Administrative Bulletin

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Tomorrow’s Good Friday, and some markets, including the US’s equity market, will be closed. The Treasury market will remain open, albeit for less time, and may enable traders to price the impacts of coming releases, including non-farm payrolls (NFP). The consensus is that the US added 235,000 jobs in March, with the unemployment rate expected to remain steady at 3.50%. Higher for longer, then? We shall see.

Moreover, the big news is that the trend in mortgage rates, followed closely in the US, continues to be down. US 30-year fixed mortgage rates fell for a fourth-straight week, though applications to buy and refinance a home declined for the first time in a month. However, borrowing costs remain generally high and housing inventory low, keeping a cap on homebuying activity.

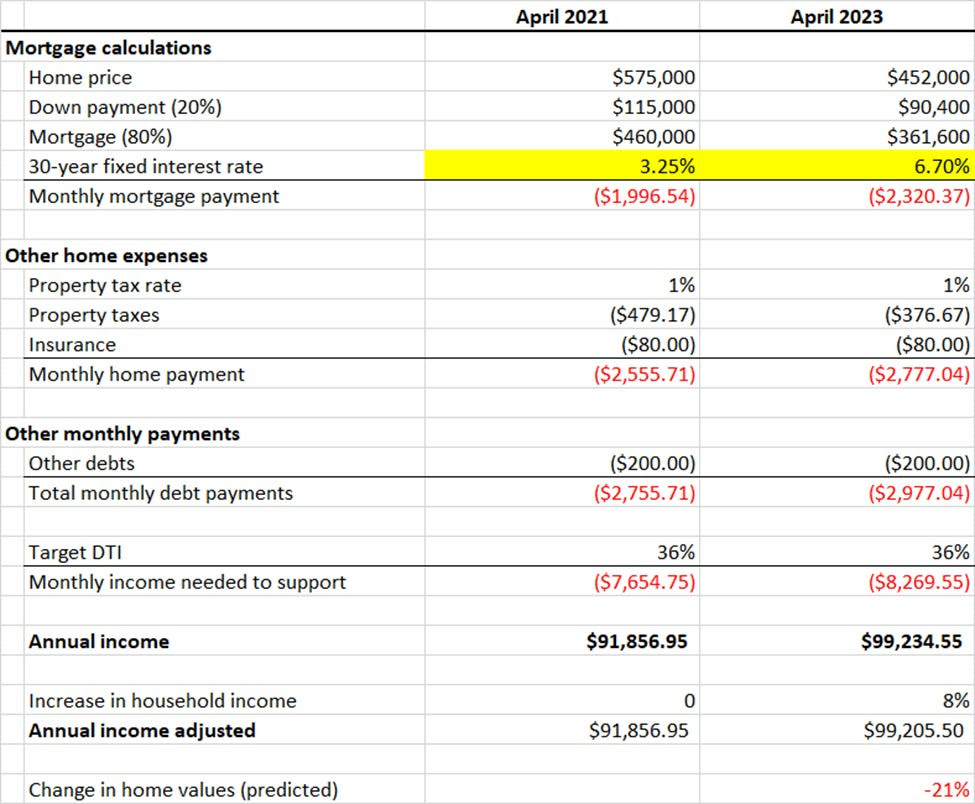

Notwithstanding, as explained by Akash Kanojia, for the housing market to “clear” on today’s affordability, home prices need to fall by about 20.00%.

To explain, typically, banks use a debt-to-income ratio to determine how much they will lend to a borrower to buy a house. Adding, they could enforce a limit of 80% on the purchase price of the house, and the remaining 20.00% is paid in cash by the borrower as a down payment.

Mortgage rates comprise the short-term risk-free rate, term premium, the Treasury-MBS spread, the primary-secondary spread, and a credit spread based on the borrower’s creditworthiness. Any of these numbers changing can influence a borrower’s final payment to the lender.

An analysis starting with a home price in 2021 of $575,000.00 and a borrower whose income was $92,000.00, and adjusting all for inflation and movements in rates, the decrease in home values to boost affordability is 21.00%.

A worst-case scenario is that the fed funds rate rises further to quell inflation. If the fed funds rate were to rise to 6.00-6.25%, matching the latest annualized CPI print, and “the market realizes the Fed is not going to cut, and the curve (e.g., 3m-7y UST) steepens to historical norms (~150 basis points long-term average), barring changes in the MBS spread, primary-secondary spread, and credit charges, this produces a ~40.00% decline in home prices.

Consequently, as the economy slows and layoffs increase, as we’re starting to see, it will negatively affect housing demand and affordability due to income stability and growth. On the bright side, inflation destroys the nominal value of debt, Kanojia says. Assuming wages keep up, buyers in hot markets may be spared if they can withhold from selling at market-clearing prices, Kanojia ends.

On a note about the doom and gloom (i.e., economy slowing and layoffs increasing, as well as yield curve steepening), JPMorgan Chase & Co’s (NYSE: JPM) Jamie Dimon says the following:

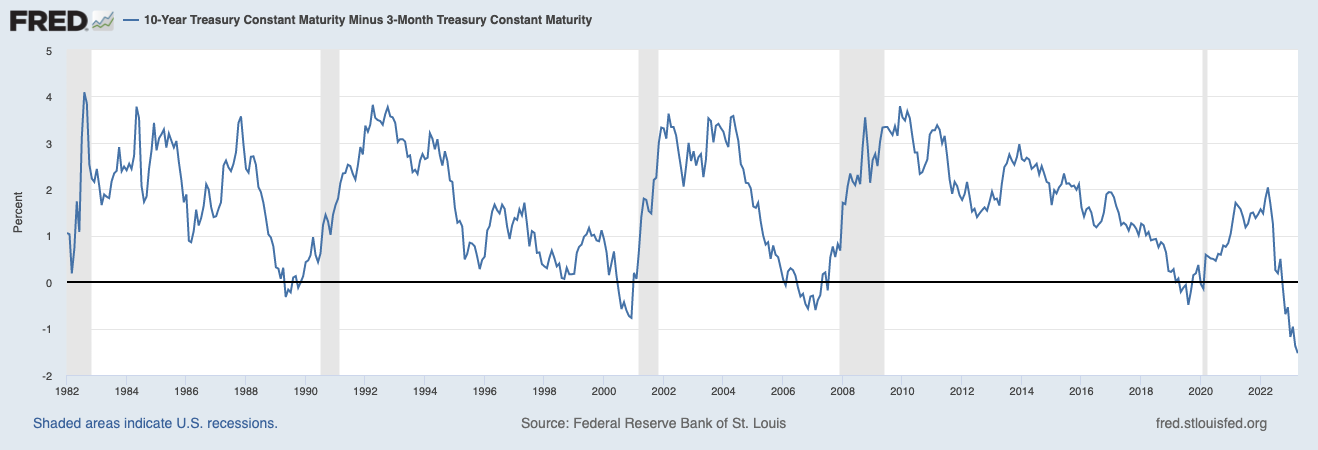

Today’s inverted yield curve implies that we are going into a recession. As someone once said, an inverted yield curve like this is ‘eight for eight’ in predicting a recession in the next 12 months. However, it may not be true this time because of the enormous effect of QT. As previously stated, longer-term rates are not necessarily controlled by central banks, and it is possible that the inversion we see today is still driven by prior QE and not the dramatic change in supply and demand that is going to take place in the future.

Dimon, the CEO of JPM, says that a graph showing the yields on bonds of different maturities is inverted, meaning that the yields on shorter-term bonds are higher than the yields on longer-term bonds. An inverted yield curve has often been a reliable indicator of an upcoming recession; it reflects investor demands for higher returns on short-term investments and expectations that short-term rates will fall in the future, which happens when the central bank cuts rates in response to a weak economy.

In other words, the conditions around the yield curve inversion are different this time.

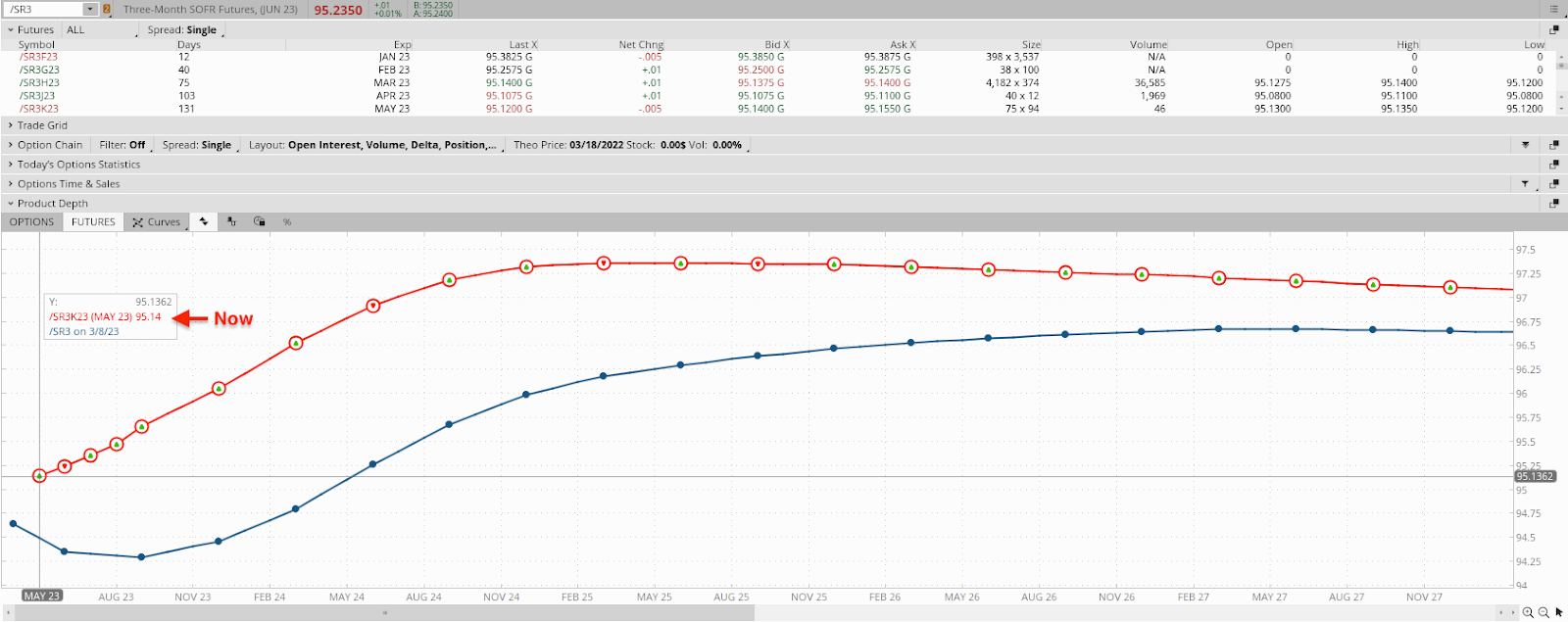

Further, a peek at the bond market shows cuts priced within six months.

Same thing with the Secured Overnight Financing Rate (SOFR) market, developed by the Federal Reserve to replace LIBOR, which was phased out due to manipulation concerns, among other things, as a benchmark interest rate.

Unlike LIBOR, which is based on unsecured lending transactions between banks, SOFR is based on actual transactions in the overnight repurchase agreement (repo) market, which makes it a more reliable benchmark. Consequently, the shift from the Eurodollar (FUTURE: /GE), used to intervene in support of the dollar and other currencies and allow lenders to lock in rates, to SOFR has accelerated, too.

As stated yesterday, options activity in the SOFR market was centered around the 95.00 strikes. To calculate the implied interest rate using the value of the 3-month SOFR future, we can use the following formula:

Implied interest rate = 100 – future price; the implied interest rate calculated using the 3-month SOFR future is an annualized rate.

For example, if the current value of the 3-month SOFR future is 95.00, the implied interest rate would be 100.00 – 95.00 = 5.00%.

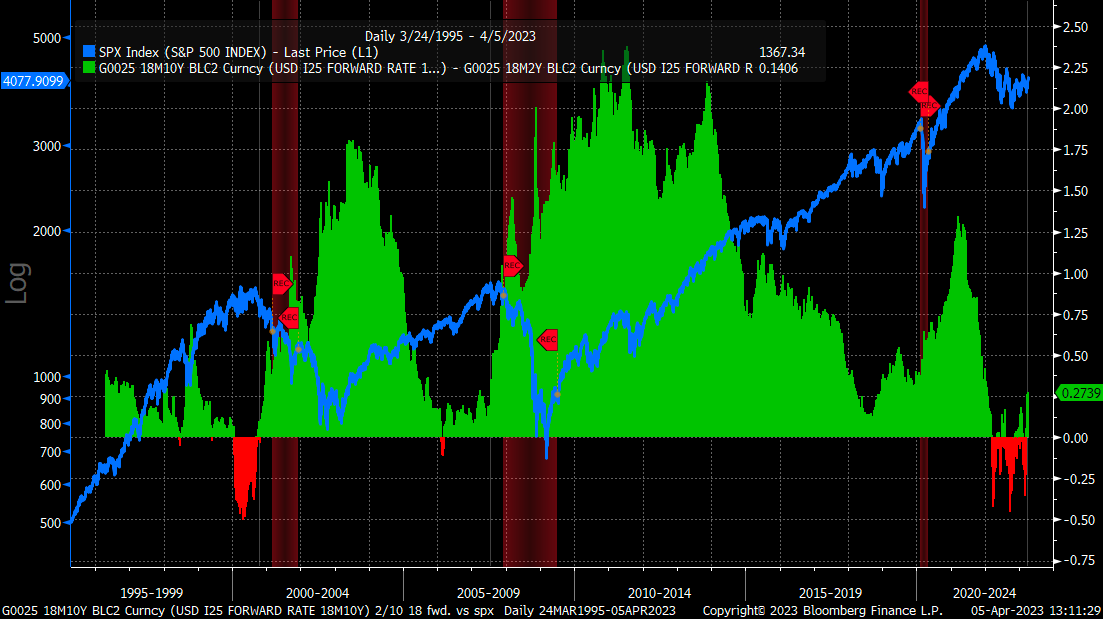

The S&P 500 (INDEX: SPX) has not bottomed based on these conditions. 3Fourteen Research concludes that the SPX has never bottomed during a Fed hike cycle, which one is still ongoing; typically, forward earnings stabilize and turn higher 3-6 months after a market bottom, which hasn’t happened; the 2-10 yield curve has never remained inverted six months after a major bear market bottom.

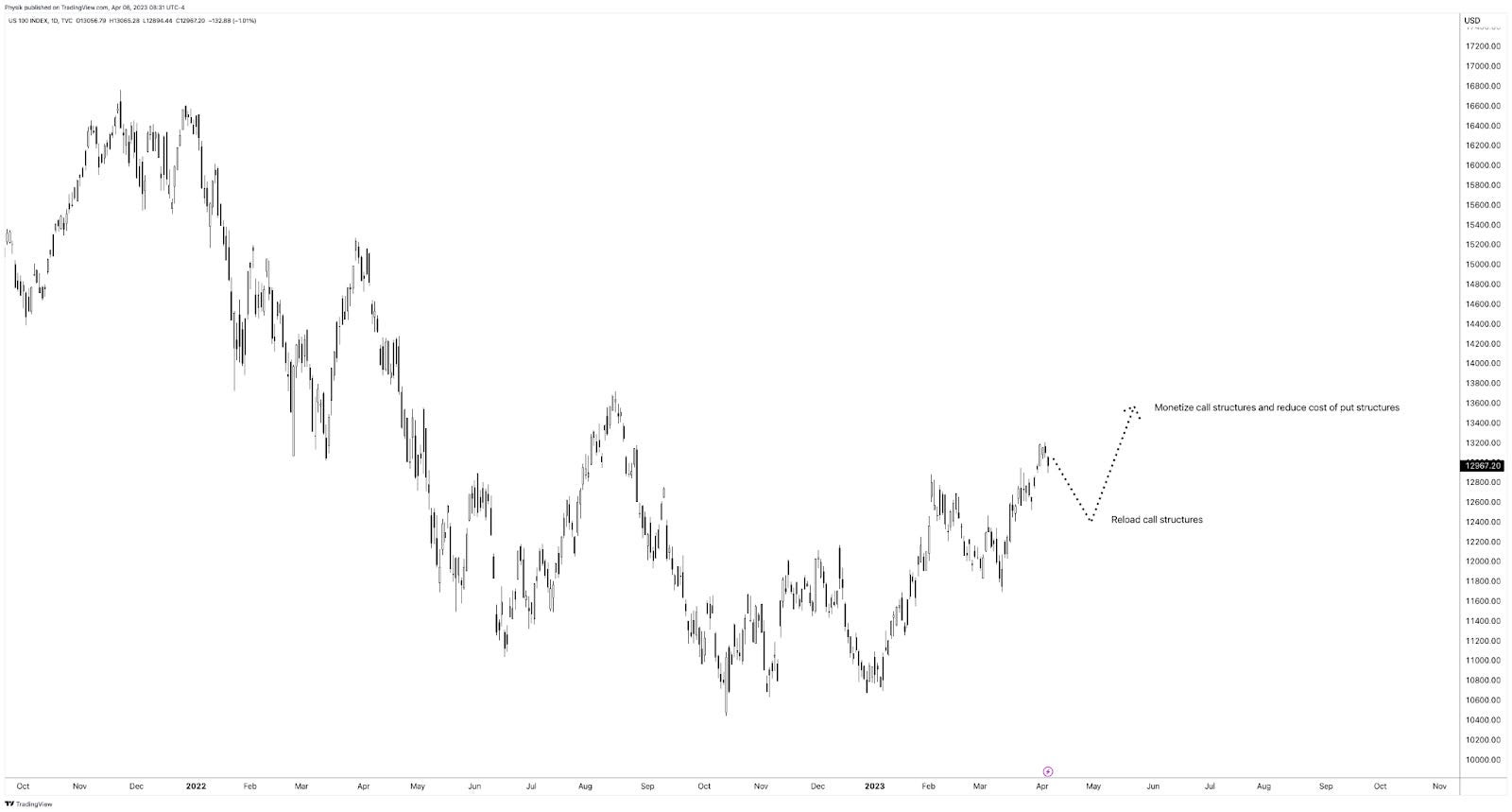

Notwithstanding all the doom and gloom, we explained in past letters that markets would likely remain strong through month-end March.

Accordingly, it made a lot of sense to own low- or no-cost call options structures in products like the Nasdaq 100 (INDEX: NDX), where many participants were caught offsides and bidding call volatility in response to the dramatic reversal; the reach for the right tail reduced the cost of ratio call spreads, making them the go-to structures.

It may make sense to re-load in similar call structures on pullbacks while using any proceeds or profits from those structures to reduce the cost of owning fixed-risk and less costly put structures (e.g., vertical) that may enable us to participate in equity market downside, as well as bet on lower rates in the future using call options structures on the /SR3 to express that opinion.

Disclaimer

Don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.