The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures auctioned sideways to higher after their late-day liquidation and break from a multi-day consolidation area on technical factors (e.g., options expirations) among other things, potentially, like the increase in personal consumption expenditures.

Broadly speaking, the narrative that investors are showing some concern over the economic outlook, with respect to geopolitical tension and monetary policy, continues to emanate.

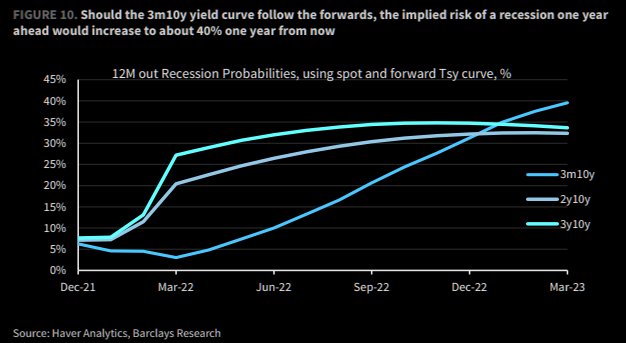

U.S. high-grade bonds shed over 5%, booking the worst quarterly performance since the ‘80s. This is as recession risks have risen more than two-fold.

Notwithstanding, the Federal Reserve’s (Fed) favorite yield curve metric remains steep; per a Bloomberg commentary, “the gap between the three-month bill rates and 10-year yields is the ‘most useful term spread for forecasting recessions,’ … [and] it currently stands at 186 basis points, versus negative 2 basis points on 2s10s.”

In terms of news, the U.K. will join the U.S. in releasing oil from its reserves to lower prices and reduce its reliance on external partners. This helped ease futures calendar spreads on oil, Reuters’ John Kemp said in a newsletter to followers; the “six-month spread [narrowing] to a backwardation of $9 per barrel, the lowest since before Russia’s invasion of Ukraine.”

Ahead is data on nonfarm payrolls, the unemployment rate and average hourly earnings, as well as labor-force participation (8:30 AM ET). Thereafter, the Chicago Fed’s Charles Evans is scheduled to speak (9:05 AM ET).

Later is Markit manufacturing PMI (9:45 AM ET), as well as ISM manufacturing index and consumer spending data (10:00 AM ET).

What To Expect

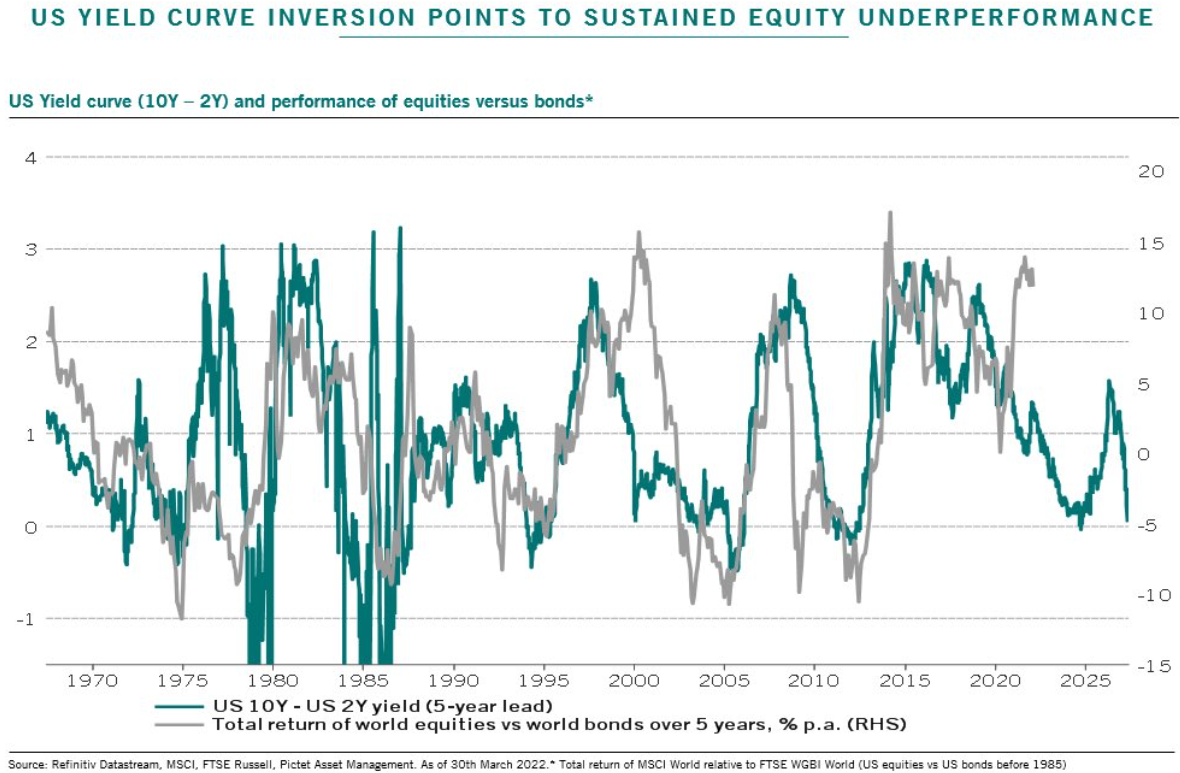

Fundamental: The S&P 500 bagged its first quarterly loss in two years as recession probabilities, implied by some yield curves, have risen.

This is as the stock performance, relative to bonds against the lagged spread of 10- and 2-year bond yields, is expected to be weak, according to insights by Pictet Asset Management.

Pictet’s narrative further validates some of the theses shared by institutions like Brevan Howard Asset Management, which is having one of its best years, Morgan Stanley (NYSE: MS), Goldman Sachs Group Inc (NYSE: GS), and Bank of America Corporation (NYSE: BAC).

Adding to the prospects for weaker earnings amid higher costs, among other things, some of these institutions see the potential for the Fed’s terminal rate to reach between 3% and 3.25%.

This would hit valuations as higher yields both reduce the present value of future earnings and “hurt those carrying the highest leverage,” potentially playing into a slowdown or recession.

“Now rates volatility can drive growth volatility and that actually becomes a vicious cycle between the two,” said Christian Mueller-Glissmann of Goldman Sachs.

“That’s a big difference to the last cycle where growth volatility drove rates volatility.”

However, this is as the dominance of rate-sensitive tech stocks is set to shrink next year amid sector reclassifications, as well as still-stimulative policy and beats of economic expectations that may feed into earnings surprises, later.

JPMorgan’s Marko Kolanoivc explains that (1) “both equity and credit markets have historically fared well at the start of monetary tightening cycles,” (2) “the real policy rate is extremely negative and thus stimulative,” and (3) “not all central banks are tightening.”

Morgan Stanley’s Michael Wilson vehemently disagrees suggesting the recent equity market turnaround “was nothing more than a vicious bear market rally,” and offers participants a clear opportunity to sell at better prices.

Taking all of the above comments and perspectives together, one thing is for certain: this period in history is like no other. It makes sense to pick a timeframe and stick with it.

Positioning: In the past weeks, according to JPMorgan Chase & Co’s Nikolaos Panigirtzoglou, the supportive “rebalancing flows away from bonds into equities” are no more and, therefore, equities are subject to increased vulnerabilities “if bond yields continue to rise.”

This is after measures of equity implied volatility were crushed heading through the mid-March FOMC and monthly options expiry (OPEX) events, and the options hedging impact of this, at least, was very supportive, as we’ve talked about many times in this newsletter.

On the contrary, measures of volatility for other assets, like the Merrill Lynch Options Volatility Estimate (INDEX: MOVE), a useful measure of bond market sentiment, are doing the opposite.

We discussed early last month, what we saw was an increased supply of equity market volatility, as a potential reason for some of these divergences.

As Bloomberg’s John Authers explained well, it, too, could have been “an aggressive central bank” that prompted a move out of bonds and into equities, and subdued target-date fund rebalancing flows which usually sell stocks and buy bonds.

“[I]t looks as though the contradictions that had built up in the market over the last two years, and in the decade before that, are being put under extreme stress by the double whammy of a newly aggressive Federal Reserve, and the worst geopolitical shock in decades,” Authers adds.

Still, realized volatility continues to trend down which ought to force those (e.g., computer-driven traders) who position (and size equity exposure) based on underlying volatility to load up, again.

Nomura Holdings Inc’s (NYSE: NMR) Charlie McElligott explains that “volatility-targeting funds and trend-following commodity trading advisers, purchased” billions of equity futures which bolstered the price rise of the last weeks.

From a positioning versus buying support perspective, the forward returns distribution is skewed positive but not by a lot; a lot of the supportive options exposure is rolling-off and this could free up (i.e., unpin) indexes for the next leg up or down.

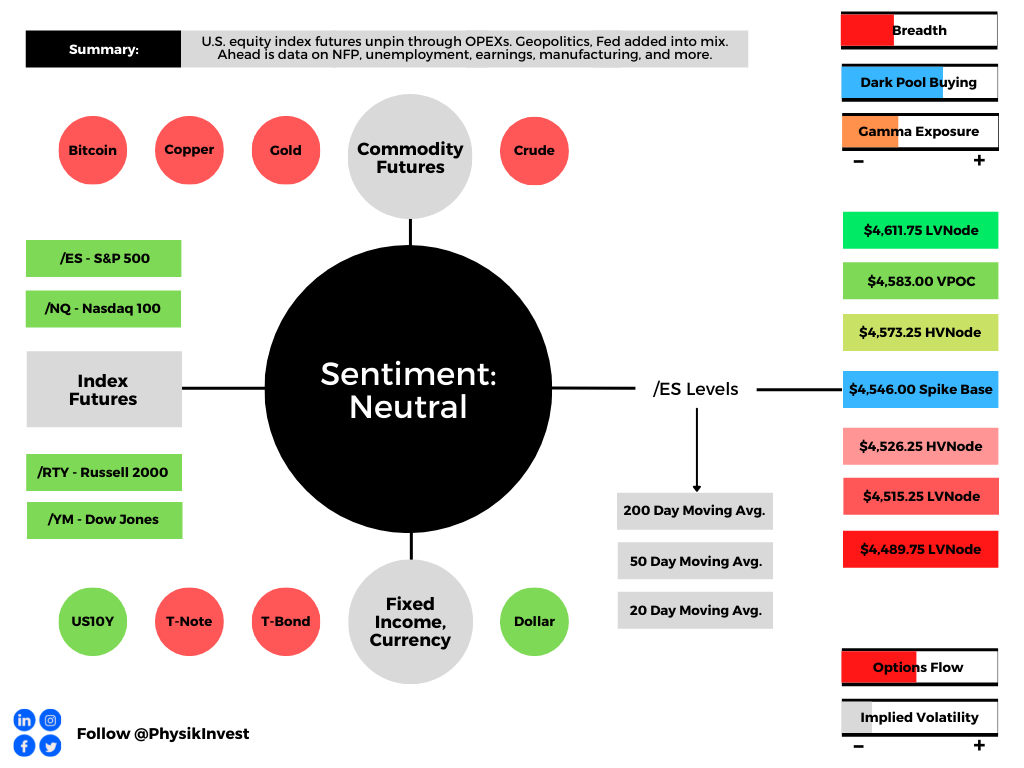

Technical: As of 6:30 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,546.00 spike base puts in play the $4,573.25 high volume area (HVNode). Initiative trade beyond the HVNode could reach as high as the $4,583.00 untested point of control (VPOC) and $4,611.75 low volume area (LVNode), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,546.00 spike base puts in play the $4,526.25 HVNode. Initiative trade beyond the HVNode could reach as low as the $4,515.25 and $4,489.75 LVNodes, or lower.

Considerations: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) occurred.

Continue to monitor for acceptance outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance. See the below graphic for more.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Marks change in dealer gamma exposure.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

One reply on “Daily Brief For April 1, 2022”

[…] After quarterly rebalances and options expiries, the reduction in counterparty exposure to positive gamma freed indexes (i.e., unpinned), as expected. […]