Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

Administrative

We will issue a content calendar revealing the dates letters are likely to be published and the content that may be covered.

Separately, due to the writer’s travel commitments, from 12/6 to 12/16 there will likely be little to no commentary. If any queries, or if you are local to New York City or Paris, ping renato@physikinvest.com or Renato Capelj#8625 on Discord.

Please check out the Daily Brief for November 29 and 30, as well as December 1.

On 11/29, we unpacked the context for a trade to take. On 11/30, we took that trade. On 12/1 we dissected the performance of that trade.

Given a time crunch, today’s letter will be lighter – really sorry!

Fundamental

Many headlines and increased alertness surround employment gauges, housing, and currency markets (e.g., yen sensitivity to U.S. Treasury yields; yen up and the dollar down after the Federal Reserve’s Jerome Powell suggested an easing in the pace of tightening). If interested, read Physik Invest’s letters on the yen and carry trades.

As an aside, an interesting quote comes from BlackRock Inc’s (NYSE: BLK) Gargi Chaudhuri, if yields were to hit “6.5% or 7%,” investors’ “fixed income will do so much of the hard work … that they don’t actually need as much of the equity exposure.” To add, however, the terminal rate sits around 5.2%.

Positioning

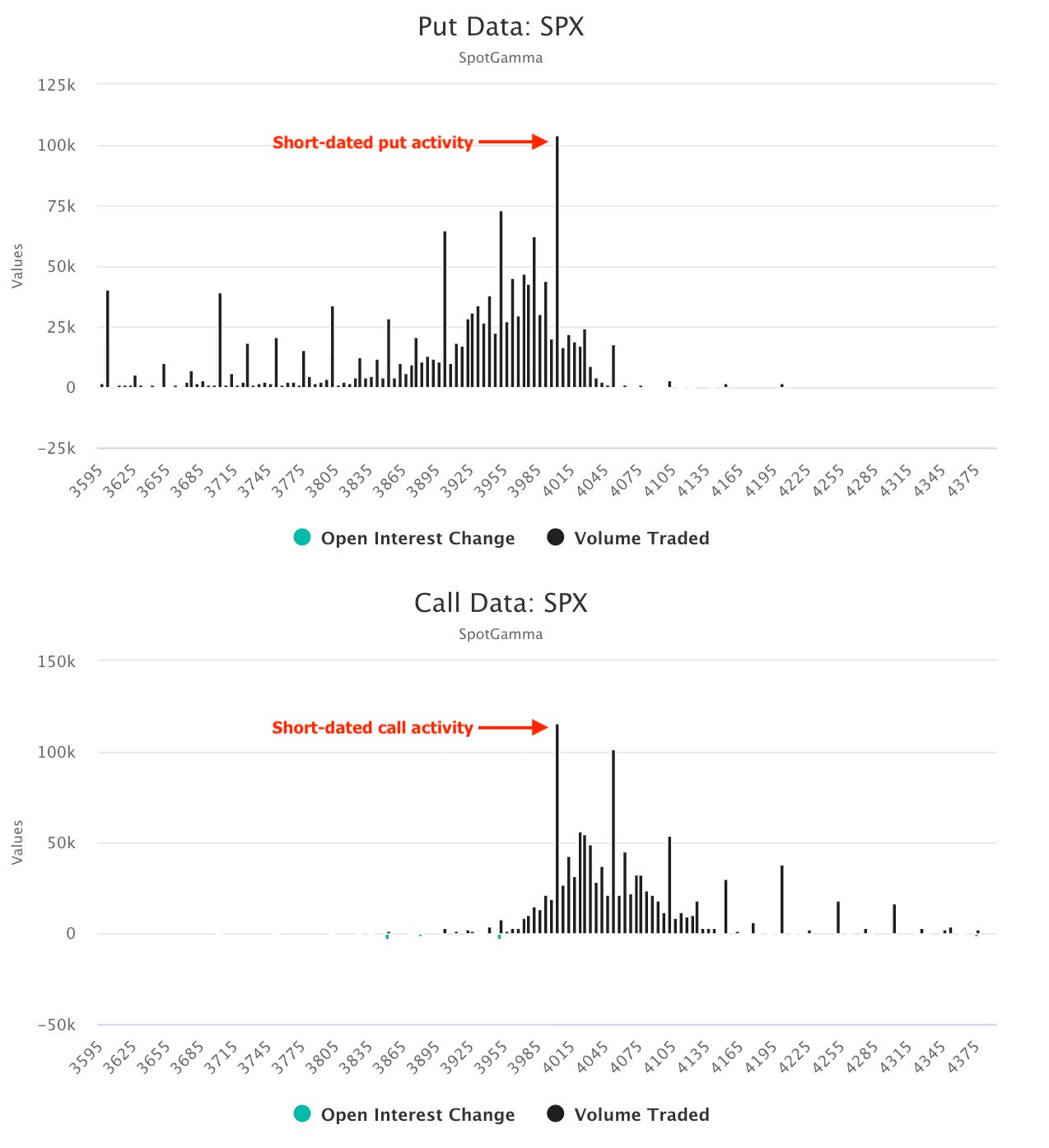

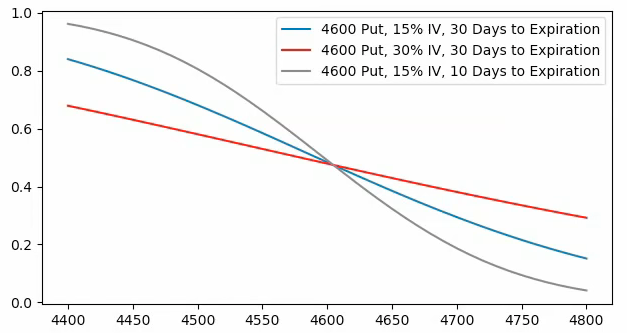

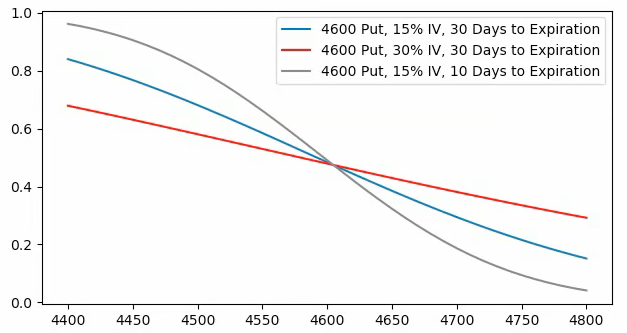

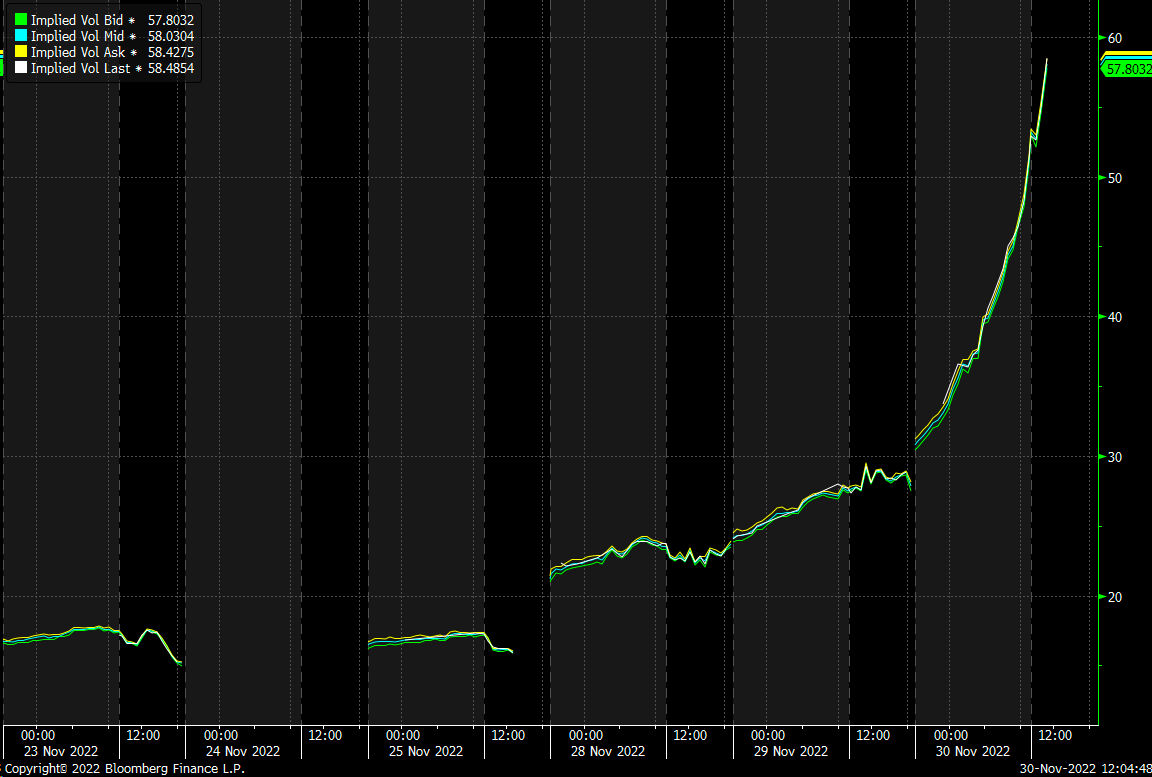

Per SpotGamma, recent action has been “dominated by very short-dated options”; on November 30, implied volatility (IVOL) measures for the same day’s expiry rose, pointing to demand for protection across options with the least time to expiry.

These options are highly sensitive and, if traded in a large enough size, can impact markets markedly (e.g., provide a big boost to bullish-type macro repositioning when the IVOL of soon-to-expire options finally compresses).

That said, a trend is intact.

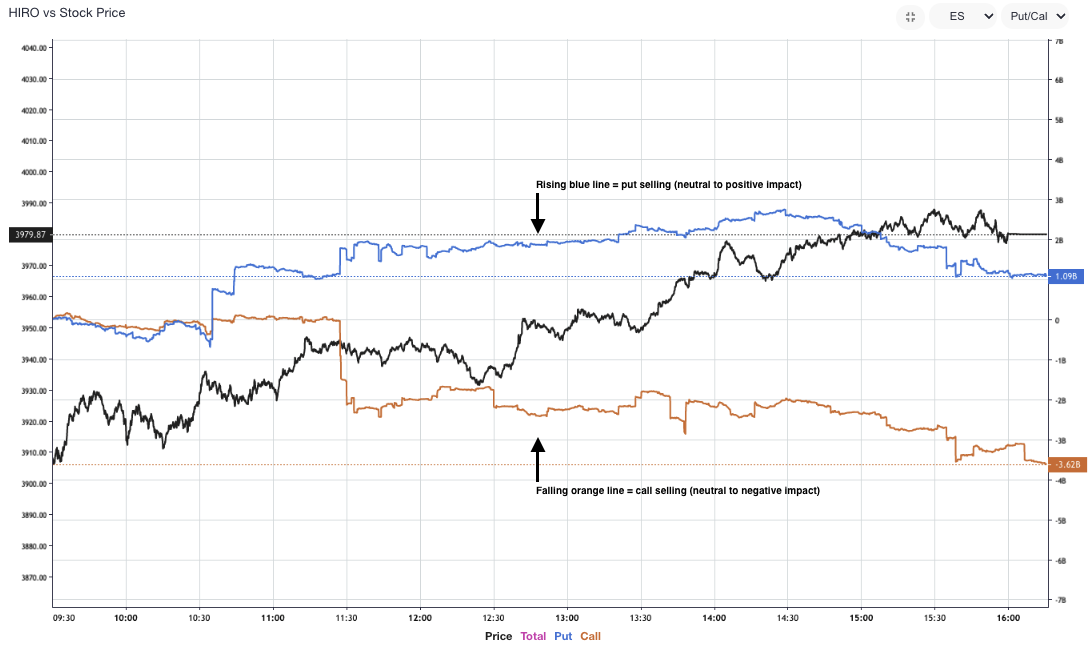

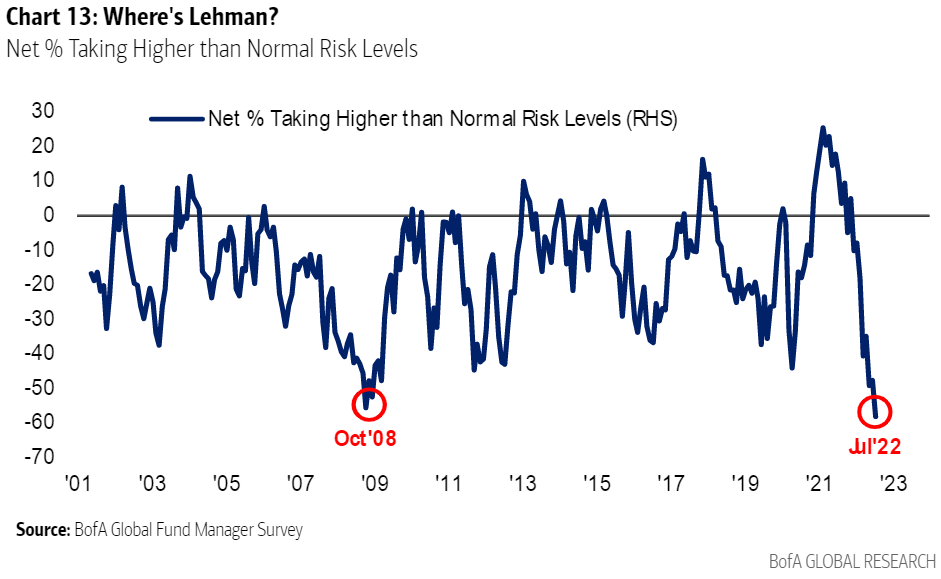

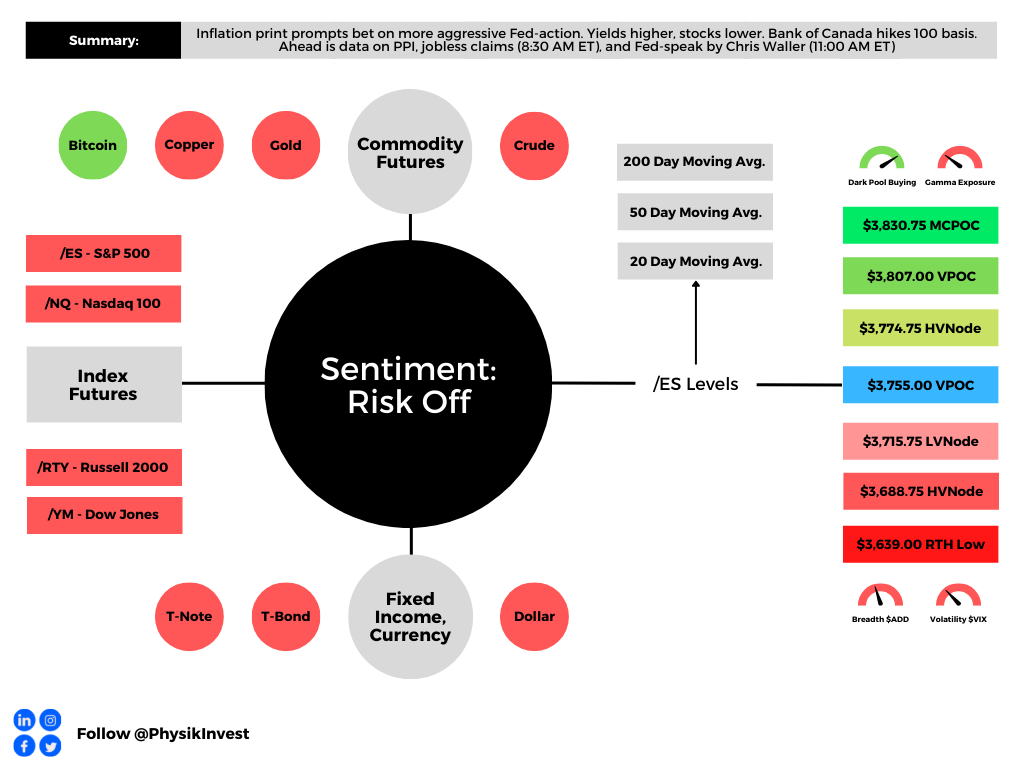

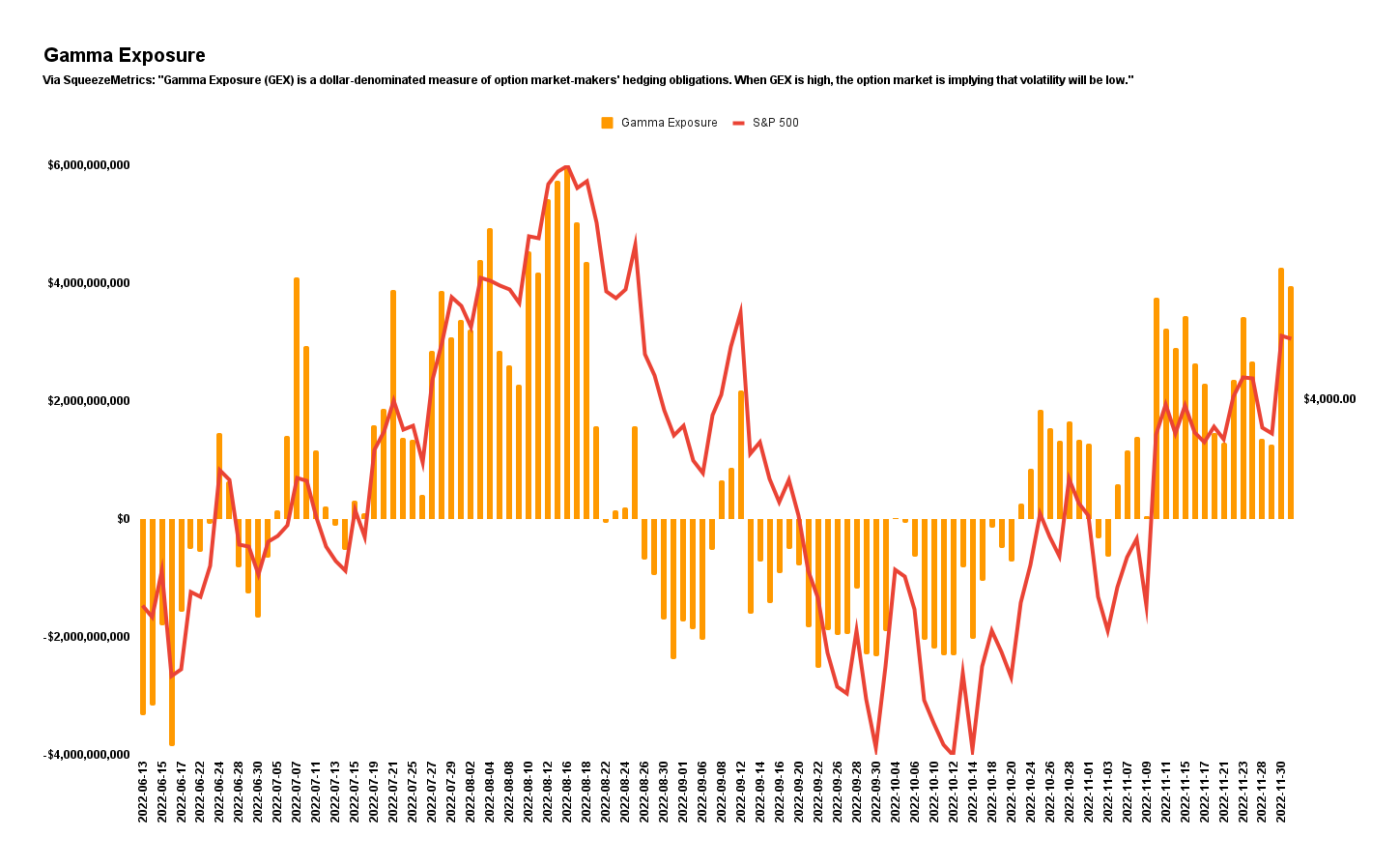

Traders’ fears continue to be assuaged, as evidenced by a general “supply of call options,” per SpotGamma, and further “implied volatility compression”; investors’ counterparts (i.e., liquidity providers) are recipient to increased positive exposure to movement (i.e., +Gamma), as evidenced by the below graphic. If movement is beneficial, and the counterparty is not interested in realizing that benefit, it may hedge in a manner that can eat away at realized volatility (RVOL), resulting in tighter ranges. SpotGamma adds that “barring big changes in positioning into 12/14 FOMC and 12/16 OPEX,” expected is more of the same (i.e., sideways to higher).

Technical

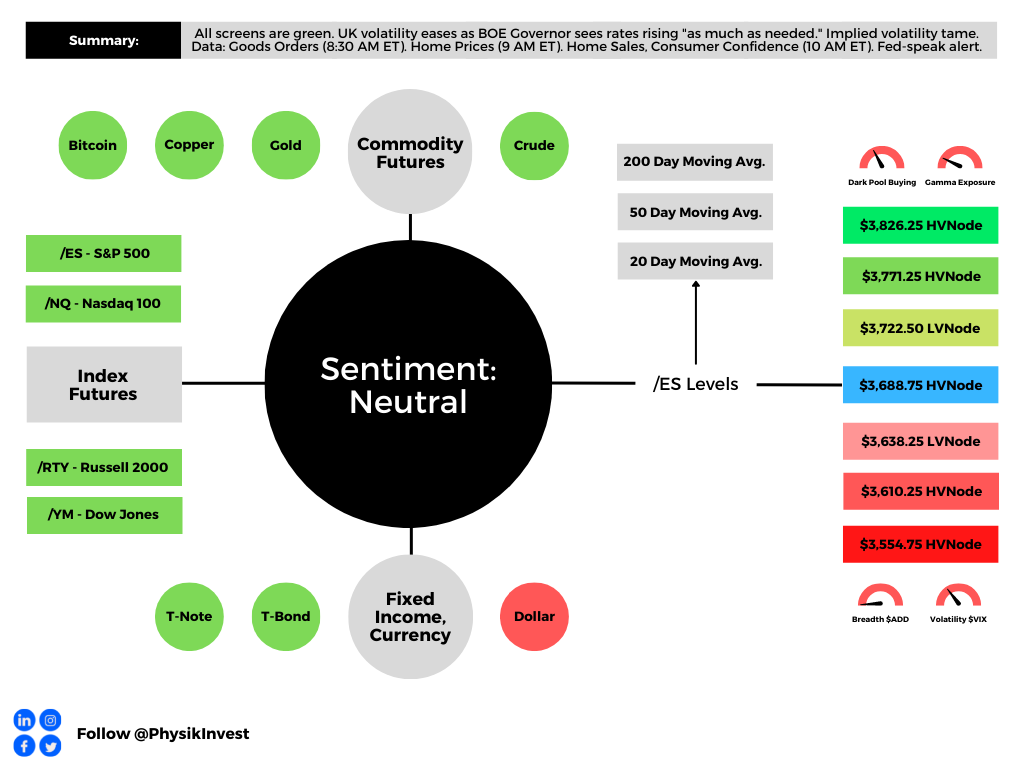

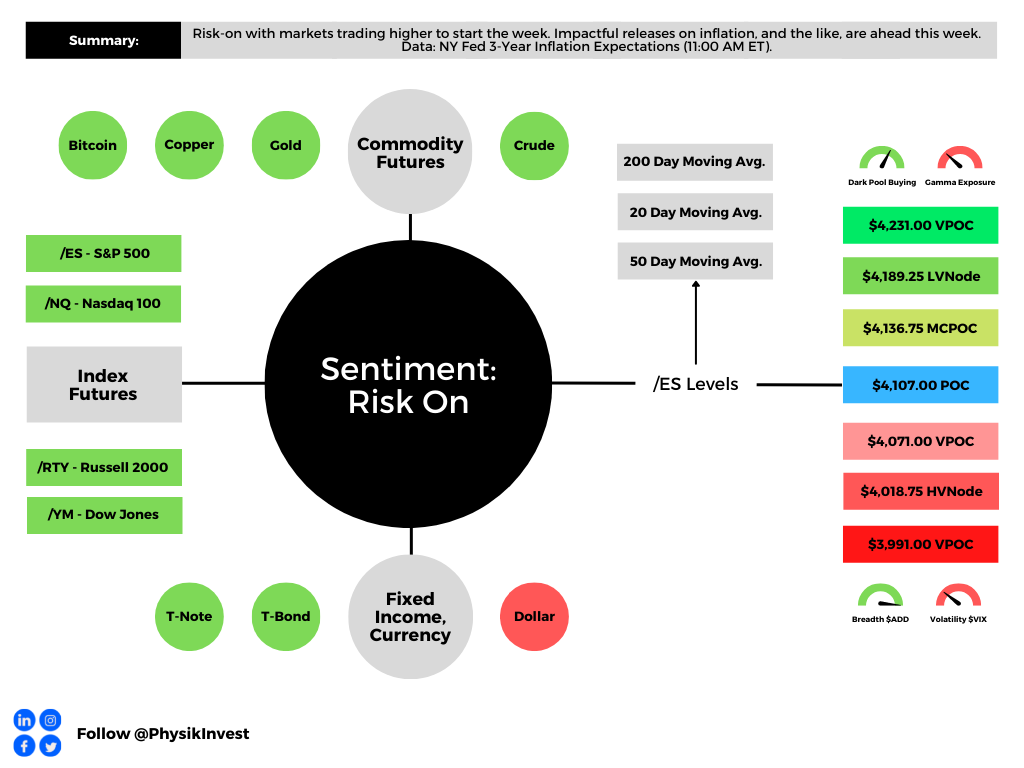

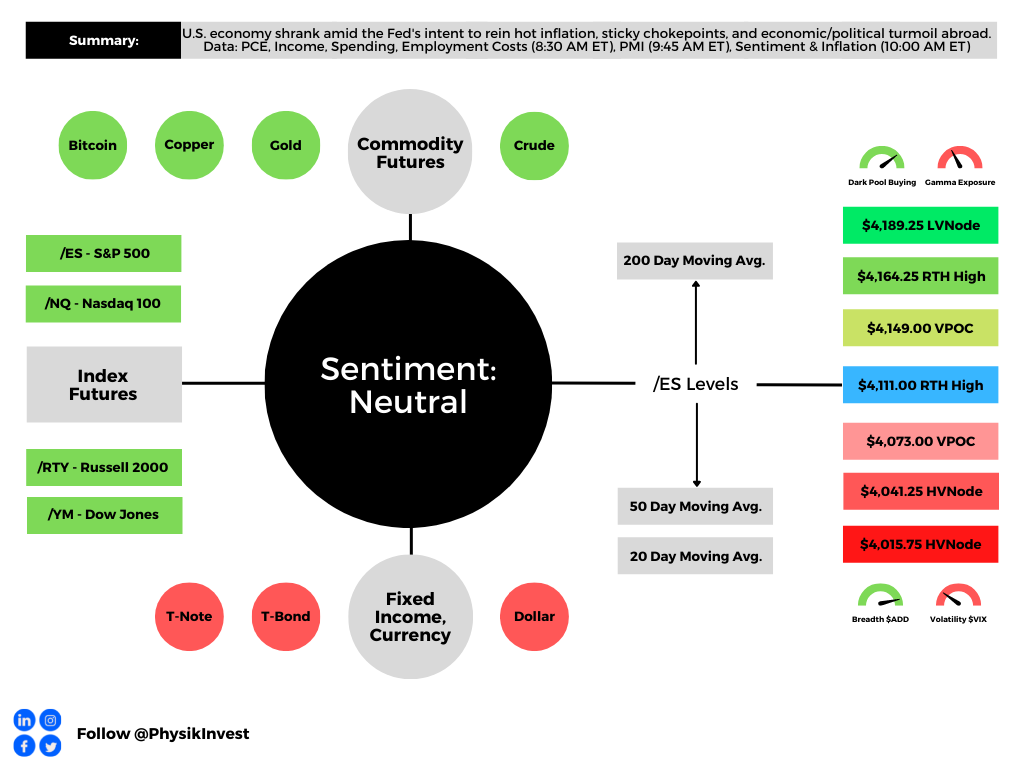

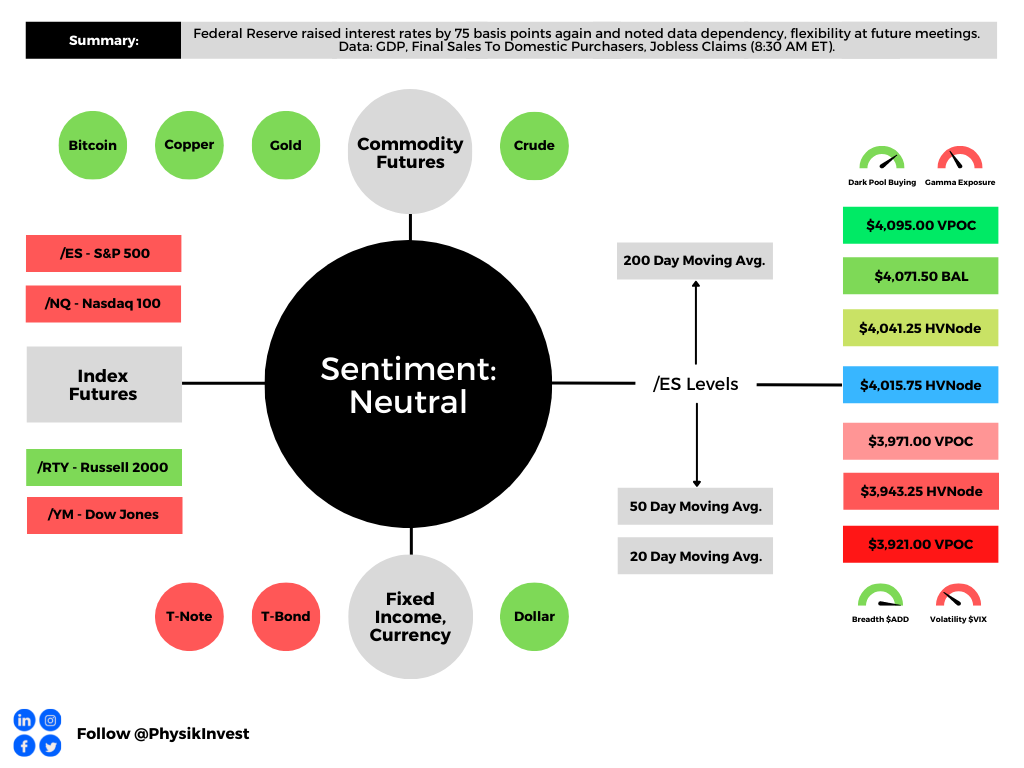

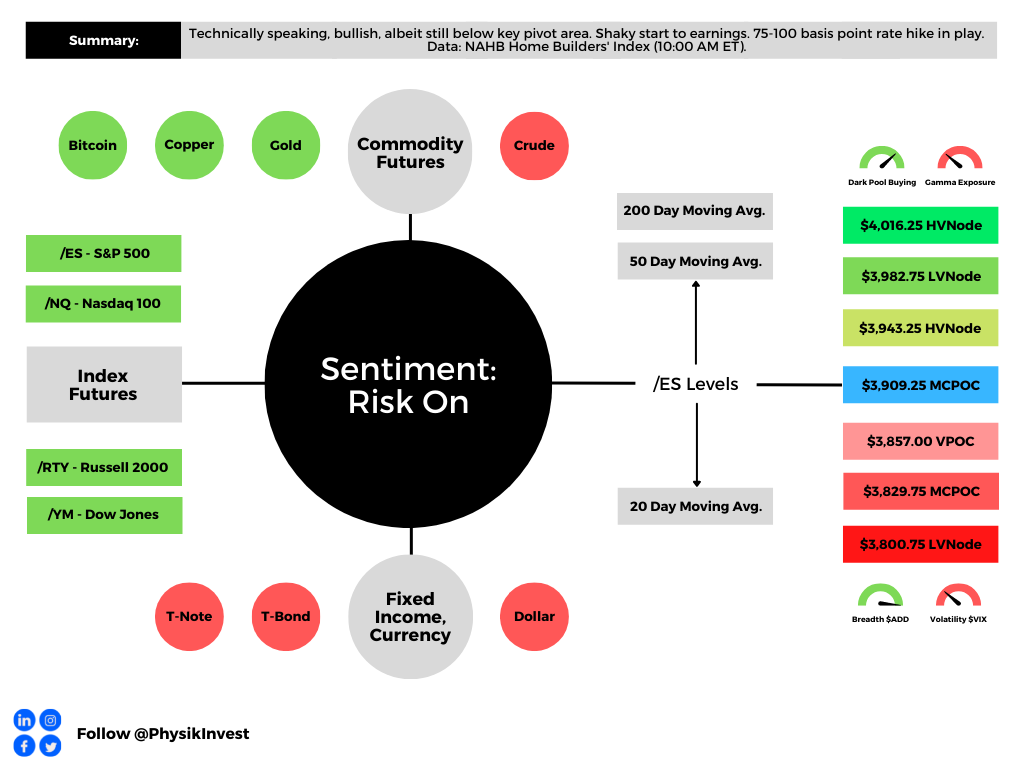

As of 7:45 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

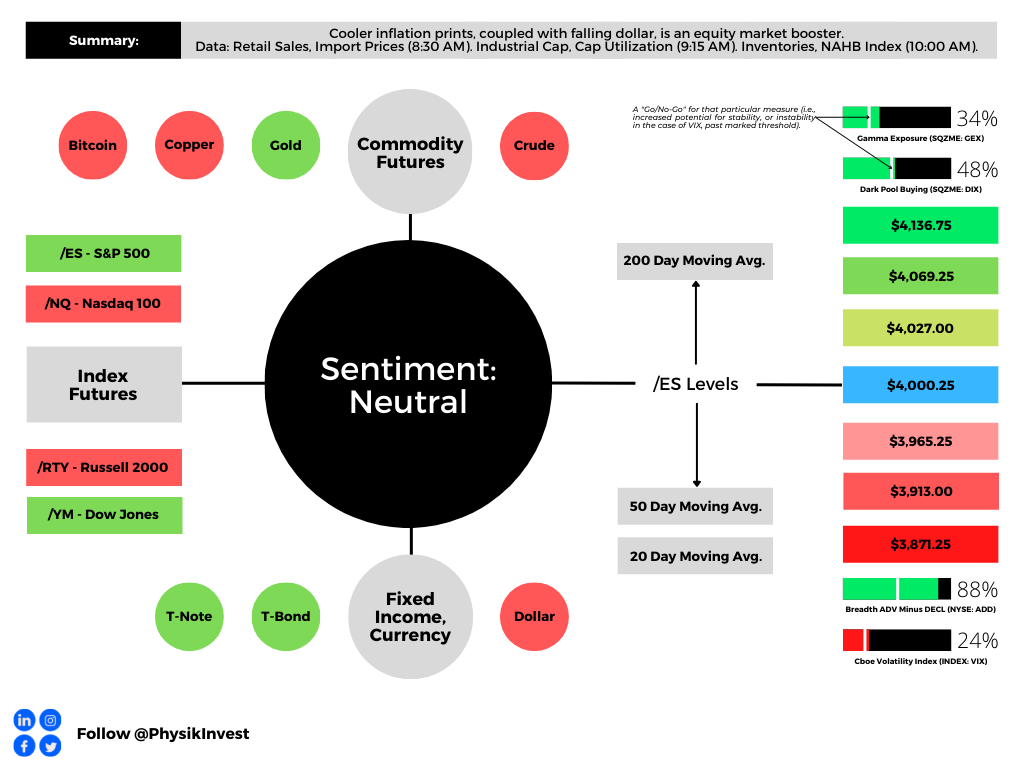

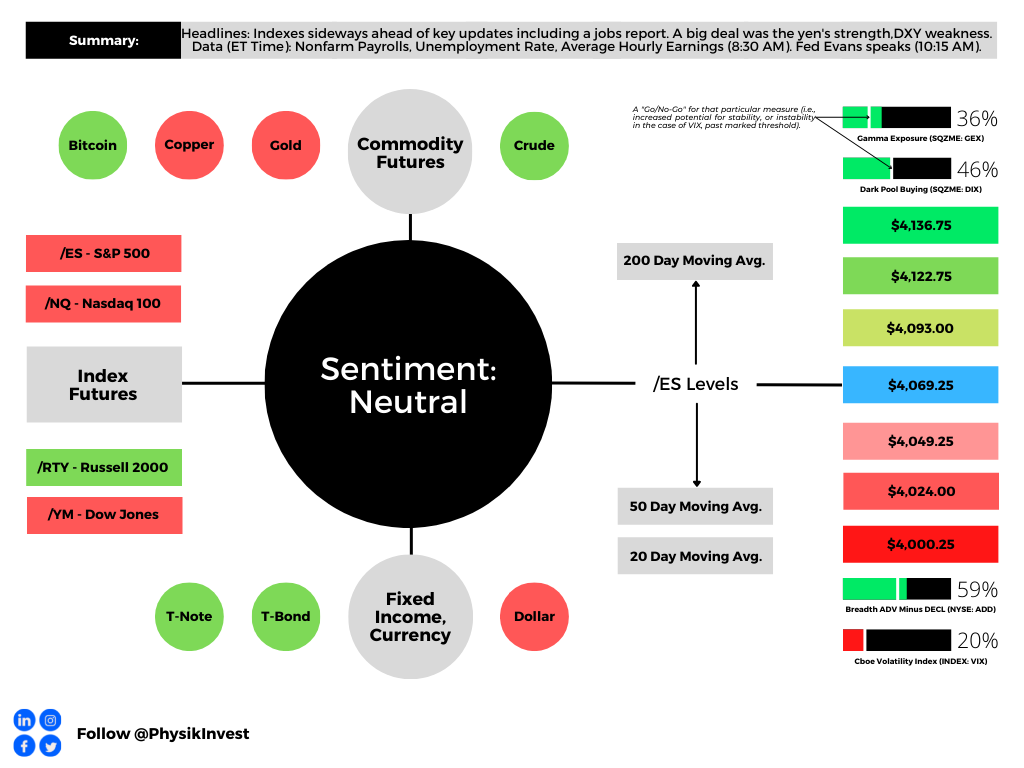

Our S&P 500 pivot for today is $4,069.25.

Key levels to the upside include $4,093.00, $4,122.75, and $4,136.75.

Key levels to the downside include $4,049.25, $4,024.00, and $4,000.25.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: Denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

In short, an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.