Editor’s Note: The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Ahead of Friday’s triple witching derivatives expiry, the equity index and most commodity futures auctioned sideways to lower.

Ahead is data on existing home sales and leading economic indicators (10:00 AM ET), as well as Fed-speak by Tom Barkin (1:20 PM ET).

What To Expect

Fundamental: Today’s focus is on market positioning. Therefore, the fundamental section is (more) lighthearted.

Equity markets rose in the context of a sharp multi-month drawdown. This is, in part, masking the concern over Russia’s economic situation, a slowing in the flow of U.S. credit, supply and demand imbalances, the impact of COVID-19, and other things.

Further, in spite of the Federal Reserve’s (Fed) comments on the strength of the economy and its likely resilience in the face of tighter policies, Goldman Sachs Group Inc (NYSE: GS) said the odds of a recession were “broadly in line with the 20-35% odds currently implied by models based on the slope of the yield curve.”

The forecast “implies below potential growth in 2022 Q1 and 2022 Q2 and potential growth for 2022 overall.”

With the Fed now eyeing about six more rate hikes in 2022 – putting the policy rate at ~2.8% before 2024 – commentators were quick to point out the “central bank’s patchy record on not tipping the economy into recession.”

Alhambra Investments’ Jeffrey Snider, however, made an interesting point.

“To believe the Fed is behind all this or can do something useful about it, like the rate hikes you would have to be” born yesterday, he said.

“On the contrary, bond curve recession probabilities are more attuned to why production levels have struggled despite prices, having more to do with global conditions and the lack of actual volume expansion. Consumer, producer, and commodity prices have obscured, to some substantial extent, the true underlying economic situation.”

Moreover, Goldman forecasts the S&P 500 (INDEX: SPX) to end 2022 near $4,700.00 (down from $4,000.00), ~6% higher than today’s prices.

“The S&P 500 has dropped about 24% from peak-to-trough around past recessions (based on the median),” Goldman said in one newsletter.

“But when the U.S. economy avoids a sustained contraction after a 10% market correction, the index has returned 15% over the next 12 months.”

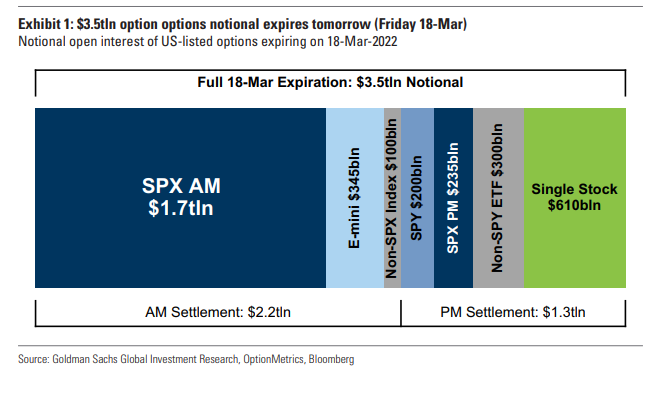

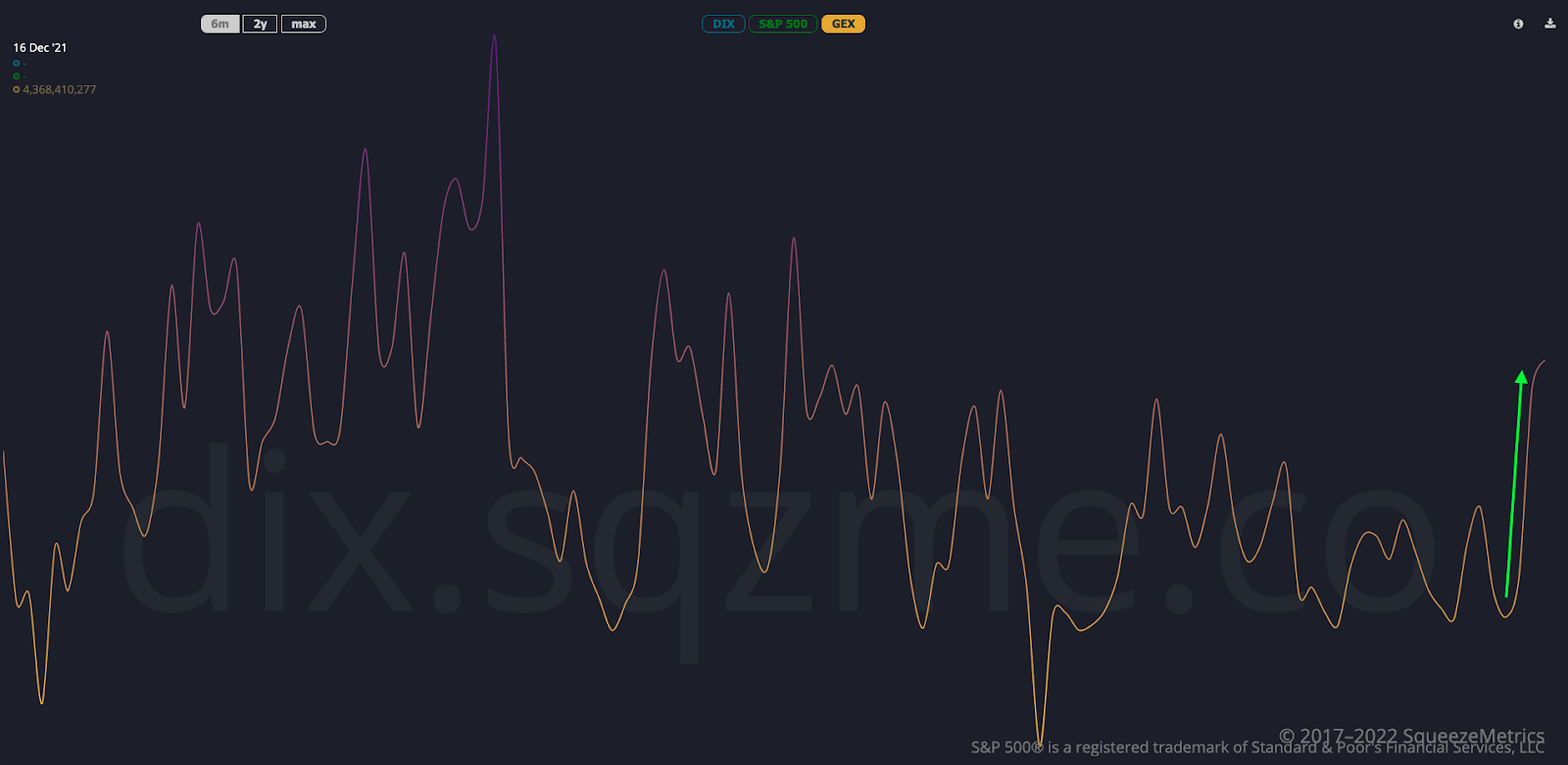

Positioning: Friday marks the quarterly triple witching options expiry and index rebalancing.

Through this event, ~$3.5 trillion in options are set to expire, according to Goldman, with “more near-the-money options are maturing than at any time since 2019.”

In terms of the index rebalance, according to Howard Silverblatt of S&P Global Inc’s (NYSE: SPGI) Dow Jones Indices, “the rebalance in the index alone could spur $33 billion of stock trades.”

This newsletter has talked about the implications of derivatives and their expirations, too, ad nauseam.

Mainly, stock moves and options activity is more correlated and this is the result of participants’ increased exposure to derivatives products (particularly those with less time to expiration).

The demand for this derivatives exposure is transmitted to underlying stocks, via the risk management of counterparties; with option volumes heightened, related hedging flows may represent an increased share of volume in underlying stocks.

As I talked about this in conversations with the Ambrus Group’s Kris Sidial and Kai Volatility’s Cem Karsan, among others, the counterparties’ response to this options trading is impactful (and often predictable).

“Moreover, heading into Wednesday’s FOMC, we saw the market well-hedged,” SpotGamma, an options modeling and analysis service explained. “Participants’ demand for protection is concentrated in options with little time to expiry (given the monthly options expiration and roll-off a significant size of S&P delta).”

“Adding, the compression of volatility [post-FOMC and into OPEX], coupled with trade higher, solicits less counterparty hedging of put protection … [and] less positive delta = less selling to hedge = less pressure.”

So, at a high level, this week’s events (a ”rally [that’s] been fueled by dealers covering short positions to balance exposures while demand for stock hedges is elevated”) have bolstered positive price action.

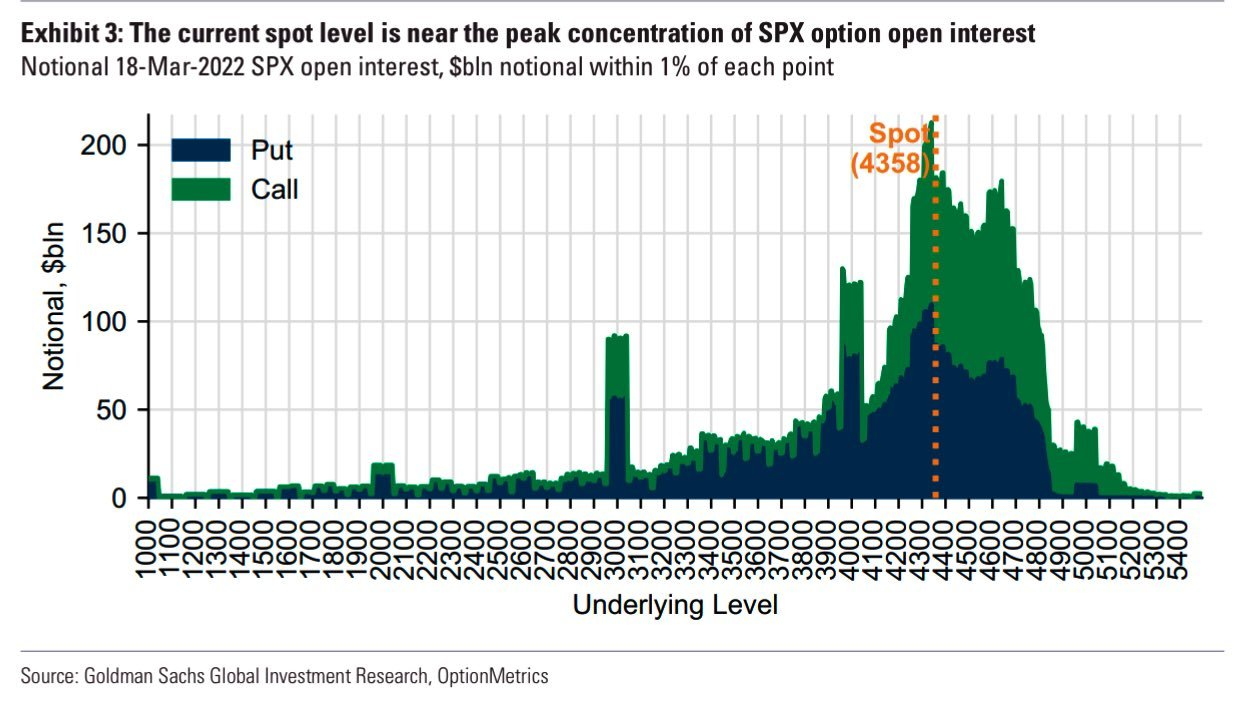

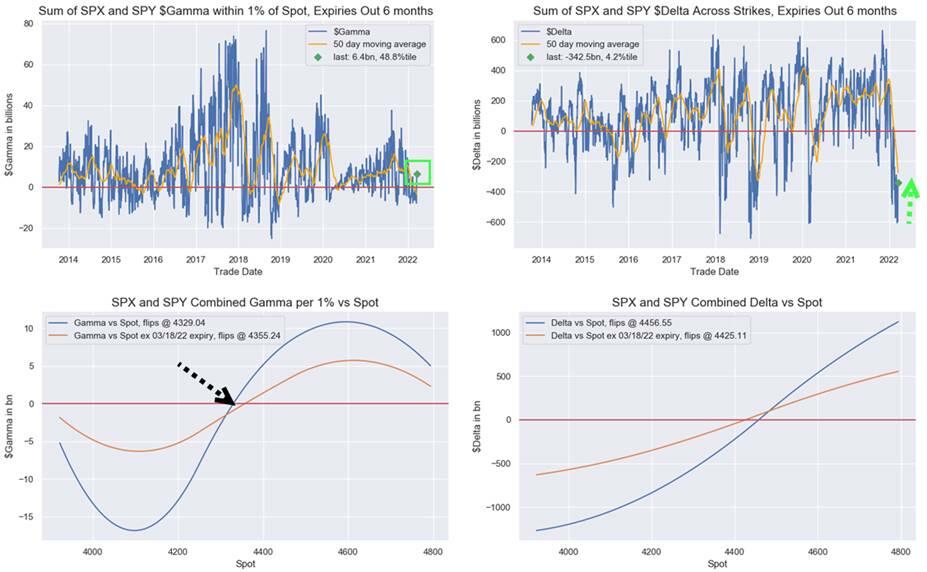

What’s interesting, also, is the S&P 500’s response to the $4,400.00, level. At this level is a concentration of call exposure.

As noted before, the dominant customer positioning, at least at the index level, is short call and long put (i.e., finance downside insurance by selling upside to hedge equity exposure).

The counterparty, in such a case, is short downside and long upside protection; when volatility contracts and underlying prices move higher, the put side, as noted above, solicits less active hedging whilst the call side solicits more active hedging.

In other words, the counterparty has less exposure to negative gamma (from puts) and more exposure to positive gamma (from calls), meaning gains are multiplied to the upside).

Knowing that “the range of spot prices across which option deltas shift from near-zero to near-100% becomes very narrow as options approach maturity (and at maturity, options on one side of the settlement value have zero delta and the other side have 100% delta),” trading into that concentration of calls (which have increased sensitivity to direction or gamma) quickly adds to counterparty positive delta exposure.

This must be offset with counterparty negative delta in the underlying (selling futures and stock to hedge). If there are enough “contracts sitting close to the spot price this time around,” that leads to more frenetic hedging as participants “actively trade around those positions,” and pressure upside, even.

Ultimately, this post-FOMC price rise may put the market in an underhedged position. In such a case, as talked about yesterday, new demand for protection would add fuel to weakness (later).

“I’ve never seen an environment where you’ve had so many potential overhangs in the market that can not be controlled,” said David Wagner, a portfolio manager at Aptus Capital Advisors. “We’ll see if people can see to redeploy their puts.”

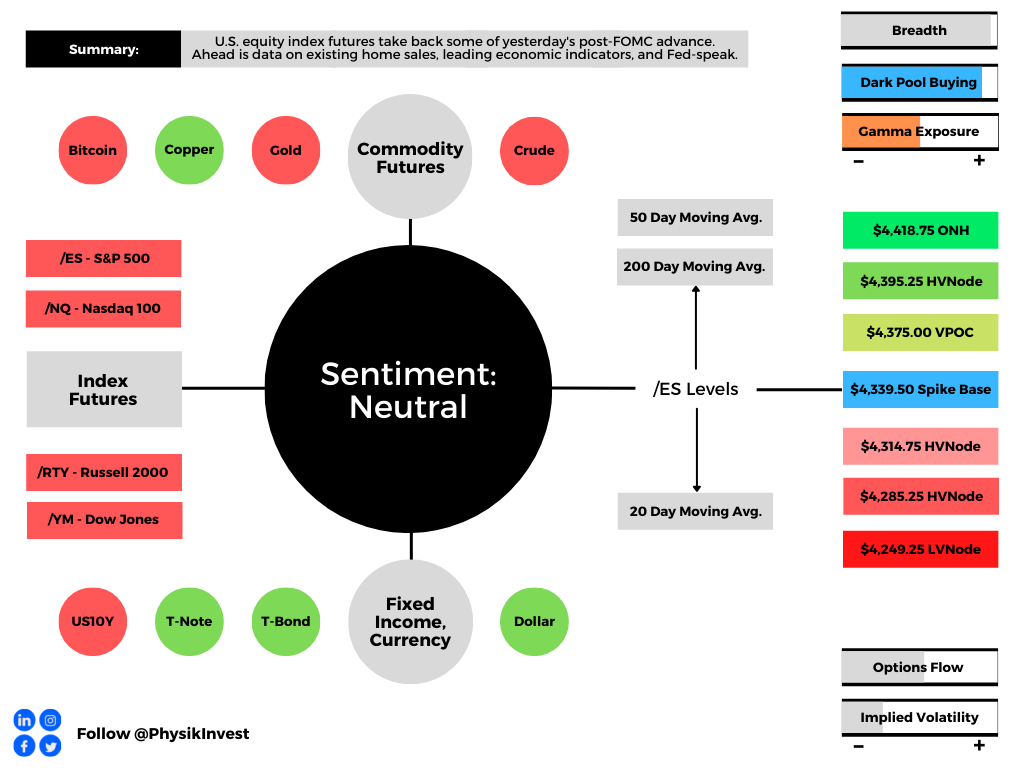

Technical: As of 6:45 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,395.25 high volume area (HVNode) puts in play the $4,418.75 overnight high (ONH). Initiative trade beyond the ONH could reach as high as the $4,438.25 HVNode and $4,464.75 low volume area (LVNode), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,395.25 HVNode puts in play the $4,355.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as low as the $4,314.75 and $4,285.25 HVNodes, or lower.

Considerations: Push-and-pull, as well as responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.