The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 900+ that read this report daily, below!

Administrative

Short and to the point, today, after yesterday’s detailed letter on inflation, monetary policy action, and beyond. Good luck, everyone!

Fundamental

Ongoing is a “messy divorce” between large powers. We have talked about this in the past.

In the news was Putin’s mobilization of troops and renewed warning of a nuclear threat. This is a day after Biden said the US would defend Taiwan against China. In response, Mao Ning, the Chinese foreign ministry spokesperson, said this:

“The US remarks seriously violate the one-China principle … and send a severely wrong signal to the separatist forces of Taiwan independence. China strongly deplores and rejects it and has made solemn complaints with the US side.”

“We will do our utmost to strive for the prospect of peaceful reunification with the utmost sincerity, while we will not tolerate any activities aimed at splitting China and reserve the option to take all necessary measures.”

The aforementioned do more to shift “the pillars of the low inflation world” – de-globalization and populism – which the Federal Reserve (Fed) has a limited toolkit to solve for.

Pending is a large “L”-shaped recession to slow inflation, generate negative wealth effects, lower demand, and position for a recovery that will likely be “fiscally funded industrial policy.”

Shifting to today, the Federal Reserve is to step up its efforts to tame inflation by raising interest rates to the highest level since 2008. The consensus calls for up to a 75 basis point rate hike.

Bloomberg economist Anna Wong, Andrew Husby, and Eliza Winger put forth:

“Powell will emphasize the committee’s determination to hold rates higher for longer. He will be more forthcoming in acknowledging the likely pain involved in bringing down inflation. He may opt not to say that the committee plans to downshift the pace of rate hikes.”

Positioning

Yesterday, we briefly talked about post-event moves which are often positive and driven by the structural “rebalancing of dealer inventory,” per Kai Volatility’s Cem Karsan.

“In the past four Fed Days, the benchmark index has climbed an average of roughly 1.4% on all days, with more than 2% gains on three of the four,” said Bloomberg’s John Authers. Adding, “the S&P 500 has averaged a gain of more than 1% on Fed Days over the last 10 meetings.”

Basically, into the event, traders have demanded protection and bid implied volatility (IVOL).

Should fears be assuaged, the supply of that protection should decrease IVOL, this is what may provide markets a boost.

From thereon, the “second move and final resolution, if you wait for it, is usually tied to the incremental effects on liquidity (QE/QT).”

In the case of the latter, per The Ambrus Group’s Kris Sidial, “[o]utright tails in single stocks continue to be ‘cheap’ relative to what you are seeing in the broad market.”

“Market is discounting any sort of crash risk. Which seems reasonable granted that a lot of the current macro theme is geared towards a longer-term effect.”

Technical

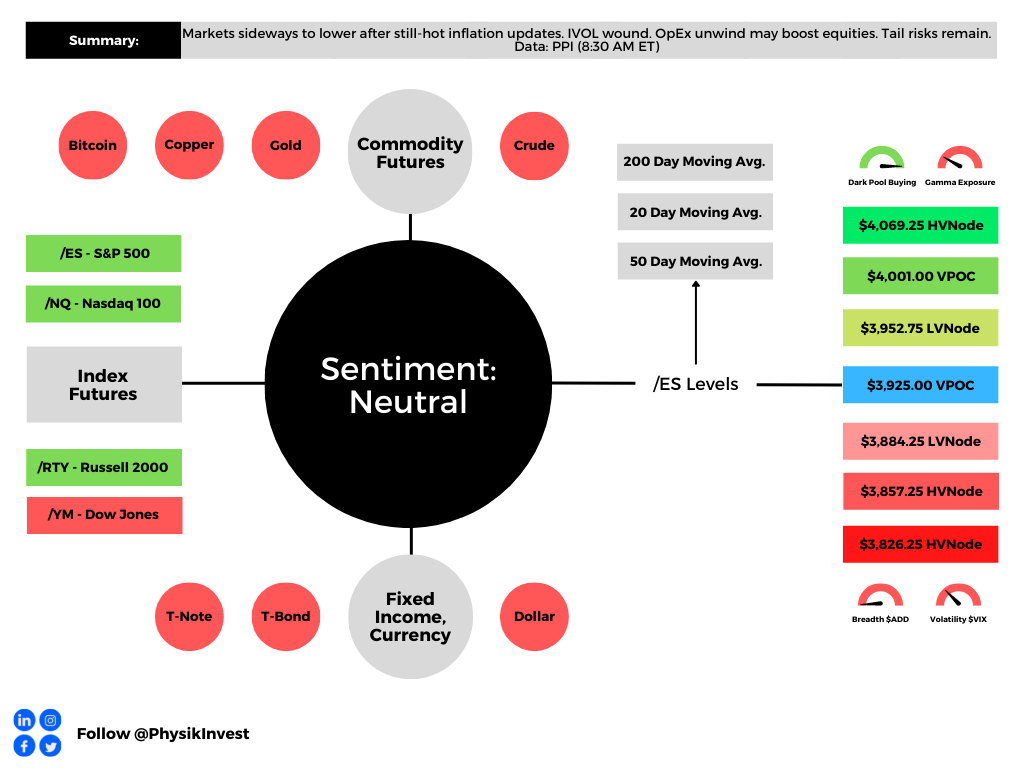

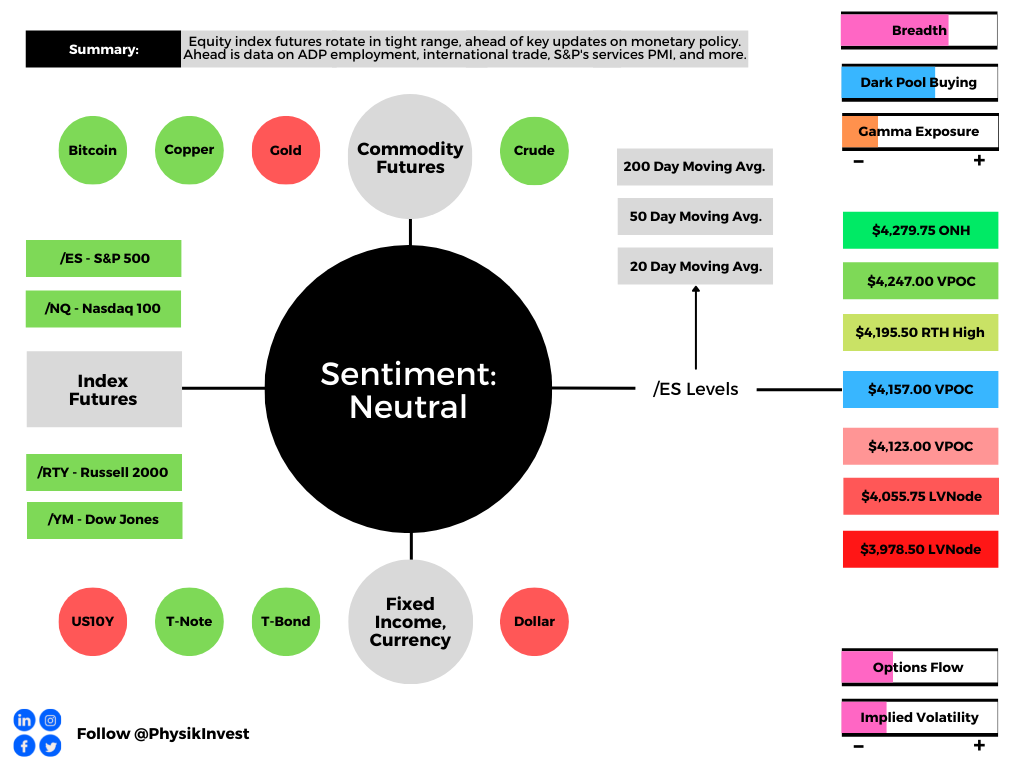

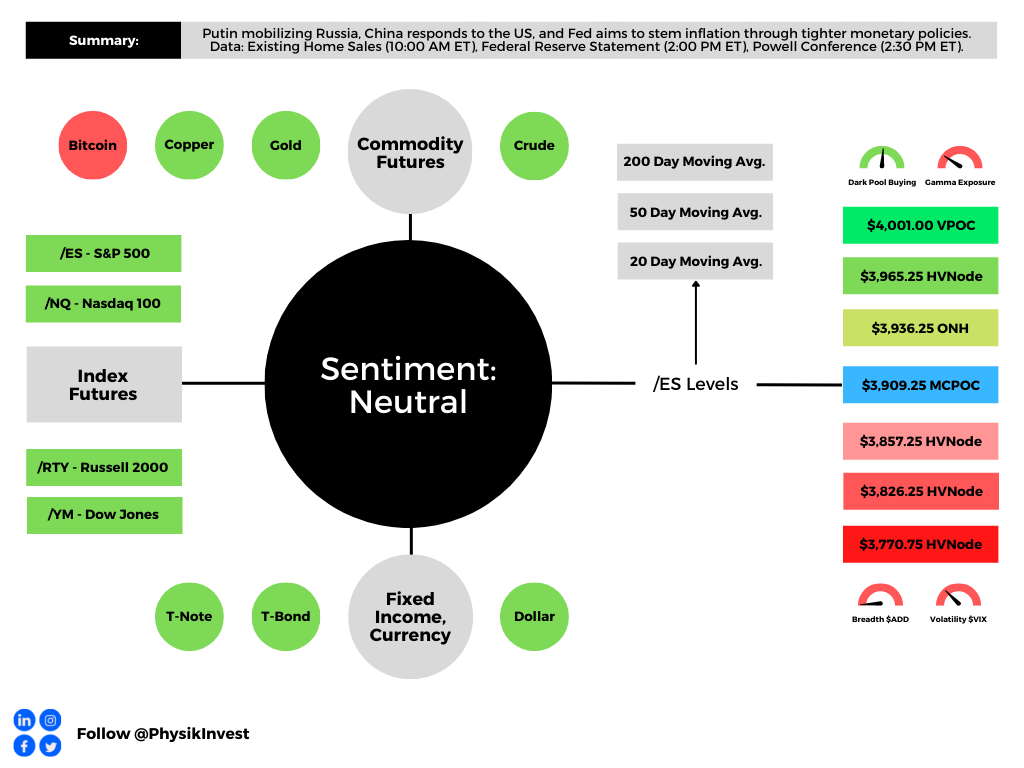

As of 7:00 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,909.25 MCPOC puts into play the $3,936.25 ONH. Initiative trade beyond the ONH could reach as high as the $3,965.25 HVNode and $4,001.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,909.25 MCPOC puts into play the $3,857.25 HVNode. Initiative trade beyond the latter could reach as low as the $3,826.25 and $3,770.75 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.