The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

Overnight, equity indices probed higher, above Thursday’s trade, which established a new swing low. The Cboe Volatility Index (INDEX: VIX) fell while yields were bid and commodities mixed.

Today, we’ll get into some key narratives including crypto turmoil and financial conditions, as well as a validation of some of our trade theses.

Ahead is data on import prices (8:30 AM ET), University of Michigan consumer sentiment and inflation expectations (10:00 AM ET), as well as Fed-speak by Neel Kashkari (11:00 AM ET).

Take care and watch your risk.

What To Expect

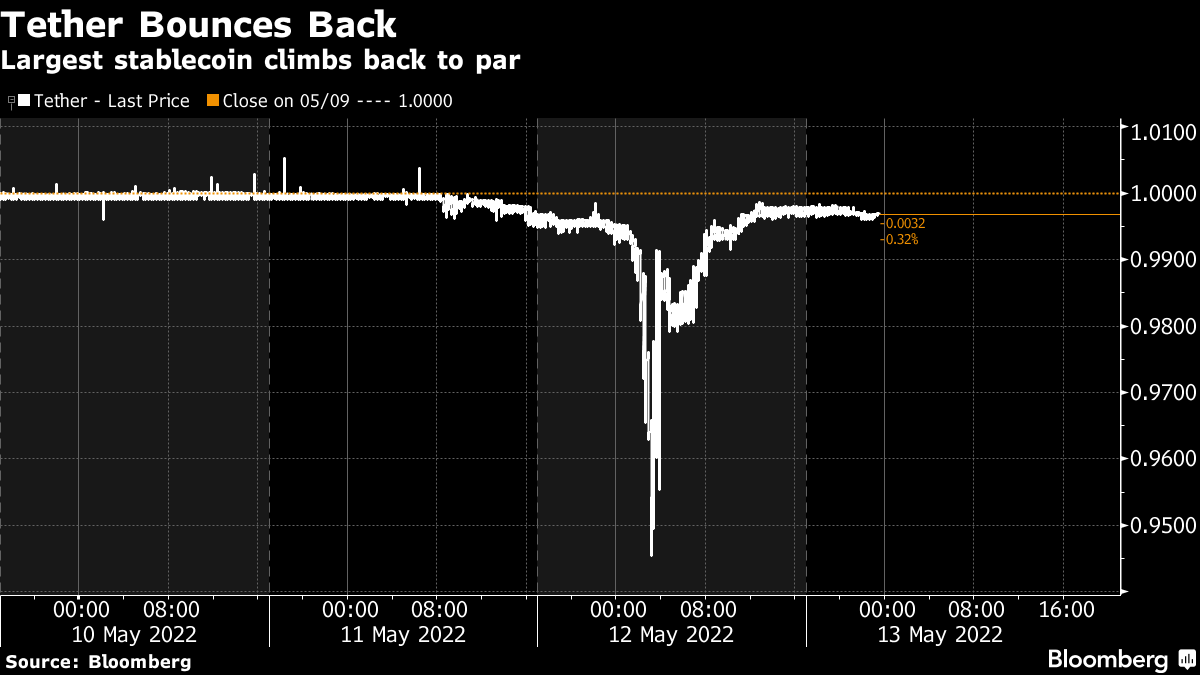

Fundamental: In the news, panic in the cryptocurrency markets eased and Tether (CRYPTO: USDT-USD), the world’s largest stablecoin, backed by commercial paper and U.S. Treasuries, climbed back to par.

JPMorgan Chase & Co’s (NYSE: JPM) Teresa Ho said there would be little impact on traditional funding markets while, according to Barclays PLC’s (NYSE: BCS) Joseph Abate, redemptions in Tether, which has a market value just shy of $90-100 billion, would only “cause meaningful strains in money markets should they exceed half of the stablecoin’s total holdings.”

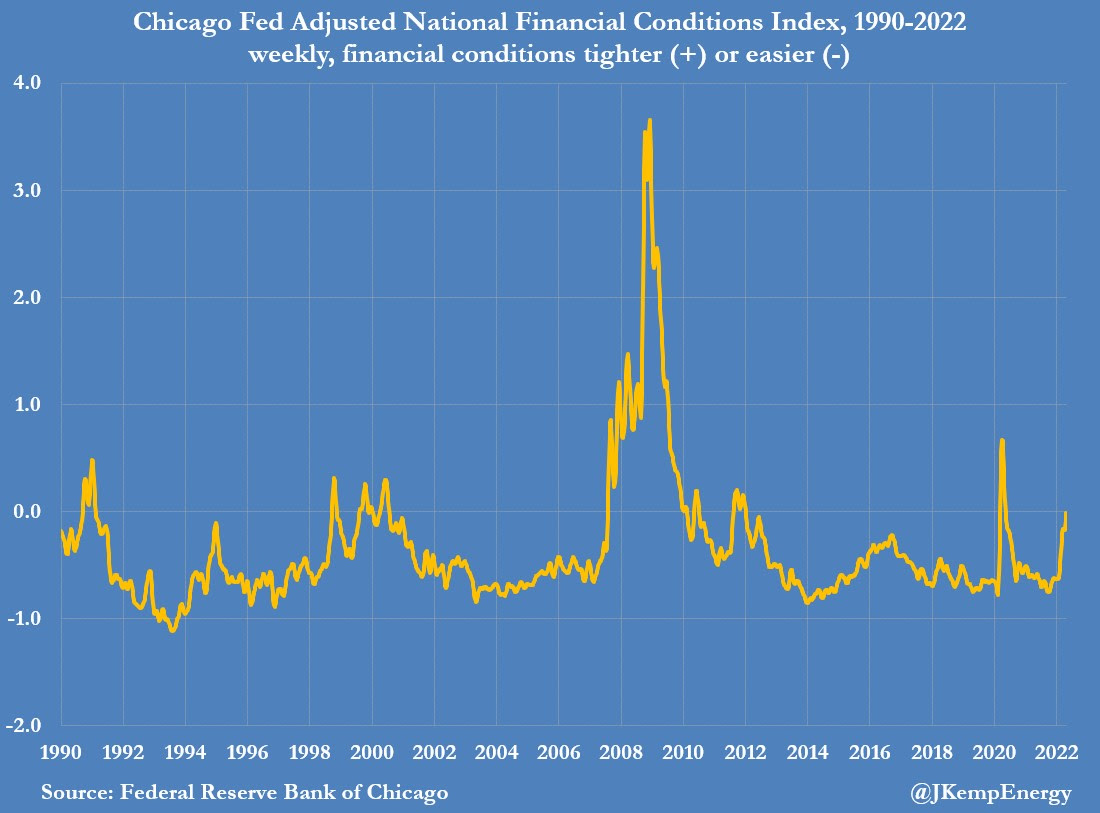

Also in the news are rising interest rates (e.g., mortgage rates up to ~5.30%) and a weak equity market (e.g., S&P 500 lower ~20%), among other things, feeding into a tightening of financial conditions (which is how monetary policy impacts the economy).

“Financial conditions for households and businesses wanting to borrow or raise capital tightened again last week and are the most restrictive since the first wave of the pandemic in 2020 and before that 2012,” Reuters’ John Kemp said.

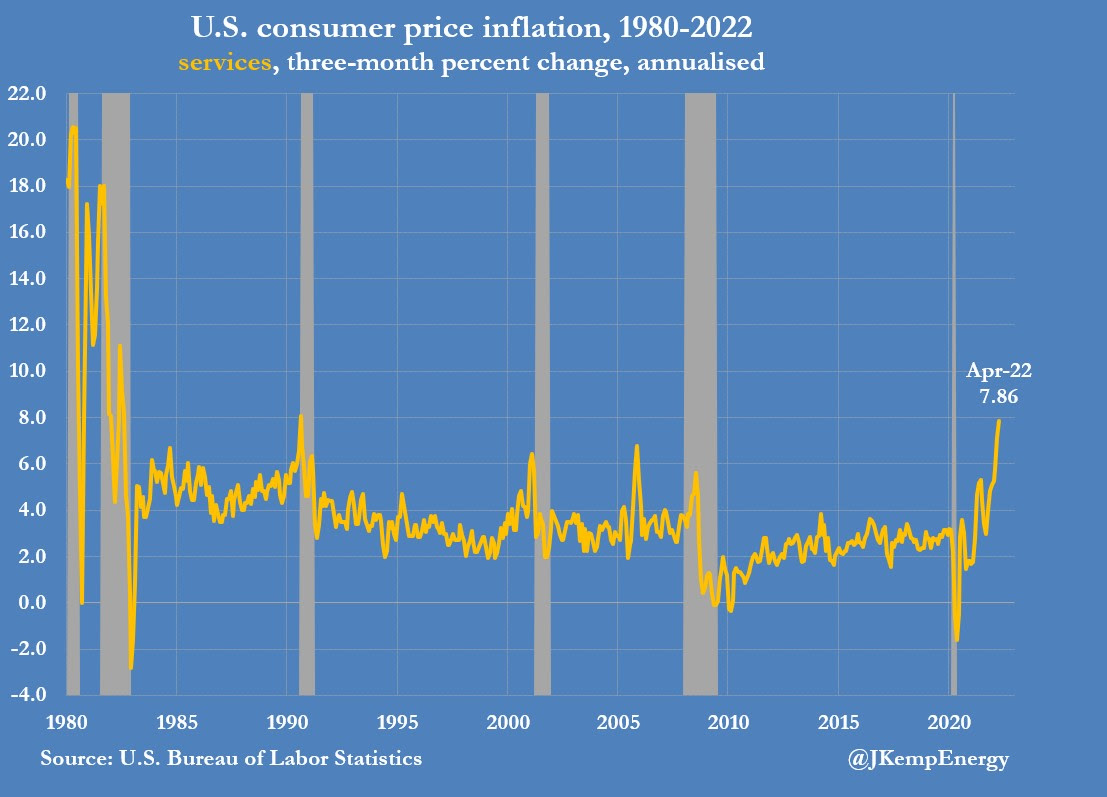

This is as inflation has become “deeply embedded,” spreading from the energy and raw materials-intensive merchandise sector to services.

“Rapid service sector price increases usually signal the imminent arrival of a recession,” Kemp said, pointing to decisions by some public companies like Uber Inc (NYSE: UBER), Twitter Inc (NYSE: TWTR), and Amazon Inc (NASDAQ: AMZN) to slow growth and cut labor forces as a validation of slowing momentum.

The accelerated selling of equities (~$6.2 billion), bonds (~11.4 billion), cash (~$19.7 billion), and some commodities (~$1.8 billion in gold), over the last week, per Bank of America Corporation’s (NYSE: BAC) Michael Hartnett is capitulation.

“The definition of true capitulation is investors selling what they love,” Hartnett said, gauging the prospects that stocks have hit a near-term bottom. “Fear and loathing suggest stocks are prone to an imminent bear market rally, but we do not think ultimate lows have been reached.”

Positioning: In past commentaries, we talked about ways to play a returns distribution that is skewed to the upside (albeit, with large negative outliers).

The following Goldman Sachs Group Inc (NYSE: GS) remark is a validation of what we’ve discussed:

“Even though the VIX’s reaction to recent spot downside has been mild, its high starting point leaves vol high overall, and we like strategies with a short volatility bias, including put selling and 1×2 call spread overlays.”

Mainly, zero- and low-cost bets ($0.00-$1.00 debit to open) that deliver asymmetric payouts (sometimes in excess of $10.00 credit to close) in case of violent and short-lived reversals.

Personally, this letter’s author is structured positive delta and gamma in the Nasdaq 100 (INDEX: NDX) via ratios spread (1×2) and butterfly (1x2x1) structures.

As stated before, width and timing are everything.

Too much time or too narrow may result in asymmetric losses when the demand for upside bets further out in price and time bids the skew that you’re short, relative to the at-the-money volatility you own.

Ten to fifteen days to expiration and 500-1000 points wide, in the Nasdaq 100 (INDEX: NDX), one of the hardest hit of the indexes, work well.

An easy check is whether the spread prices for a debit or credit to close if the underlying moves to the long strike of the spread, all else equal.

Debits (which may run as low as $0.00, depending on trade location) can be offset with credits from put sales.

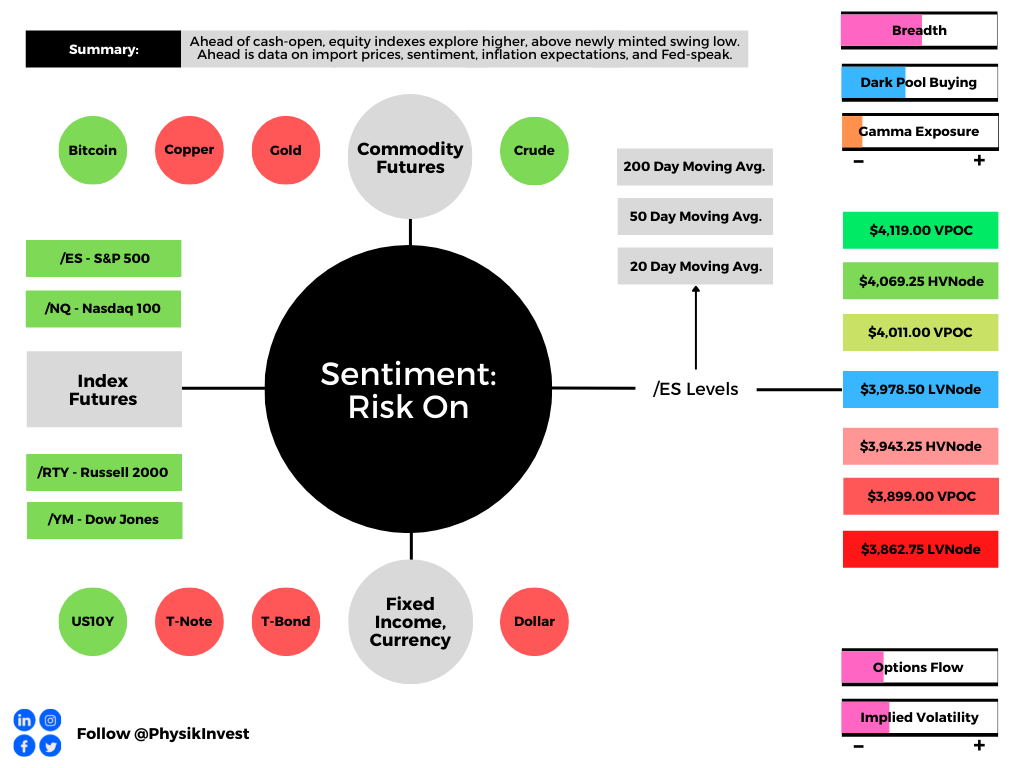

Technical: As of 6:45 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value, suggesting a higher potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $3,978.50 low volume node (LVNode) puts into play the $4,011.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,069.25 high volume area (HVNode) and $4,119.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower; activity below the $3,978.50 LVNode puts into play the $3,943.25 HVNode. Initiative trade beyond the HVNode could reach as low as the $3,899.00 VPOC and $3,862.75 LVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Gap scenarios are in play.

Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator.

Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

3 replies on “Daily Brief For May 13, 2022”

[…] Early on Friday morning, we approached trade too optimistically but, to our credit, we focused on participating with as little risk as […]

[…] continue to focus on participating in upside with as little debit risk as possible, via the use of complex strategies, further validated by quoted […]

[…] the “high starting point” in IVOL makes it possible to put on zero- and low-cost bets that deliver asymmetric payouts in case of violent and short-lived […]