Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

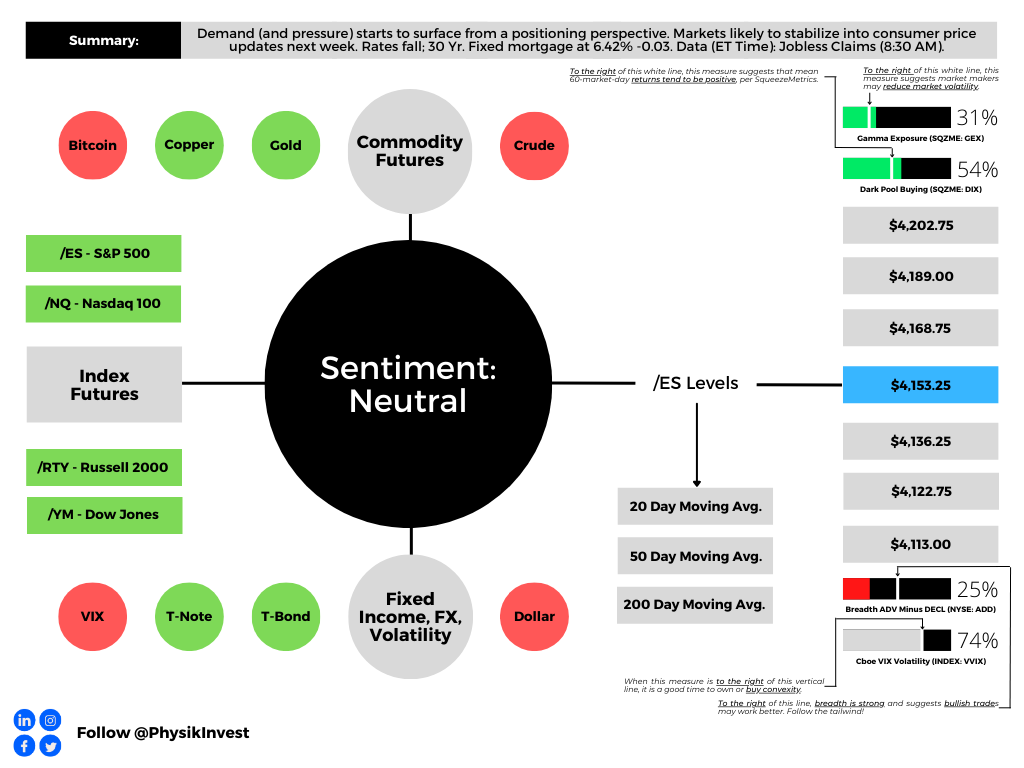

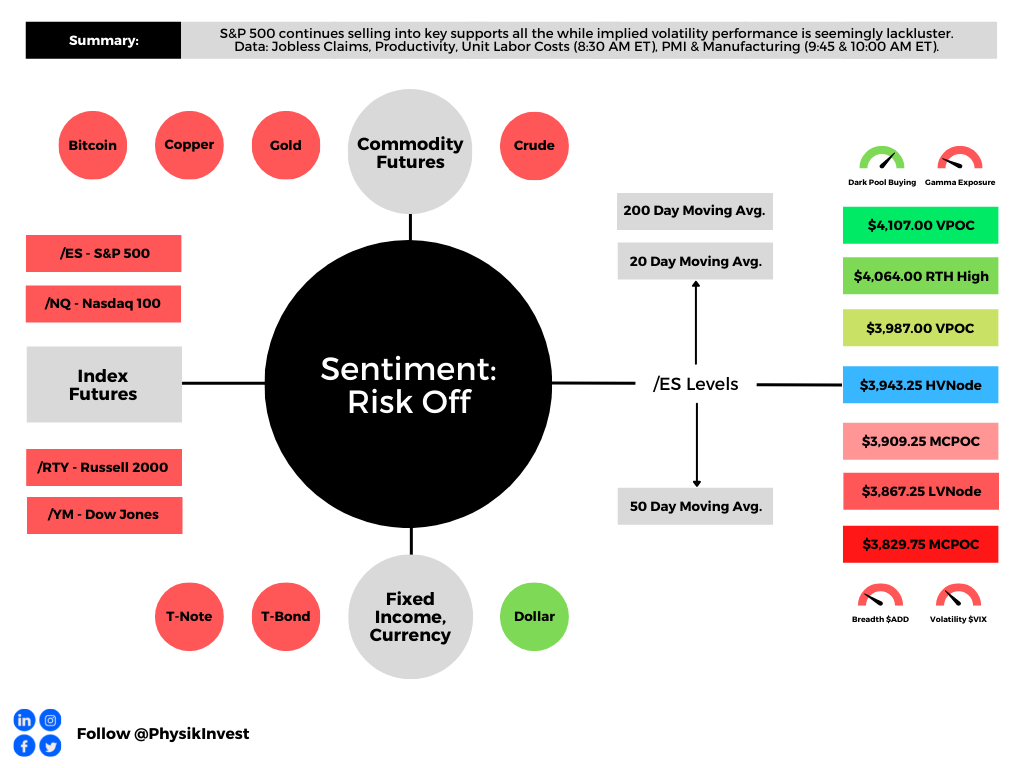

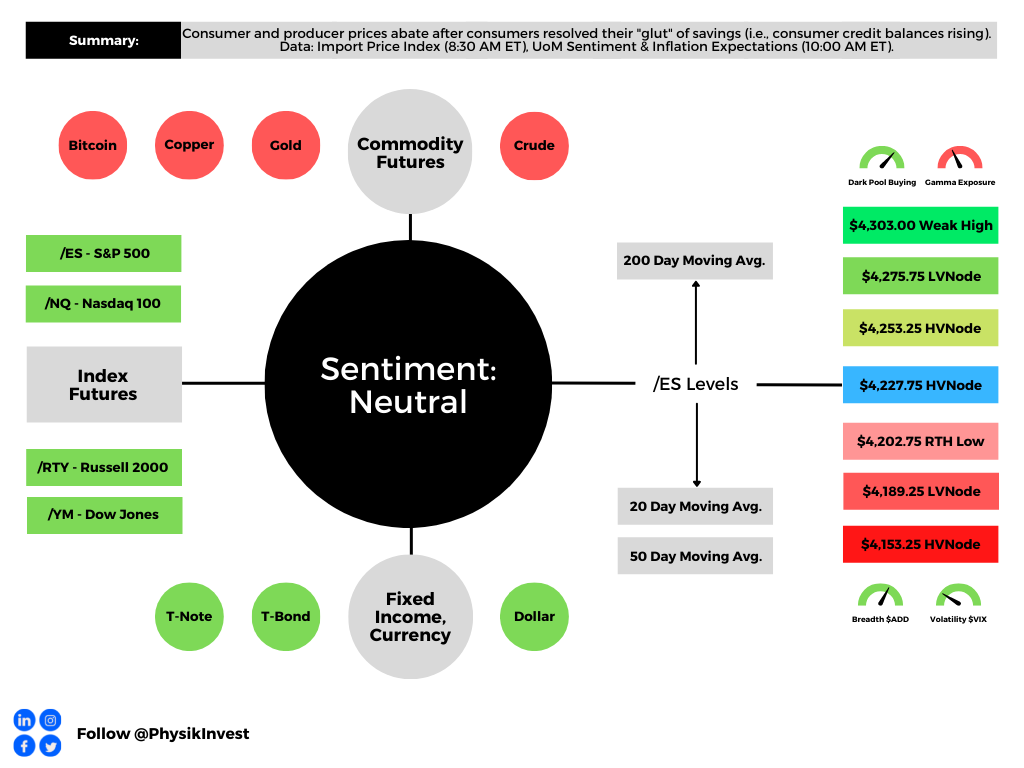

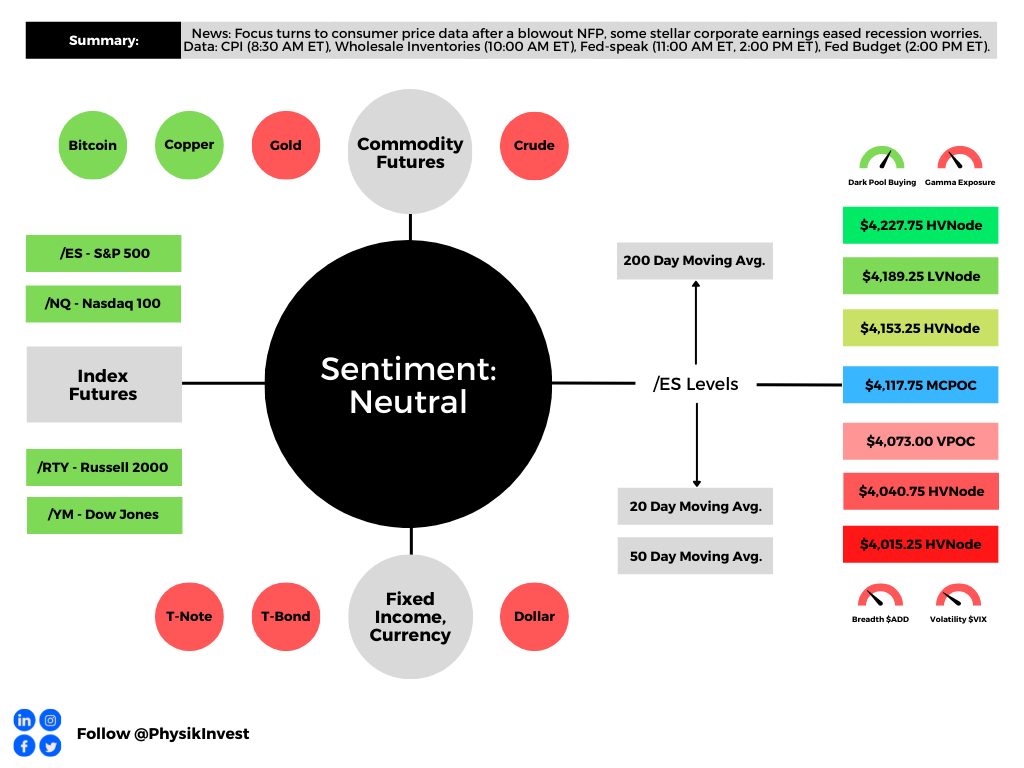

Graphic updated 7:20 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility.

Positioning

The cross-cutting forces on inflation are set to net out says Bob Elliott, the CIO at Unlimited. The former Bridgewater Associates executive thinks short-term inflation pressures are skewed upward, and that new data suggests “the respite in inflation … is probably going to fade and higher numbers are going to print.”

In short, disinflation from oil prices and the amelioration of supply chains “cannot persist, and that’s what we’re seeing now. It looks like those upward pressures on inflation are moving faster than the pace that services prices and housing costs are moving down.”

Consequently, there is a potential for broad inflation measures to remain higher for longer, hence the thinking that the Federal Reserve (Fed) indeed stays tougher on inflation for longer (i.e., higher rates for longer). This would support traders’ recent desire to bet large on downside movement next week when the Consumer Price Index (CPI) is set to update.

Publicized by Kai Volatility’s Cem Karsan and Damped Spring’s Andy Constan, some trader(s) bought to open 24,000 put options at the $4,050.00 S&P 500 (FUTURE: /ES) strike expiring February 17, 2023. The trade coincided with market makers selling to open “roughly 7,200 [/ES] futures contracts worth roughly $1.5 billion.” This “caused the local low,” Constan, who also worked at Bridgewater (and your letter writer had the honor of interviewing before), explained.

This trade, and others like it, compounded the pressures of the dealers selling their existing stock and futures “to re-hedge their call options exposures that are declining in value.”

Graphic: Retrieved from SqueezeMetrics.

Accordingly, the Cboe Volatility Index (INDEX: VIX) is bid, as is the Cboe VIX Volatility Index (INDEX: VVIX), which your letter writer talked about in a SpotGamma note last night. Basically, traders are hedging more, and this is observed by previously low readings of convexity moving higher. Still, given that there is still some time to CPI, there’s potential for “current prices the SPX trades at [to] appear sticky for lack of better phrasing,” SpotGamma explained; pre-CPI, traders often sell short-term volatility as a bet on limited movement. It’s the post-CPI expirations in which implied volatility (IVOL) is wound and will serve as a catalyst for a fast move higher or lower.

Graphic: Retrieved from TradingView. Blue = VVIX. Orange = VIX.

So, in the short-term, there may be some pinning, followed by an expansion of range into the mid-February (2/17) monthly options expiration (OpEx). This event likely puts the market in a precarious position and at the whims of macro-type repositioning, which may be bearish based on the insights this letter has covered in the past.

Graphic: Retrieved from Physik Invest. Data from SqueezeMetrics. Gamma exposure is set to fall in mid-February, and this may result in less support from the options market.

Trades that look and are working well include those that use short-call vertical credits to finance long-put vertical debits out months from now. For instance, for every two units of short call verticals (SOLD -1 VERTICAL SPX 100 19 MAY 23 [AM] 4150/4200 CALL), your letter writer is looking to own one unit of the long put vertical (BUY +1 VERTICAL SPX 100 16 JUN 23 [AM] 3450/3350 PUT). Remember that your letter writer may not necessarily think the market will trade that far, rather it may be a bet on IVOL repricing.

A case study on last week’s ultra-successful call ratio spreads is coming soon. Take care and watch your risk!

Technical

As of 7:20 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, inside of the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $4,168.75.

Key levels to the upside include $4,189.00, $4,202.75, and $4,214.25.

Key levels to the downside include $4,153.25, $4,136.25, and $4,122.75.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

About

The author, Renato Leonard Capelj, works in finance and journalism.

Capelj spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market. Separately, Capelj is an options analyst at SpotGamma and an accredited journalist.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 970+ that read this report daily, below!

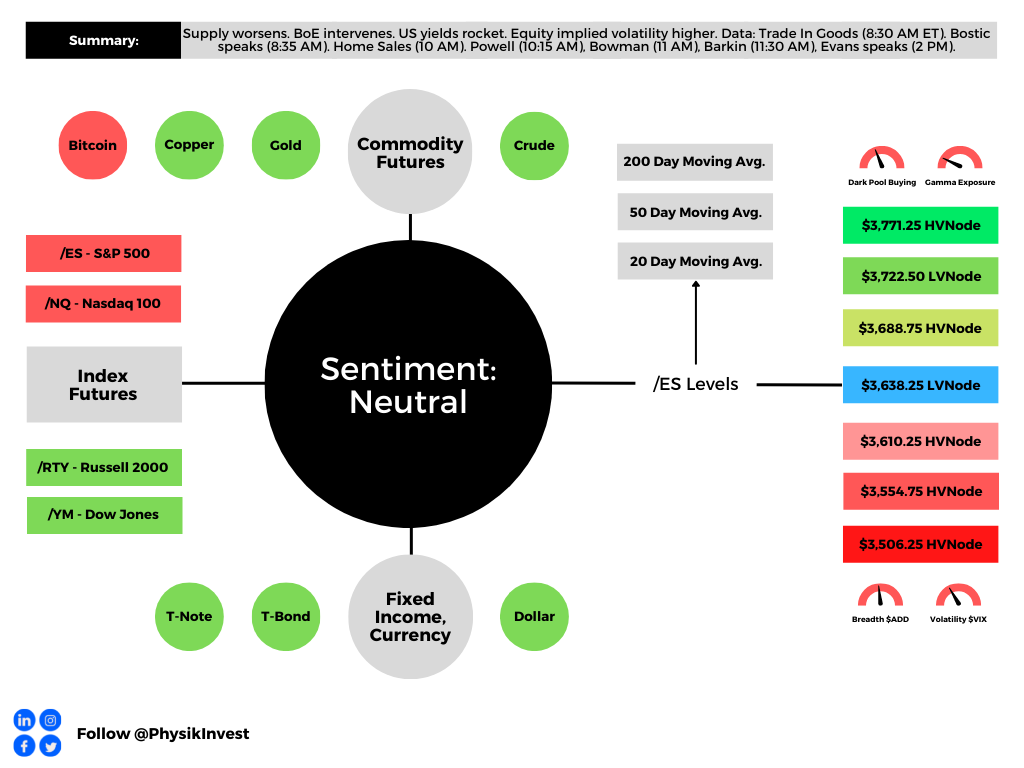

Graphic updated 8:20 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Administrative

Apologies, team, if the quality was lacking these past few days. Extremely busy on my end and I look forward to some detailed letters in the near future! – Renato

Fundamental

“Great powers are waging hot wars involving the flow of technologies, goods, and commodities.”

That’s according to Credit Suisse Group AG’s (NYSE: CS) Zoltan Pozsar who believes that the pillars forming the context for a low-inflation world are changing, and this is setting the stage for longer-lasting structural inflation.

In short, inflationary impulses are incoming from non-linear geopolitical and economic conflicts.

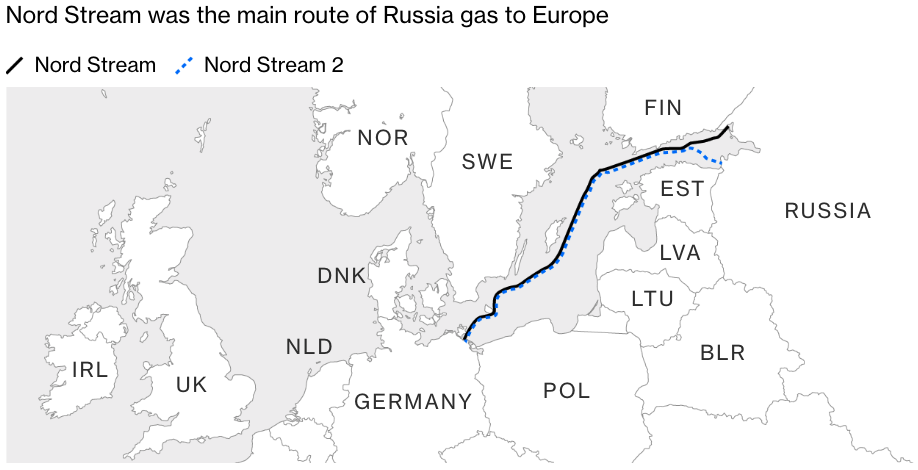

Just yesterday, Europe was investigating attacks on pipelines from Russia; there were “major leaks into the Baltic Sea from two Russian gas pipelines at the cent[er] of an energy standoff.”

“The word sabotage springs to mind,” Javier Blas of Bloomberg, said. “In a single day, the conduits, which link Russia with Germany under the Baltic Sea, have suffered not one, not two, but three separate major leaks.”

Per reports by Refinitiv, seismologists nearby registered “powerful blasts” that “do not resemble signals from earthquakes.” Instead, the explosions likely correspond with hundreds of “kilos (kg) of dynamite.”

Given that Nordstream 1 and 2 are not operational, now, the “leaks are more likely a message: [if truly the culprit], Russia is opening a new front on its energy war against Europe.”

Accordingly, gas prices were higher but “below this year’s peaks,” Refinitiv reported. Generally, across some benchmarks, prices read “more than 200%, higher than in early September 2021.”

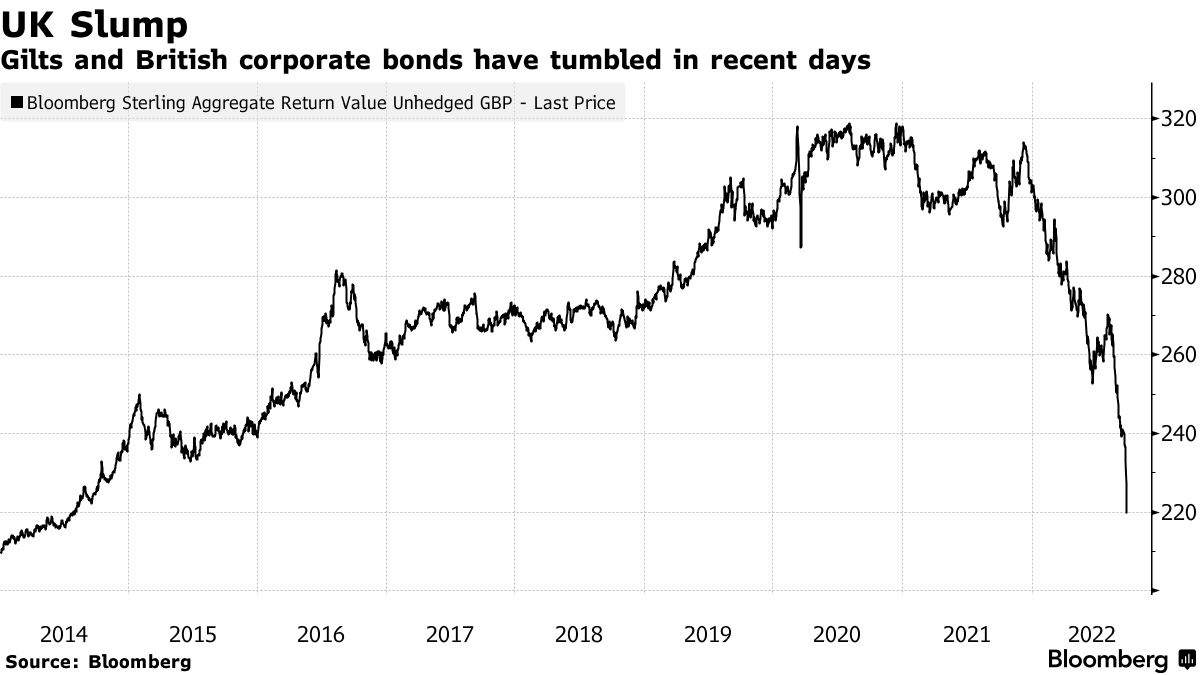

Separately, the Bank of England (BoE) is delaying quantitative-tightening (QT) bond sales and opting to purchase longer-dated government bonds in an attempt to restore stability, which we discussed was at risk on Monday and Tuesday.

Graphic: Retrieved from Bloomberg. Credit Default Swaps (CDSs) are a tool for investors to offload credit risk to other market participants.

As a result, after a near-vertical drop (visible below) in Gilts and British corporate bonds (which impacted mortgage lending, for one), UK yields saw some of their biggest drops on record.

Graphic: Retrieved from Bloomberg. Updated September 26, 2022.

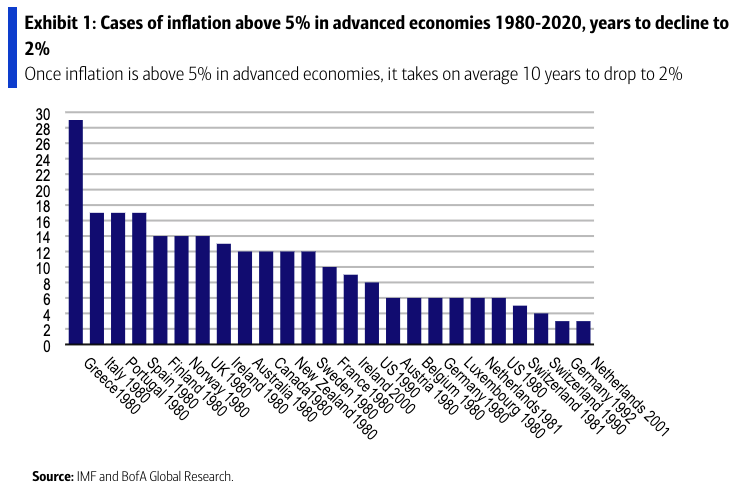

The actions over the past few days complicate the Monetary Policy Committee’s (MPC) objective to reach a return to 2% inflation in the medium term.

Graphic: Retrieved, initially, from Bank of America Corporation (NYSE: BAC). Via The Transcript. Interest rates “may be higher for longer” than expected.

At home, here, in the US, yields on the 10-year topped 4.00%. There is a heightened chance of a Federal Reserve (Fed) bump in rates that brings the target rate to 375-400 basis points, while the UK, in stemming its inflationary pressures, is expected to bump by double that amount.

The action to stem inflation is feeding through to demand. Apple Inc (NASDAQ: AAPL) said it would ease plans to boost iPhone production “after an anticipated surge in demand failed to materialize,” a Bloomberg report said.

“The supply constraints pulling down on the market since last year have eased and the industry has shifted to a demand-constrained market,” said Nabila Popal, research director at IDC.

“High inventory in channels and low demand with no signs of immediate recovery has OEMs panicking and cutting their orders drastically for 2022,” a fear we said ARK Invest’s Catherine Wood shared, not too long ago.

Positioning

The beginning of the week was characterized by a sideways-to-lower S&P 500 (INDEX: SPX) and implied volatility (IVOL) metrics, such as the Cboe Volatility Index (INDEX: VIX), rising.

Per IVOL the term structure, demand for options protections seems to be concentrated in options that are shorter-dated and far more sensitive to changes in direction and volatility.

That means for large shifts in price and/or volatility, hedging ratios (e.g., Delta) shift markedly, too. This prompts “hedging feedback mechanisms in both market directions,” per SpotGamma.

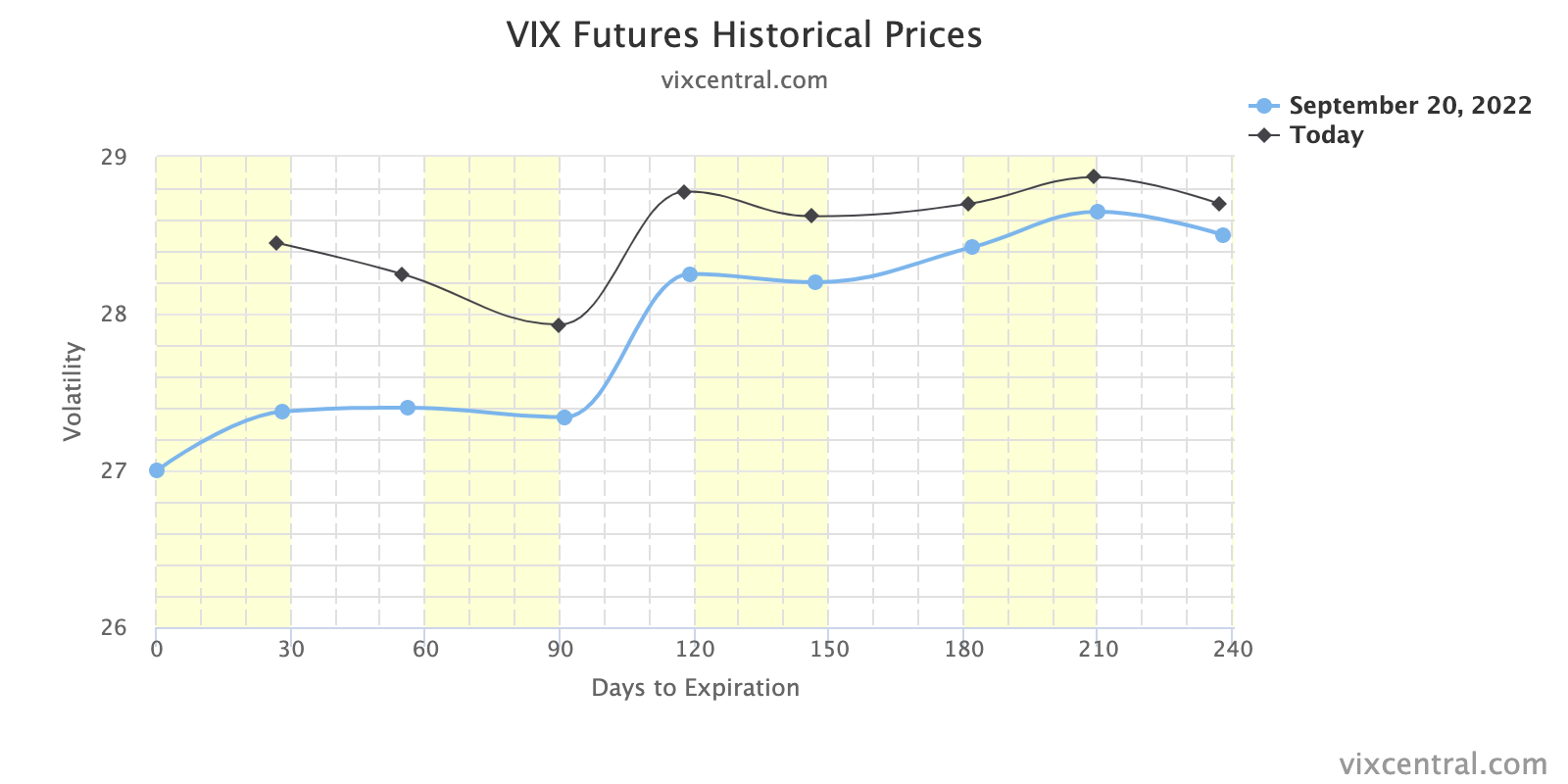

Graphic: Retrieved from VIX Central. Taken from The Market Ear. Updated 9/27/2022.

Moreover, the risks are skewed to the upside, SpotGamma added.

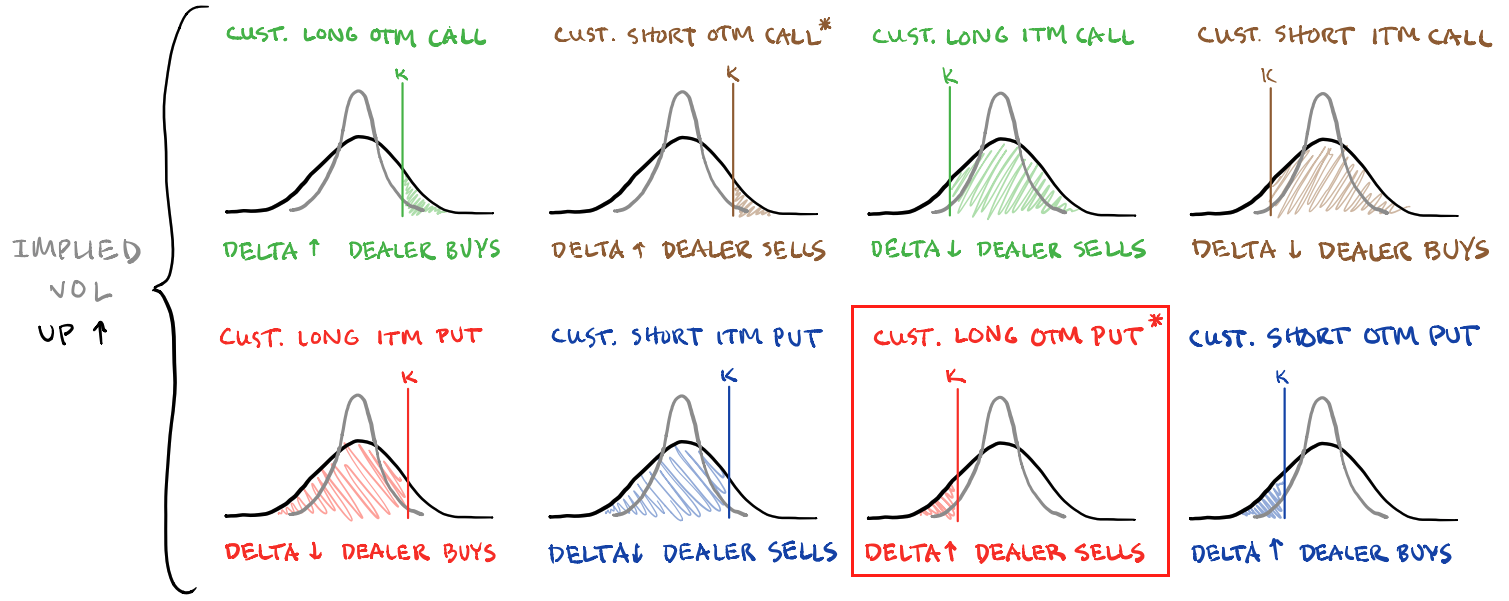

“For pumped-up options far from the money to retain their value, there essentially needs to be an adverse move (in price and volatility). Should nothing bad happen, the probability of these options paying out will fade, as will their exposure to direction (or Delta). [In] re-hedg[ing] decreased exposure to Delta, liquidity providers [] may provide the market with a boost.”

Graphic: Retrieved from SpotGamma. SPX prices X-axis. Option delta Y-axis. When the factors of implied volatility (Vanna) and time change (Charm), hedging ratios change. The graphic is for illustrational purposes, only.

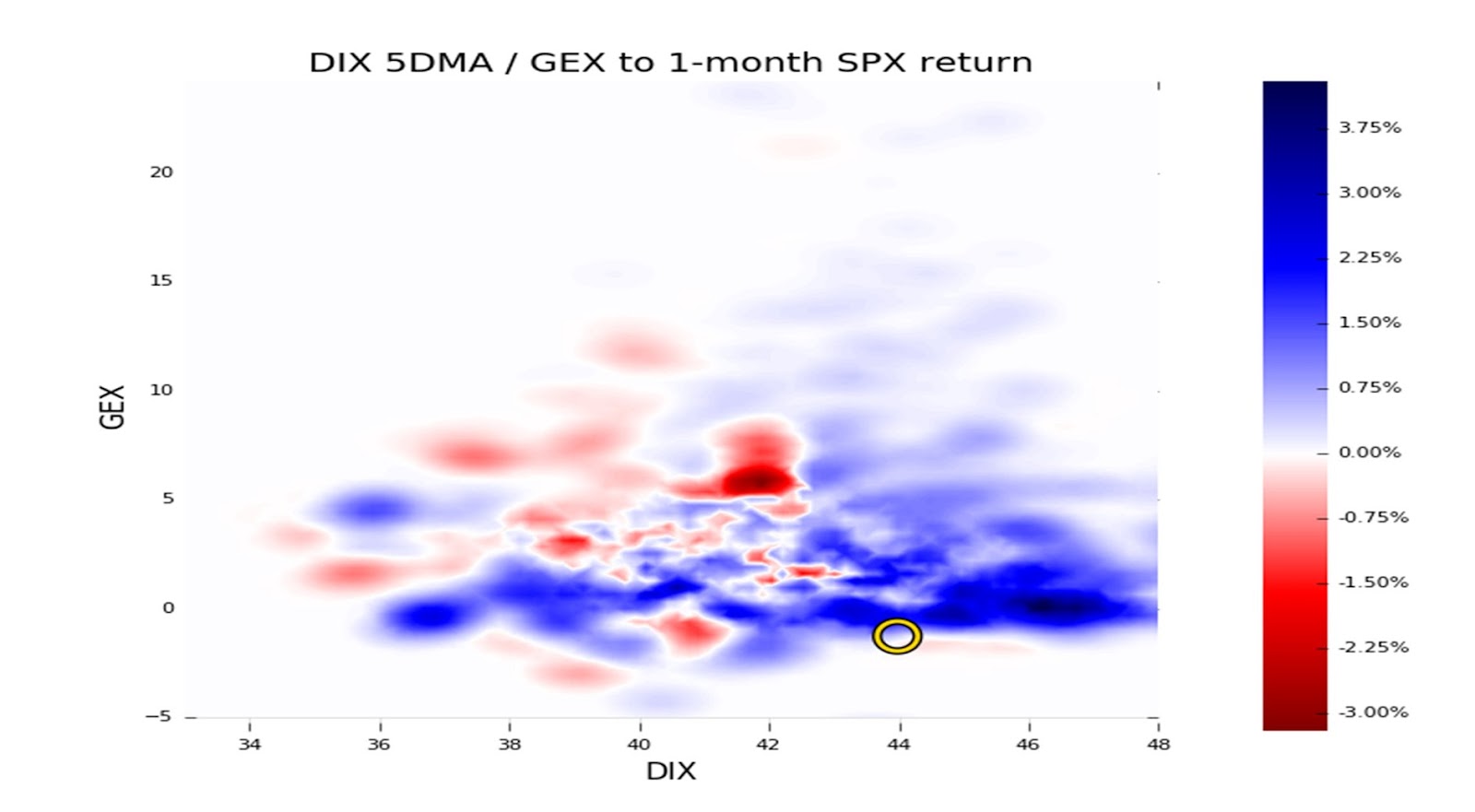

At the same time, there appears to be some “dealer disintermediation” amid “less incentive to make deep, tight markets” due to “capital constraints,” potentially, explained SqueezeMetrics, the creator of the DIX (Dark Pool Index).

This comes after months of high average readings in DIX (likely as market-makers assembled “basket[s] of S&P 500 stocks to create ETF shares, or to hedge away the exposure of a futures contract[s]”). Typically, high DIX readings are associated with stronger 1-month market returns, particularly when put flows are strong (i.e., lower Gamma exposure readings, like now).

Overall, the trend change is “suggestive of some second thoughts from the [buy-the-dip] crowd, and perhaps (likely!) some deleveraging from elsewhere,” SqueezeMetrics ended.

Technical

As of 8:20 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,638.25 LVNode puts into play the $3,688.75 HVNode. Initiative trade beyond the HVNode could reach as high as the $3,722.50 LVNode and $3,771.25 HVnode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,638.25 LVNode puts into play the $3,610.75 HVNode. Initiative trade beyond the HVNode could reach as low as the $3,554.75 and $3,506.25 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 950+ that read this report daily, below!

Graphic updated 8:00 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Administrative

An easy read, today. For more complex, see the September 20 and 19 letters. Also, there will not be a letter published for Friday, September 23, 2022. See you next week, team!

Fundamental

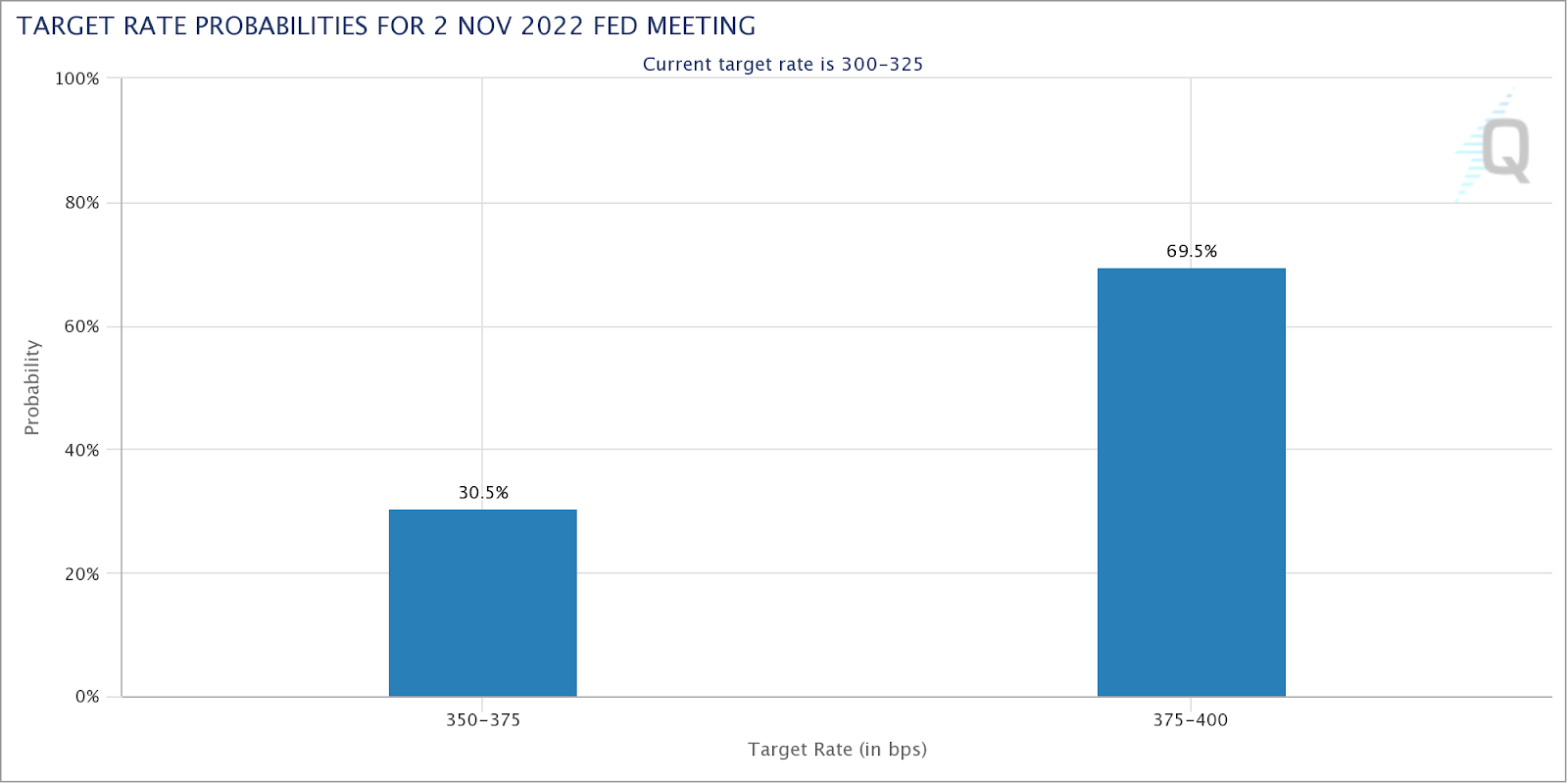

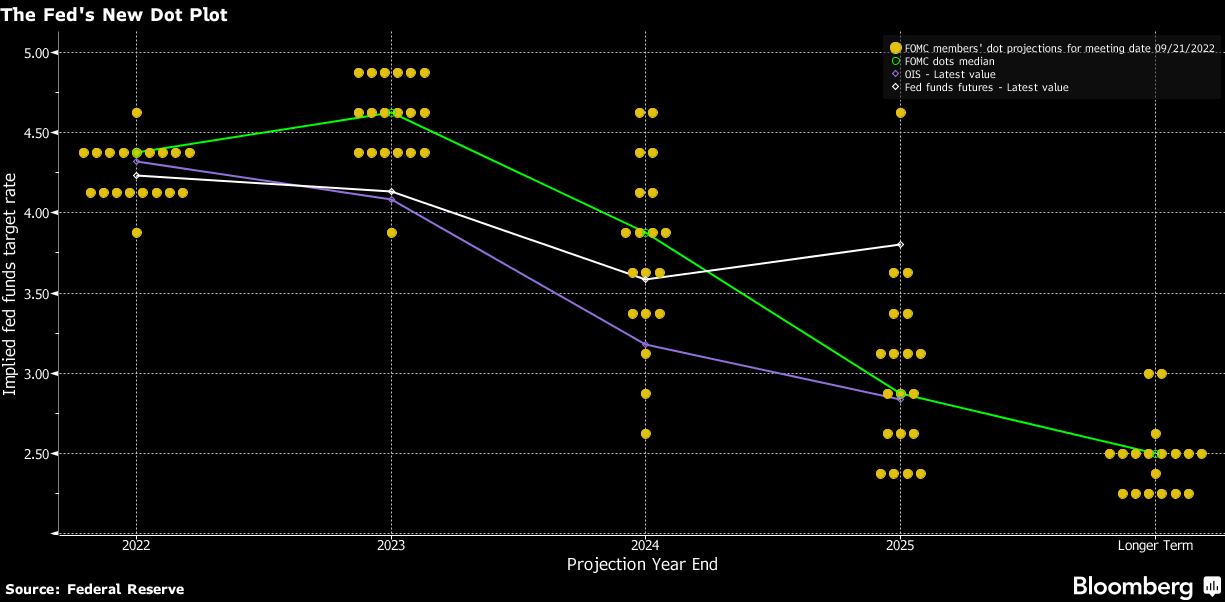

Equity markets traded down, yesterday, on the heels of the Federal Reserve’s (Fed) decision to raise interest rates by 0.75% and “keep at it” for longer, eyeing a 1.25% jump, in sum, by 2023.

This puts the current target rate at 3.00-3.25%.

Separately, if the “keep at it” quote sounds familiar, that’s because it is. The Fed Paul Volcker’s memoir is titled “Keeping at It.”

Graphic: CME Group Inc’s (NASDAQ: CME) FedWatch Tool shows higher odds of a 75 to 100 basis point rate hike in November, along the lines of what the futures market was pricing heading into the event.

The Fed Chair Jerome Powell admitted there may be below-trend growth and the potential for unemployment to reach 4.4% next year, up from the current rate of 3.7%. Projected increases, as of yesterday, show interest rates at 4.4% by 2023, and 4.6% in 2023, before moderation in 2024 to 3.9%, as well summarized by Bloomberg.

Moreover, economists suggest that raising rates to 4.5% would cost the economy nearly 1.7 million jobs while rates at 5% would bring that number to 2 million. A higher savings rate and increased funds at the state level would likely cushion the blow, however.

In response, the likes of Ark Invest’s Cathie Wood, who we quoted recently regarding her thoughts on why the Fed needs to lower the pace of tightening and/or cut, said:

“Most disappointing about the Fed’s decision today was its unanimity. None of those voting on the Federal Reserve is focused on the significant price deflation in the pipeline. The Fed seems to be making decisions based on lagging indicators and analogies.”

She adds that the Fed is setting the stage for deflation:

“The Fed is solving supply chain issues by crushing demand and, in my view, unleashing deflation, setting it up for a major pivot.”

Graphic: Initially retrieved from Bloomberg. Taken from Ophir Gottlieb who concludes costs are dropping, as observed via shipping, gasoline, manufacturing, cars, and rent measures.

Moreover, it’s the case that “[a]s rates rise and debt servicing costs increase, ‘many zombie institutions, zombie households, corporates, banks, shadow banks, and zombie countries are going to die,’” said economist Nouriel Roubini, who predicted the 2008 financial crisis.

Prior to the Fed event, Roubini forecasted a 75 basis point hike in September, followed by a 50 basis point hike in November. The market is pricing more than what Roubini thought the Fed would probably do after Wednesday’s Fed meeting.

In his opinion, stay “light on equities and have more cash, … [as] equities and other assets can fall by 10%, 20%, 30%.”

Positioning

In short, unexpected was the post-event response. In recent times, post-Fed moves have been positive, driven by the “rebalancing of dealer inventory,” per Kai Volatility’s Cem Karsan.

That didn’t happen and let’s unpack why.

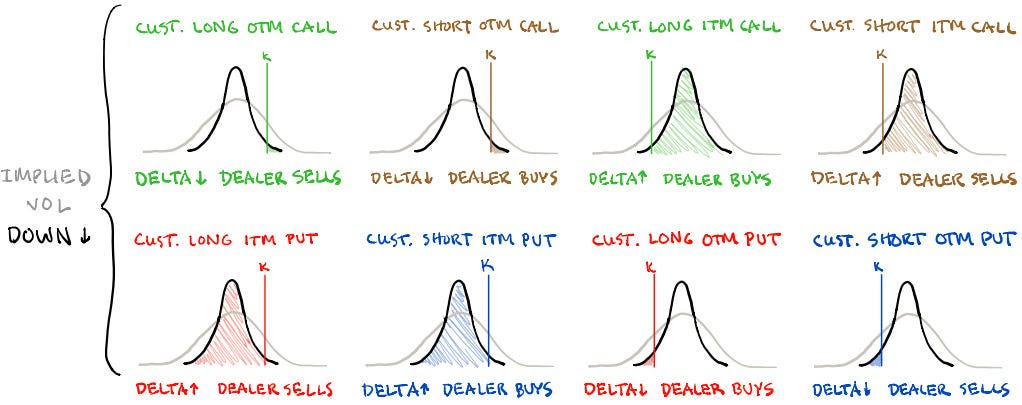

Basically, into the event, traders demanded protection and bid implied volatility (IVOL). The assumption is that counterparties, who are likely on the other end, have exposure to positive Delta and negative Gamma, which they hedge through negative Delta trades in the underlying.

Should fears have been assuaged, the supply of that protection once demanded, would have decreased IVOL (and options Delta), providing the markets a boost.

That didn’t happen. Instead, traders added protection, as shown by this SpotGamma graphic tracking changes in put open interest on the S&P 500 (INDEX: SPX).

Graphic: Retrieved from SpotGamma.Updated September 22, 2022.

This bid some basic measures of IVOL into the close.

Graphic: Retrieved from VIX Central. Updated September 21, 2022.

That’s as these particular options, which were added at much lower prices, as I explained in a SpotGamma note, recently, “are far more sensitive to changes in direction and IVOL.”

These options can go “from having very little Delta (exposure to direction) to a lot more Delta on the move lower,” quickly. “If we maintain that liquidity providers are short those puts, a positive Delta trade, then those liquidity providers [will sell] futures and stock, a negative Delta trade to stay hedged.”

Notwithstanding, it’s still the case that a “reload on fresh short-dated downside” flows heighten the risk of a “negative Delta squeeze … into month end,” said Nomura Holdings Inc’s (NYSE: NMR) Charlie McElligott.

Therefore, “you have to consider a move up [to] $4,000.00 as part of your distribution of outcomes to the upside,” as that is near where “market makers are ‘long,’” as part of an impactful collar trade many are aware sits.

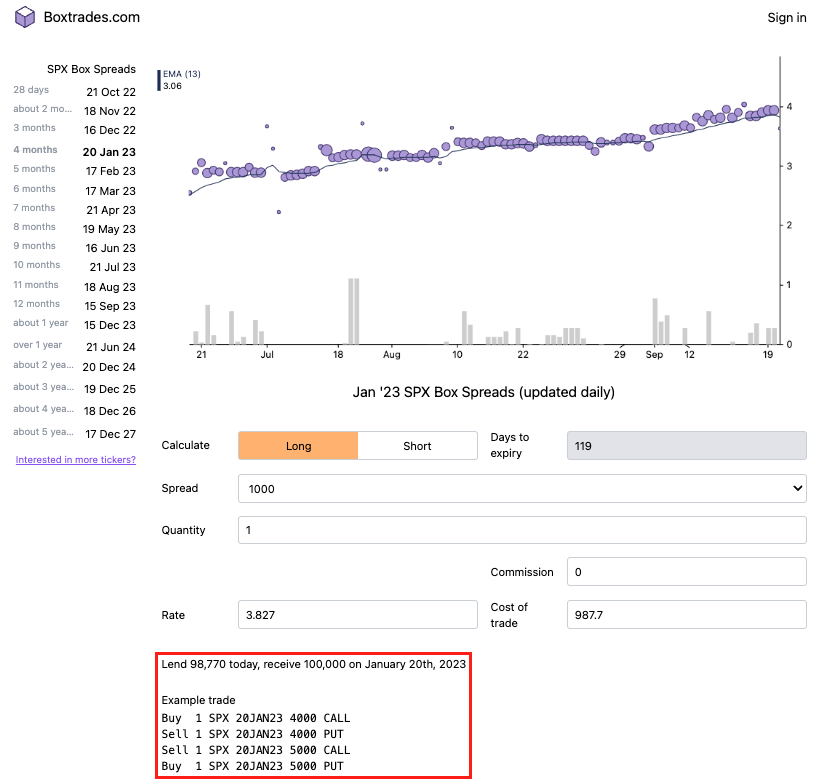

As an aside, some online conversation was sparked around placing cash into riskless trades for some small, but guaranteed, rates of return. In that conversation, Box Spreads were put forth as a solution to lend cash and earn a competitive interest rate.

For context, “Boxes allow market participants to create a loan structure similar to a Treasury bill. T-bills are ‘discount’ instruments that are purchased at a value less than the stated face value. Upon maturity, bills call for the return of the stated face value.”

“For example, one might buy a $1 million 90-day T-bill for $998,000. Ninety days later, the $1 million face or principal value is returned and the $2,000 discount is earned as interest. One may represent the rate on this transaction as a 0.80% or 80 basis point discount yield [= (360/90) x ($2,000/$1,000,000)]. The effective rate on a box represents a ‘discount yield’ similar to a quoted T-bill rate.”

IPS Strategic Capital’s Pat Hennessy explains that SPX boxes “typically yield[] 20-40 bps above [the] corresponding maturity risk-free rate.” Additionally, there are tax advantages to using the S&P 500’s 1256 contracts.

For easier fills, use the “3K/4K line in an AM settled expiry,” Hennessy noted. “Helps if you know where the broker market is.”

Technical

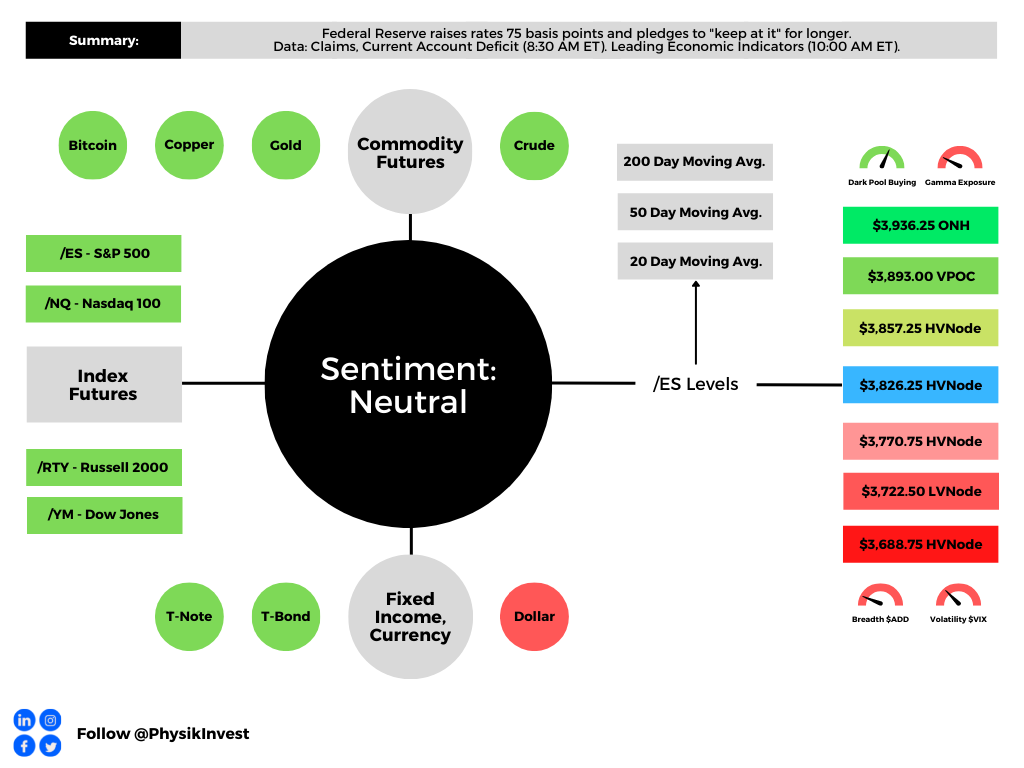

As of 8:00 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,826.25 HVNode puts into play the $3,857.25 HVNode. Initiative trade beyond the latter could reach as high as the $3,893.00 VPOC and $3,936.25 ONH, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,826.25 HVNode puts into play the $3,770.75 HVNode. Initiative trade beyond the HVNode could reach as low as the $3,722.50 LVNode and $3,688.75 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 900+ that read this report daily, below!

Graphic updated 6:50 AM ET. Sentiment Risk-Off if expected /ES open is below the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Administrative

A longer note so stick with me!

Updates are pending for the above dashboard. Exciting! Beyond this, the newsletter is getting a revamp in other parts. If you have any feedback on what should be changed, please comment!

Also, I am going to refer everyone to a conversation between Joseph Wang and Andy Constan, as well as some updates Cem Karsan of Kai Volatility made (HERE and HERE). That is, in part, a primer for what we will be talking more about, soon.

Fundamental

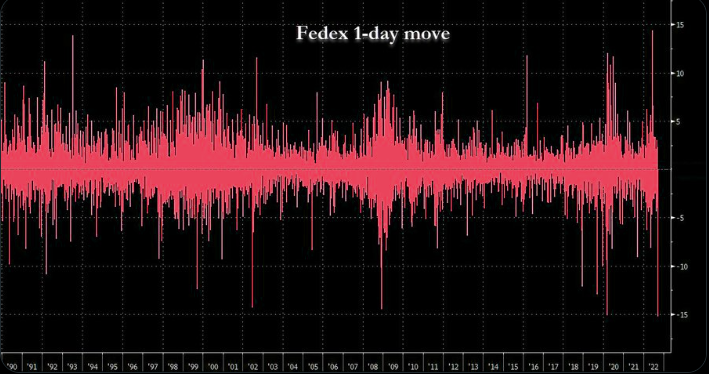

Talked about yesterday was the prospects of contractionary monetary policy reducing inflation and growth. BlackRock Inc (NYSE: BLK) strategists, even, put forth that a “deep recession” is needed to stem inflation. In short, “there is no way around this,” they claim.

Graphic: Retrieved from The Market Ear. FedEx Corporation (NYSE: FDX) sold 20% on warning about the global economy.

From thereon, we talked about how rates rising would “bring private sector credit growth down,” as well as “private sector spending and, hence, the economy.”

Based on where rates are at, the market may still be too expensive.

Graphic: Retrieved from Bloomberg via Michael J. Kramer. “What is amazing is how expensive this market is relative to rates. The spread between the S&P 500 Earnings yield and the 10-Yr nominal rate is at multi-year lows.”

On the other hand, some argue inflation peaks are in. ARK Invest’s Cathie Wood suggests “deflation [is] in the pipeline, heading for the PPI, CPI, PCE Deflator.”

Tesla Inc’s (NASDAQ: TSLA) Elon Musk added that he thinks the Federal Reserve (Fed) may make a mistake noting “a major Fed rate hike risks deflation.” Musk suggested the Fed should drop 0.25%, basing his decision on non-lagging indicators, unlike the Fed.

That’s not in line with what CME Group Inc’s (NASDAQ: CME) FedWatch tool shows. Through this tool we see traders pricing an 80% chance of a 0.50-0.75% hike, all the while quantitative tightening (reducing Fed Treasuries and mortgage-backed securities holdings) accelerated on September 15.

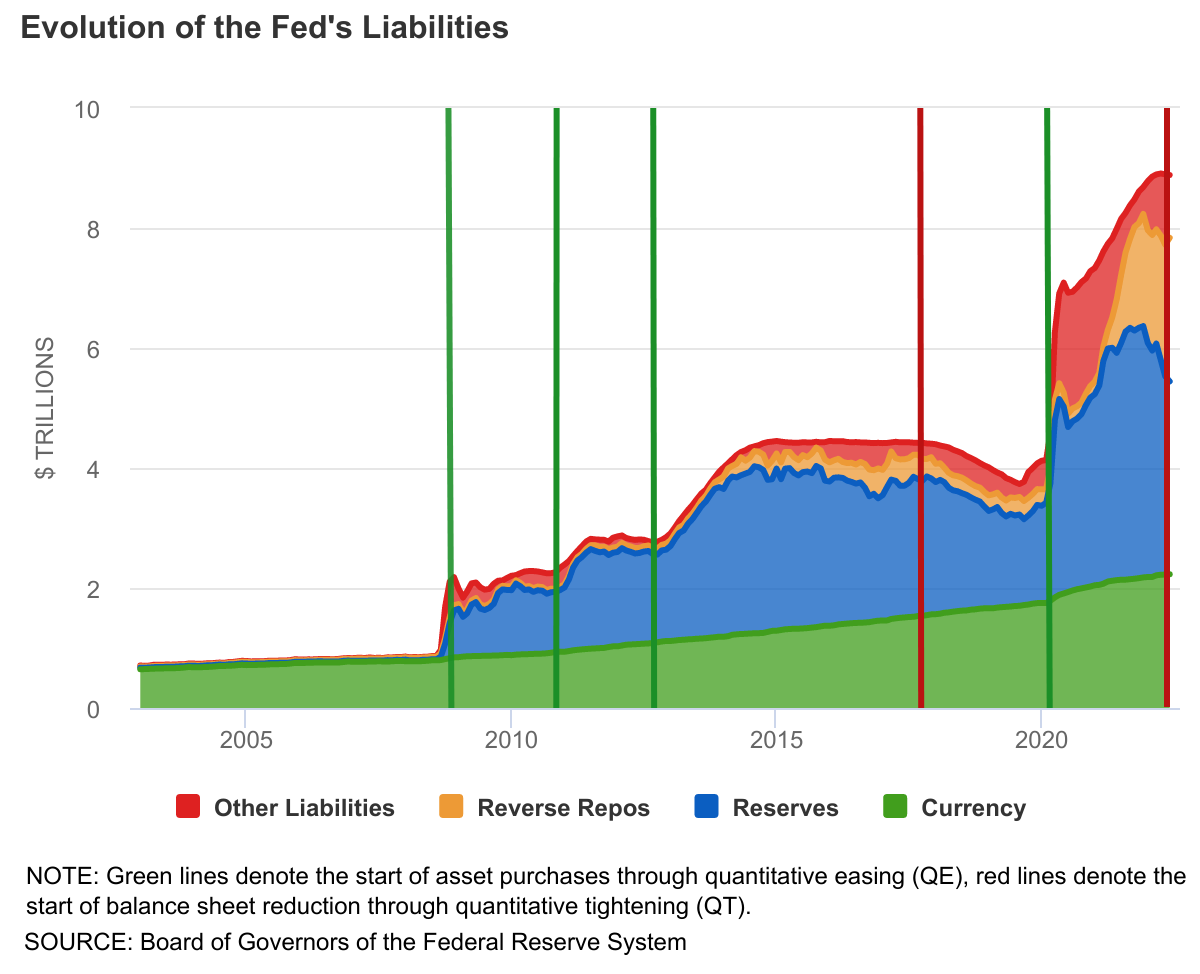

UST and MBS will roll off (which could turn into “outright sales”) at a pace of $95 billion per month, now, increasing competition for funding among commercial banks, and bolstering borrowing costs, as explained, below.

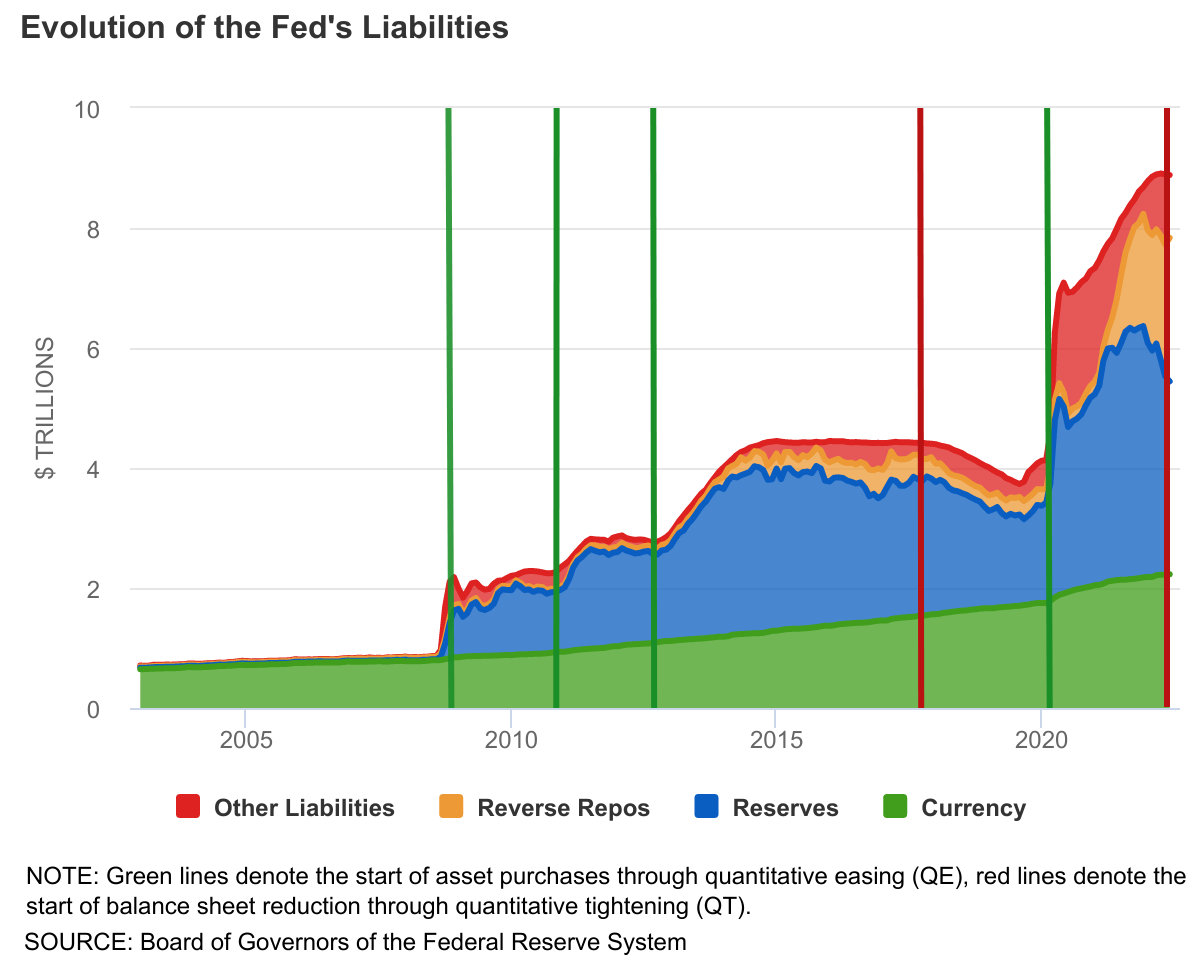

Graphic: Via Physik Invest. Data compiled by @jkonopas623. Fed Balance Sheet data, here. Treasury General Account Data, here. Reverse Repo data, here. NL = BS – TGA – RRP.

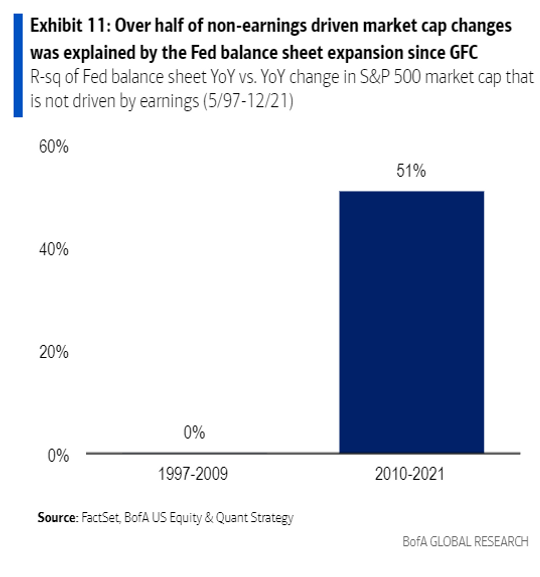

According to Bank of America Corporation (NYSE: BAC), since 2010, nearly 50% of the moves in market price-to-earnings multiples were explained by quantitative easing (QE), the inverse of QT, through which the Fed (or central banks, in general) creates credit used to buy securities in open markets, MarketWatch explains.

Graphic: Retrieved from the Federal Reserve Bank of Richmond. “The Fed Is Shrinking Its Balance Sheet. What Does That Mean?”

The “purchases of long-dated bonds are intended to drive down yields, which is seen enhancing appetite for risk assets as investors look elsewhere for higher returns. QE creates new reserves on bank balance sheets. The added cushion gives banks, which must hold reserves in line with regulations, more room to lend or to finance trading activity by hedge funds and other financial market participants, further enhancing market liquidity.”

Graphic: Retrieved from Bank of America Corporation (NYSE: BAC) via MarketWatch.

The liability side of the Fed’s balance sheet is what “matters to financial markets.”

Thus far, “reductions in Fed liabilities have been concentrated in the Treasury General Account, or TGA, which effectively serves as the government’s checking account” to run the day-to-day business.

Given that we’re talking about balance sheets, here, Fed liabilities must match assets. Thus, a rise in the TGA must be accompanied by a decline in bank reserves (which are liabilities to the Fed). This, as a result, decreases the room banks have to “lend or to finance trading activity by hedge funds and other financial market participants, [which] further [cuts into] market liquidity.”

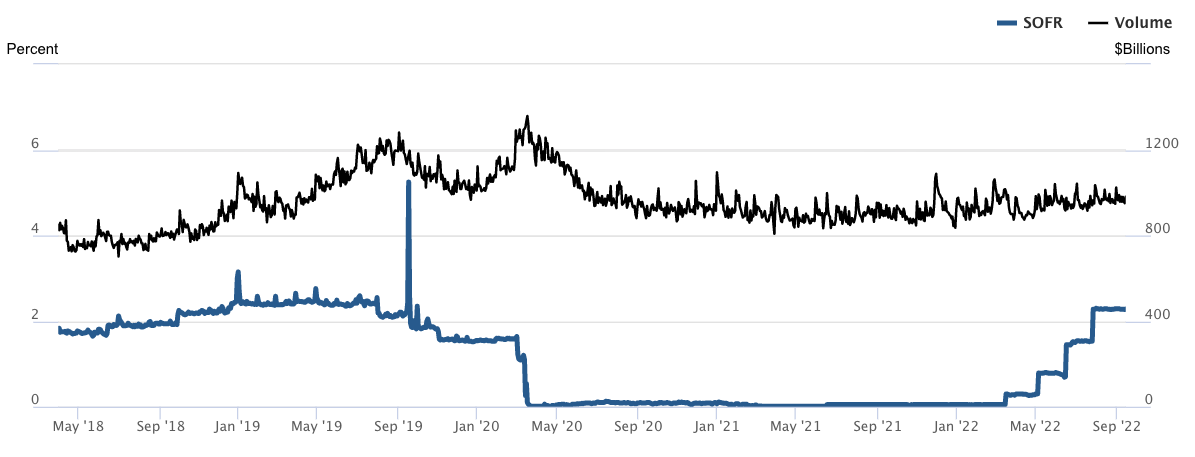

With the Treasury set to increase debt issuance, boosting TGA, it will effectively take “money out of the economy and put[] it into the government’s checking account.” The linked reduction in bank deposits and reserves bolsters “repurchase agreement rates and borrowing benchmarks linked to them, like the Secured Overnight Financing Rate,” per Bloomberg.

Graphic: Retrieved from the Federal Reserve Bank of New York. “The Secured Overnight Financing Rate (SOFR) is a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities.”

Adding, this may play into “an additional tightening of overall financial conditions, in addition to the increase in the main fed funds rate target that the central bank intends to continue boosting.”

This will “put more pressure on the private sector to absorb those Treasurys, which means less money to put into other assets” that may be riskier, like equities, said Aidan Garrib, the head of global macro strategy and research at Montreal-based PGM Global.

Positioning

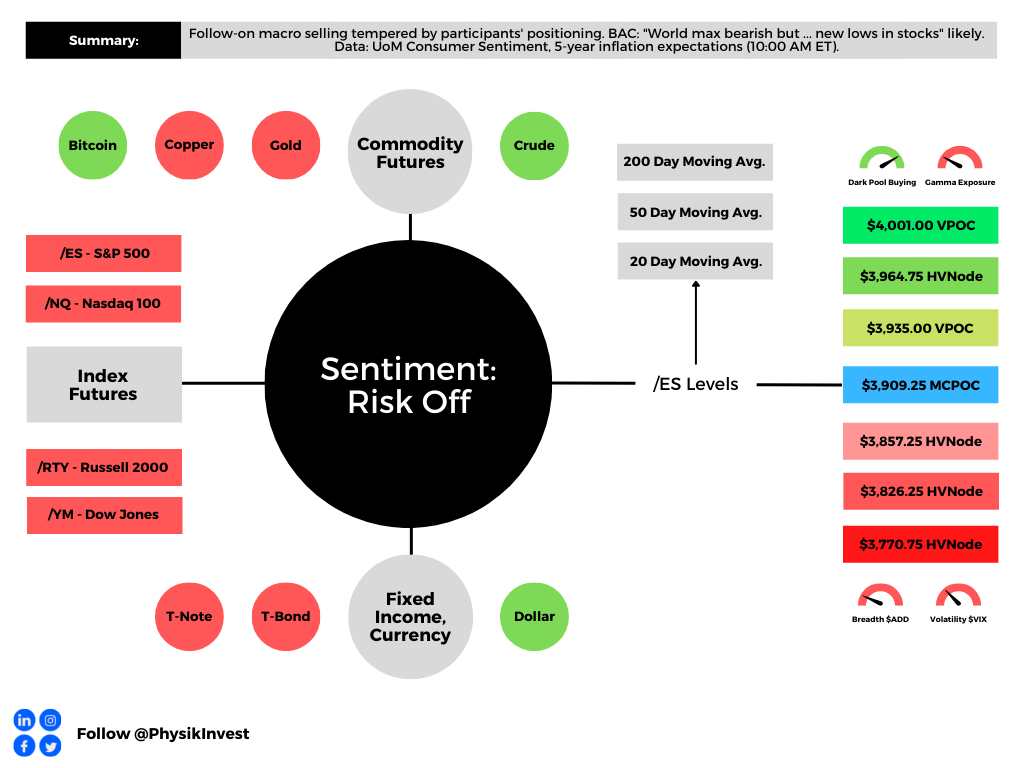

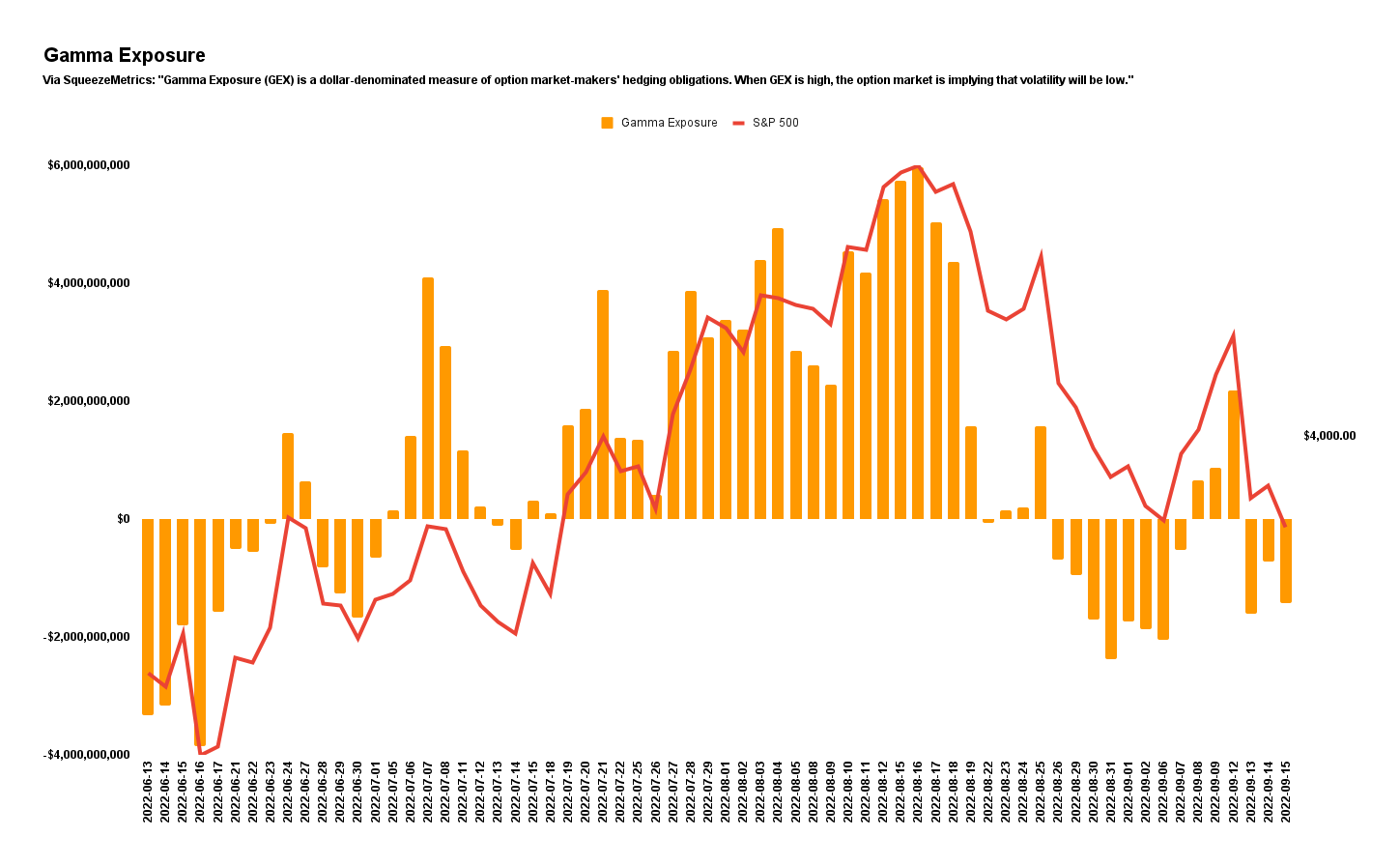

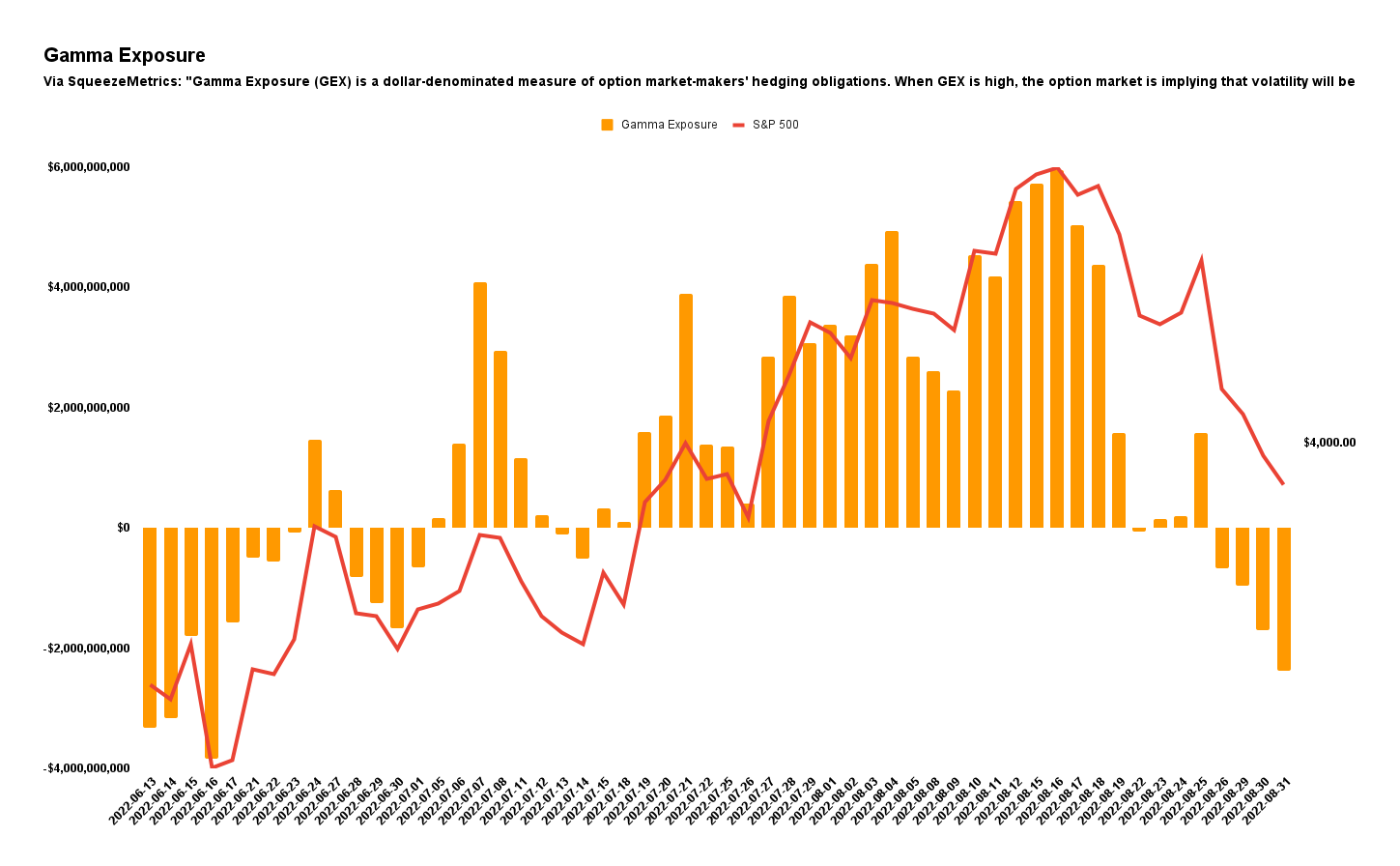

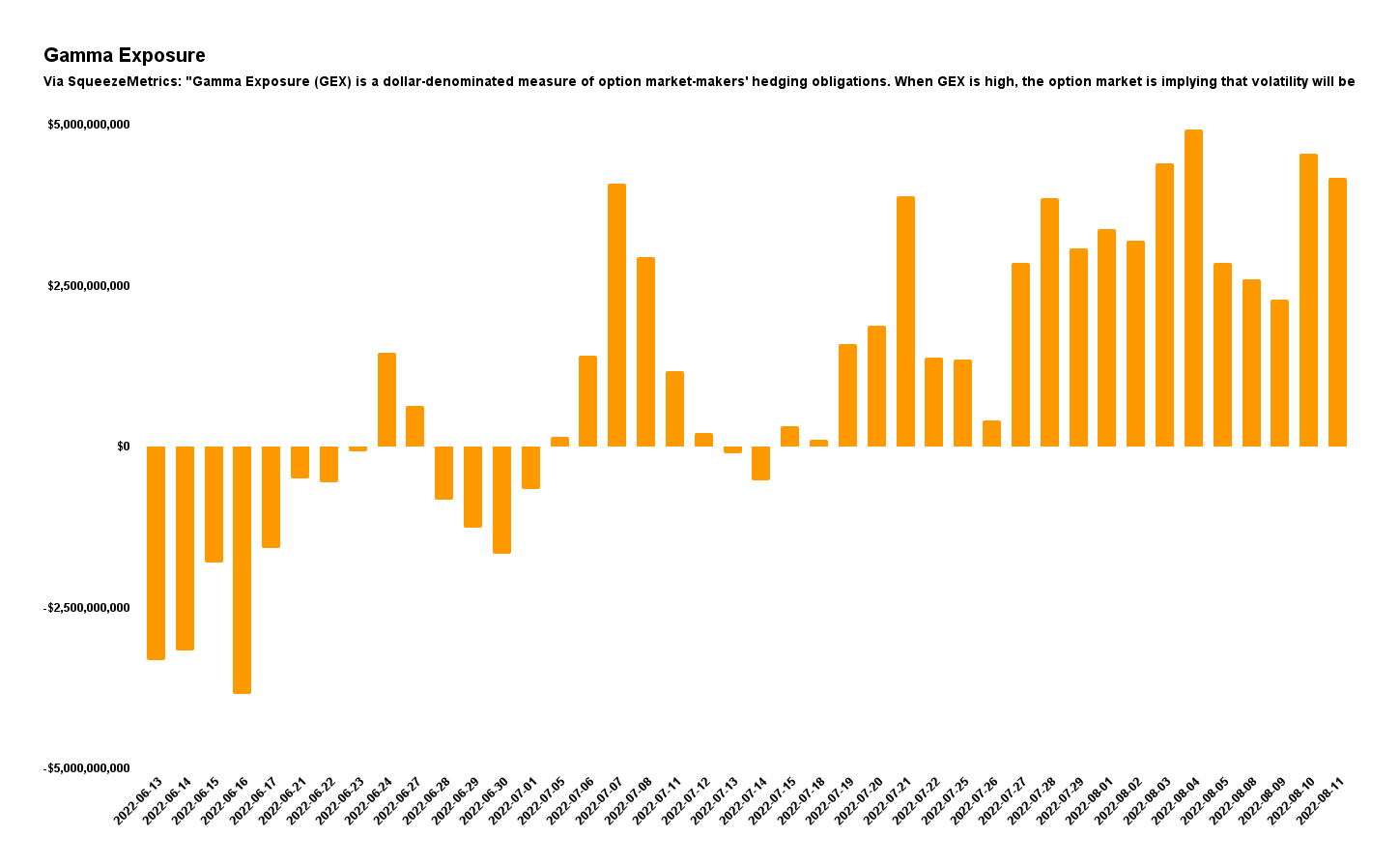

As of 6:50 AM ET, Friday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.44%. Net gamma exposures decreasing may promote generally more expansive ranges.

Graphic: Via Physik Invest. Data retrieved from SqueezeMetrics.

Given where realized (RVOL) and implied (IVOL) volatility measures are, as well as skew, it is beneficial to be a buyer of options structures.

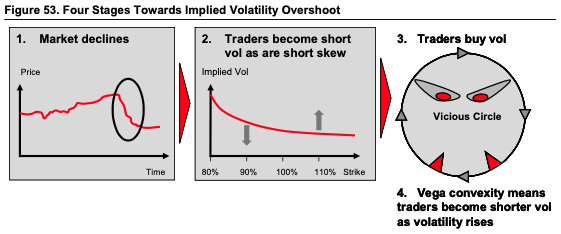

This is as there’s been a lot of speculation, particularly on the downside (put options), setting the stage for a more volatile and fragile market environment, says Kai Volatility’s Cem Karsan.

“On the index level, people are not well hedged,” a departure from what the case was heading into and through much of 2022. It’s the case that heading into 2022, traders were well hedged. Into and through the decline, traders’ monetization of existing hedges, as well as counterparty reactions, “compressed volatility” realized across US equities, as explained on July 15, 2022.

This made for some attractive trade opportunities seen here.

Graphic: Retrieved from The Market Ear. “VIX has decoupled from cross-asset volatilities.”

Now, given that the go-to trade is to sell stock and puts, short interest has grown, as have other risks, associated with this activity; essentially people are “los[ing] faith in convexity and risk premia’s ability to work,” as a result of “poor performance of vol,” and, the reaction to their “pain and financial loss,” is setting the stage for tail risks heading into the Q1 and Q2 2023.

The sale (purchase) of the front (back) expirations will bolster market pinning; as SpotGamma puts forth, “the positive impact of put closers and rolls, as well as decay,” is easing the market drop. However, this “positioning likely compounds drops and adds to volatility,” in the future.

To quote: “Though the removal of put-heavy exposures can boost markets higher, too add, the positive impacts are dulled via the demand for put exposures at much lower prices.”

Graphic: Retrieved from SpotGamma.

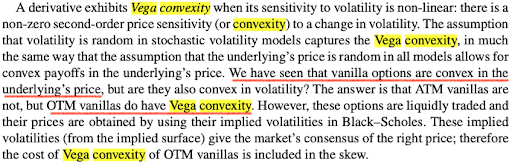

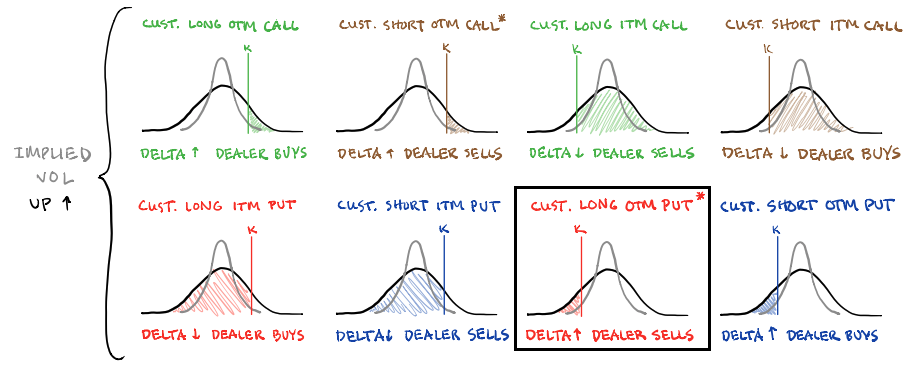

These particular options, which are at much lower prices, “are far more sensitive to changes in direction and IVOL,” as I explained in a SpotGamma note. These options can go “from having very little Delta (exposure to direction) to a lot more Delta on the move lower,” quickly.

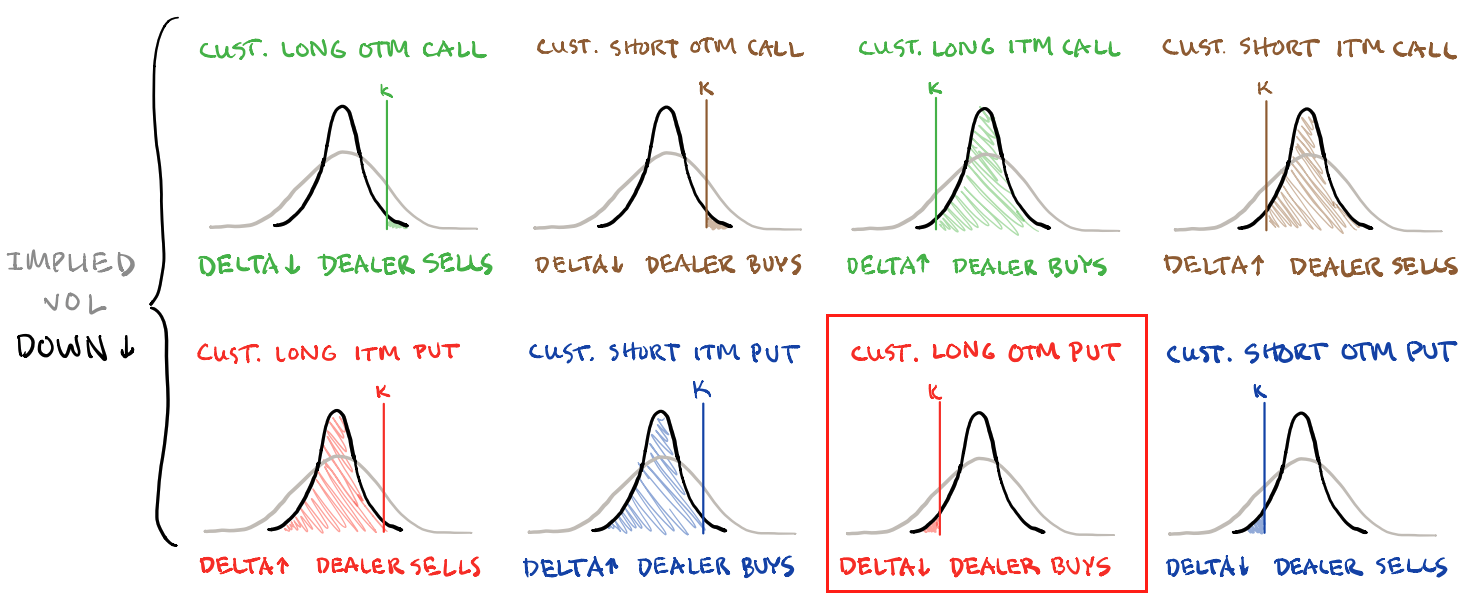

Graphic: Via Mohamed Bouzoubaa et al’s Exotic Options and Hybrids.

“If we maintain that liquidity providers are short those puts, a positive Delta trade, then those liquidity providers [will sell] futures and stock, a negative Delta trade to stay hedged.”

Graphic: Via Banco Santander SA (NYSE: SAN) research.

Technical

As of 6:50 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,909.25 MCPOC puts into play the $3,935.00 VPOC. Initiative trade beyond the latter could reach as high as the $3,964.75 HVNode and $4,001.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,909.25 MCPOC puts into play the $3,857.25 HVNode. Initiative trade beyond the latter could reach as low as the $3,826.25 and $3,770.75 HVNodes, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Considerations: A feature of this 2022 down market was responsiveness near key-technical areas (that are discernable visually on a chart). This suggested to us that technically-driven traders with shorter time horizons were very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

That’s changing. The key levels, quoted above, are snapping far easier and are not as well respected. That means other time frame participants with wherewithal are initiating trades.

Those are the participants you should not fade.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 900+ that read this report daily, below!

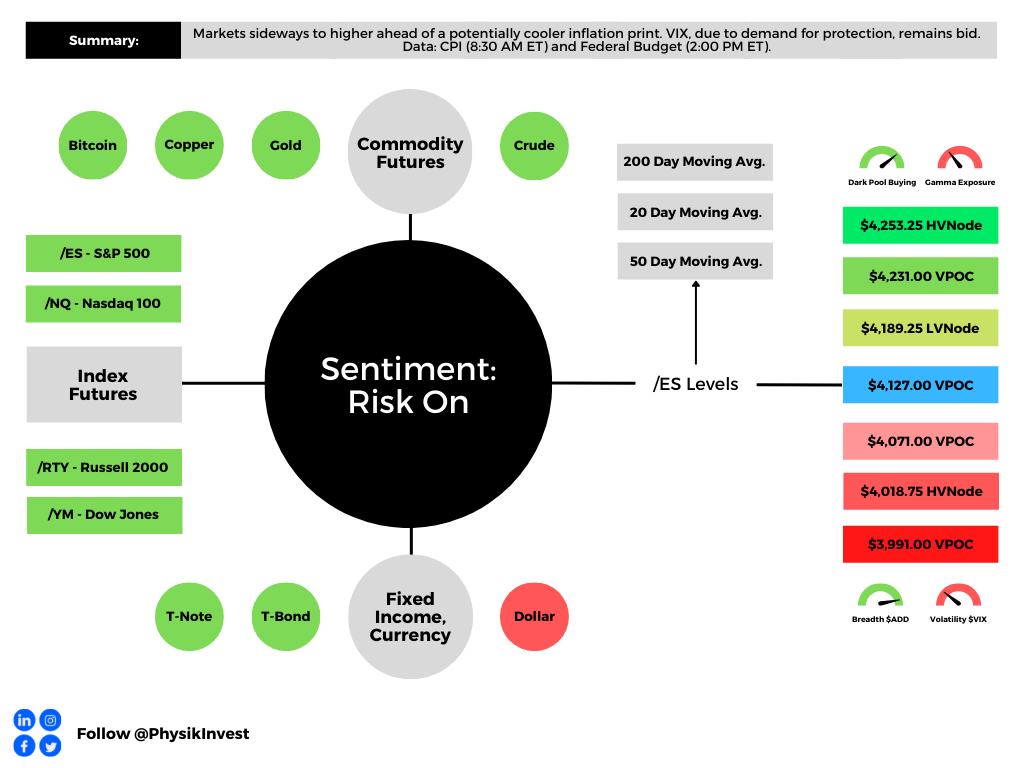

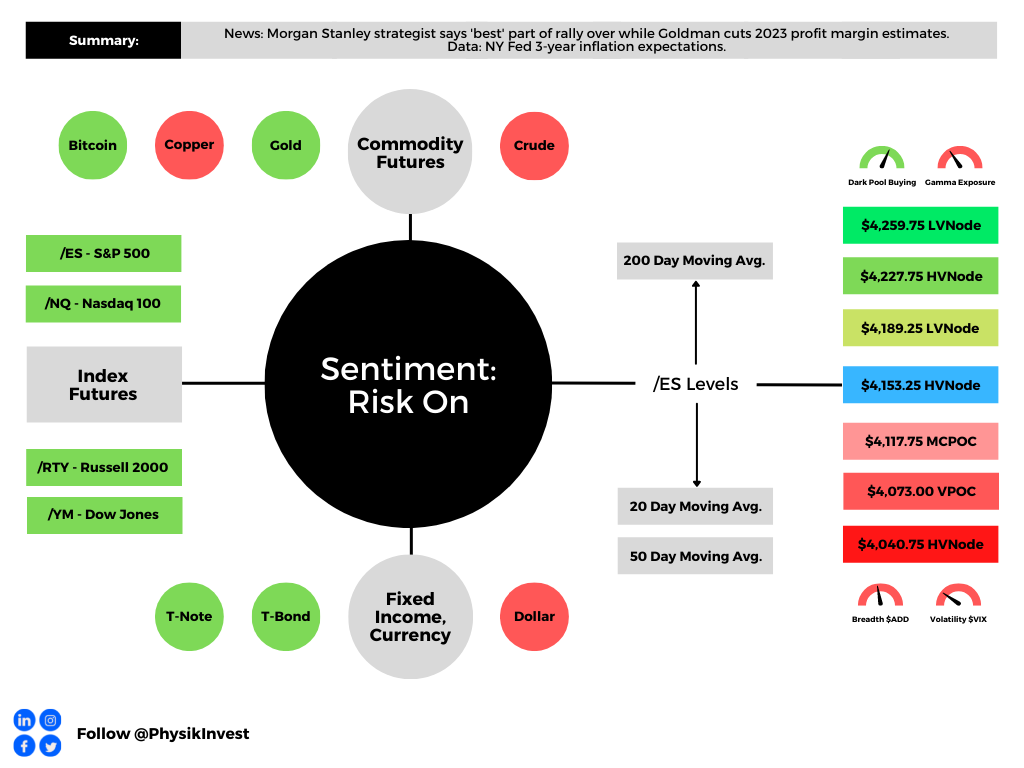

Graphic updated 7:45 AM ET. Sentiment Risk-On if expected /ES open is above the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Fundamental

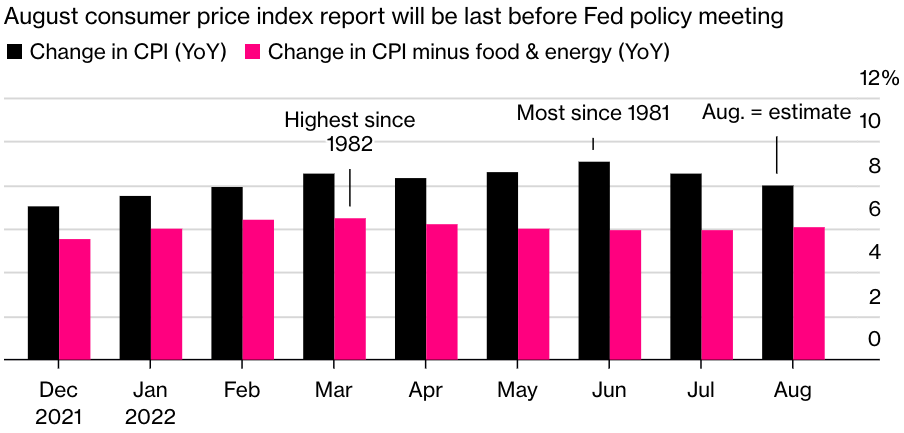

Today, traders get inflation updates. These will help drive perceptions regarding monetary policy.

Expected is an 8.1% rise year-over-year (YoY) and 0.1% fall month-over-month (MoM). In July, these numbers were 8.5% and 0.0%, respectively.

Core CPI (which excludes food and energy) is expected to rise by a rate higher than in July, 6.1% YoY and 0.3% MoM, respectively.

Mattering most is core inflation, which the Fed has more control over. If lower than expected, that may warrant some appetite for risk.

Notwithstanding, prior to July’s release, the average movement in the S&P 500, after CPI, was -1.27%. Still, though, the expectation is that August data will show improvement.

“The market has concluded that both the ECB and even the Fed, despite their protestations otherwise, are both being viewed as data-dependent,” Peter Tchir of Academy Securities said.

“I cannot see any scenario where the market doesn’t decide that CPI is heading the right direction and … [this] should allow markets to continue to enjoy the strength.”

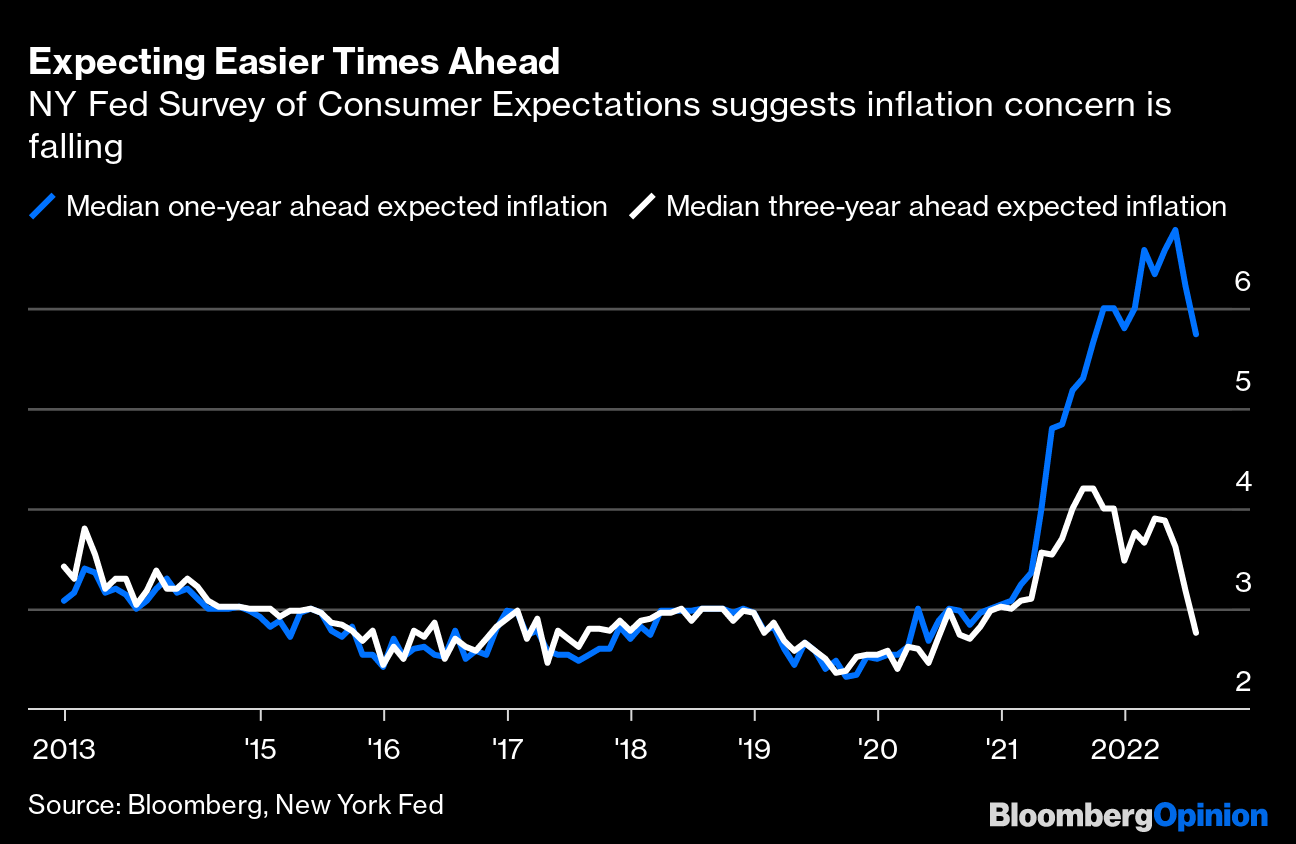

Graphic: Retrieved from Bloomberg. “Stronger evidence that a wage-price spiral can indeed be avoided came from Monday’s publication of the New York Fed’s latest Survey of Consumer Expectations.”

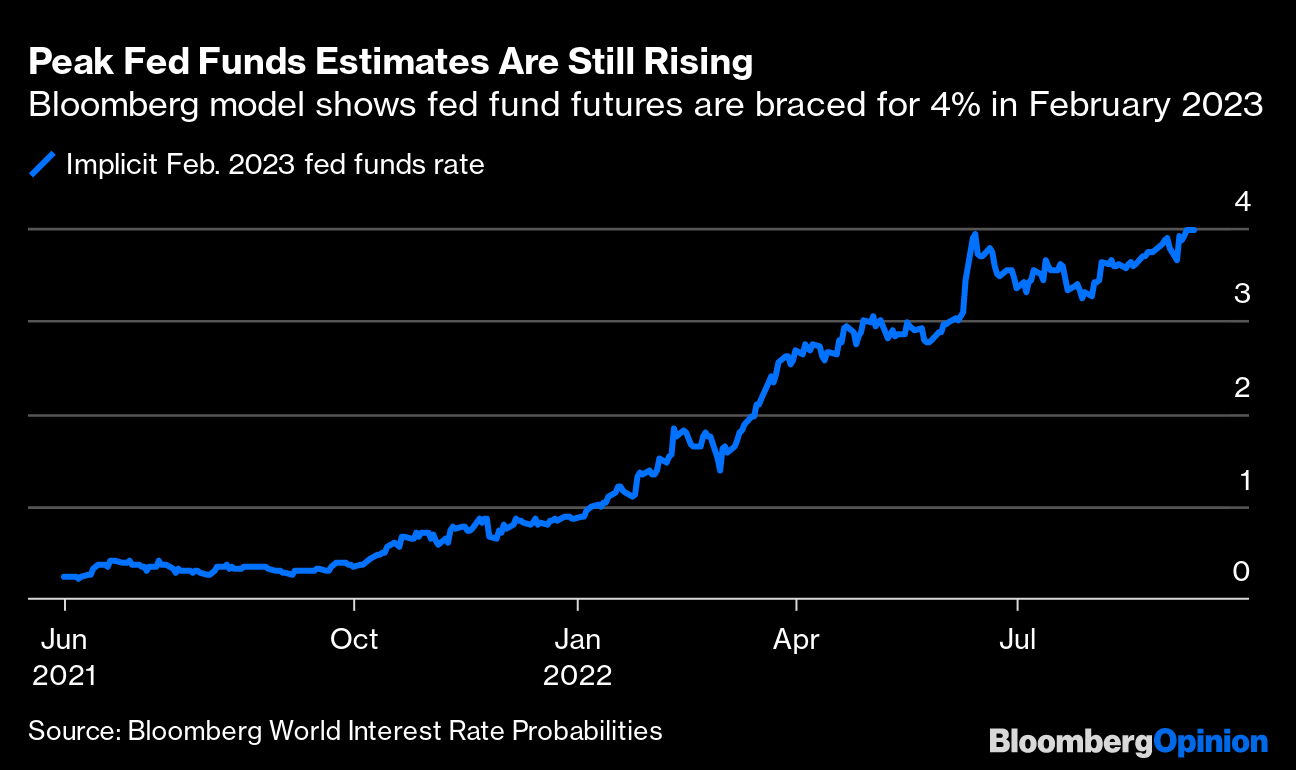

At this point, in spite of the prospects of inflation continuing to cool, expectations regarding Fed (Federal Reserve) action remain sticky with the fed funds futures pricing a peak in rates of 4%.

Graphic: Retrieved from Bloomberg.

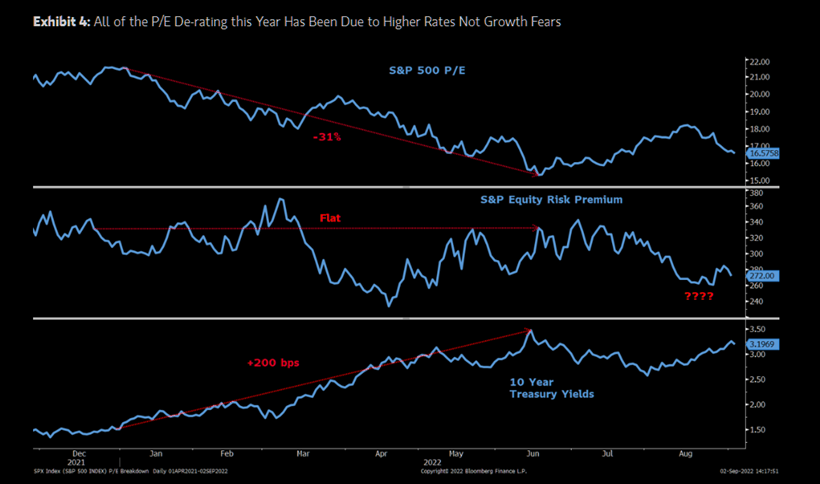

Unchanged, all else equal, this means markets have accounted for the rise in interest rates and their impact on valuations. From hereon, further de-rating is not out of the question, particularly if inflation continues to rise and/or growth fears materialize, as some like Fitch Ratings believe.

Graphic: Retrieved from The Market Ear. Via Morgan Stanley (NYSE: MS). “MS Research thinks the lows for this bear market will likely arrive in the fourth quarter with 3,400 the minimum downside and 3,000 the low if a recession arrives.”

According to Fitch, a decline in corporate profits is likely to speed up in the coming quarters, and this will highlight economic slowing (below-trend GDP growth) that leads to a 2023 recession.

Graphic: Retrieved from Bloomberg, via Bank of America Corporation (NYSE: BAC). “Bank of America … remains ‘fundamentally and patiently bearish.’”

To quote CFO Dive, “Downward revisions to consensus expectations for earnings next year ‘will likely accelerate as monetary tightening continues to reduce inflation and growth slows.’”

Thus far, the economy has shrunk 0.6% in the second quarter, after slumping 1.6% in the first, which is “the common definition of a recession” despite the continued growth of the economy as shown by other metrics like “nonfarm employment, consumer spending, industrial production, and weekly hours worked.”

Positioning

As of 7:45 AM ET, Tuesday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.24%. Net gamma exposures increasing may promote some market stability.

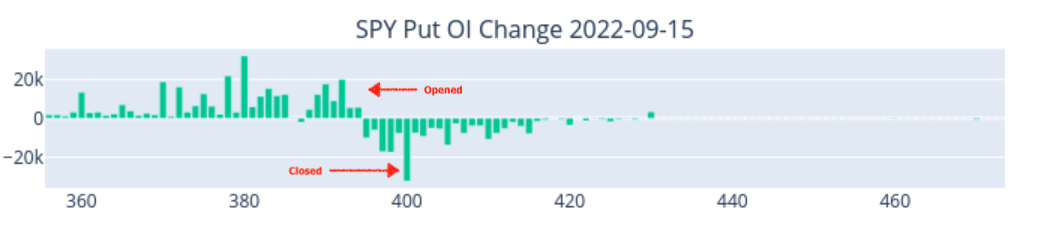

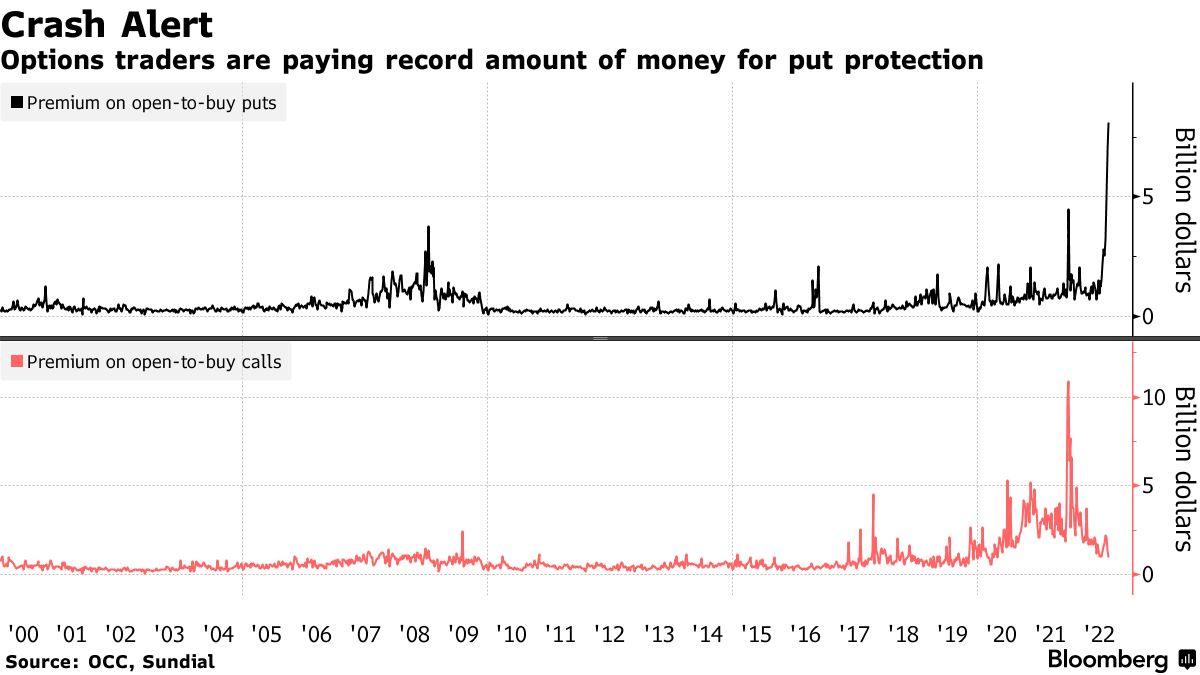

It’s the case that there is this trend in demand for equity downside put options protection. This is evidenced by figures of open interest, volume, as well as bid implied volatility (IVOL) metrics like the Cboe Volatility Index (INDEX: VIX).

“They’re buying protection against a crash at a pace unlike anything the market has ever seen,” said Jason Goepfert, chief research officer at Sundial. This is as Nomura Holdings Inc’s (NYSE: NMR) Charlie McElligott says more traders are taking shots amid “hawkish global central bank escalations,” and tightening measures of liquidity, among other things.

Graphic: Via Physik Invest. Data compiled by @jkonopas623. Fed Balance Sheet data, here. Treasury General Account Data, here. Reverse Repo data, here. NL = BS – TGA – RRP.

Goepfert adds that the “massive hedging activity” feels “unsettling.” That has to do with what the reaction to that protection entails should markets drop lower and IVOL increase, accordingly.

Graphic: Retrieved from SqueezeMetrics. Learn the implications of volatility, direction, and moneyness.

Notwithstanding, should nothing bad happen, the activity, which is structured in soon-to-expire options, will quickly fall out of favor (as will the probability of those options paying out). Liquidity providers, on the other side of those trades, will reduce their negative Delta (short futures and stock) hedges which may further add support to markets.

Graphic: Retrieved from Goldman Sachs Group Inc (NYSE: GS).

The concern is that soon after this big options expiration passes, new fear and demand for protection may feed into another bout of weakness as traders rush to re-protect and liquidity providers add pressure in their hedging, accordingly.

Graphic: Retrieved from Goldman Sachs Group Inc (NYSE: GS).

Technical

As of 7:00 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $4,127.00 VPOC puts into play the $4,189.25 LVNode. Initiative trade beyond the LVNode could reach as high as the $4,231.00 VPOC and $4,253.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $4,127.00 VPOC puts into play the $4,071.00 VPOC. Initiative trade beyond the VPOC could reach as low as the $4,018.75 HVNode and $3,991.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 850+ that read this report daily, below!

Graphic updated 8:15 AM ET. Sentiment Risk-Off if expected /ES open is below the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

This is all the while the conflict between Russia and Ukraine continues to rage, bolstering the structural issues contributing to the longer-lasting inflation we discussed on August 3 (HERE).

In that August 3 letter, we cited Credit Suisse Group AG’s (NYSE: CS) Zoltan Pozsar on his perspectives regarding the weakening of “the pillars of the globalized, low inflation world.”

Since then, Pozsar wrote another note titled “War and Industrial Policy,” published on August 24 (HERE), alleging a “messy divorce” ongoing between large powers like the US and China.

For instance, the note said: “Pentagon chief’s calls to China go unanswered amid Taiwan crisis.”

Yikes! Let’s unpack what’s going on a bit, further.

Basically, it’s the case that powers like Russia became “rich selling cheap gas” to countries like Germany who became “rich selling expensive stuff produced with cheap gas,” the note says.

Per Andreas Steno Larsen, now, countries like Germany are in a precarious position.

It’s possible that the country “will likely make it through winter unless Russia 1) halts the gas flow completely and 2) the winter is extremely severe.”

No matter what, the “Germany economy will take a hit, … [and], given current forward prices, we are looking at CPI numbers well above 10% y/y. In France and Spain, that picture is even worse with numbers above 15% y/y.”

To dampen the impact of this inflation, countries like Denmark have resorted to “handing checks out almost randomly,” which does less to take from “inflationary pressures down the road.”

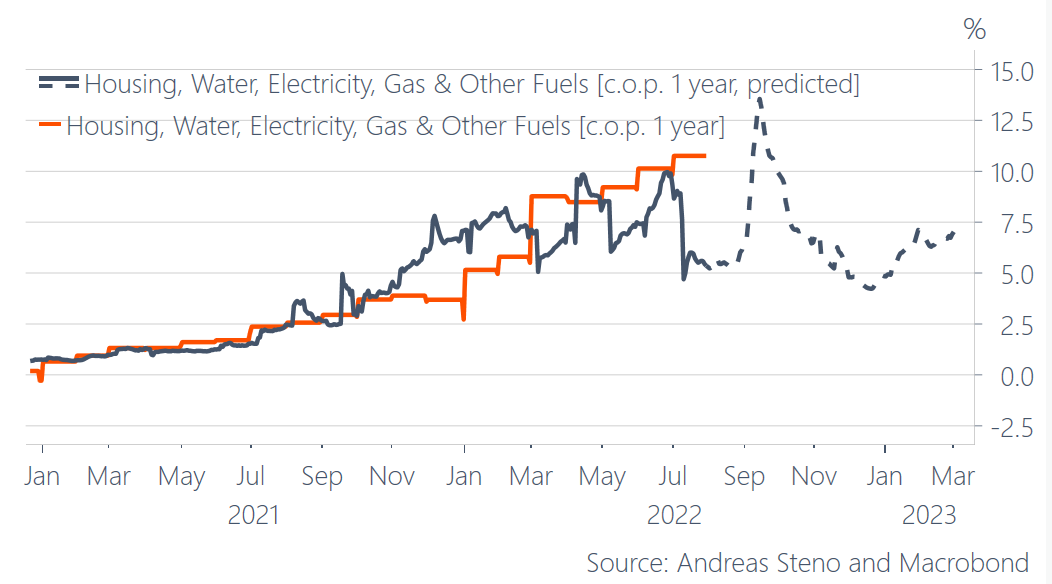

Graphic: Via Andreas Steno Larsen. “German energy component of CPI is only getting worse.”

In short, via de-globalization and populism, “the pillars of the low inflation world are changing,” per Pozsar and, the recourse, now, is a fight via asset price deflation, put forth on August 3.

In other words, de-globalization and populism have prompted an “inward shift of supply curves across multiple fronts (labor, goods, and commodities).” Accordingly, the economy is on a path that is “L”-shaped (i.e., vertical drop in activity via recession, and flatline for a period of time as rates remain higher for longer to prevent a sharp rise in inflation, again).

Graphic: Via Physik Invest. Data compiled by @jkonopas623. Fed Balance Sheet data, here. Treasury General Account Data, here. Reverse Repo data, here. NL = BS – TGA – RRP.

As Pozsar summarises: “we [have] to generate a big, “L”-shaped recession to slow inflation down; we [have] to generate a round of negative wealth effects to lower demand such that it becomes more in line with the new realities of supply.”

Separately, a Minsky Moment looms, Pozsar said.

“Minsky moments are triggered by excessive financial leverage, and in the context of supply chains, leverage means excessive operating leverage: in Germany, $2 trillion of value added depends on $20 billion of gas from Russia…that’s 100-times leverage – more than Lehman’s.”

Moreover, it is the case that, ultimately, after inflation is reduced, a “recovery [will be driven by] fiscally funded industrial policy” that:

(1) Re-arms (to defend the world order); (2) re-shores (to get around blockades); (3) re-stocks and invests (commodities); (4) re-wires the grid (energy transition).

Graphic: Text retrieved from Kai Volatility’s Second Quarter (2022) Market Commentary And Outlook. Annotated by Physik Invest’s Renato Leonard Capelj.

With that in mind, Pozsar ends that there will likely be a commodity supercycle that is part of a new regime, Bretton Woods III. Read the full note, here, and/or listen to the below podcast.

Positioning

As of 6:35 AM ET, Thursday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.42%. Gamma exposures falling, at an increasing pace, may add to ranges and pressure.

Graphic: Created by Physik Invest. Data by SqueezeMetrics.

As discussed thoroughly in our August 31 (HERE) and August 18 (HERE) letters, our analyses had us structuring spreads against the $3,700.00-$3,500.00 area in the S&P 500 (INDEX: SPX).

Graphic: Retrieved from Cboe Global Markets Inc (BATS: CBOE). Updated August 17, 2022.

To quote the August 18 letter, it was “beneficial to be a buyer of options structures to protect against (potential) downside (e.g., S&P 500 [INDEX: SPX] +1 x -2 Short Ratio Put Spread | 200+ Points Wide | 15-30 DTE | @ $0.00 or better).”

This trade is near-finished and it is time to monetize (i.e., closing and converting a position to cash) as there is a risk of losing the Deltas built up this decline on a fast move higher, should one probably occur here, soon, with the S&P 500 trading into a key support zone we outlined.

Graphic: Retrieved from VIX Central. Compression in implied volatility would solicit positive delta hedging flows (vanna), and this could provide markets with a boost.

In short, it is beneficial to be a seller of those options structures (e.g., S&P 500 [INDEX: SPX] -1 x +2 Ratio Put Spread | 200+ Points Wide | 15-30 DTE).

Note: Trades Renato has personally taken remain to be unpacked in subsequent commentaries. Both the mistakes and successes, as well as what to do better.

Technical

As of 8:10 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,943.25 HVNode puts into play the $3,987.00 VPOC. Initiative trade beyond the VPOC could reach as high as the $4,064.00 RTH High and $4,107.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,943.25 HVNode puts into play the $3,909.25 MCPOC. Initiative trade beyond the MCPOC could reach as low as the $3,867.25 LVNode and $3,829.75 MCPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 750+ that read this report daily, below!

Graphic updated 7:00 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Fundamental

We’ll skip the fundamentals section, today, and do an in-depth review, sometime next week.

Positioning

As of 7:00 AM ET, Friday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.06%. Net gamma exposures generally rising may promote tighter trading ranges.

Graphic: Via Physik Invest. Data retrieved from SqueezeMetrics.

As stated yesterday, it may be beneficial for traders to shift their focus to dynamic structures. In other words, be a buyer of options structures (i.e., replace static directional exposures or Delta with those that are dynamic).

This is (1) due to where realized (RVOL) and implied (IVOL) volatility measures, and skew.

Graphic: Retrieved from Interactive Brokers Group Inc’s (NASDAQ: IBKR) Trader Workstation.

As well as (2) increased average stock correlation and lower return dispersion which, per Societe Generale SA (OTC: SCGLY) research, make stock picking hard(er).

It can be the case that Delta hedging becomes easier, too, as one asset, in a more correlated environment, can better offset the first-order sensitivities elsewhere.

Graphic: Retrieved from Bloomberg. Via Societe Generale.

The reason why?

In regards to the correlation and dispersion remark, that’s more to do with the risk-off sentiment and the impact of tightening liquidity affecting all risk assets, basically.

Graphic: Via PhysikInvest. Data compiled by @jkonopas623. Fed Balance Sheet data, here. Treasury General Account Data, here. Reverse Repo data, here. NL = BS – TGA – RRP.

Regarding the volatility issue (RVOL, IVOL, and skew), that’s more to do with hedging trends.

Essentially, the monetization and counterparty hedging of existing customer hedges, as well as the sale of short-dated volatility, particularly in some of the single names where there was “rich” volatility, into the fall, lent to lackluster performance in IVOL and index mean reversion.

Accordingly, “if commodities are not performing … as a hedge, that opens the door,” to markets falling and traders demand equity volatility hedges, per The Ambrus Group’s Kris Sidial.

Learn about options dealer flows, inflation, and investing in a changing world with Cem Karsan.

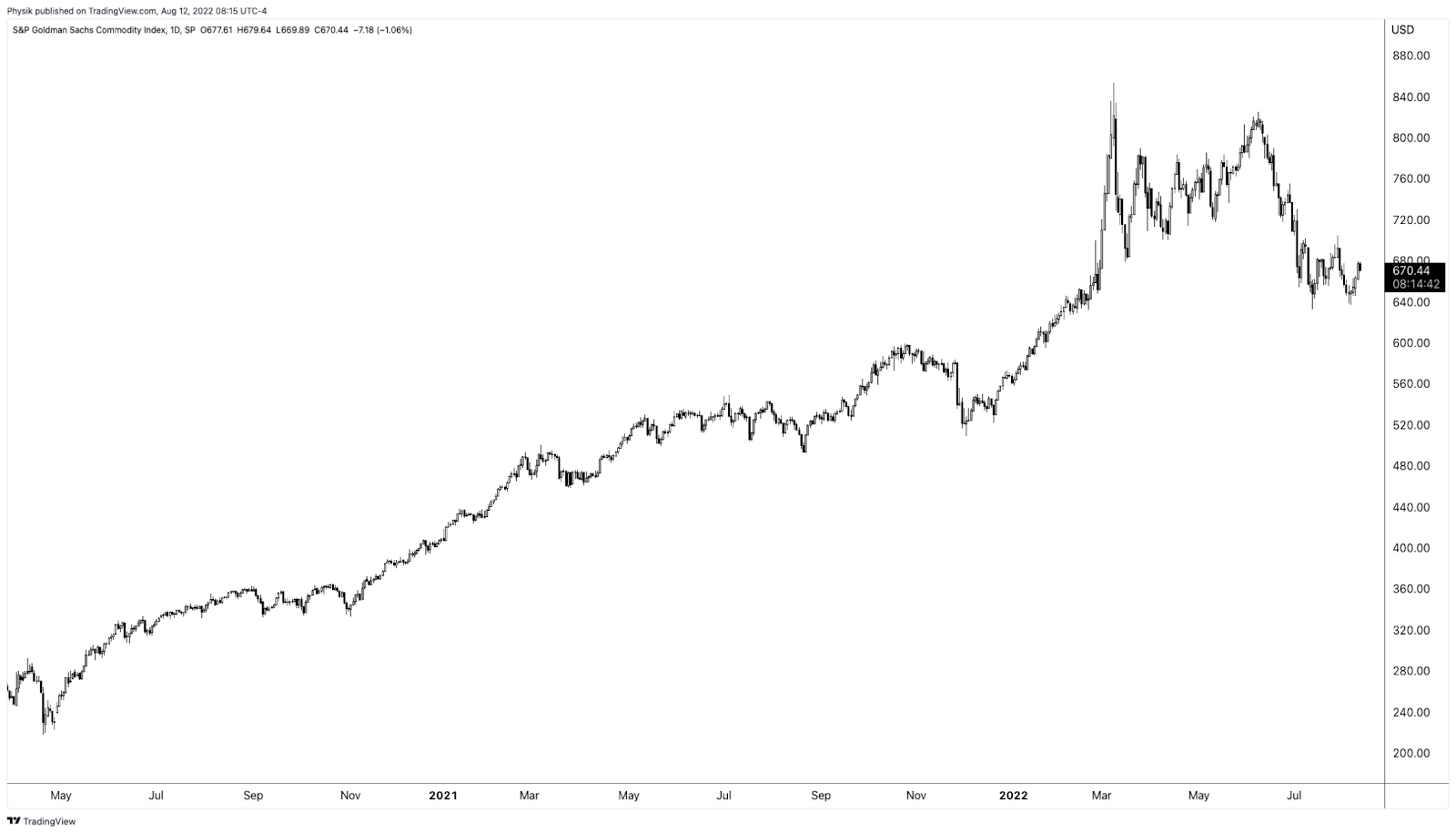

Graphic: Retrieved by Physik Invest from TradingView. S&P Goldman Sachs Commodity Index.

Adding, per to SpotGamma, “a lot of the boost from volatility compression has played out. With IVOL at a lower bound, it may be opportune to replace static Delta bets for those that are dynamic (i.e., long option exposures) and have less to lose in this lower volatility environment.”

Graphic: Retrieved from Vix Central. The term structure of IVOL.

“In a case where market participants see the Fed keeping its commitment to aggressive monetary policy action, negative Delta options exposures may outperform static short equity (bets on the downside).”

Graphic: Retrieved from Bloomberg. “Thursday’s message was that on mature reflection, the progress on the economy didn’t justify taking the stock market any higher than it was at the start of the day.”

If bullish, sample structures to consider, given a smiley skew, include low- or zero-cost bullish call ratio spreads, against the trend resistances in products like the S&P 500 (INDEX: SPX).

Graphic: Retrieved from Bloomberg. Drawn on by Physik Invest.

Technical

As of 7:00 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a nearly balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $4,227.75 HVNode puts into play the $4,253.25 HVNode. Initiative trade beyond the latter could reach as high as the $4,275.75 LVNode and $4,303.00 Weak High, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $4,227.75 HVNode puts into play the $4,202.75 RTH Low. Initiative trade beyond the RTH Low could reach as low as the $4,189.25 LVNode and $4,153.25 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 750+ that read this report daily, below!

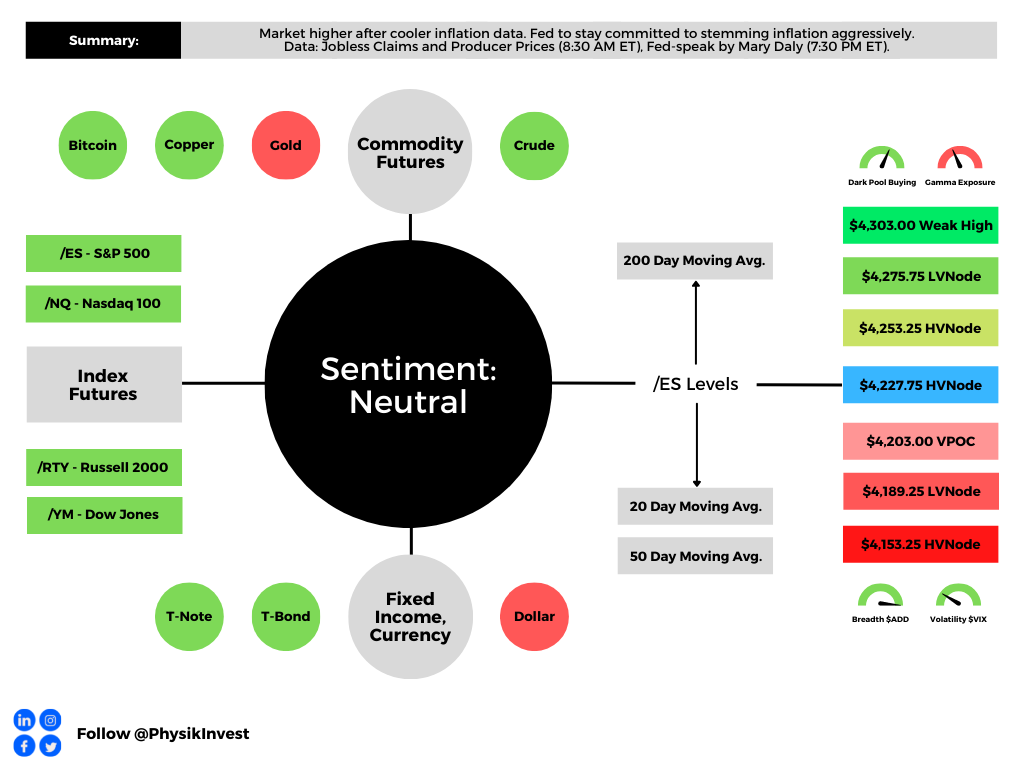

Graphic updated 7:30 AM ET. Sentiment Risk-On if expected /ES open is above the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Fundamental

Equity market rally spurred by cooler a Consumer Price Index (CPI).

Expected was an 8.7% rise year-over-year (YoY) and 0.2% month-over-month (MoM). Core CPI (which excludes food and energy) was to rise by 6.1% YoY and 0.5% MoM, respectively.

Officially, the headline number rose to 8.5%. The core CPI rose 5.9% YoY and 0.3% MoM, meaning the March peak remains (6.5% YoY, then).

Participants responded positively to the number, as expected could happen in a case where the CPI printed lower.

As I talked about in yesterday’s morning letter and in a SpotGamma note, with easing inflation:

(1) investors may command a lower rate of return for their purchasing power and (2) lower rates (if policymakers were to become less aggressive) do less to negatively impact discounted cash flows and the ability to finance future growth.

It is the case that immediately after the release of the CPI, traders dramatically shifted their bets on monetary action.

Previously, it was thought a 75 to 100 basis point hike would follow the report. Now, there are higher odds, as priced by the market, that there is a 25 to 50 basis point hike.

Graphic: Retrieved from CME Group Inc (NASDAQ: CME).

“I think the market is a bit overly giddy on this CPI number and it’s probably unlikely that the [Federal Reserve] (Fed) will start to ease up and take a less hawkish stance,” The Ambrus Group’s Kris Sidial put forth.

“The increase in risk assets somewhat gives the Fed the green light to be able to move more swiftly with a hawkish tone.”

Accordingly, the Fed’s Mary Daly said it is too early to declare victory in the inflation fight (and rightfully so), signaling, however, that she may support a slower pace of hikes.

This is as home buyers and renters, in some areas, are seeing large hikes in prices. For instance, per one Bloomberg article, a Miami native saw their rent increase “by $650 to $2,400.00 a month,” forcing them to search for new places to live.

The Ambrus Group’s Sidial adds:

“Inflation is one of those things that is difficult to control when it’s out [of] the bag (historically). I think the Fed understands this and if they have the opportunity to tame it, while not completely obliterating risk assets, it seems like a perfect scenario.”

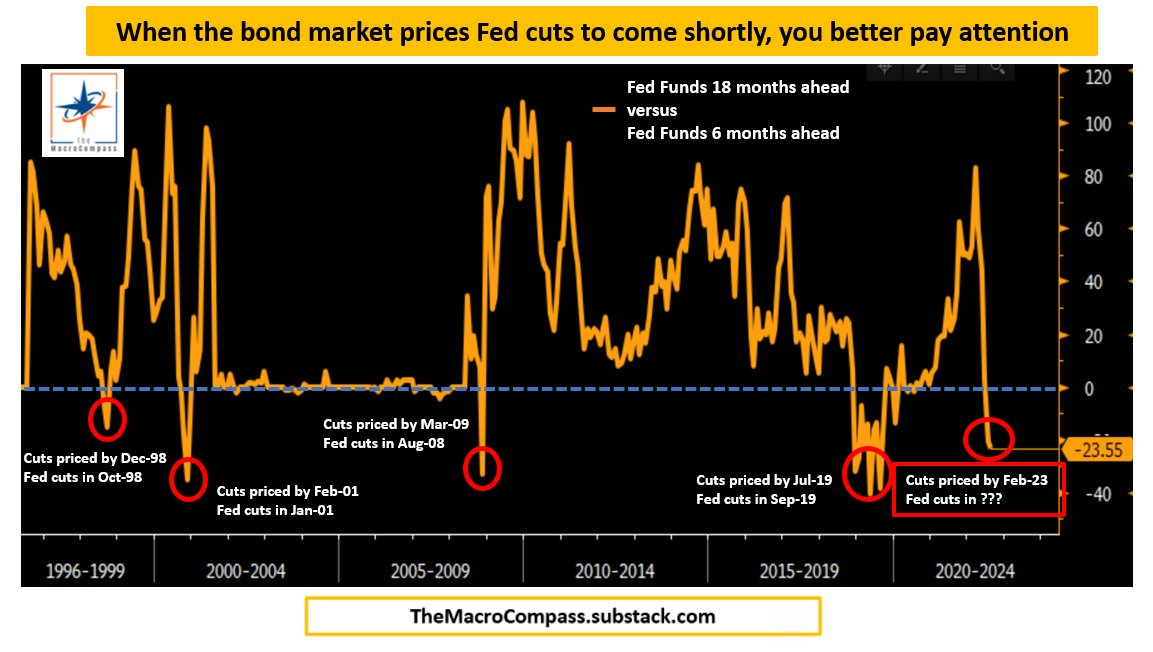

Ultimately, farther out in time, some metrics, which have incredible success in forecasting pivots, show the Fed likely to cut in 2023, shortly following the aggressive hiking cycle.

Graphic: Retrieved from Alfonso Peccatiello of The Macro Compass.

On the topic of (eventual) declines and slowing in the risk assets (like housing), “in most cases today, a borrower with 60 points of equity in their property, even facing moderate declines in their current home price, are not a big default risk,” explains Dan Ivascyn of PIMCO.

“A lot of what we like in the market today is seasoned-type risk that benefits from the multi-years of home price appreciation, and therefore is much less sensitive to what goes on from this point forward.”

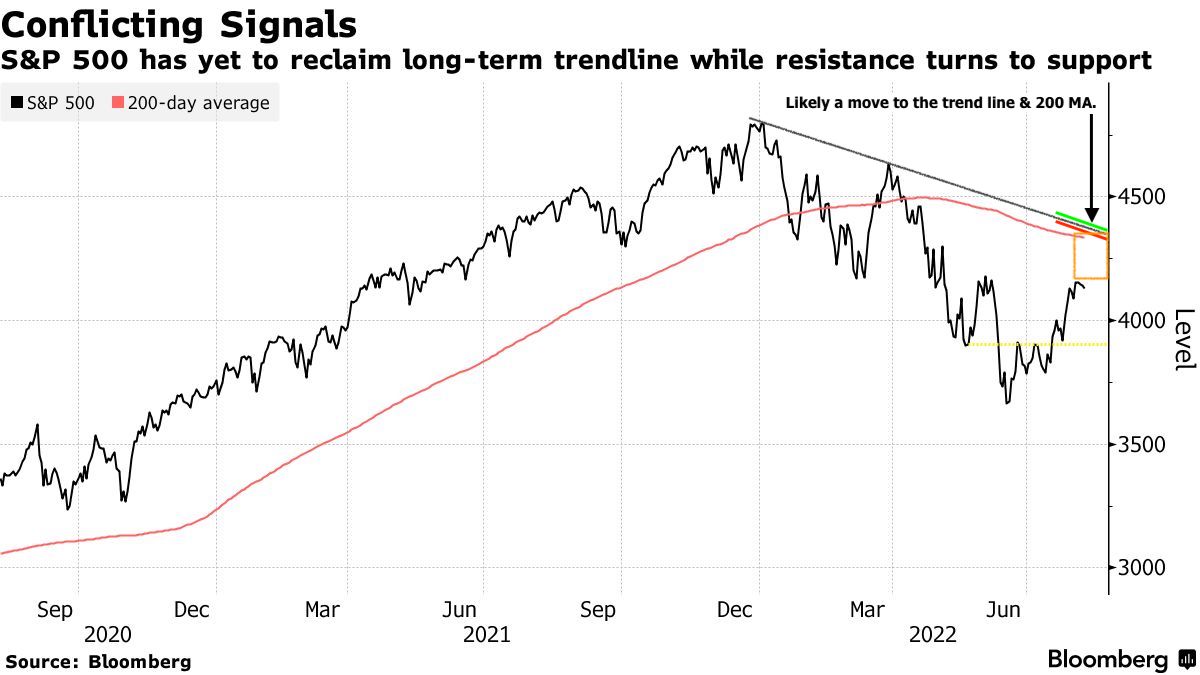

From an S&P 500 (INDEX: SPX) perspective, the index has basically recouped half its losses for the year. This often came after the bear lows were in.

Graphic: Retrieved from Bloomberg.

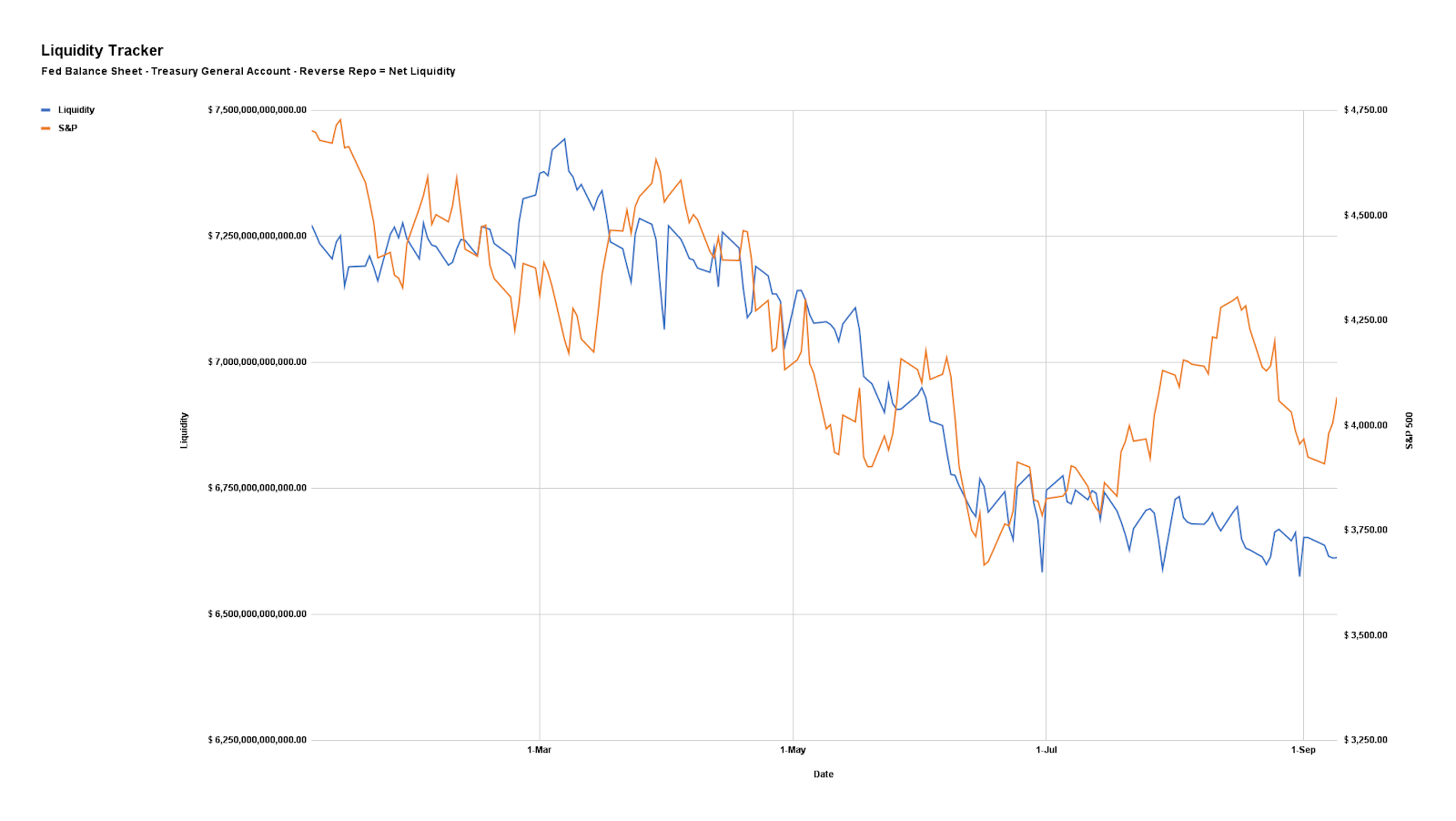

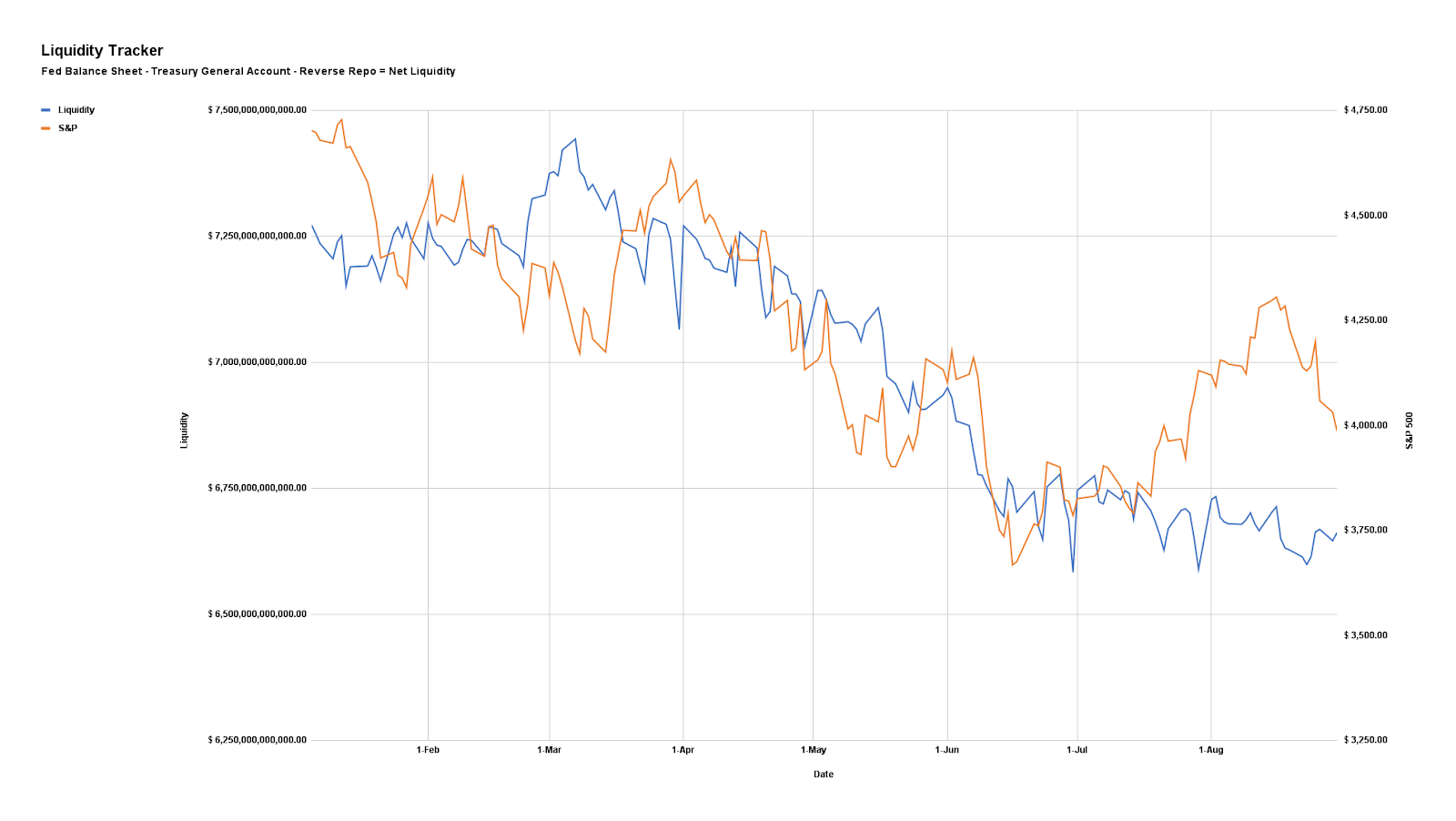

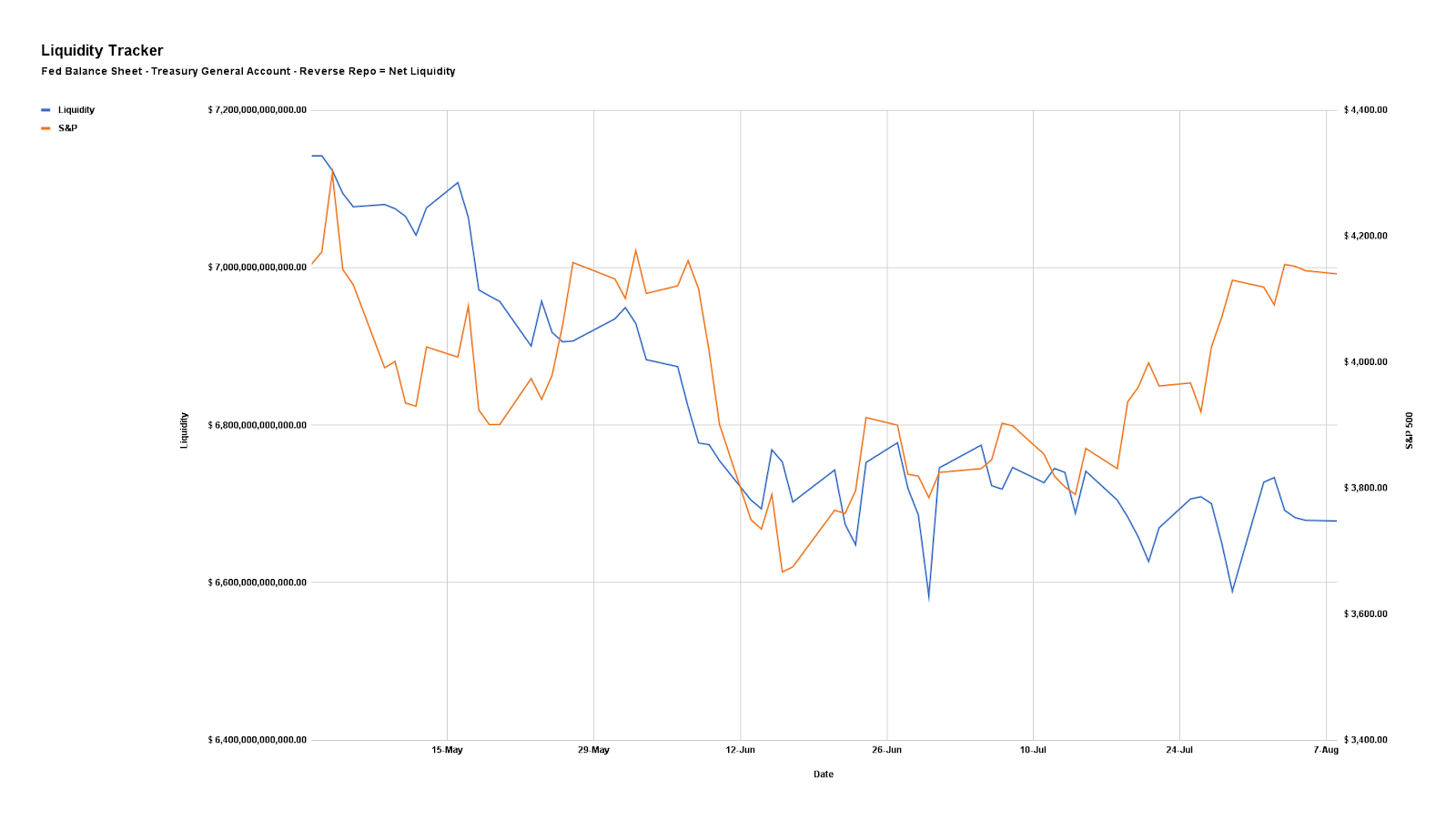

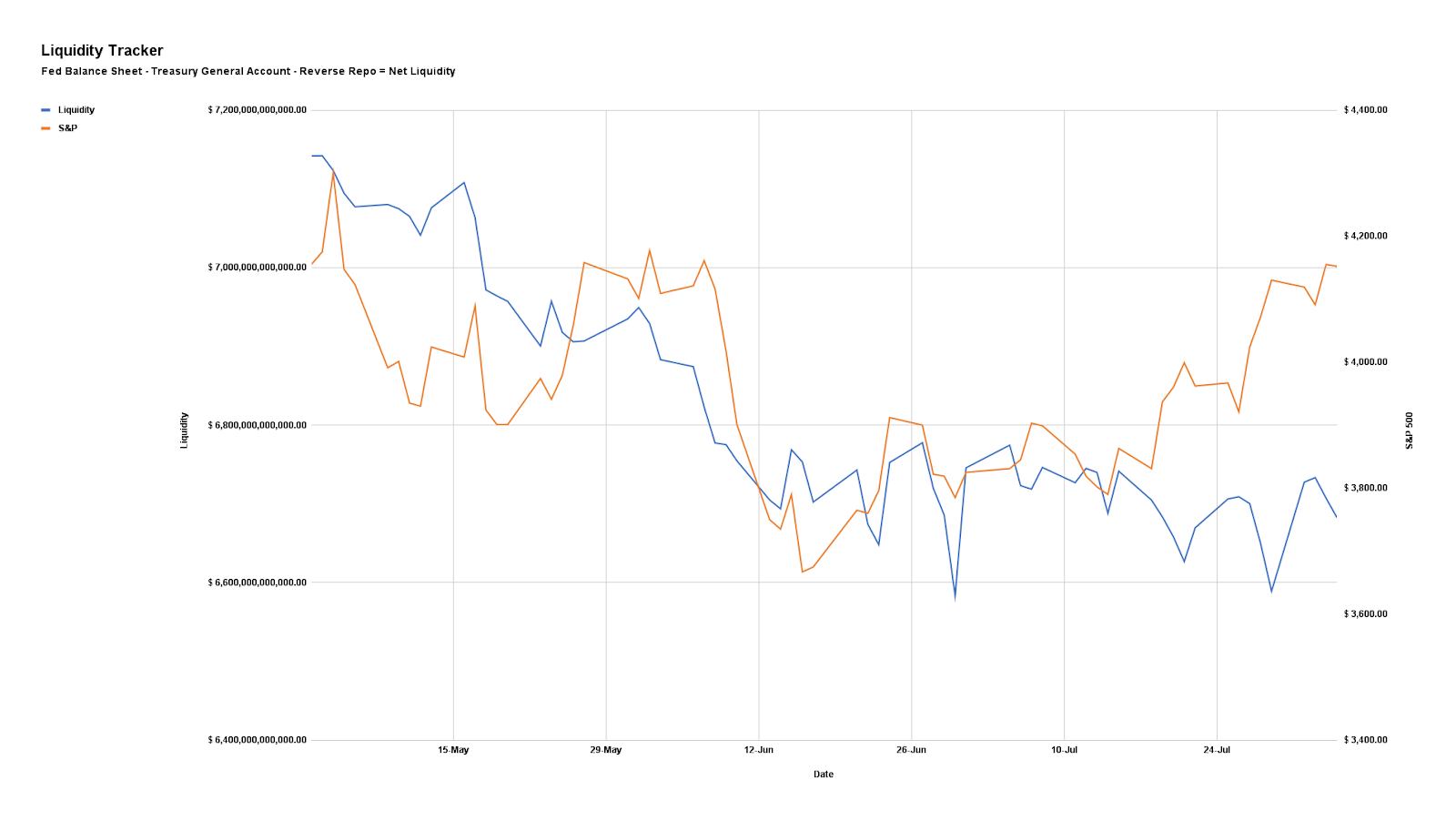

Notwithstanding, here’s our updated liquidity tracker that is monitoring the “preeminent driver of markets during the post-crisis decade.”

Graphic: Via Physik Invest. Data compiled by @jkonopas623. Fed Balance Sheet data, here. Treasury General Account Data, here. Reverse Repo data, here. NL = BS – TGA – RRP.

Positioning

As of 7:15 AM ET, Thursday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.04%. Net gamma exposures increasing may promote tighter trading ranges.

Given where realized (RVOL) and implied (IVOL) volatility measures are, as well as skew, it is beneficial to be a buyer of options structures (i.e., replacing static directional exposures or delta with those that are dynamic) tied to the broader measures we follow like the S&P 500 (given increased average stock correlation and lower return dispersion).

The reason why?

Per SpotGamma: “From an options perspective, a lot of the boost from volatility compression has played out. With implied volatility at a lower bound, it may be opportune to replace static delta bets for those that are dynamic (i.e., long option exposures) and have less to lose in this lower volatility environment.”

“In a case where market participants see the Fed keeping its commitment to aggressive monetary policy action, negative delta options exposures may outperform static short equity (bets on the downside).”

Technical

As of 7:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $4,227.75 HVNode puts into play the $4,253.25 HVNode. Initiative trade beyond the latter could reach as high as the $4,275.75 LVNode and $4,303.00 Weak High, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $4,227.75 HVNode puts into play the $4,203.00 VPOC. Initiative trade beyond the VPOC could reach as low as the $4,189.25 LVNode and $4,153.25 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 750+ that read this report daily, below!

Graphic updated 7:40 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Fundamental

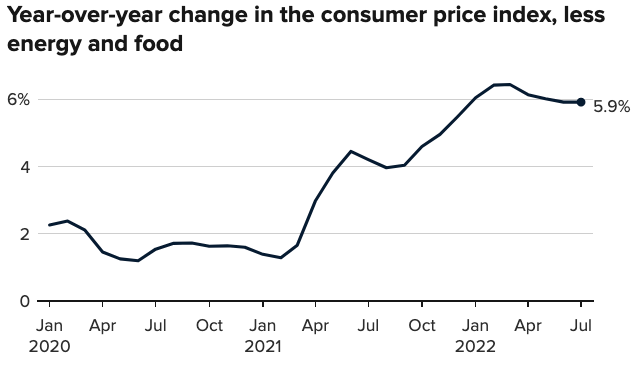

Wednesday’s inflation figures – the CPI (Consumer Price Index) – will help drive perceptions regarding future Fed activity.

Expected is an 8.7% rise year-over-year (YoY) and 0.2% month-over-month (MoM). In June, these numbers were 9.1% and 1.3%, respectively.

Core CPI (which excludes food and energy) is expected to rise by a rate higher than in June, 6.1% YoY and 0.5% MoM, respectively.

Mattering most is core inflation, which the Fed has more control over. If lower than expected, that may warrant some appetite for risk.

Over the last 6 months, immediately after the release of CPI data, the average movement in the S&P 500 was -1.27%.

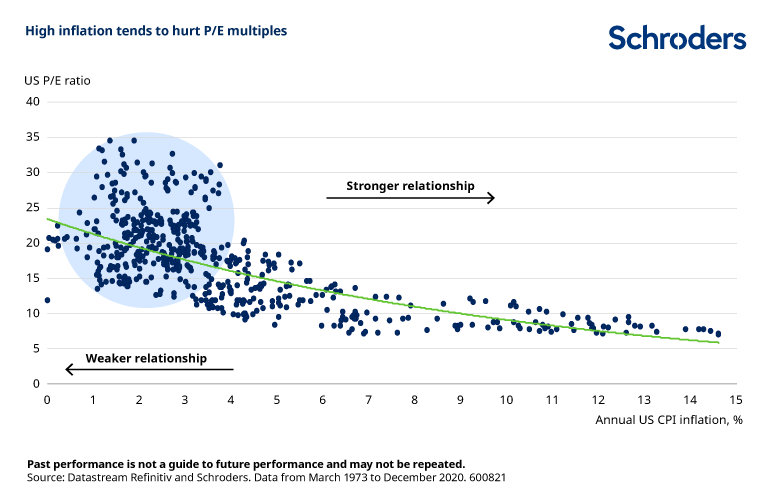

Moreover, businesses with promising futures often command a price high above their level of earnings (P/E). However, with inflation, prices in the economy rise, resulting in investors requiring better rates of return to maintain their purchasing power, per Investopedia.

Accordingly, if investors demand a higher rate of return, the P/E has to fall. That’s because you are “paying less for more earnings and, as earnings grow, the return you achieve is higher.”

Graphic: Retrieved from the Weekly S&P 500 ChartStorm. Via Schroders Plc (OTC: SHNWF).

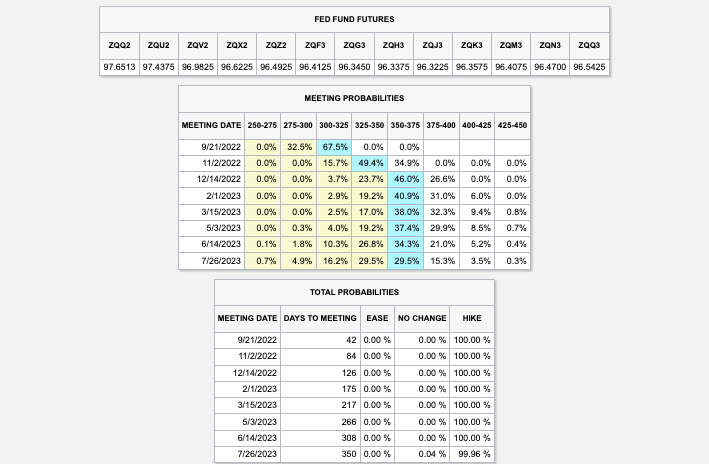

In response to much hotter inflation participants may make significant changes in their forecasts for action by the Federal Reserve (Fed).

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

To explain, to stem inflation, the Fed reversed its easy monetary policies and is both raising rates and engaging in quantitative tightening (QT), which amplifies the effects of the former and is the opposite of quantitative easing (QE), “widely seen as the preeminent driver of markets during the post-crisis decade.”

Those stocks commanding some of the highest prices in anticipation of future growth are (and will) be impacted the most as their discounted cash flows and ability to finance growth reduce.

Though “rates take up most attention,” what’s more important are “the decisions the Fed — and other central banks — have to make about bringing their balance sheets down,” per Bloomberg.

Graphic: Via Physik Invest. Data compiled by @jkonopas623. Fed Balance Sheet data, here. Treasury General Account Data, here. Reverse Repo data, here. NL = BS – TGA – RRP.

Positioning

As of 7:15 AM ET, Wednesday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.17%. Net gamma exposures decreasing may promote larger trading ranges.

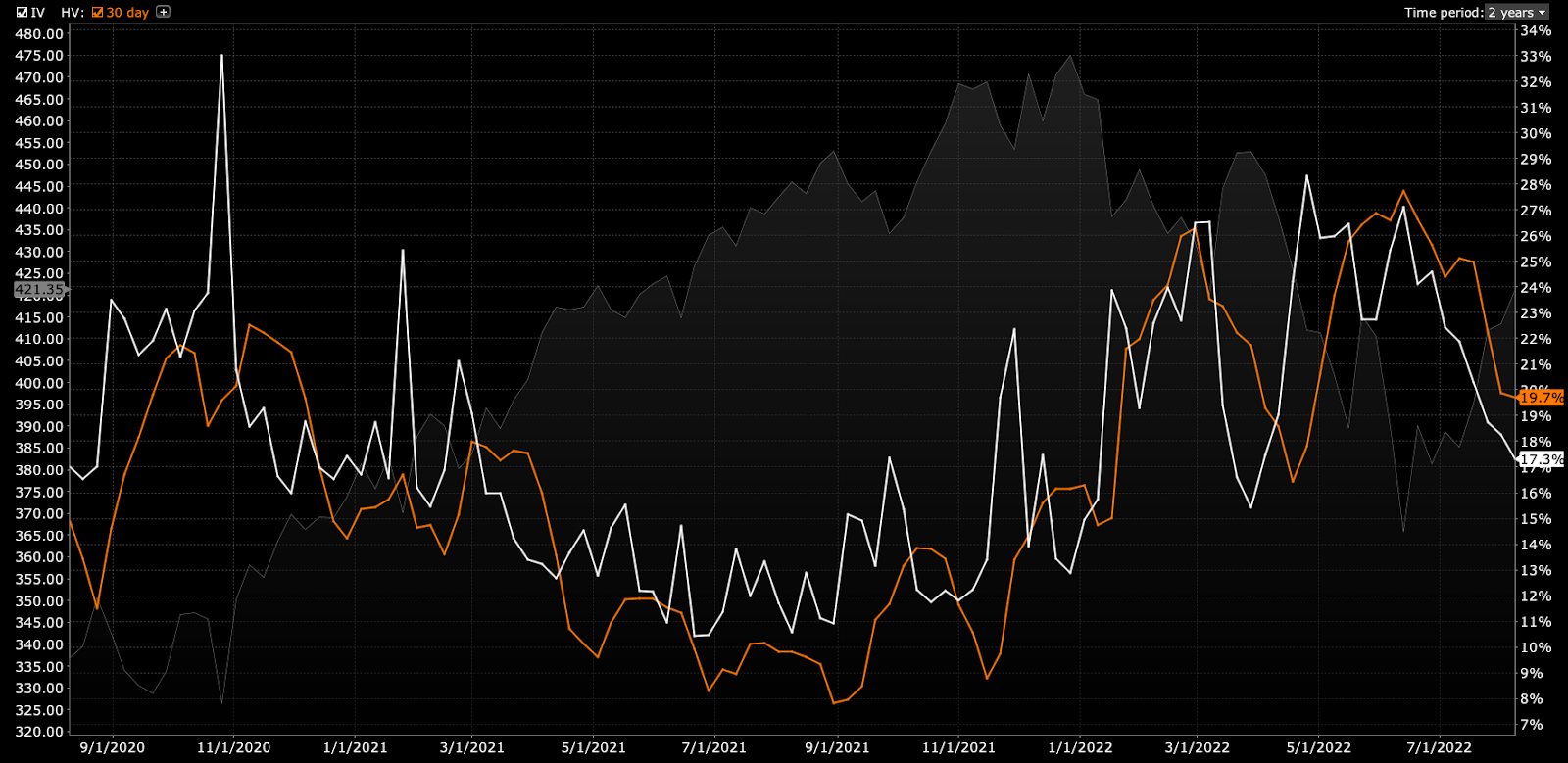

Adding, volatility is at a low point and the “flattening in the downside fixed strike skew” seems to have played its course.

As SpotGamma explains, “given that implied volatility is at a low point, if participants’ fears with respect to [CPI] are assuaged, volatility compression would likely do less to bolster equity market upside than when the VIX was at a higher starting point (e.g., 30).”

On the other hand, “the marginal impact of increased demand for options strikes down below, further out in time, is likely to do a lot to add to underlying market pressures.”

So, per Kai Volatility’s Cem Karsan, though the first market moves after CPI may be a “function of inevitable rebalancing of dealer inventory post-event,” if the “final resolution is lower,” per “the incremental effects” of liquidity (i.e., QE and QT), then options could outperform their delta (i.e., exposure to direction), not like what happened over the past half-year, as said August 5.

Sample structures to consider include low- or zero-cost bullish call ratio spreads to the upside, against the trend resistances in products like the S&P 500 (INDEX: SPX).

Graphic: Retrieved from Bloomberg. Drawn on by Physik Invest.

Technical

As of 7:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity, all else equal.

In the best case, the S&P 500 trades higher.

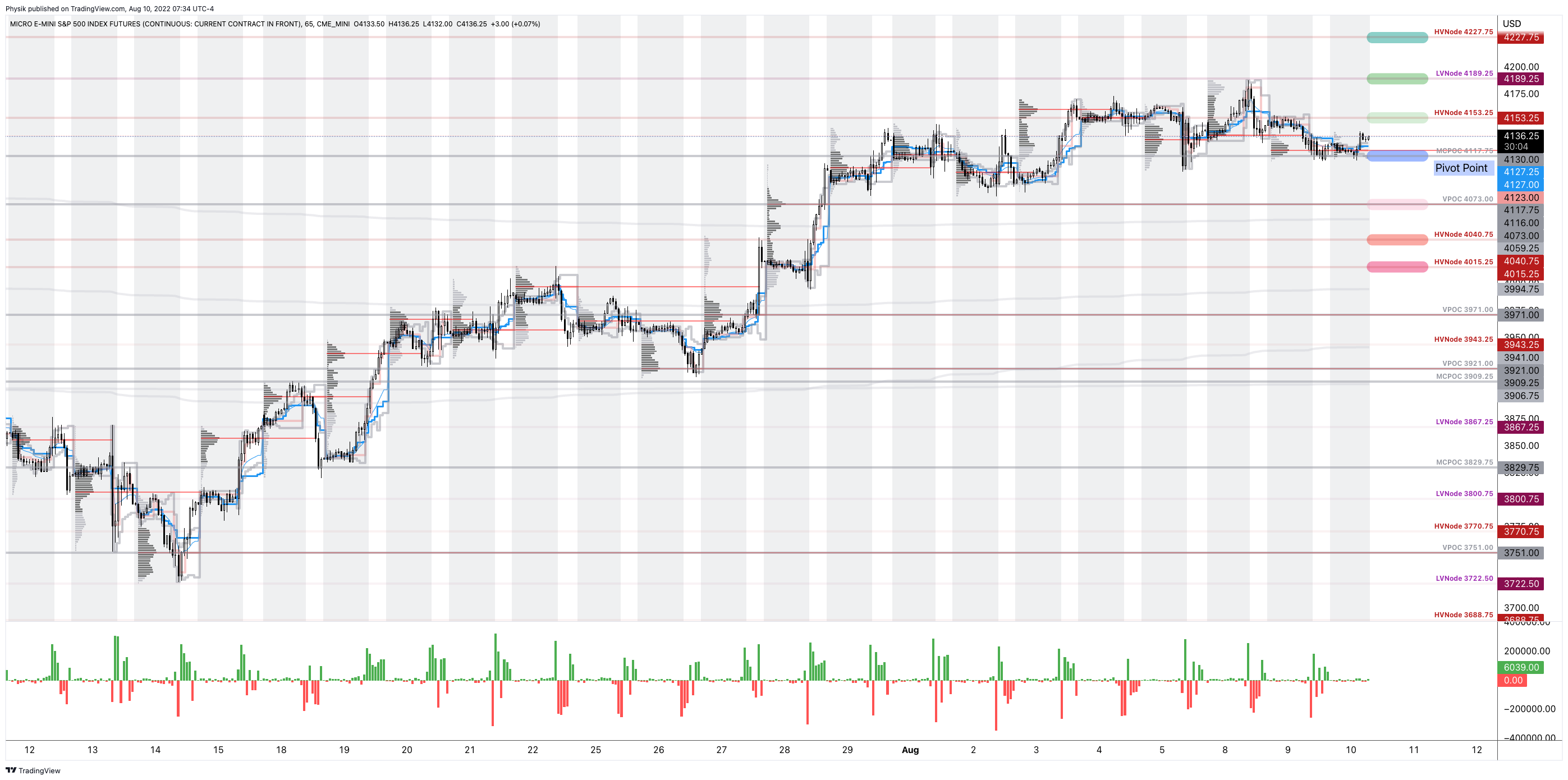

Any activity above the $4,117.75 MCPOC puts into play the $4,153.25 HVNode. Initiative trade beyond the HVNode could reach as high as the $4,189.25 LVNode and $4,227.75 HVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $4,117.75 MCPOC puts into play the $4,073.00 VPOC. Initiative trade beyond the VPOC could reach as low as the $4,040.75 and $4,015.25 HVNodes, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 750+ that read this report daily, below!

Graphic updated 7:45 AM ET. Sentiment Risk-On if expected /ES open is above the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Fundamental

In a non-farm payroll update, it was shown that the US added more than two times the jobs many economists thought it would.

“Some of this is driven by a reduced participation rate – a smaller portion of the population seeking work and showing up in unemployment data,” Bloomberg’s John Authers explained.

Graphic: Retrieved from Bloomberg.

“It now becomes much easier for the Federal Reserve (Fed) to [continue] rais[ing] rates. If the employment market is still strengthening, while inflation remains its highest in decades, it’s hard to see why it shouldn’t.”

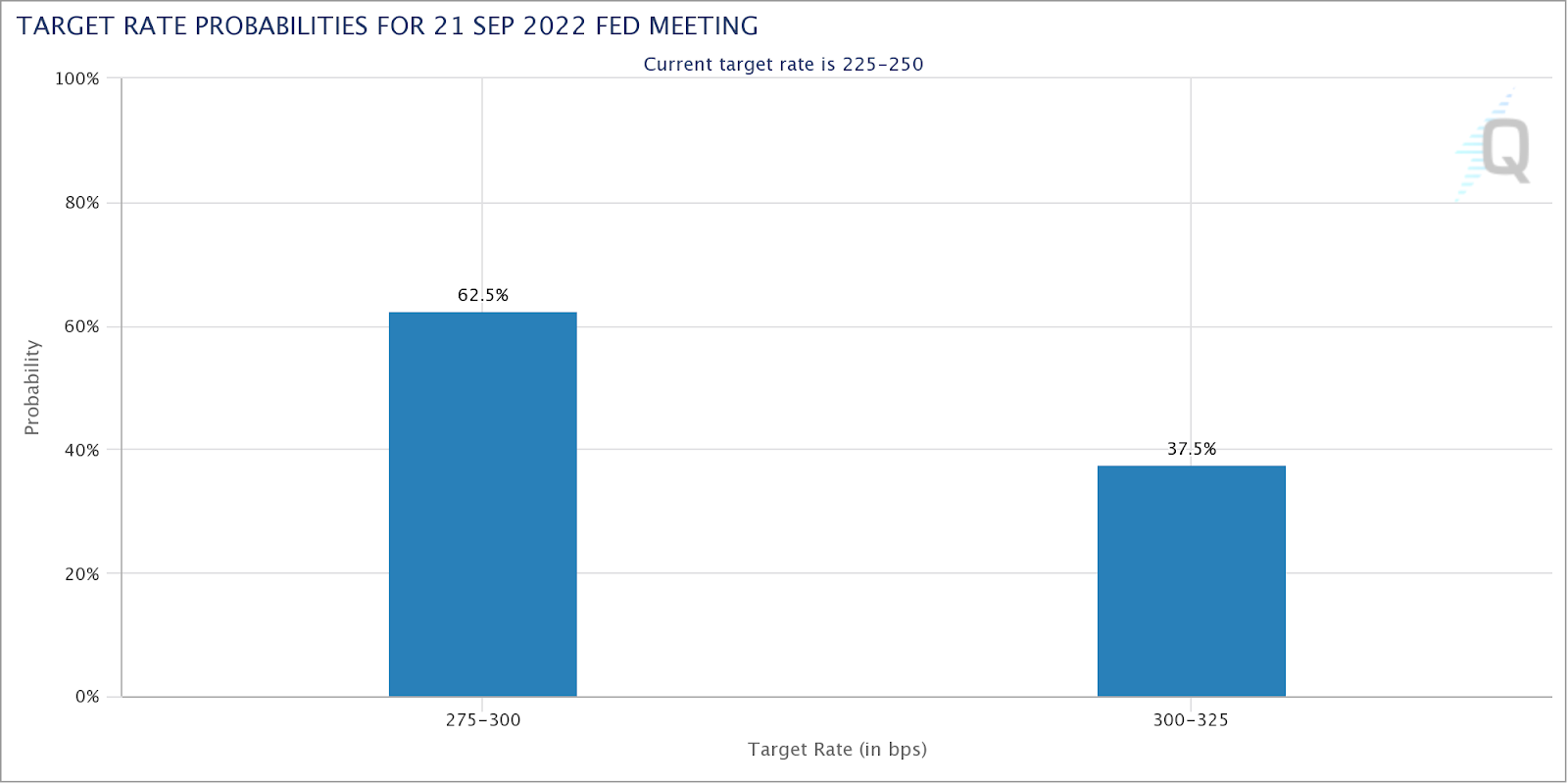

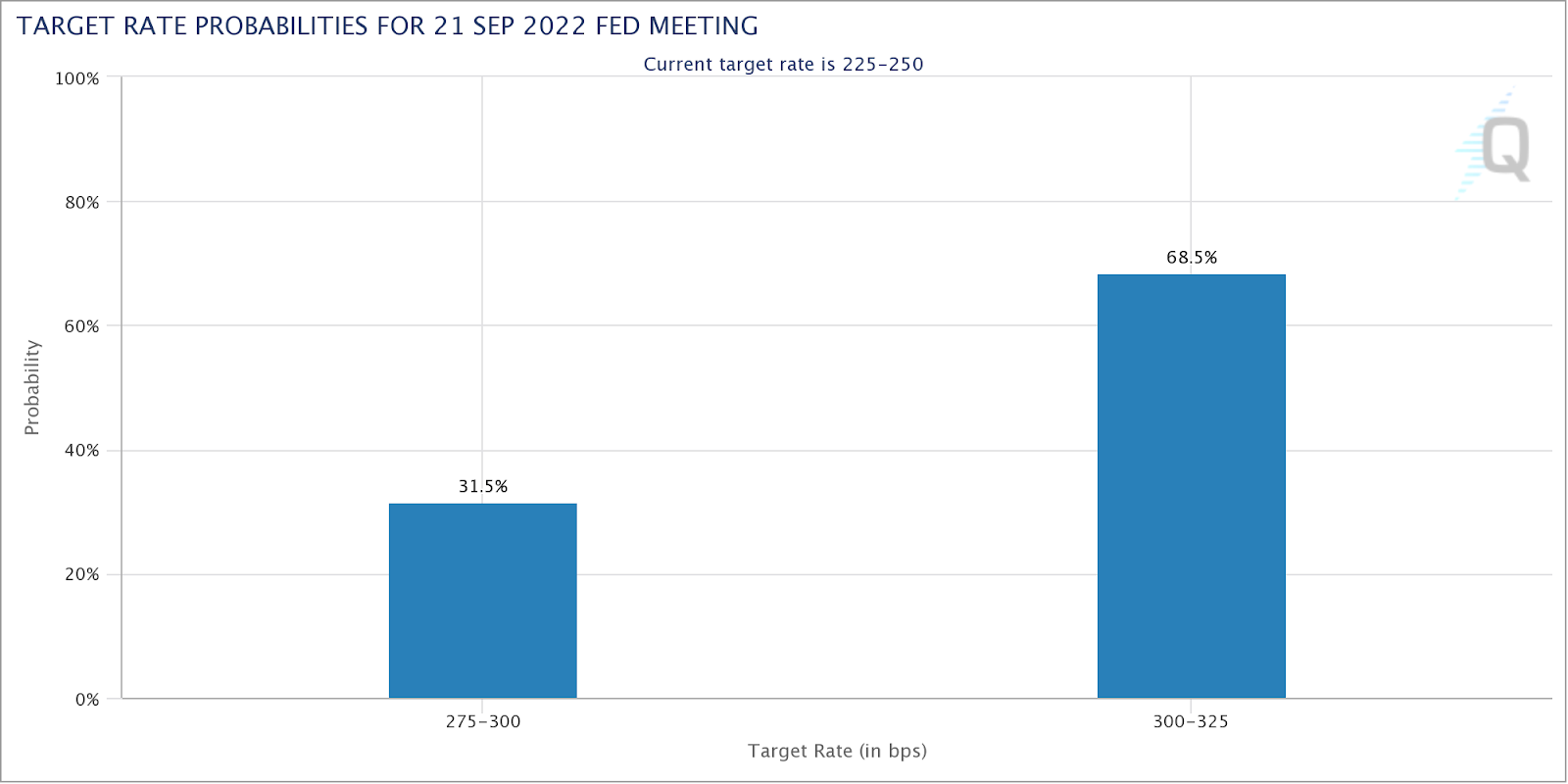

Accordingly, market participants are pricing a greater than 50% chance of the target Fed Funds rate increasing by 75 to 100 basis points to a target range of 300 and 325 basis points, up from 225 and 250 right now.

Graphic: Retrieved from CME Group Inc’s (NASDAQ: CME) FedWatch tool.