Hey team, you’re going to have to forgive me. Still am traveling through the rest of this month. Therefore, coverage will remain sporadic and less in-depth. Apologies and take care!

What Happened

Overnight, equity index futures were mixed after last week’s liquidation alongside news that the Federal Reserve was interested in sharper interest-rate hikes and balance-sheet reductions to stem inflation.

China equities were weak on the implications of COVID-19 outbreaks, among other things.

Some Russian entities entered into effective default, as ruled by markets. The conflict between Russia and Ukraine, that spurred crippling economic sanctions, is ongoing.

And, in other news, some Bitcoin (CRYPTO: BTC) pundits suggest weakness in risk assets, like technology, may bring down cryptocurrency.

Crypto prices “do not trade on the fundamentals of being peer-to-peer, decentralized, censorship-resistant digital networks designed for the transfer of money,” explained BitMEX founder Arthur Hayes on correlations with the Nasdaq 100 trading at record highs.

Crypto “will lead equities lower as we head into the downturn, and lead equities higher as we work our way out of it.”

Ahead is data on NY Fed median 1- and 3-year expected inflation (11:00 AM ET). Fed-speak by Charles Evans (12:40 PM ET). The quarterly earnings season begins this week. Bank stocks to start reporting Wednesday, April 13.

What To Expect

Fundamental: The ruling narrative, so to speak, is concerned with the management of inflation through monetary policies, credit impulse contractions, as well as the implications of Russia’s invasion of Ukraine, China’s COVID-19 actions, and beyond.

The Federal Reserve’s (Fed) roadmap for shrinking the balance sheet and raising rates was revealed in the recent release of Federal Open Market Committee (FOMC) minutes.

“The FOMC stayed far too easy for far too long and has belatedly realized their mistake,” said Stephen Stanley, chief economist at Amherst Pierpont Securities LLC.

“They are now scrambling to get policy back to neutral as quickly as they can. Once they arrive at something close to neutral, they will have to ascertain over time how far into restrictive territory they have to move to get inflation back under control.”

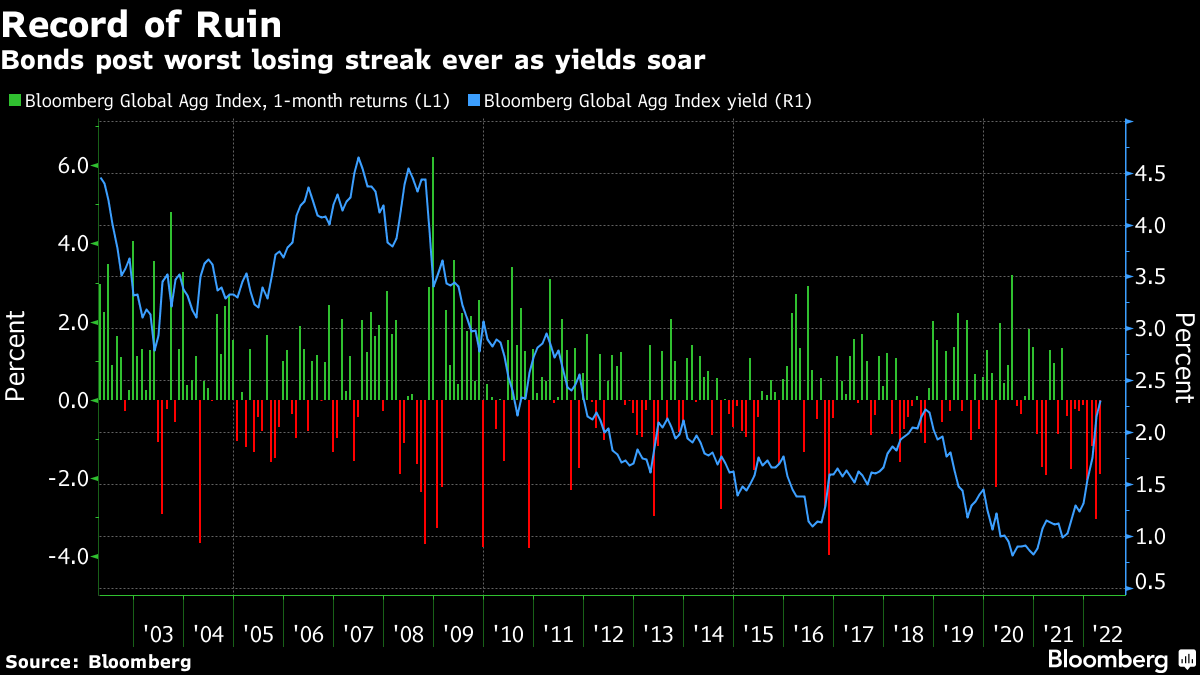

Moreover, as talked about in past commentaries, quantitative tightening (QT) amplifies the impact of rate hikes.

Per statements by JH Investment Management, through QT, central banks remove assets from their balance sheet. This is “either through the sale of assets they purchased or deciding against reinvesting the principal sum of maturing securities.”

With that, we note that when bonds rise in value, their yields decline; “when the Fed embarks on bond-buying program[s] to support the U.S. economy, … [it nudges] the prices of these assets higher while pushing yields lower, which also has the effect of driving yield-hungry investors into relatively riskier asset categories that promise high returns.”

As liquidity is removed, this may prompt risk assets to converge with fundamentals.

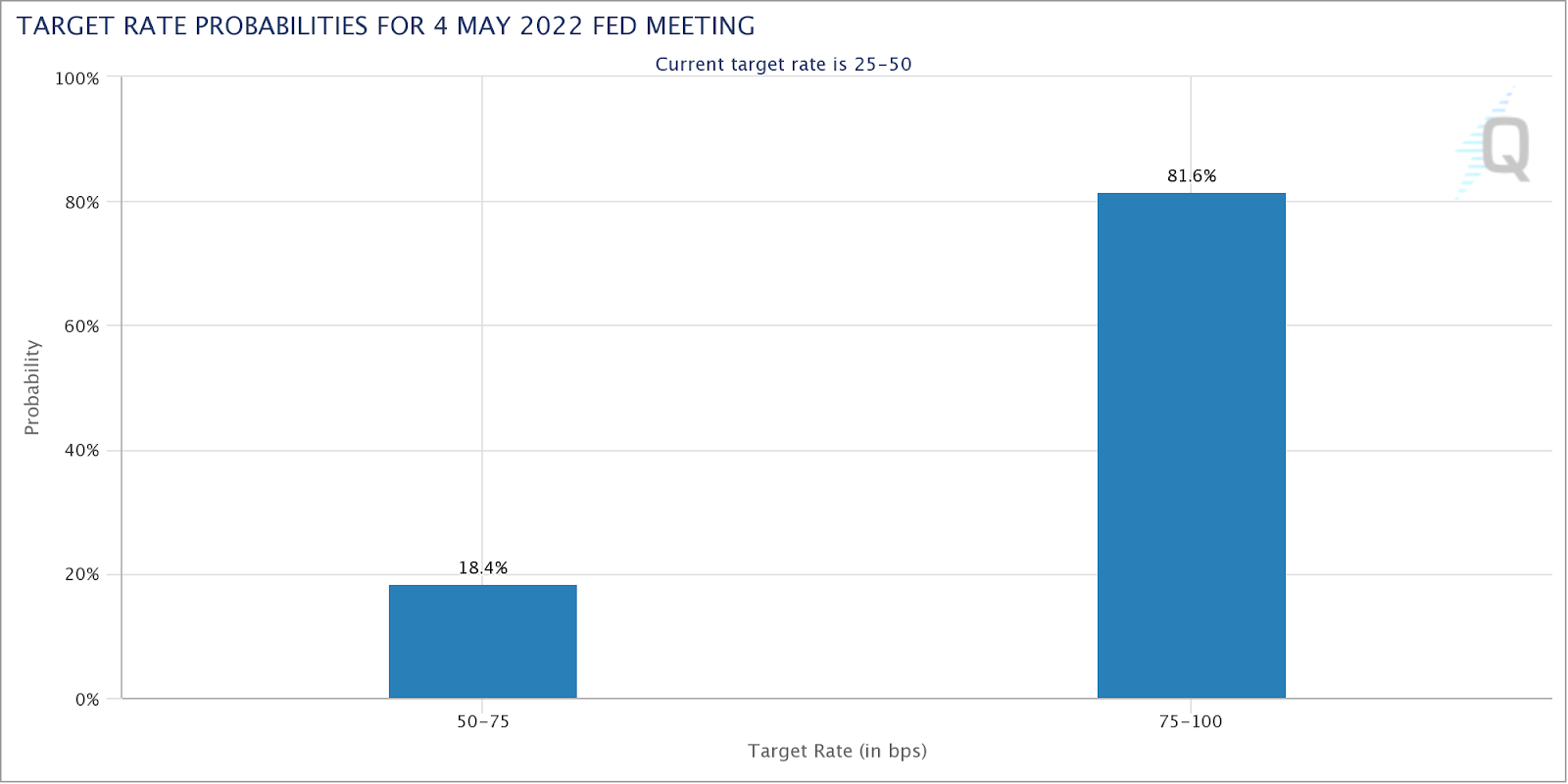

At present, via CME Group Inc’s (NASDAQ: CME) FedWatch tool, participants are pricing in a heightened probability of a half-point hike next month.

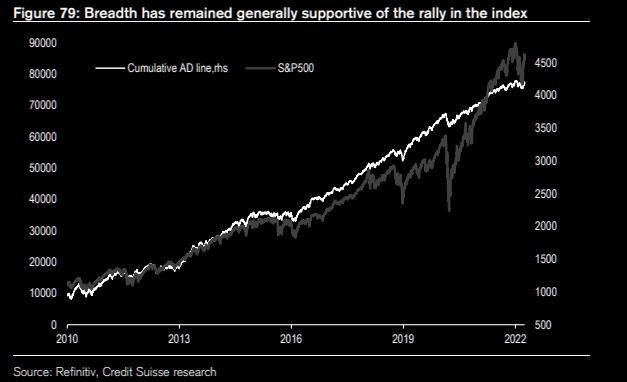

Notwithstanding, per Credit Suisse Group AG (NYSE: CS) research, there has been no meaningful breadth disconnect; breadth remains supportive of higher S&P 500 prices.

At the same time, JPMorgan Chase & Co’s (NYSE: JPM) Mislav Matejka sees continued gains in earnings while equity versus credit and bond yields are still supportive of valuations.

Positioning: Keeping this section light, today.

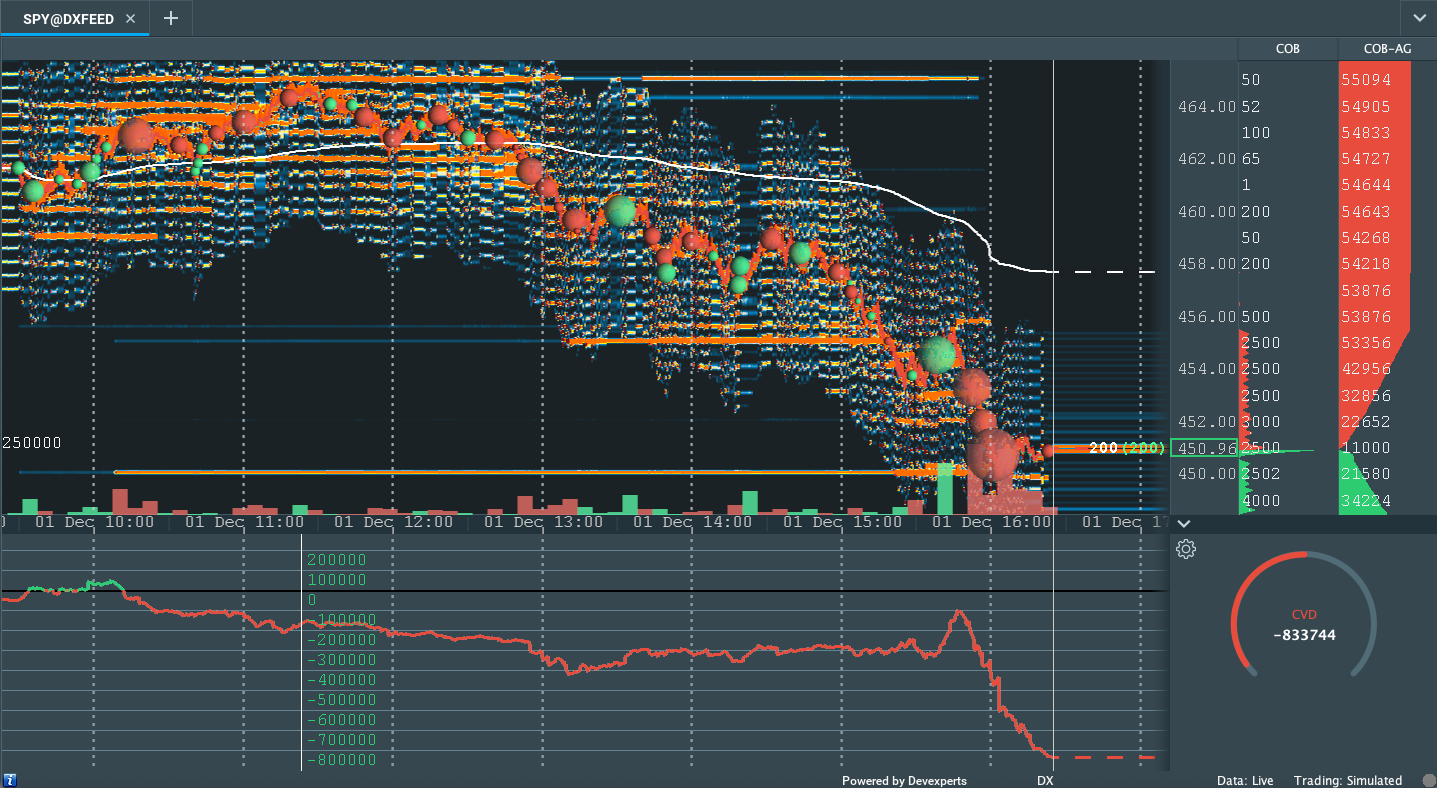

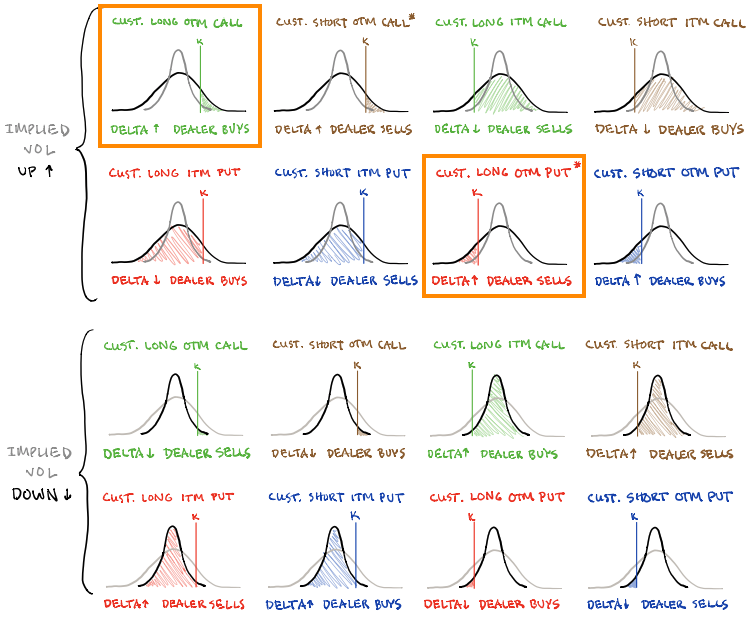

After quarterly rebalances and options expiries, the reduction in counterparty exposure to positive gamma freed indexes (i.e., unpinned), as expected.

Why?

We see counterparties as those participants who take the other side of customer trades. The collapse in realized volatility and the move higher in equity markets solicited counterparties’ decreased (increased) hedging of put (call) options.

The naive assumption is that counterparties are short (long) put (call) protection. When implied volatility declines and underlyings move higher, counterparties have less (more) exposure to amplified losses (gains).

To hedge, they sell into strength and buy into weakness, basically.

As participants start to concentrate their bets in shorter-dated expiries, at higher prices, counterparties take from underlying movement in their provision of liquidity. It takes an options expiry, or some exogenous event, to disrupt this balance.

That happened at the end of last month. Since then, increases in implied volatility and lower underlying equity prices have helped pressure indexes and increase realized volatility.

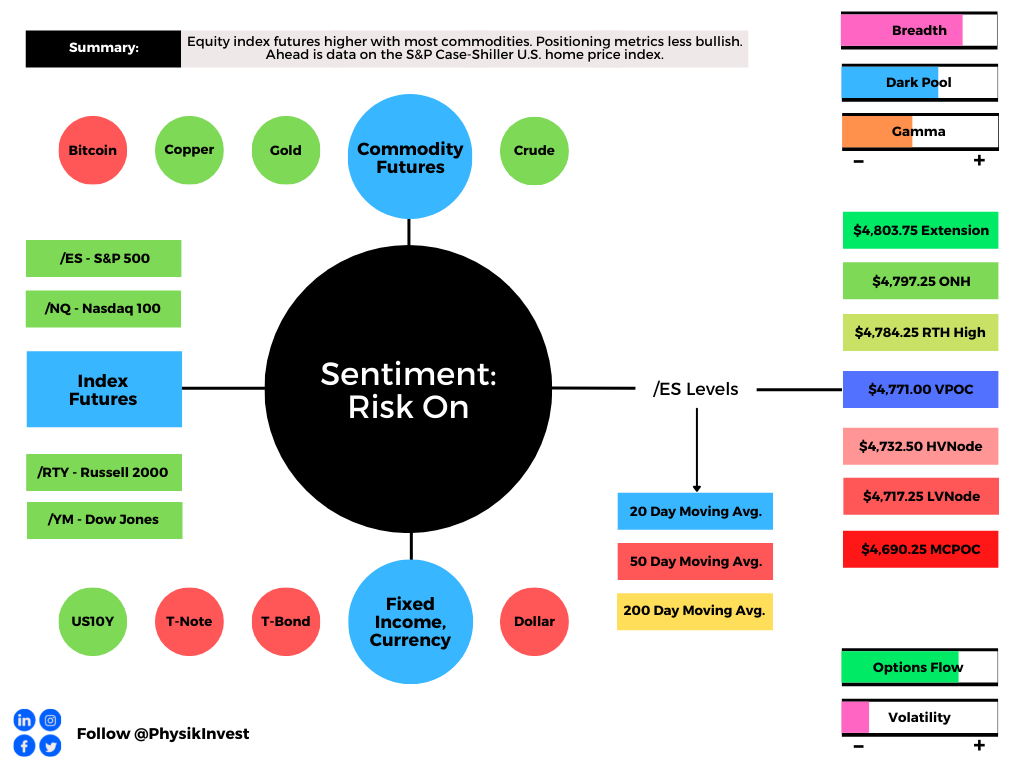

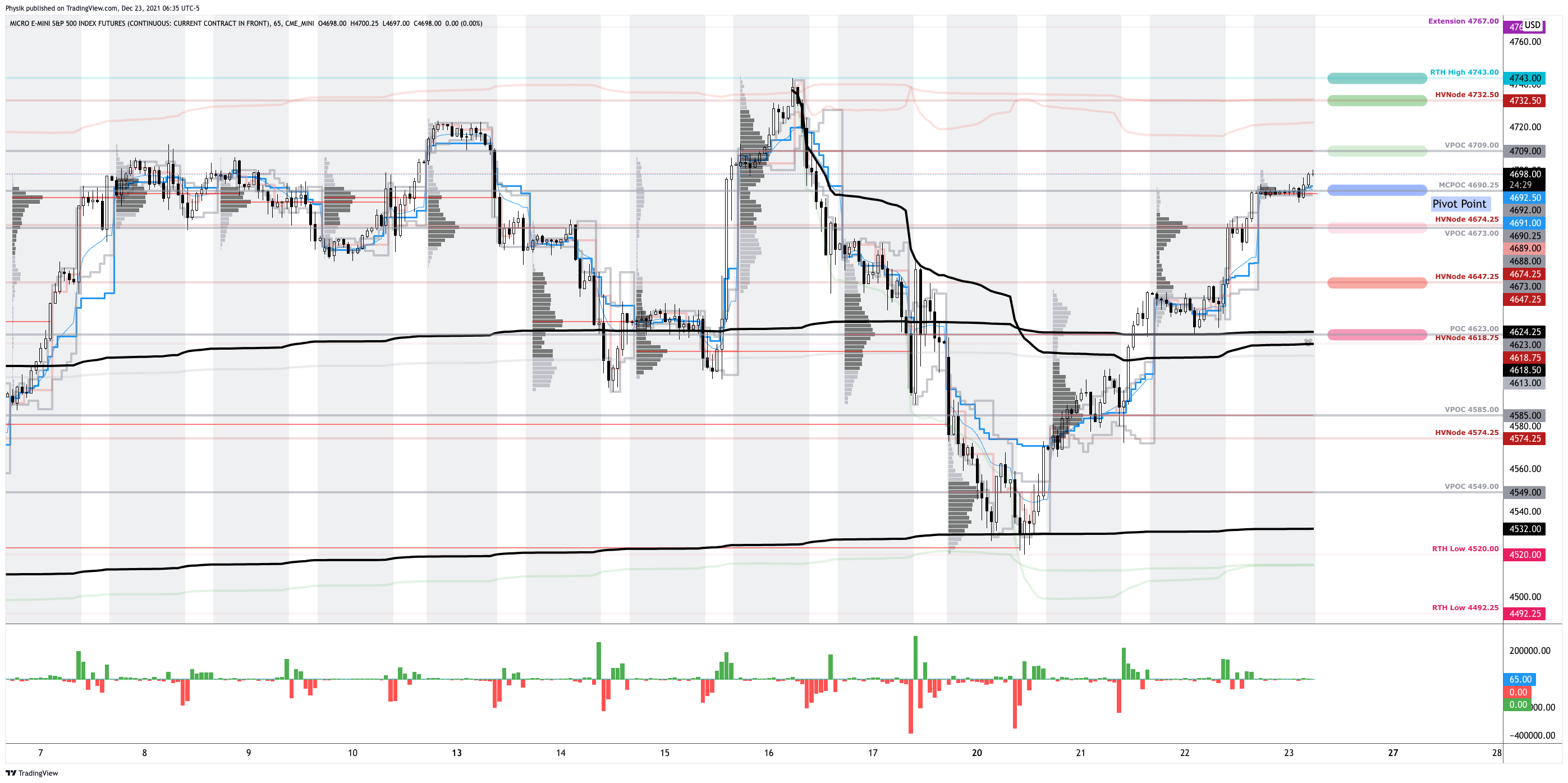

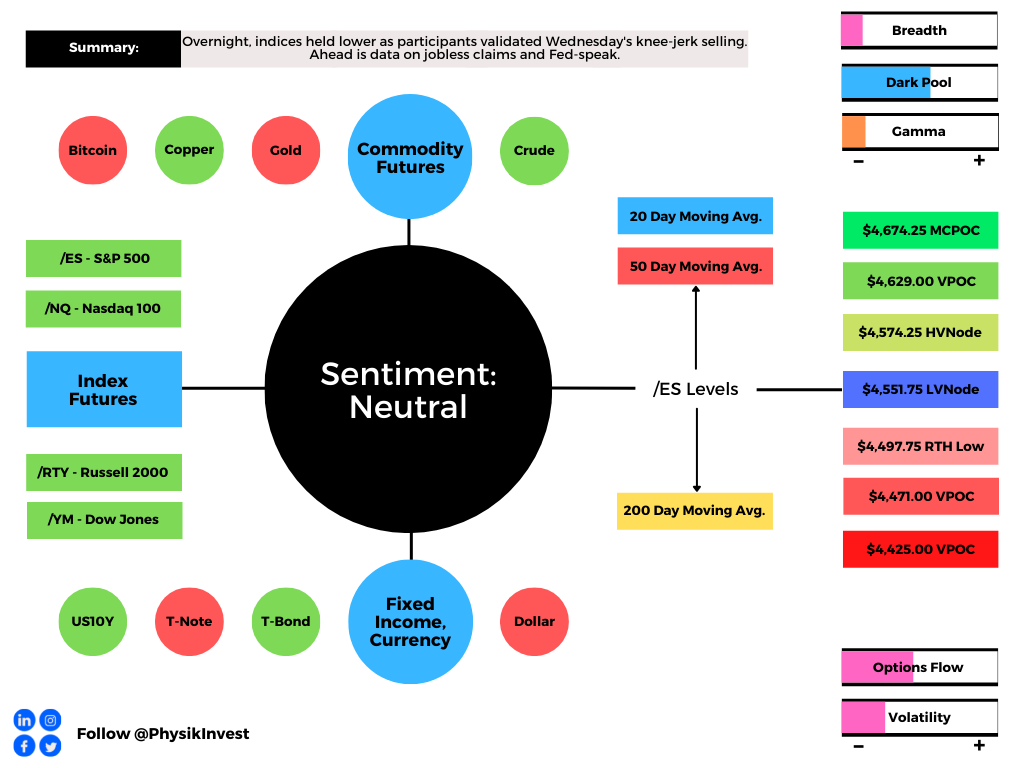

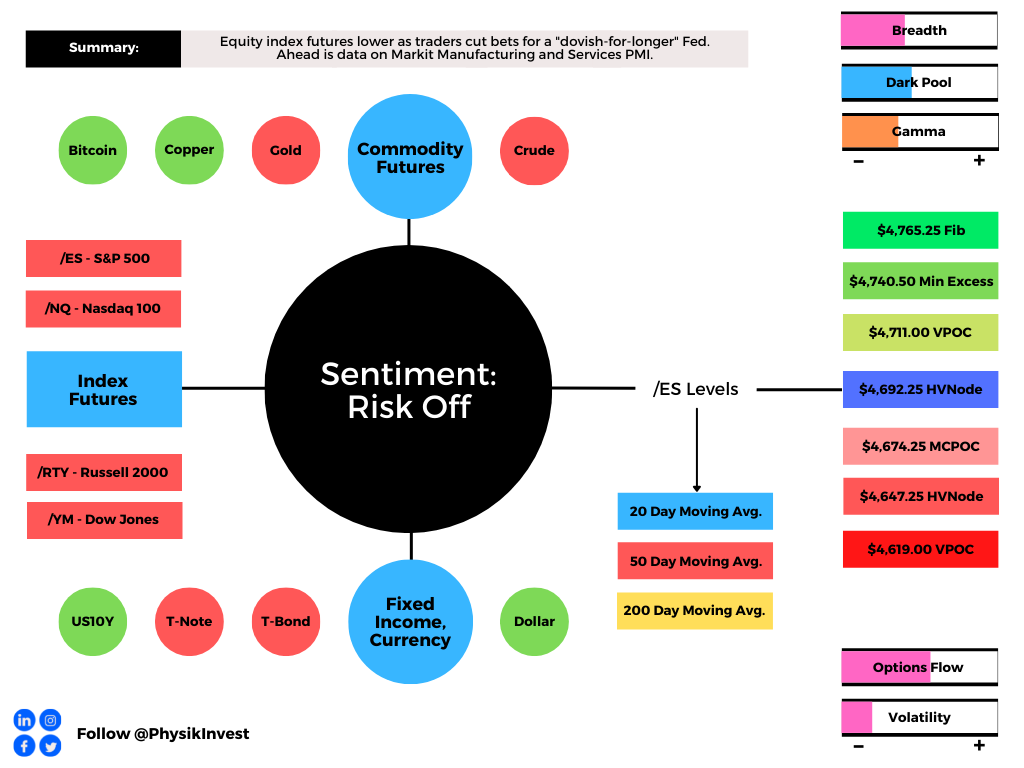

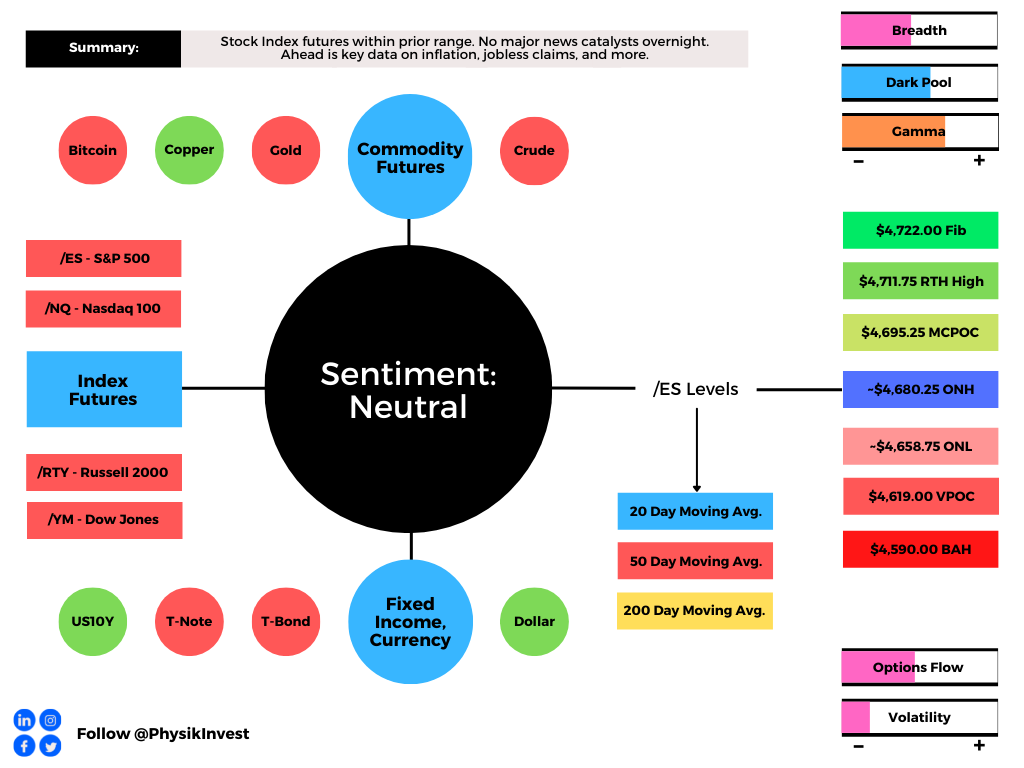

Technical: As of 6:45 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,468.75 poor low puts in play the $4,489.75 low volume area (LVNode). Initiative trade beyond the LVNode could reach as high as the $4,501.00 VPOC and $4,519.75 overnight high (ONH), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,468.75 poor low puts in play the $4,444.50 weak low. Initiative trade beyond the weak low could reach as low as the $4,409.00 VPOC and $4,395.25 high volume area (HVNode), or lower.

Considerations: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator.

Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.