The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

Overnight, equity index futures auctioned lower after a failed attempt to solicit strong buying on a break of Friday’s regular trade high.

Coincidentally, after a test of an anchored volume-weighted average price level, some measures from China had traders concerned about global growth, and that fed into a risk-off sentiment and probe further into Friday’s range.

Moreover, ahead is data on Empire State Manufacturing (8:30 AM ET).

Today, we add light context to our narratives with an aim to elaborate further in letters later this week. Take care!

What To Expect

Fundamental: Data from China shows contraction in light of COVID-19 troubles.

Bloomberg’s John Authers explains that a contracting China “would be a deflationary force for the rest of the world.”

Andreas Steno Larsen, of the Stenos Signals letter, recently talked about this “lack of economic activity in China,” as well as “slowing demand in the West,” both of which are to “lead inflation expectations lower.”

Notwithstanding, the Federal Reserve (Fed) remains on track “to deliver substantial QT and rate hiking,” all the while investors “hold a relatively risk-friendly position in equities and credits.”

Steno Larsen explains: “That disconnect [between sentiment and exposure to risk] will have to wane before I truly dare to re-add risk asset exposure to my list of recommendations.”

Pursuant to that remark, Authers notes that the latest Chinese data emboldens the risks of a recession which Credit Suisse Group AG’s (NYSE: CS) Zoltan Pozsar explains is not enough.

“[T]he risk of recession, whether it is real or merely implied by an inversion of the yield curve, won’t deter the Fed from hiking rates higher faster or from injecting more volatility to build up negative wealth effects, and signs of a recession might not mean immediate rate cuts to ramp demand back up.”

“Rallies could beget more forceful pushback from the Fed – the new game.”

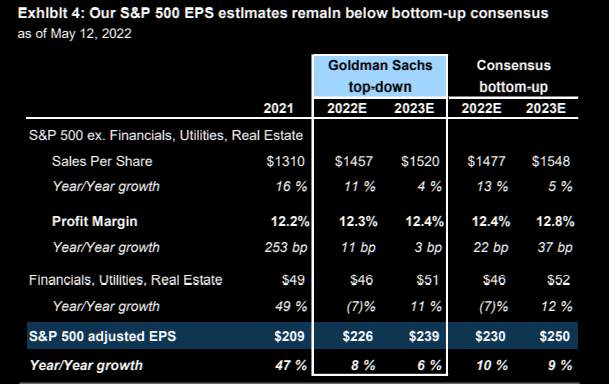

Per Goldman Sachs Group Inc (NYSE: GS), baseline forecasts assume “no recession” and imply the S&P 500’s P/E ends unchanged at 17x.

“A recession would see the index fall by 11% to $3,600.00 as the P/E drops to 15x.”

Positioning: Early on Friday morning, we approached trade too optimistically but, to our credit, we focused on participating with as little risk as possible, via the use of complex strategies, as validated by quoted research.

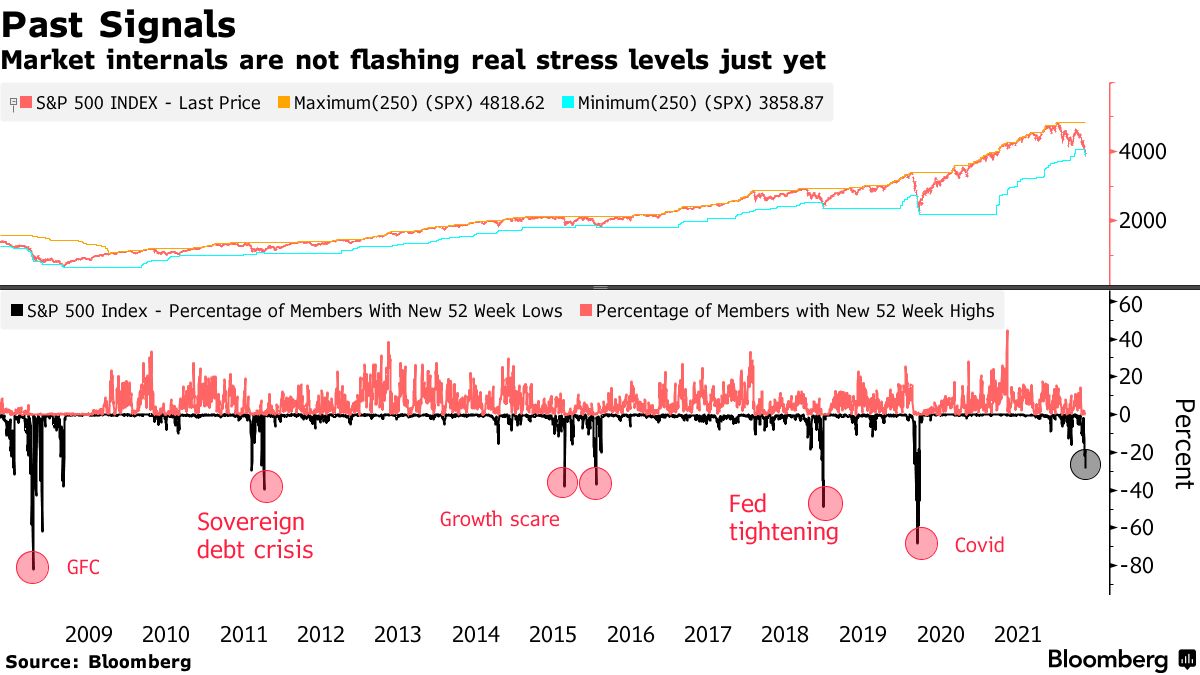

Heading into Monday’s regular trade, little has changed and indexes are holding well, relative to some constituents.

This is as participants are hedged and volatility markets remain well-supplied, due in part to suppressive volatility selling, as well as passive flows supporting the largest index constituents.

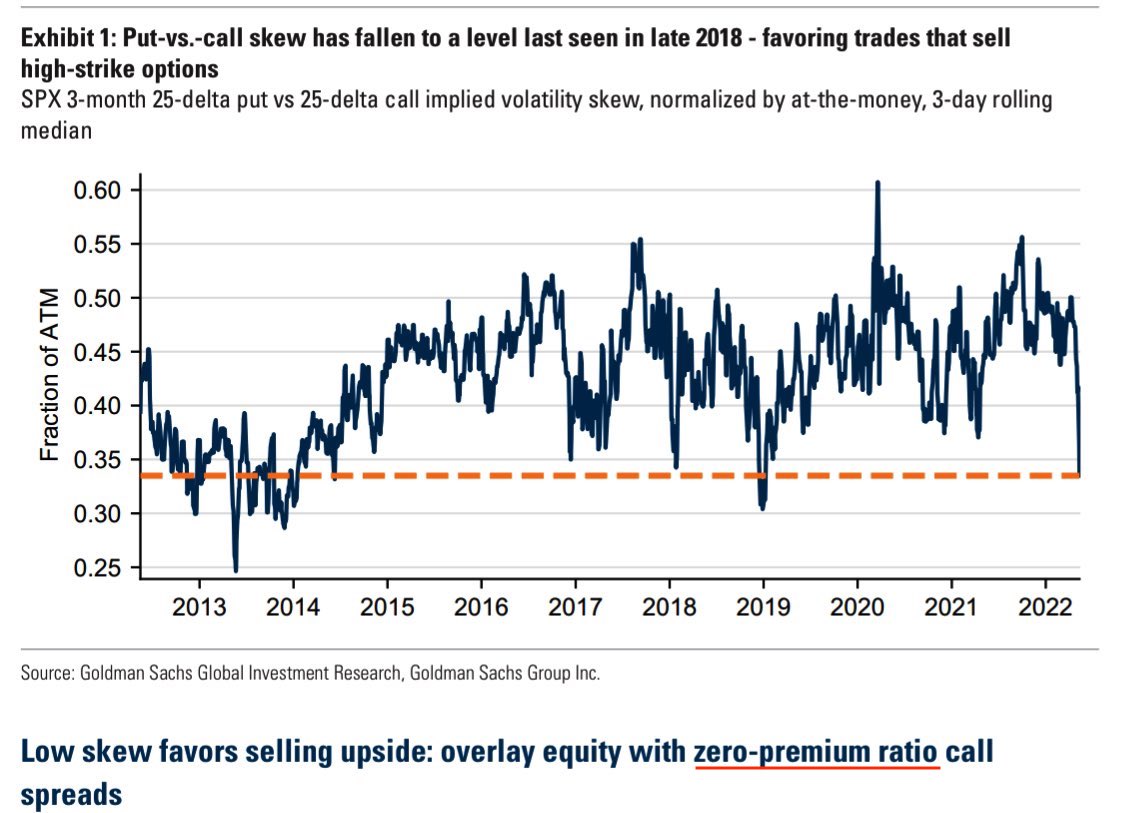

Kai Volatility’s Cem Karsan hypothesizes: “If a meaningful [volatility] event has happened within the last year, participants are more likely to be prepared for the move. So the ‘2nd event’ dramatically underperforms [implied volatility] skew expectations.”

“Take Jan/Feb 2016, Oct-Dec 2018, &…Sep 2020? All these ‘2nd Events’ ended up being as meaningful as their 1st events, if not more, for markets, but were much more orderly [and] accompanied by poor [volatility] performance.”

Given the aforementioned supply and demand dynamic, we continue to observe “divergence in the volatility (movement of underlying equity market up and down) realized, versus that which is implied by options activity,” SpotGamma says.

For “divergences in volatility realized and implied to resolve, it would likely take forced selling. Liquidity providers’ response to demand for protection would, then, likely exacerbate the move and aid in the repricing of volatility to levels where there would be more stored energy to catalyze a rally.”

All else equal, SpotGamma adds, there is no catalyst to rally until the May 20, 2022 options expiration (OPEX). Till then, rallies are subject to failure.

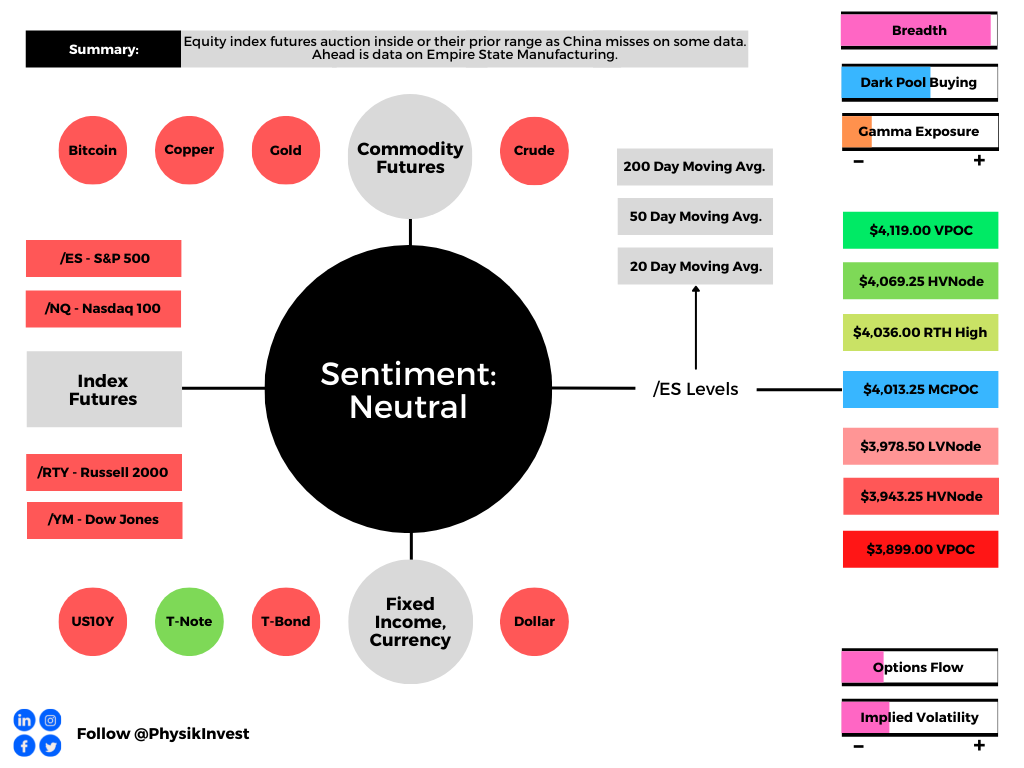

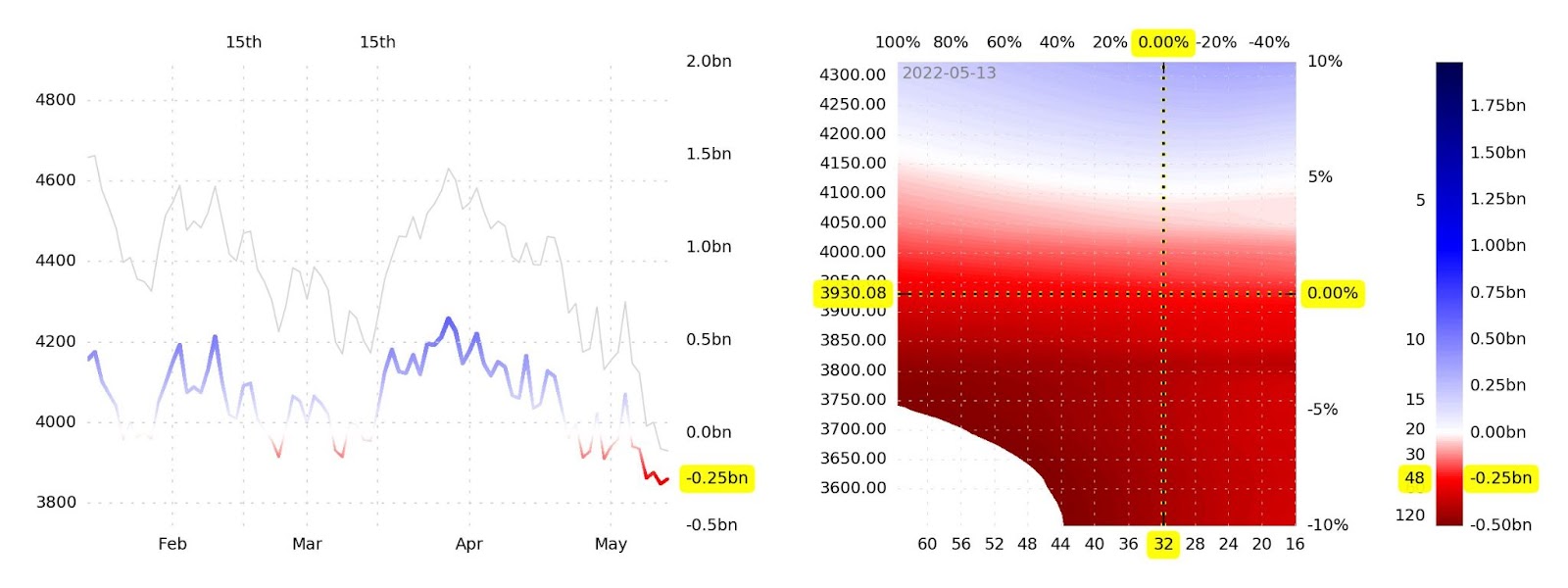

Technical: As of 6:30 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,013.25 micro composite point of control (MCPOC) puts in play the $4,036.00 regular trade high (RTH High). Initiative trade beyond the $4,069.25 high volume area (HVNode) could reach as high as the HVNode and $4,119.00 untested point of control (VPOC), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,013.25 MCPOC puts in play the $4,3978.50 low volume area (LVNode). Initiative trade beyond the LVNode could reach as low as the $3,943.25 HVNode and $3,899.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

4 replies on “Daily Brief For May 16, 2022”

[…] is dropping from, and the general divergence between the volatility realized and implied, talked about […]

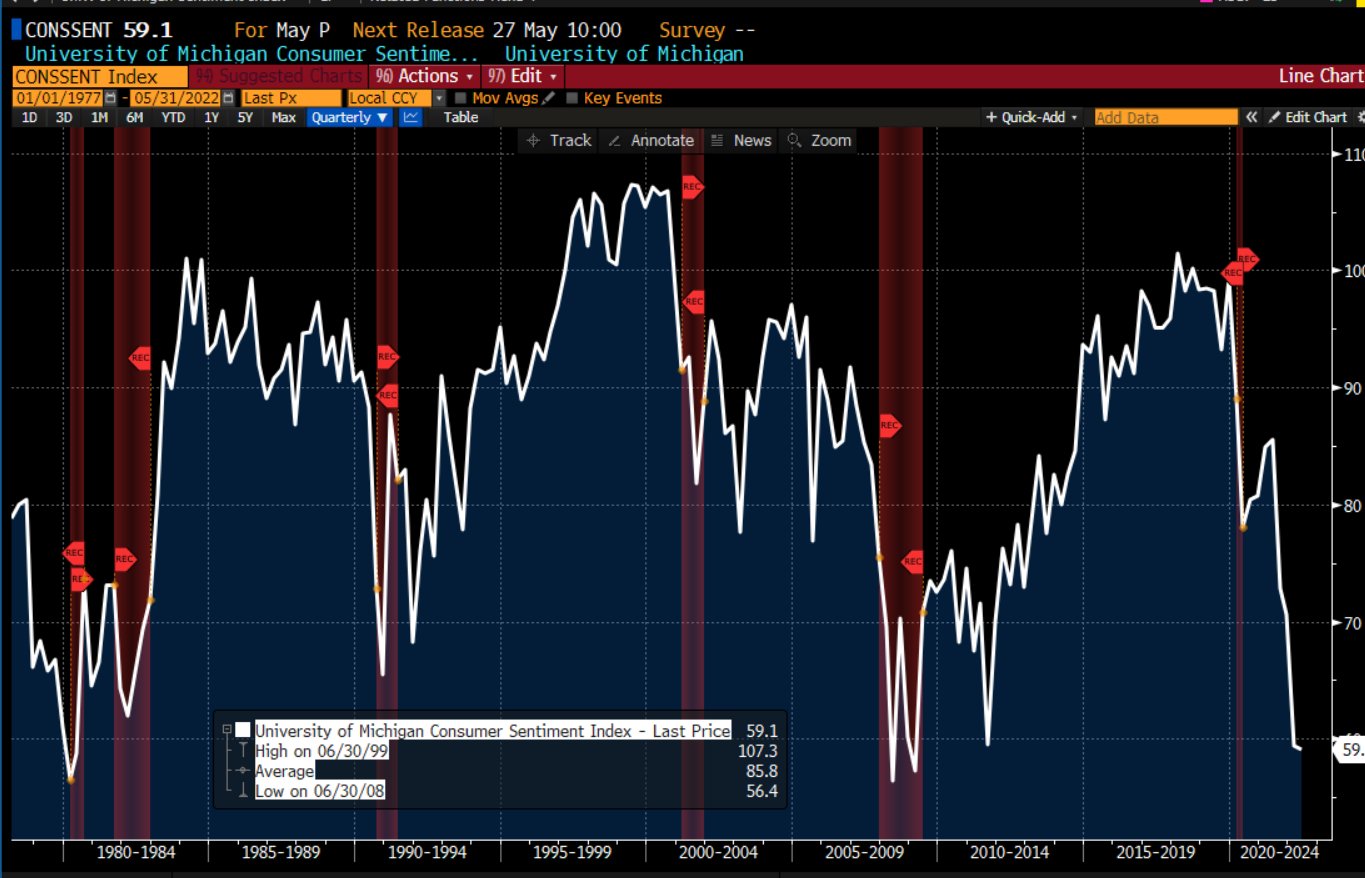

[…] At the same time, sentiment has plunged to Great Recession levels, all the while consumers are “rebelling against their loss of purchasing power,” and China is in turmoil (talked about May 16). […]

[…] this event, participants are hedged and volatility remains well-supplied, due in part to suppressive volatility selling, as well as passive flows supporting the largest index […]

[…] participants are hedged and volatility remains well-supplied, due in part to suppressive volatility selling, as well as passive flows supporting the largest index […]