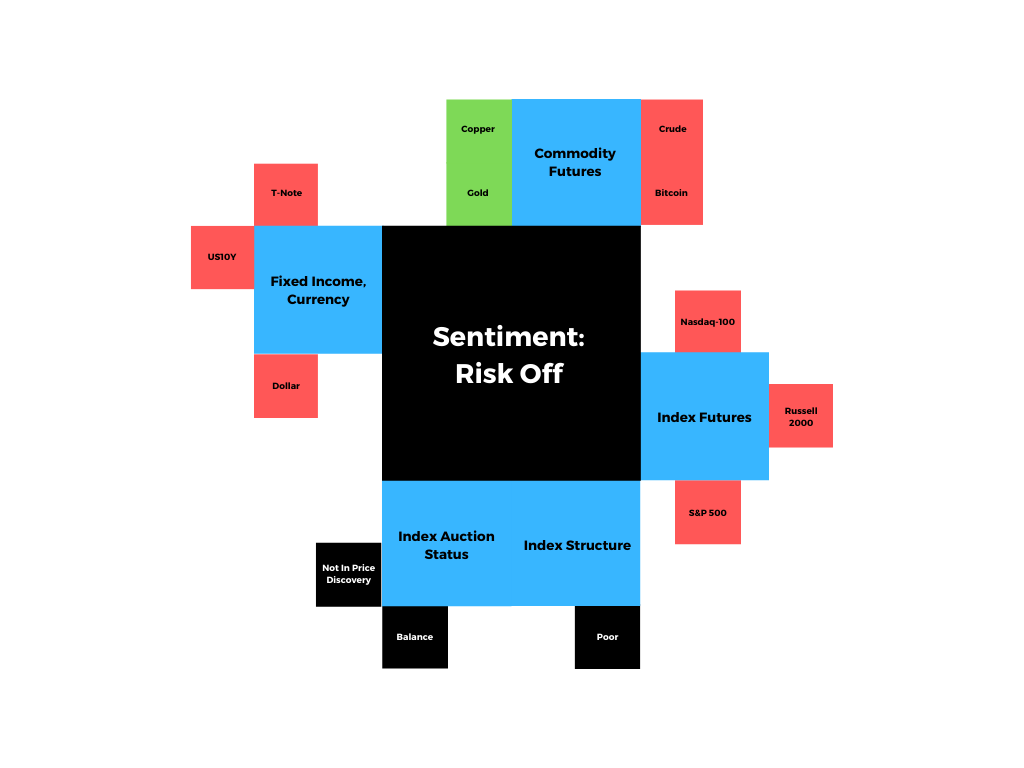

What Happened

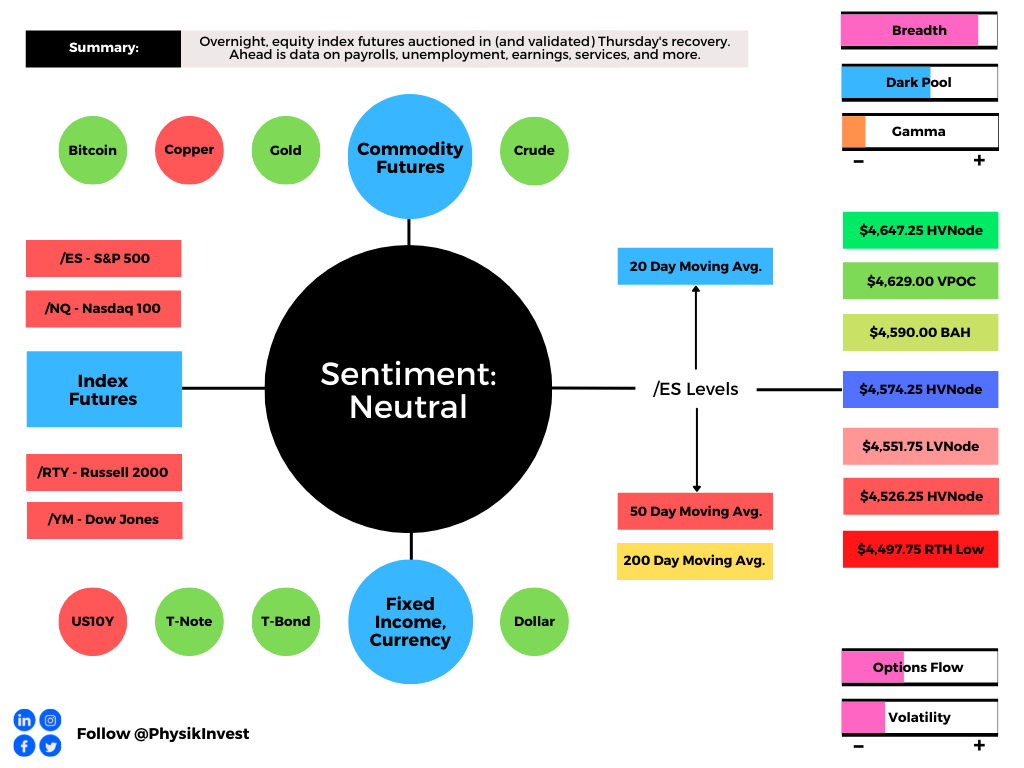

Overnight, equity index futures auctioned in-sync, within the confines of yesterday’s recovery.

This is as participants position themselves for Friday’s data dump that may shed light on how fast the Federal Reserve (Fed) intends to tighten monetary policy.

Ahead is data on nonfarm payrolls, the unemployment rate, and average hourly earnings (8:30 AM ET). Later is Fed-speak by James Bullard (9:15 AM ET), Markit services PMI (9:45 AM ET), as well as ISM services, factory orders, and core capital goods orders (10:00 AM ET).

What To Expect

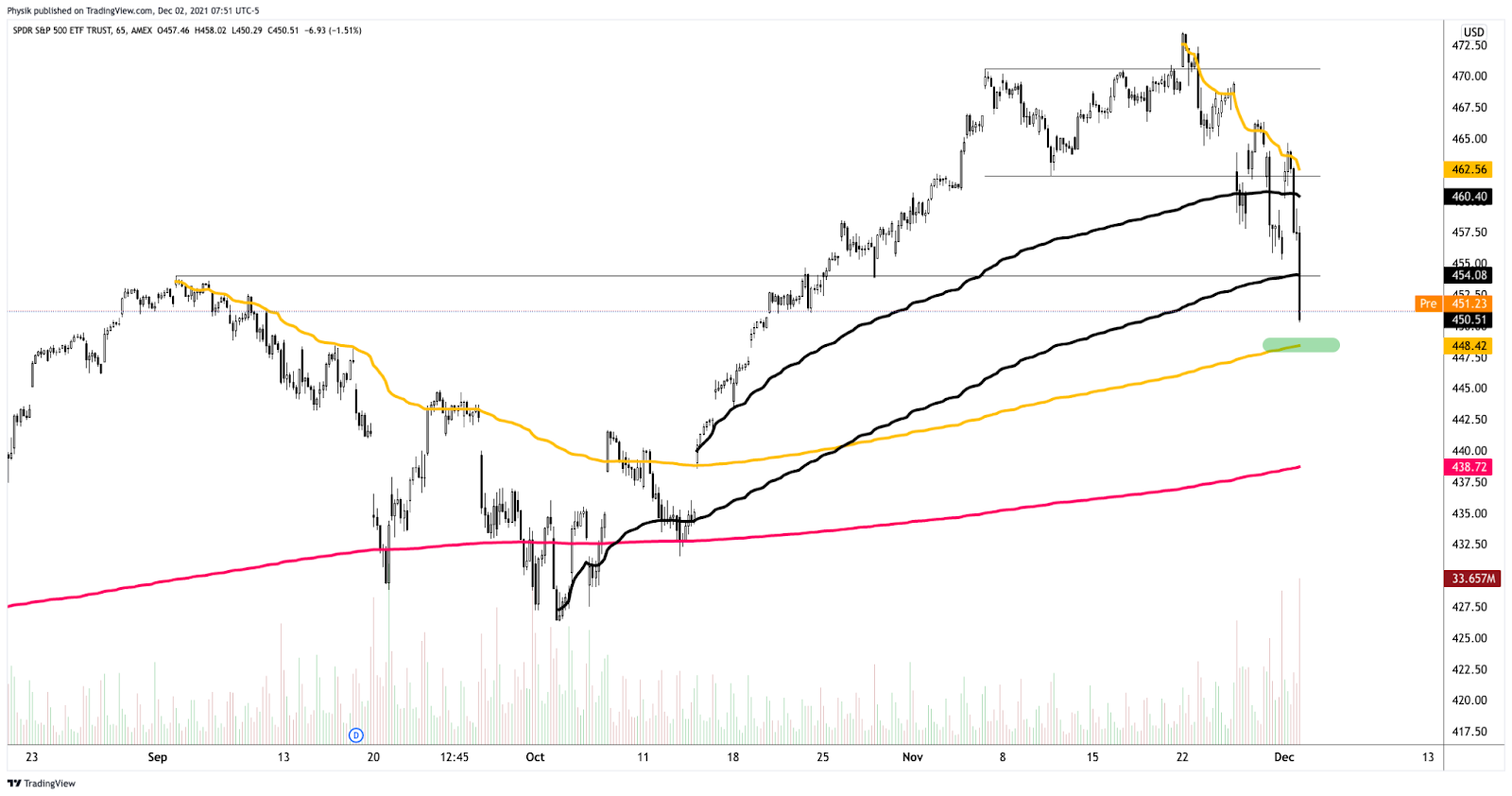

In the face of strong intraday breadth, the best case outcome occurred, evidenced by the recovery of Wednesday’s value (i.e., the prices at which 70% of that day’s volume occurred).

This action negated the knee-jerk selling that coincided with COVID-19 variant news.

As a result, the S&P 500 is back inside of a short-term consolidation; participants had no interest in transacting the S&P 500 on prices advertised below the balance area.

Context: The Fed’s intent to moderate stimulus and uncertainty with regards to how a new COVID-19 variant will impact the global recovery.

In the face of it all, according to Bloomberg, “The market is again pricing June 2022 as the most likely timing for the first Fed rate hike, same as on Nov. 24. At various stages over the intervening days traders looked at July, or even as late as September.”

This is as an emerging trend from the Fed, confirmed by Chair Jerome Powell’s Congressional testimony – for weeks into this most recent equity – resulted in a re-pricing of bond market risk.

That fear – demand for protection in the bond market – failed to appear in the equity market.

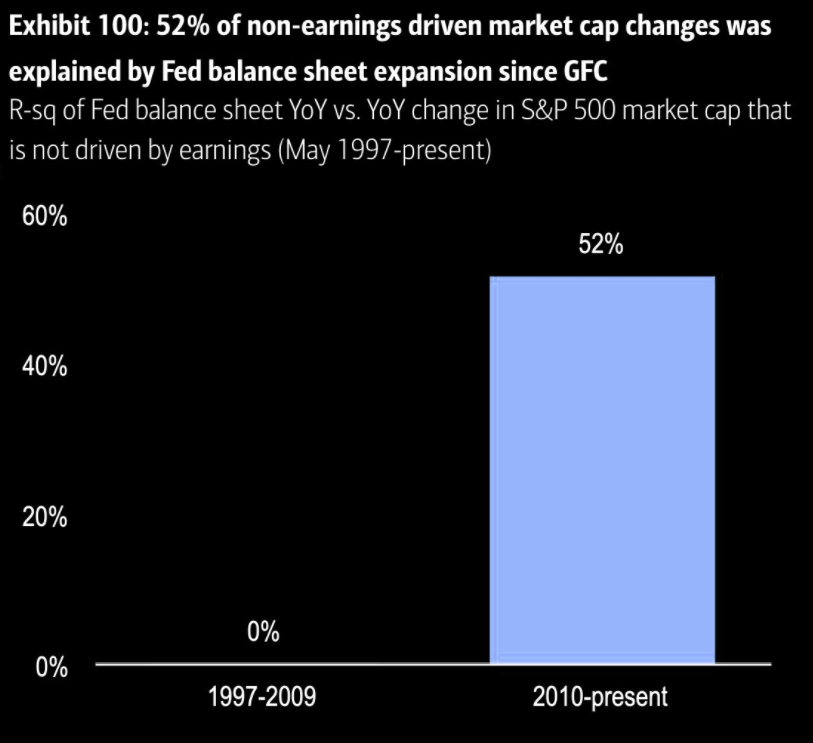

Instead, there was an insatiable appetite for stocks, according to Bloomberg, with investors pouring more cash in 2021 than in the past 19 years, combined.

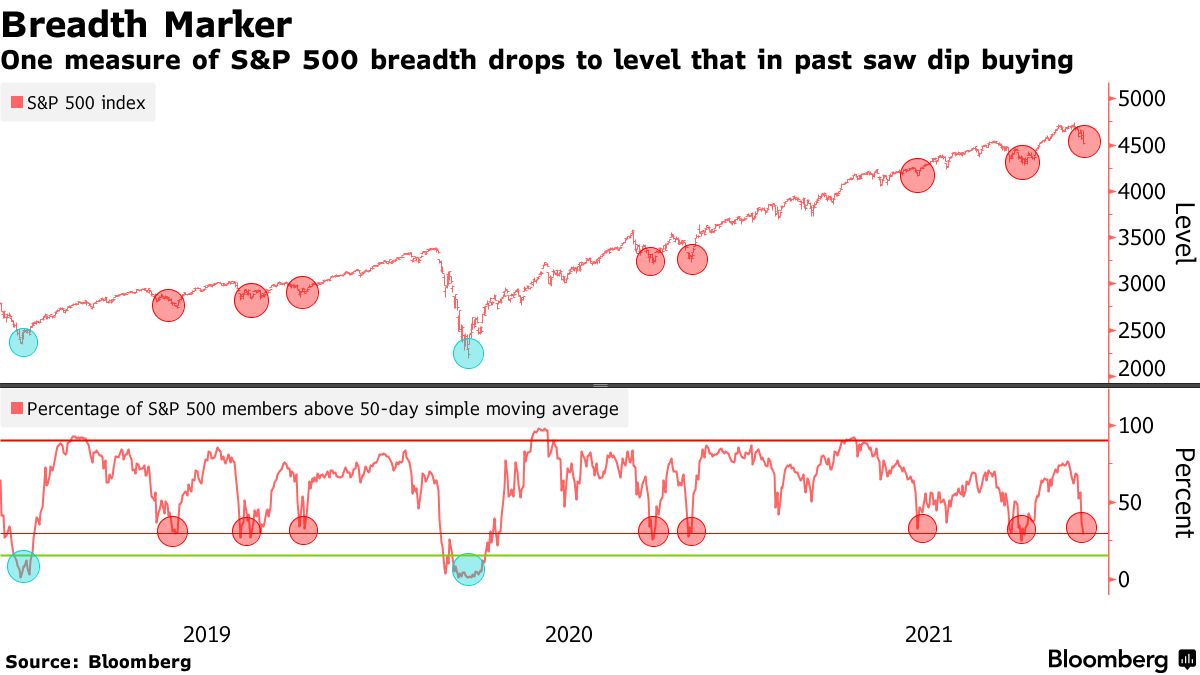

That appetite for risk fed into the activity of some high-flyers like Tesla Inc (NASDAQ: TSLA), and, more recently Apple Inc (NASDAQ: AAPL). At the same time, the broader market was weakening, evidenced by a decline in breadth.

With indices pinned, heading into the November monthly options expiration (OPEX), as a result of sticky and supportive hedging flows, correlations declined.

Think about it. If heavily weighted index constituents are higher and the indices are pinned, then something has to give!

After OPEX, the removal of certain hedging flows had the market succumb to fundamental forces. The addition of participants’ underexposure to downside put protection, according to SpotGamma, resulted in more rampant two-way volatility.

The reason being? The market quickly entered into an environment known as short-gamma.

“What the heck is that? Please explain to me like I’m ten.” Okay, hold my beer.

Basically, funds holding long equity, in the interest of lower volatility returns, hedge. The S&P 500 is a benchmark and one of the best places to hedge, given liquidity, and so on.

These participants will sell calls against their long equity exposure. The proceeds from that sale will be put toward downside protection. Long equity, short call, long put. Get it?

The counterparty to this dominant positioning is a buyer (seller) of upside (downside) protection, a carry trade (i.e., long delta).

This exposure is hedged, yes! However, this exposure will also decay, in time, all else equal.

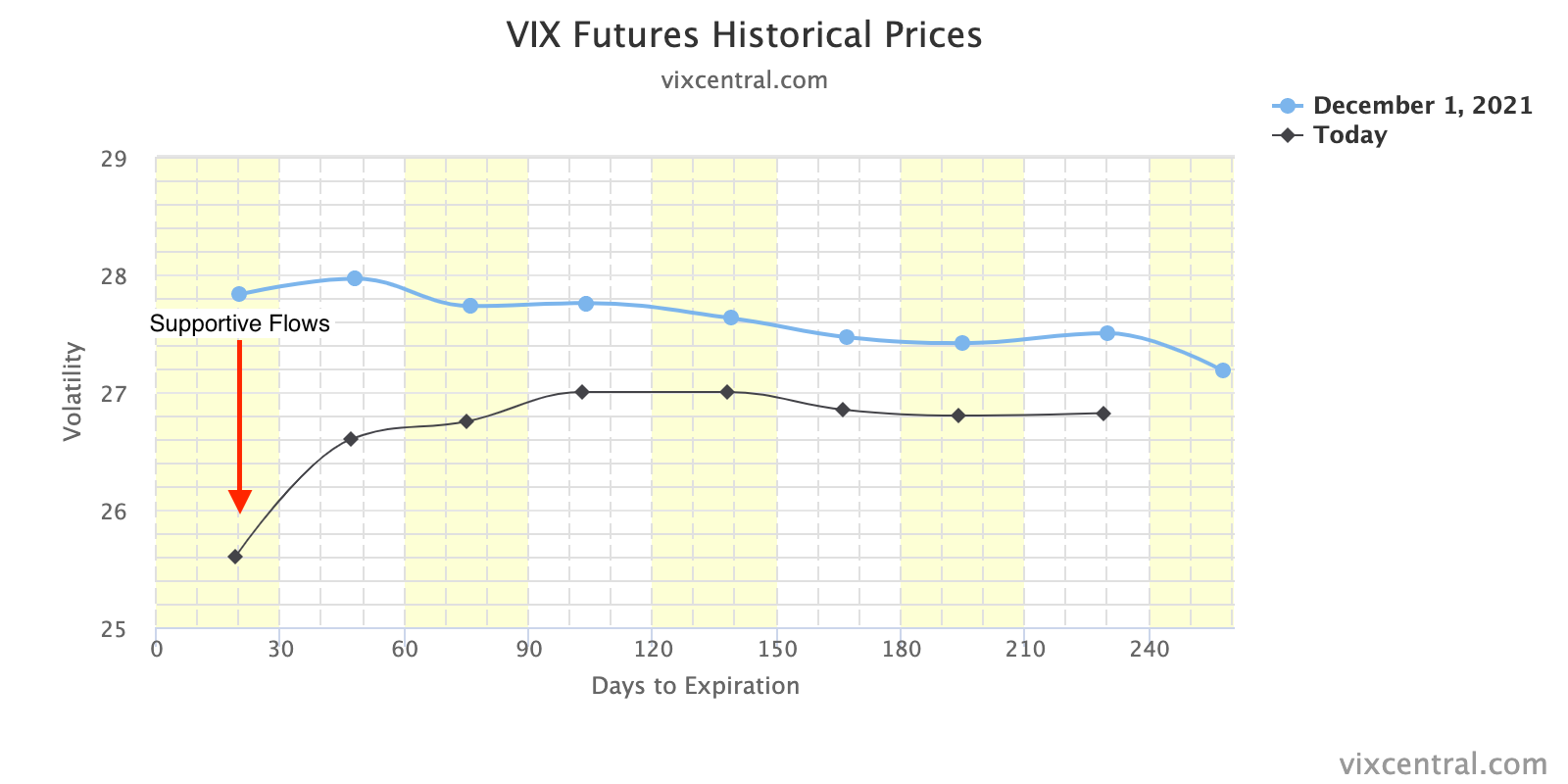

Volatility will slide down its term structure (vanna) and time will pass (charm); “as volatility ebbs and time passes, the unwind of these hedges brings in positive flows that can lead to lengthy sprints.” – Cem Karsan of Kai Volatility.

Now, within a certain range, said counterparties are, long-gamma also. Gamma is basically “the rate of change of delta per 1-point move in the underlying,” according to SqueezeMetrics.

As volatility and time to expiration decline, the gamma of at-the-money options rises; “option market-makers will hedge their positions in a fashion that stifles volatility (buying into lows, selling into highs).”

There are times, also, when the market is in a short-gamma; a “negative [gamma] implies the opposite (selling into lows, buying into highs), thus magnifying market volatility.”

With participants underexposed to downside protection, post-OPEX demand kicked the market into short-gamma; the conditions worsened when much of the activity was concentrated in shorter-dated tenors where the sensitivity of options to direction is higher, as stated.

Once that short-dated protection rolls off the table (and/or is monetized), counterparties will quickly reverse and support the market, buying to close their existing stock/futures hedges.

This flow is stabilizing and may play into a seasonally-aligned rally into Christmas as participants see defenses rolled out against the new COVID-19 variant, and the positive effects of pro-cyclical inflation and economic growth, improvements in global trade, and continuity at the Fed, among other dynamics, play out.

We see participants opportunistically buying the dip, already, via metrics like DIX that’s derived from liquidity provision on the market-making side.

Notwithstanding, the market is still in short-gamma and unless participants began betting on the upside (i.e., committing increased capital to calls at strikes higher in price and out in time), and we cross over to long-gamma, volatility ought to remain.

To assuage fears, though, here is a quote from Goldman Sachs Group Inc (NYSE: GS):

“We find that the market has already priced in a significant downgrade in the growth outlook off the back of Omicron concerns. While we don’t believe that the most extreme downside scenarios are fully reflected in current market pricing, there are clearly still scenarios that could prove better than anticipated by the sharp shift in pricing in recent weeks, in our view”.

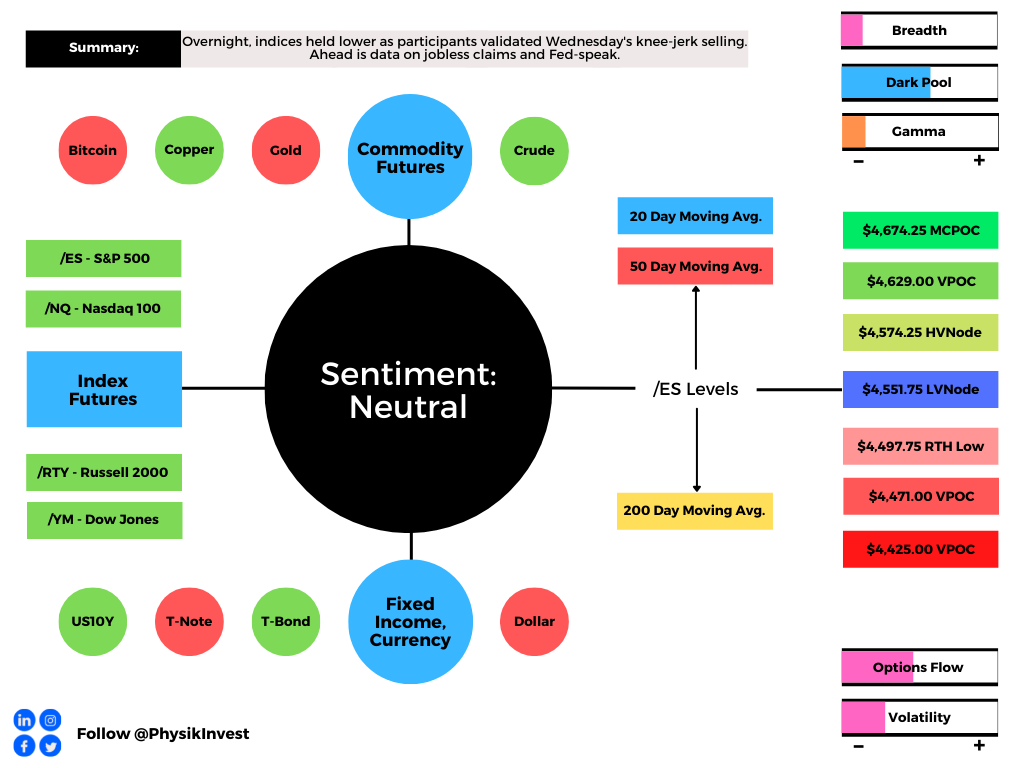

Expectations: As of 6:45 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,574.25 high volume area (HVNode) puts in play the $4,590.00 balance area high (BAH). Initiative trade beyond the BAH could reach as high as the $4,629.00 untested point of control (VPOC) and $4,647.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,574.25 HVNode puts in play the $4,551.75 low volume area (LVNode). Initiative trade beyond the LVNode could reach as low as the $4,526.25 HVNode and $4,497.75 regular trade low (RTH Low), or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

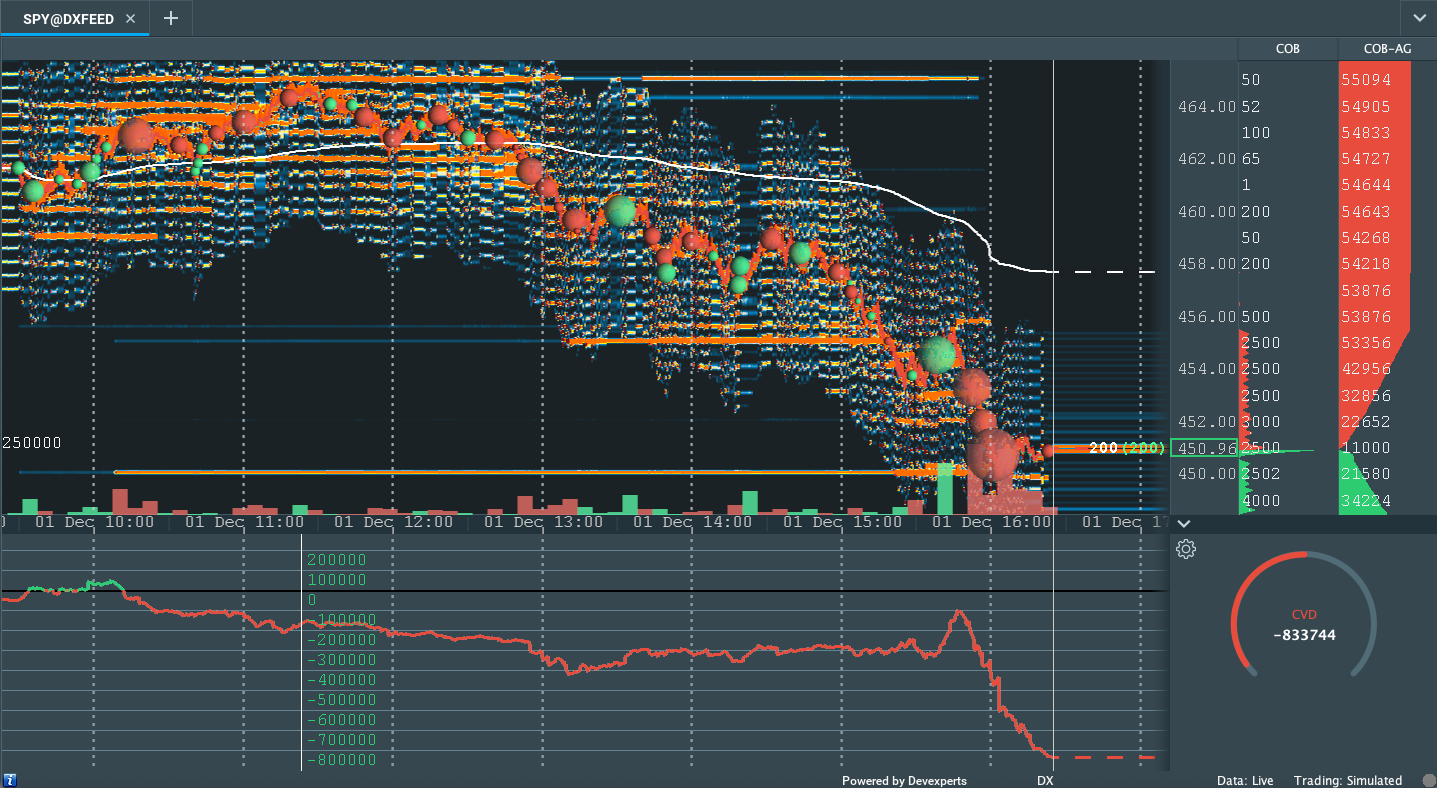

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

DIX: For every buyer is a seller (usually a market maker). Using DIX — which is derived from short sales (i.e., liquidity provision on the market-making side) — we can measure buying pressure.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Vanna: The rate at which the delta of an option changes with respect to volatility.

Charm: The rate at which the delta of an option changes with respect to time.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure.

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance-areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

Modus operandi is responsive trade (i.e., fade the edges), rather than initiative trade (i.e., play the break).

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

Rates: Low rates have to potential to increase the present value of future earnings making stocks, especially those that are high growth, more attractive. To note, inflation and rates move inversely to each other. Low rates stimulate demand for loans (i.e., borrowing money is more attractive).

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.