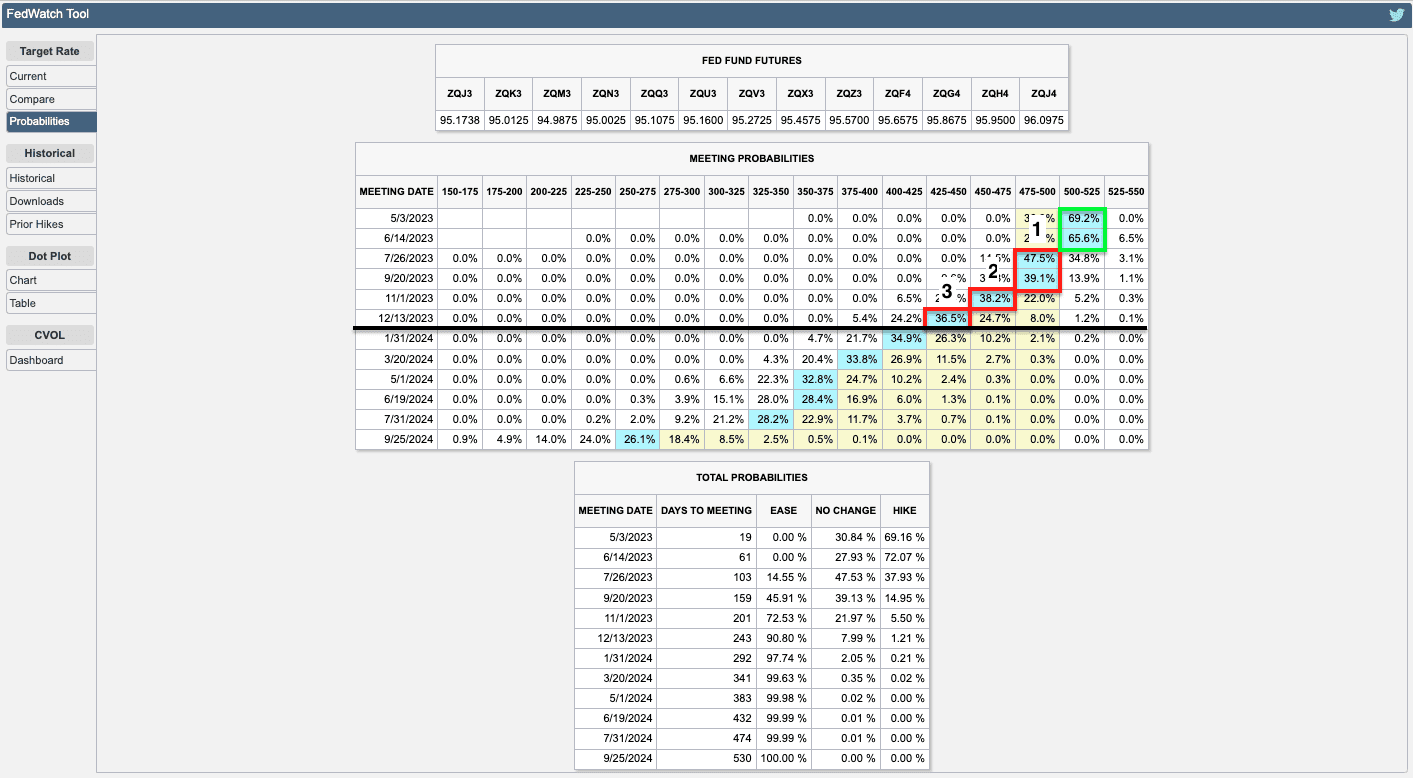

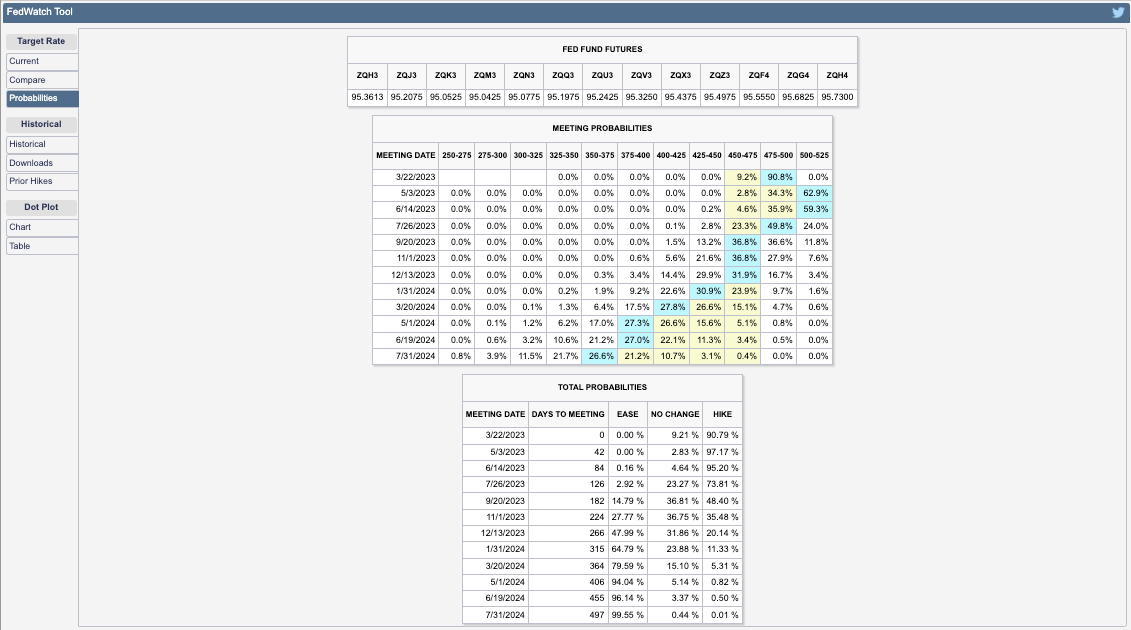

US consumer prices rose by 4.9% in the 12 months to April, down from the previous month’s 5%. Wednesday’s figures suggest inflation is moderating and emboldens the case for a pause to interest rate increases.

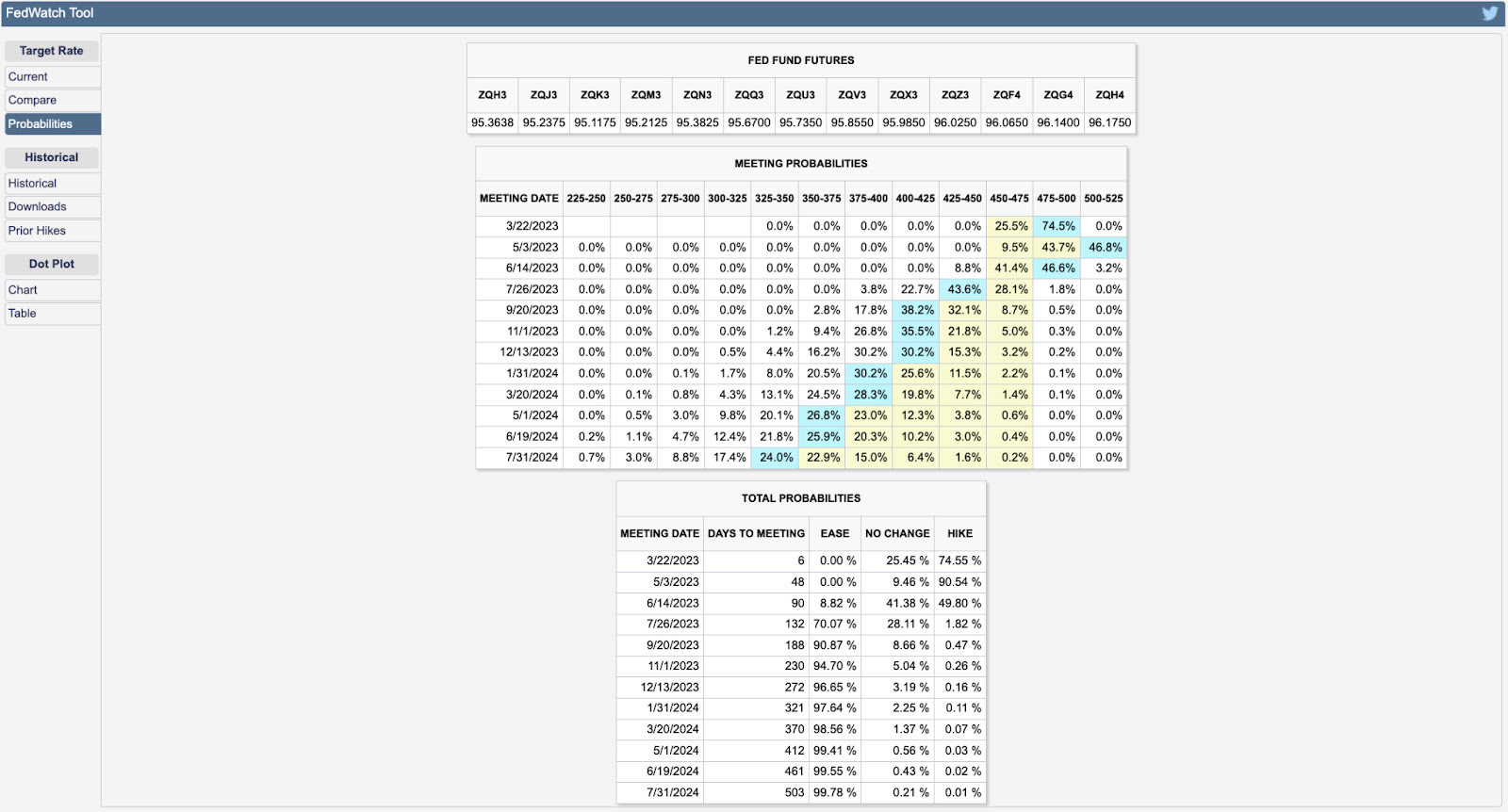

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

“The Fed will want to see declines in these statistical measures for a few more months before it could feel comfortable about cutting rates,” John Authers writes.

Notwithstanding “sticky price inflation” falling (only “if shelter prices are excluded,” the most challenging “front in the battle on inflation”), applications to purchase and refinance homes rose with yields falling, and that’s exactly what the Fed doesn’t want.

Many maintain the Fed is looking to walk-up long-end yields, and that’s problematic for assets; higher interest rates portend lesser allocations toward risky assets.

Pimco’s Erin Browne and Emmanuel Sharef add that “12-month returns following the final rate hike could be flat for 10-year U.S. Treasuries, while the S&P 500 could sell off sharply.”

Accordingly, bonds look attractive “for their diversification, capital preservation, and upside opportunities,” while “earnings expectations appear too high, and valuations too rich,” warranting “underweight” equities positioning.

Compounding the risks are flows “that eventually will constrain lending and nominal growth on a 6- to 12-month horizon,” writes Goldman Sachs Group Inc (NYSE: GS).

Graphic: Retrieved from Bloomberg via The Market Ear. “The bull in money market funds refuses to cool down.”

In other news was worry over a US debt default.

The US government has been using accounting measures to provide cash after reaching a borrowing limit. Treasury Secretary Janet Yellen informed Congress that these measures might be exhausted by June, resulting in payment disruptions; a default would cause an economic disaster and “global downturn,” threatening “US global economic leadership” and “national security,” Yellen says. A solution (e.g., to raise the debt ceiling) could manifest issuance of “a substantial amount of bills in 2H23 … that would drain liquidity,” Morgan Stanley (NYSE: MS) writes.

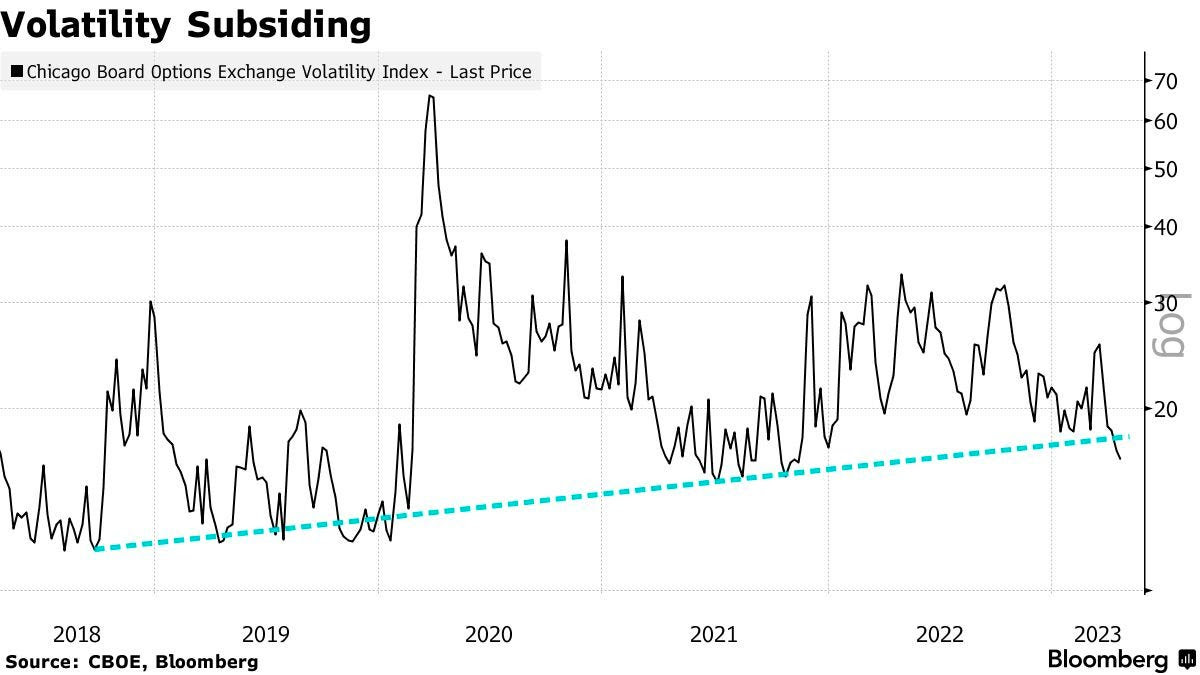

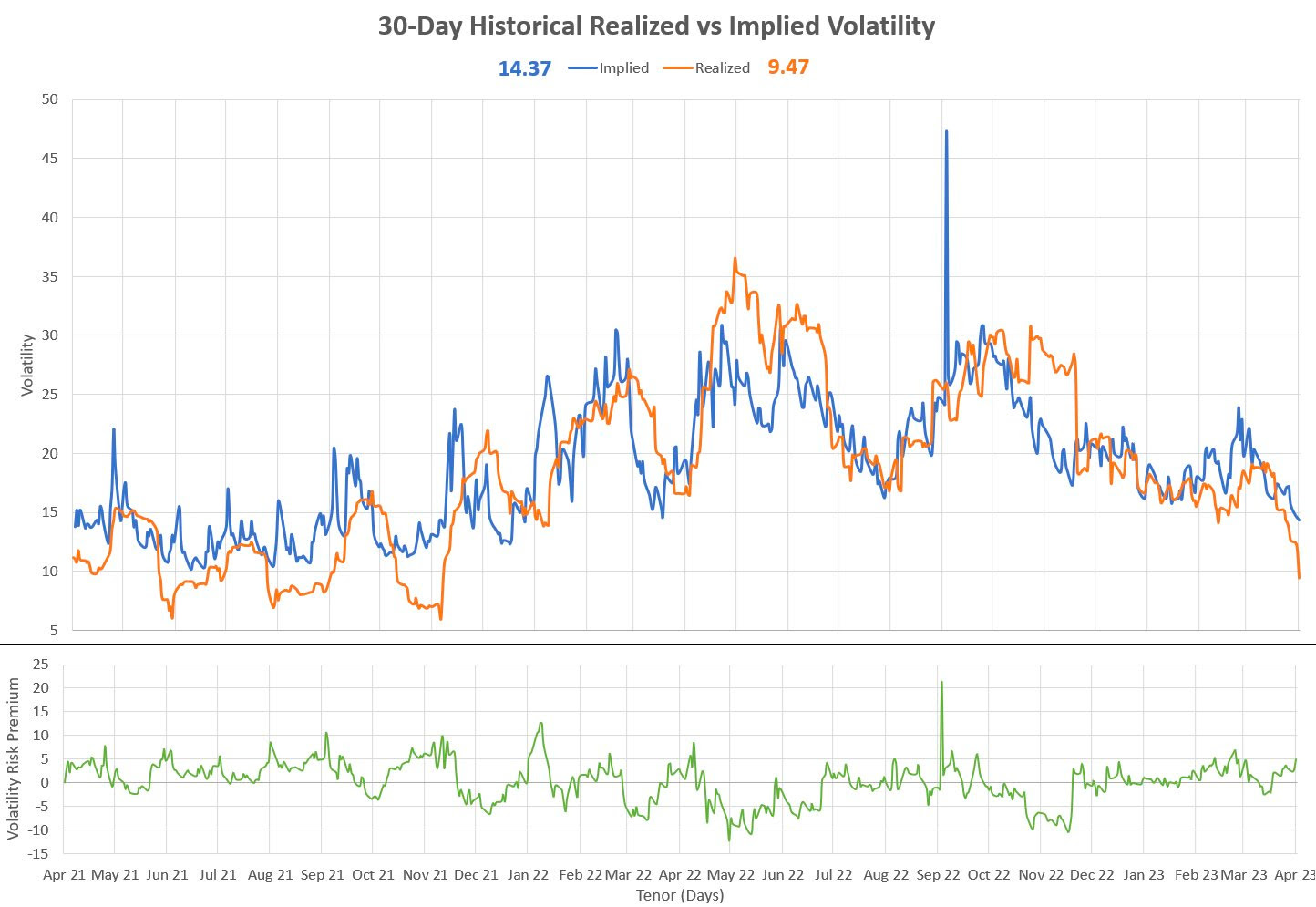

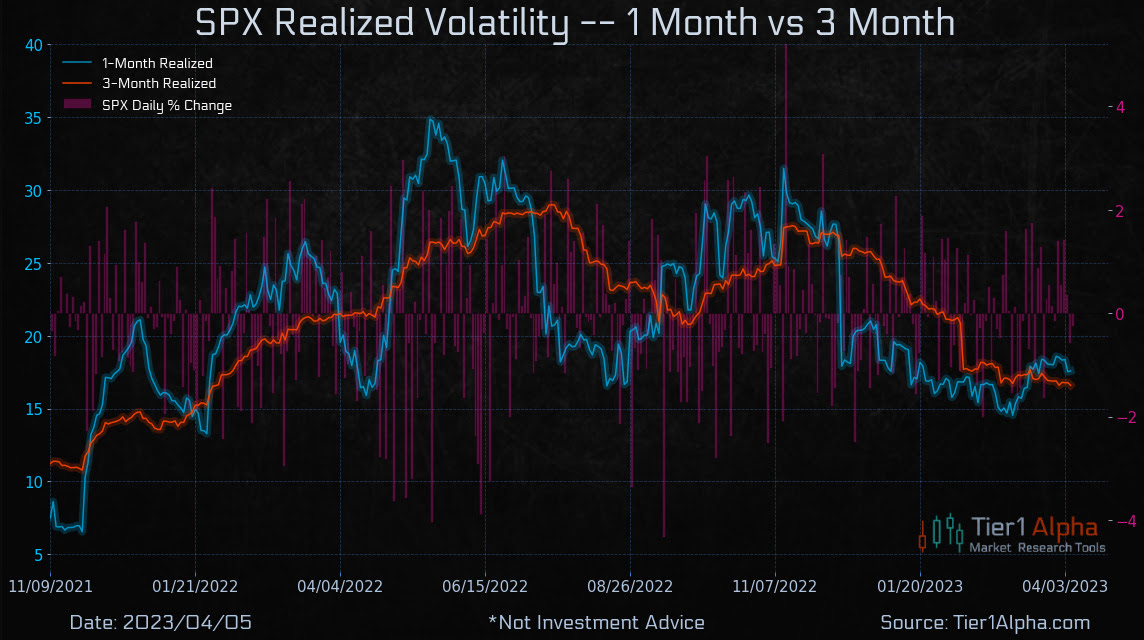

Despite the worry, markets are contained in part due to positioning contexts. Decline in realized volatility (RVOL), coupled with implied volatility (IVOL) premium, makes it difficult for the market to resolve directionally.

In fact, Nomura Holdings Inc (NYSE: NMR) said it sees “significant further potential for additional equities re-allocation buying from the vol control space over the next month if this ongoing rVol smash / tight daily ranges phenomenon holds—i.e., +$37.8B of US Equities to buy on theoretical 50bps daily SPX change).”

Options are sold systematically as traders aim to extract the premium; the Ambrus Group’s Kris Sidial says there is a puking off options exposures and short-bias activity (i.e., selling options) used as yield enhancement as traders call bluff on authorities not being there to prevent crises.

Graphic: Retrieved from Sergei Perfiliev. “This is a 1-month vol – it’s 30 calendar days for implied and I’m using 20 trading days for realized – both of which represent a month.” Note that “juicy VRP = big difference between options’ implied vol (what you pay) and realized vol (what you got). Options are cheap historically, but expensive relative to realized vol.”

Should readers wish to hedge the debt ceiling debacle, June call options on the Cboe Volatility Index appear attractive, some suggest. But, with RVOL as low as it is, owning optionality is not generally warranted. The risk is lower volatility, not higher.

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.

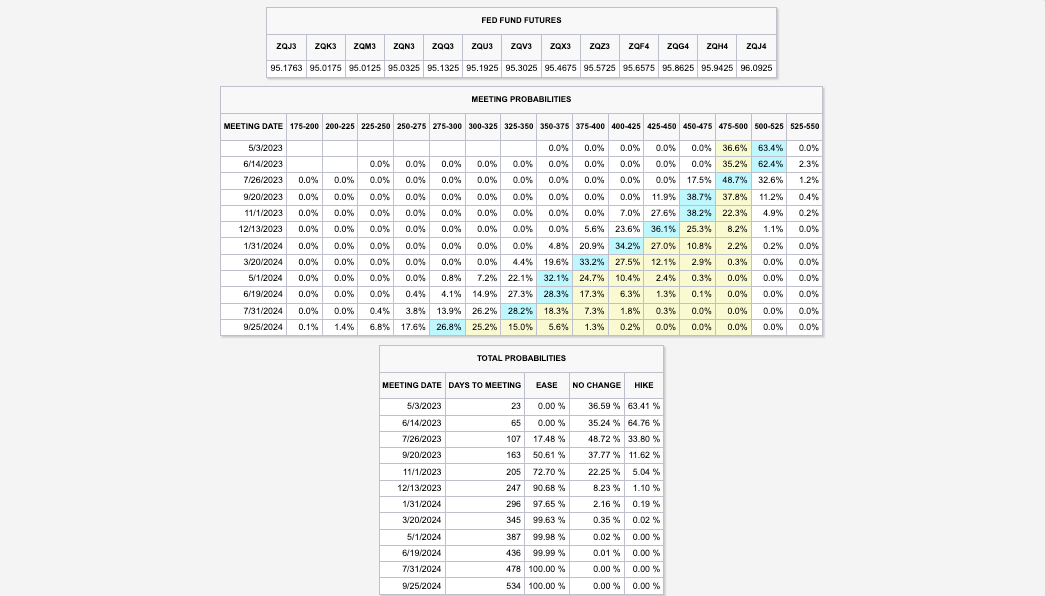

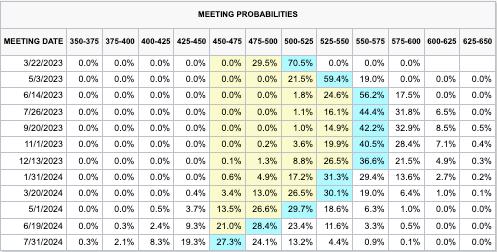

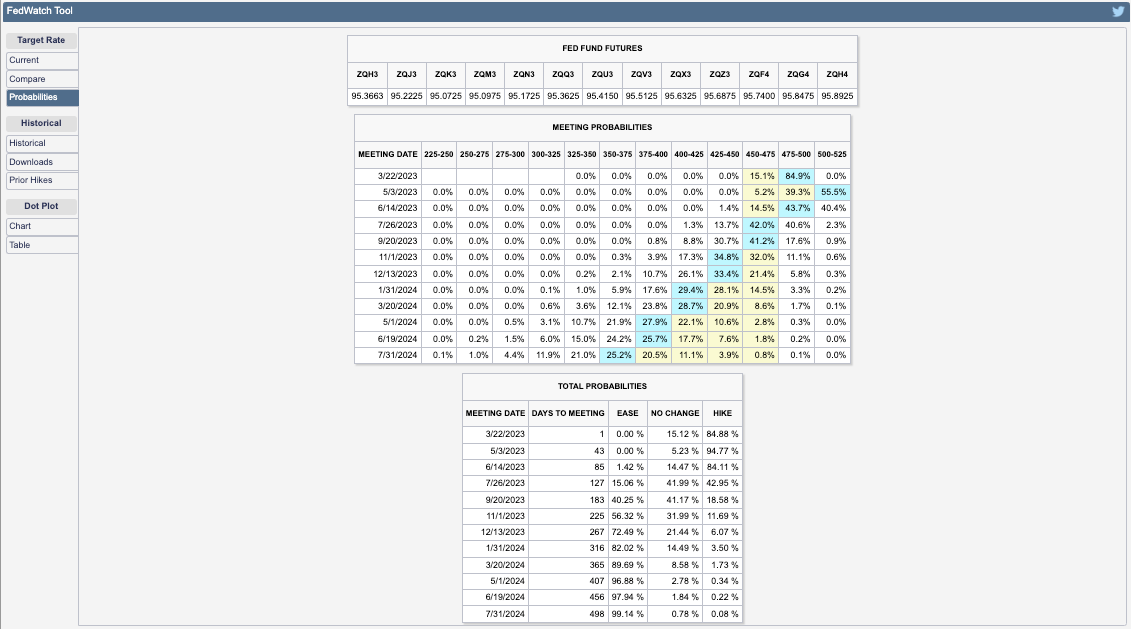

Consensus is a tightening cycle that climaxes on May3 with one final 25 basis point hike. Most traders price three cuts after—one in July, November, and December.

Note: After the release of strong bank earnings today, this analysis remains intact.

Graphic: Retrieved from CME Group Inc (NASDAQ: CME).

Though policymakers are successful in walking up traders’ interest rate expectations, the long end of the yield curve hasn’t budged much; despite the response to banking turmoil helping “calm conditions, … and lessen the near-term risks,” many believe the Fed will have to pivot, soon.

The Federal Reserve’s ranks expect a “mild recession,” too, validating people such as Bank of America Corporation’s (NYSE: BAC) Michael Hartnett, who said investors should steer clear of stocks. Hartnett added the expectations of a recession would solidify following the upcoming earnings season, a test of how companies have managed headwinds like the bank crisis and slowing demand.

Graphic: Retrieved from Bank of America Corporation (NYSE: BAC).

Despite billions in redemptions over the past week or so, the market’sstrengthcan continue for longer, though. Here’s why.

Graphic: Retrieved from Goldman Sachs Group Inc (NYSE: GS) via The Market Ear.

Contextually, positioning overwhelmingly supports the market at this juncture. That’s per the likes of Cem Karsan of Kai Volatility have explained.

Falling volatility has led to billions more in buying flows from volatility-controlled funds rebalancing their risk exposures, Tier1Alpha adds, noting “there is a chance realized volatility [or RVOL] will continue to decrease until the end of next week as long as the SPX returns stay muted. If volatility rises beyond the +/- 2% threshold, net equity sales could exceed $5 billion.”

“This is not expected due to favorable CPI data and dealer positioning,” however.

With markets likely to be contained in the short to medium term, and fundamental weaknesses, such as the Fed hiking long-end yields, likely to cause them to fail in the long run—play near- or medium-term strength via call spread structures, and use the profits to lower the cost of longer-dated bets on markets or rates falling.

In support of this view, per The Market Ear’s summary of some Goldman Sachs Group Inc (NYSE: GS) analyses, “the disconnect between Nasdaq 100 (INDEX: NDX) and bond yields has grown to statistically significant levels.” Thus, “owning downside asymmetry” is starting to look “more attractive.”

Graphic: Retrieved from VIX Central. The compression of implied volatility, or IVOL, is a booster for equities. Investors are mostly bullish with a +1 Put, +100 Stock, -1 Call position, while dealers hold the opposite with a -1 Put, -100 Stock, +1 Call position. As the volatility trends lower (e.g., S&P 500 realized volatility or RVOL is ~10), options lose value, and dealers must buy back their short stock to re-hedge. This supports the market.

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.

US payroll data has increased the possibility of a rate hike by the Federal Reserve or Fed in early May, leading to higher rates and affecting those who expected a pause or pivot through poorly performing yield curve steepener trades. The market expects the Fed to raise its target rate to 5.00-5.25% and keep it there through mid-year.

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

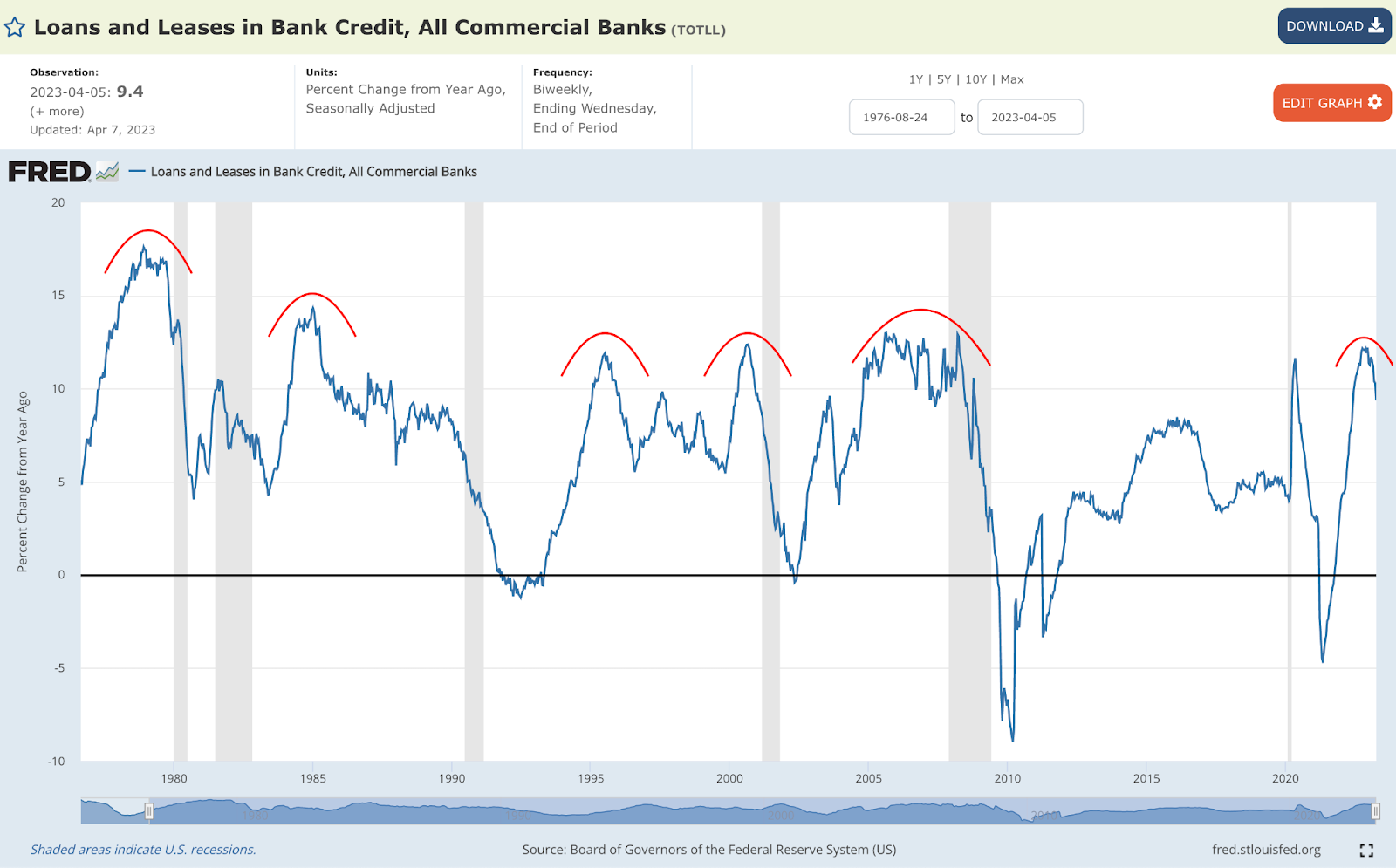

There is more to the pressure than just yields. Surveys indicate a drop in profits for sensitive areas of the equity market, such as technology and banks; as soon as the labor market starts softening, a credit crunch is expected to accelerate by some.

Graphic: Retrieved from the St. Louis Fed via Cubic Analytics.

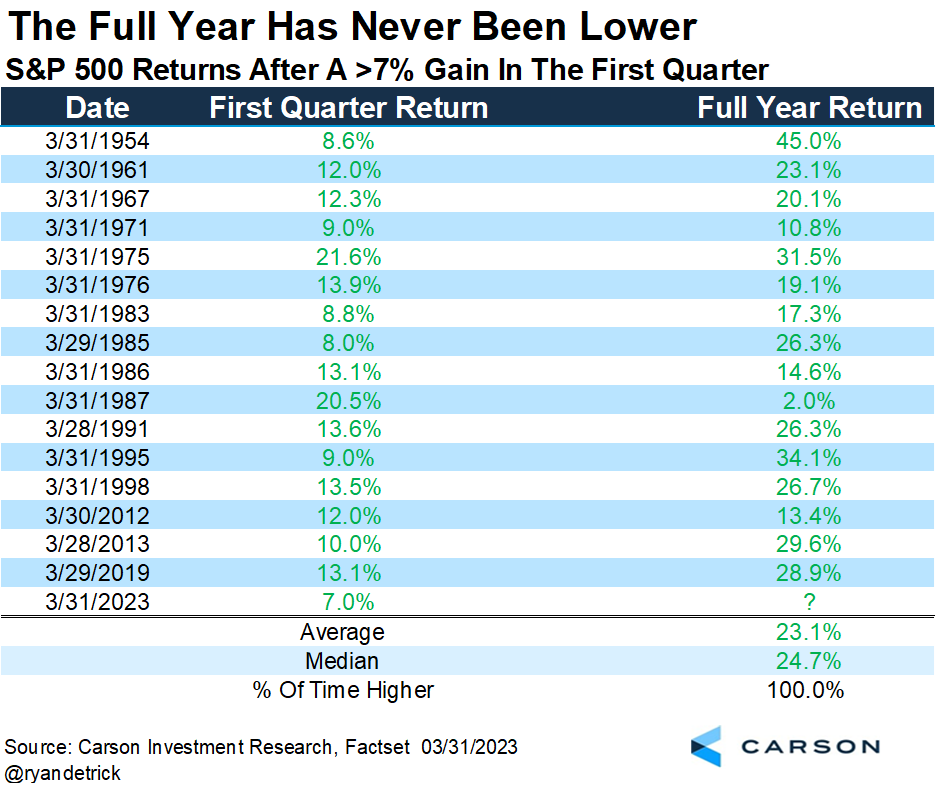

Despite the turbulence from earnings, data suggests the S&P 500 (INDEX: SPX) may perform well through year-end. Historically, the full-year return was always positive when the S&P 500 had a positive first quarter. However, there have been exceptions, says Callum Thomas, quoting data gathered by Ryan Detrick.

Graphic: Retrieved from Ryan Detrick via Callum Thomas’ Weekly S&P 500 ChartStorm.

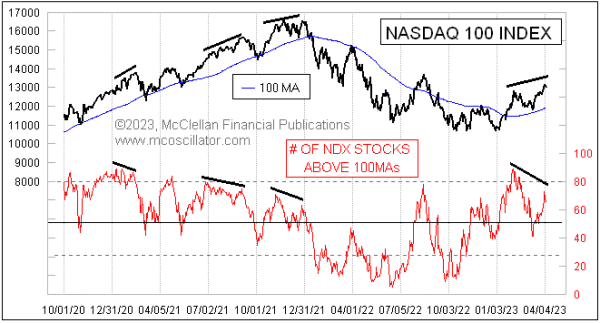

Peeking beneath the hood, only a few (primarily rate-sensitive) stocks have bolstered recent index strength; many components are not participating in the rally, which could be a harbinger of potential post-earnings weaknesses.

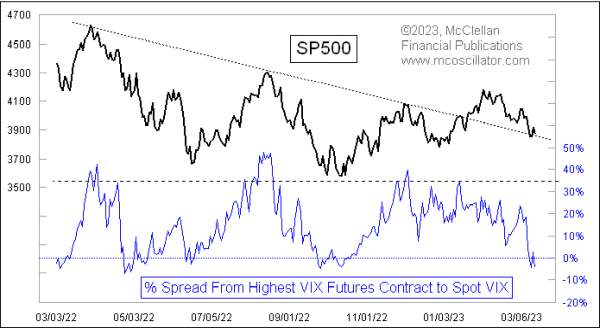

Graphic: Retrieved from McClellan Financial Publications.

Notwithstanding, if rates continue to fall, so do borrowing costs; falling inflation cuts pressures on input cost; rising unemployment helps keep labor costs under control, Bloomberg reports. The forecasts (not surveys) actually show earnings holding up better than the narrative suggests.

So what, then? In an annual report, JPMorgan Chase & Co (NYSE: JPM) concludes that if “we have higher inflation for longer, the Fed may be forced to increase rates higher than people expect despite the recent bank crisis.” Compounding the rate hikes is quantitative tightening or QT, the process of a central bank reducing the amount of money it has injected into an economy by selling bonds or other financial assets, which “may have ongoing impacts that might, over time, be another force, pushing longer-term rates higher than currently envisioned.” The net effect, though insights gleaned from the curve may be muddied due to the scale of recent interventions, is an “inverted yield curve [implying] we are going into a recession” and lower credit creation because, as Sergei Perfiliev well puts it, “if capital ends with the Fed, it is dead – it has left the economy and the banking system.”

Graphic: Retrieved from Bank of America Corporation (NYSE: BAC) via TheMarketEar.

How do we position ourselves, given all these narratives? Equity volatility implied (IVOL) and realized (RVOL) decreased. This may continue to be a booster. In fact, “if markets remain within a +/-1.5% range, a drop in volatility could trigger significant buying activity from the vol-control space, with up to $14 billion in notional flows hitting the tape, creating a favorable environment for equities,” says Tier1Alpha.

So, positioning-wise, stocks could trade up into a “more combustible” state where “volatility is sticky into a rally,” as Kai Volatility’s Cem Karsan said would happen.

SpotGamma confirms that, based on current positioning, SPX IVOL is projected to move up as the underlying index moves up; there are likely many people chasing the rally with long calls, “creating a swelling of call skew.”

In this environment, very wide call ratio spread structures discussed in past letters may continue to do well. We can use the profits from those call structures to cut the cost of our bets on the equity market downside and lower interest rates.

Graphic: Retrieved from SpotGamma’s Weekend Note.

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.

Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

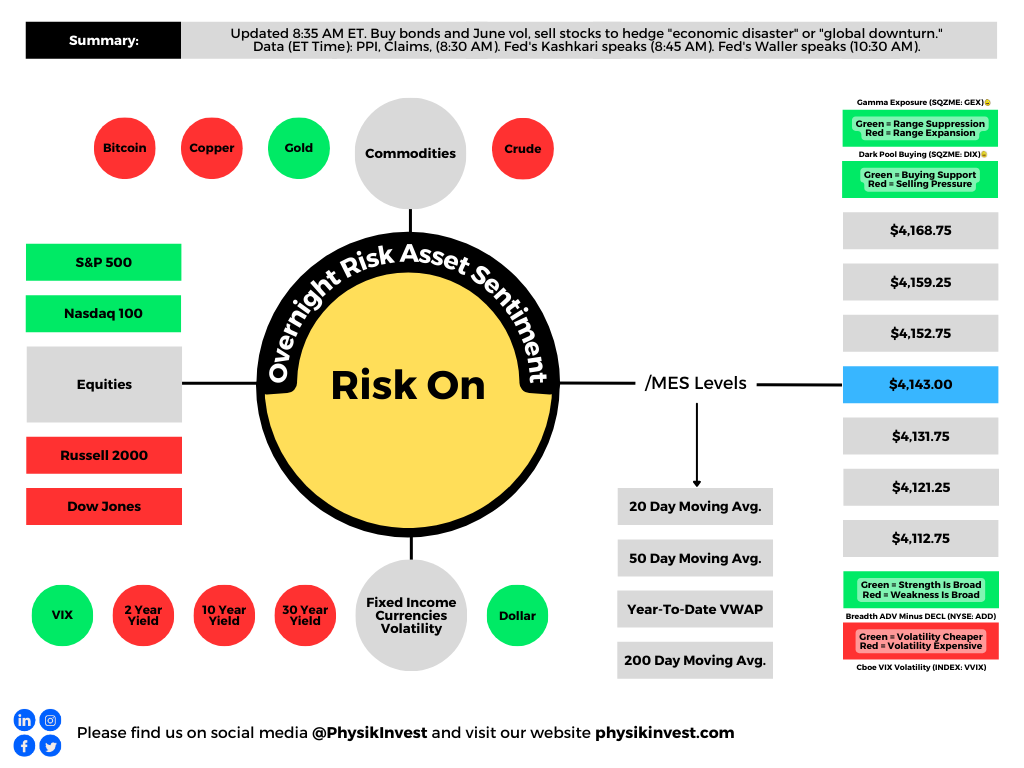

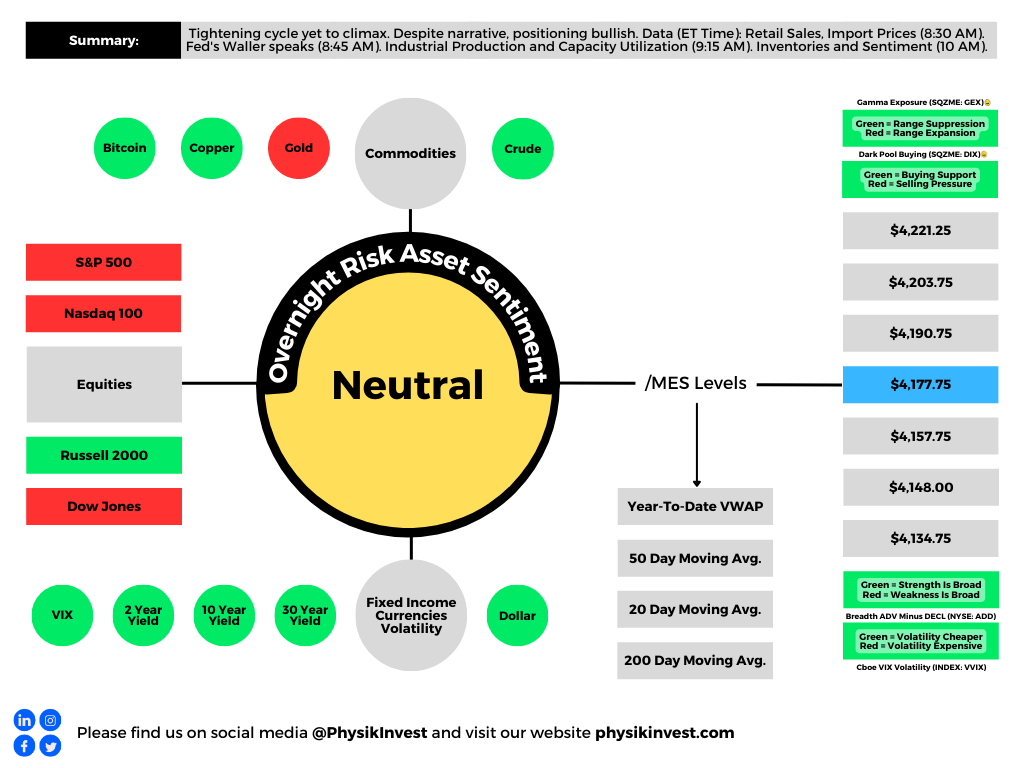

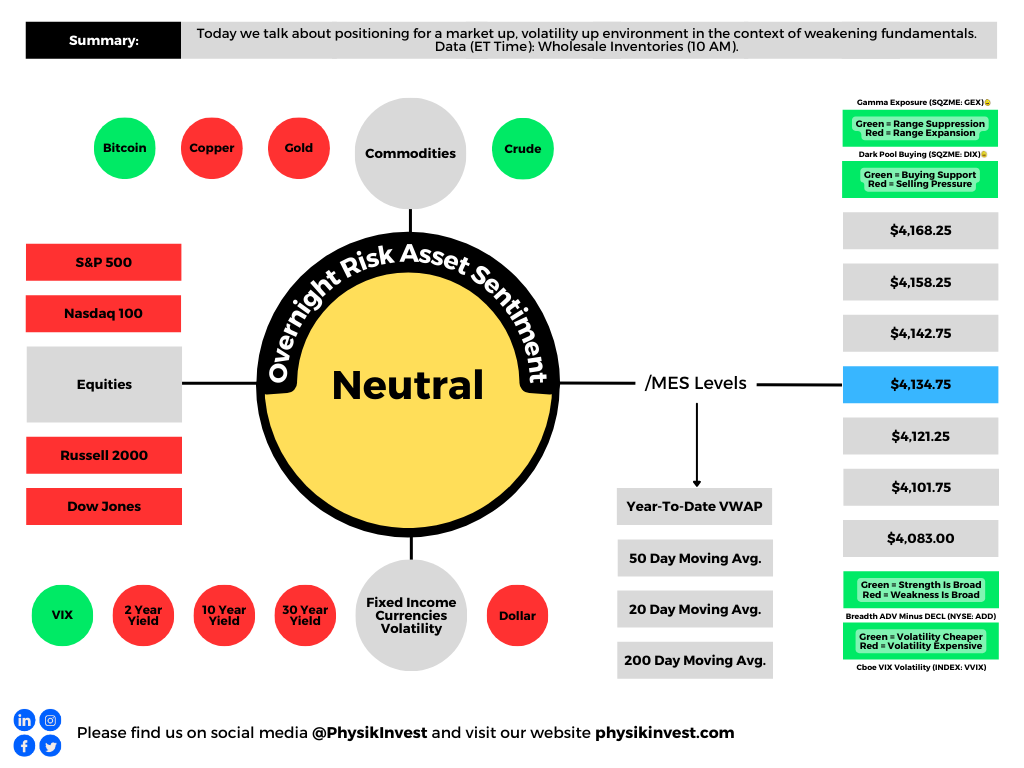

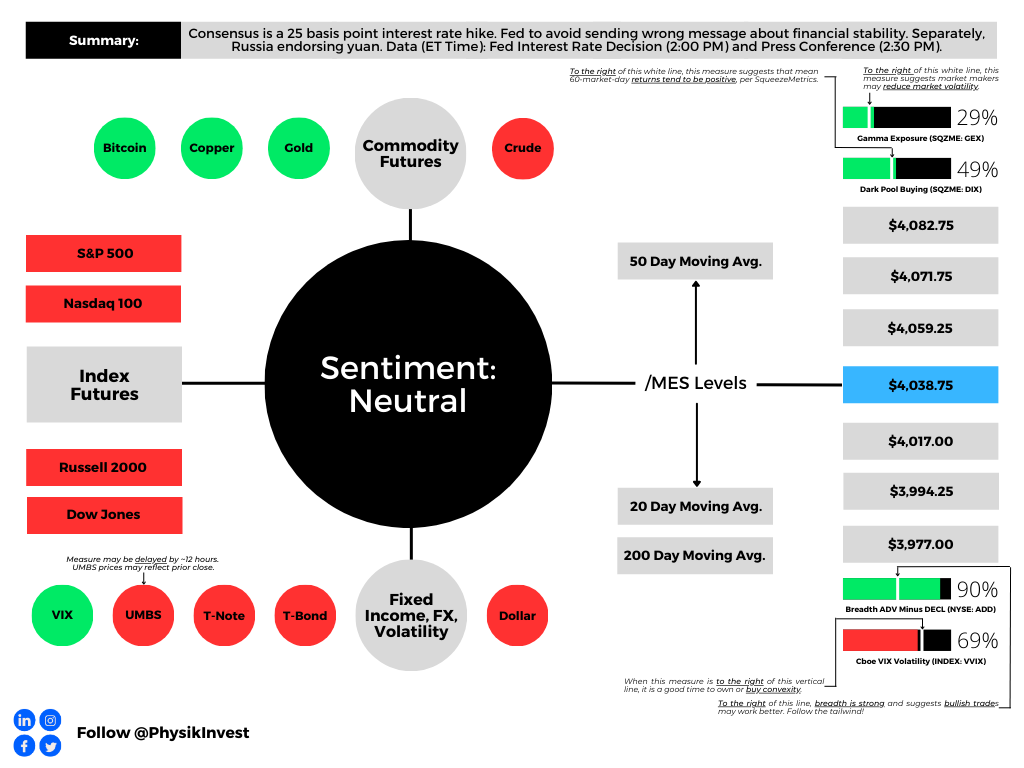

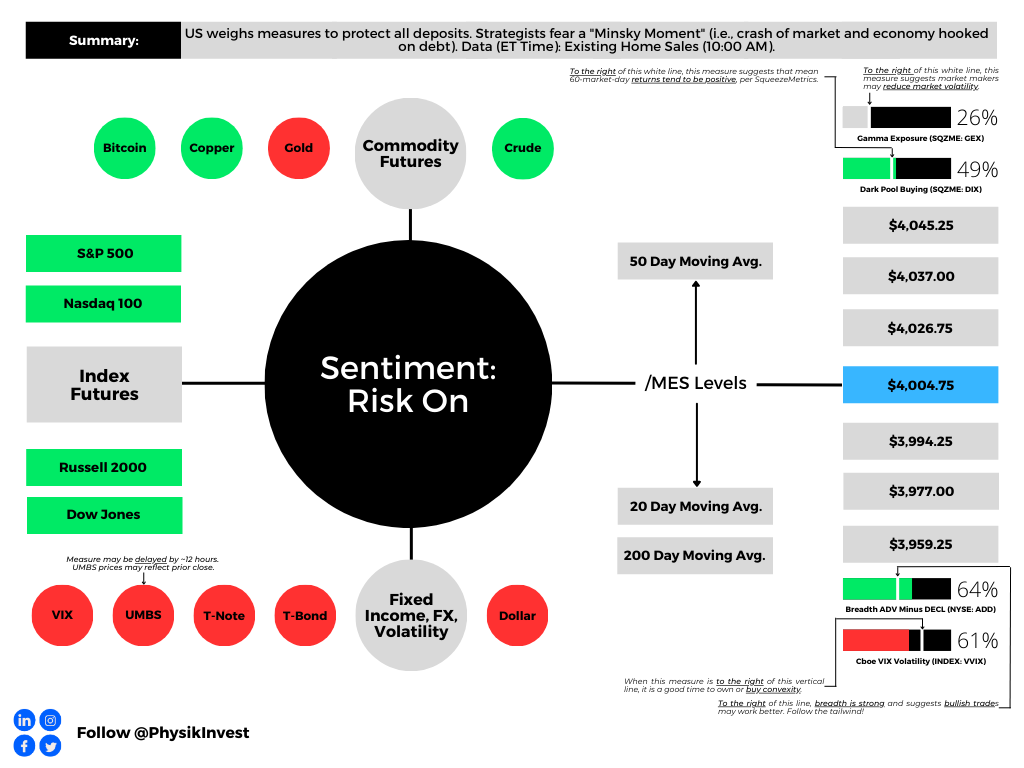

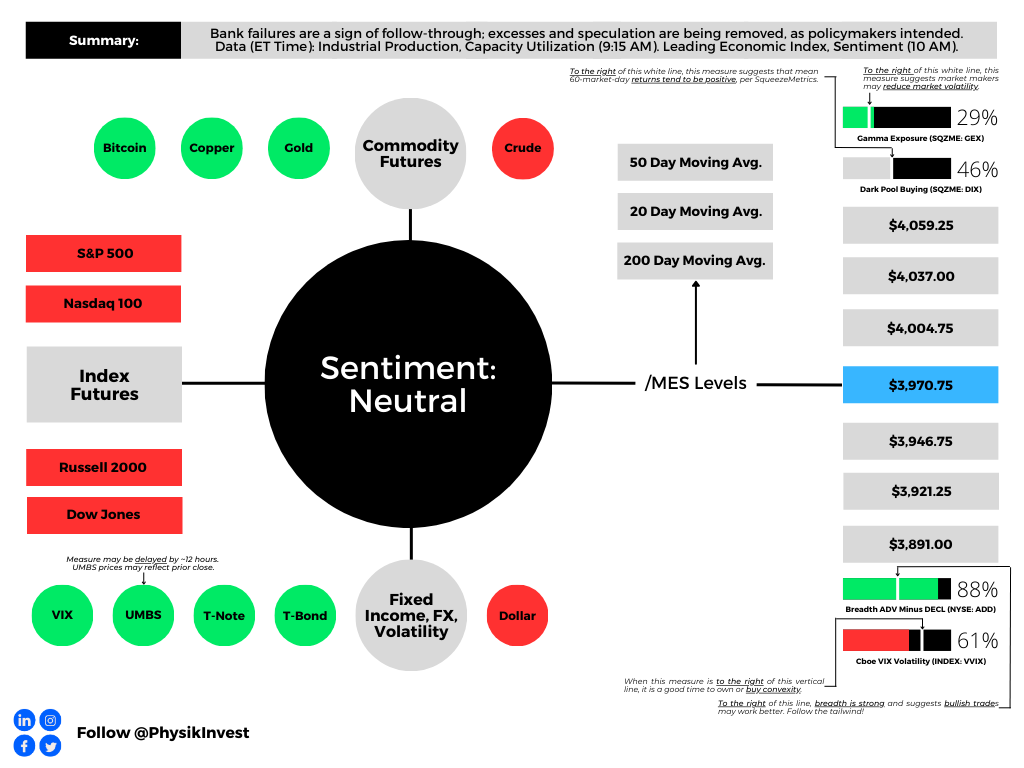

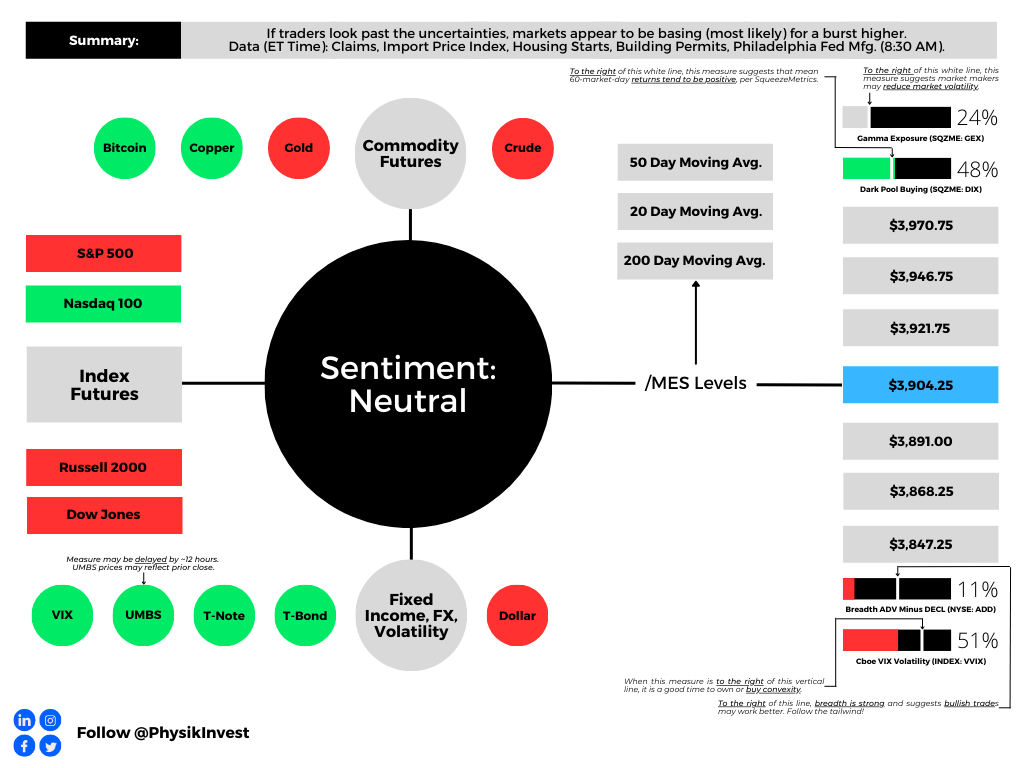

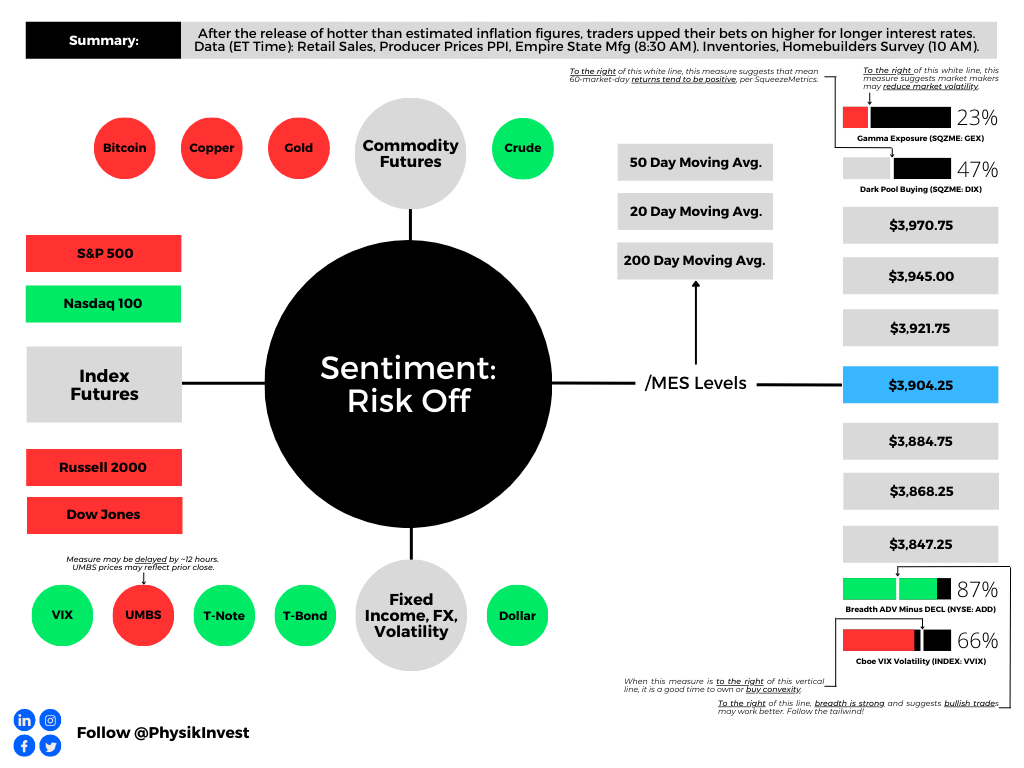

Graphic updated TIME AM ET. Sentiment Neutral if expected /MES open is inside of the prior day’s range. Sentiment Risk-On if expected /MES open is above the prior day’s range. Sentiment Risk-Off if expected /MES open is below the prior day’s range. /MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

Administrative

A shorter letter today, so there may be some holes we patch later. Take care!

Fundamental

The Federal Reserve (Fed) bumped its target rate up 25 basis points to 4.75-5.00% and opened the door to more hikes, barring market-induced financial tightening, as this letter put forward yesterday morning.

“The events in the banking system over the past two weeks are likely to result in tighter credit conditions for households and businesses, which would, in turn, affect economic outcomes,” Fed chair Jerome Powell commented, adding that credit tightening significantly means monetary policy “may have less work to do.”

Further, before the recent collapses of a few financial institutions, including SVB Financial Group, the market was pricing a 50 basis point hike.

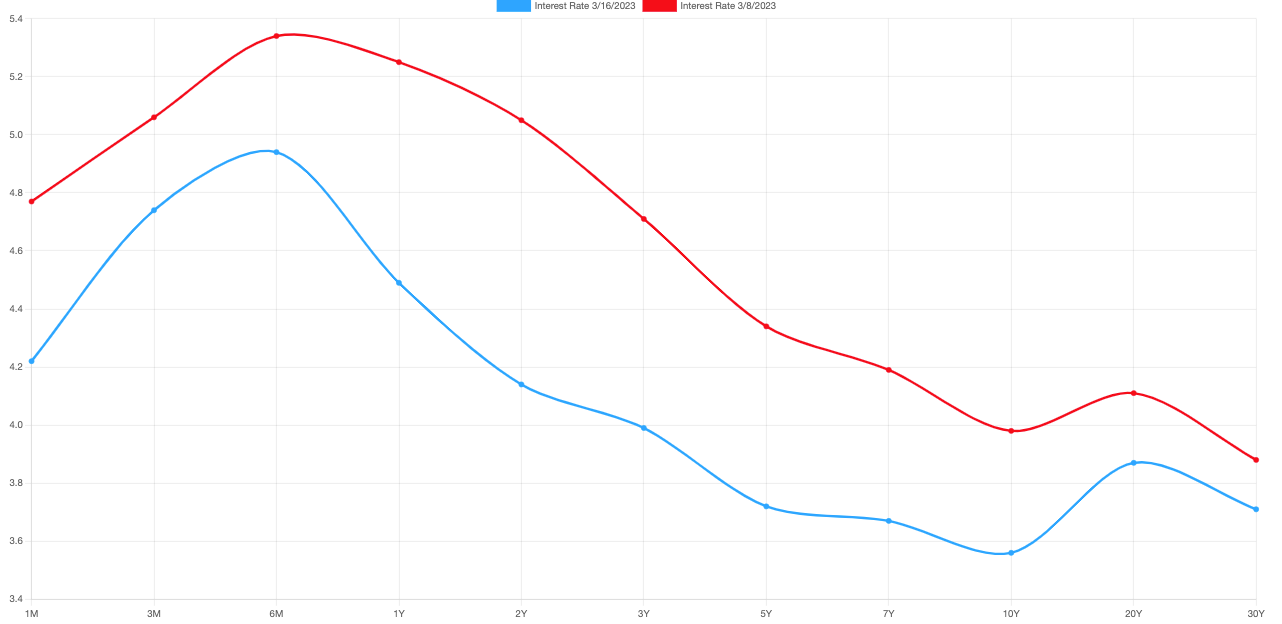

The below CME Group Inc’s (NASDAQ: CME) FedWatch Tool shows the market’s expectations on March 8. Note the 5.50-5.75% terminal (peak) rate.

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool via The Daily Brief for March 8, 2023.

“Absent SVB, the Fed would have likely raised 50 basis points,” TS Lombard’s Steve Blitz said. “SVB did happen, however, and so this FOMC, ever anxious about facing a recession (rising unemployment), is more than happy to let ‘tighter credit conditions for households and businesses … weigh on economic activity, hiring, and inflation.’ As for financial instability, they believe they have the tools to keep a few poorly managed banks from imploding the whole sector.”

Global layoff tally has moved up to nearly 500k since beginning of October per @Bloomberg … Tech & Consumer Discretionary sectors have led; and for nearly 800 companies that have cut jobs, median layoff has left company workforce 10% smaller pic.twitter.com/d6vlsPgQwj

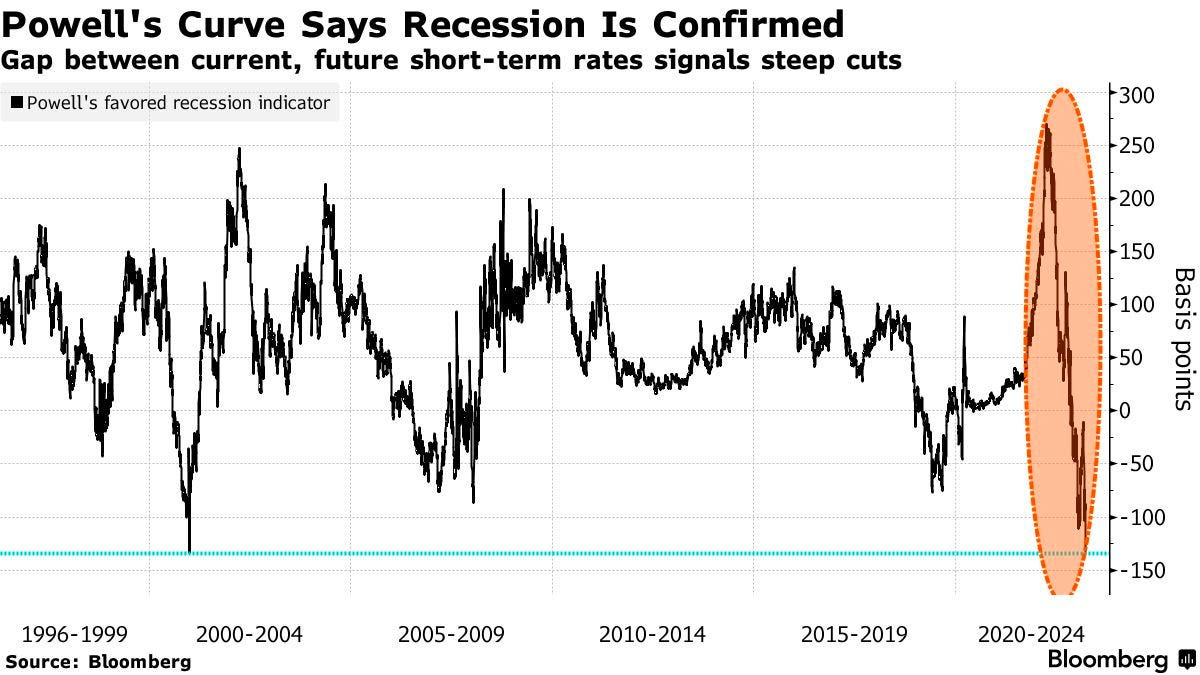

This is far higher than what the markets are pricing. Powell’s go-to measure for spotting economic troubles suggests steep cuts are also coming sooner than later.

Graphic: Retrieved from Bloomberg. “Frankly, there’s good research by staff in the Federal Reserve system that really says to look at the short — the first 18 months — of the yield curve. That’s really what has 100% of the explanatory power of the yield curve. It makes sense. Because if it’s inverted, that means the Fed’s going to cut, which means the economy is weak.” — Fed Chair Powell on March 21, 2022.

Anyways, given that what was expected happened, markets responded positively. If interested in why that is the case following important events as of late, see the Daily Brief for 2/1 and 2/2.

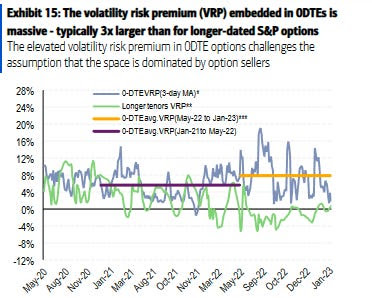

Graphic: Retrieved from Bank of America Corporation (NYSE: BAC) via Bloomberg. “Viewed through the lens of implied volatility — or expectations of how much an underlying asset will swing in the future — zero-day options aren’t particularly cheap in reality. The gap over the S&P 500’s realized volatility, something in derivatives parlance known as volatility risk premium, is typically three times higher than longer-dated contracts, according to BofA.” The compression of “will naturally lead to a buyback” that supports the market, Kai Volatility’s Cem Karsan says.

It was Treasury secretary Janet Yellen who took the market lower. Yellen said she has “not considered or discussed anything having to do with blanket insurance of guarantees of deposits,” and markets did not like that.

The likes of Pershing Square’s Bill Ackman responded he “would be surprised if deposit outflows don’t accelerate.” Adding, Federated Hermes’ Steve Chiavarone thought it was “astounding” Yellen and Powell would give contradictory messages.

“Powell essentially said that all deposits are safe; Yellen said, ‘Hold my beer.’ You would have thought that they would have coordinated,” responded Federated Hermes’ Steve Chiavarone.

To keep it brief, we’ll end with references to letters for 3/20 and 3/21, noting that the conditions for weak equity markets are present. The S&P 500 forward earnings are declining, the yield curve is inverted, unemployment is below average, manufacturing PMIs are below 50, and 40% of banks are tightening lending, Morgan Stanley (NYSE: MS) strategists explain.

Technical

As of 8:55 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET) in the S&P 500 will likely open in the middle part of a positively skewed overnight inventory inside the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $3,994.25.

Key levels to the upside include $4,004.25, $4,017.00, and $4,026.75.

Key levels to the downside include $3,977.00, $3,959.25, and $3,946.75.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold, barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for some time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future value tests as they offer favorable entry and exit.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.

Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Graphic updated 8:20 AM ET. Sentiment Neutral if expected /MES open is inside of the prior day’s range./MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

Administrative

Recall our past letters pondering the use of the yuan for settlements in the East. Well, there’s been progress on that end.

Putin: We are in favor of using the Chinese yuan for settlements between Russia and the countries of Asia, Africa, and Latin America. I am confident that these forms of settlement in yuan will develop between Russian partners and their counterparts in third countries. pic.twitter.com/Mnw1WfjW4Y

Also recall “the recycling of petrodollars by oil-rich nations” fueling “several emerging market debt crises” and prompting “the creation of a more speculative, debt-fueled economy in the US.” Is this a reversing trend? We shall unpack in a future letter, soon.

Fundamental

The Federal Reserve (Fed) is likely to bump its current target rate up 25 basis points to 4.75-5.00%. Failing to bump interest rates would likely send the wrong message about financial stability. To give up on the inflation fight (a pause or interest rate cut) would tell investors “look out below,” Bloomberg summarizes.

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

The path after is less certain, though most think there is likely to be at least one additional hike in the coming months. The catch is that if market-induced financial tightening persists through the second quarter, it would substitute for rate hikes.

Assuming the Fed publishes its summary of economic projections (SEP) or dot plot, they will likely show the governors “getting less aggressive,” adds Bloomberg’s John Authers.

If we recall, Kai Volatility’s Cem Karsan talked about the Fed not wanting liquidations; they want a slow sale, not a fire sale. So, with there being a lag, the Fed may want to slow and assess, carefully telegraphing this being not a pivot. A pivot would probably inspire confidence among investors to own assets “mak[ing] things hotter,” Karsan explains, noting that the Fed really needs to walk up the long end of the yield curve. Recall that the long end fell considerably on the back of the turmoil and intervention, as well as recent data (e.g., housing starts showing more supply, likely a mortgage application booster that would further “make things hotter”).

In large part the result of low liquidity, Treasury volatility could prompt the Fed to adjust their quantitative tightening or QT (i.e., the flow of capital out of capital markets) program, instead. Just as quantitative easing or QE (i.e., the flow of capital into capital markets) did little to spark off inflation, it’s unlikely that temping QT would disrupt efforts to rein inflation.

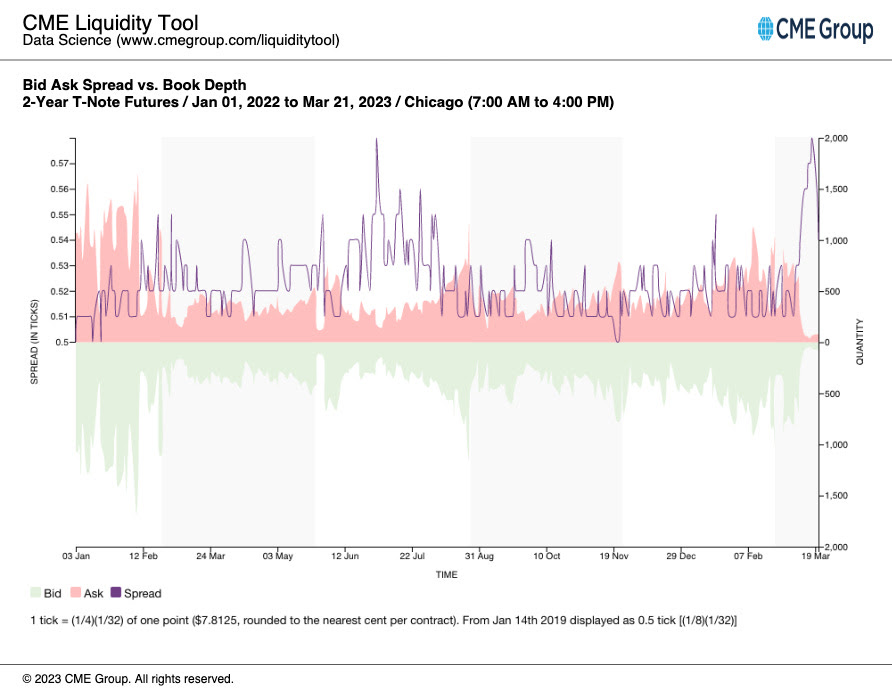

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) Liquidity Tool. Per a Bloomberg article, “the spread between offered prices and what sellers will accept has widened for all maturities, … a sign of thinning market depth” and illiquidity.

Adjusting QT, which is contributing to the excessive volatility, “would be preferable to not raising rates … [since] an abrupt pause in rate hikes would likely resurrect the notion that there’s, indeed, a Fed ‘put’ designed to bail out Wall Street at the first sign of stress,” a potential catalyst for market upside, says Robert Burgess.

In Tuesday’s letter, we talked about the potential for fears of downside easing and fears of missing out (i.e., FOMO) on upside rising. Specifically, the letter said the following:

“A response may be FOMO-type demand for call options exposures, coupled with CTAs further ‘raising their equity exposure’ on trend signals and lower volatility, boosting markets into a ‘more combustible’ state as explained on 2/17. This fear of missing out is visible in options volatility skew; traders are hedging those tail outcomes.”

In support of the most recent strength, per JPMorgan Chase & Co’s (NYSE: JPM) trade desk commentary, there is a buy skew. Goldman Sachs Group Inc (NYSE: GS) strategists agree, noting that flows are almost entirely “cover-driven.”

Recall that traders sought protection amidst all the calamities recently. Accordingly, measures of implied volatility or IVOL including the Cboe Volatility Index or VIX rose (e.g. traders demand exposure to downside put protection by way of S&P 500 options which bids options prices and manifests higher IVOL and counterparty pressure from their equity future/stock sales to hedge this demand). These same measures of IVOL are now falling as traders’ closure of protection results in counterparty pressures being lifted (helping explain, in part, the above “cover-driven” remark by GS).

Does this rally have breadth behind it? Look no further than market internals.

Graphic: Retrieved from Bloomberg via Liz Young. “The Nasdaq’s Cumulative Advance-Decline line has parted ways with index direction in recent days. In other words, the index has rallied despite weak breadth (more stocks falling than rising), the two lines are likely to find their way back together somehow…”

A pause before the Fed announcement, and then breadth catches up to price?

Or, has the typical post-Fed IVOL boost been spent?

Regardless, we maintain that low-cost call options structures as proposed in previous letters worked (and may continue to work). Notwithstanding, look for opportunities to play the downside should markets trade higher into a “more combustible” position.

More on trade ideas in the next letters. Take care.

Technical

As of 8:15 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a negatively skewed overnight inventory, inside of the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $4,038.75.

Key levels to the upside include $4,059.25, $4,071.75, and $4,082.75.

Key levels to the downside include $4,017.00, $3,994.25, and $3,977.00.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures (bottom middle).

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.

Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Graphic updated 7:00 AM ET. Sentiment Risk-On if expected /MES open is above the prior day’s range. /MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

Administrative

Not all doom and gloom. Make sure to read to the end!

Fundamental

In the Daily Brief for 3/20, we summarized the financial industry and policymaker responses that would turn asset fire sales into managed, orderly asset sales.

The net result of the intervention would be a reduction in credit creation, a tightening of financial conditions, as well as a slowing of the economy and inflation while, potentially, setting “a dangerous precedent that simply encourage[s] future irresponsible behavior” (e.g., risky lending/borrowing), the House Freedom Caucus put eloquently. Basically, the fear is in policymakers underwriting the losses of prevailing carry-type strategies and setting the stage for an even bigger unwind or so-called “Minsky moment,” the “sudden crash of markets and economies that are hooked on debt,” Bloomberg reports.

"Regional banks relied on a business model that relied on uninsured deposits," says @Lazard's @porszag. "The government needs to make explicit what a lot of people are assuming: that for the foreseeable future, uninsured deposits don't exist. Everything is insured." pic.twitter.com/GgZ9ZF2f7r

A systemic credit event is among strategists’ biggest fear, indeed. A Bank of America Corporation (NYSE: BAC) survey shows a credit event happening on the heels of a US shadow banking, corporate debt, and developed-market real-estate collapse. Recall this letter writer’s conversation with Simplify Asset Management’s Michael Green who said he sees “cracks in bubbles like commercial real estate” already appearing, too.

Bloomberg adds that JPMorgan Chase & Co (NYSE: JPM) strategists think the inverted yield curve signals recession and the stocks are likely nearing their high point.

Graphic: Retrieved from Callum Thomas’ Weekly S&P 500 ChartStorm.

JPM adds that market lows won’t occur until interest rate cuts ensue.

Graphic: Retrieved from BNP Paribas ADR (OTC: BNPQY).

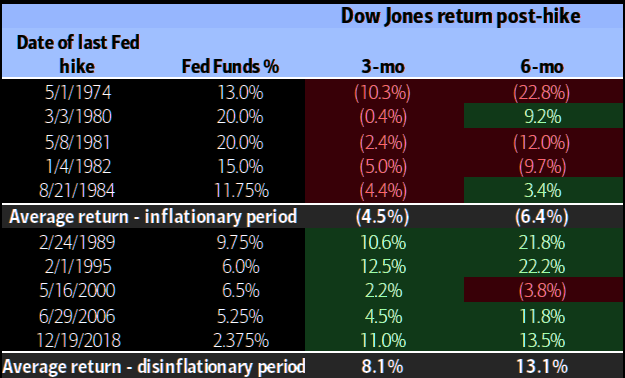

Recall 3/20’s letter citing BAC research that finds selling markets on the last Fed rate hike is a good strategy. The “Minsky moment” comment/fear has others at JPM adding that investors should sell into relief bounces.

Graphic: Retrieved from Bank of American Corporation (NYSE: BAC) via The Market Ear.

Most participants foresee rates continuing to rise by at least 25 basis points, per the CME Group Inc’s (NASDAQ: CME) FedWatch Tool. Following Wednesday’s (expected) hike, the path forward appears uncertain. Yesterday, the terminal/peak rate was at 4.75-5.00%. Today, the peak has shifted higher to 5.00-5.25%.

Graphic: Retrieved from CME Group Inc (NASDAQ: CME).

Financials look ready to fall off a cliff, to add. If they do, the whole market likely goes.

Graphic: Retrieved from Callum Thomas’ Weekly S&P 500 ChartStorm.

Positioning

We keep referring back to our Daily Briefs published last week (e.g., 3/13 and 3/14). In those letters, we talked about the growing concern about markets enduring some exogenous shocks.

We opted to take the less extreme side since policymakers’ response was likely to stem (or push into the future) turmoil. Additionally, with participants easing up on their long-equity exposure, equity markets were likely to stay contained, relative to bond markets where the lack of liquidity is an issue, some believe. Anyways, following important events including inflation updates (i.e., CPI) and derivatives expiries, short bursts of strength (particularly in some of the previously depressed products such as the Nasdaq 100 or NDX, as explained 3/17) were likely to ensue heading into the end of this month and next month. Additionally, certain rates trades via options we set forth on 3/14 were ripe for monetization, too.

Rotating into a money market or T-bill fund or box spreads, while allocating some remaining cash to leverage potential by way of some call options structures, appeared attractive. While the T-bill or box spread exposures did not budge much, call options structures as proposed on 3/14 worked (and are likely to continue to work) rather well. The monetization of the rate structures discussed on 3/14 was timely, also.

The potential for coming events including the Federal Reserve’s (Fed) interest rate decision on Wednesday 3/22 to assuage participants’ fears of slowing may, accordingly, prompt fears of missing out on the upside, Bloomberg reports. A response may be FOMO-type demand for call options exposures, coupled with CTAs further “raising their equity exposure” on trend signals and lower volatility, boosting markets into a “more combustible” state as explained on 2/17. This fear of missing out is visible in options volatility skew; traders are hedging those tail outcomes.

Technical

As of 7:00 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, outside of the prior day’s range, suggesting a potential for immediate directional opportunity.

The S&P 500 pivot for today is $4,004.75.

Key levels to the upside include $4,026.75, $4,037.00, and $4,045.25.

Key levels to the downside include $3,994.25, $3,977.00, and $3,959.25.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Reduction in dealer Gamma exposure. There may be an increase in volatility after the removal of large options positions and associated hedging.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.

Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Graphic updated 8:10 AM ET. Sentiment Neutral if expected /MES open is inside of the prior day’s range. /MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

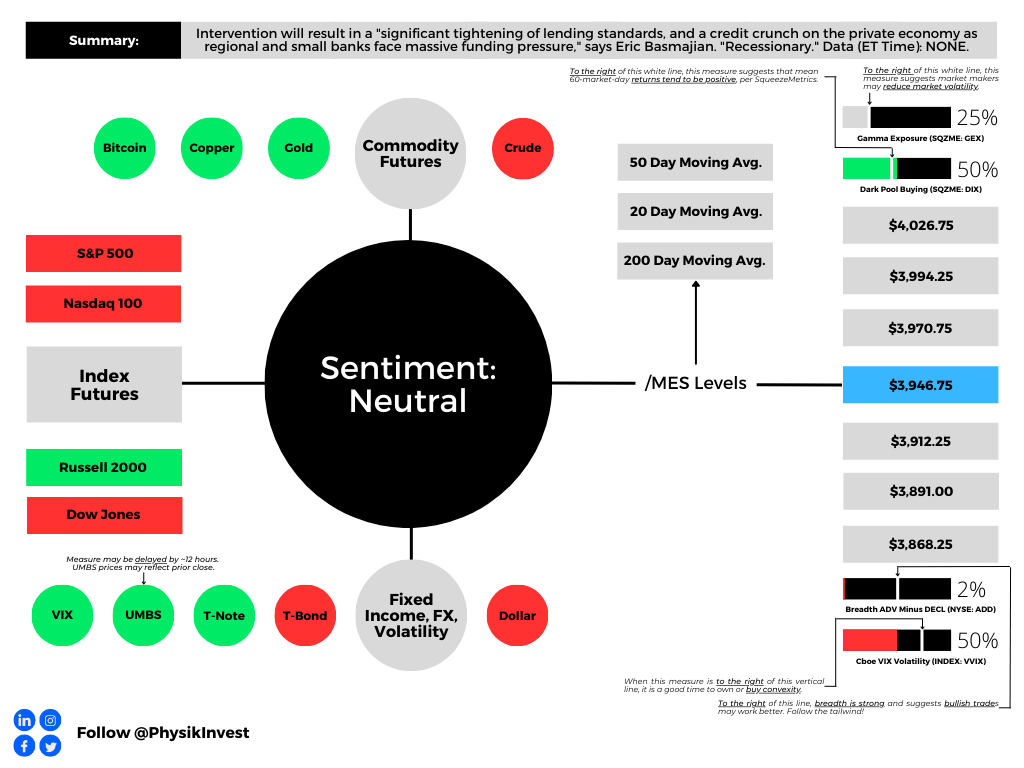

Fundamental

As well summarized by Eric Basmajian, inflation, and growth are on a downward trajectory. Most leading indicators “suggest recessionary pressure will be ongoing.” The banking crisis and response, which will ultimately “cause a tightening of lending to the private economy,” likely exacerbates the ongoing recessionary pressures.

Most strategists including the Damped Spring’s Andy Constan agree. In a recent video, Constan detailed the implications of policymakers’ intervention. In short, an asset fire sale was turned into a managed sale, and a reduction in credit creation will tighten financial conditions, slowing the economy and inflation.

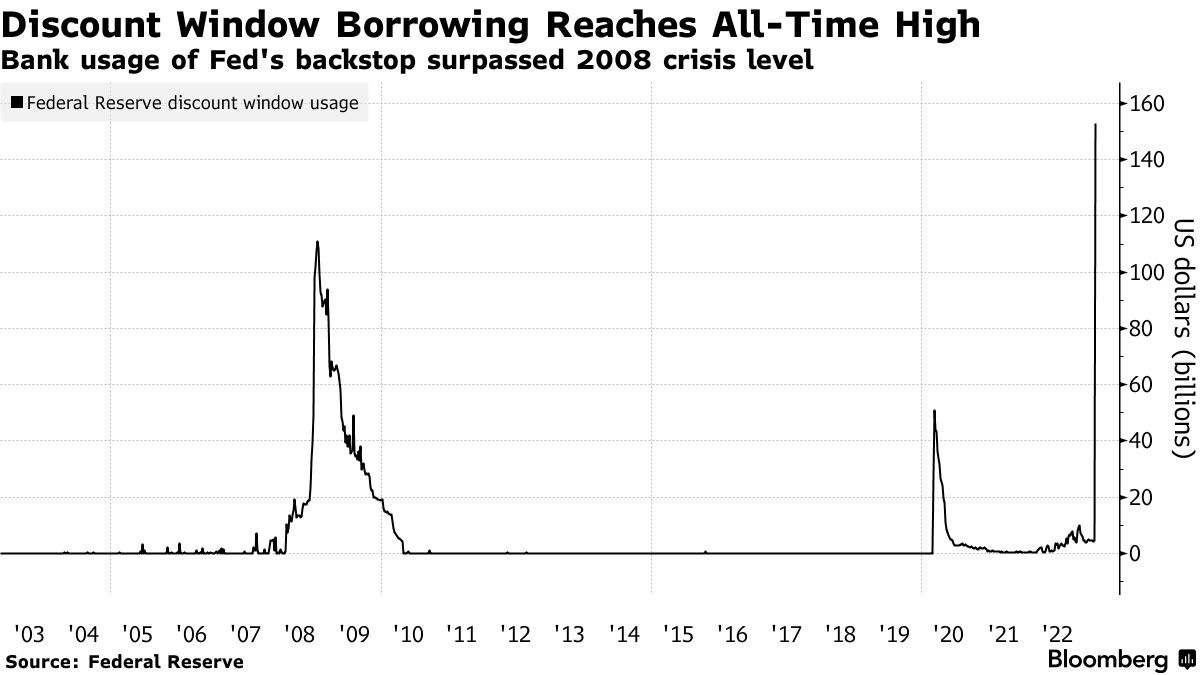

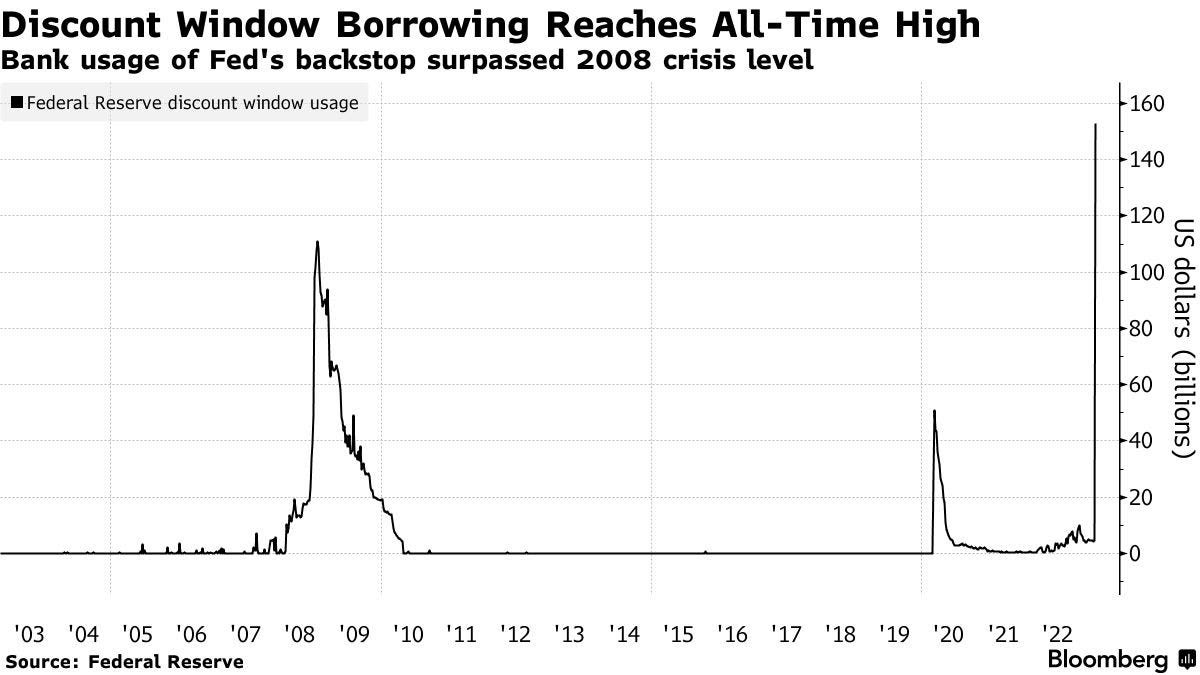

“Small banks that are facing deposit outflows will see earnings and margins collapse as their cost of funds surges from 1% or 2% on deposits to 4% or 5% at the Fed funding facility,” Basmajian summarizes, noting that the increase in the Federal Reserve (Fed) balance sheet came from the discount window, new bank funding facilities, and spillover from the FDIC insurance backstop, all of which are not to be confused with quantitative easing or QE (i.e., monetary stimulus and a flow of capital into capital markets).

Graphic: Retrieved from Bank of American Corporation (NYSE: BAC) via The Market Ear.

“As deposits leave regional and smaller banks for more yield and safety, they will flow into bigger banks that do less lending or into money market funds that don’t drive credit creation.” Consequently, there will be “a significant tightening of lending standards, and a credit crunch on the private economy as regional and smaller banks face massive funding pressure.”

Graphic: Retrieved from Morgan Stanley (NYSE: MS) via The Market Ear. “MS models show that a permanent +10pt tightening in lending standards for C&I loans leads to a 35bps rise in the unemployment rate over the next two years. Historically, recessions have arrived more than half a year after jobless claims begin a sustained rise.”

Traders are conflicted about the Fed’s coming interest rate decision. Many were expecting a couple more hikes of at least 25 basis points in size. However, following the recent bank turmoil in the US and abroad, it appears that traders think it will be one additional 25 basis point hike before rate cuts ensue in mid-2023.

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

Historically, selling markets on the last Fed rate hike is a good strategy, Bank of America found.

Graphic: Retrieved from Bank of American Corporation (NYSE: BAC) via The Market Ear.

Positioning

Top-line measures of implied volatility or IVOL including the Cboe Volatility Index or VIX are higher heading into Monday’s trade.

Macro uncertainties have some frightened, hence “equity volatility present[ing] itself in a much stronger way,” said The Ambrus Group’s Kris Sidial. For this equity volatility (i.e., implied volatility or IVOL) to continue performing well, realized volatility or RVOL (i.e., the movement that actually happens and is not implied by traders’ supply and demand of options) must shift and stay higher as well (note: in many ways RVOL and IVOL reinforce the other during extreme greed or fear events.

Though big options expiries (OpEx) “may help unpin the market” and manifest market downside and follow-through in RVOL needed to keep IVOL performing, the window for this to happen may be closing.

The monetization of profitable options structures, as well as volatility compression and options decay, may result in counterparties buying back their short stock and/or futures hedges (to the short put positions they have on), thus boosting the market (particularly the depressed and rate-sensitive Nasdaq 100).

If the market rallies, that has the potential to “make things hotter” in the economy, explained Kai Volatility’s Cem Karsan, which emboldens policymakers to make and keep policy tighter. So, barring follow-through to the downside, any equity market upside that arises is likely limited, as a disclaimer, some think.

Apologies for rushing this section, today. More on positioning in the coming letters.

Technical

As of 8:10 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a negatively skewed overnight inventory, inside of the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $3,946.75.

Key levels to the upside include $3,970.75, $3,994.25, and $4,026.75.

Key levels to the downside include $3,912.25, $3,891.00, and $3,868.25.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 (FUTURE: /MES) bottom-middle.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.

Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Graphic updated 8:50 AM ET. Sentiment Neutral if expected /MES open is inside of the prior day’s range. /MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

Fundamental

Higher asset prices boosted household wealth and demand; consumers’ increased ability to spend more wealth pushed up inflation. If policymakers use their tools to lower household wealth and demand, this should cut down on inflation.

Kai Volatility’s Cem Karsan says the latter was a policy objective and recent financial institution failures are a sign of follow-through; excesses and speculation are being removed, as policymakers desired.

Policymakers don’t want liquidations, however. They want lower asset prices. Recent events put policymakers in an odd position after raising rates non-stop. In the Federal Reserve’s (Fed) case, and we paraphrase Karsan, policy/rates moved very quickly with little pause. With there being a lag, the Fed may want to pause and assess. However, they have to telegraph this carefully so that the market does not read it as a pivot. If the market rallies, that “makes things hotter,” Karsan says.

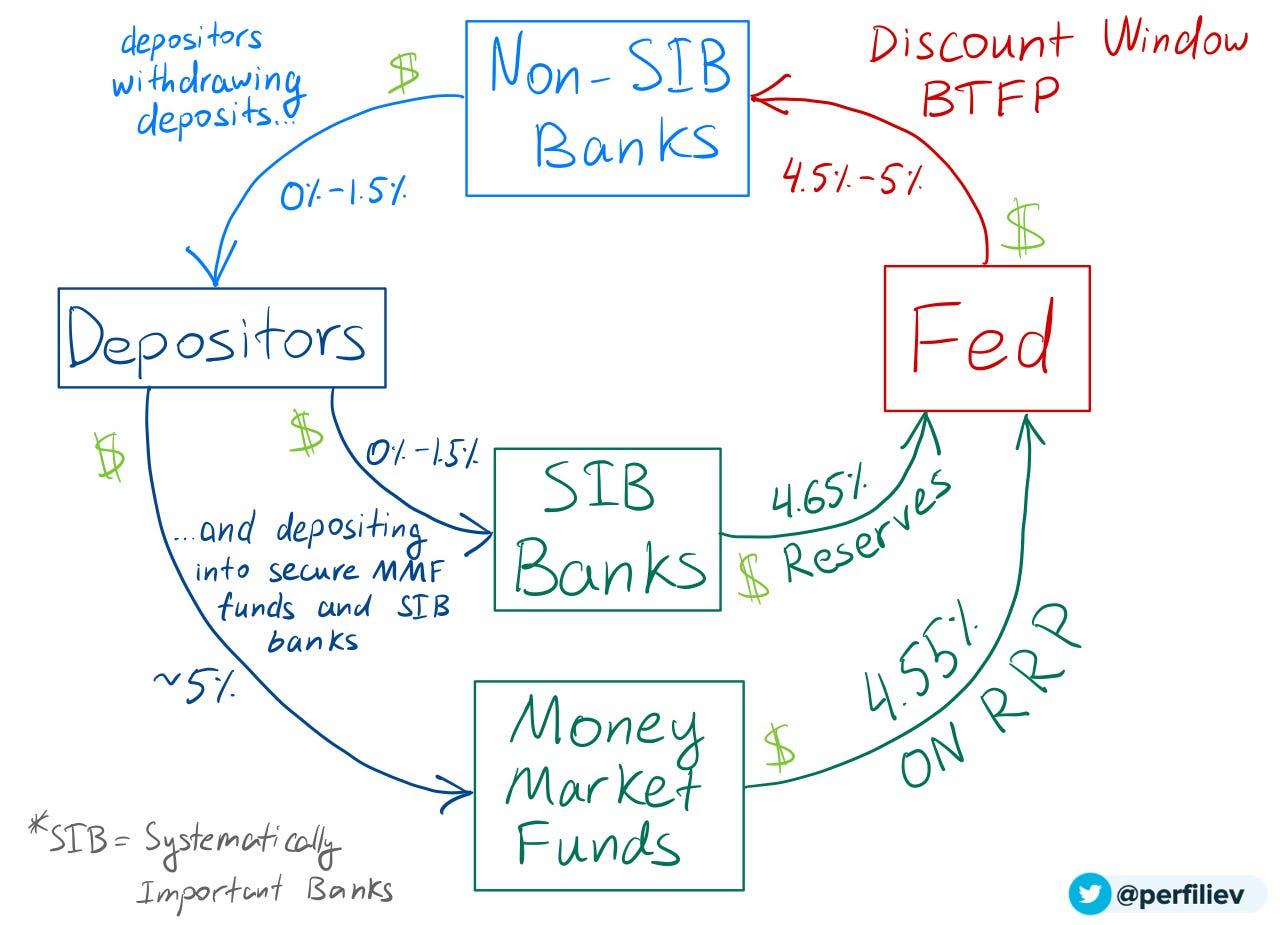

Before BTFP. Fire sale of assets from bank experiencing a run. Bank getting new deposit already has desired equity risk and no need to lever

After BTFP 1 year to sell assets of losing bank Bank getting new deposit already has desired equity risk and no need to lever

There’s already been an overreaction in the bond market, he adds, which is not ideal. The Fed does not want the long end of the yield curve to fall, as it has on the back of the turmoil and intervention, as well as data including housing starts which show more supply coming onto the market, likely a mortgage application booster in the near term.

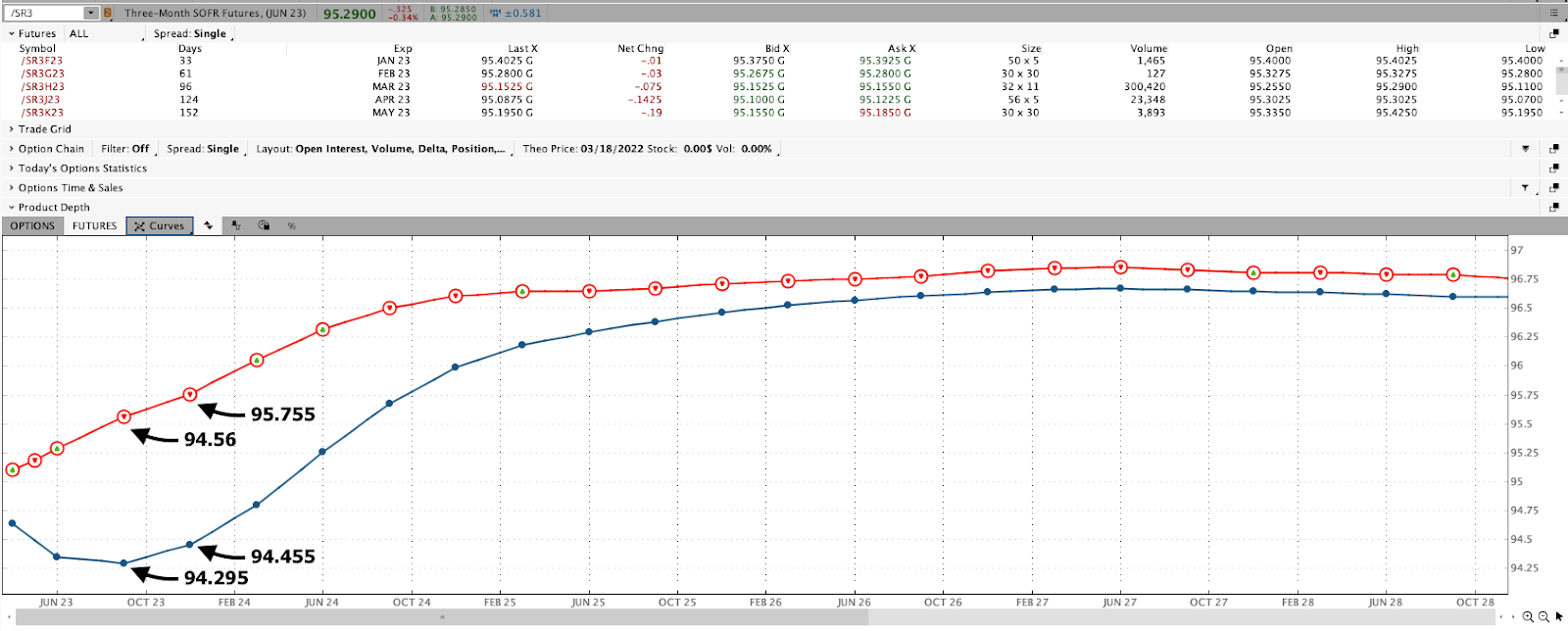

Even at the front end, there’s been lots of movement. This has “forc[ed] widespread risk liquidation,” Bloomberg says. Take a look at the Three-Month SOFR (FUTURE: /SR3), a tool used to hedge USD short-term interest rates.

Graphic: Retrieved from Charles Schwab Corporation-owned (NYSE: SCHW) TD Ameritrade’s thinkorswim platform.

The consensus, which Karsan agrees with, is that the Fed moves forward with a 25 basis point hike while telegraphing it wants the long end of the curve to rise or higher for longer as it is colloquially referred to.

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

It is possible for the US policymakers to adopt a meeting-by-meeting stance, as their counterparts have in Europe, letting uncertainties regarding the likes of Credit Suisse Group AG (which just received a ~$54 billion or so liquidity backstop and is mulling a combination with other lenders), SVB Financial Group (NASDAQ: SVB) and First Republic Bank (NYSE: FRC) pan out.

Graphic: Retrieved from Bloomberg. “[T]he credit extended through the two backstops show a banking system that is still fragile and dealing with deposit migration in the wake of the failure of Silicon Valley Bank of California and Signature Bank of New York last week.” Per John Authers: the phenomenal borrowing from the Fed’s discount window suggests that if these are just liquidity problems, they are widespread and serious. Further, the point of the exercise is to slow down the economy, which will in time tend to put pressure on banks’ solvency.”

Pausing, or intending to pause explicitly, could raise inflation expectations or “boost the odds of a recession by spooking consumers and companies into believing that the economy is worse off than they thought,” Bloomberg explains, noting: “All told, the emergency loans reversed around half of the balance-sheet shrinkage that the Fed has achieved since it began so-called quantitative tightening — allowing its portfolio of assets to run down — in June last year.”

Graphic: Compiled by Physik Invest.Per Jefferies Financial Group Inc’s (NYSE: JEF) Christopher Wood: “2022 was the year when US equities suffered multiple contraction from monetary tightening. This year will be the year when earnings downgrades hit the stock market if the US recession forecast proves to be accurate. This is now the key issue in world financial markets. Then 2024 will be the year when markets will have to deal with the emerging credit problems in the private space.”

Positioning

Heading into this most recent market decline, investors foresaw increased volatility and were positioned for it as indicated by the pricing of tail risk and performance of implied volatility or IVOL (as investors continued to demand protection during this window of non-strength), said Laya Royer of Citadel Securities.

Recall that Kris Sidial warned us of this. Options, colloquially referred to as volatility, would serve as the only hedge in an environment wherein commodities, stocks, and bonds don’t combine or balance each other as well as they did in 2022.

Now, there are options expirations (OpEx) nearing (March 16 and 31); monetization of profitable options structures, as well as volatility compression and options decay, have counterparties buying back their short stock and/or futures hedges (to the short put positions they have on), boosting the market (particularly the depressed and rate-sensitive Nasdaq 100) through this OpEx/triple witching window.

Graphic: Retrieved from Cboe Global Markets (BATS: CBOE).

Following this period, the “rollover” of existing positions may result in “price swings” that last, Bloomberg puts forth. “This quarterly expiry may help unpin the market.”

Structures proposed in the Daily Brief for March 14 may work in reducing portfolio downside while allowing you to participate directionally at less cost.

Technical

As of 8:50 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a negatively skewed overnight inventory, inside of the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $3,970.75.

Key levels to the upside include $4,004.75, $4,037.00, and $4,059.25.

Key levels to the downside include $3,946.75, $3,921.25, and $3,891.00.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 (FUTURE: /MES) at the middle bottom.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.

Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Graphic updated 7:15 AM ET. Sentiment Neutral if expected /MES open is inside of the prior day’s range. /MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

Administrative

As previously indicated, through the end-of-this week, newsletters may be shorter due to the letter writer’s commitments. Take care!

Fundamental

Based on the 30-Day Fed Funds (FUTURE: /ZQ), traders expect the Federal Reserve (Fed) to continue its tightening campaign with a 25 basis point rate hike at the next Federal Open Market Committee (FOMC) meeting. Following this, traders expect one more 25 basis point hike that brings the terminal or peak rate to 5.00-5.25%.

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

Earlier this week, traders were pricing out hikes on financial institutions’ liquidity issues (e.g., SVB Financial Group) and data, including producer prices and retail sales, “moving in the right direction,” said Vital Knowledge’s Adam Crisafulli.

Graphic: Retrieved from Bloomberg via Gavekal Research/Macrobond. Recall that the Fed believes in needs a certain level of reserves for the proper functioning of the financial system (~$2 trillion). In 2019, banks dumped a lot of their reserves into repo to earn some extra return. When QT was about to end, there was less money in their reserves which preceded a spike in rates and a blow-up among those who needed the money the most, as explained here. Read the Daily Brief for September 20, 2022, for more.

Now, with fear of contagion ebbing on authorities’ commitment to preventing an “all-out systemic crisis,” explains Bloomberg’s John Authers, traders are again expecting a 5.00-5.25% terminal or peak rate.

Read: Credit Suisse Group AG (NYSE: CS) protection reaches prohibitively expensive levels as banks rush into CDS after big shareholders hesitate to boost their stake. Switzerland was forced to step in with a $54 billion lifeline to stabilize the crisis.

Graphic: Retrieved from Bloomberg via Holger Zschaepitz.

Adding, as Unlimited’s Bob Elliott puts it, “in the [Global Financial Crisis], credit risk spread rapidly. Today, there is very little [credit default swap] impact” or carryover.

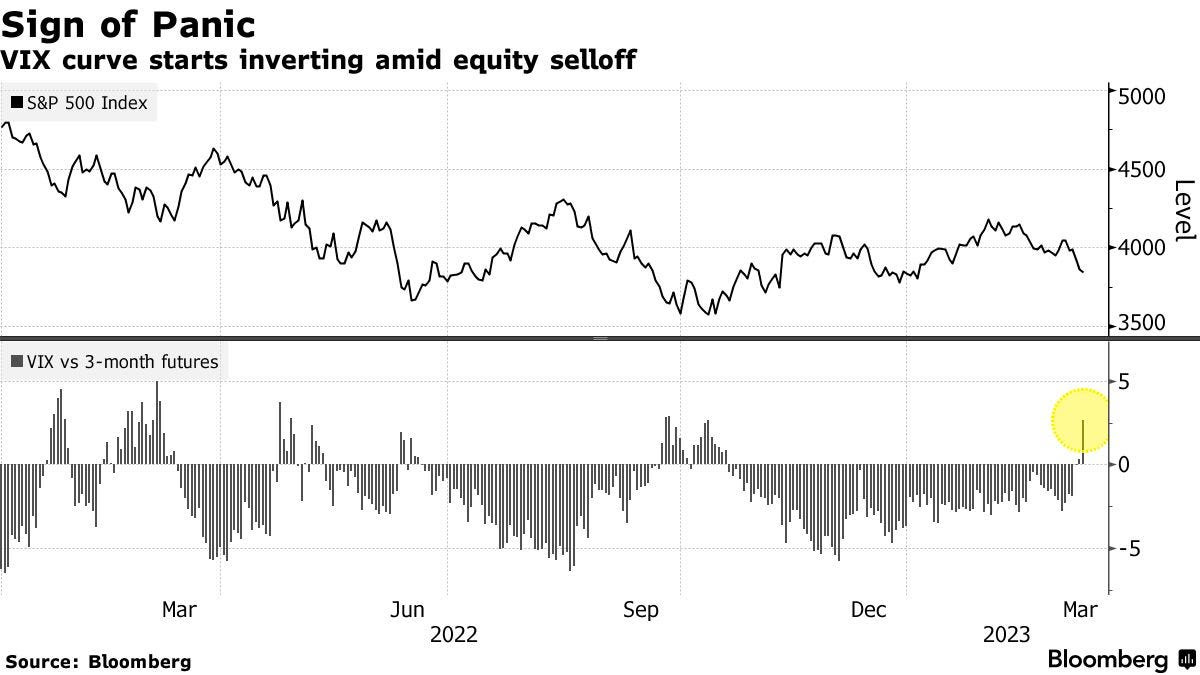

Following measures of US Treasury yield volatility implied by options (i.e., bets or hedges on or against market movement) adjusting higher, equity market volatility strengthened as observed by measures of convexity (e.g., Cboe VIX Volatility Index or VVIX). The Daily Brief for March 14 talked about this in detail.

Graphic: VVIX chart retrieved from TradingView.

For this protection to keep its value and continue to perform well, realized volatility or RVOL must shift higher substantially and stay elevated. That’s not really happening to some big extent, at least in the equity market. Consequently, put structures such as bear put spreads in the S&P 500 (INDEX: SPX), for example, are not performing.

Graphic: Retrieved from Alpha_Ex_LLC. “Easy to argue that rate vol is leading and in this context, one could suggest VIX has room to rise from here.” However, it would “take a lot for the MOVE to sustain itself at this level.”

This information, coupled with falling implied volatility or IVOL, the passage of nearing derivatives expiries, and the strength of products like the Nasdaq 100 (INDEX: NDX) relative to others like the Russell 2000 (INDEX: RUT), has your letter writer leaning optimistic. Though it may be too early to position for strength, one may consider it the way it was explained in the Daily Brief on March 14.

Graphic: Retrieved from Tom McClellan. “The direct message is that the SP500 options traders who drive the VIX Index are feeling more fearful than the VIX futures traders believe is merited.”

Technical

As of 7:15 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a balanced overnight inventory, inside of the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $3,904.25.

Key levels to the upside include $3,921.25, $3,946.75, and $3,970.75.

Key levels to the downside include $3,891.00, $3,868.25, and $3,847.25.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures (bottom middle).

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.

Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Graphic updated 6:15 AM ET. Sentiment Risk-Off if expected /MES open is below the prior day’s range. /MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

Administrative

As indicated yesterday, through the end-of-this week, newsletters may be shorter due to the letter writer’s commitments. Therefore, please read the Daily Brief for March 14, if you haven’t already, for a big discussion on bond and equity market volatility, as well as the odds of the market falling apart or rising, and positioning contexts that support that movement. If there are any incomplete statements below, we shall complete them in the coming letters. We’re laying it all out for awareness. Take care!

Fundamental

Headline inflation via CPI (Consumer Price Index) fell most on energy and core goods while shelter, food, and services inflation continues to be sticky. Core prices continue to be high, risking “inflationary psychology [] becoming ingrained,” Bloomberg’s John Authers explains.

“There’s nothing in this report to suggest that inflation is defeated already,” explained Authers. “Not to raise the fed funds rate next week, with median inflation above 7%, would be a sign of panic,” and an acknowledgment of uncertainties with regard to the banking system, as talked about in the Daily Brief on March 14.

To note, however, contagion appears contained, despite Moody’s Corporation (NYSE: MCO) cutting its outlook for the banking system to negative from stable, and placing lenders including First Republic Bank (NYSE: FRC) on a downgrade review.

JPMorgan Chase & Co’s (NYSE: JPM) Marko Kolanovic did cut his equity allocation warning that not all carry trades, something this letter has talked about numerous times before (i.e., borrow at a low rate and invest in something that provides higher return), can be bailed out. Kolanovic appears worried about commercial real estate, which Simplify Asset Management’s Michael Green just told your letter writer is in a bubble that “we’re seeing crack,” finally.

Graphic: Retrieved from Bloomberg. The Federal Reserve’s new Bank Term Funding Program or BTFP is “QE in another name – assets will grow on the Fed balance sheet which will increase reserves.” Recall that QE is the flow of capital into capital markets while QT is the opposite. Q is for quantitative while E is for easing and T is for tightening.

Anyways, following yesterday’s CPI, traders price higher odds of a 25 basis point hike which puts the terminal or peak fed funds rate at 4.75-5.00%. Following this spring, factoring potential inflation plateau and financial system uncertainties, traders foresee the Fed easing. By year-end, traders expect rates to fall down to 3.75-4.00%. Recall that at the beginning of last week, there were no expectations of easing in 2023. Also, traders thought the Fed would raise as high as 5.50-5.75%.

Mortgage rates, determined by changes in the price of mortgage-backed securities or MBSs, fell too.

ARK Invest’s Cathie Wood, who your letter writer had the honor of interviewing in person for Benzinga articles, thinks we’re on the cusp of the “roaring twenties” as inflation “is likely to surprise on the low side of expectations” with the banking crisis also leading to “bad deflation.”

“Today, five major innovation platforms are evolving at the same time – multiomics sequencing, robotics, energy storage, artificial intelligence, and blockchain technology, all of which are converging,” she elaborates.

“Once the Fed stops looking backward at CPI inflation and starts addressing the deflationary banking crisis that a 19-fold increase in short rates and an inverted yield have caused, we would not be surprised to see a return to the Roaring Twenties.”

Graphic: Retrieved from Bloomberg.

On the backward-looking measures quote in the above paragraph, former Fed trader Joseph Wang notes that the Fed and central banks, in general, are aware segments of the market may break, but that won’t discourage them from tightening further.

“As the BOE saved the gilt market through purchases and kept tightening, so the Fed can save banks and keep tightening.”

Positioning

Tuesday’s letter said that following important events like CPI, the compression of wound implied volatility or IVOL, coupled with the nearing large options expirations (OpEx), sets the market up for potential short bursts of strength into the end of the month and next month.

That’s along the lines of what is happening. The S&P 500 rose mechanically after the release of CPI yesterday. Later, though the index succumbed, internally speaking the market remained strong through end-of-day, hence some short bursts boosted by some short-dated options activities, also.

As explained, yesterday, the recent re-grossing theme appears intact. Any further compression of wound IVOL and the passage of options expirations (OpEx) could support equities as month-end approaches. Though it may be too early to position for strength, one may consider it the way it was explained in the Daily Brief on March 14.

Technical

As of 6:15 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a negatively skewed overnight inventory, inside of the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $3,904.25.

Key levels to the upside include $3,921.75, $3,945.00, and $3,970.75.

Key levels to the downside include $3,884.75, $3,868.25, and $3,847.25.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.