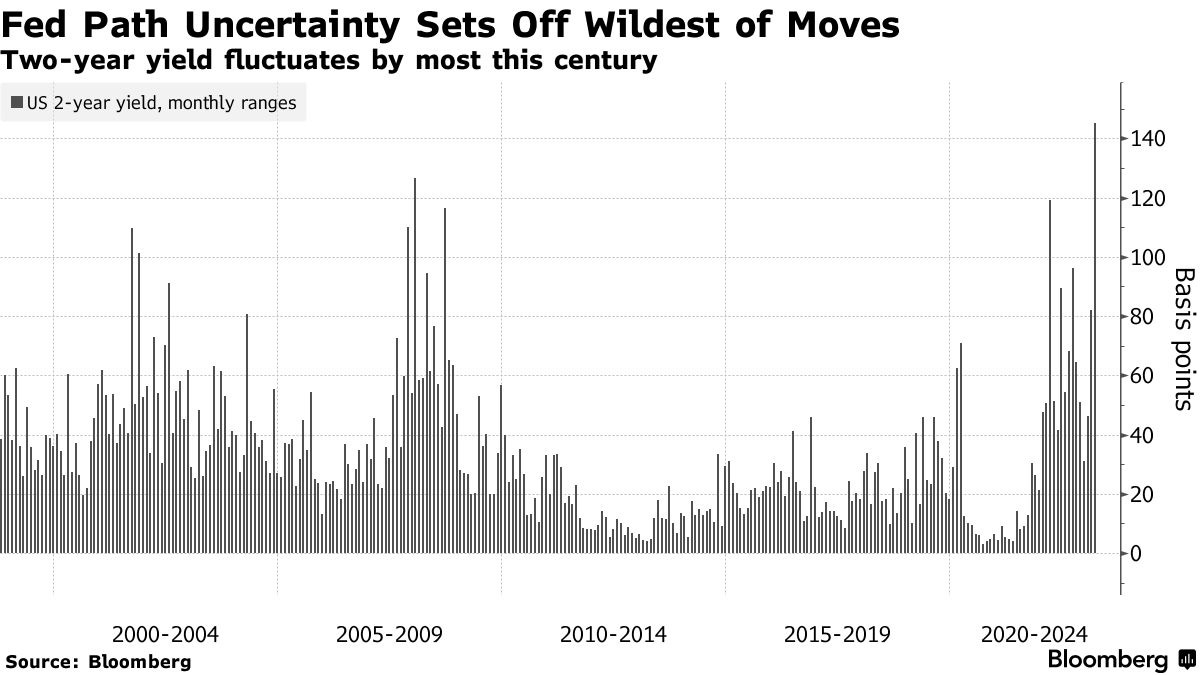

On 3/22, we mentioned news of Russia wanting to adopt the yuan for settlements.

And, with that, publications covering these East alliances use some tough language. One Bloomberg article notes China and Russia “roll[ing] back US power and alliances … [to] create a multipolar world … [and] diminish the reach of democratic values, so autocratic forms of government are secure and even supreme.”

Let’s rewind a bit to understand why all the toughness and fear.

Recall Chinese President Xi Jinping speaking with Saudi and GCC leaders. Here is our 1/4 summary takeaway:

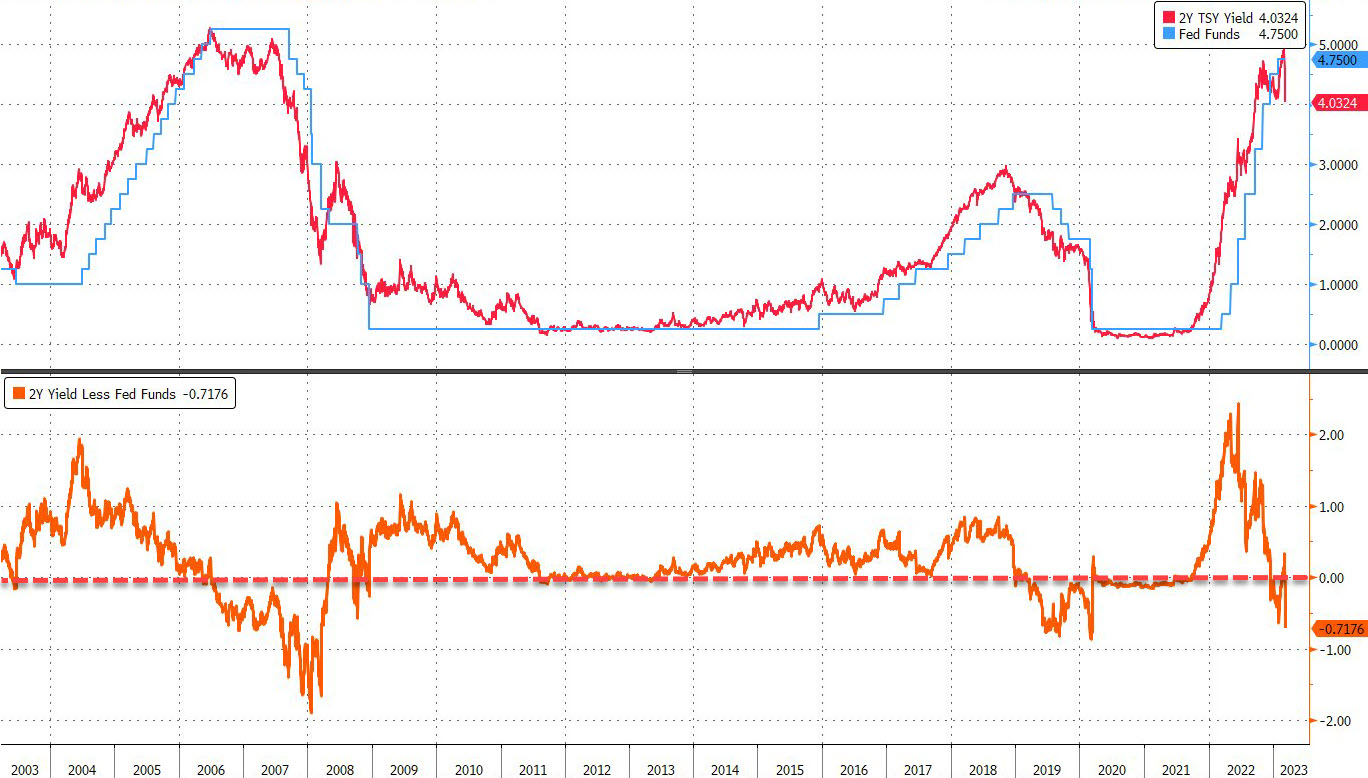

Essentially, those remarks confirm the East is hedging sanctions risk. Reliance on the West is falling, and this inevitably will present “non-linear shocks” (i.e., “inflation mess caused by geopolitics, resource nationalism, and BRICS”) monetary policymakers are not equipped to handle. So, are the markets at risk?

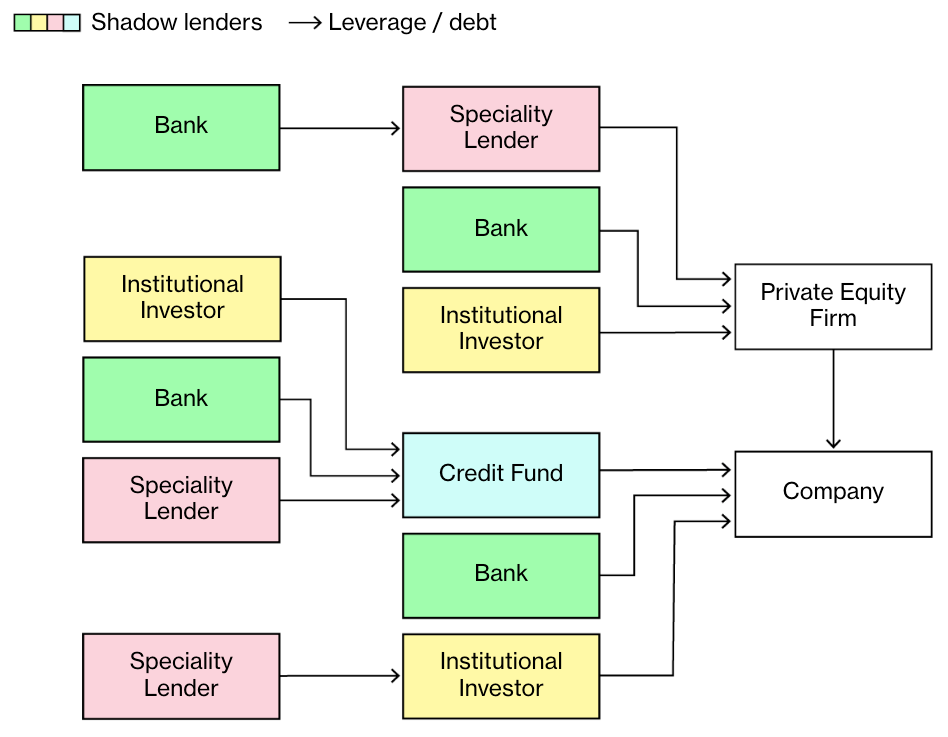

This most recent meeting between China and Russia increases the risks of unwinding the “debt-fueled economy in the US,” FT’s Rana Foroohar confirms, as we wrote in the Daily Brief for 1/4. Further, this is a threat to “hidden leverage and opaqueness.” That means the markets are at risk. Let’s explain more.

With the encumbrance of commodities, among other initiatives, these nations’ weight in currency baskets may rise and keep “inflation from slowing.” If that happens, future rate expectations are off. Additionally, “the US dollar and Treasury securities will likely be dealing with issues they never had to deal with before: less demand, not more; more competition, not less,” we quoted Zoltan Pozsar (ex-Credit Suisse) saying on 1/5.

The markets most responsive to this are public, as we saw with 2022’s de-rate. In 2023 and beyond, added liquidation-type risks lie in the private markets. This will have knock-on effects.

The likes of The Ambrus Group’s Kris Sidial mentioned to your newsletter writer in a Benzinga interview that private market investors’ raising of cash to meet capital calls could prompt sales of their more liquid public market holdings. This is a major risk Sidial noted he was watching, in addition to some risks in the derivatives markets.

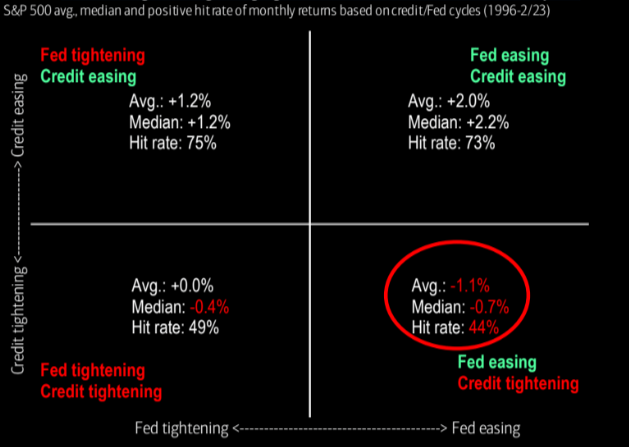

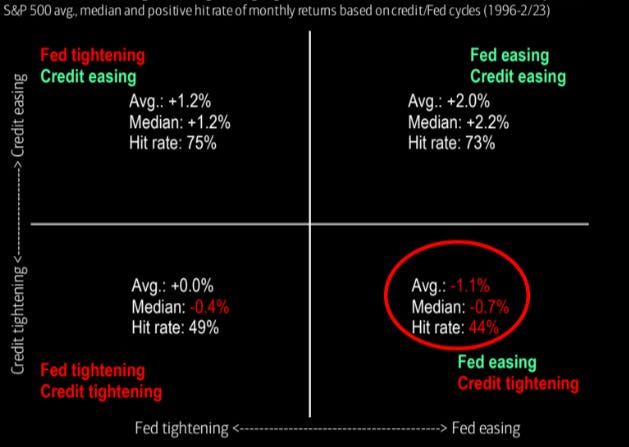

At the same time, Eric Basmajian believes the “banking crisis will cause a tightening of money and credit.” This will further solidify the “broader business cycle and corporate profit recession.”

Positioning

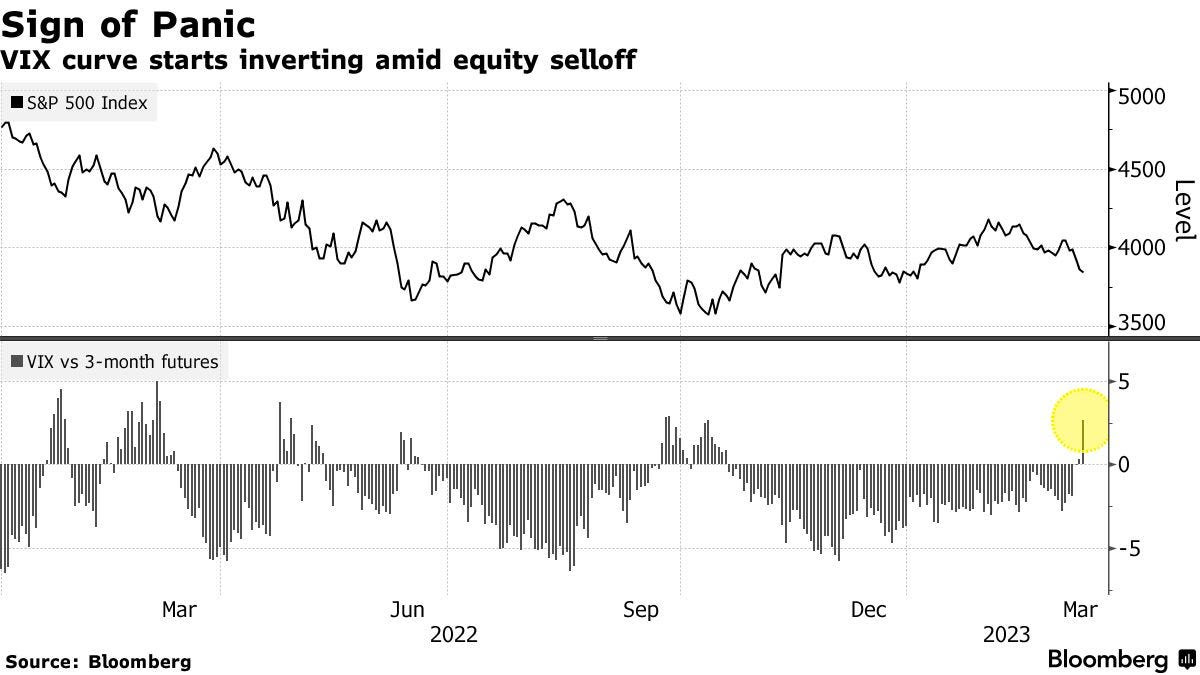

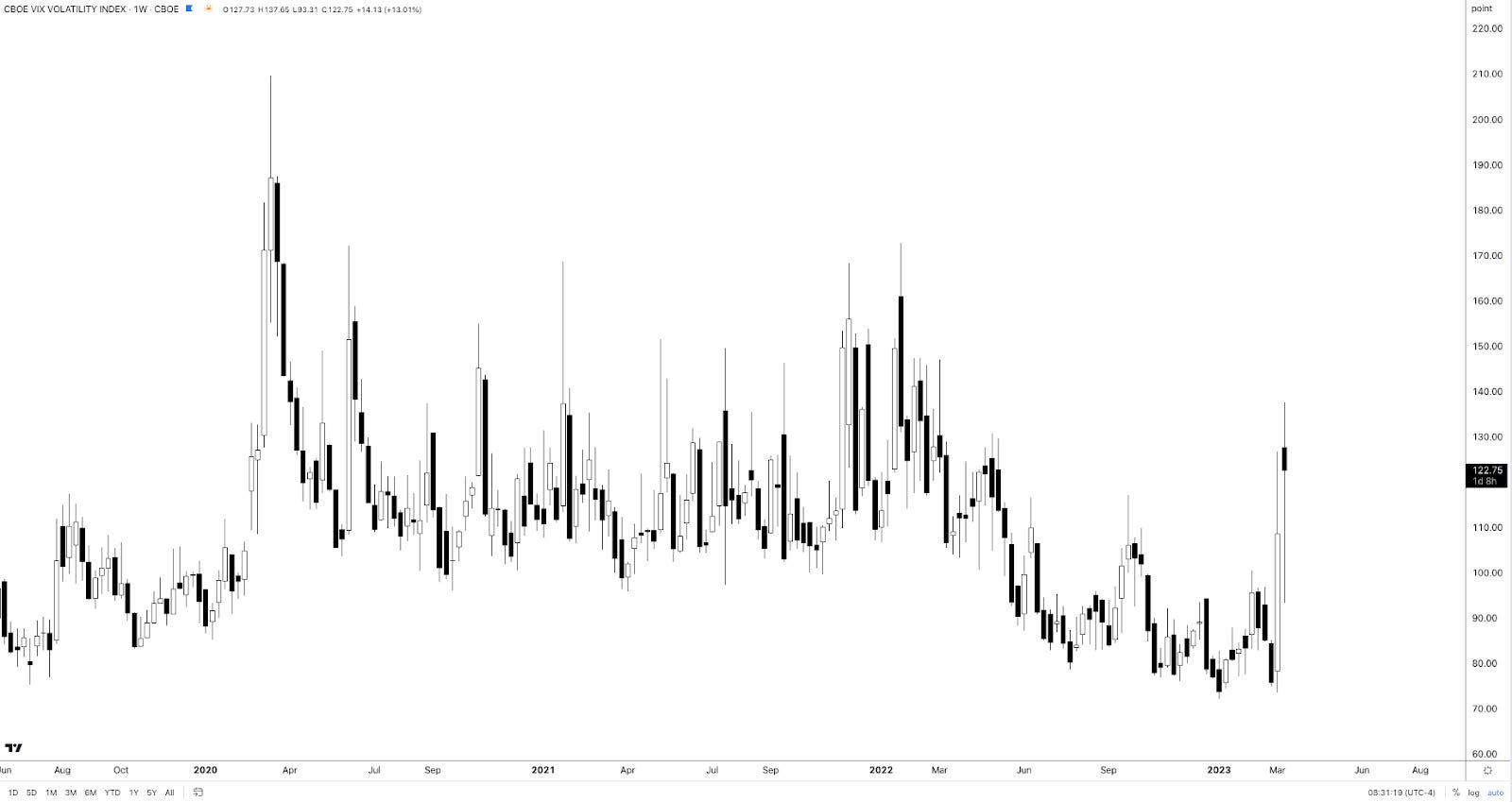

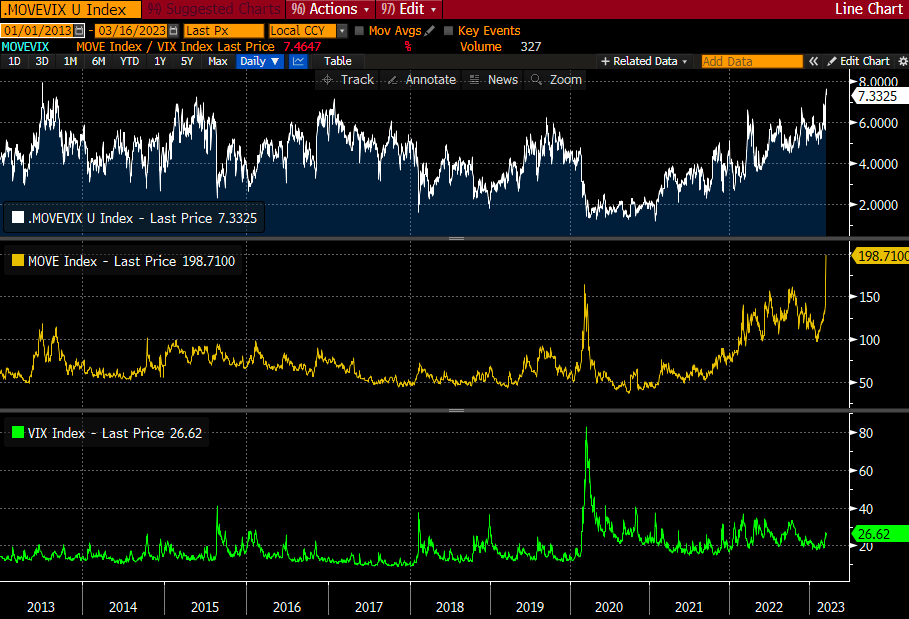

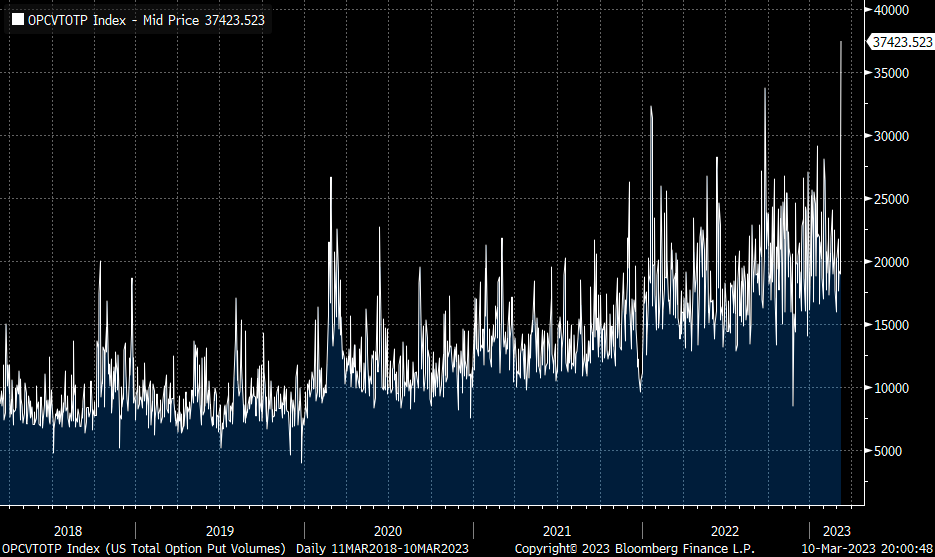

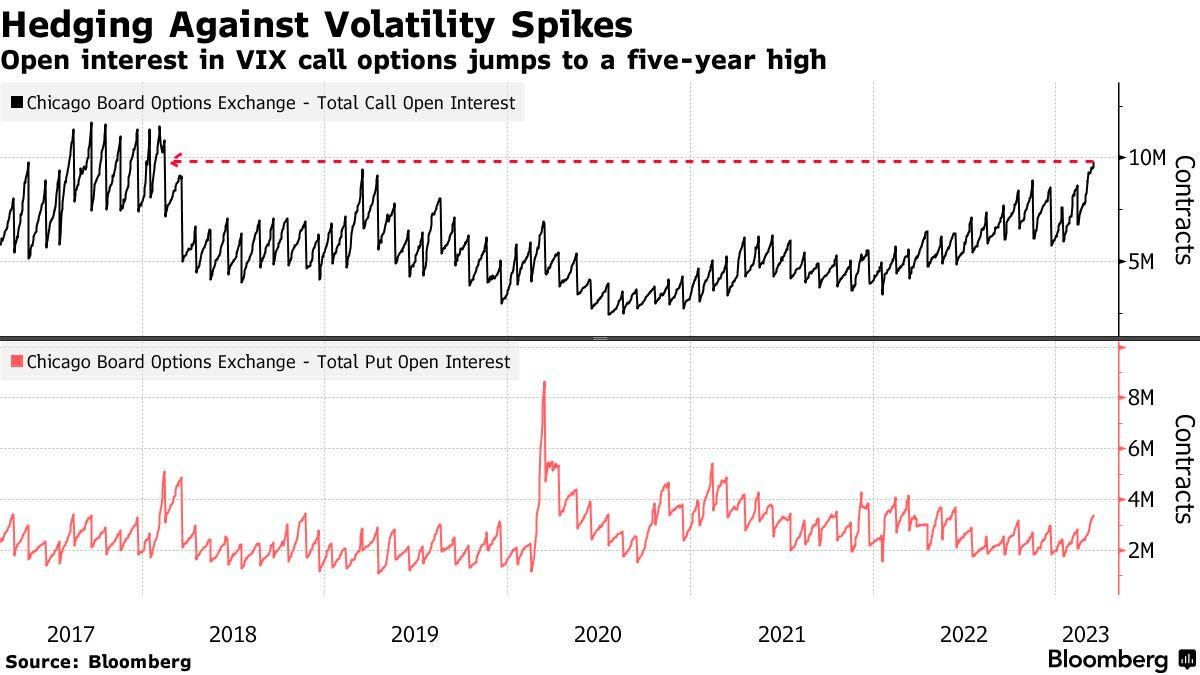

Sidial’s well positioned to take advantage of the realization of these risks. In January, he explained that measures like the Cboe VIX Volatility Index (INDEX: VVIX) were low. This suggested, “we can get cheap exposure to convexity while a lot of people are worried.” In an update to Bloomberg, Sidial said The Ambrus Group’s tail-risk strategy (which Sidial has explained to us before) has performed well as the VIX index has risen, a sign of traders hedging concerns about “some contagion hitting and their portfolios being destroyed on that.”

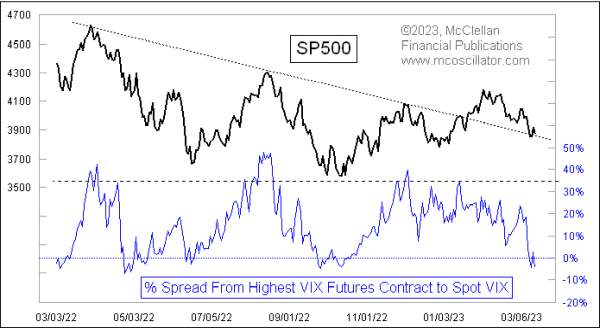

“We have seen an increase in tail hedging,” added Chris Murphy of Susquehanna International Group. “We have continued to see call buying in the VIX since the bank turmoil began.” The caveat, though, is that realized volatility or RVOL, not just implied volatility or IVOL (i.e., that which is implied by traders’ supply and demand of options), must shift and stay higher for those options to maintain their values, which may be difficult according to Kai Volatility’s Cem Karsan.

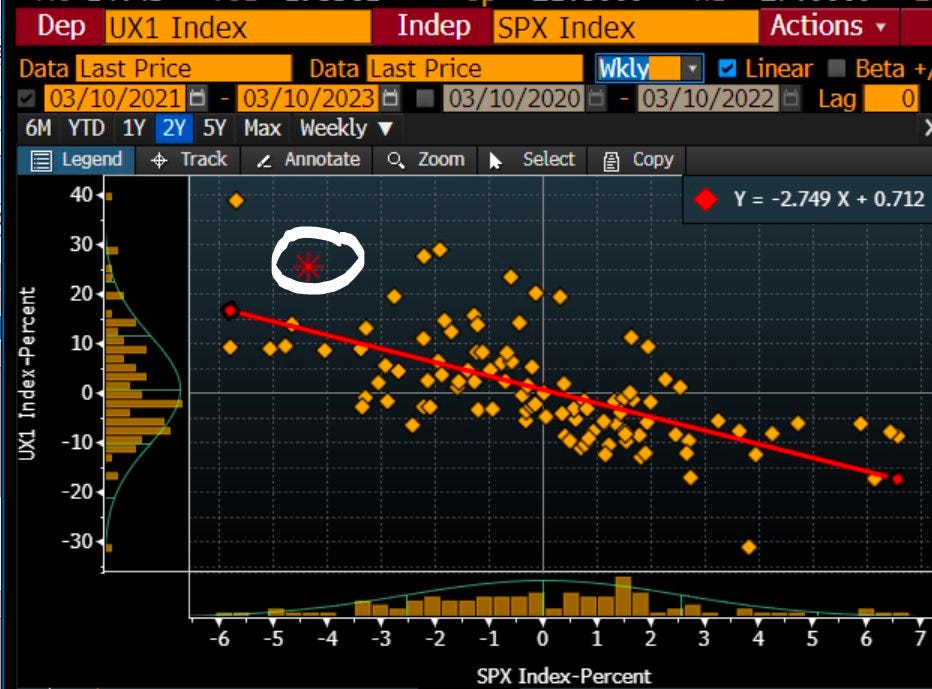

Though Karsan thinks markets will likely see RVOL come back in a big way, he thinks policymakers’ intervention will be stimulative short-term as it reverses a lot of the quantitative tightening or QT (i.e., flow of capital out of capital markets). Stimulation will be compounded by the continued unwinding of hedging strategies in previously depressed products like the Nasdaq 100 (INDEX: NDX). What do we mean by this?

Recall that traders’ closure and/or monetization of put protection results in options counterparties buying back their short stock and/or futures hedges. Therefore, before any downside is realized, the market may trade into a far “more combustible” position.

Consequently, look for low- and zero-cost call structures (e.g., ratio spreads) to play the upside while opportunistically using higher prices and elevated volatility skew to put on bear put spreads (i.e., buy put and sell another put at a lower strike price) for cheaper prices.

Consider following and supporting us on social media:

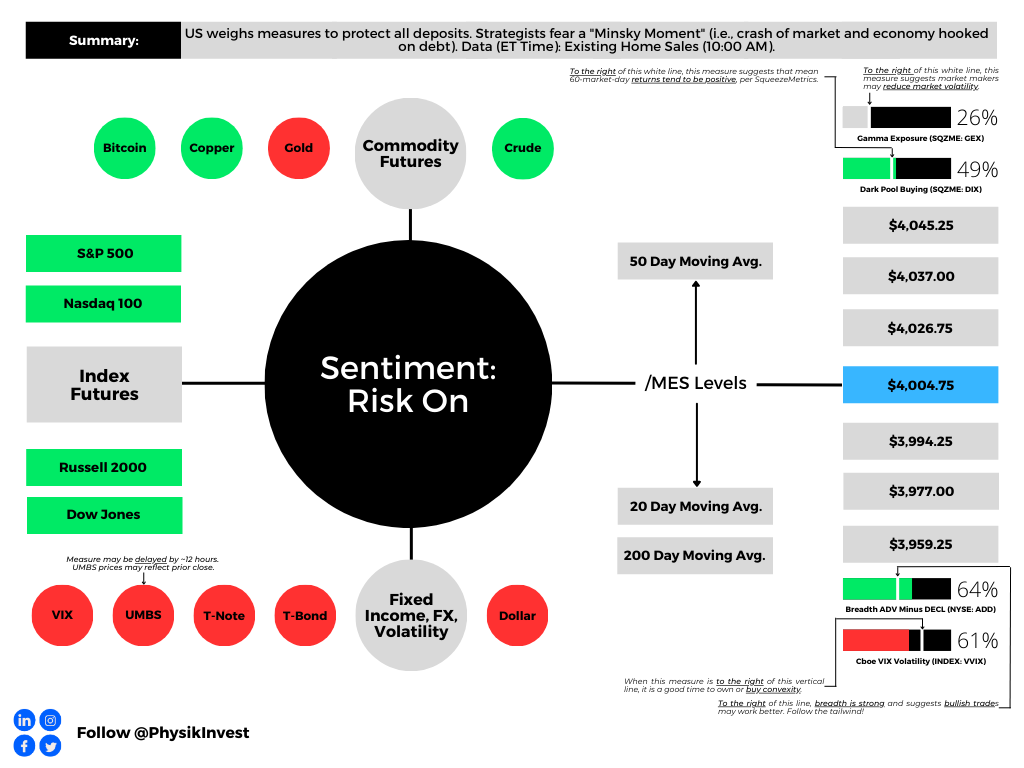

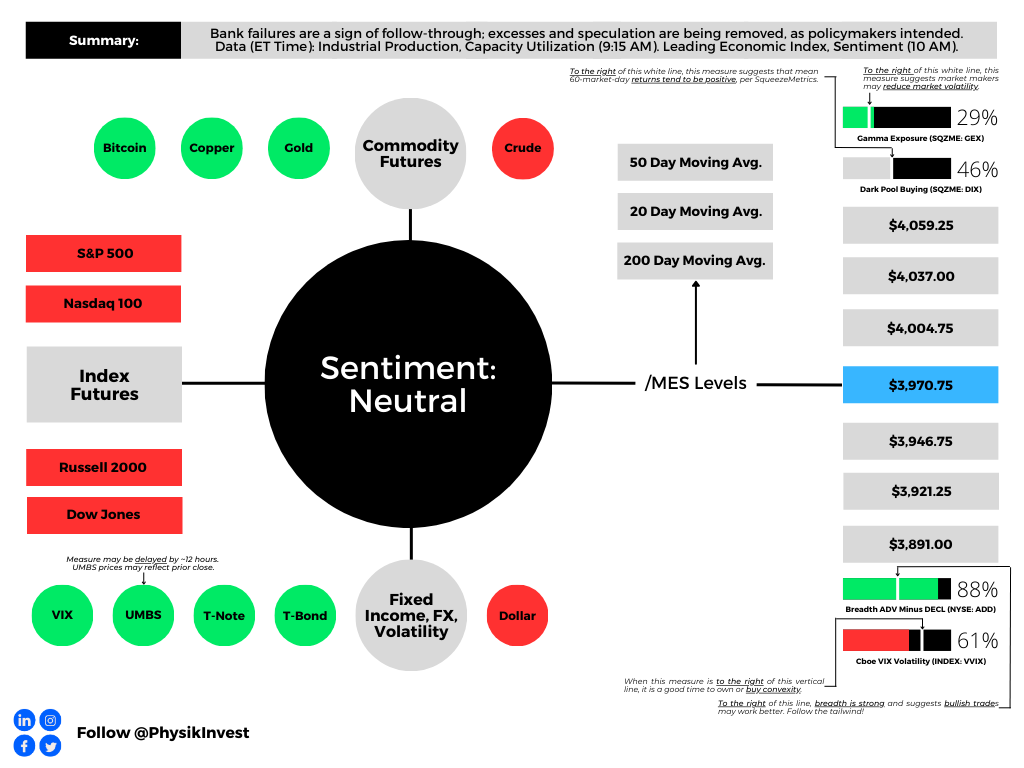

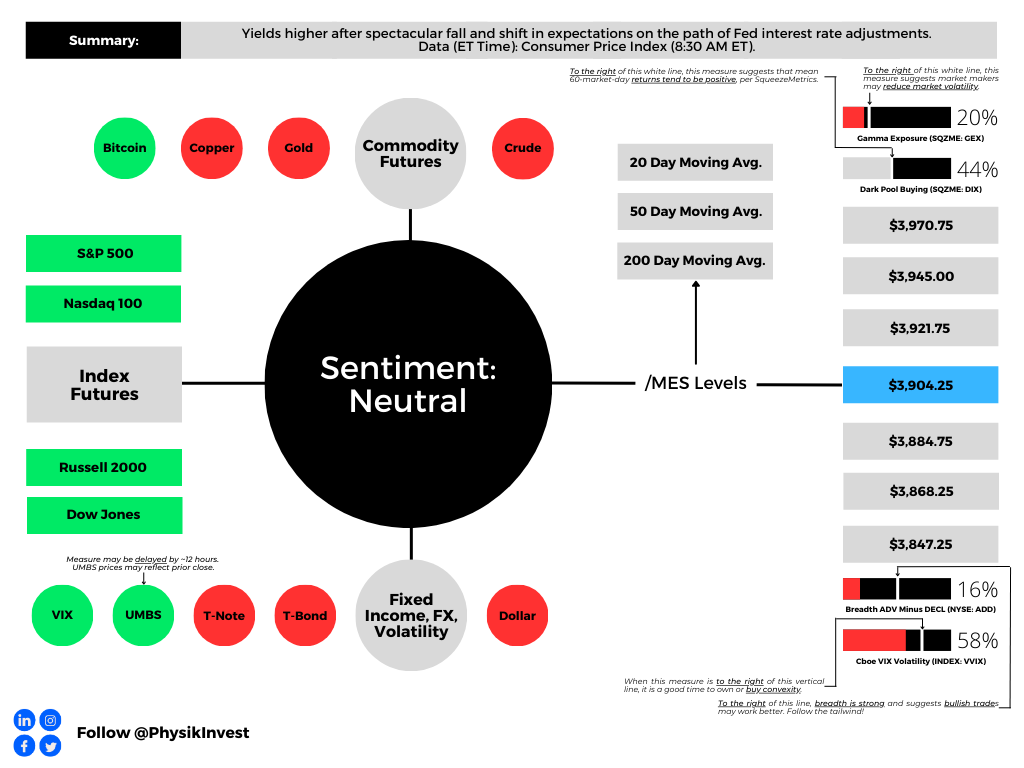

Technical

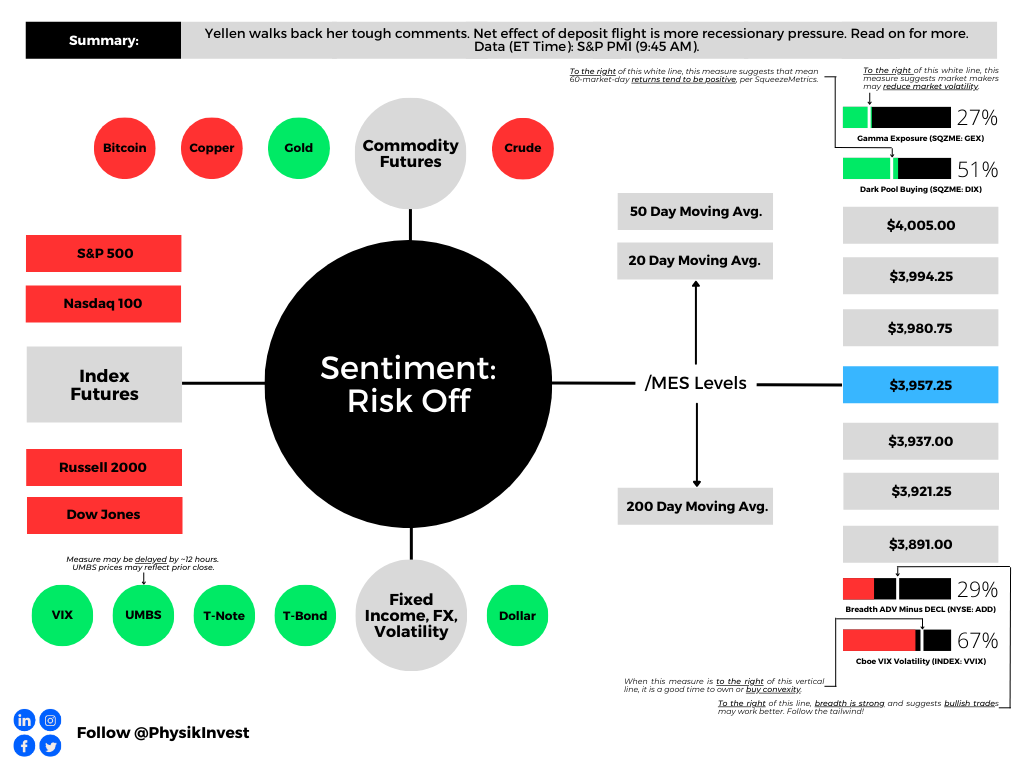

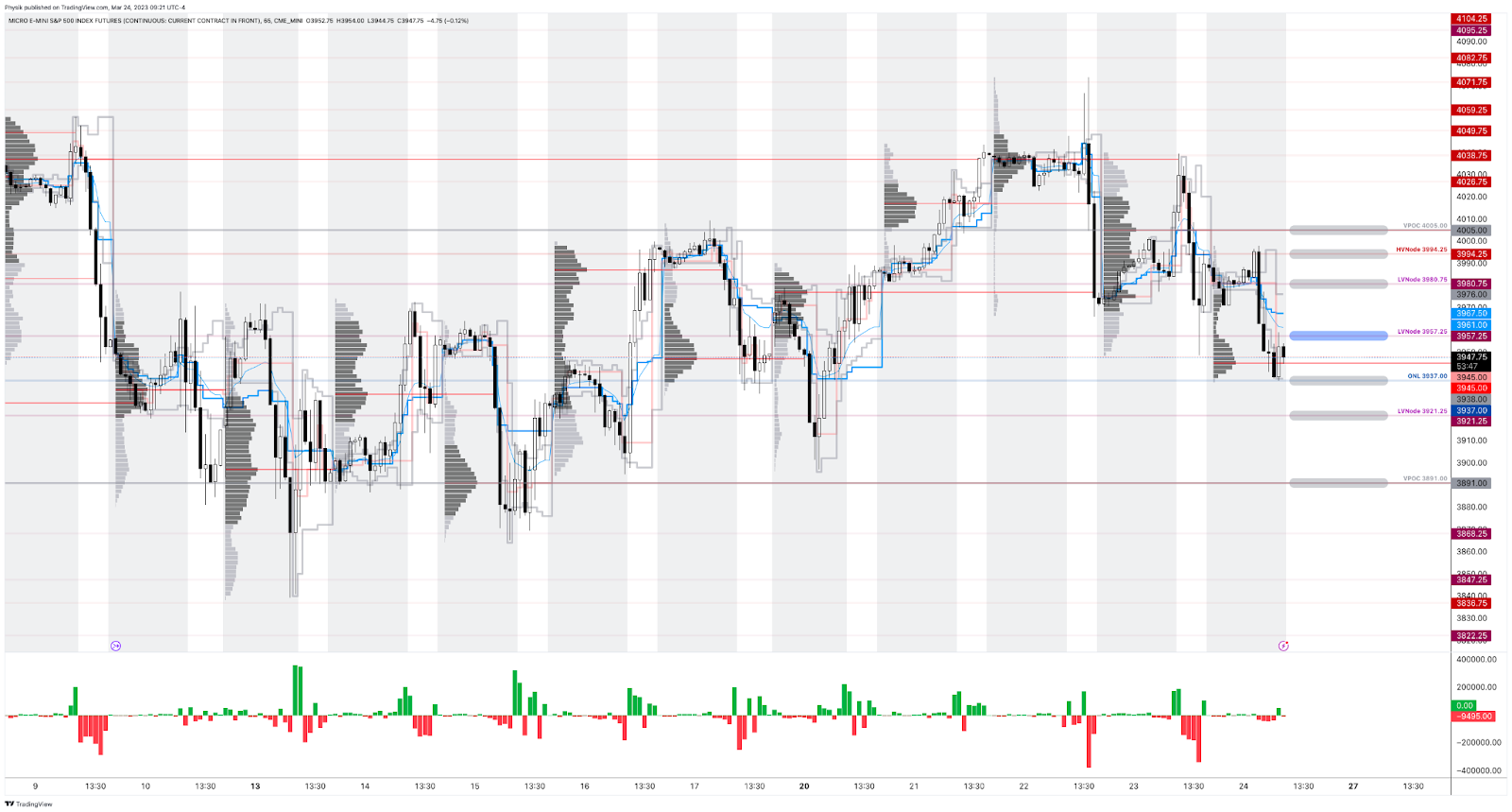

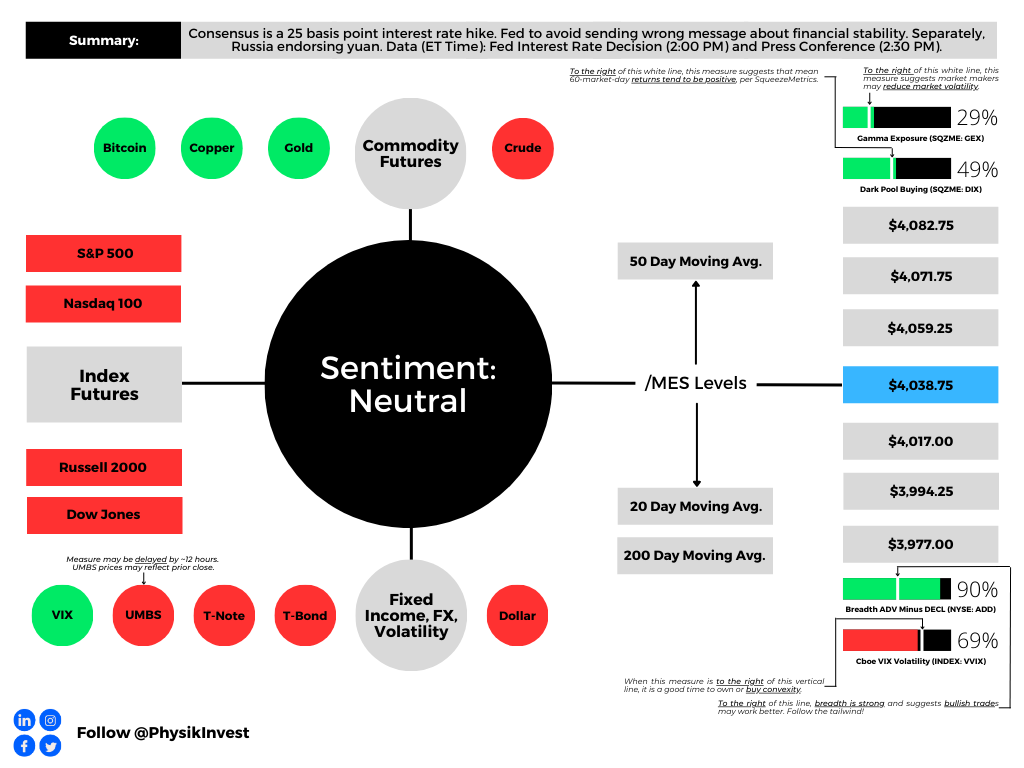

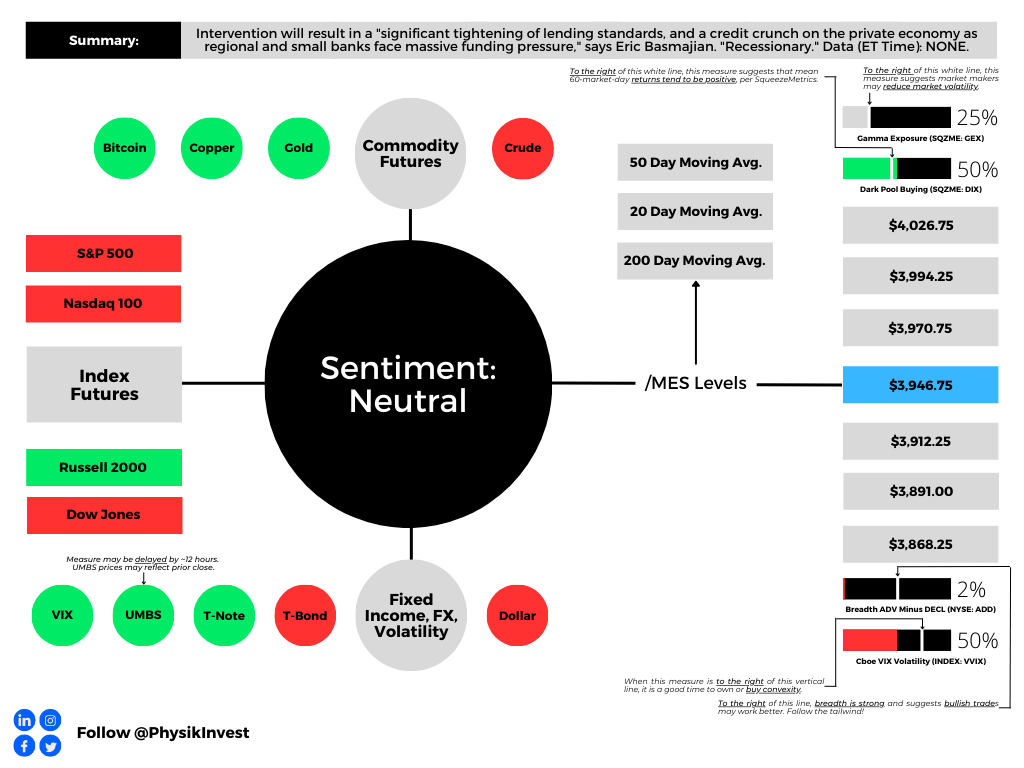

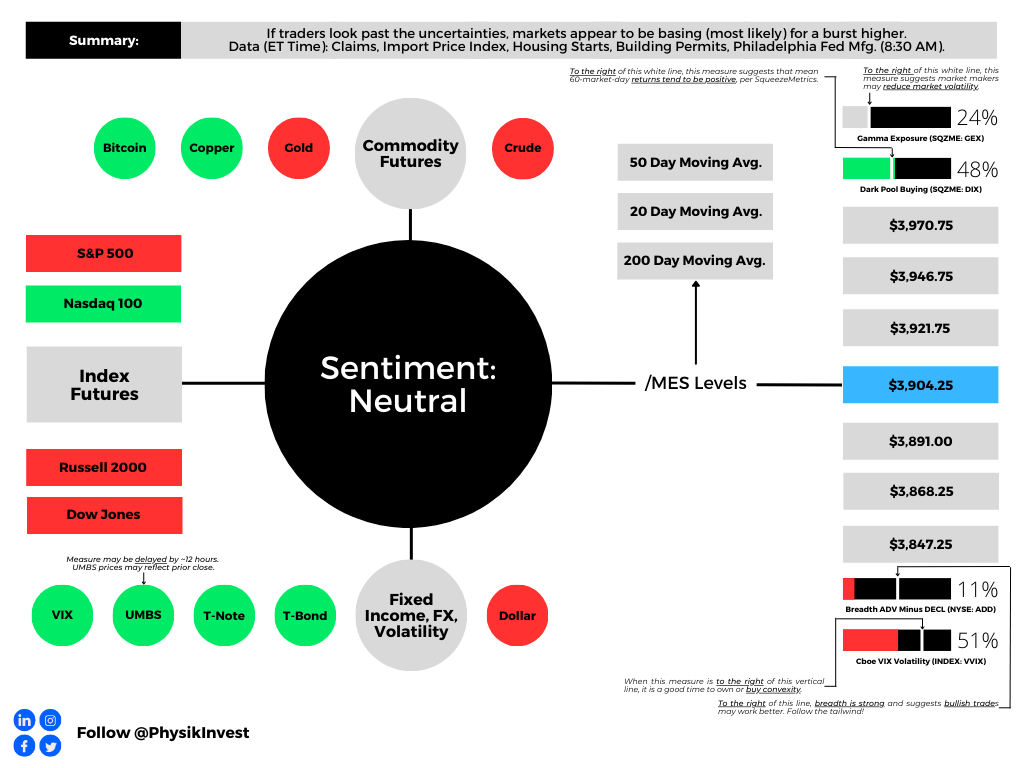

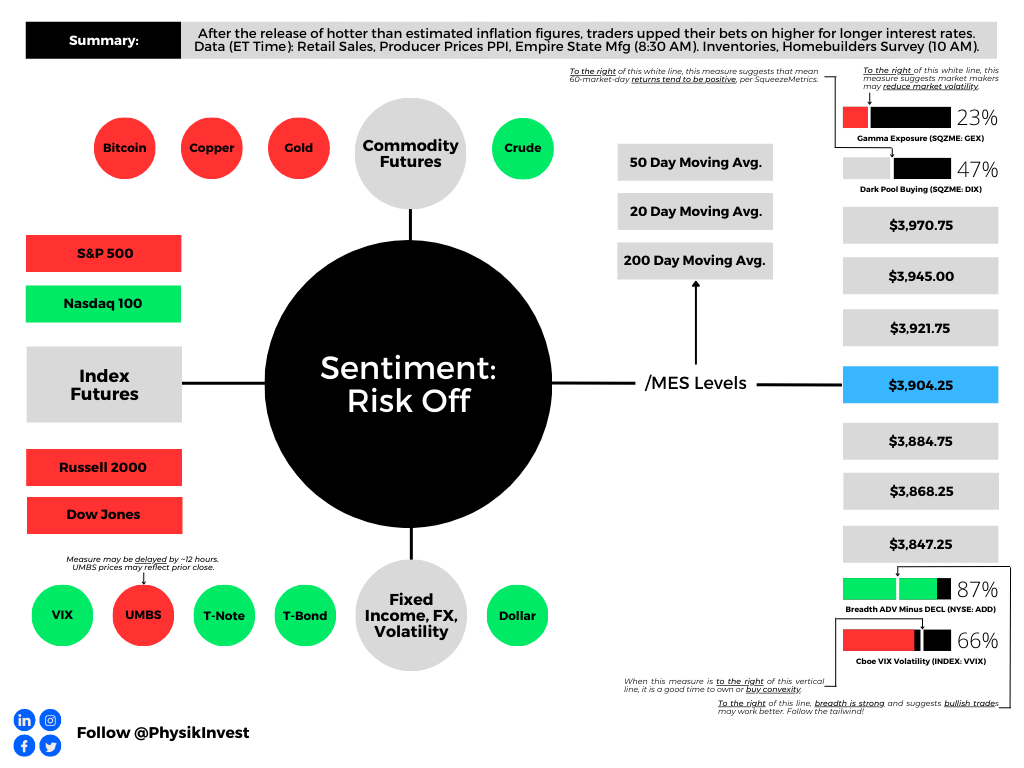

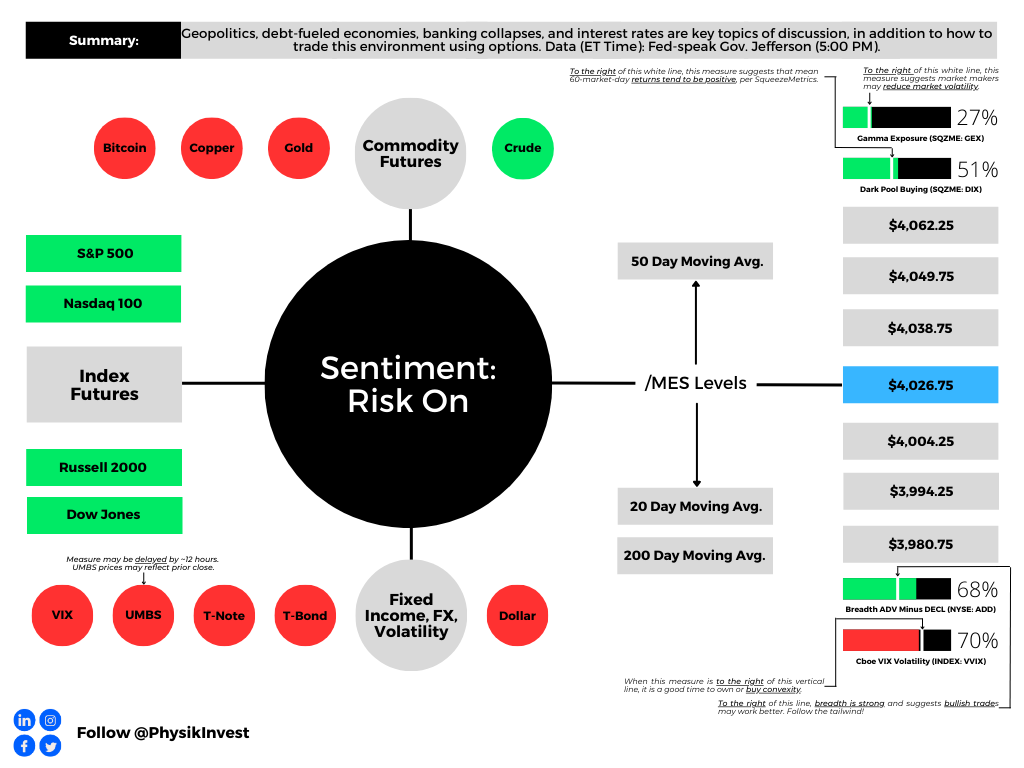

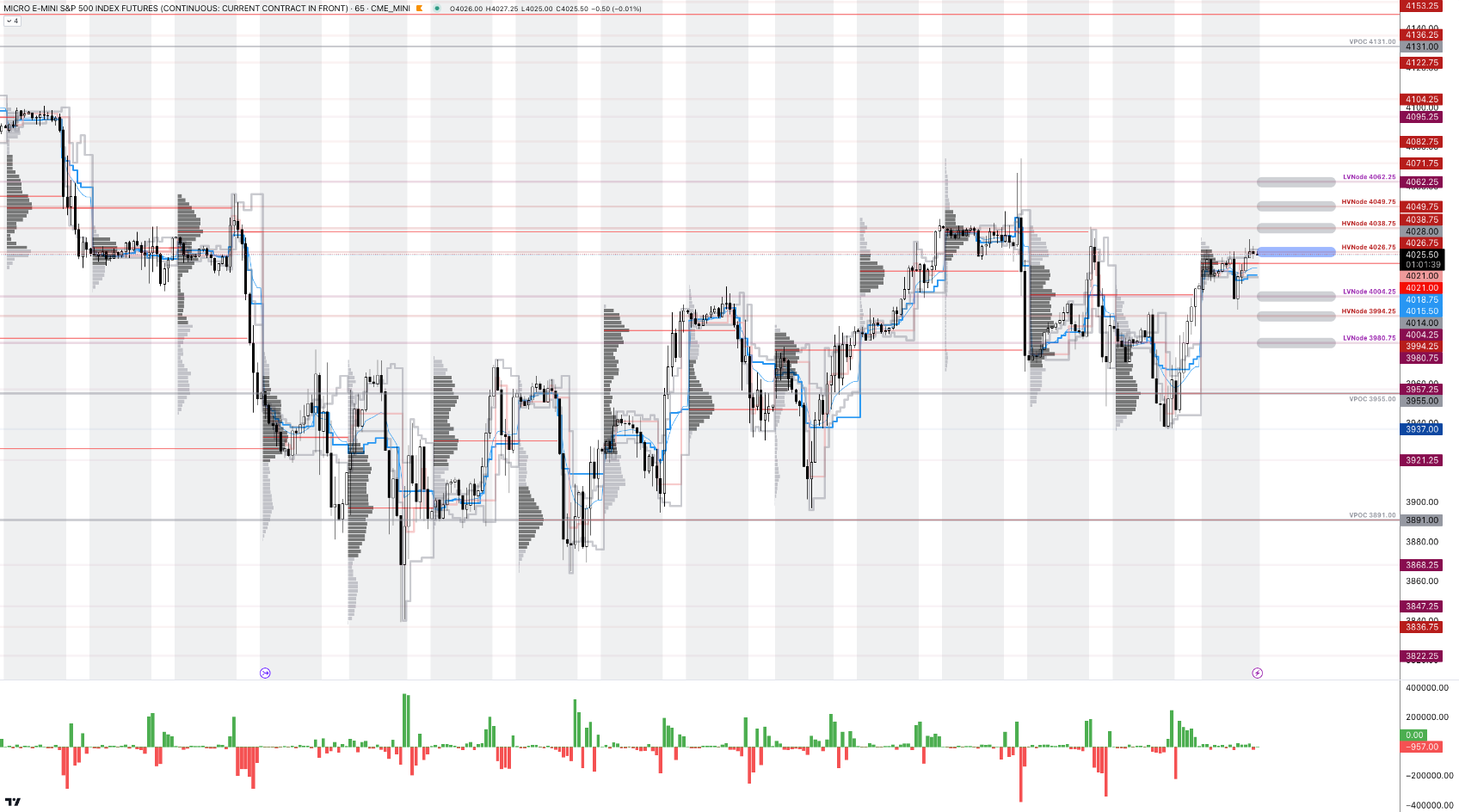

As of 9:10 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, outside of the prior day’s range, suggesting a potential for immediate directional opportunity.

The S&P 500 pivot for today is $4,026.75.

Key levels to the upside include $4,038.75, $4,049.75, and $4,062.25.

Key levels to the downside include $4,004.25, $3,994.25, and $3,980.75.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for some time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

Separately, Capelj is an accredited journalist with past works including interviews with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, North Dakota Governor Doug Burgum, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Connect

Direct queries to renato@physikinvest.com. Find Physik Invest on Twitter, LinkedIn, Facebook, and Instagram. Find Capelj on Twitter, LinkedIn, and Instagram. Only follow the verified profiles.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.