The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

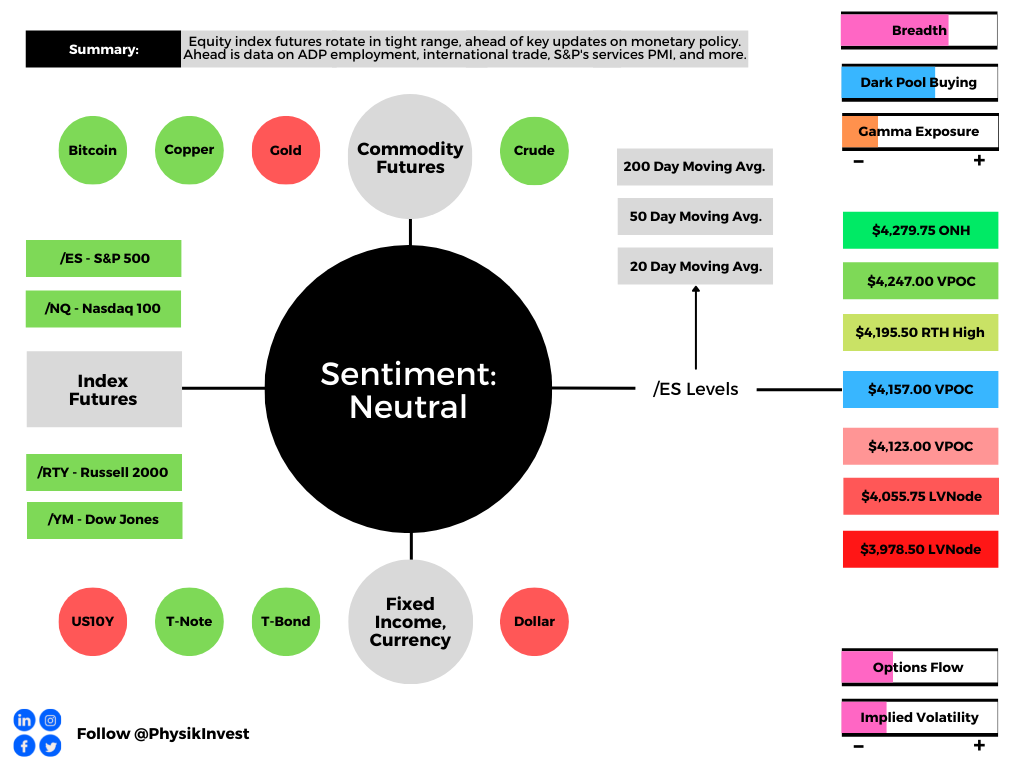

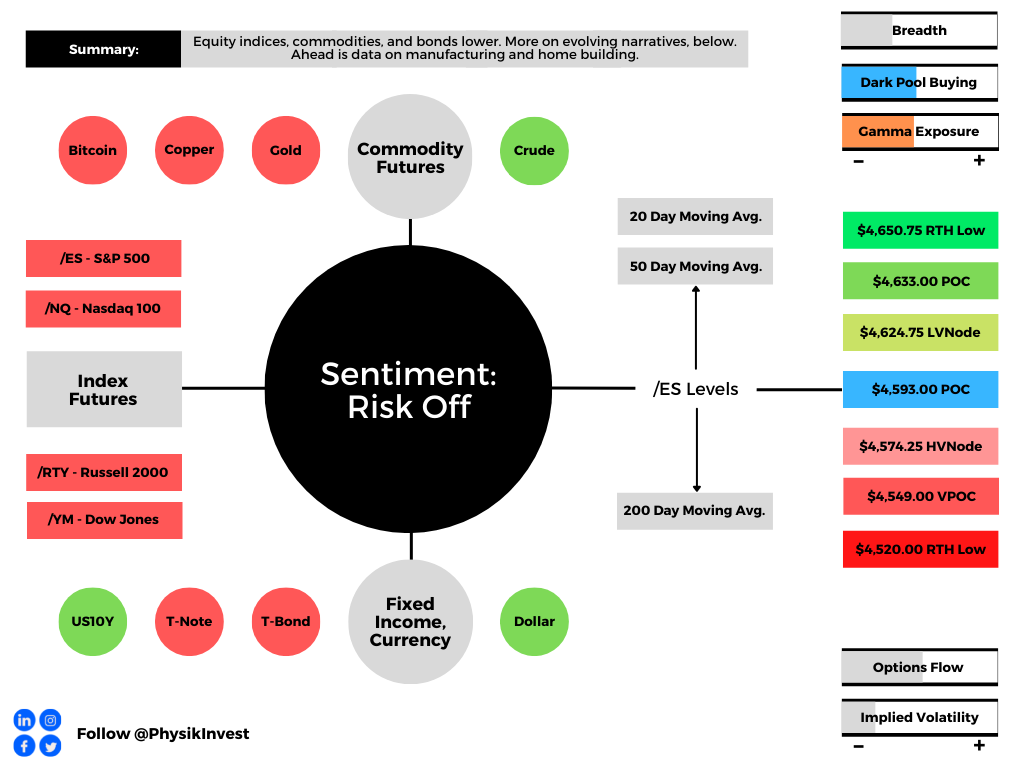

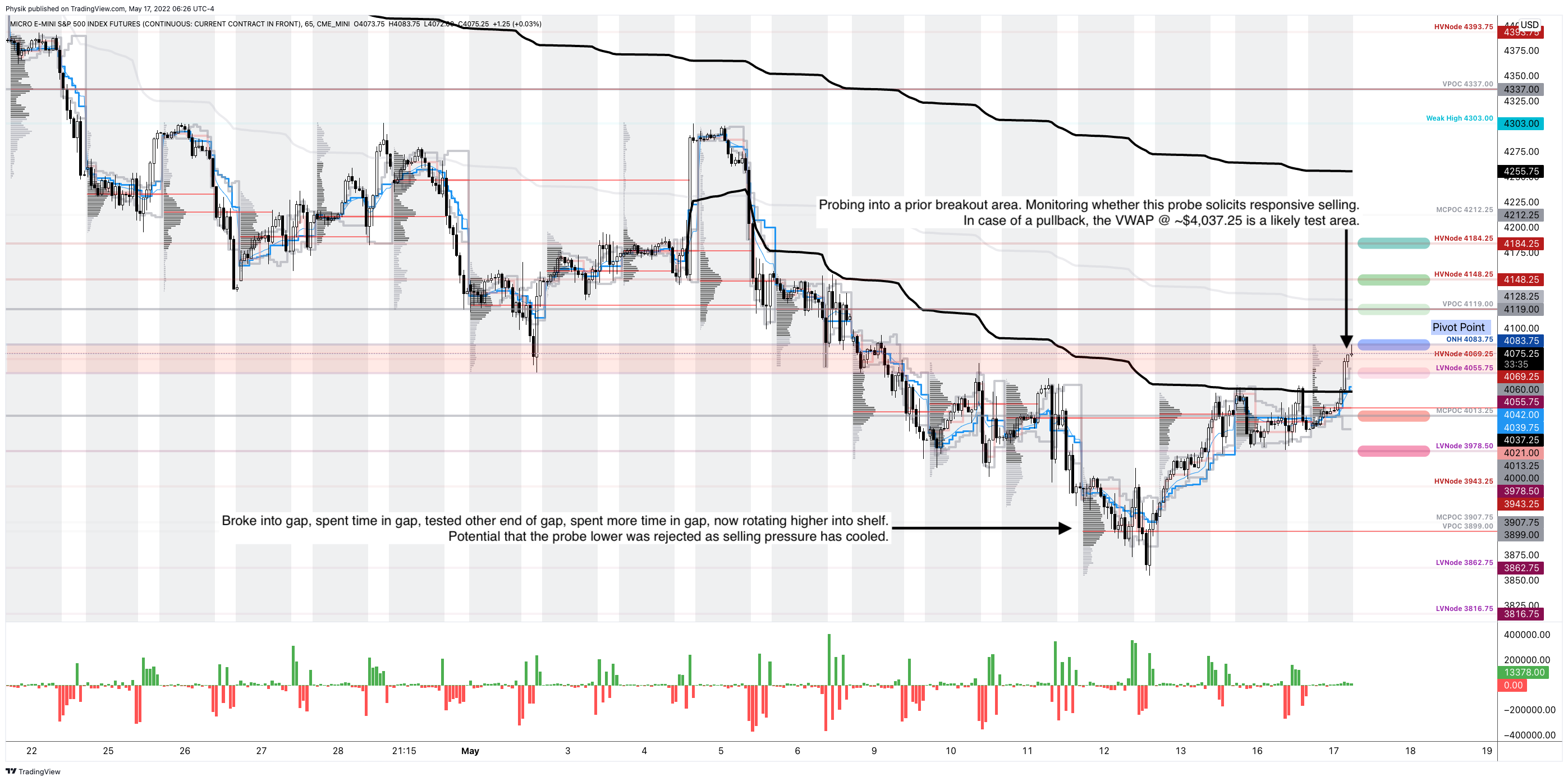

Overnight, equity index futures were higher. The S&P 500, in particular, probed the high end of the low-volume (gap) area it broke into on May 9, 2022.

The key is to monitor whether the S&P 500 is able to sustain the prices it discovered overnight. If so, then the odds that participants are, indeed, hammering out a bottom are heightened.

Ahead is data on retail sales (8:30 AM ET), industrial production and capacity utilization (9:15 AM ET), the NAHB home builders’ index, and business inventories (10:00 AM ET).

Fed-speak is scattered. At 9:15 AM ET, the Philadelphia Fed’s Patrick Harker speaks on health care. At 2:00 PM ET, Fed Chair Jerome Powell is interviewed by the WSJ. At 2:30 PM ET, the Cleveland Fed’s Loretta Mester talks at an inflation conference. And, lastly, at 6:45 PM ET, the Chicago Fed’s Charles Evans speaks.

What To Expect

Fundamental: Out of all the news, it was noteworthy when Elon Musk broke with the prevailing opinion to declare the U.S. was facing a tough recession that would last up to 18 months.

This is on the heels of a large “misallocation of capital,” he says, caused by the government printing “a zillion amount of more money than it had.”

Musk cautioned companies to watch their costs and cash flows, the latter of which we talked on the importance of in cycles where monetary conditions are tighter and there is less money to be had for corporates who are taking “the long view” and “competing on eyeballs and growth,” per Kai Volatility’s Cem Karsan who this letter’s writer spoke with last summer.

As Karsan puts it, over the last four decades, monetary policy was a go-to for supporting the economy. Money was sent to capital and that promoted deflation, ultimately creating “a disinterest and unimportance to cash flows.”

“Monetary policy has a velocity of almost zero, it goes directly to ‘Planet Palo Alto,’ and Palo Alto creates new technologies,” Moontower’s Kris Abdelmesih puts well in a summary of Karsan’s macro thesis.

“They’re sophisticated, futuristic people. They provide new self-driving cars and things getting delivered to your doorstep. They create supply … [and] does not increase demand. And so it is deflationary.”

Over the last years, in light of talk to address increasing inequality, money was sent to labor, so to speak, and that promoted inflation.

Moreover, today’s contractionary monetary policy is a blunt tool and is not equipped to “address the main problem which is a lack of supply to absorb the demand.”

Please read Moontower’s full write-up, here.

That’s sort of in accordance with comments we quoted Credit Suisse Group AG’s (NYSE: CS) Zoltan Pozsar making, yesterday. Essentially, “the Fed is pursuing demand destruction through negative wealth effects,” as the “central banks can only deal with nominal” chokepoints.

By that token, we must “[c]onsider at least the possibility that the extreme volatility and lack of liquidity [we] see in markets is by design, and the Fed will not be deterred by it, but rather that it will be emboldened by it in its singular pursuit of price stability.”

With even President Biden endorsing the closure of the “wealth window,” Karsan believes corporations will have to worry about making money again.

“These cycles are a lot shorter than the monetary supply-side cycles but they tend to be very bad for multiples and great for economic growth.”

With that in mind, there is no escape. Even the traditional bond-stock relationship – the 60/40 framework – is at risk of being upended.

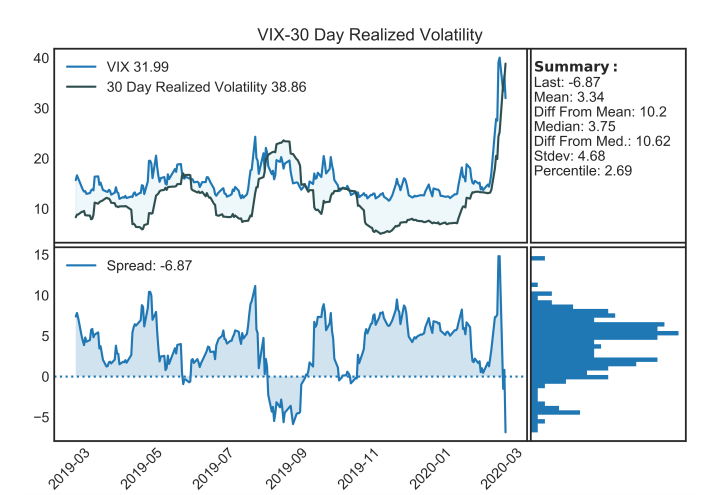

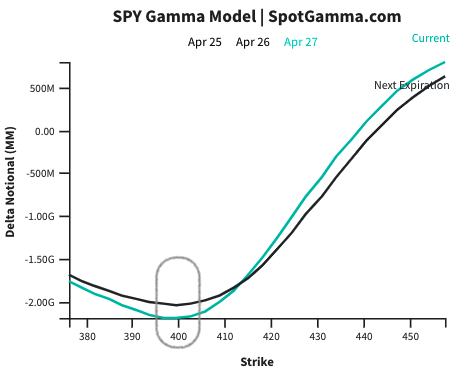

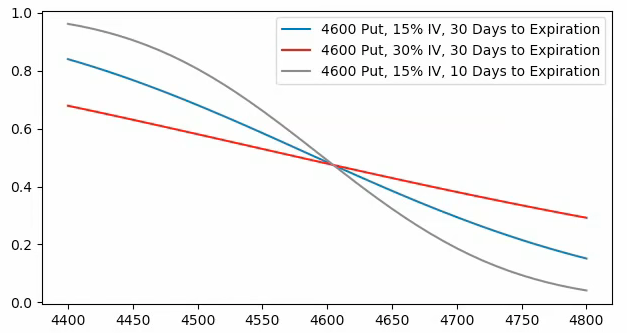

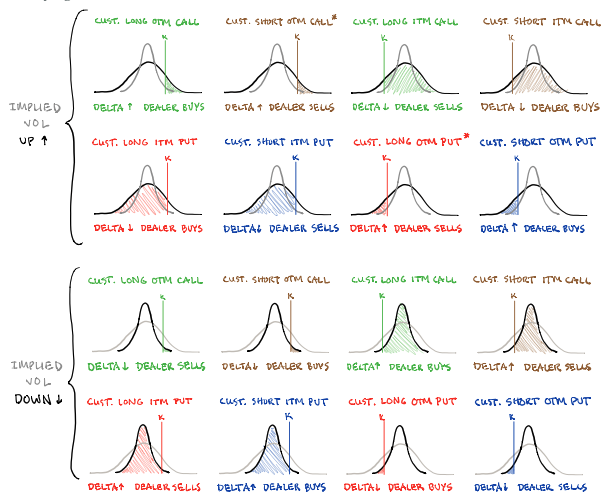

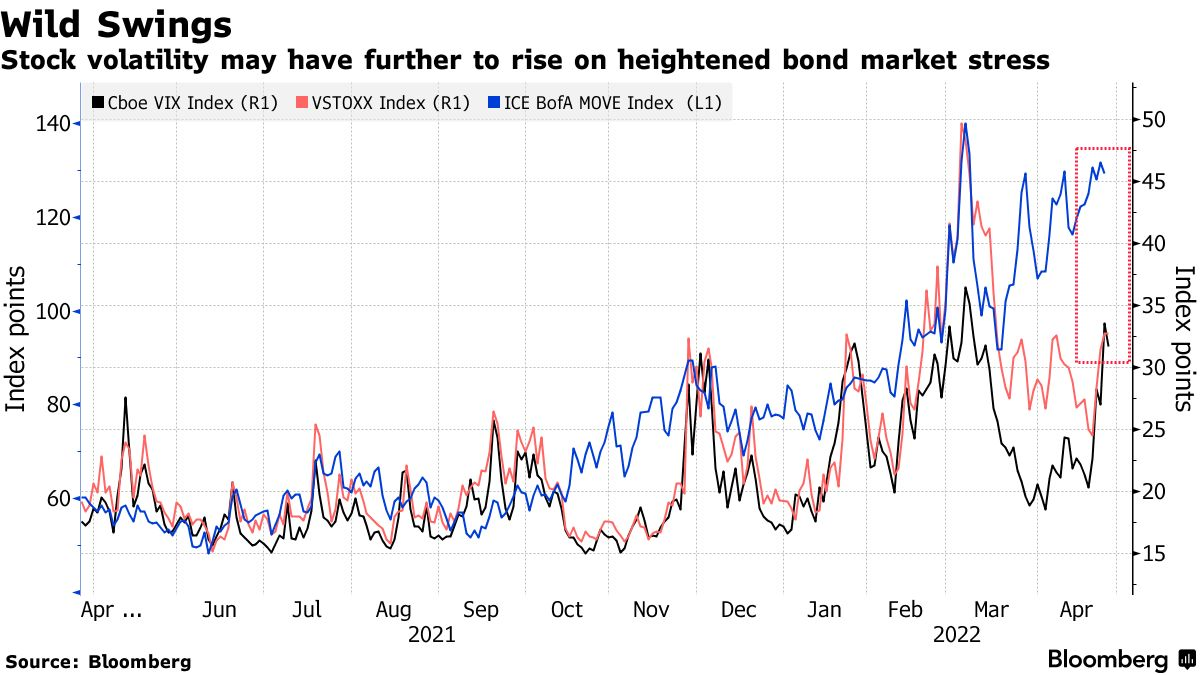

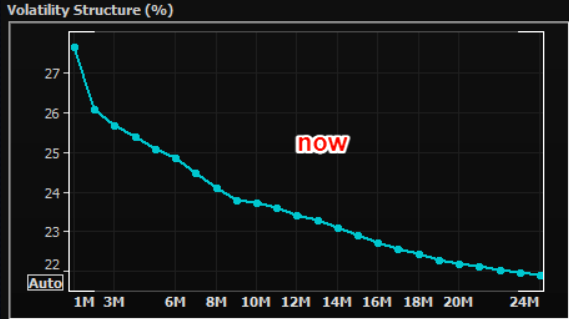

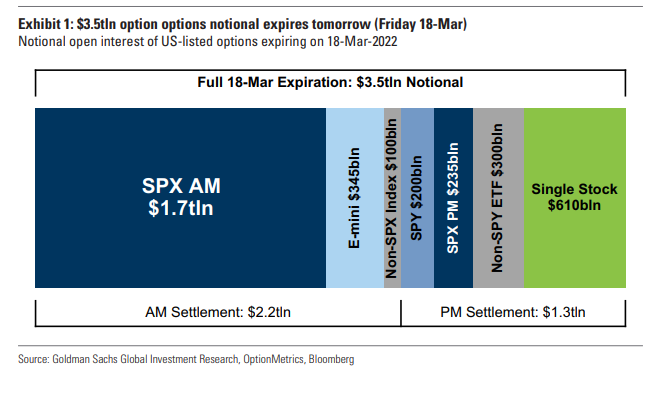

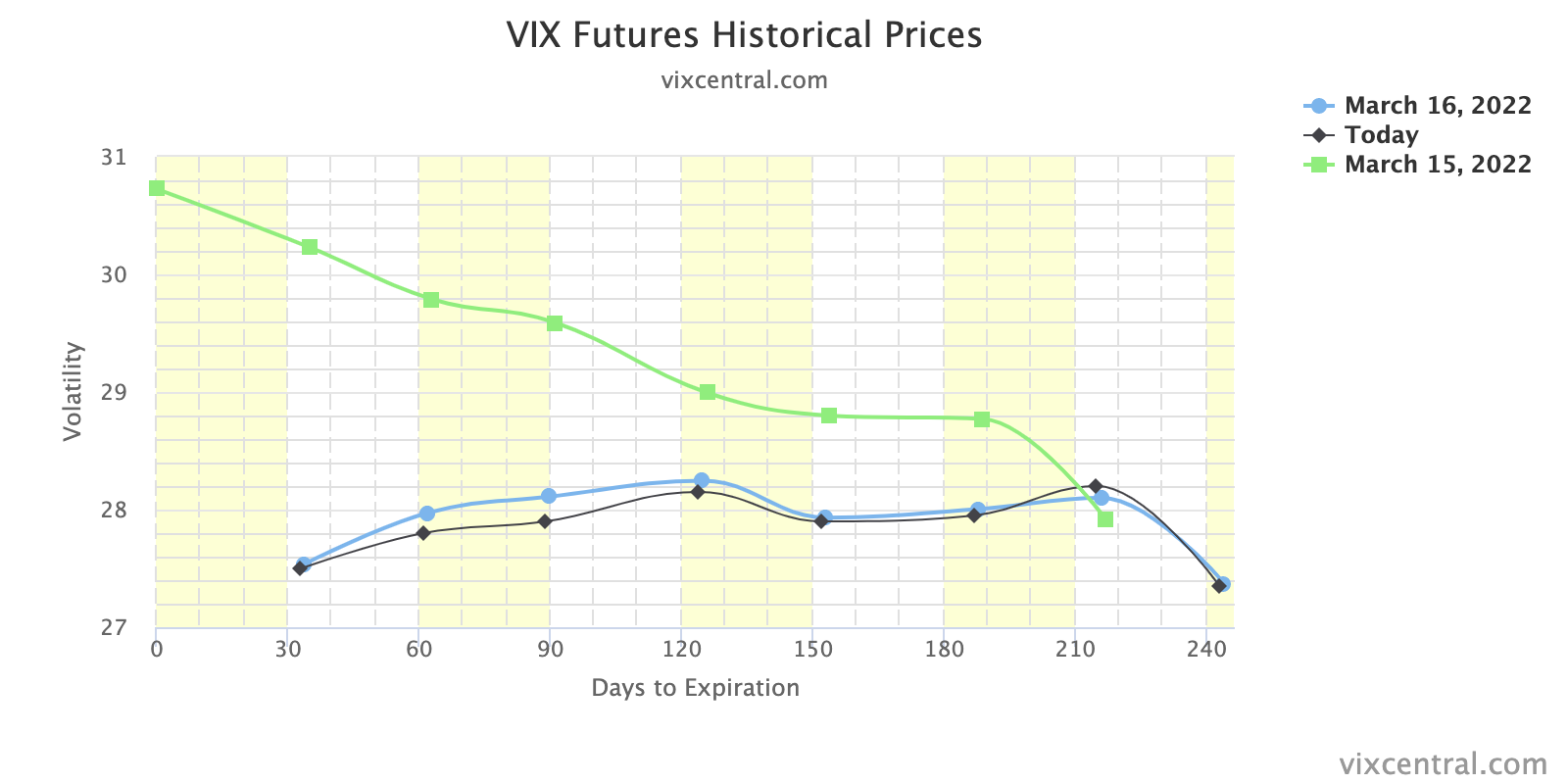

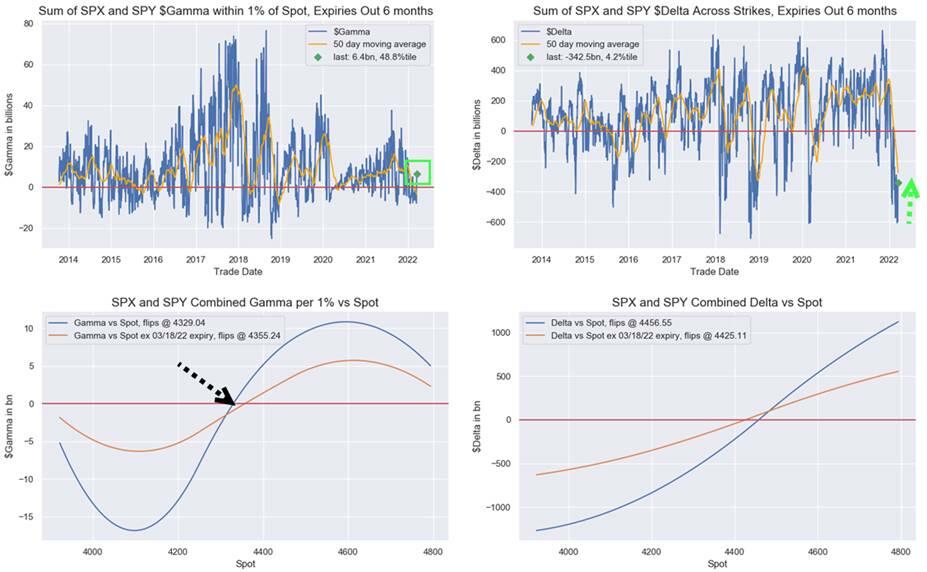

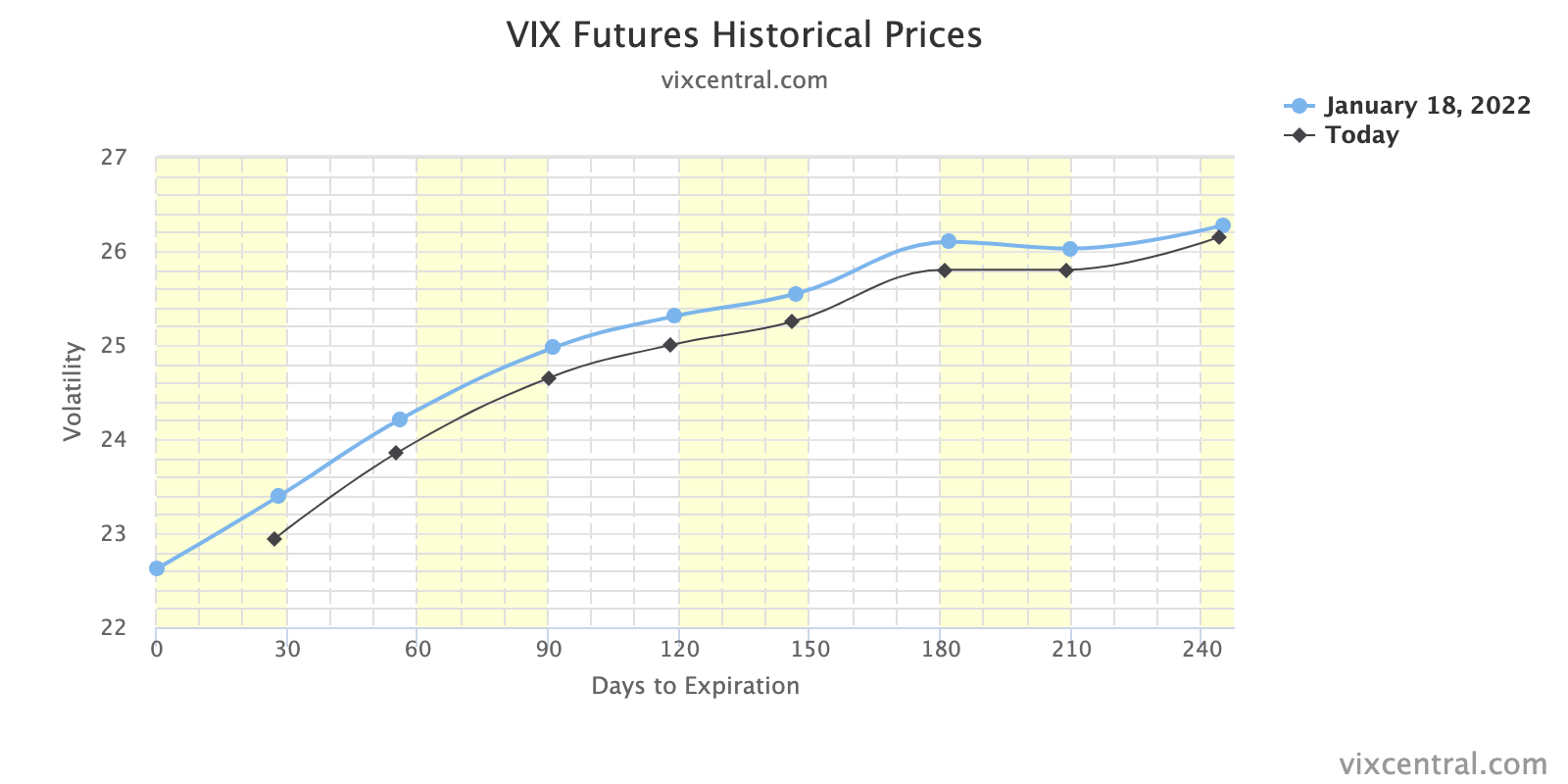

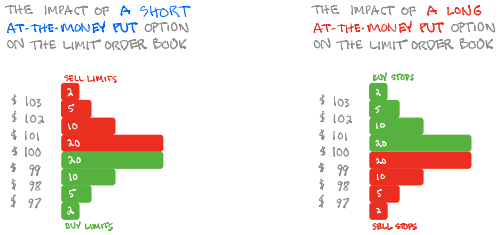

Positioning: Measures of implied volatility came in. That’s significant since participants have a lot of exposure to put options.

Further, we see liquidity providers being short those puts. As volatility continues to come in, the exposure of those options to direction (delta) compresses.

As a result, liquidity providers will taper some of their negative delta short stock and futures hedges to that positive delta put position.

Those delta hedging flows with respect to changes in volatility (vanna) are on top of what has historically been a front-running of the bullish flow associated with the delta decay of options, particularly with respect to time (charm), into options expirations (OPEX).

Notwithstanding, though proxies for buying and this hedging of existing options positioning, at the surface, appear to point to positively (skewed) forward returns, we have concern over the level at which from implied volatility is dropping from, and the general divergence between the volatility realized and implied, talked about yesterday.

Basically, as SpotGamma says, there’s not as much “stored energy to catalyze a rally.”

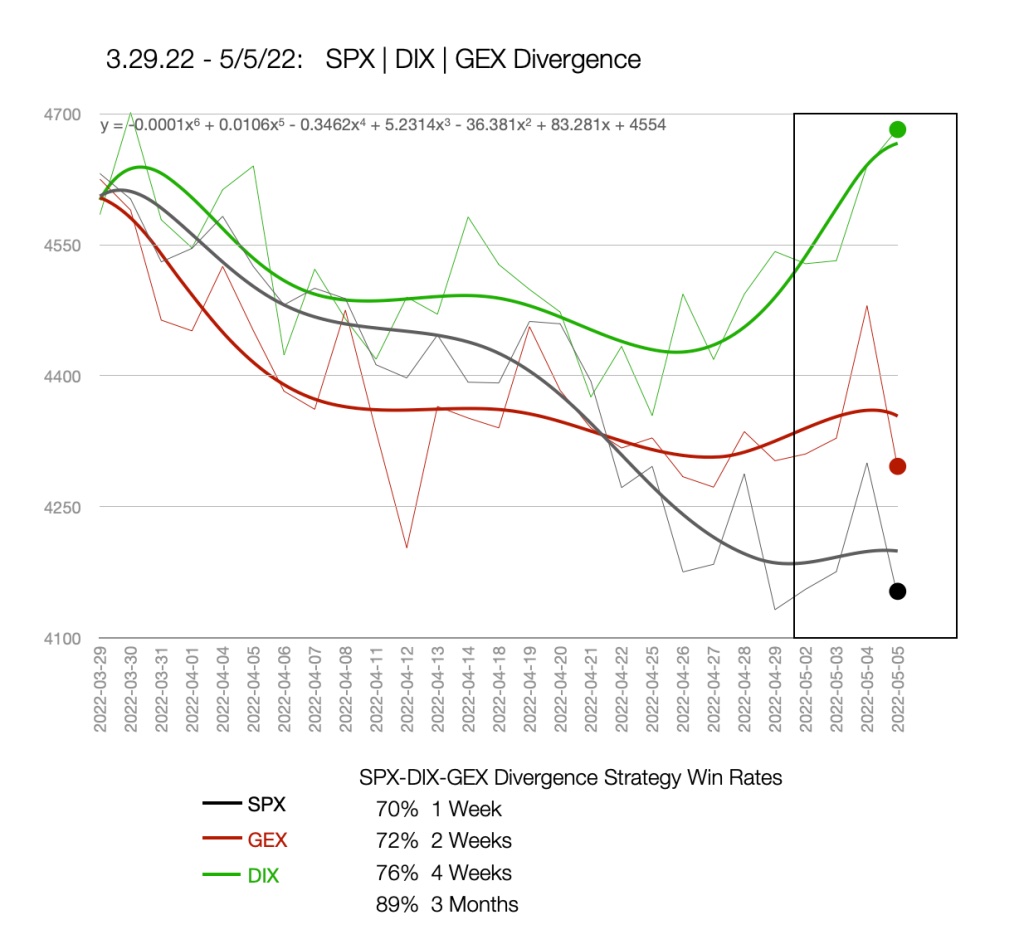

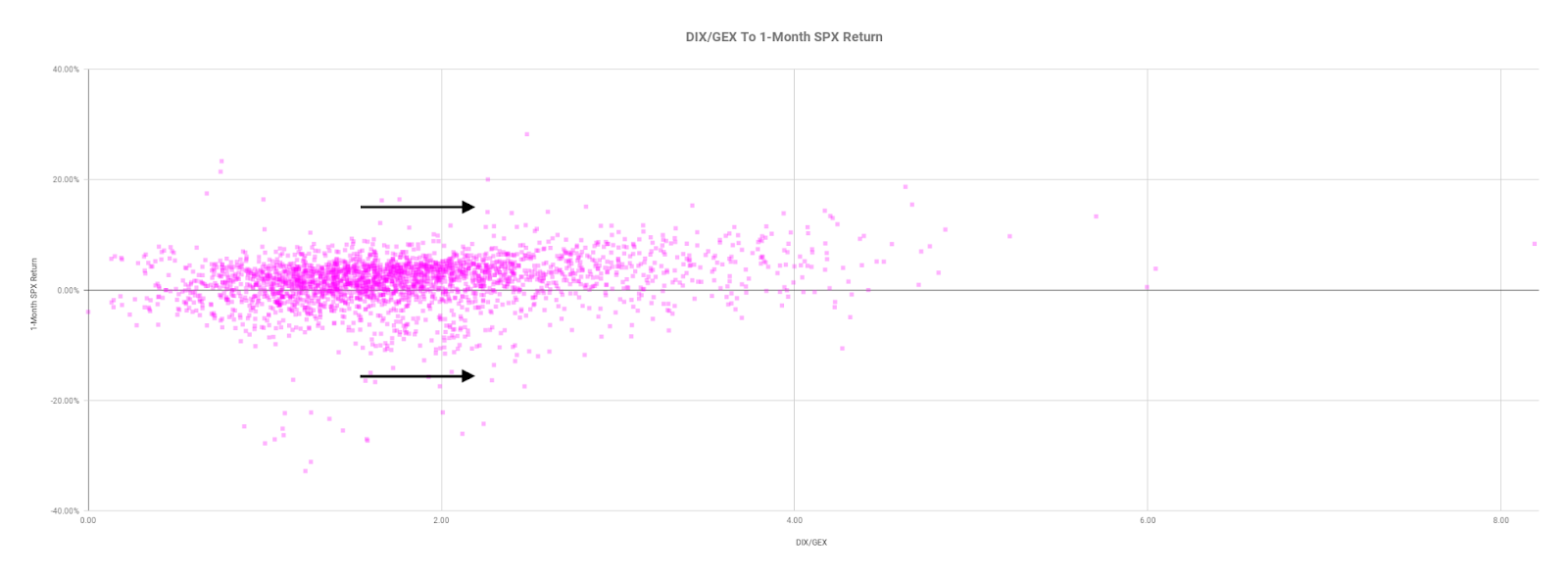

SqueezeMetrics adds:

The Cboe Volatility Index (INDEX: VIX) compressing, while dealer gamma exposure is “more negative than it’s been in years is not how you get sustained rallies–it’s how you get energy for bigger downside moves.”

Therefore, we continue to focus on participating in upside with as little debit risk as possible, via the use of complex strategies, further validated by quoted research.

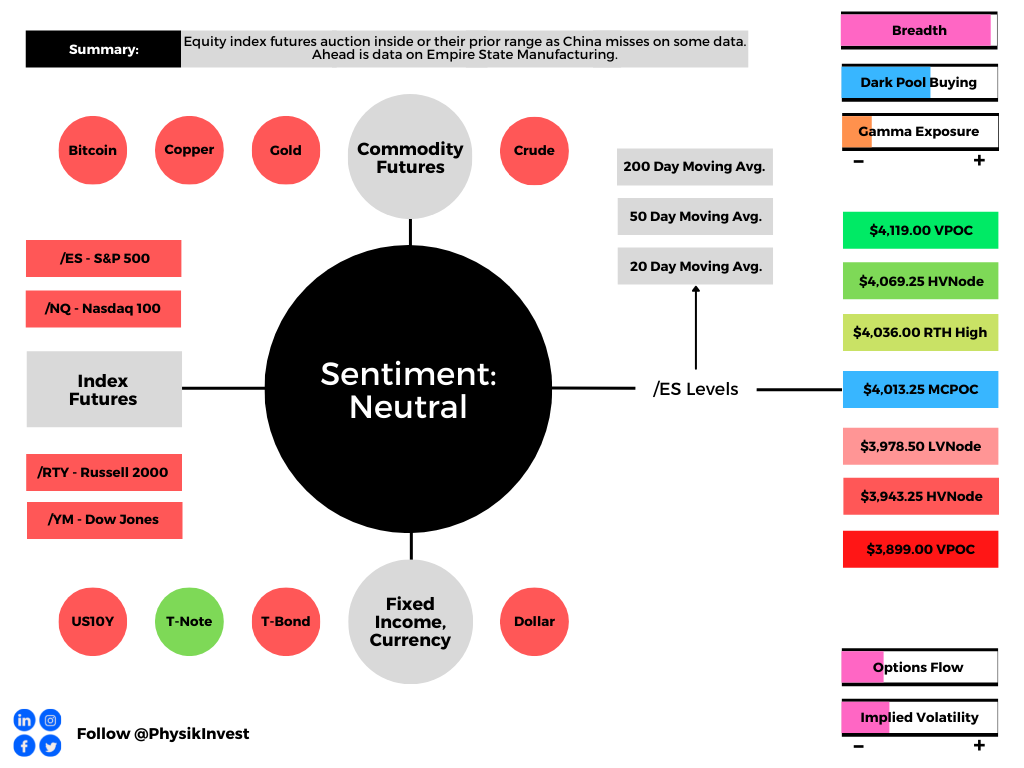

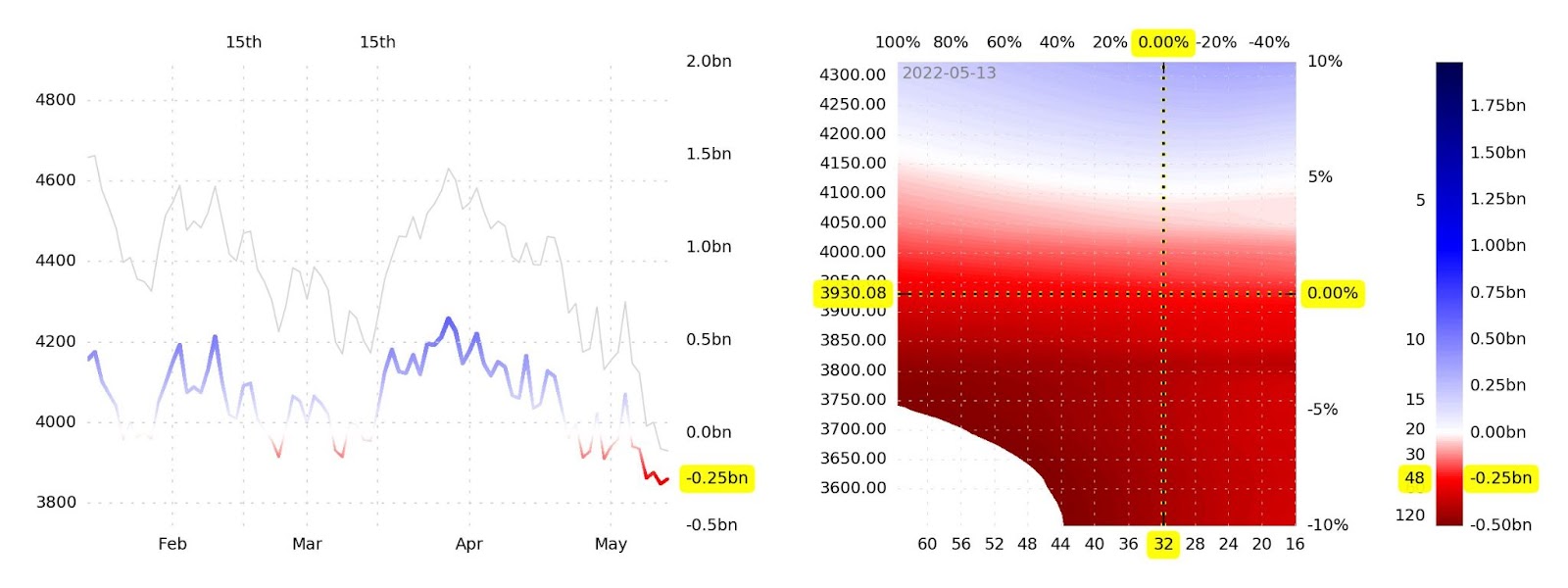

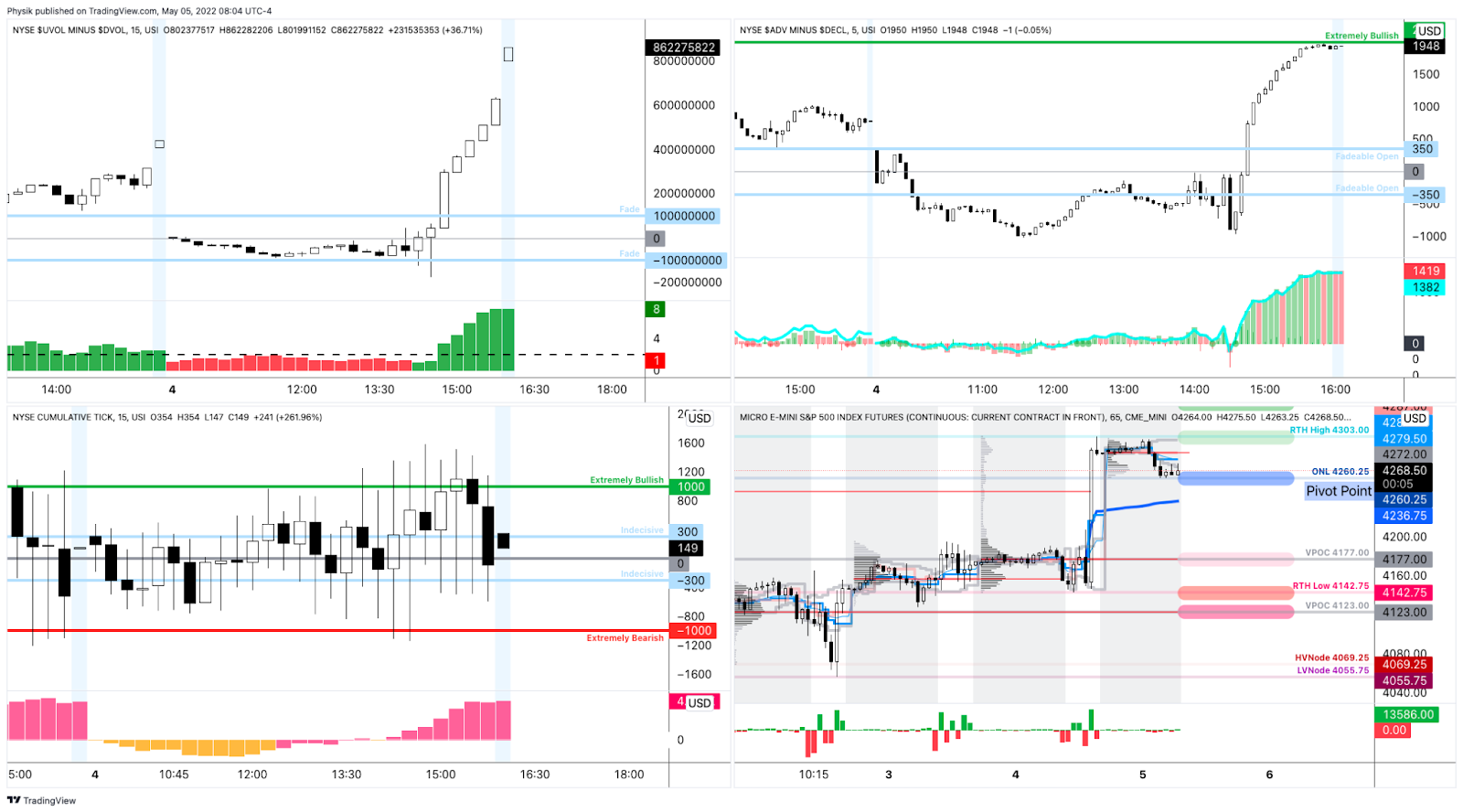

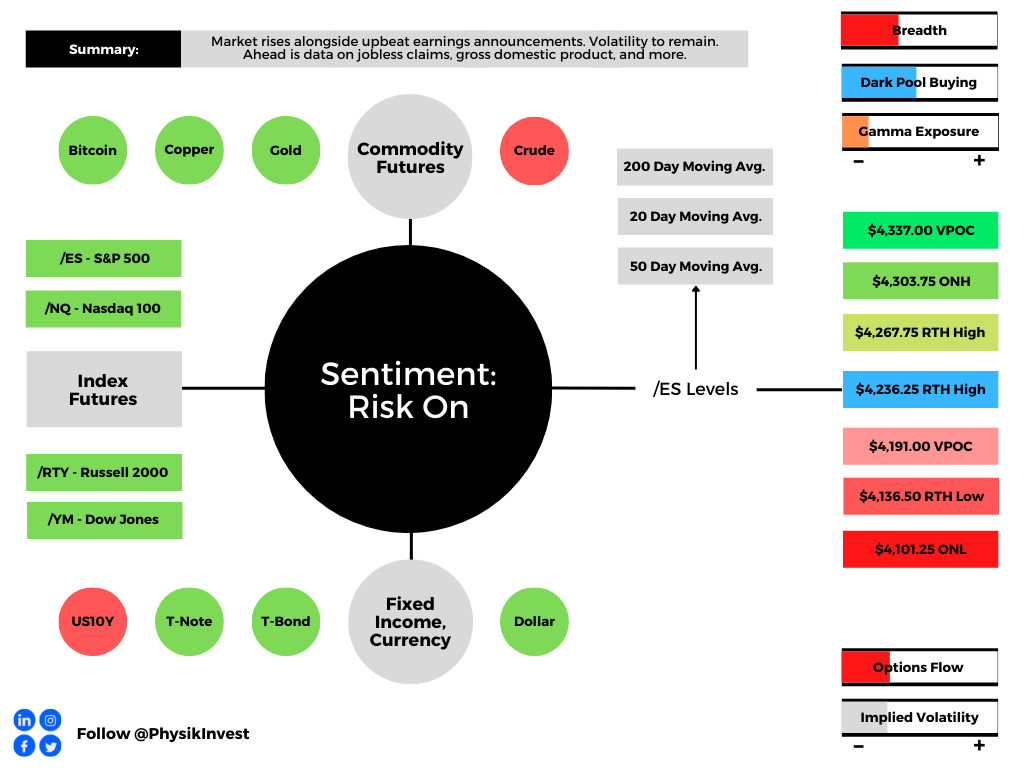

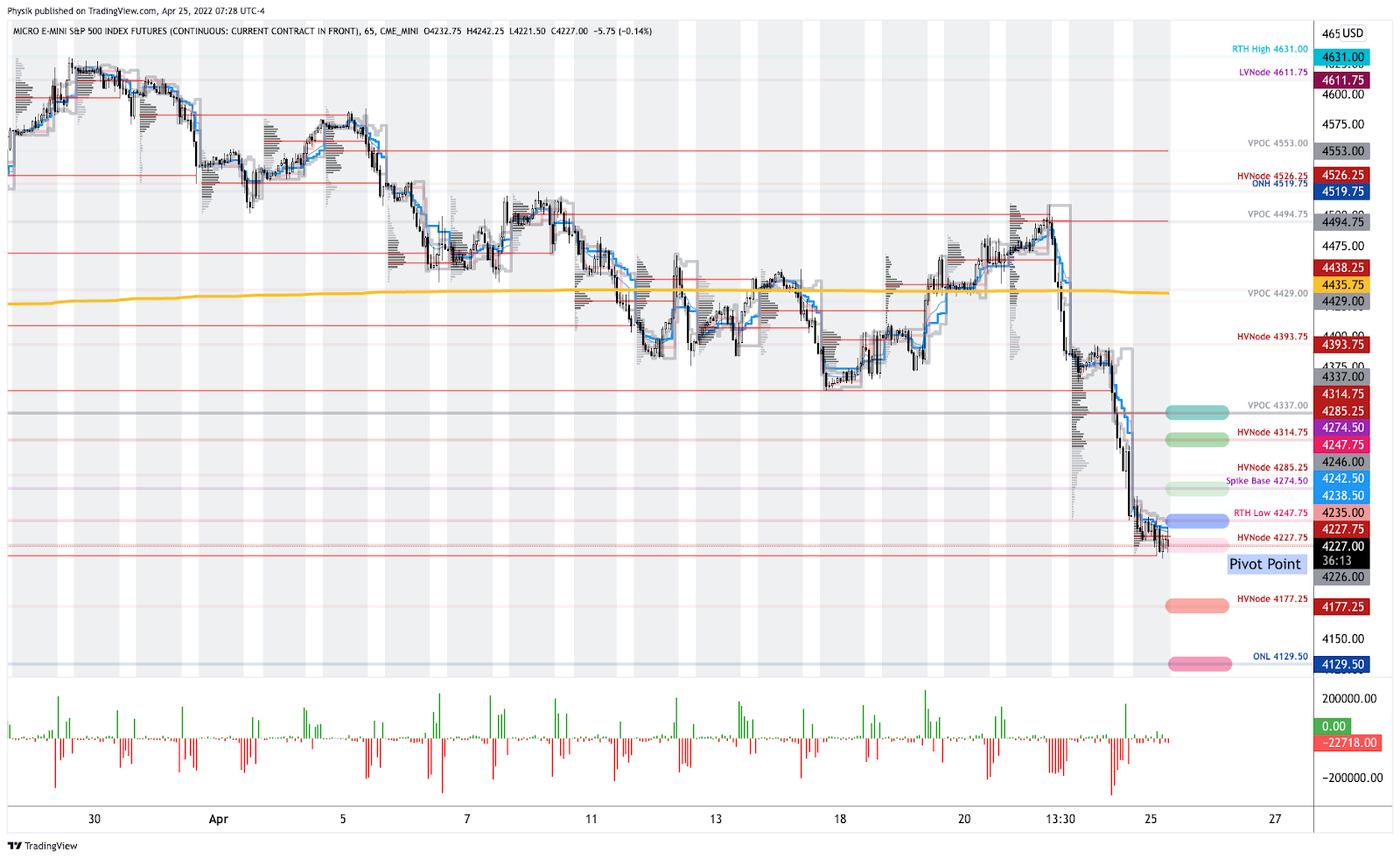

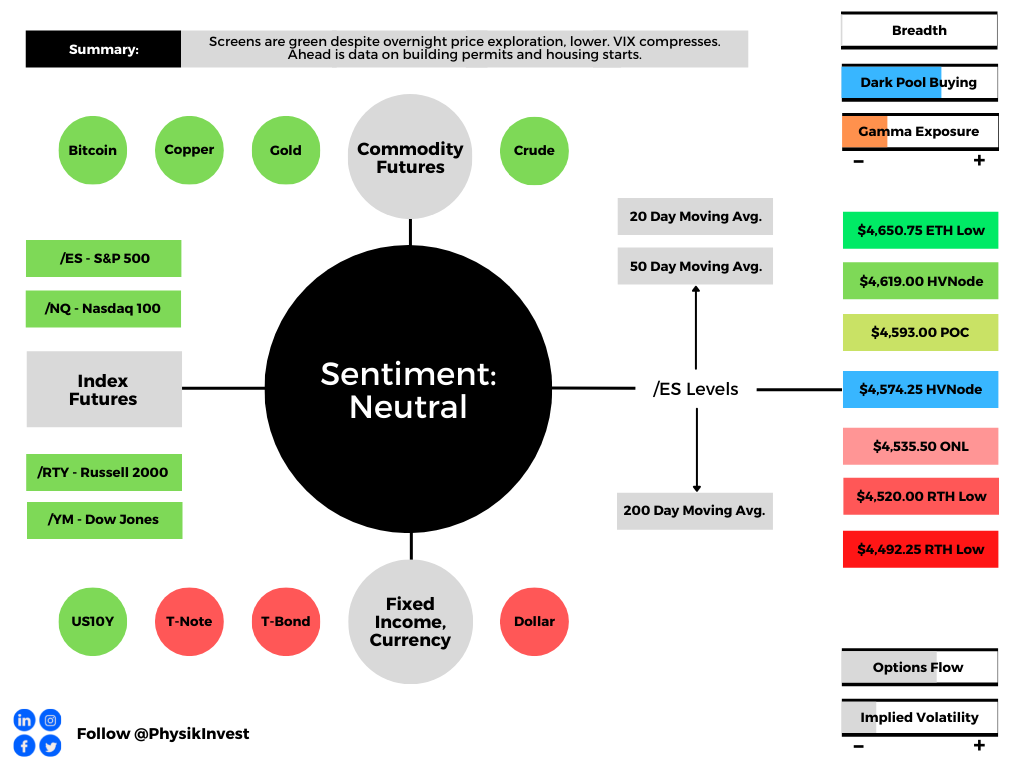

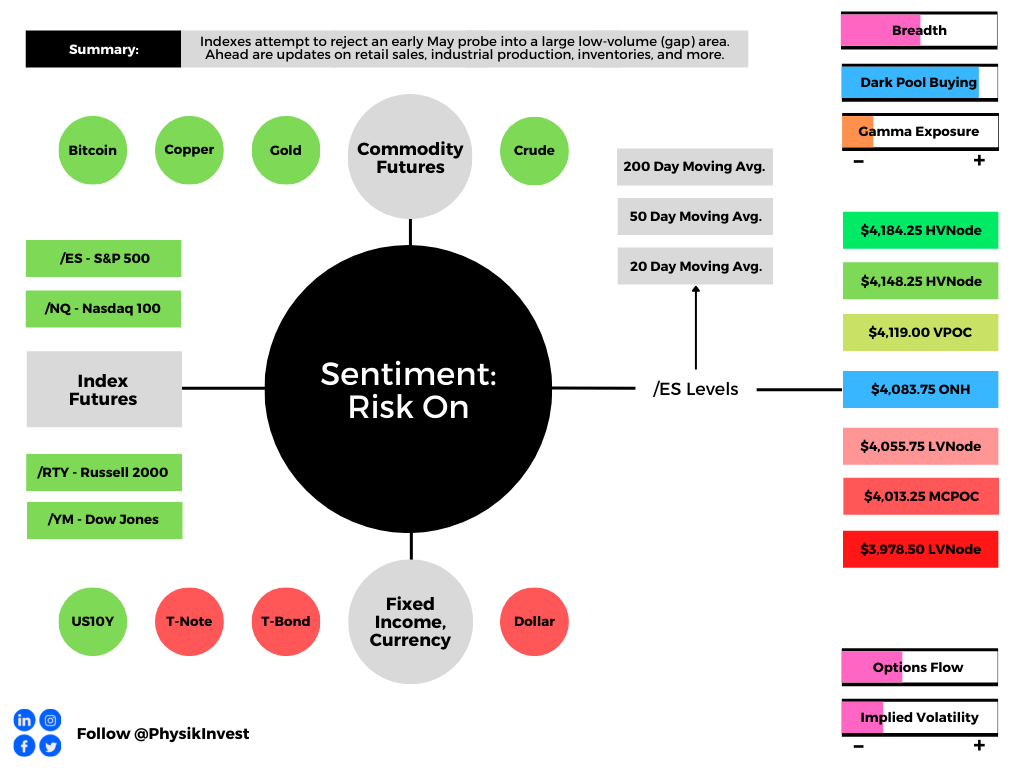

Technical: As of 6:30 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,083.75 overnight high (ONH) puts in play the $4,119.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,148.25 and $4,184.25 high volume nodes (HVNodes), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,083.75 ONH puts in play the $4,055.75 low volume area (LVNode). Initiative trade beyond the LVNode could reach as low as the $4,013.25 micro composite point of control (MCPOC) and $3,978.50 LVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

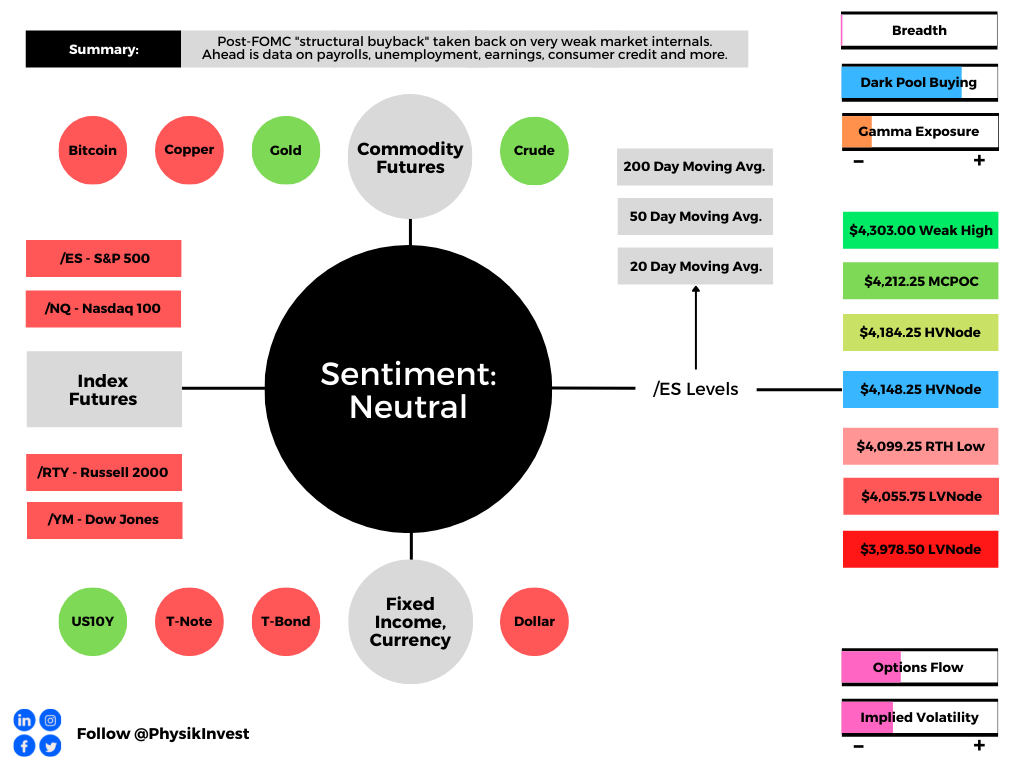

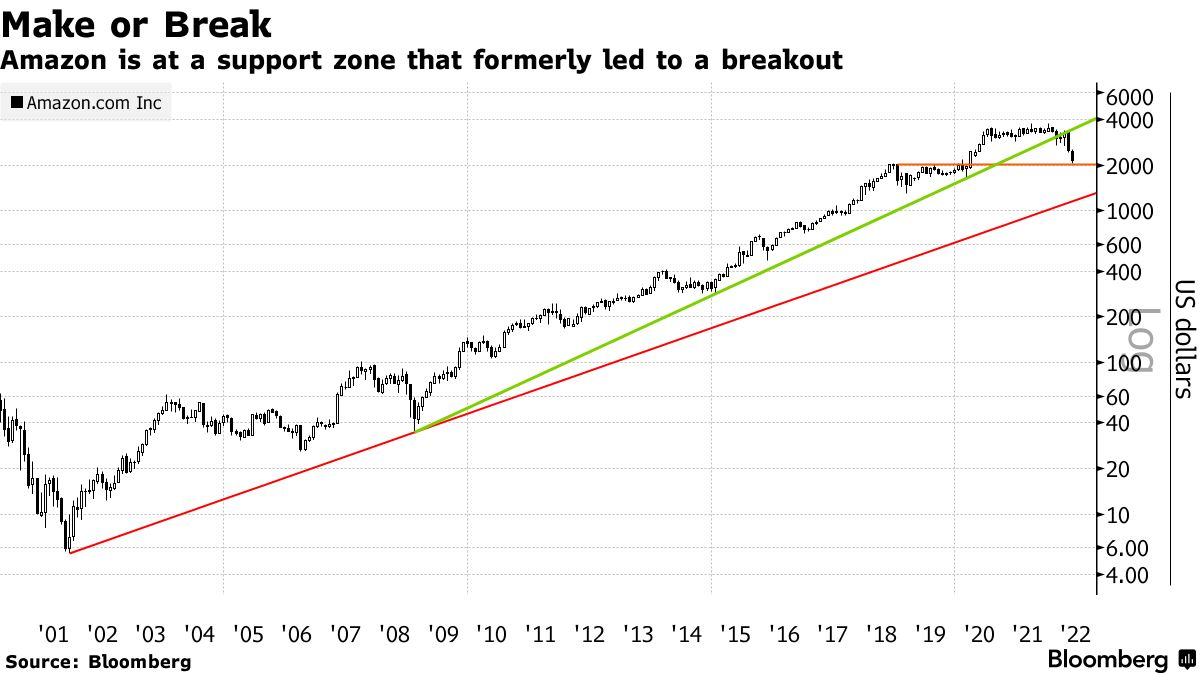

Considerations: A push-and-pull between the largest of S&P 500 weights.

For instance, Apple Inc (NASDAQ: AAPL) is clinging to its prior trend.

All the while products like Amazon Inc (NASDAQ: AMZN), are trading into key supports.

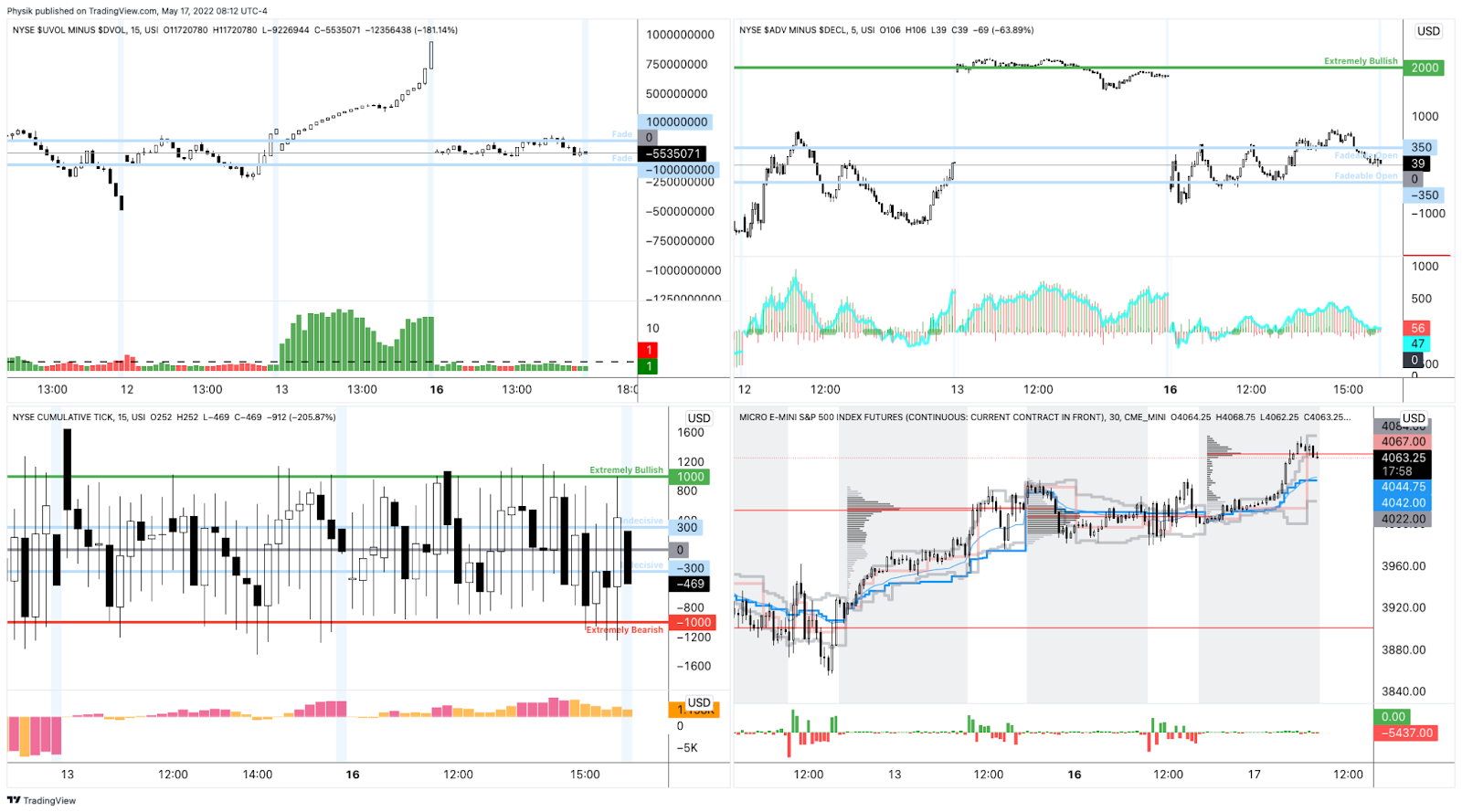

We continue to monitor our market internals and (large) changes in positioning (e.g., open interest builds at higher prices further out in time) that will provide further validation to this most recent S&P 500 reversal.

What People Are Saying

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.