The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures were quiet, auctioning sideways-to-higher, ahead of updates on monetary policies.

A check on some naive measures suggests we’re in for an expansion of range (i.e., heightened realized volatility) in the coming session(s). Key, today, are Federal Open Market Committee (FOMC) updates (2:00 PM ET) and a news conference (2:30 PM ET).

The expectation is a 50 basis point hike and balance sheet contraction with run-off caps of $95 billion. If the action is in line with expectations (priced in), the reaction is likely to be positive.

Today’s economic calendar includes, also, a release of the Automatic Data Processing Inc’s (NASDAQ: ADP) employment report (8:15 AM ET), international trade balance (8:30 AM ET), S&P Global Inc’s (NYSE: SPGI) U.S. services PMI (9:45 AM ET), and the ISM services index (10:00 AM ET).

What To Expect

Fundamental: Expected is front-loaded tightening, by the Federal Reserve (Fed), today.

The consensus is anchored around a 50 basis-point hike in May and no adjustments to the Reverse Repo Rate (RRP) or Interest on Reserve Balances (IORB), says Nordea Bank (OTC: NRDBY) research. The Fed may opt, also, to initiate a 75 basis-point hike in June.

“We believe that after the FOMC hikes by a half-point in May and presents a detailed plan to reduce the Fed balance sheet,” imminently, says Anna Wong, Yelena Shulyatyeva, Andrew Husby, and Eliza Winger of Bloomberg.

“Powell will avoid definitive guidance about the size of future hikes, as policymakers assess how the runoff is affecting the economy in coming months.”

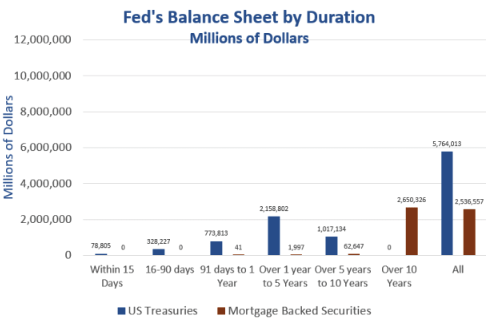

As noted before, the key (risk) is the statements on the Fed’s balance sheet and the (imminent) process to shrink it through quantitative tightening (QT).

Per Nordea, QT is likely to consist of a 3-month phase-in period and run-off caps of $95 billion (i.e., $60 billion on U.S. Treasuries [USTs] and $35 billion in mortgage-backed securities [MBSs]), effectively lowering the Fed’s balance sheet by $670 billion by year-end.

This is alongside the realization that “1Q may be the last good quarter of earnings as higher costs and increased recession risks weigh on future growth,” Morgan Stanley’s (NYSE: MS) Mike Wilson explains.

Market weakness in the past weeks was the result of “growing evidence that growth is slowing faster than most investors believe,” Wilson adds, and “the market is currently so oversold, any good news [such as Fed action being as expected] could lead to a vicious bear market rally.”

“We can’t rule anything out in the short term but we want to make it clear this bear market is far from complete.”

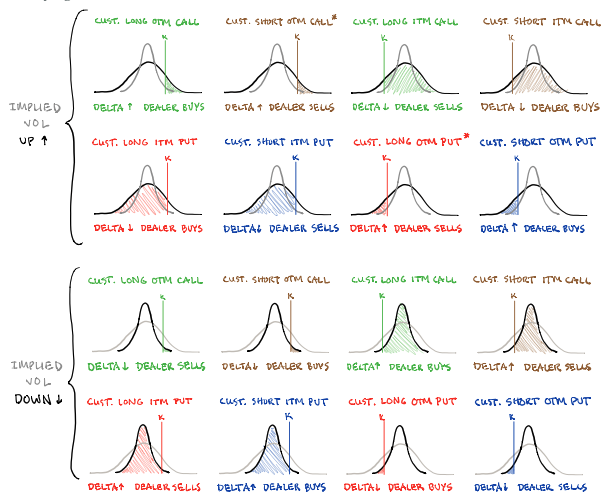

Positioning: Borrowing from yesterday’s letter, as little has changed, bets on the direction are concentrated in negative delta (long puts, short calls). The exposure is short-dated and highly sensitive to changes in implied volatility and direction.

This exposure’s roll-off and compression in volatility ought to coincide with liquidity provider support to markets (i.e., relief of pressure from hedges to concentrated options positioning).

Per Kai Volatility’s Cem Karsan, on a Fed day, “the first move tends to be structural. A function of the inevitable rebalancing of dealer inventory post-event. The second move and final resolution, if you wait for it, is usually tied to the incremental effects on liquidity (QE/QT).”

Validation of the latter (move) ought to be confirmed by participants’ new concentration of bets. In other words, if participants start to concentrate their bets at higher prices, further out in time, that confirms (changing sentiment) and (improves) the odds of sustained follow-through.

If not, it’s likely that prices, after a short-term relief, will succumb to fundamental weaknesses.

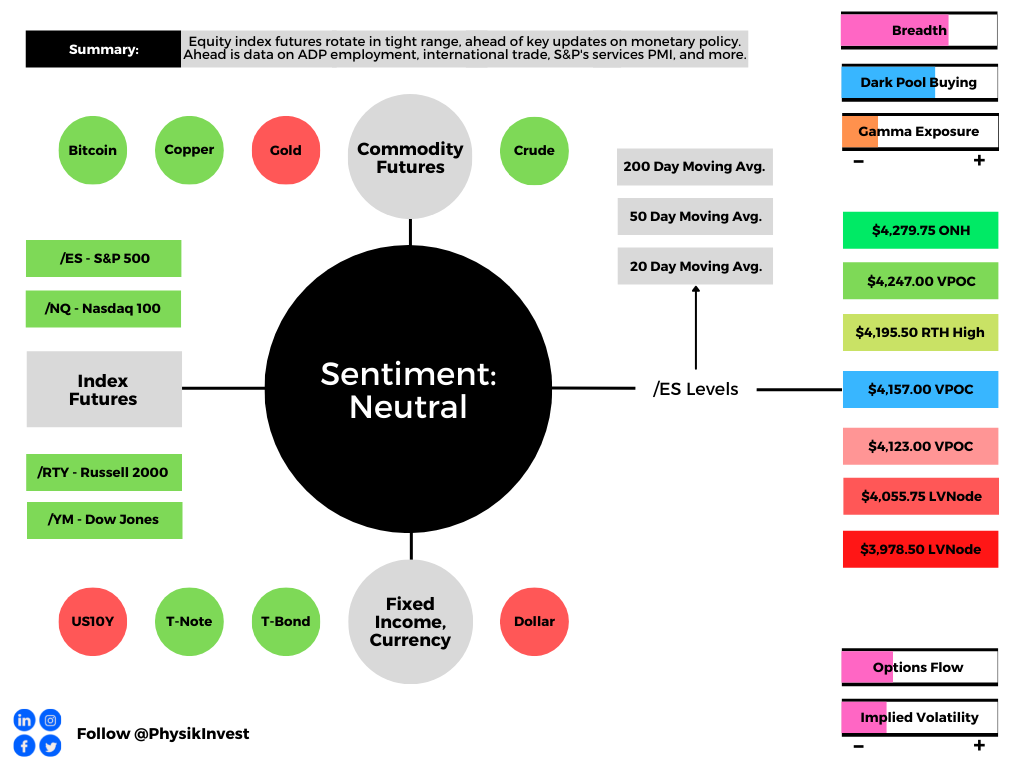

Technical: As of 7:00 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a balanced overnight inventory, just inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,157.00 untested point of control (VPOC) puts in play the $4,195.50 regular trade high (RTH High). Initiative trade beyond the RTH High could reach as high as the $4,247.00 VPOC and $4,279.75 overnight high (ONH), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,157.00 VPOC puts in play the $4,123.00 VPOC. Initiative trade beyond the $4,123.00 VPOC could reach as low as the $4,055.75 and $3,978.50 low volume areas (LVNodes), or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.