The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures took back a small chunk of Wednesday’s post-Federal Open Market Committee (FOMC) advance. Both bonds and equity indexes were lower while most commodities and the dollar were bid.

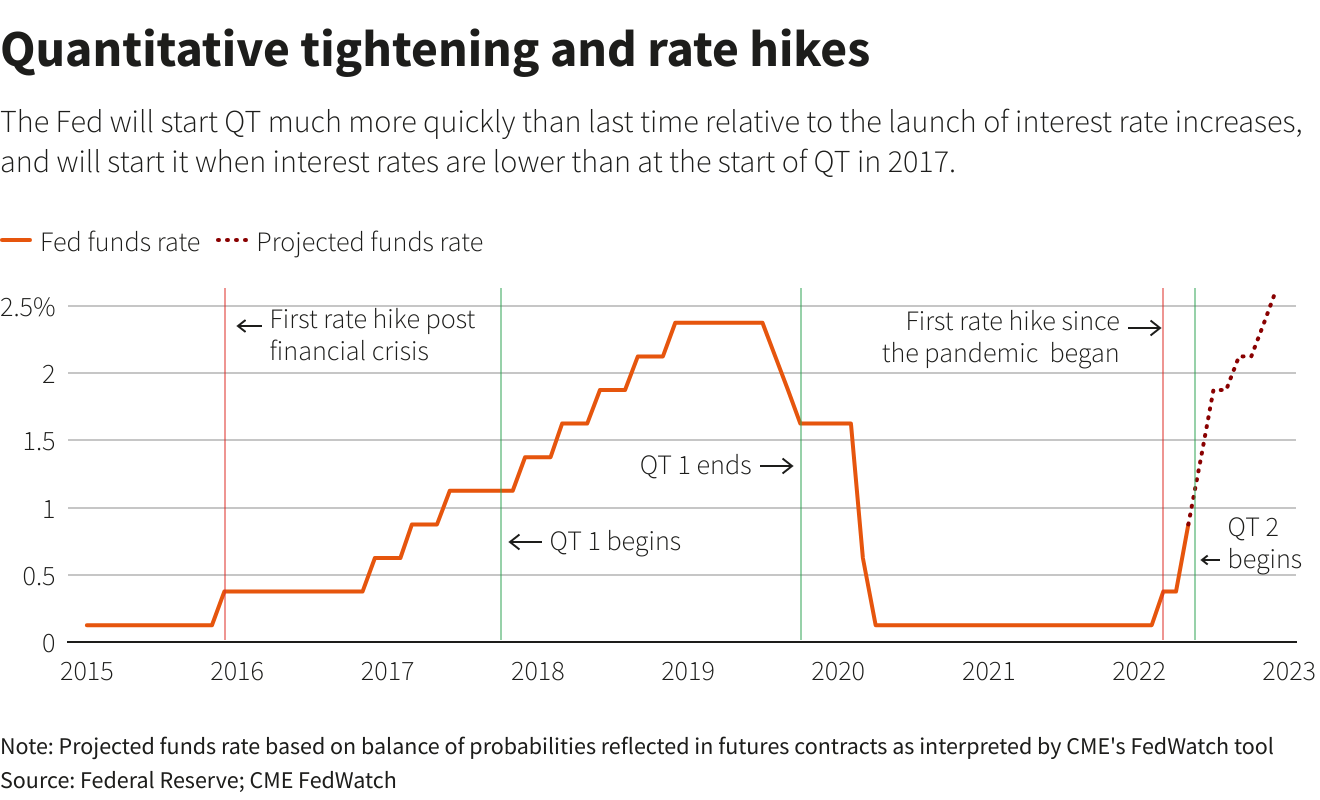

The Federal Reserve hiked interest rates by 50 basis points while knocking the odds of a larger hike (~0.75 or above) later this year, all else equal. The Fed’s holdings of U.S. Treasuries (UST) and mortgage-backed securities (MBS) are set to fall starting June 1.

As expected, the Fed will cut $95 billion a month from its holdings, split between $60 billion of USTs and $35 billion of MBS, per Reuters, in the span of three months.

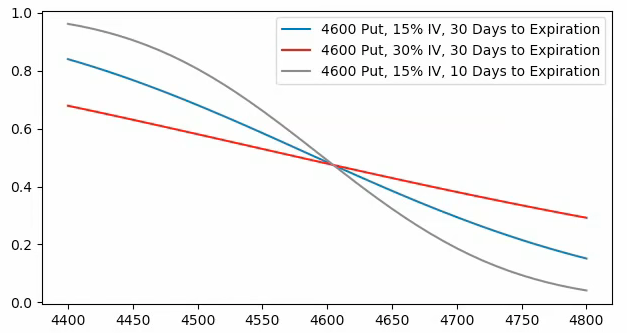

Heading into the FOMC event, markets were sold and protection, particularly that which is shorter-dated, was demanded. This was evidenced via metrics like the VIX’s term structure which had short- and mid-term VIX futures prices higher than those that are longer-term.

The compression of implied volatility after the event affecting existing concentrations of options positioning, particularly at the short-end, coupled with lackluster options buying and selling at the index level, has us questioning the rally’s sustainability.

Ahead is data on jobless claims, productivity, and unit labor costs (8:30 AM ET).

What To Expect

Fundamental: The Fed is raising rates and reducing the size of its balance sheet in light of the economy’s “strong underlying momentum,” as Nordea Bank (OTC: NRDBY) research puts it, a hot labor market and elevated inflation.

During a press conference after the release of meeting statements, the Fed’s Jerome Powell assuaged participants of their fears regarding a 75 basis point hike in later meetings.

Instead, it’s likely the fed tightens twice more by 50 basis points before scaling back to 25 basis point hikes, helping bring inflation down to the 2% target.

On June 1, the Fed will start the process of balance sheet reduction at $47.5 billion ($30B UST and $17.5B MBS) a month for the first three months. This will increase to $95 billion ($60B UST and $35B MBS), after, “roughly double the maximum pace of $50 billion a month targeted in the 2017-2019 cycle.”

With QT, central banks remove assets from their balance sheet “either through the sale of assets they had purchased or deciding against reinvesting the principal sum of maturing securities,” as JH Investment Management explains.

Since March, the Fed’s balance sheet was at $9 trillion, steadied by the reinvestment of proceeds from maturing securities. After a small run-up, starting in September, the Fed will allow for a maximum of $95 billion to roll off without reinvestment.

Per MarketWatch, “In this cycle, one key to markets is when the Fed might actually sell some of its holdings of mortgages $2.7 trillion. This will ripple out through U.S. debt markets.”

This, however, “would be announced well in advance,” enabling “suitable progress toward a longer-run … portfolio composed primarily of Treasury securities.”

When bonds fall in value, their yields rise. This may have the effect of driving yield-hungry investors into relatively less risky asset categories.

Positioning: There was a large squeeze, post-FOMC.

The prevailing narrative is that participants’ fears, with respect to how aggressive the Fed would tighten, were assuaged.

Per Standard Chartered’s (OTC: SCBFY) Steve Englander, at its core, “it is fair to say that positioning and excess pessimism reflect a big part of the market reaction.”

“Overall, the tone was much more balanced than at the January and March FOMC meetings.”

As discussed in the past few letters, markets were stretched and participants were demanding protection in size. To quote the May 2 letter:

“Barring a worst-case scenario, if markets do not perform to the downside (i.e., do not trade lower), those highly-priced (often very short-dated) bets on direction will quickly decay, and hedging flows with respect to time and volatility may bolster sharp rallies.”

That’s precisely what happened. The question now is whether there’s a sustained reversal.

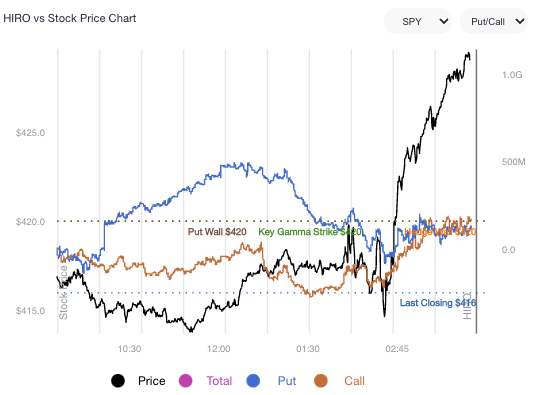

Based on SpotGamma’s Hedging Impact of Real-Time Options Indicator (HIRO), participants’ reaction to the FOMC was lackluster and capital was not committed to bets further out in price and time at higher or lower prices.

If participants start to concentrate their bets at higher prices, further out in time, that confirms the odds of sustained follow-through. If not, it’s likely that indexes, after a short-term relief, will succumb to fundamental weaknesses.

According to Kai Volatility’s Cem Karsan, the rally was purely a function of “structural buyback” and the baseline is that the bear trend holds.

This is because Fed is expected to continue withdrawing liquidity, and this will prompt risk assets to converge with fundamentals as “QT is a direct flow of capital to capital markets.”

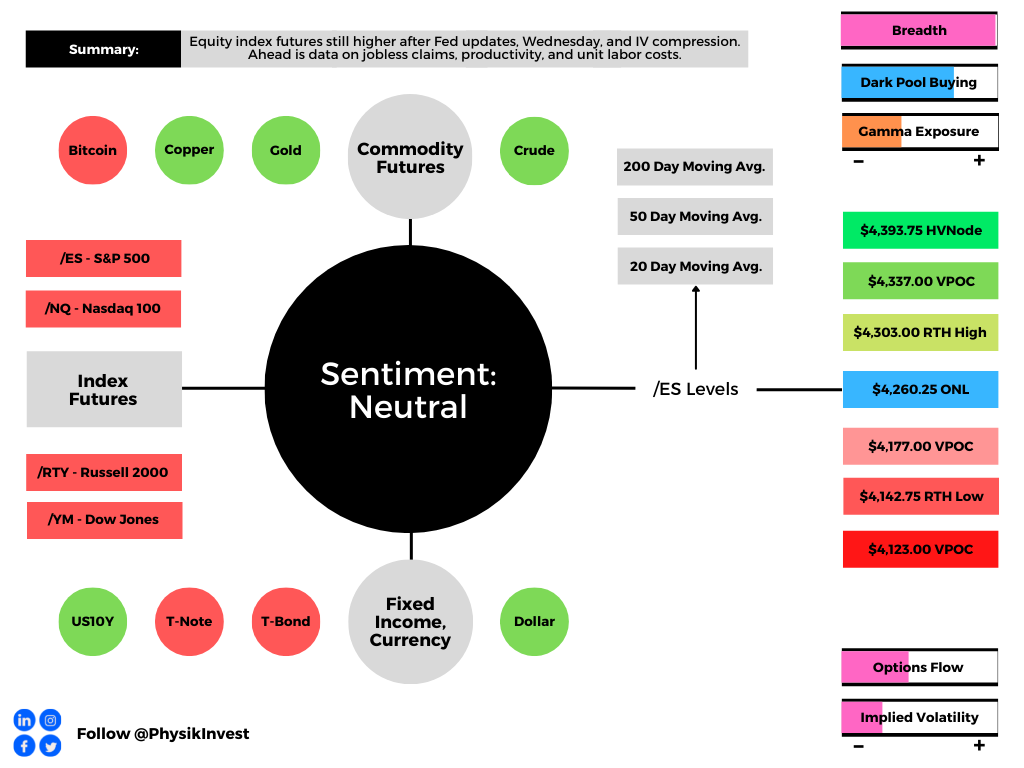

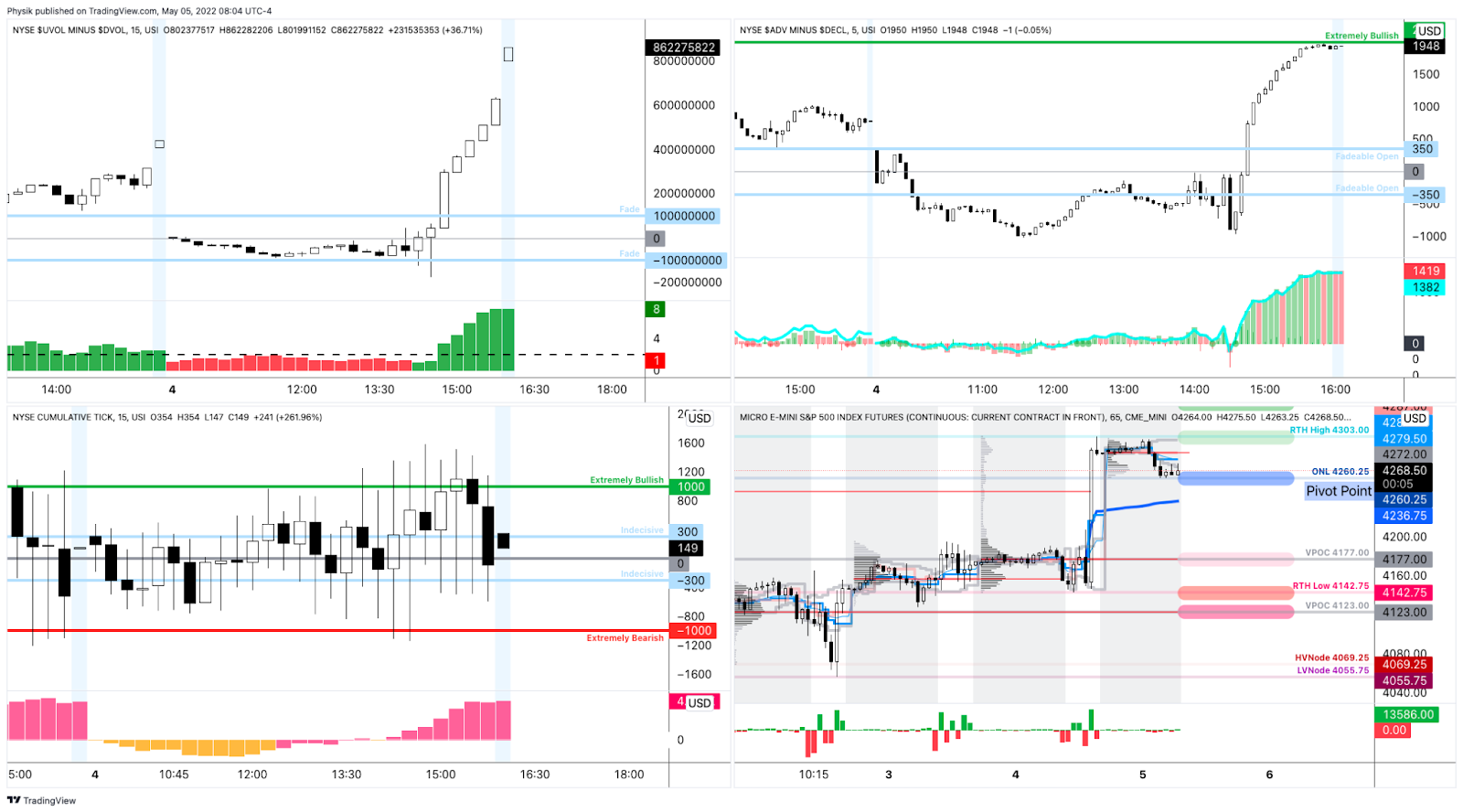

Technical: As of 6:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,260.25 overnight low (ONL) puts in play the $4,303.00 regular trade high (RTH High). Initiative trade beyond the RTH High could reach as high as the $4,337.00 untested point of control (VPOC) and $4,393.75 high volume area (HVNode), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,260.25 ONL puts in play the $4,177.00 VPOC. Initiative trade beyond the VPOC could reach as low as the $4,142.75 RTH Low and $4,123.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Strong advance, yesterday, characterized by very supportive breadth.

The weaker of the indexes we monitor – the Invesco QQQ Trust Series 1 (NASDAQ: QQQ) – just retook a major VWAP anchored from the lows of March 2020.

That indicator denotes the level at which the average buyer/seller is in. In other words, that’s the fairest price to pay for Nasdaq 100 exposure (since March 2020) and, instead of being construed as a so-called supply zone, the level ought to, again, be looked at as a demand area.

What’s next? Looks like there are some key areas where supply is likely to show. Mainly the $340.00 and $360.00 areas in the QQQ are of significance. In the SPY, those areas include $435.00 and $445.00.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

3 replies on “Daily Brief For May 5, 2022”

[…] stock buybacks are lowering SLRs [], and the Fed is about to embark on QT,” Pozsar says. For context, QT (Quantitative Tightening) is the central banking authorities’ removal of balance sheet […]

[…] read our Daily Brief For May 5, 2022, here, for more on the Federal Reserve’s […]

[…] by $17.5 billion per month, ultimately rising to $35 billion, in accordance with our post-FOMC letter published May 5, […]