The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 850+ that read this report daily, below!

Fundamental

Please pardon the light letter, team.

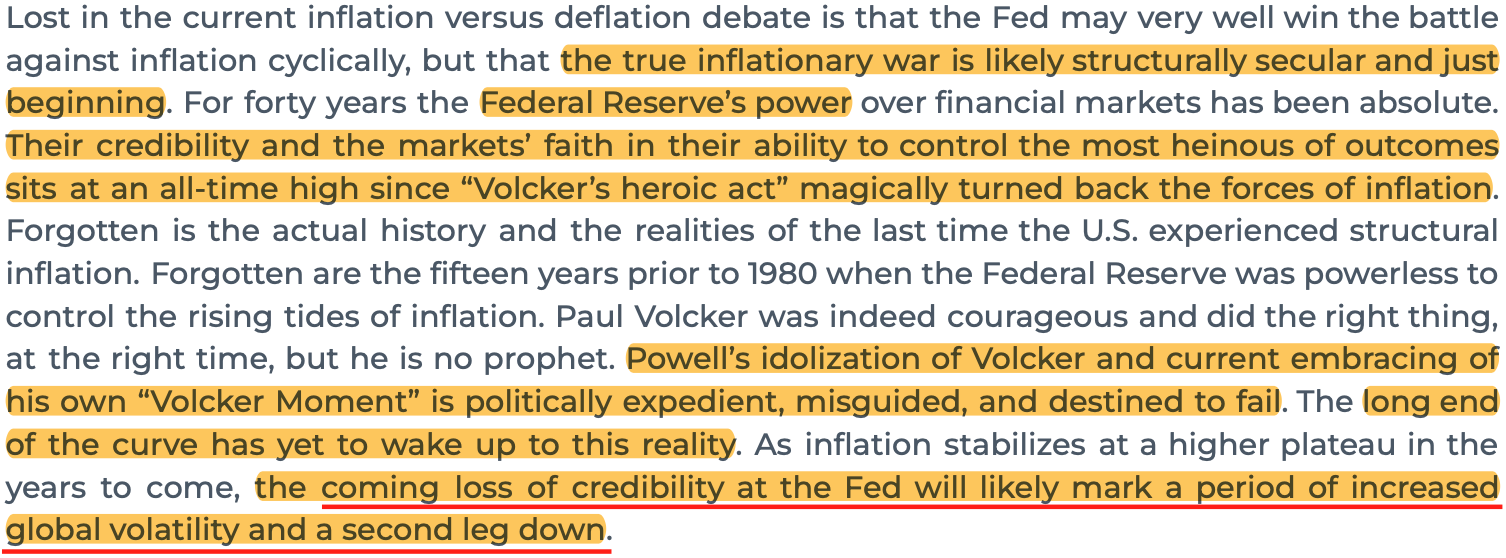

The Federal Reserve (Fed) Chair Jerome Powell will speak on monetary policy today at 9:10 AM ET. He is likely to embolden the tone set forth yesterday by the Fed’s Lael Brainard who said that higher rates for far longer seem necessary at this juncture.

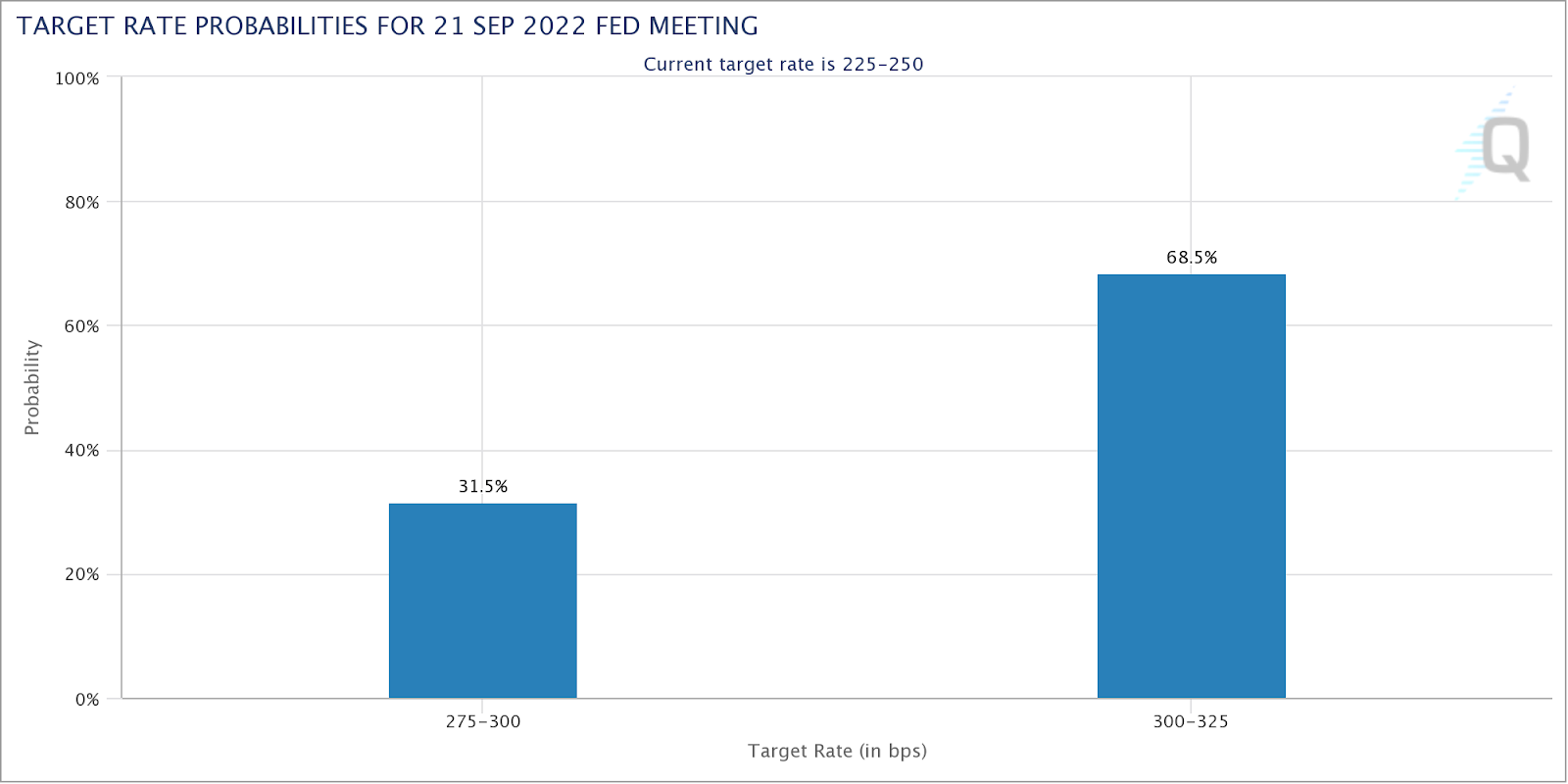

The base case calls for a 75 basis point hike to interest rates this month, followed by 50 basis points in November, according to Goldman Sachs Group Inc (NYSE: GS) forecasts.

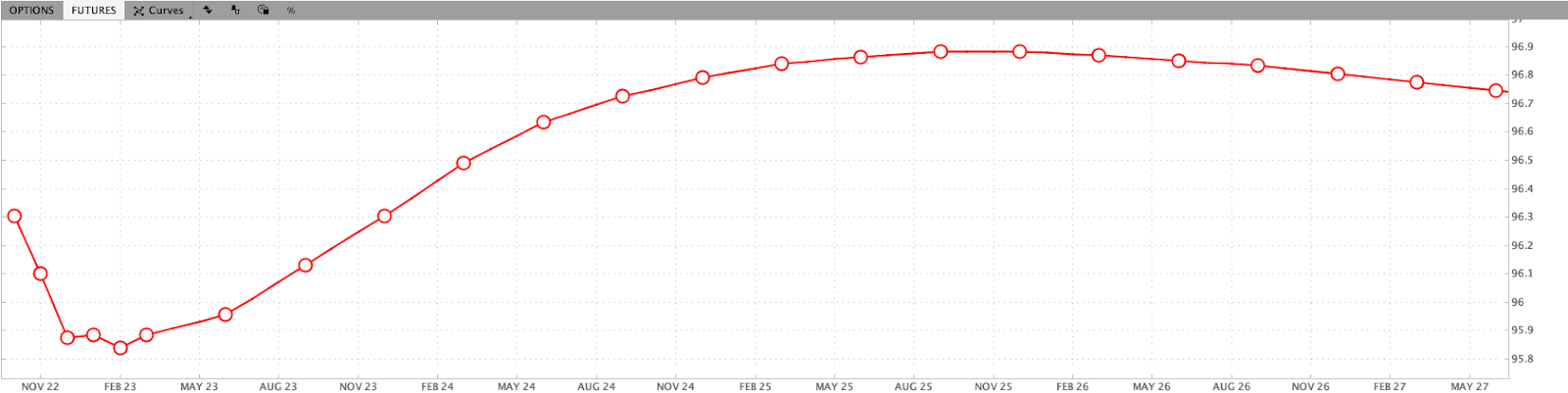

A quick check of the Eurodollar – which reflects the interest offered on U.S. dollar-denominated deposits held at banks outside of the U.S. (i.e., participants’ outlook on interest rates) – shows a peak in the overnight rate at 4.155% in February of 2023. From thereon, rate cuts are implied.

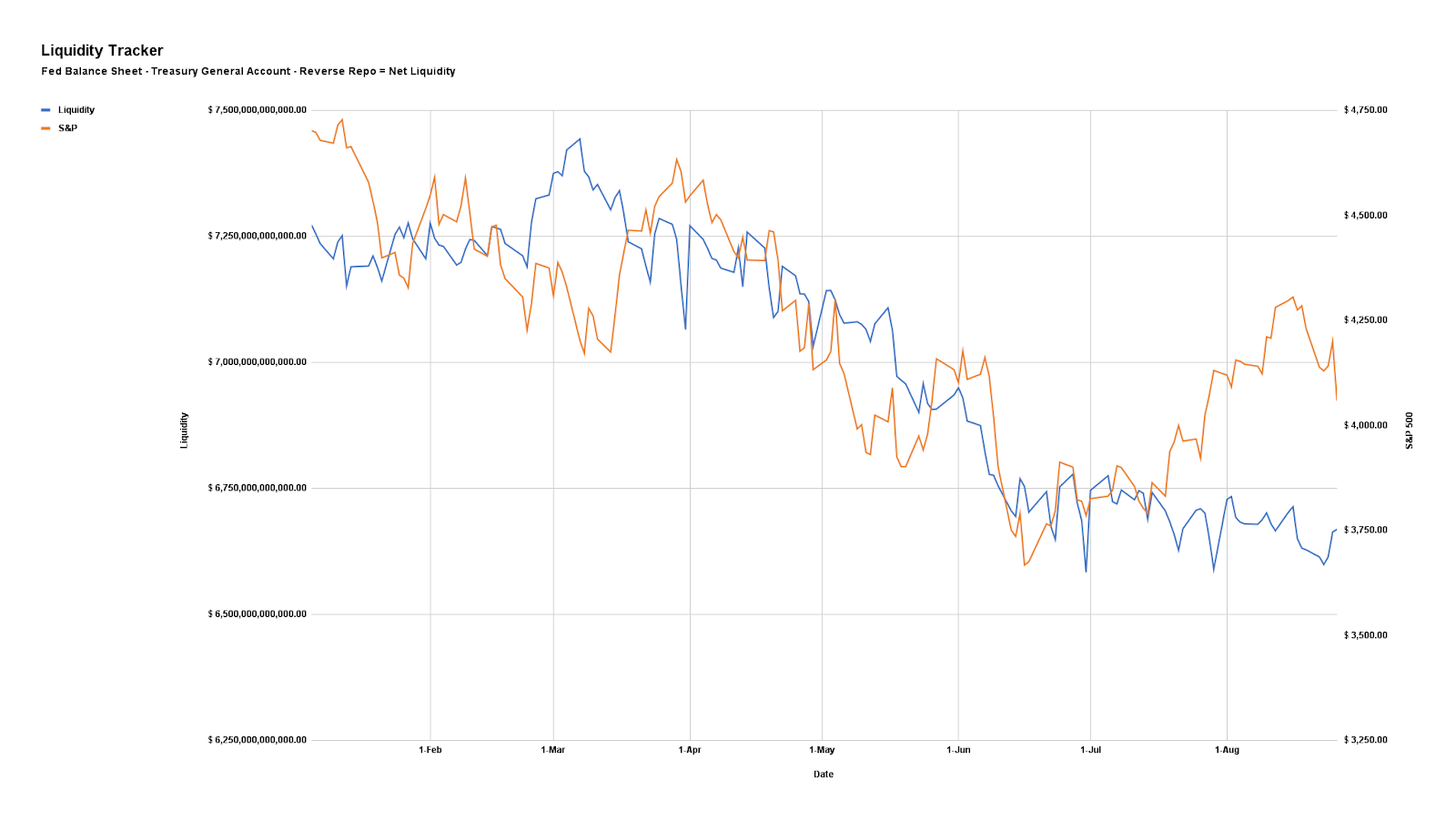

It’s the case that monetary policies implemented resulted in too many dollars (still) chasing too few goods. We spoke on supply side dislocations last week and put forth that, from a monetary perspective, the Fed, among its peers like the ECB, can only and will tighten to stem inflationary pressures that are (to remain) structural.

It is the case that the economy is on a path that is “L”-shaped (i.e., vertical drop in activity via recession, and flatline for a period of time as rates remain higher for longer to prevent a sharp rise in inflation, again).

Zoltan Pozsar of Credit Suisse Group AG (NYSE: CS) puts forth that policymakers now have to “generate a round of negative wealth effects to lower demand such that it becomes more in line with the new realities of supply.”

Technical

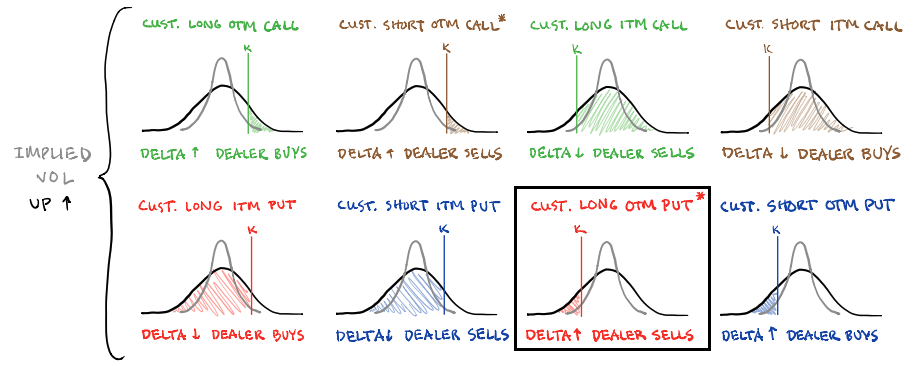

Implied volatility (IVOL) is wound and markets are in an environment characterized by two-way ranges that are larger. Yesterday, we unpacked one way traders could have played the entry into this environment.

Further, as SpotGamma puts it well, a positive response to Powell’s remarks, into and through events such as the next update on consumer prices and the Federal Open Market Committee (FOMC) meeting, opens the door to IVOL compression and this would be “a boost for equities.”

That’s because the Delta risk counterparties are exposed to by holding short put options, for instance, reduces with falling IVOL. Accordingly, since the short puts carry less positive Delta, the counterparty reduces its negative Delta exposure via the underlying future or stock, which can support markets.

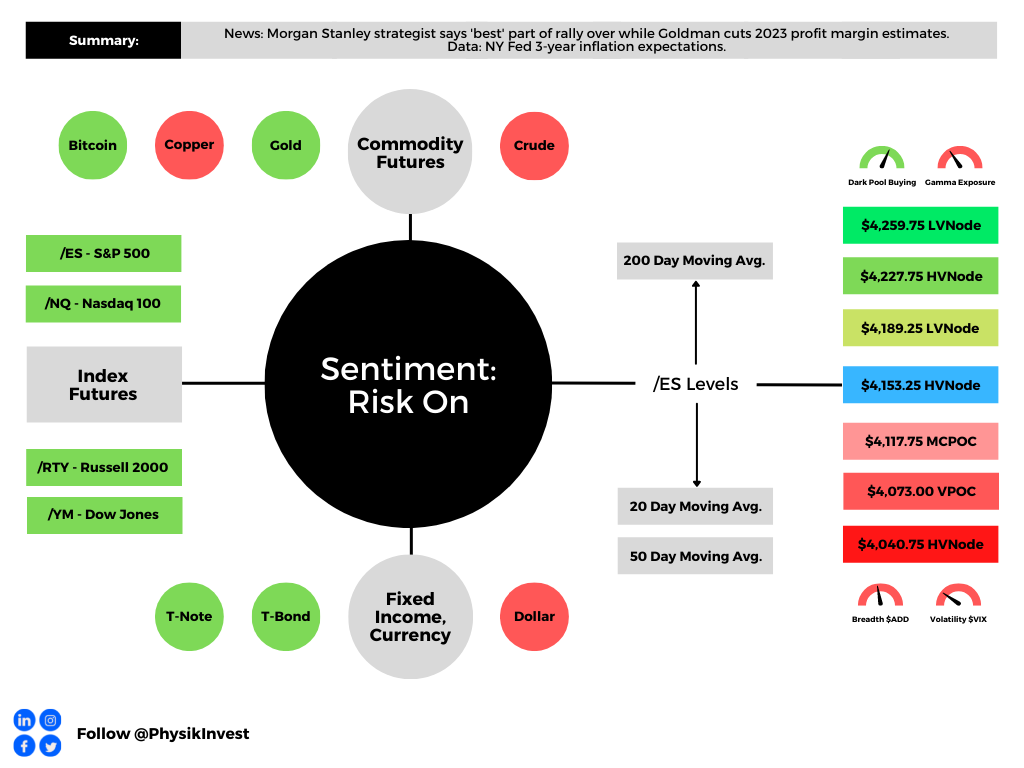

Technical

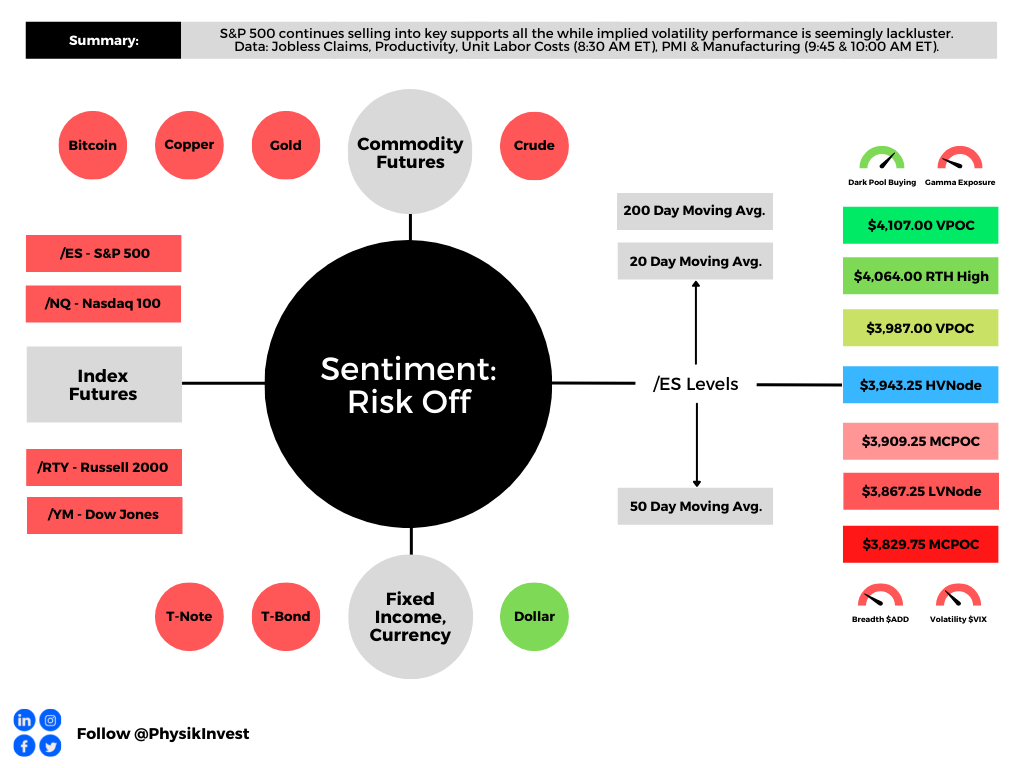

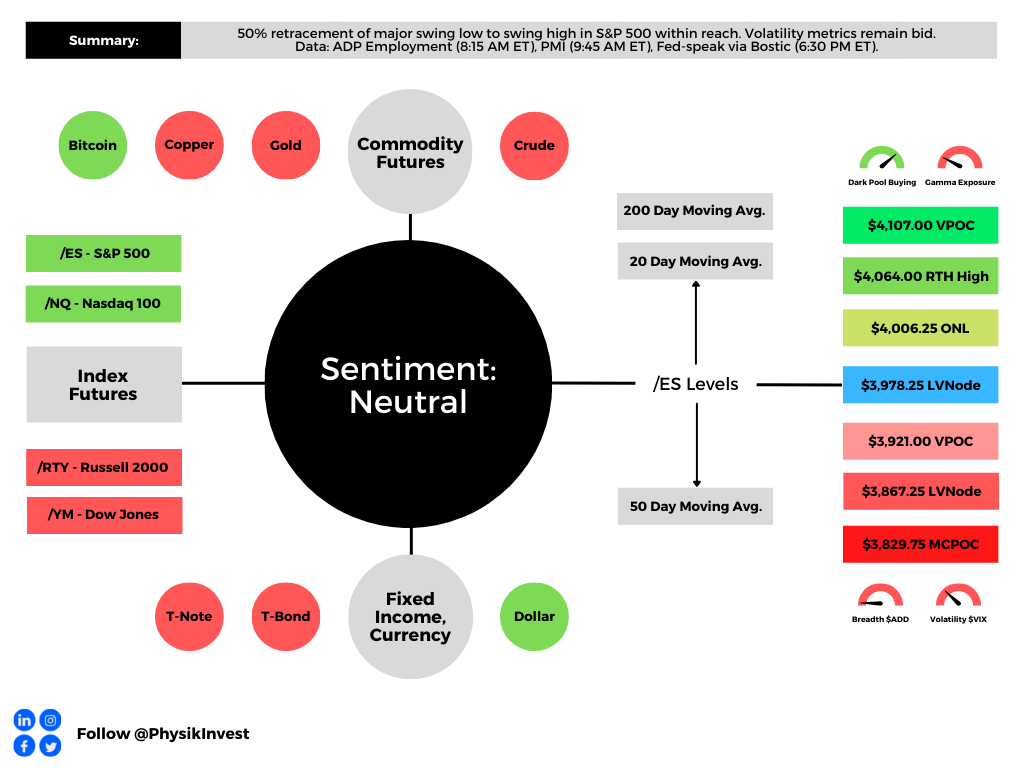

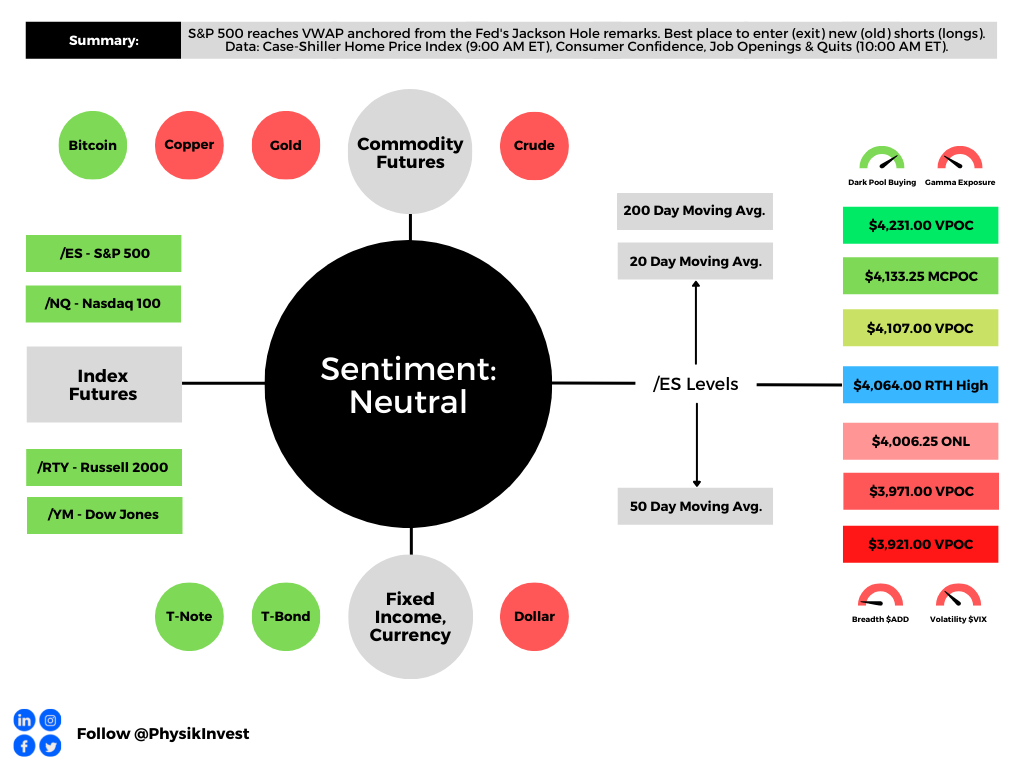

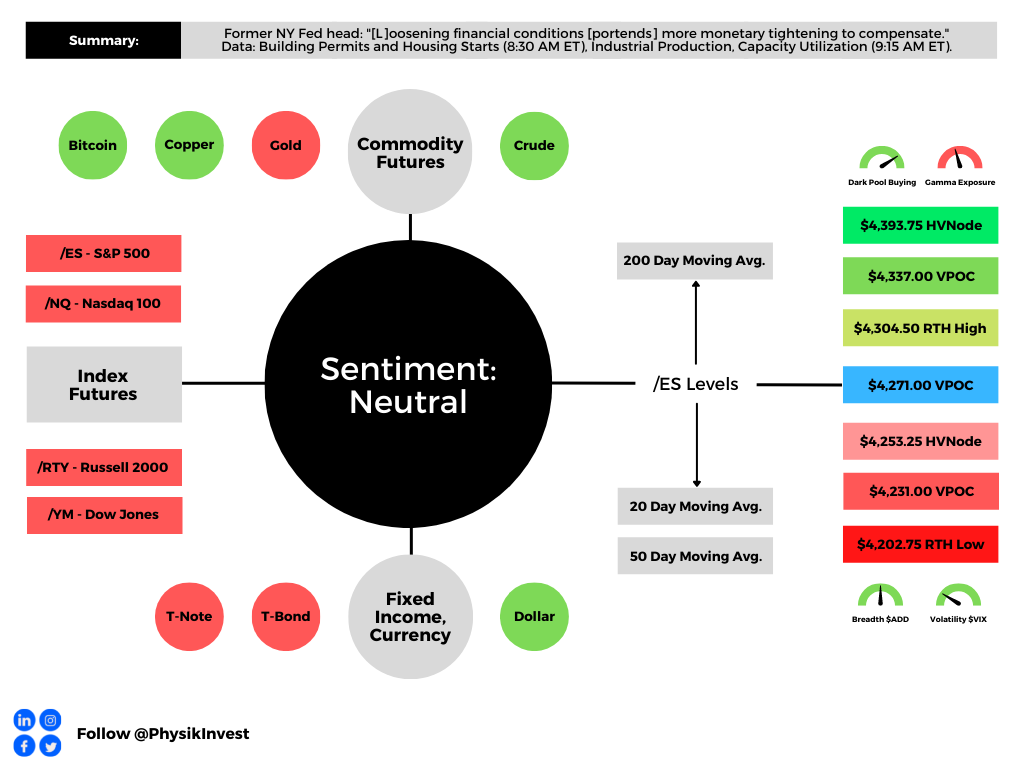

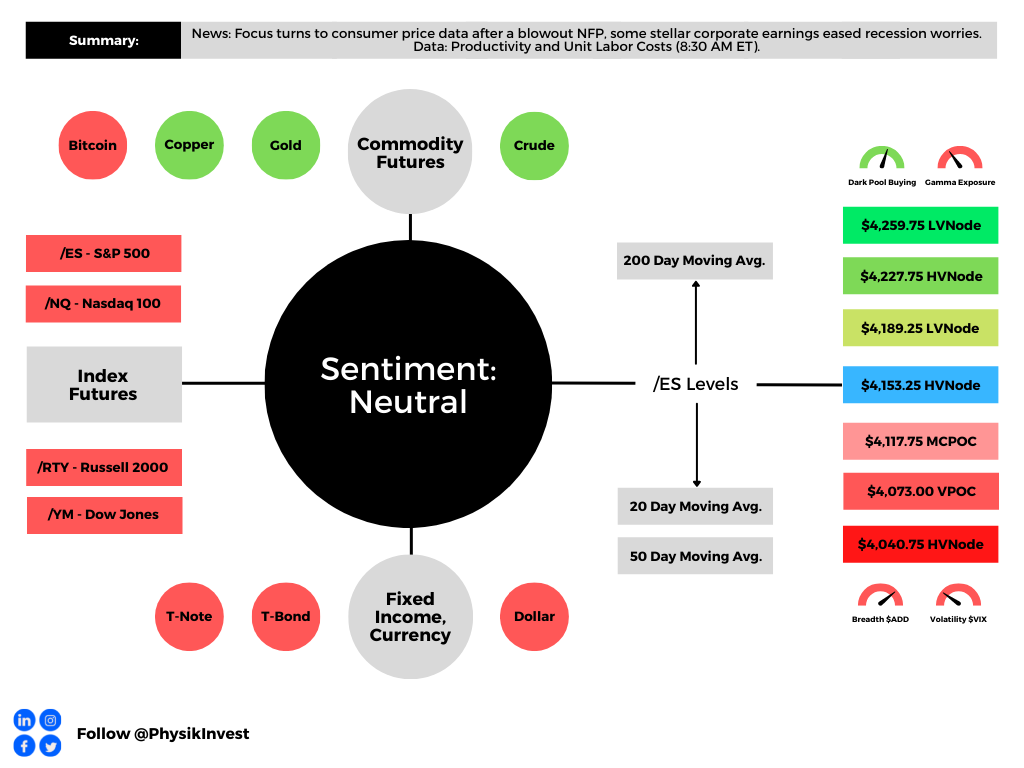

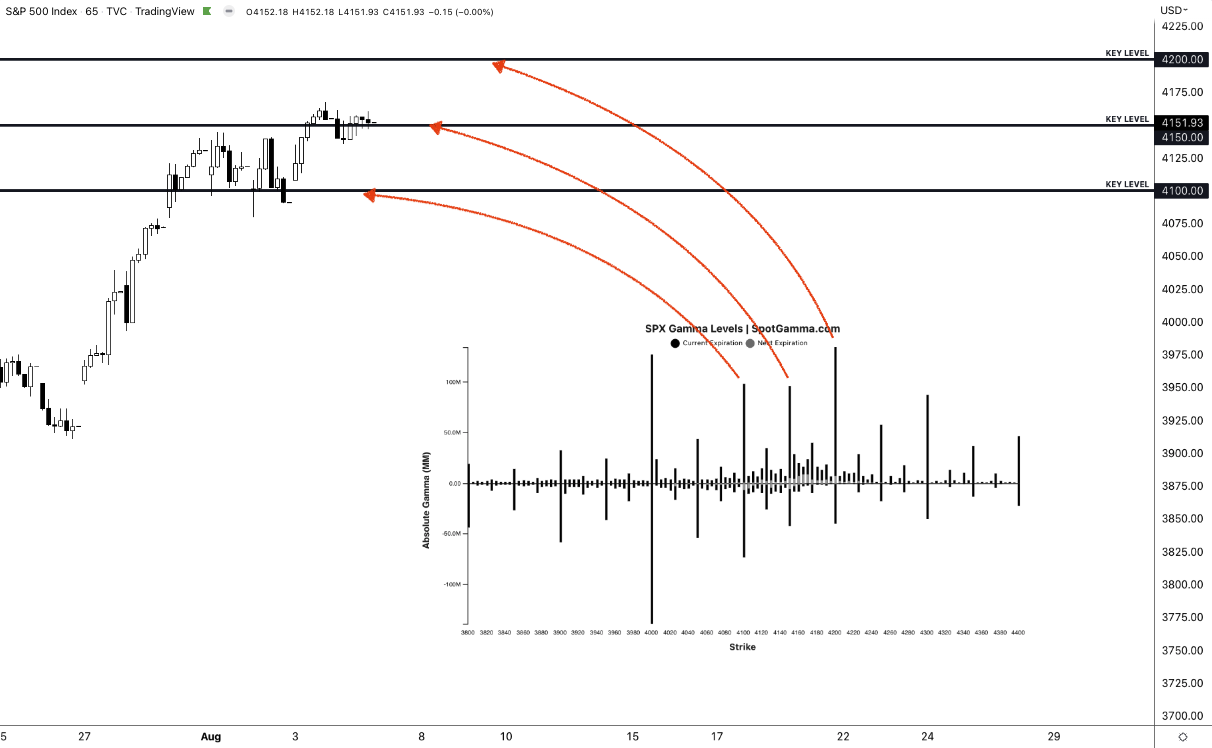

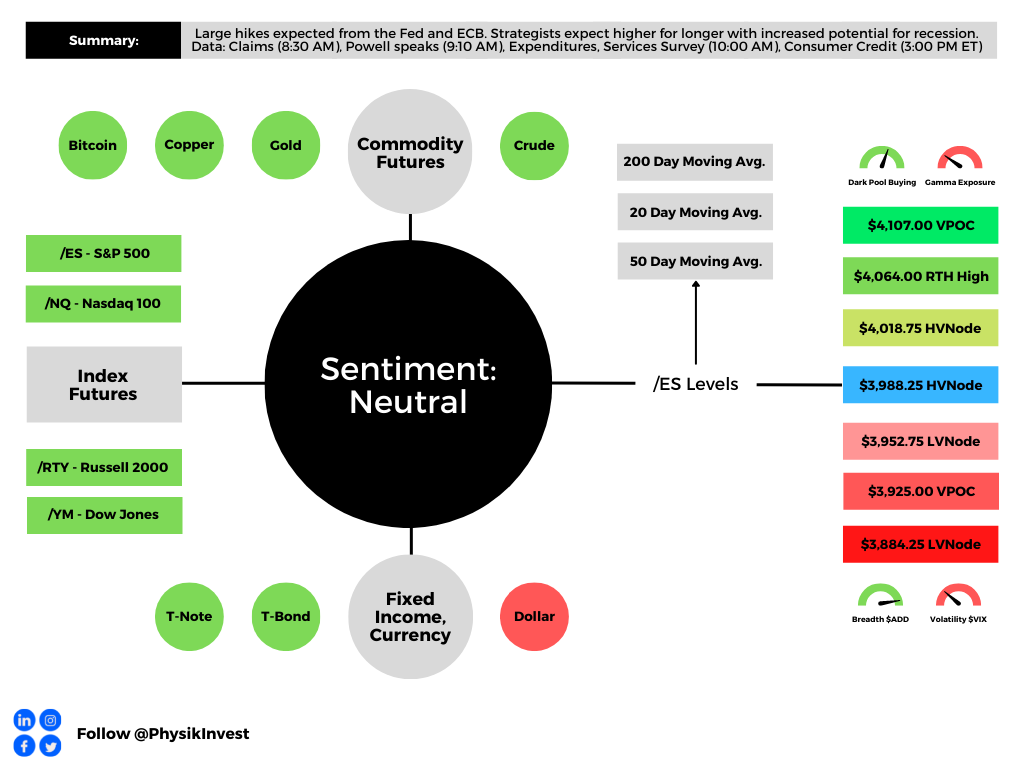

As of 7:15 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,988.25 HVNode puts into play the $4,018.75 HVNode. Initiative trade beyond the latter could reach as high as the $4,064.00 RTH High and $4,107.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,988.25 HVNode puts into play the $3,952.75 LVNode. Initiative trade beyond the LVNode could reach as low as the $3,925.00 VPOC and $3,884.25 LVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.