What Happened

Overnight, equity indices were flat-to-up while commodities and bonds were sideways to lower.

The prevailing narratives include the prospects of a Russian invasion of Ukraine, COVID-19 resurgence in the U.S., concerns over the pace of inflation and its impact on the economy, China developer debt payments, and the like. Your typical doom and gloom stuff!

Ahead is data on job openings, University of Michigan consumer sentiment, and five-year inflation expectations (10:00 AM ET).

What To Expect

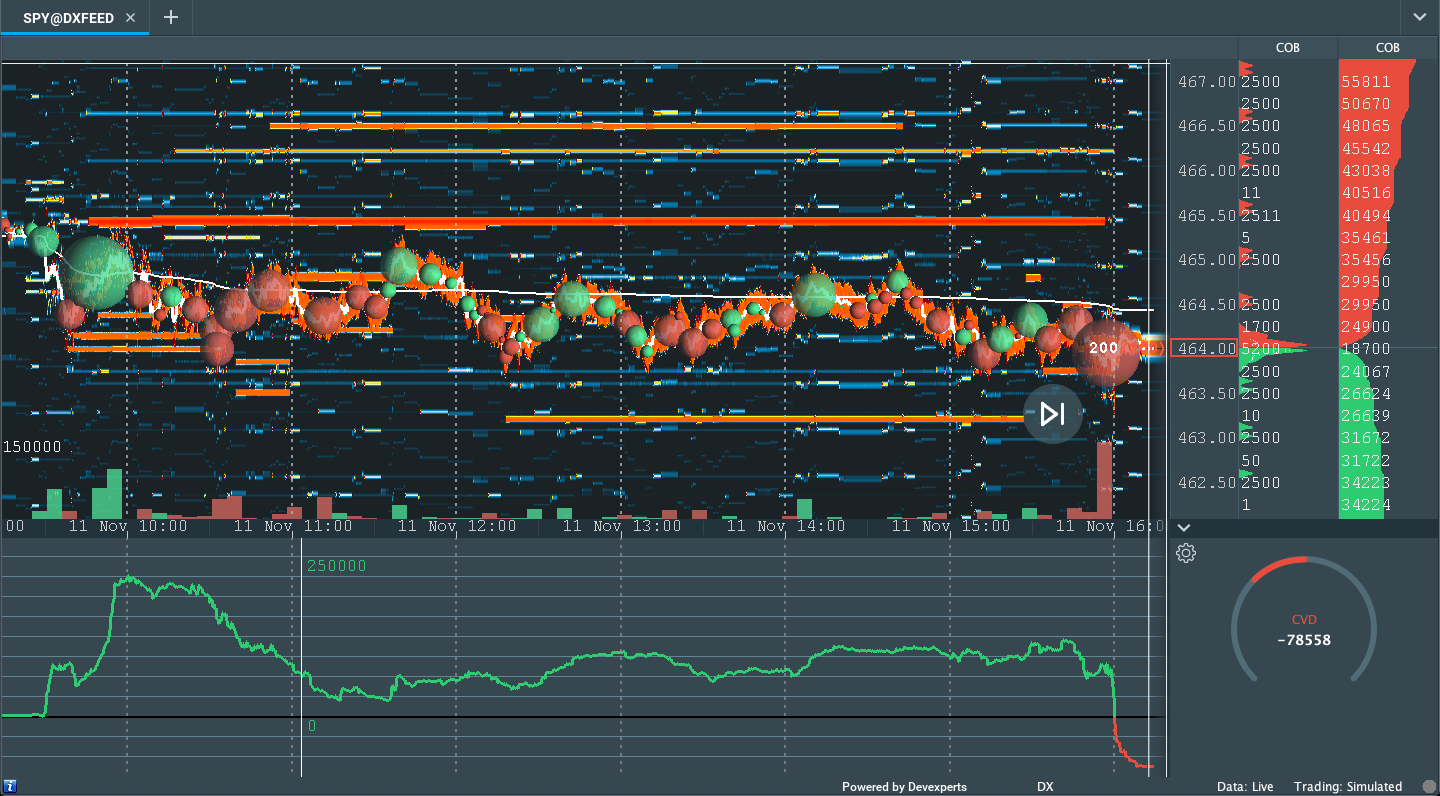

On lackluster intraday breadth and market liquidity metrics, the best case outcome occurred, evidenced by the balance and overlap of value areas in the S&P 500.

This activity, which suggests participants’ willingness to position for directional resolve, comes alongside the presence of poor structure, a dynamic that adds to technical instability.

Context: The aforementioned trade is happening in the context of a lot of big-picture dynamics such as the growth of derivatives exposure and tail risk, the heightened moneyness of nonmonetary assets, trends in seasonality, buybacks, earnings growth, inflation, and more.

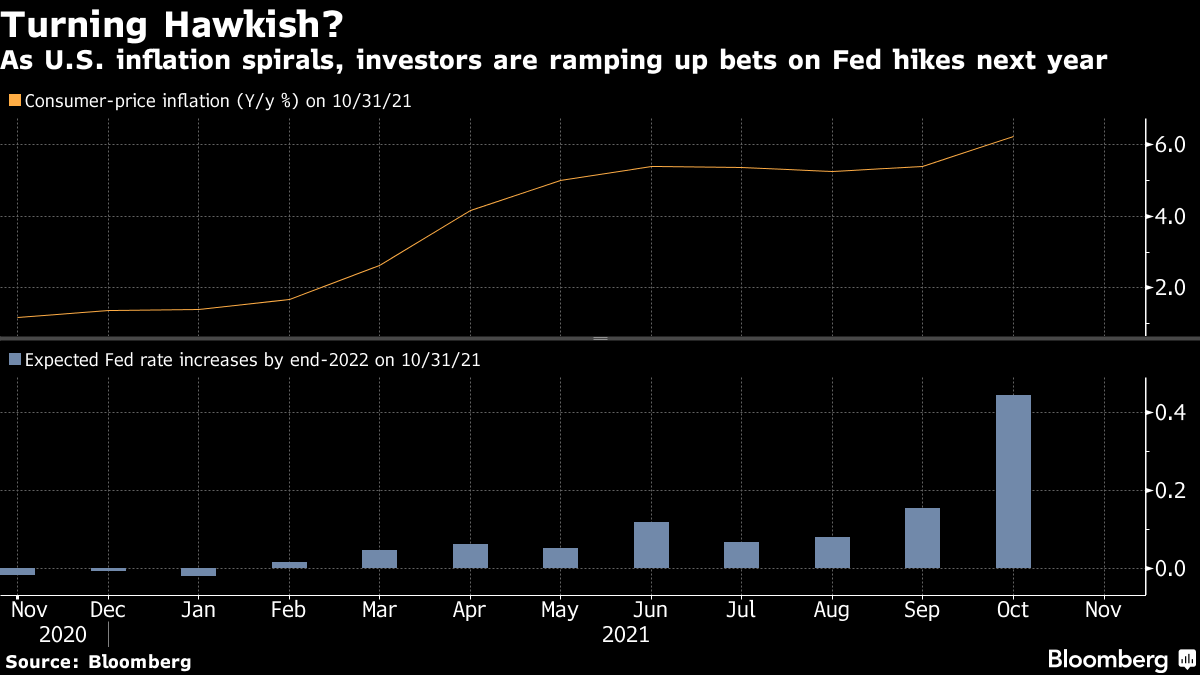

On the topic of inflation, the October consumer price index (CPI) is worrisome, according to some.

“We think it is time to rethink positioning related to inflation,” Citigroup Inc (NYSE: C) strategists led by Scott Chronert wrote in a note. “A focus on sectors and industry groups negatively correlated to inflation provides a contrarian opportunity.”

Citi sees value in consumer and health-care stocks, as a result of negative correlations to CPI.

Despite the hot prints, the CPI doesn’t paint the entire picture; it’s too soon to change rate-hike calculations, according to the Federal Reserve’s Mary Daly.

That thinking brings me back to recent comments made by Ark Invest’s Cathie Wood.

Mainly, Wood feels that inflation is on its way out with a decline in the velocity of money and increased moneyness of nonmonetary assets.

A prime example of this is inflation in housing; “Ivy Zelman of Zelman Research came out this week. She made a fantastic call on the housing bubble and bust starting in 05-06, and she was right, just a little early. She is very concerned that the housing prices we’re seeing right now are not sustainable,” because of speculation, as well as iBuying and private equity.

“This is unsustainable … and I’m wondering if even the housing market inflation is going to give way, here,” Wood added.

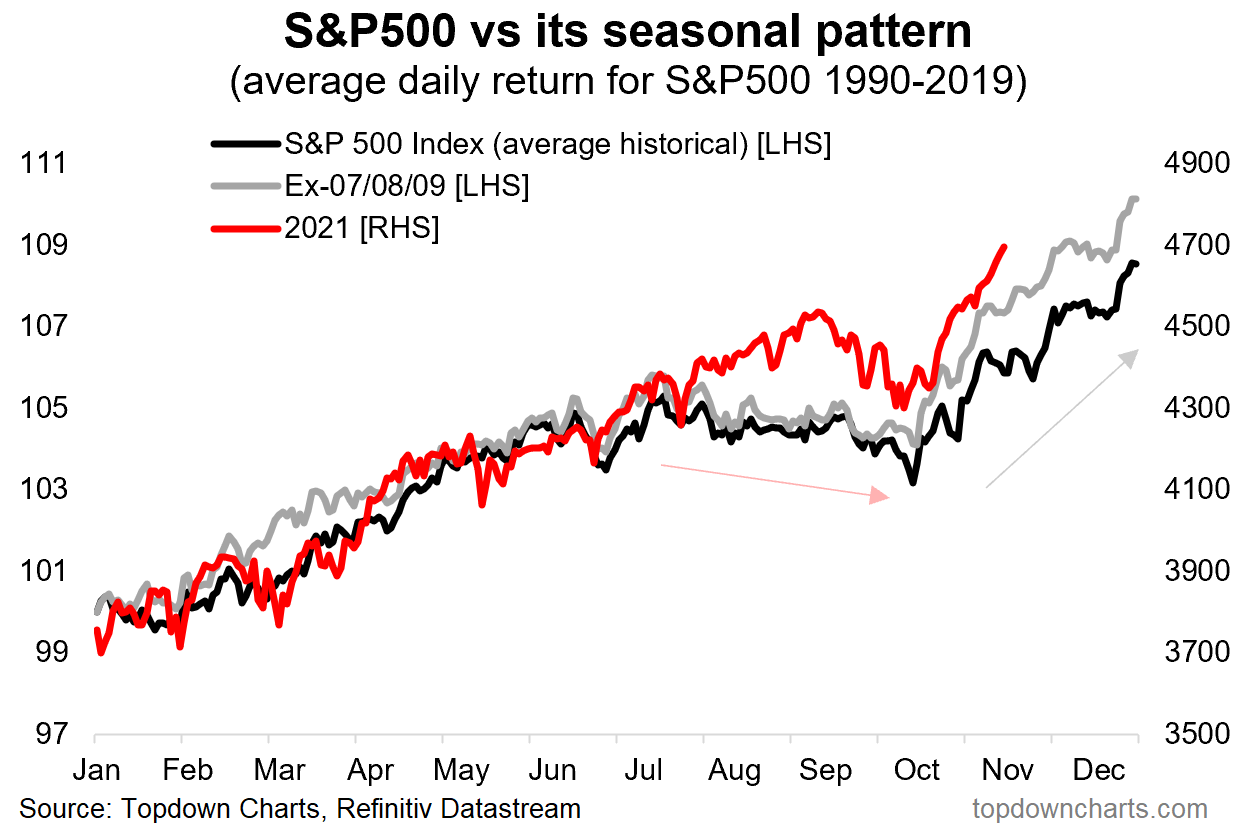

For now, with more of the same – bullishness in the face of moderating monetary policy, strong retail participation, seasonality, and buybacks supporting the valuations we’re at, now – what other narratives are there to add (or roll forward)?

Given my interest in the options market – because option volumes are comparable to stock volumes and related hedging flows, as a result, represent an increased share of volume in underlying stocks – I’m in the camp of “the market is fragile, given current positioning.”

According to SpotGamma, single-stock exuberance of the past weeks fed into the S&P complex, itself, evidenced by a lack of interest in put options at lower strikes; the S&P 500 options strike with the largest negative gamma – delta sensitivity to underlying price – failed to roll higher, while the strike of the option with the largest positive gamma did.

This came as investors marked the S&P 500 up to the $4,700.00 strike, at which positive gamma – delta sensitivity to underlying price – is highest.

“As volatility continues to decline, the gamma of those options, which are now at the money, ought to increase, forcing counterparties to supply more liquidity,” SpotGamma explained.

Therefore, coming into this week, $4,700.00 was expected to be a magnet (or resistance) into that aforementioned pre-monthly options expiration (OPEX) weakness.

This was unless (1) volatility declined markedly, “a tailwind for the S&P complex as options slid[ing] down their term structure would cause dealers to continue covering their hedges in an asymmetric manner,” or (2) more capital was committed to options at higher strikes.

Neither happened.

Instead, the CBOE Volatility Index (INDEX: VIX) was higher, with demand coming in across the front area of the VIX futures term structure. This suggested a demand for hedges and a reduction in the flows (e.g., vanna) that support sideways to higher trade.

The implications of customers now covering their levered, long-delta exposure and demanding out-of-the-money hedges may have the effect of forcing counterparties to hedge in a manner that exacerbates underlying price movement to the downside (e.g., Tesla).

With that single-stock exuberance still reflected by positioning in the S&P, itself, as SpotGamma said: “This sets us up for what may be a volatile pre- and post-OPEX week.”

Expectations: As of 5:30 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Balance-Break Scenarios: A change in the market (i.e., transition from two-time frame trade, or balance, to one-time frame trade, or trend) ought to occur on a break of day-session balance. We monitor for acceptance (i.e., more than 1-hour of trade) outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance.

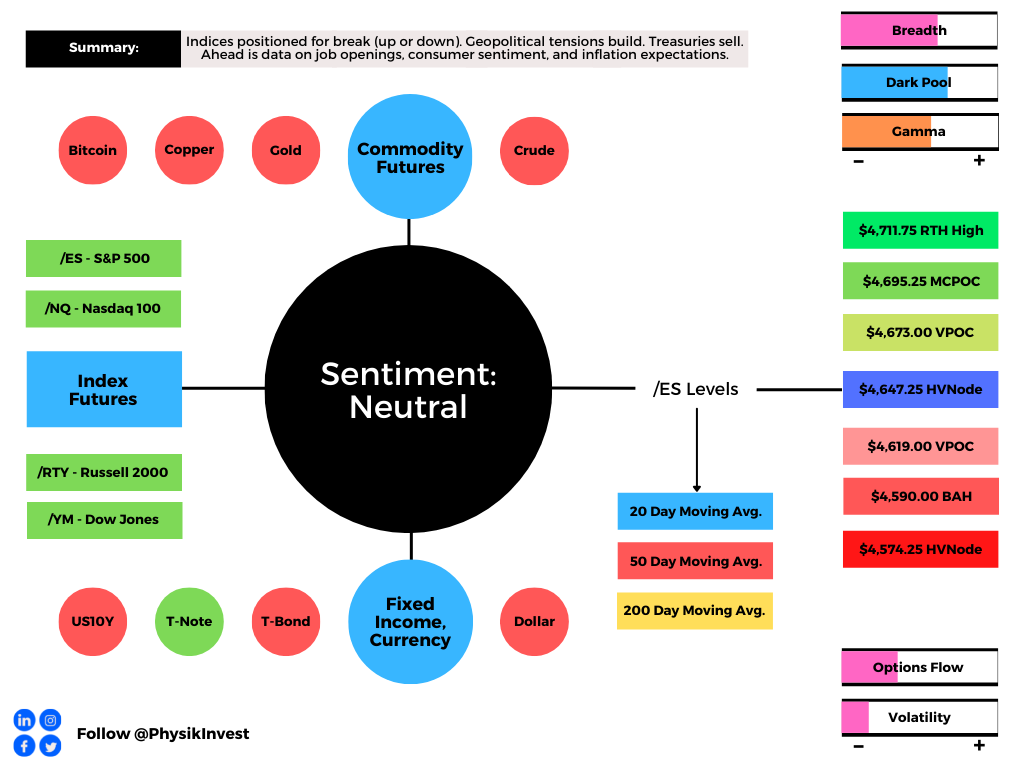

In the best case, the S&P 500 trades sideways or higher; activity above the $4,647.25 high volume area (HVNode) puts in play the $4,673.00 untested point of control (VPOC).

Initiative trade beyond the VPOC could reach as high as the $4,695.25 micro composite point of control (MCPOC) and $4,711.75 regular trade high (RTH High), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,647.25 HVNode puts in play the $4,619.00 VPOC.

Initiative trade beyond the VPOC could reach as low as $4,590.00, a prior balance area high (BAH), and $4,574.25 HVNode, or lower.

To note, a breach of Wednesday’s low likely puts the S&P 500 in a short-gamma environment.

Those participants that take the other side of options trades will hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they buy into strength and sell into weakness, exacerbating volatility. When dealers are long-gamma, they buy into weakness and sell into strength, calming volatility. -- Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Cave-Fill Process: Widened the area deemed favorable to transact at by an increased share of participants. This is a good development.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.