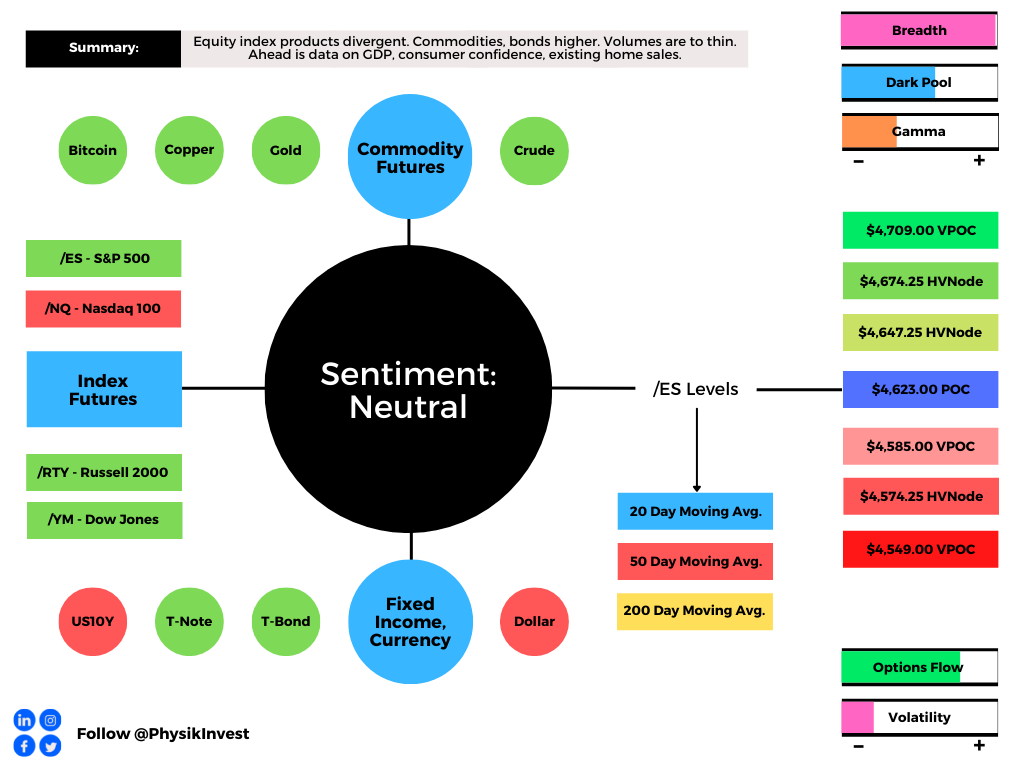

Overnight, equity index futures were divergent while most commodity and bond products were sideways to higher. This is as traders position themselves for the less liquid holiday trade.

Ahead is data on gross domestic product and income (8:30 AM ET), consumer confidence, and existing home sales (10:00 AM ET).

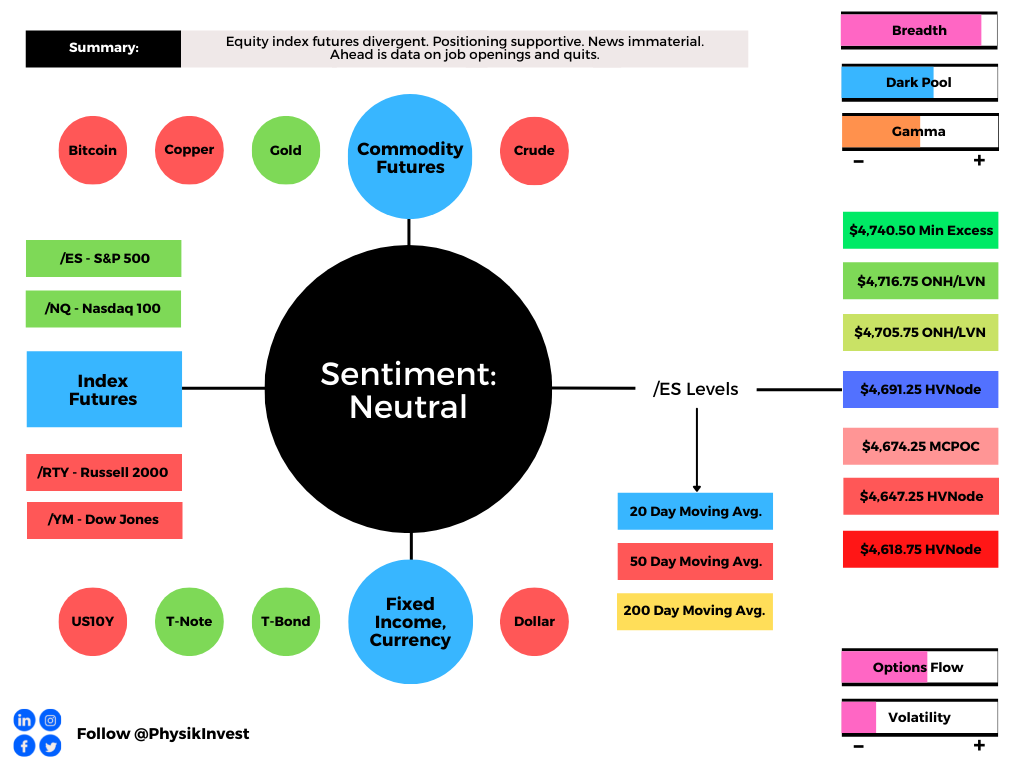

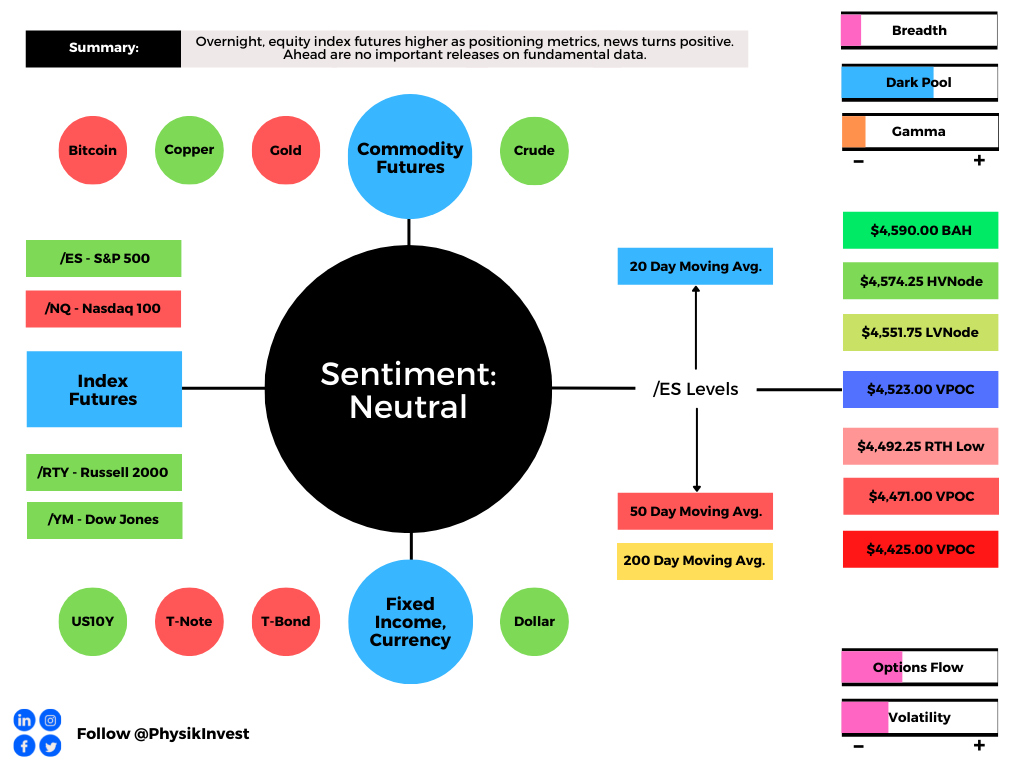

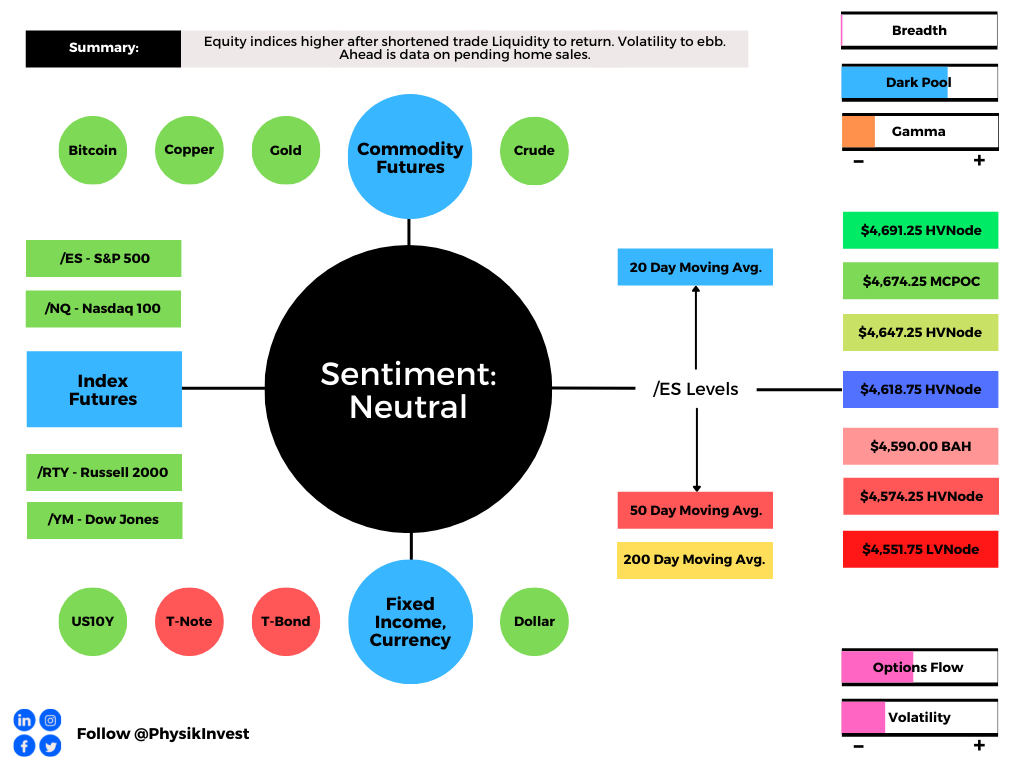

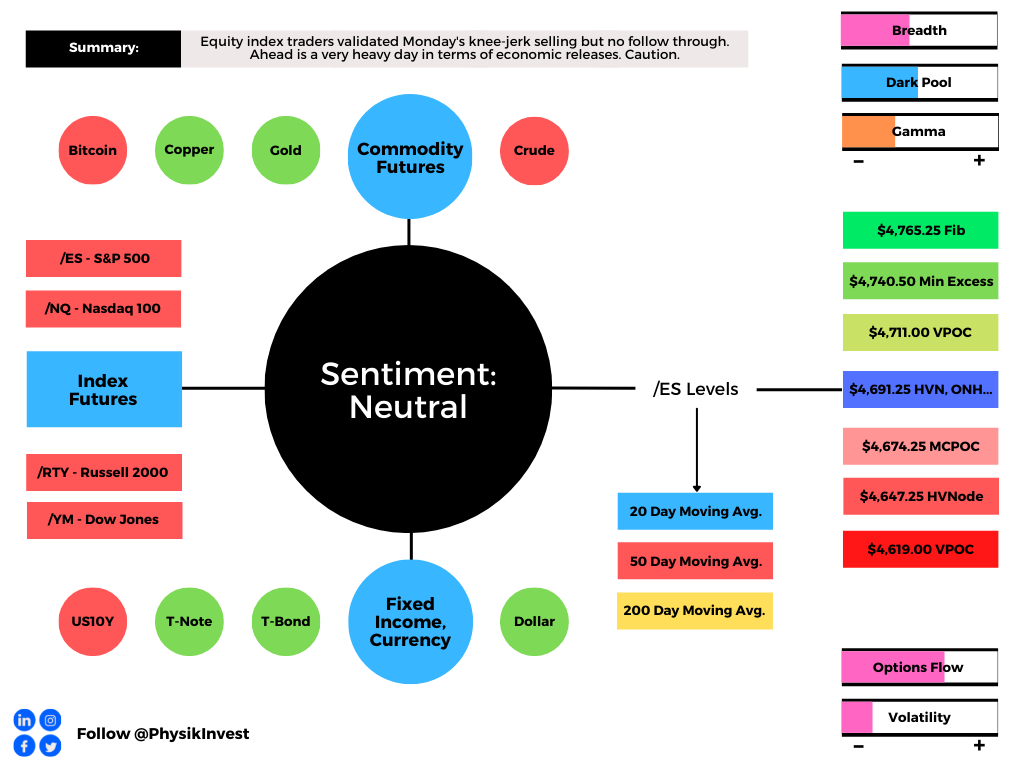

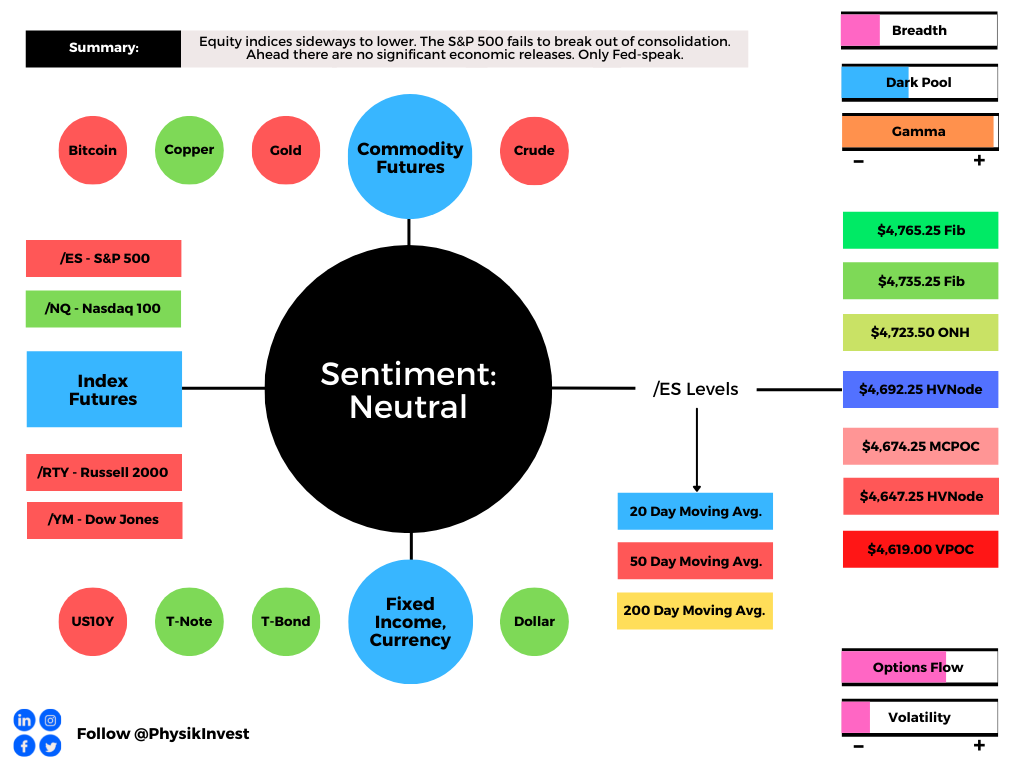

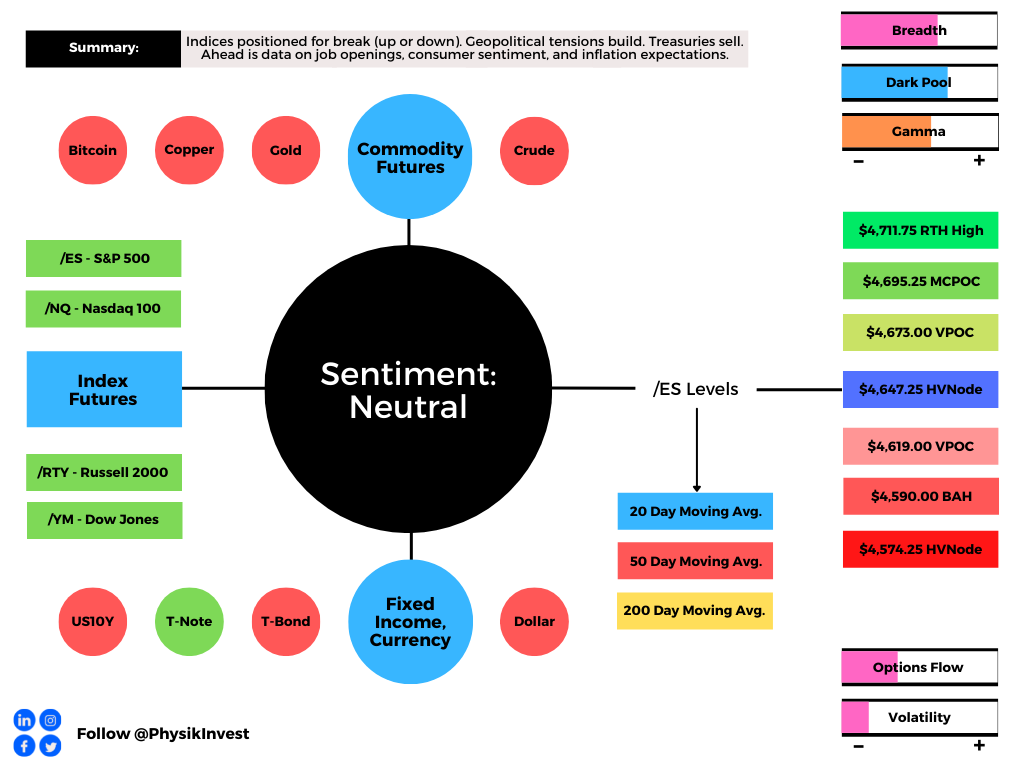

Graphic updated 6:30 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

On supportive intraday breadth and divergent market liquidity metrics, the best case outcome occurred; the S&P 500 auctioned away from intraday value, the levels at which participants found it most favorable to trade at.

Given the mechanical responses to key technical levels, visually-driven, weaker-handed participants (which seldom bear the wherewithal to defend retests) are very much in control.

Moreover, Tuesday’s activity, which was follow-through on Monday’s responsive buying, left low-volume structures in its wake.

Virgin tests of the low-volume – a void of sorts – ought to hold. Successful penetration portends follow-through given the participants that were most active at those levels.

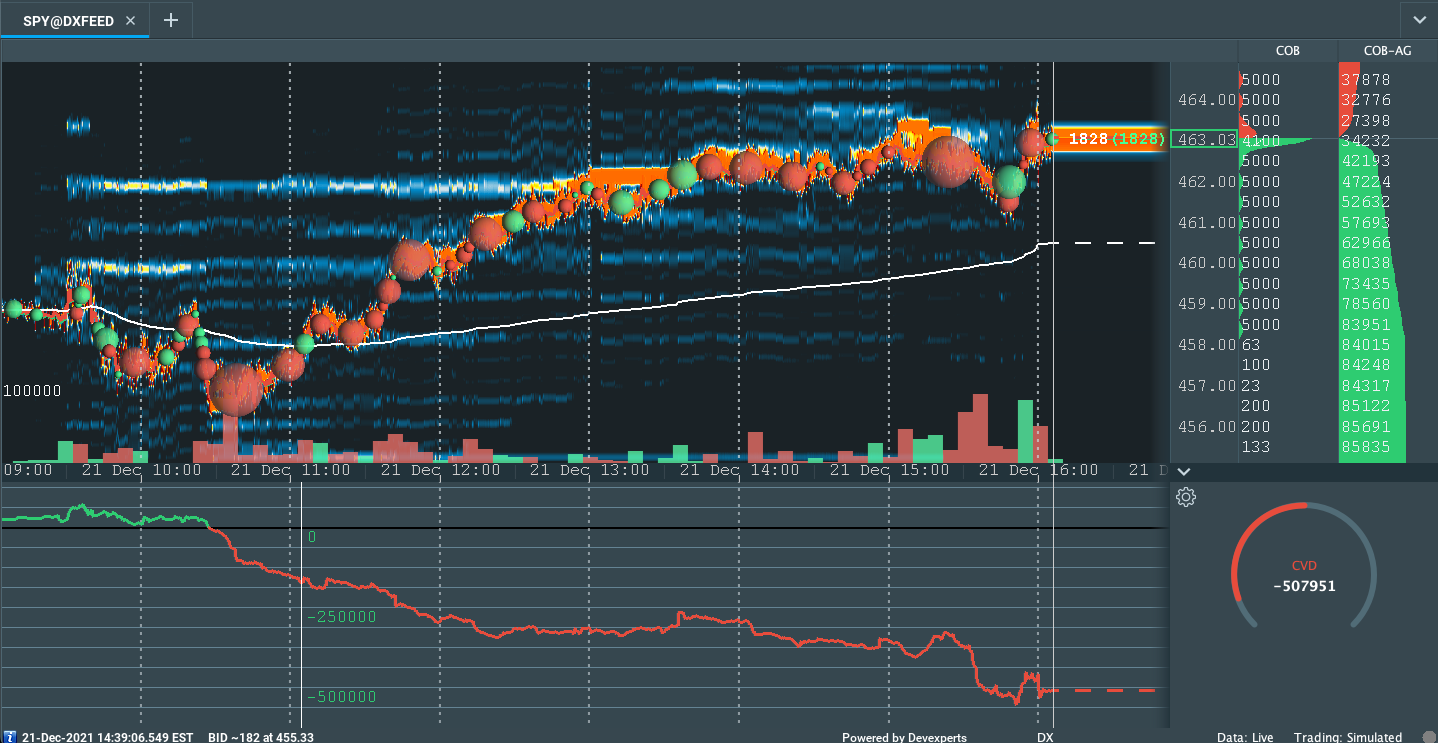

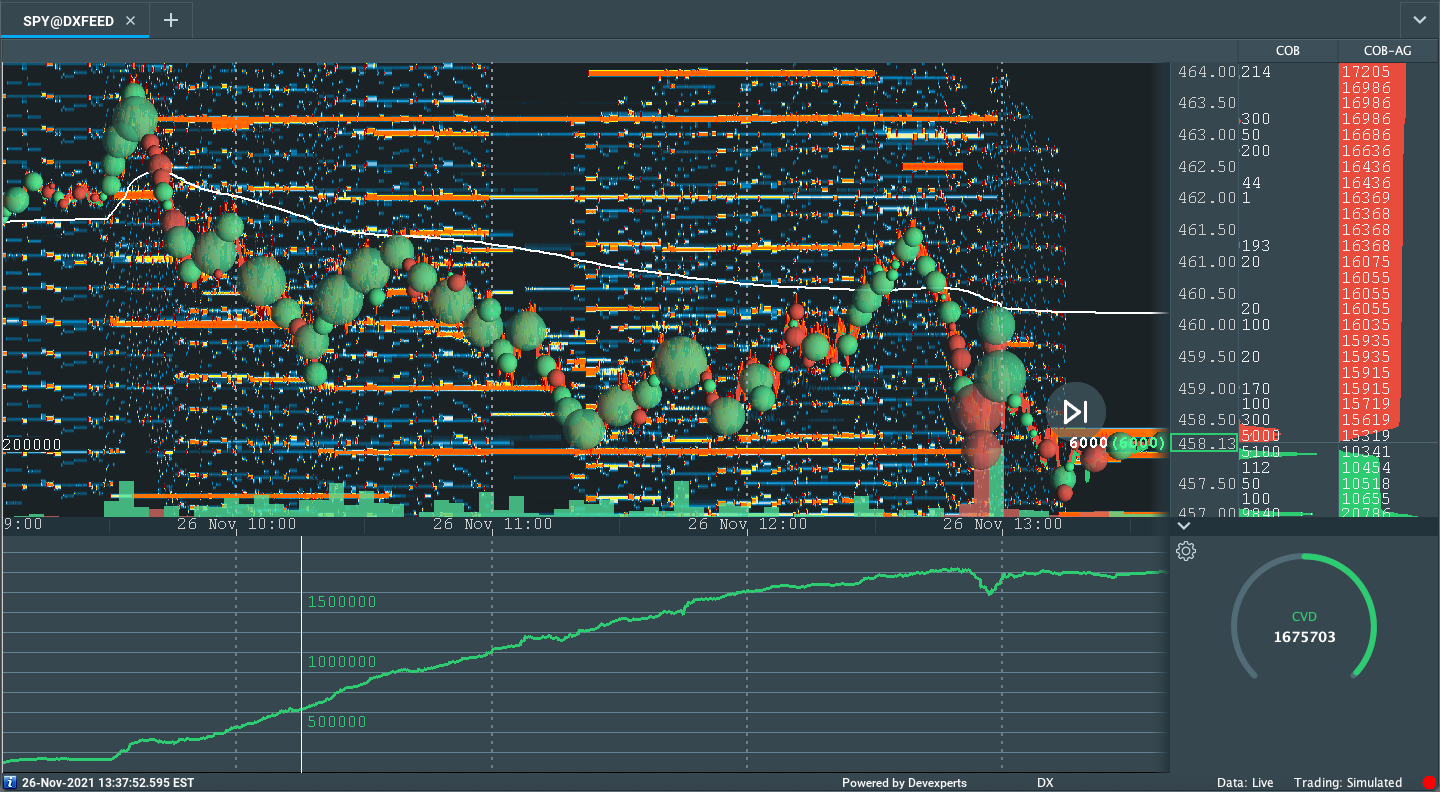

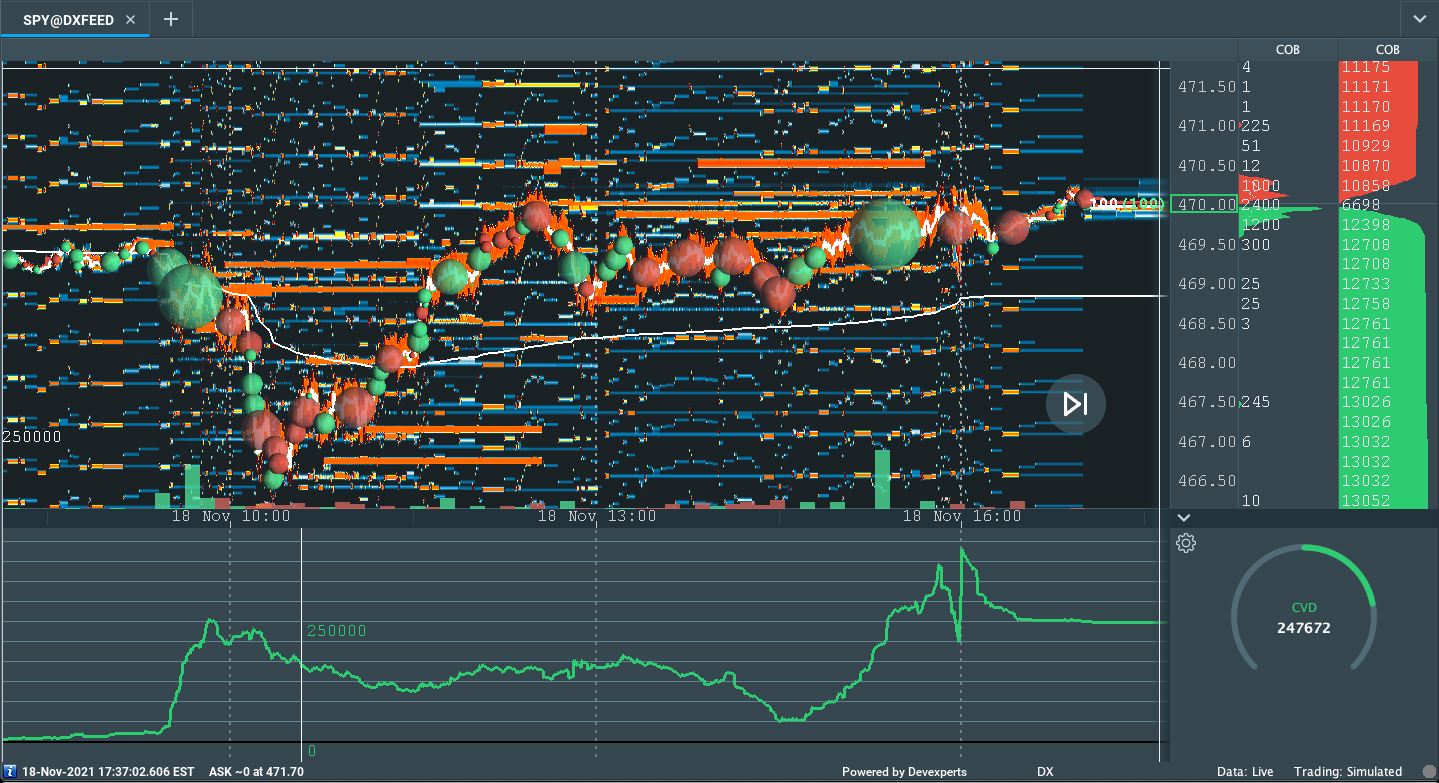

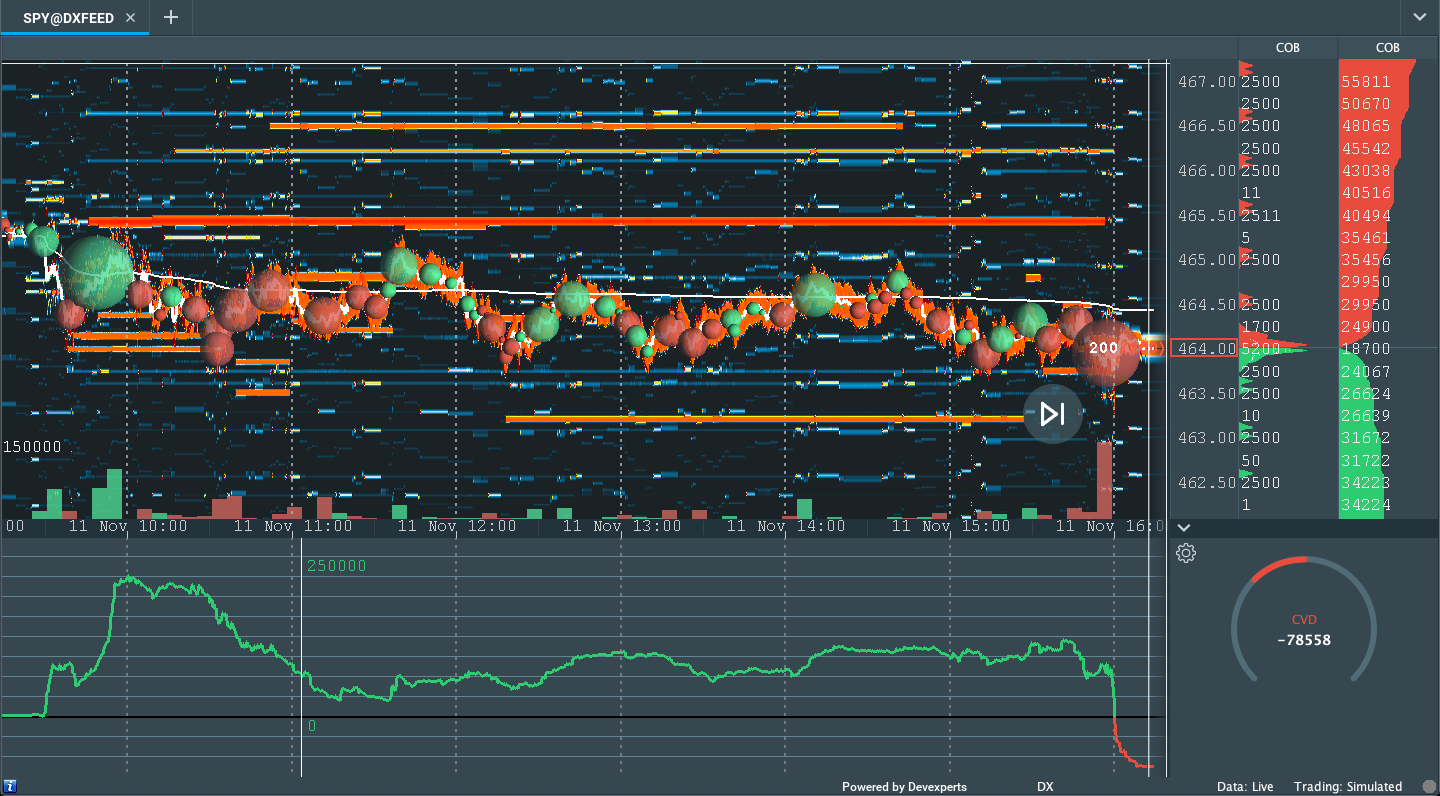

Graphic: Divergent delta (i.e., non-committed buying as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, via Bookmap. The readings are supportive of responsive trade (i.e., rotational trade that suggests current prices offer favorable entry and exit; the market is in balance).

Context: In light of elevated implied volatility and limited macro, and micro catalysts, Goldman Sachs Group (NYSE: GS) sees “options selling strategies as attractive in the near term.”

“We estimate there is a 12% probability of a 1-month 5% down-move in the SPX in this economic environment based on our GS-EQMOVE model. Options are pricing a 22% probability of that size move indicating that puts are overvalued.”

The commitment of capital on lower directional volatility results in counterparties taking on more exposure to positive gamma which they will offset by supplying the market with liquidity, thereby pressuring the price discovery process.

Note: As a position’s delta rises with stock or index price rises, gamma (or how an option’s delta is expected to change given a change in the underlying) is added to the delta.

“I use this analogy of a jet,” Kai Volatility’s Cem Karsan once explained to me, referencing the three factors – the change in the underlying price (gamma), implied volatility (vanna), and time (charm) – that are well known to impact an options exposure to directional risk or delta.

“As volatility is compressed, those jets will keep firing because … the hedging vanna and charm flows, and whatnot will push the markets higher.”

Still, many products are in lower liquidity and short-gamma (wherein an options delta decreases with stock prices rises and increases when stock prices drop) in which moves are more erratic.

If the S&P were to further trend sideways, as a result of the aforementioned hedging pressures, a decline in correlation – among volatile constituents – would be the only reconciliation.

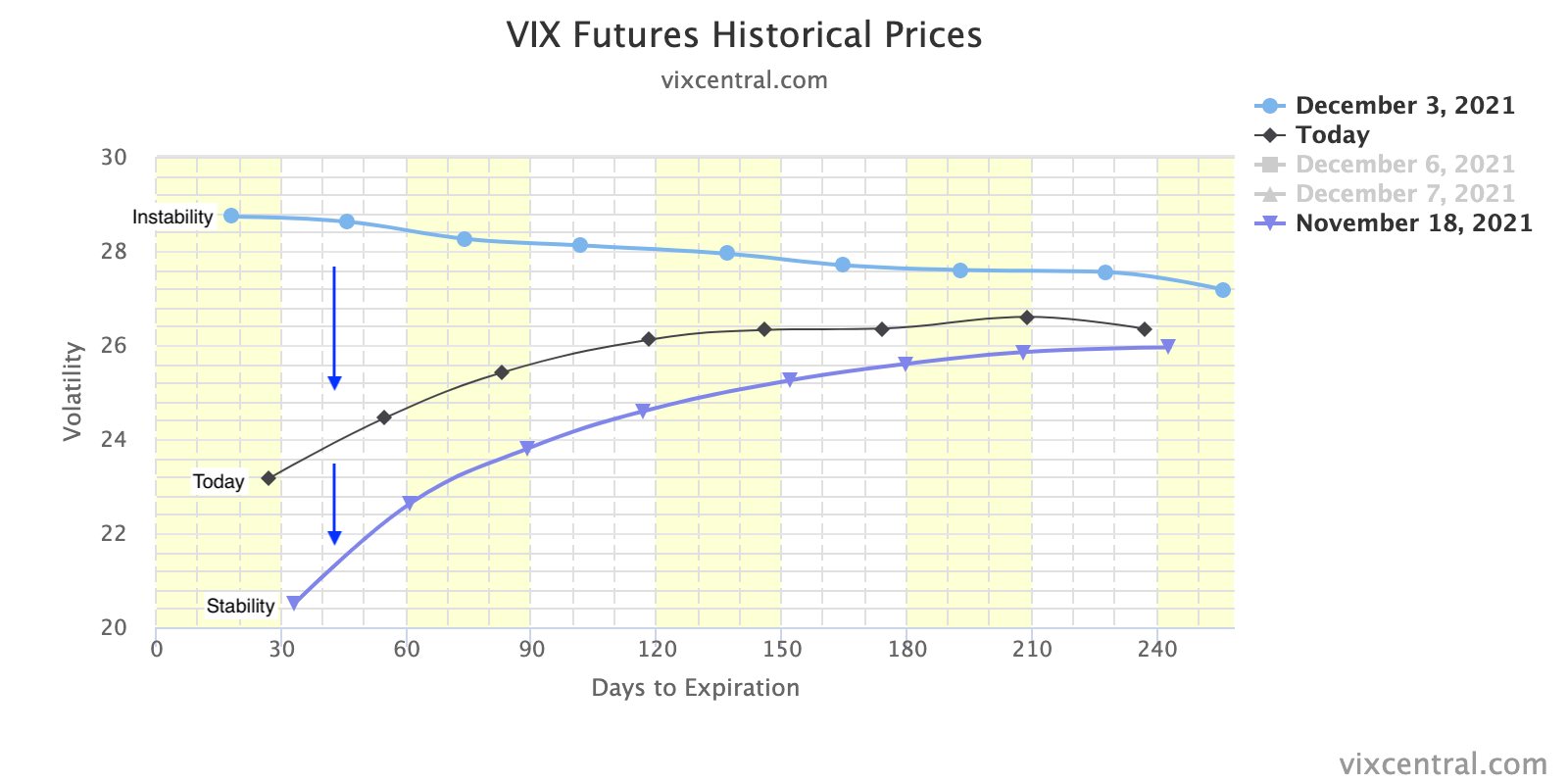

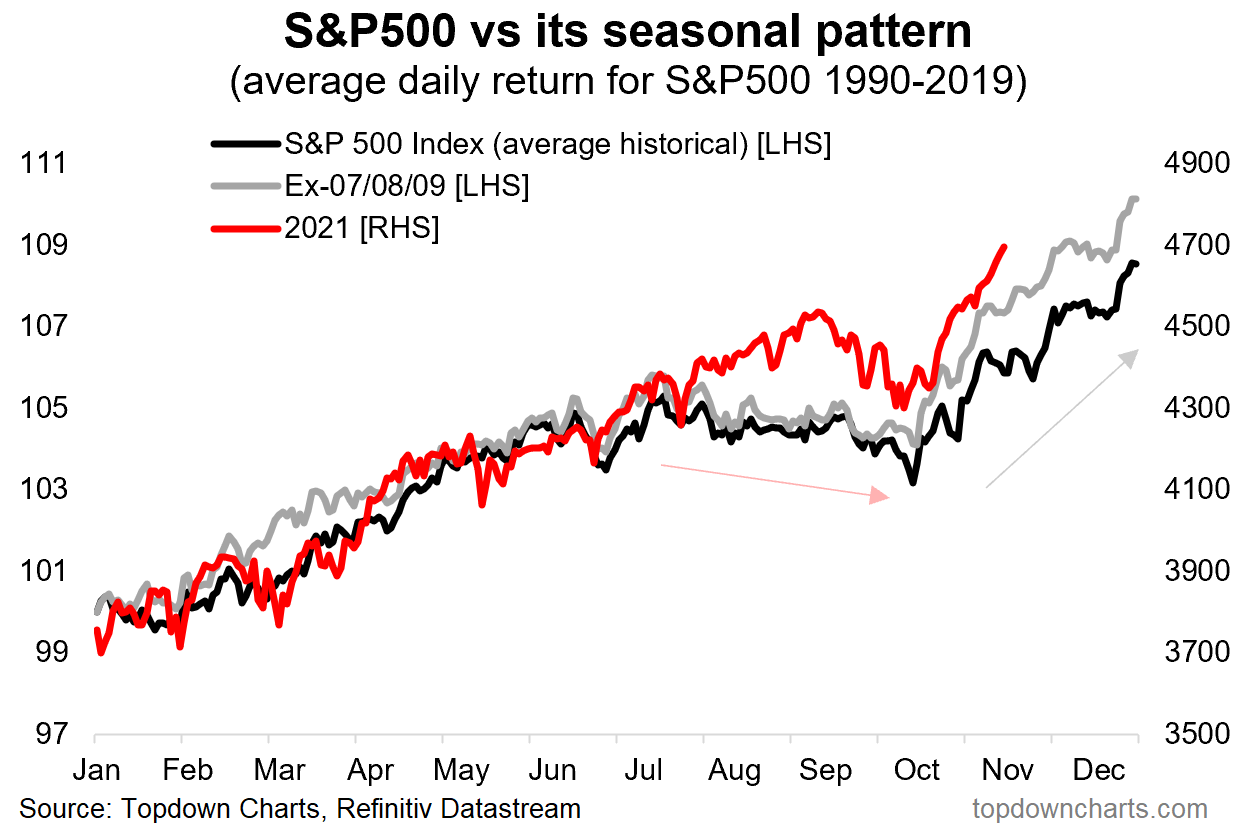

A post-holiday collapse in implied volatility, coupled with the management of massive S&P positions, and relentless, seasonally-aligned “passive buying support,” may bring in positive flows that would bolster any attempt higher.

Graphic: A compression in the VIX term structure would provide markets a boost.

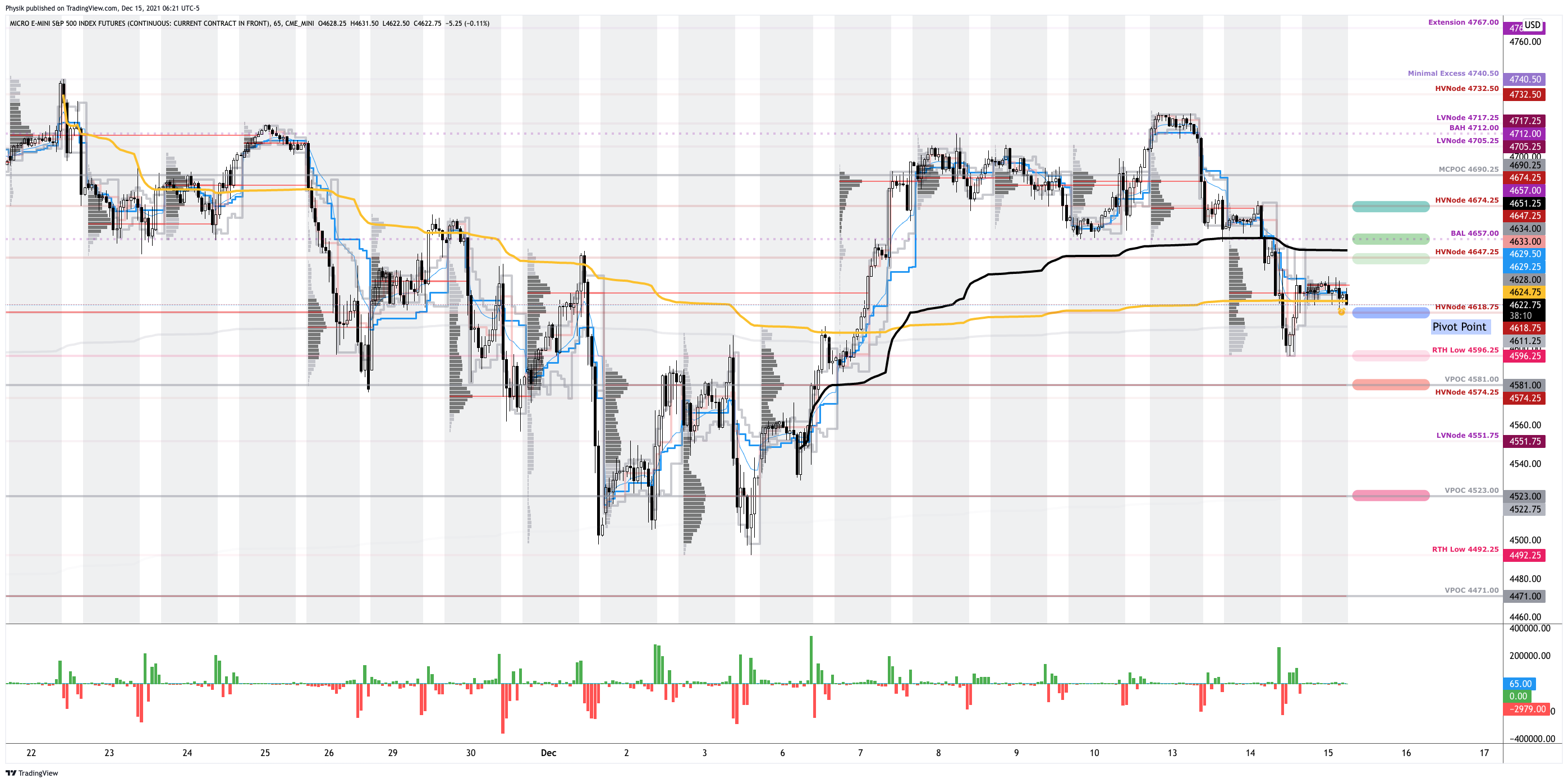

Expectations: As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a balanced overnight inventory, just outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios In Play: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator.

Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,623.00 point of control (POC) puts in play the $4,647.25 high volume area (HVNode). Initiative trade beyond the HVNode could reach as high as the $4,674.25 HVNode and $4,709.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,623.00 POC puts in play the $4,585.00 VPOC. Initiative trade beyond the VPOC could reach as low as the $4,574.25 HVNode and $4,549.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

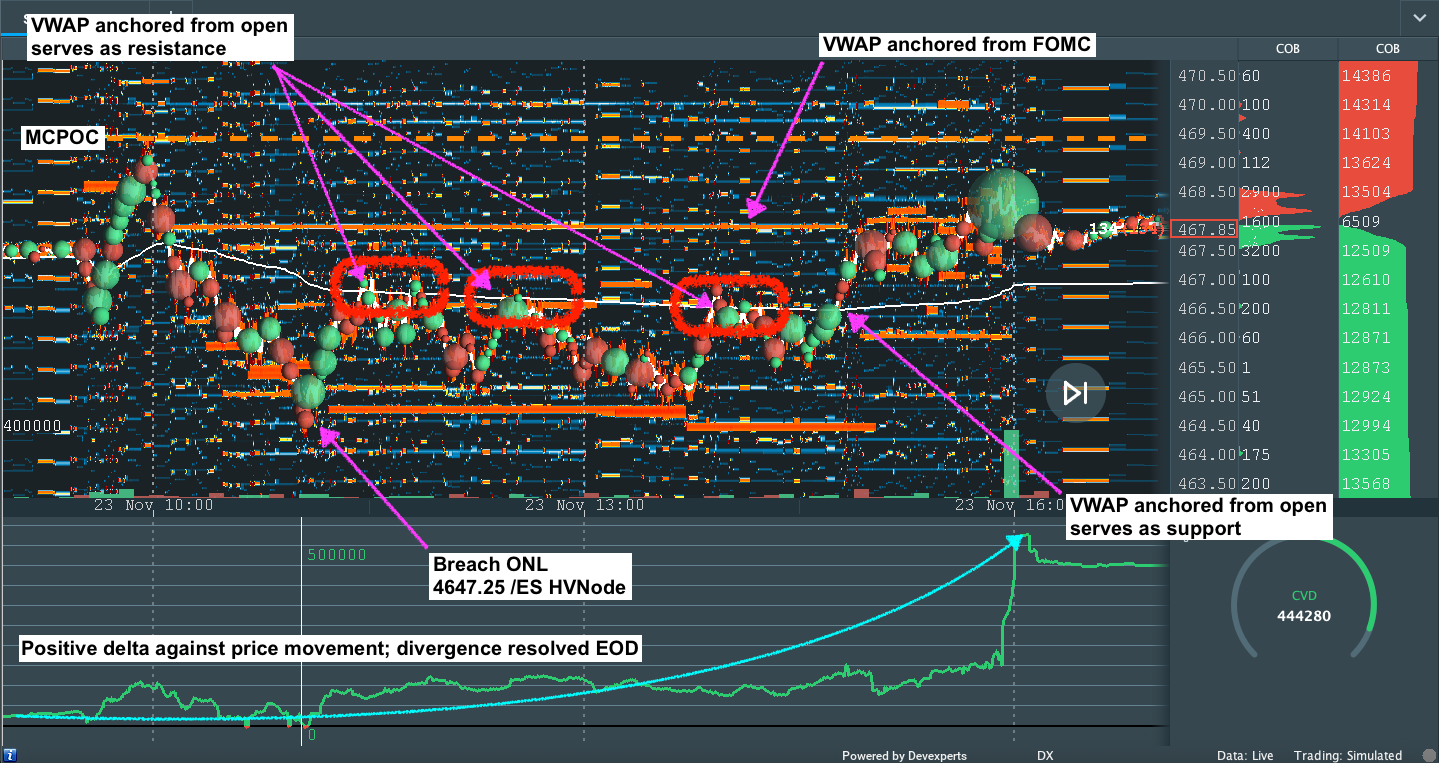

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

What People Are Saying

To me, this is really the most cautious sign in this environment.

Contrary to the news outlets, there has not been any real “fear” hitting the derivatives market. Yes there was a bid in vol, but we have been noticing a lot of orders on the tape opening to sell Vega. https://t.co/scRyKSSTTy

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, helping develop insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not carry the right to provide advice. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

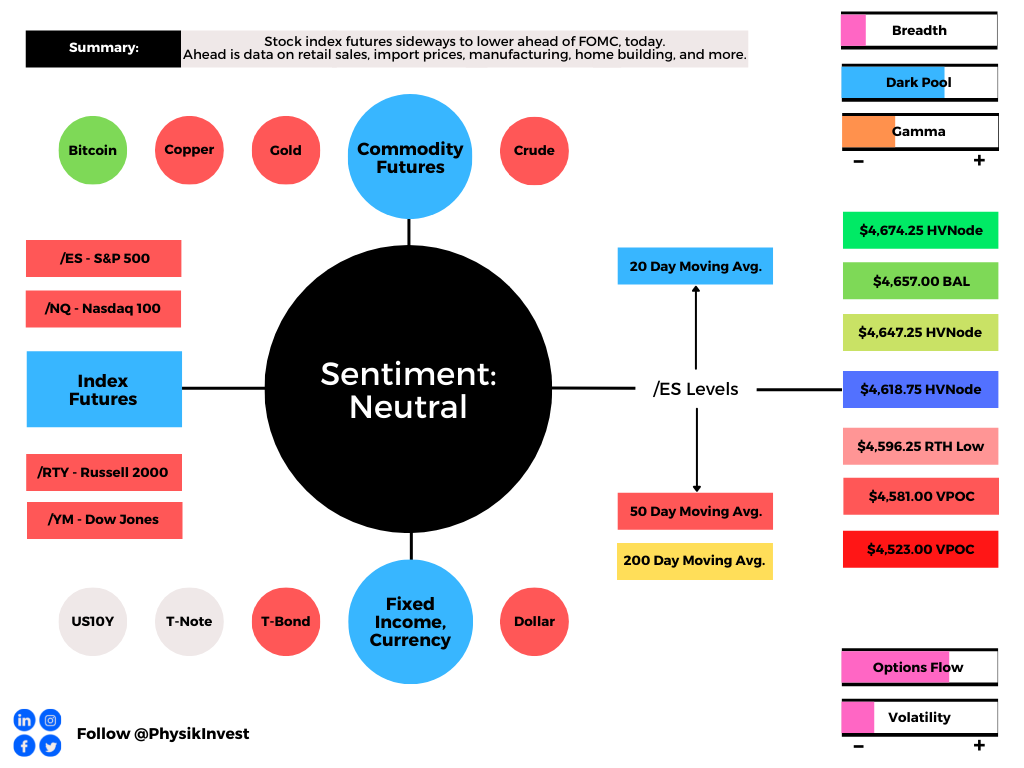

Equity index futures are lower after Monday’s failed balance-area breakout in the S&P 500 had that index rotate to and through the opposite end of a multi-day consolidation, yesterday.

This trade is in the face of expectations the Federal Reserve (Fed) will accelerate the taper to bond-buying, clearing the way for interest-rate hikes.

Rising rates, among other factors, have the potential to decrease the present value of future earnings, thereby making stocks, especially those that are high growth, less attractive.

The ruling narrative, so to speak, has resulted in the selling of expensive areas of the market.

Ahead is retail sales, import prices, and Empire State Manufacturing Index (8:30 AM ET) data.

Then there are releases on the NAHB Home Builders’ Index, business inventories, inventory-sales ratio (10:00 AM ET). Later is a Federal Open Market Committee (FOMC) announcement (2:00 PM ET) and press conference (2:30 PM ET).

Graphic updated 6:25 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

According to SpotGamma, into this week, participants had been increasing their short-delta exposure (via a lot of call selling and a bit of put buying).

This resulted in dealers selling (buying) futures into strength (weakness), a dynamic that promotes consolidation.

Later, as participants positioned for the FOMC event, demand for protection expanded and the S&P 500 made it to and through the low-end of the consolidation against the $4,700.00 high activity options strike.

The trade built out areas of high volume (HVNode) via the cave-fill process in locations where prior discovery left weak structure – gaps and p-shaped emotional, multiple distribution profile structures (i.e., old-money covering shorts).

As evidenced by the divergent delta, below, responsive buyers surfaced at a key volume-weighted average price (VWAP) level (near $4,600.00 S&P 500), at which liquidity algorithms are benchmarked and programmed to buy and sell.

Graphic: Divergent delta (i.e., non-committed selling as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, via Bookmap. The readings are supportive of responsive trade (i.e., rotational trade that suggests current prices offer favorable entry and exit; the market is attempting in balance).

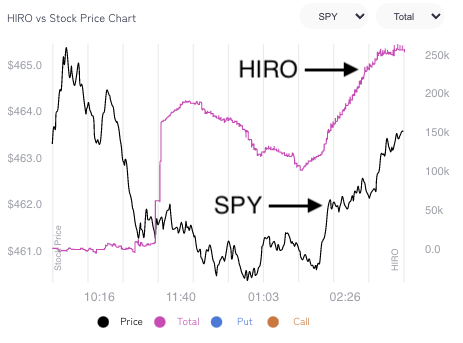

At the same time, as SpotGamma (beta) Hedging Impact of Real-Time Options (HIRO) indicator suggested “participants saw lower prices as an opportunity to express their opinion of lower volatility into Wednesday’s Federal Open Market Committee (FOMC) update.”

Graphic: SpotGamma’s Hedging Impact of Real-Time Options (HIRO) indicator, which is pink in color, was sideways to higher. This suggests positive options delta trades likely had dealers buying stock/futures into the close.

Context: Today, we get clarity from the Fed.

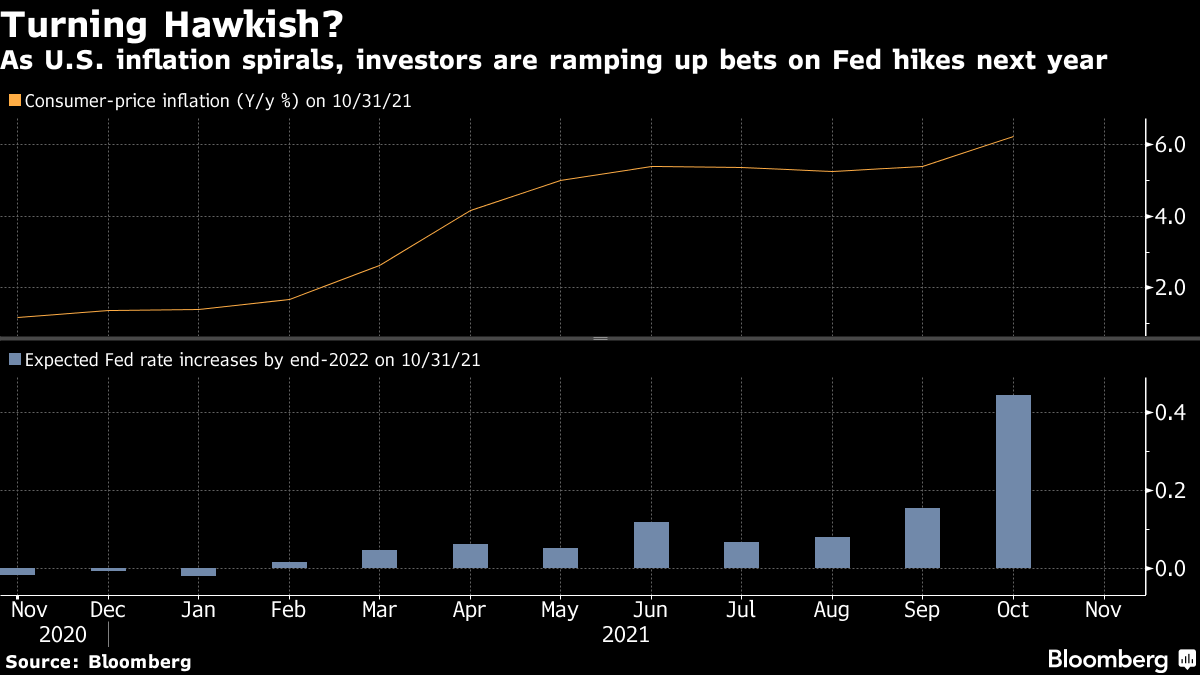

The expectation is that the asset purchases are scaled back by $30 billion per month versus the expected $15 billion. In doubling the pace of the taper to bond-buying, the odds of earlier rate hikes increase markedly.

“If the Fed does not address inflation soon, they risk long rates shooting much higher,” says Jim Bianco of Bianco Research.

“But if they follow the market’s lead in aggressively hiking rates, they risk hurting the economy. We understand the Fed’s paralysis given the massive uncertainty coming out of the pandemic. However, the longer they wait to address inflation, the worse this conundrum will become.”

Notwithstanding, today’s rates are supporting validations better than in the ‘90s.

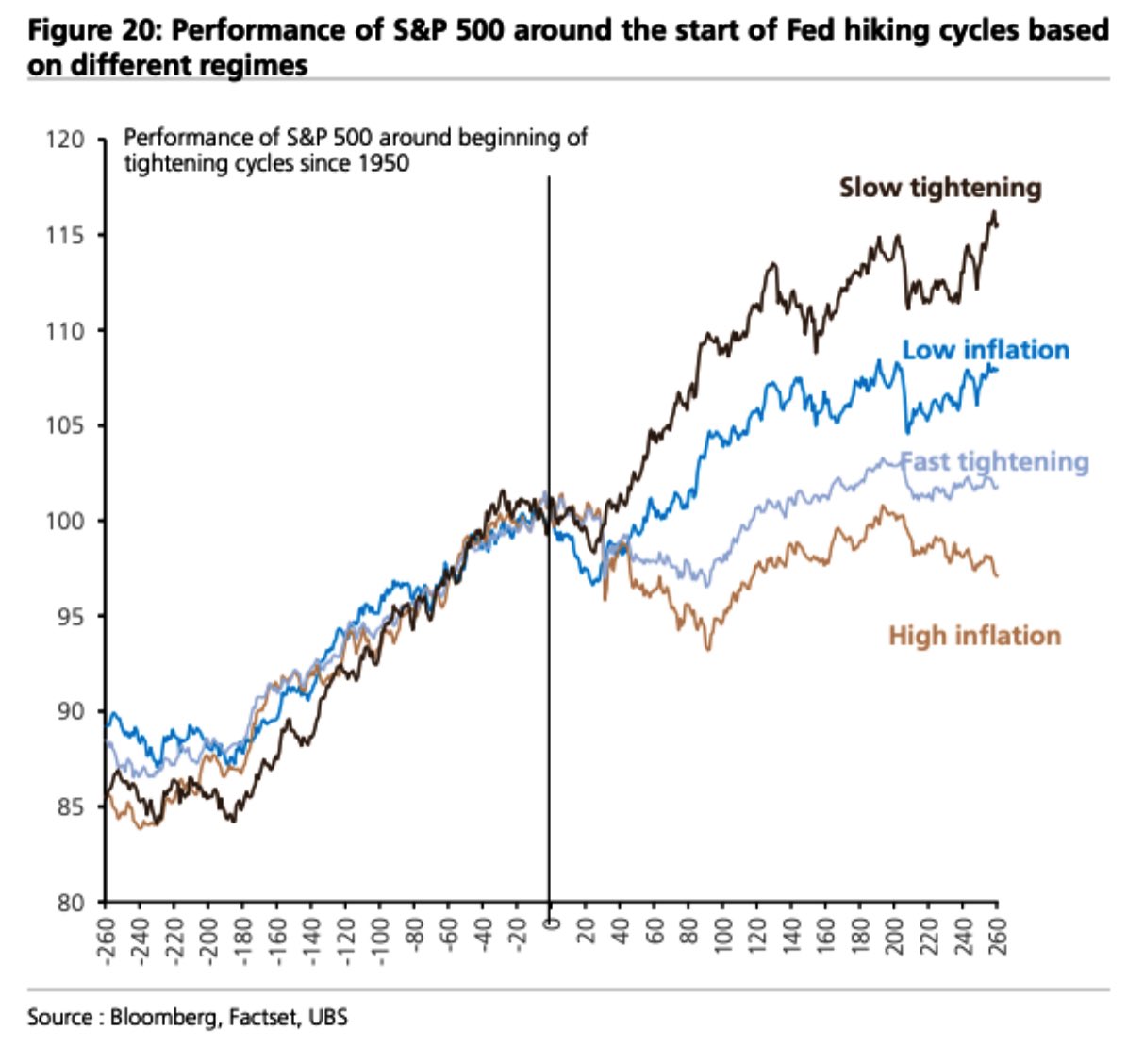

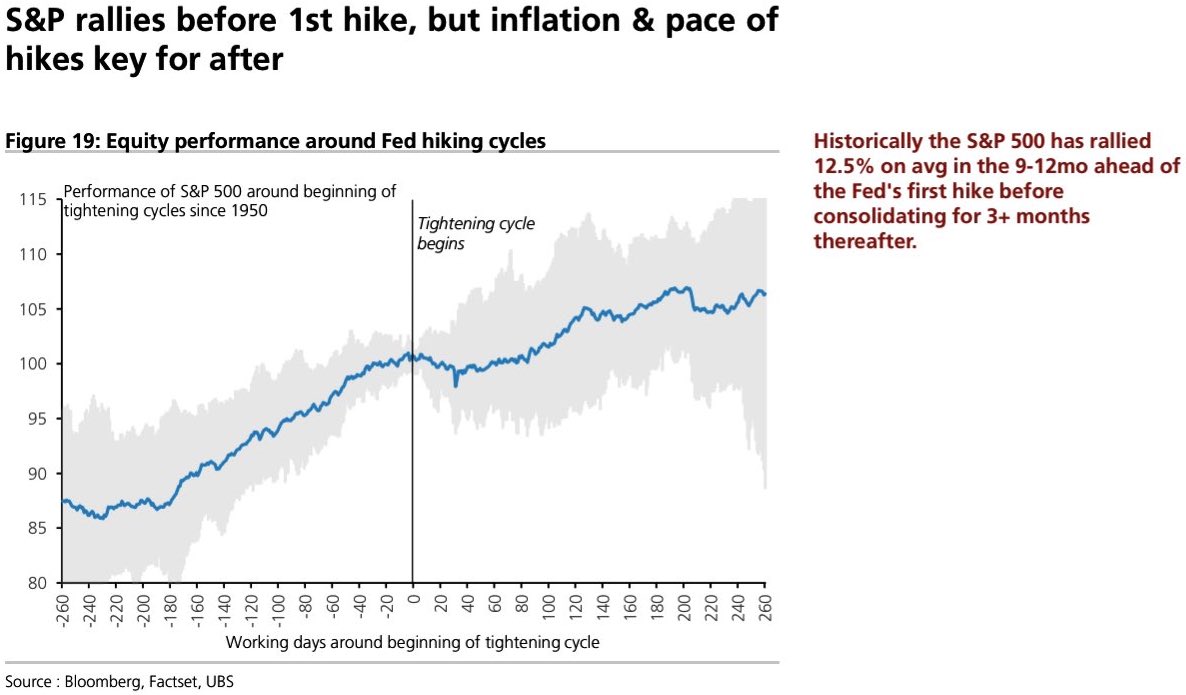

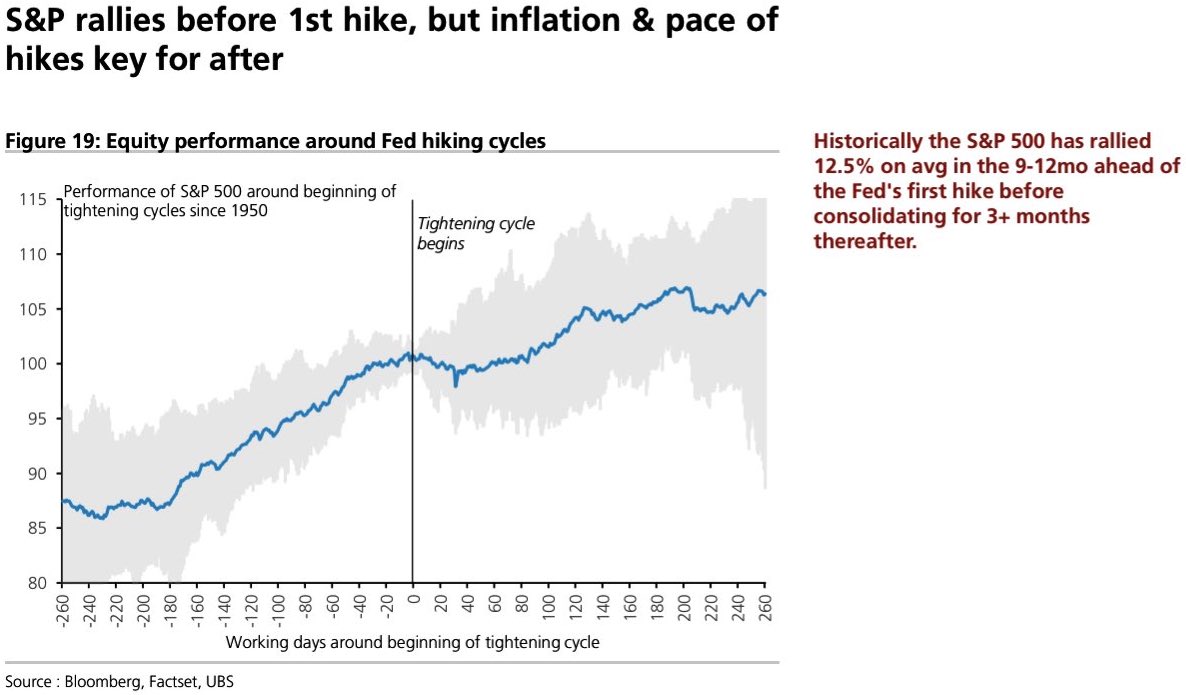

At the same time, equity markets tend to rally into the first hike; Moody’s Corporation’s (NYSE: MCO) forecast aligns with that – “the Dow Jones Industrial Average increases this quarter and peaks in early 2022, … [followed by] steady decline through 2022.”

Graphic: S&P 500 performance before and after rate hikes.

Immediate risks, though, remain.

There are growing pockets of weakness – as evidenced by divergent breadth – in the face of U.S. stocks’ inflation-adjusted earnings yield turning negative.

Similarly, participants are more exposed to leveraged products, among other things, which increases the speed with which volatility is realized.

“One potential catalyst would be an explosion in the value of margin accounts at brokers and dealers, which amounted to $595 billion in the second quarter, nearly double the pre-pandemic level. A drop in stock prices could trigger margin calls.”

So despite “natural, passive buying support” and positioning metrics flashing a buy, as well as expectations of “the strongest quarterly nominal [economic] growth in more than three decades,” offsides positioning may prompt a reaction that exacerbates underlying price movements.

So what? The market is in a positive-gamma environment wherein the counterparties to customer options trades add market liquidity and temper realized volatility.

If participants’ monetary policy fears are assuaged, a collapse in event-related implied volatility ought to bring positive flows as the long delta (from dealers’ exposure to short puts) decreases.

The decrease in dealer supply (short delta) post-FOMC and -OPEX, via the covering of short stock/futures hedges to put-heavy positioning, ought to bolster any attempt higher.

That’s not to say that some of the vulnerabilities like participants’ large exposure to leveraged products (which increases the speed with which volatility is realized) couldn’t prompt a round of destabilizing demand for downside protection.

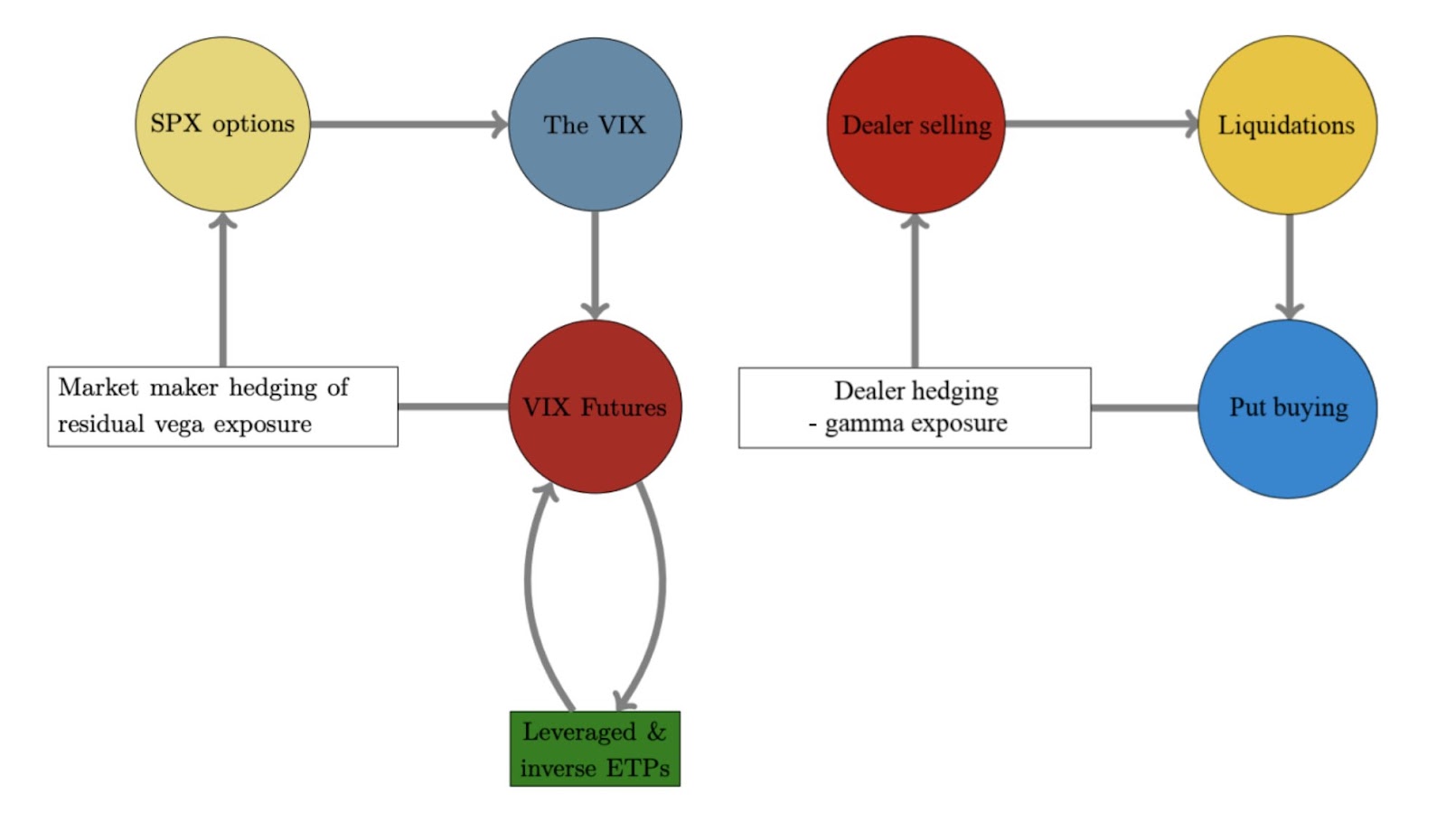

Graphic: The “Biggest tail risk to SPX isn’t any macro data/virus/war but its own options market.”

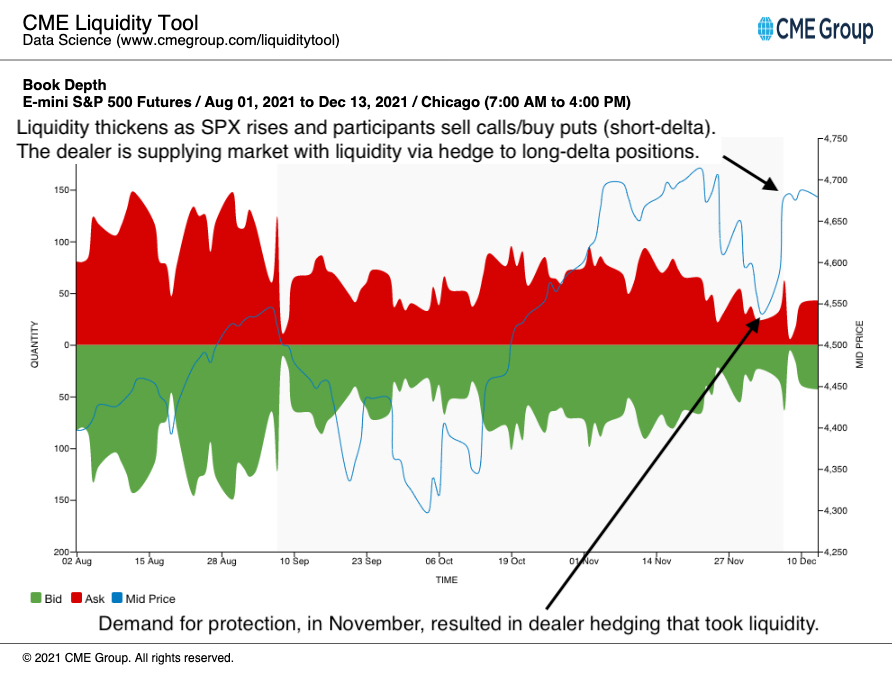

Though order book depth “in isolation is not the correct method to gauge liquidity,” it can help in roughly assessing participants’ demand/supply as volatility (and stress, by that token) increases.

Graphic: Analysis of book depth for the E-mini S&P 500 futures contract, via CME Group Inc’s (NASDAQ: CME) Liquidity Tool. For more on the implications of participants’ options positioning and dealer hedging, read here.

Already, according to Bloomberg, some participants are positioning for “a seasonably favorable period for stocks” in 2021; “someone purchase[d] roughly 20,000 call spreads that are linked to the S&P 500 and expire right before the Christmas holiday. The transaction involved selling calls with a strike price at 4,750 to fund bullish options exercisable at 4,650.”

Graphic: S&P 500 finds support in area between the 20- and 50-day simple moving average. The aforementioned bullish “call spread” trade expiring before the Christmas holiday is included.

Expectations: As of 6:25 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,618.75 high volume area (HVNode) puts in play the $4,647.25 HVNode. Initiative trade beyond the latter could reach as high as the $4,657.00 balance area low (BAL) and $4,674.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,618.75 HVNode puts in play the $4,596.25 regular trade low (RTH Low). Initiative trade beyond the RTH Low could reach as low as the $4,581.00 and $4,523.00 untested point of control (VPOC), or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

What People Are Saying

The end of the year (December) is typically a tough trading month for me. Ive learned that it’s about what people have to do in the market, not what they want to do. Correlations are also deceiving because of this. Don’t ruin Christmas by overthinking & over trading in December

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, helping develop insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not carry the right to provide advice. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

Editor’s Note: The purpose of these commentaries is to align ourselves better for the day ahead. Seldom, however, do we step away to align ourselves with trade across larger time horizons.

Given the proximity to the new year, I shall be placing more attention on planning.

How do we model a trading plan? Here is one link on things to consider.

What Happened

Overnight, equity index futures were divergent; the Russell 2000 and Dow Jones Industrial Averaged traded weak relative to their peers the S&P 500 and Nasdaq 100.

This is as scientists discovered a harder-to-detect version of omicron that may be countered with an extra dose of vaccine.

In other news, the U.K. was set to impose new COVID-19 restrictions, the House passed a bill opening the way to a quick debt ceiling increase, and the list of Chinese developers warning they may not be able to meet upcoming financial obligations grew.

Ahead is data on job openings and quits (10:00 AM ET).

Graphic updated 6:30 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

On strong intraday breadth and divergent market liquidity metrics, the best case outcome occurred, yesterday, evidenced by an upside gap, expansion of range, and separation of value.

Similar to Tuesday’s commentary, though this activity marks participants’ willingness to change the trend, the structure is poor. As a result, there is technical instability.

Specifically, both Monday and Tuesday’s sessions left gaps and p-shaped emotional, multiple-distribution profile structures (i.e., old-money shorts covering).

As said before, participants will look to revisit, repair, and strengthen – build out areas of high volume (HVNodes) via the cave-fill process – these areas of low volume (LVNodes).

Graphic: Divergent delta (i.e., non-committed buying as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, via Bookmap. The readings are supportive of responsive trade (i.e., rotational trade that suggests current prices offer favorable entry and exit; the market is attempting to balance).

Context: Has anything really changed since the November monthly options expiration (OPEX)?

Sure, we had some news with respect to COVID-19, China, and U.S. growth, but any associated fears were fast assuaged.

In the span of four days, the S&P 500 rose nearly 5.00%. That’s just over 200 points!

Much of what we’re seeing is the direct result of changing market structure; participants are more exposed to leveraged products, among other things, which increases the speed with which volatility is realized.

This is really rather remarkable.

On one hand you have equity put volume (orange) unleashing the kraken. Meme's deleveraging.

Other corner: SPX, uninspired.

“There lies a sleeping giant. Let him sleep! For when he wakes, he will shake the world.” pic.twitter.com/RK7nOTQwV7

Participants went from being exuberant and underexposed to protection – in the face of weakening breadth/fundamentals – to generating destabilizing demand for protection.

Alongside that demand of (shorter-dated) protection (where options sensitivity to direction is higher) was the market’s entry into short-gamma. In such an environment, counterparties to customers’ options trades exacerbate underlying volatility through hedging.

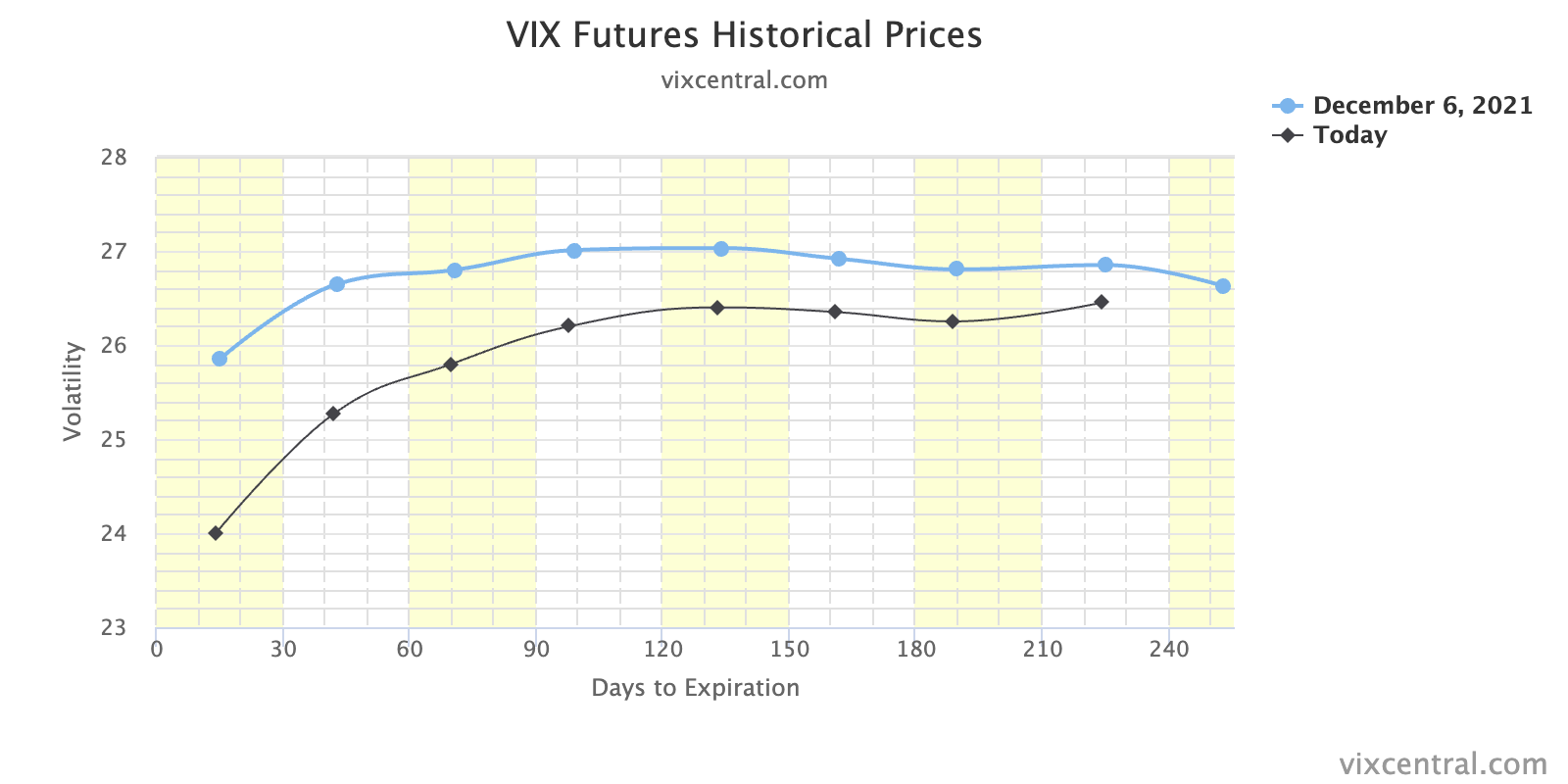

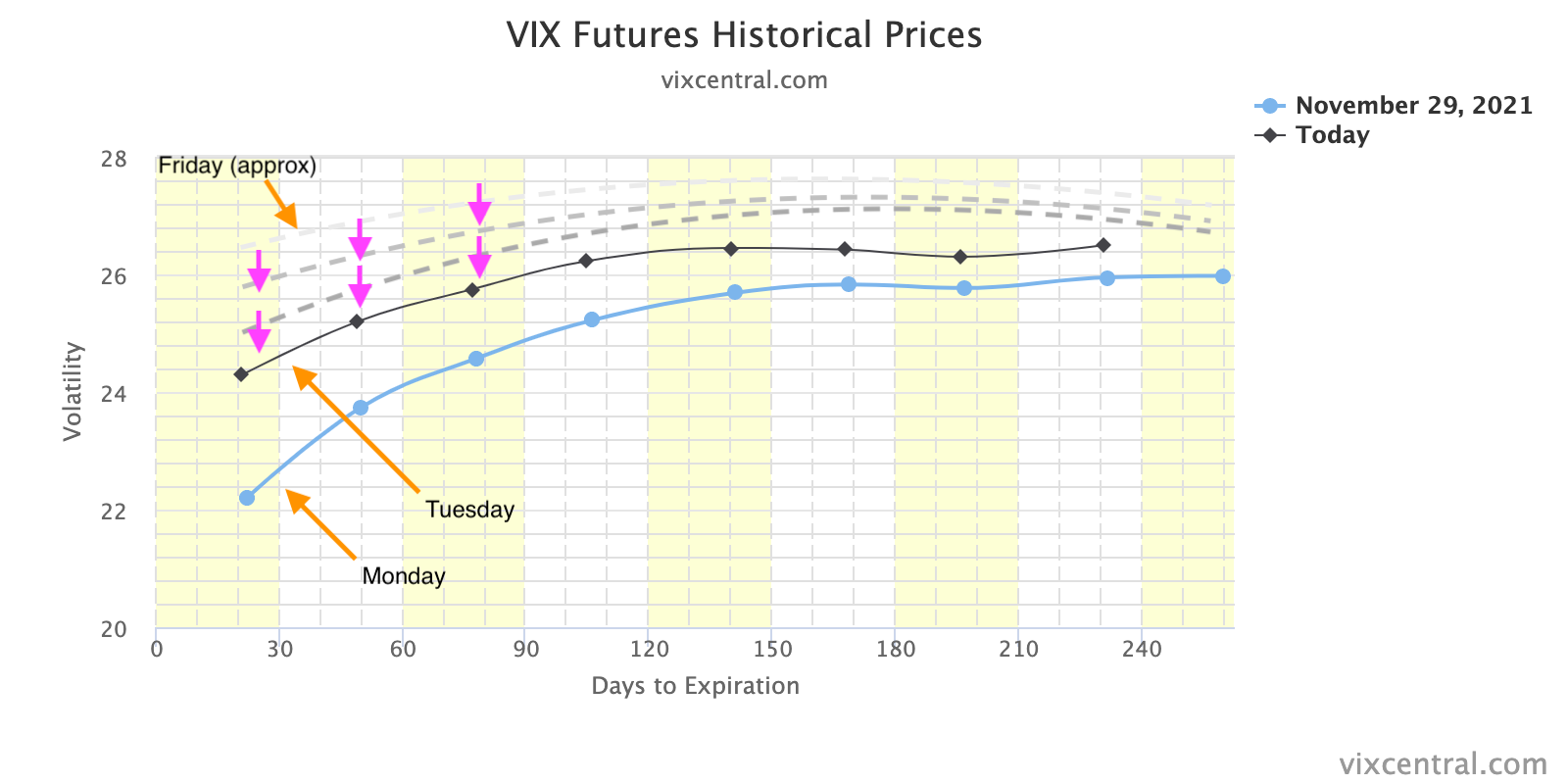

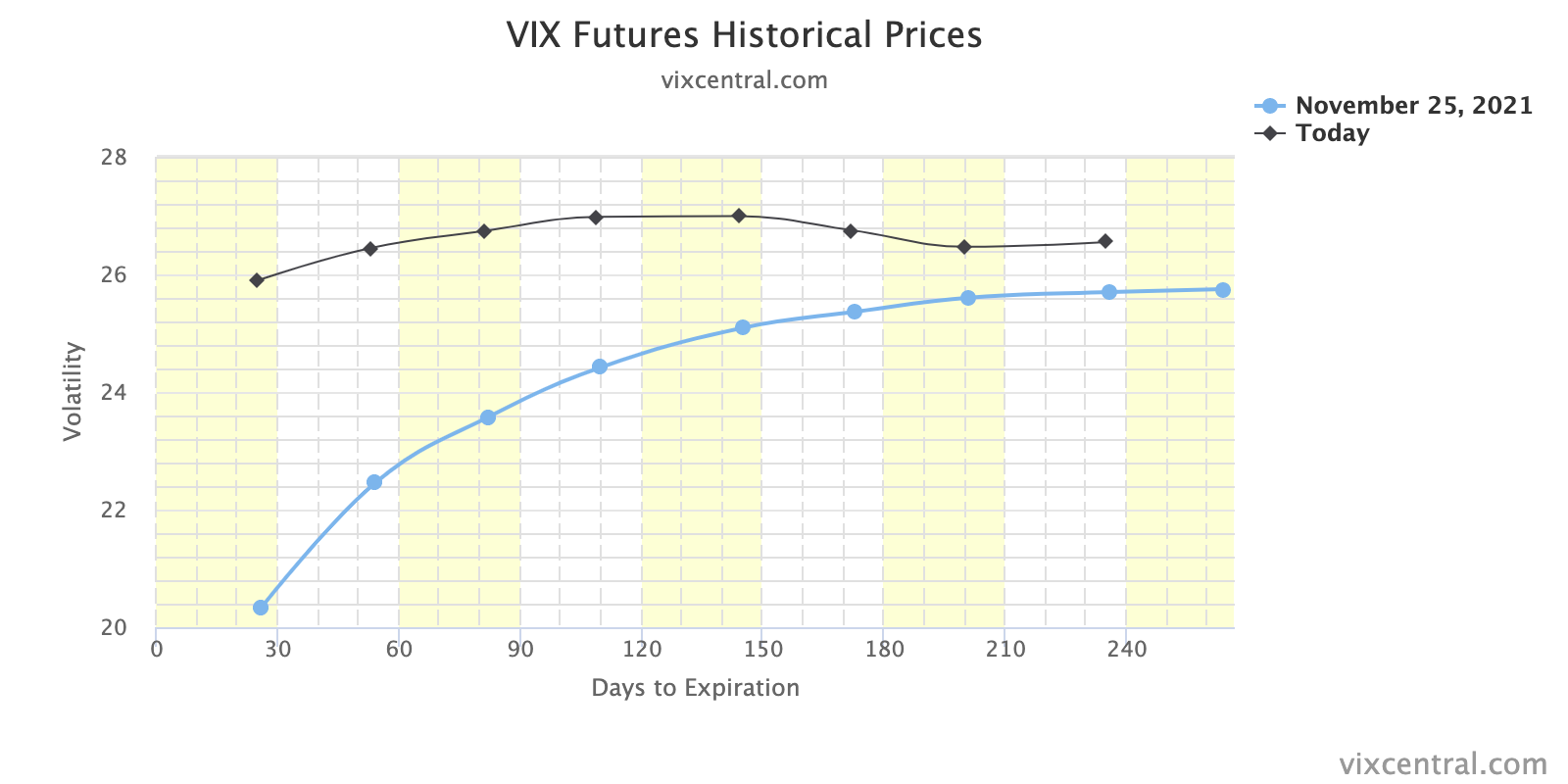

Note all that movement in the front-end of the VIX futures term structure, below. Wow!

$VIX futures term structure starting to move down to the pre-Thanksgiving levels. I call these episodes "There and Back Again". Always good to test your trading strategy against such episodes taking into account not only profit and loss but also changes in margin requirements. pic.twitter.com/1fY9wHn2fe

In the face of all the fear was “natural, passive buying support,” however, and expectations that short-dated protection (if realized volatility was to not be expressed to the downside) would either roll off the table (expire) or be monetized, resulting in counterparties reversing their hedges (initially short stock/futures) and supporting the market (buying to cover).

As said on December 6, and many commentaries before that, this “flow is stabilizing and may play into a seasonally-aligned rally into Christmas as participants see defenses rolled out against the new COVID-19 variant,” and so on.

Based on this week’s trade, thus far, it seems that the bull thesis is playing out.

So you’re telling me to buy every S&P 500 call under the sun, right? NO!

There has yet to be a notable strengthening in overall market breadth and volatility remains rich in the face of the fast-approaching December OPEX and December 15-16 Federal Open Market Committee (FOMC) meeting.

Traders are antsy and have already started pricing in potential rate overshoots; Federal Reserve Chair Jerome Powell went from being uber dovish to increasingly hawkish on the topic of taper and interest rate expansion.

Though today’s rates and earnings support validations better than in the ‘90s, an intent to moderate stimulus serves as a headwind; the U.S. may realize the swiftest tightening in financial conditions since 2005 if the Fed was to hike rates three times next year. Yikes!

So, we have to be careful here.

Despite the S&P rallying into the first hike, historically, dynamics with respect to market structure introduce a lot of noise. Therefore, we ought to be looking at structures that have little to lose in episodes where stress surfaces and volatility is expressed to the downside.

Graphic: UBS Group AG (NYSE: UBS) research on S&P performance into rate hikes.

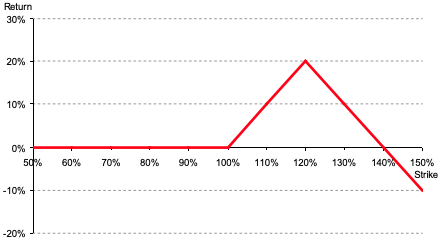

Examples of low-cost options structures include call-side calendars, butterflies, and ratio spreads.

Graphic: Via Banco Santander SA (NYSE: SAN) research, the return profile, at expiry, of a classic 1×2 (long 1, short 2 further away) ratio spread.

If opportune (and well-capitalized), there are opportunities to finance debits on the call side with structures on the put side.

This, above, is no recommendation. It’s more so how I’m looking at the current market.

In summation, the return distribution is skewed positive, still, at this juncture, but a lot of the opportunity (based on how participants were positioned just a weak ago) has disappeared.

That’s not to say we can’t go higher; upon a smooth passage of the December FOMC and OPEX there may be an unwind of “structural positioning that naturally drives markets higher as long as volatility is compressed.”

Expectations: As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,691.25 HVNode puts in play the $4,705.75 LVNode and overnight high (ONH). Initiative trade beyond the latter could reach as high as the $4,716.75 LVNode/ONH and $4,740.50 minimal excess high, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,691.25 HVNode puts in play the $4,674.25 micro composite point of control (MCPOC). Initiative trade beyond the MCPOC could reach as low as the $4,647.25 and $4,618.75 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

What People Are Saying

A month ago, @SqueezeMetrics shared an intriguing idea about $TSLA potentially destroying passive income from within the $SPX index.

He referred to it as the Trojan horse.

I decided to explore this scenario further and outline how it might play out 👇https://t.co/UM66zYgkBI

You have to minimize your losses and try to preserve capital for those very few instances where you can make a lot in a very short period of time. What you can’t afford to do is throw away your capital on suboptimal trades.

1. Big picture failed breakout 2. Broken intermediate-term uptrend 3. Retest of the underside of a flat 200d MA 4. First Daily RSI oversold reading since 3/2020

Cave-Fill Process: Widened the area deemed favorable to transact at by an increased share of participants. This is a good development.

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure.

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, helping develop insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not carry the right to provide advice. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

Overnight, screens went green as equity index and commodity futures auctioned sideways to higher as fears regarding the Chinese economy and omicron were assuaged.

Specifically, China moved to ease monetary policy and studies revealed GSK’s antibody treatment working on the COVID-19 omicron variant.

Ahead is data on the trade deficit, productivity, and unit labor costs (8:30 AM ET), as well as consumer credit (3:00 PM ET).

Graphic updated 6:30 AM ET. Sentiment Risk-On if expected /ES open is above the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

On supportive intraday breadth and divergent market liquidity metrics, the best case outcome occurred, evidenced by an upside gap, expansion of range, and separation of value.

This activity, which marks participants’ willingness to change the trend, is on top of poor structure, a dynamic that adds to technical instability.

Specifically, Monday’s session left a gap and p-shaped emotional, multiple-distribution profile structure (i.e., old-money shorts covering).

Going forward, participants will look to revisit, repair, and strengthen – build out areas of high volume (HVNodes) via the cave-fill process – these areas of low volume (LVNodes).

Graphic: Divergent delta (i.e., non-committed buying as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, via Bookmap. The readings are supportive of responsive trade (i.e., rotational trade that suggested current prices offered favorable entry and exit).

Context: COVID-19, China, and U.S. growth, as well as improvements in positioning metrics.

Overnight, there was news that GlaxoSmithKline Plc’s research showed its antibody treatment effective against mutations in the omicron variant.

This came after China’s decision to reduce the cash banks must hold in reserves; the development releases “funds in long-term liquidity to bolster slowing economic growth.”

As noted yesterday, though there is a potential that the U.S. realizes the swiftest tightening in financial conditions since 2005, now, more than during the tech-and-telecom bubble, do rates and earnings growth support current valuations.

At the same time, DIX, which is derived from short sales (i.e., liquidity provision on the market-making side), pointed to “natural, passive buying support,” while negative gamma exposures (i.e., an environment characterized by options dealers hedging their exposure by selling into lows and buying into highs), as a result of increased demand for very short-dated downside protection, left the market prone to destabilizing volatility.

Graphic: Sensitivity in the VIX term structure, at the front end, suggests heightened activity in shorter-dated protection. As we’re starting to see, once that short-dated protection rolls off the table (and/or is monetized), counterparties/dealers will reverse and support the market, buying to close their existing stock/futures hedges.

Taken together, the distribution of forward S&P 500 returns was skewed positive, heading into Monday’s session.

Subsequent price action, after participants’ powerful responsive buying at the S&P 500’s 50-day simple moving average, which coincided with a large base of resting liquidity at $4,500.00, is follow-through on indices being positioned for a vicious rebound.

Graphic: “[N]atural, passive buying support,” coupled with strong put flows results in positive return distribution. Data via SqueezeMetrics. Graph via Physik Invest.

To tame our expectations, I end with a statement from Morgan Stanley (NYSE: MS) research:

“We reiterate our view that tapering is tightening for the markets and it will lead to lower valuations like it always does at this stage of any recovery. How much lower? We forecast S&P 500 forward P/Es to fall to 18x, or approximately 12% below current levels. Obviously, for the more expensive parts of the market, that decline will be larger.”

Expectations: As of 6:30 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator.

Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,647.25 HVNode puts in play the $4,674.25 micro composite point of control (MCPOC).

Initiative trade beyond the MCPOC could reach as high as the $4,691.25 HVNode and $4,707.00 LVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,647.25 HVNode puts in play the $4,618.75 HVNode.

Initiative trade beyond the latter could reach as low as the $4,581.00 untested point of control (VPOC) and $4,551.75 LVNode, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

What People Are Saying

Quick tips :

1. Flies are gamma trades. You buy one,you’re betting that the gamma will be tame&the underlying will drift toward your short strike.

2. The wings you buy need to be cheap. So Flies are also skew trades. Sell the guts expensive,buy the wings cheap(relative). https://t.co/5CjWsB6Nri

Cave-Fill Process: Widened the area deemed favorable to transact at by an increased share of participants. This is a good development.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

Overnight, equity index futures auctioned sideways to higher after Friday’s liquidation had the S&P 500 undercutting its 50-day simple moving average (SMA), a visual go/no-go level.

Strength shifted, again, to the Russell 2000 while the tech-heavy Nasdaq 100 was underwater. This comes as policymakers look to temper inflation with the tightening of monetary policy.

In regards to news, China’s central bank looked to boost liquidity for its slowing economy. It was also found that a new virus variant was not fueling a surge in hospitalizations; the U.S.’s adviser on the issue, Anthony Fauci, said there wasn’t “a great degree of severity to omicron.”

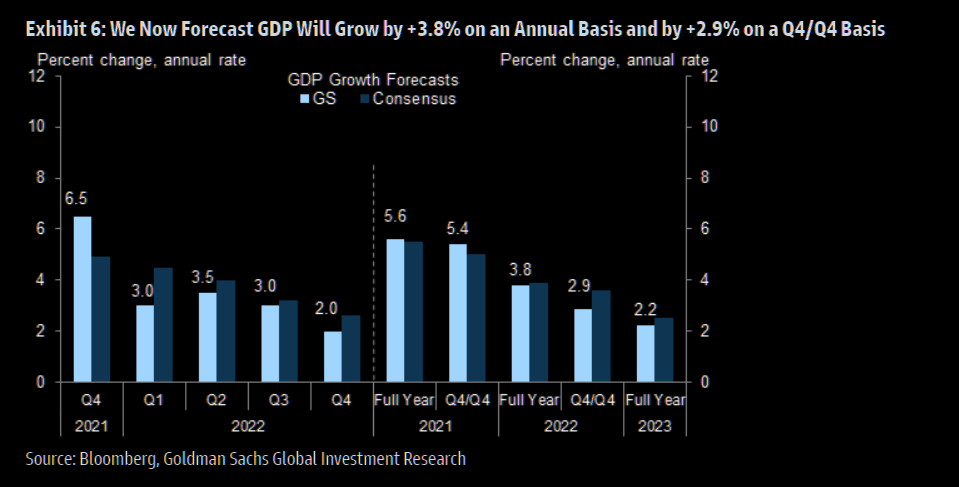

That didn’t stop the economists at Goldman Sachs Group Inc (NYSE: GS) from cutting their forecasts for U.S. GDP next year; the estimates were revised down on an expectation the omicron strain would drag growth.

Ahead are no important releases on fundamental data.

Graphic updated 6:30 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

On weak intraday breadth and divergent market liquidity metrics, the worst outcome occurred; there was an expansion of range, to the downside, and participants spent the majority of the session building value at lower prices (i.e., levels at which 70% of that day’s volume occurred).

The lower bound of Friday’s range was $4,500.00 or so, at which the 50-day SMA corresponded with a large base of resting liquidity.

To note, the 50-day is visual level at which short-term, technically-driven participants were likely buying in response to probes below developing balance.

Successfully auctioning beneath the 50-day is a concern. Those short-term participants lack the wherewithal (both emotional and financial) to defend retests.

Continuation lower, in such a case, is likely.

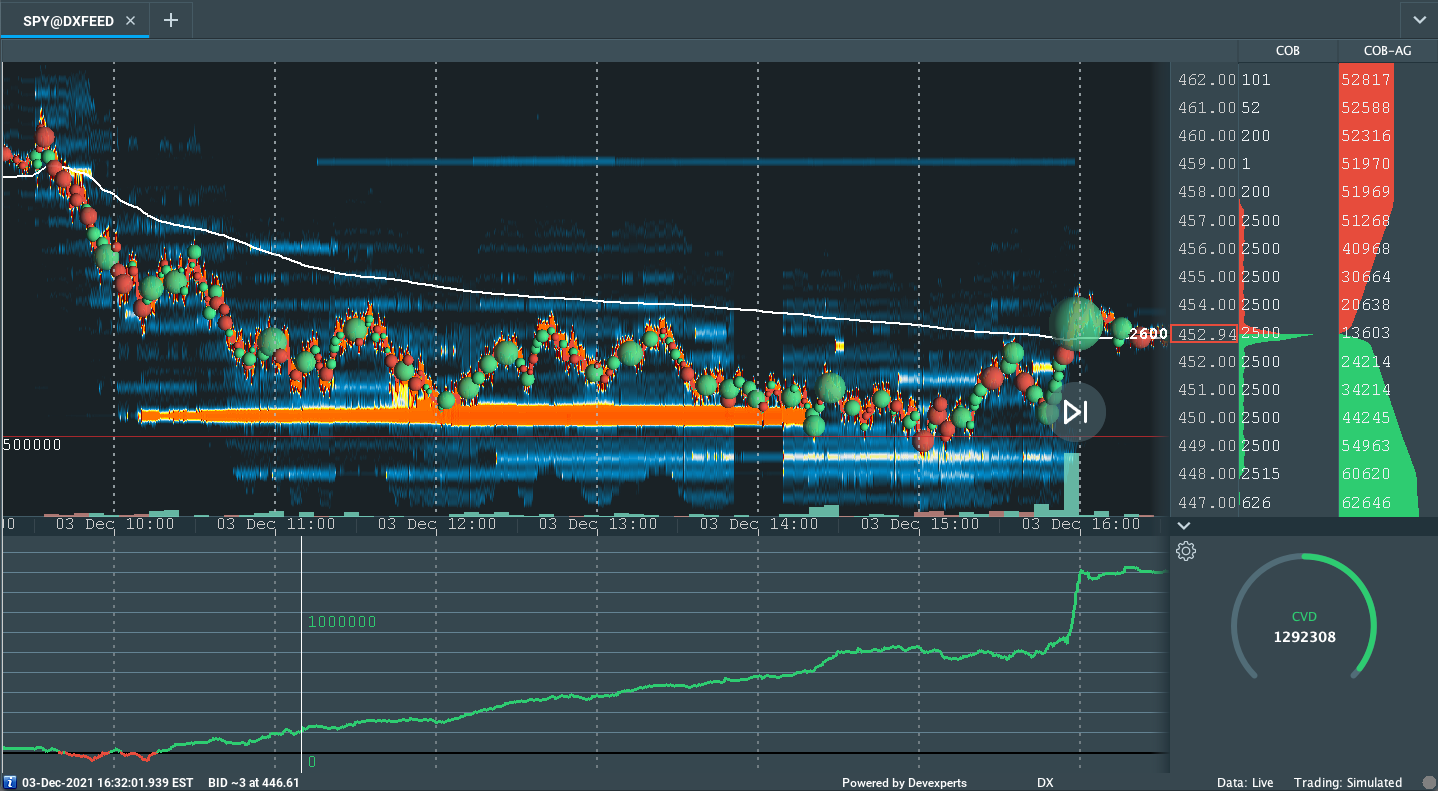

Graphic: Divergent delta (i.e., non-committed selling as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, via Bookmap. The readings are supportive of responsive trade (i.e., rotational trade that suggests current prices offer favorable entry and exit; the market is in balance).

Context: The Fed’s intent to moderate stimulus and uncertainty with regards to how a new COVID-19 variant will impact the global recovery.

According to Bloomberg, “the Fed is seen responding to the inflation fears stalking businesses by leaning toward an older playbook of prioritizing the fight against price pressures — even if that risks weaker growth over the longer term.”

In line with the aforementioned, traders already started pricing in potential rate overshoots with the “December 2024 eurodollar yields [rising] above December 2025 contracts, a curve inversion that signals expectations the central bank may consider cutting rates in 2025.”

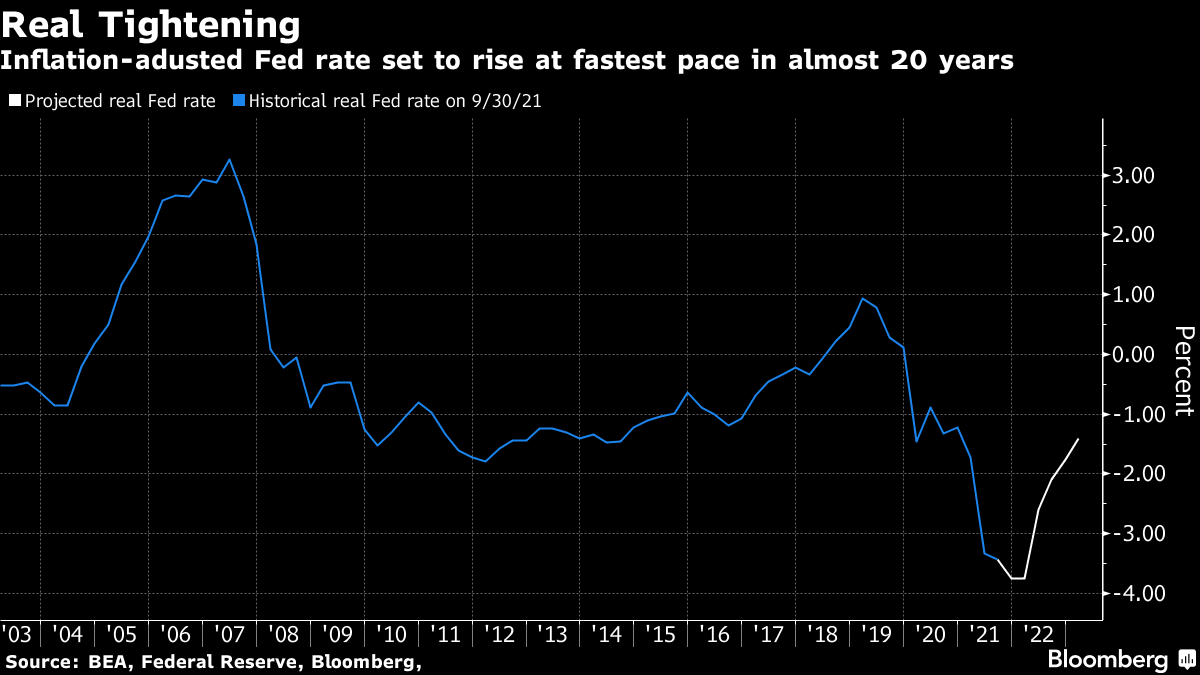

The result is that the U.S. may realize the swiftest tightening in financial conditions since 2005 if the Fed was to hike rates three times next year.

Graphic: Via Bloomberg, trades price in a rapid increase in the real Fed rate.

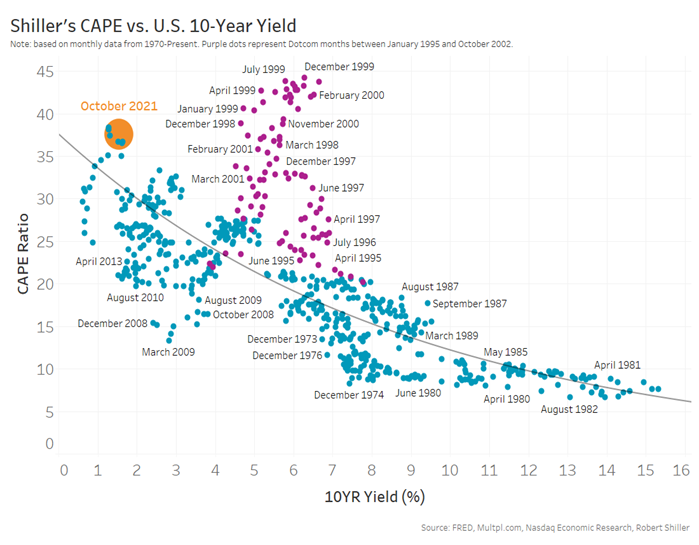

This development carries weight; now, more than during the tech-and-telecom bubble, low rates support current valuations.

Graphic: Low rates support current valuations better than the ‘90s, according to Nasdaq.

The reason being?

“Lower interest rates lead to future cashflow discounting less – leading to higher valuations. From another perspective, a company with a 5% profit margin is a much more attractive investment when long-term borrow costs are less than 2%, as they are now than when it costs 5%-7% to borrow money back in the ‘90s.”

The Fed’s intent to taper faster, and eventually hike rates, just as liquidity conditions have deteriorated, pushed “the orange dot [in the above graphic] toward the right during the year.”

Notwithstanding, “growth in earnings is so far stronger than the multiple compression caused by rising rates (blue line),” and that is helping support this year’s rally.

The intent to moderate stimulus is likely to serve as a headwind; there’s always a possibility of unanticipated policy adjustments, in the face of a resurgent COVID-19 digging further into the economy’s growth.

That’s partially why we saw Goldman Sachs cut their forecasts for GDP.

Graphic: Via The Market Ear. Goldman Sachs cut its forecast for GDP.

But, for every negative view, there is a positive (either by the same institution or a competitor).

We see JPMorgan Chase & Co (NYSE: JPM), among others, doubling down on their bullishness.

“We are calling for another year of positive earnings surprises, relative to current consensus estimates.”

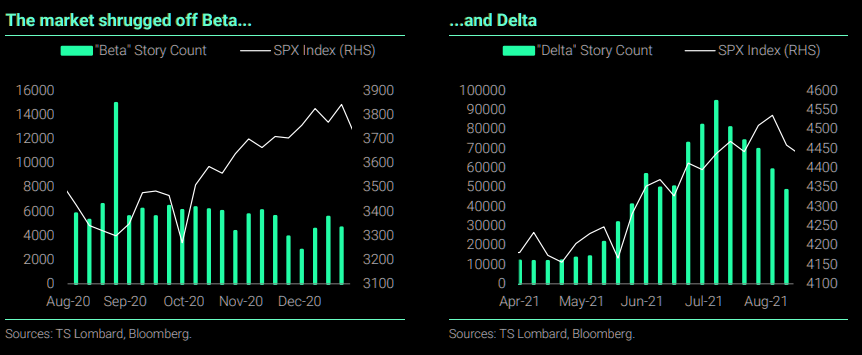

Similarly, the market may shrug off omicron just as it did beta and delta.

Graphic: Via The Market Ear, the market shrugs off COVID-19 variants with ease.

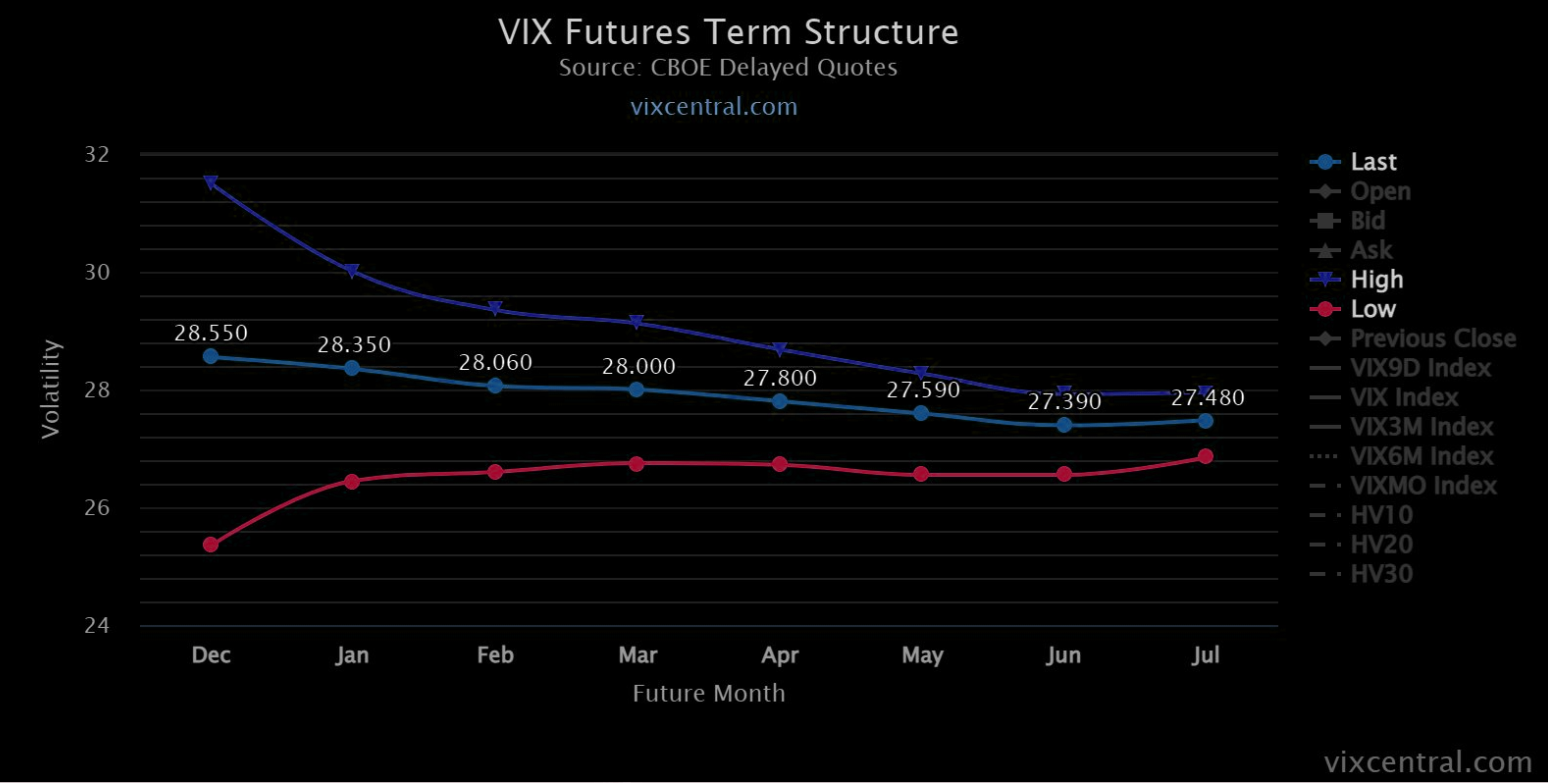

And, despite the market’s trade in short-gamma (a “negative [gamma] implies the opposite [selling into lows, buying into highs], thus magnifying market volatility”) destabilizing demand for downside protection is concentrated in shorter-dated options.

Graphic: A roll lower in the VIX term structure brings in supportive flows. Via The Market Ear.

Once that short-dated protection rolls off the table (and/or is monetized), counterparties will quickly reverse and support the market, buying to close their existing stock/futures hedges.

This flow is stabilizing and may play into a seasonally-aligned rally into Christmas as participants see defenses rolled out against the new COVID-19 variant, and the positive effects of pro-cyclical inflation, economic growth, and improvements in global trade.

Such development plays into a thesis held by Moody’s Corporation (NYSE: MCO).

“The forecast is that the Dow Jones Industrial Average increases this quarter and peaks in early 2022. However, the rest of the contours of the forecast didn’t change. We expect the DJIA to steadily decline throughout 2022, but because it will now peak later than previously thought, the level of the DJIA will be higher at the end of next year and over the near-term forecast.”

Similarly, here are some views by Morgan Stanley (NYSE: MS), compiled by The Market Ear.

“The Morgan Stanley’s Global Risk Demand Index (GRDI) [fell] to a 10Y low reading of -4.2SD, last Friday (currently -3.SD). Historically, such a level has proved to be a solid buy signal over the next 3m. Other signs that investor sentiment has overshot to the downside include the VIX > 30, a steep put-call skew, and the AAII survey where 42% of respondents are bearish (90th percentile reading). Over the last decade, MSCI ACWI has risen 98% of the time over the next 3m post this signal and by an average of 10%.”

Expectations: As of 6:30 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Balance-Break Scenarios: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) may occur.

Monitor for acceptance (i.e., more than 1-hour of trade) outside of the developing balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,523.00 untested point of control (VPOC) puts in play the $4,551.75 low volume area (LVNode). Initiative trade beyond the LVNode could reach as high as the $4,574.25 high volume area (HVNode) and $4,590.00 balance area high (BAH), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,523.00 VPOC puts in play the $4,492.25 regular trade low (RTH Low). Initiative trade beyond the RTH Low could reach as low as the $4,471.00 and $4,425.00 VPOC, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

What People Are Saying

The "Gamma Trap"

Dec SPX has 3.3mm puts which is the largest of any expiration. The chunkiest of these puts are likely held by funds which will hold to 12/17 expiration. The 4000 strike has the most put interest.

If the market goes under 4500, the gamma trap could set: (1/n)

The 10 day moving average of the combined put-call ratio has been a long time solid guide to human behavior in the markets. When everyone is bullish (.50 ish) markets top and pull back. When everyone is bearish (.70 ish) markets bottom and rally. Ending the week at .75 pic.twitter.com/MDUhUncrMW

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Liquidation Breaks: The profile shape suggests participants were “too” long and had poor location.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

Overnight, equity index futures auctioned sideways to lower. The Russell 2000 led the decline while the Nasdaq 100 buoyed the S&P 500 as yields were a touch lower.

Though volatility is bid, related metrics suggest the removal of fear and added market stability.

In short, conditions aren’t as bad as they were, Friday.

Ahead is data on the S&P Case-Shiller Home Price Index (9:00 AM ET), Chicago PMI (9:45 AM ET), Consumer Confidence (10:00 AM ET). Scheduled also is testimony by Federal Reserve and Treasury members (10:00 AM and 1:00 PM ET).

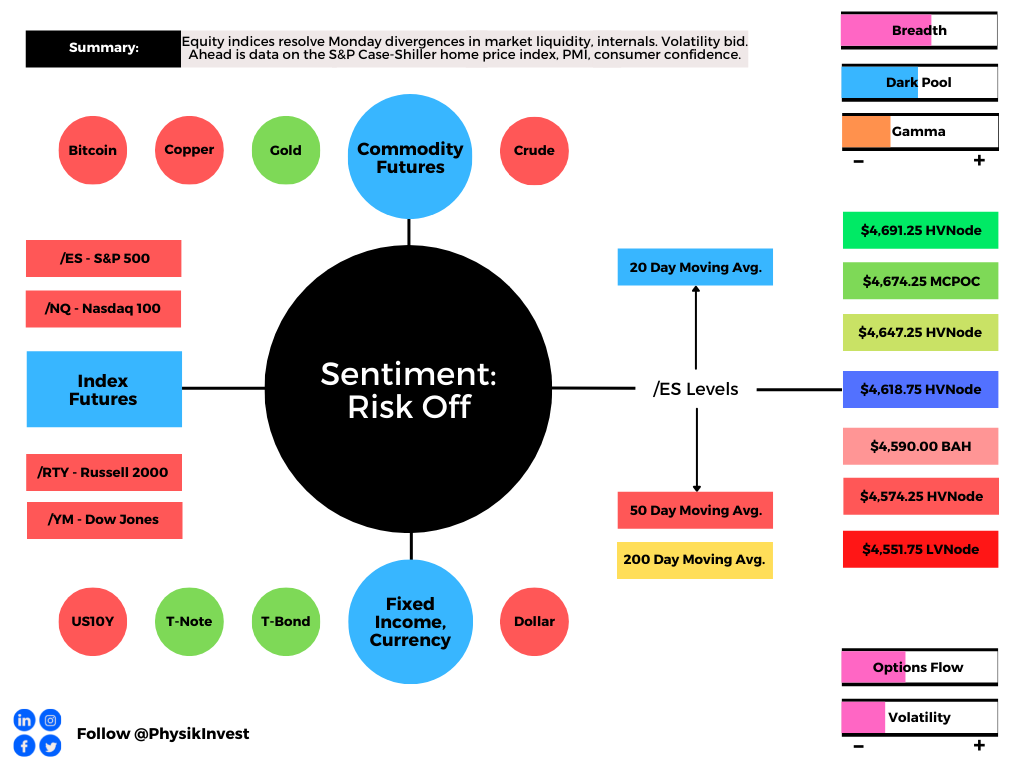

Graphic updated 6:30 AM ET. Sentiment Risk-Off if expected /ES open is below the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

On lackluster intraday breadth and divergent market liquidity metrics, the best case outcome occurred, yesterday, evidenced by a decisive move away from intraday value (i.e., the price levels at which 70% of the day’s volume occurred), into an area of resting liquidity that coincided with a volume-weighted average price (VWAP), anchored from the start of the decline.

To note, VWAPs are metrics highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

Moreover, given the divergences (one is pictured below), we can surmise that Monday’s recovery was responsively sold.

Given the push and pull between the big indices, as well as lackluster breadth and market liquidity metrics, there is increased potential for sideways trade; participants are likely to base for a directional move in anticipation of new information in regards to dynamics like COVID-19, monetary policy evolution, and the like.

Graphic: Divergent delta (i.e., non-committed buying as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, via Bookmap. The readings are supportive of responsive trade (i.e., rotational trade that suggests current prices offer favorable entry and exit; the market is attempting to bracket/balance).

Context: Keeping it to the point, today.

There is less fear coming into Tuesday’s session than there was Friday.

This dynamic is most clearly visualized with the VIX futures term structure which is much less flat, so to speak, than it was.

Graphic: VIX term structure.

Though one could surmise that there is less risk of instability, as a result, rather, we should think about it as the demand for protection through time. The demand has cooled.

In building on that, we saw the market enter into a destabilizing environment characterized by counterparties to options trades selling into weakness and buying into strength.

After a brief exit from that environment, Monday, an overnight liquidation has us on the cusp of re-entry. With options activity most concentrated in shorter-dated tenors where the sensitivity of options to direction is higher, if we will, then the expectation is that we realize more volatility.

That’s not to say that the market must trade lower. No. Instead, sideways trade as investors seek more information (in regards to COVID-19, monetary policy moderation, and the like) to base a directional move is just as likely.

In that case, the short-dated, out-of-the-money protection that was demanded will quickly evaporate; associated hedging flows (i.e., the buy-back of short stock/futures hedges) ought to support the market.

Should participants’ fears be assuaged, the aforementioned flows could play into a seasonally-aligned rally into Christmas.

For that thesis to not play out, there would have to be increased participation below $4,600.00 in the S&P 500 (i.e., value, internals, market liquidity must support downside price discovery).

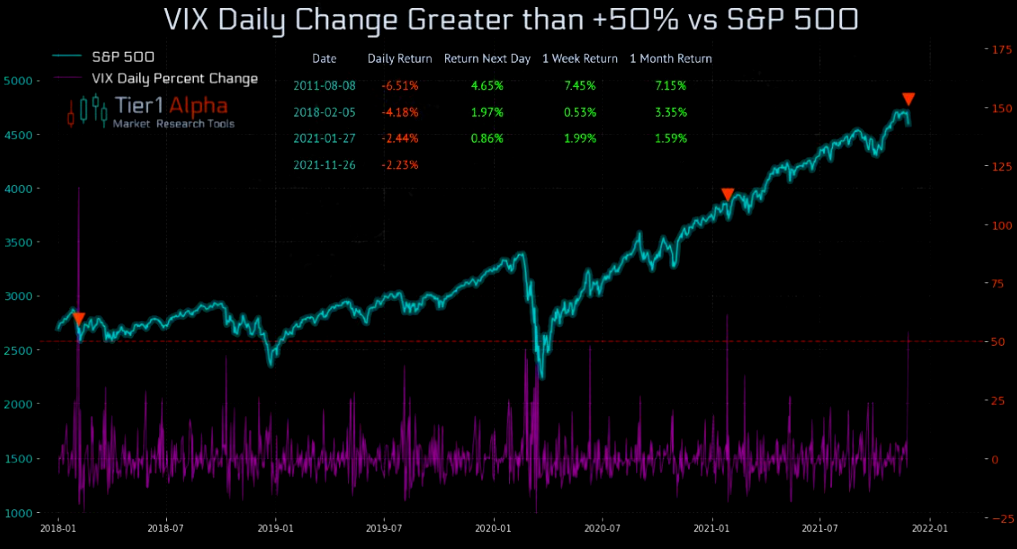

Graphic: Daily changes in the CBOE Volatility Index (INDEX: VIX) greater than 50% precede positive S&P 500 performance.

Expectations: As of 6:30 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator.

Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,618.75 high volume area (HVNode) puts in play the $4,647.25 HVNode. Initiative trade beyond the latter HVNode could reach as high as the $4,674.25 micro composite point of control (MCPOC) and $4,691.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,618.75 HVNode puts in play the $4,590.00 balance boundary (BAH). Initiative trade beyond the BAH could reach as low as the $4,574.25 HVNode and $4,551.75 LVNode, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

Charts To Watch

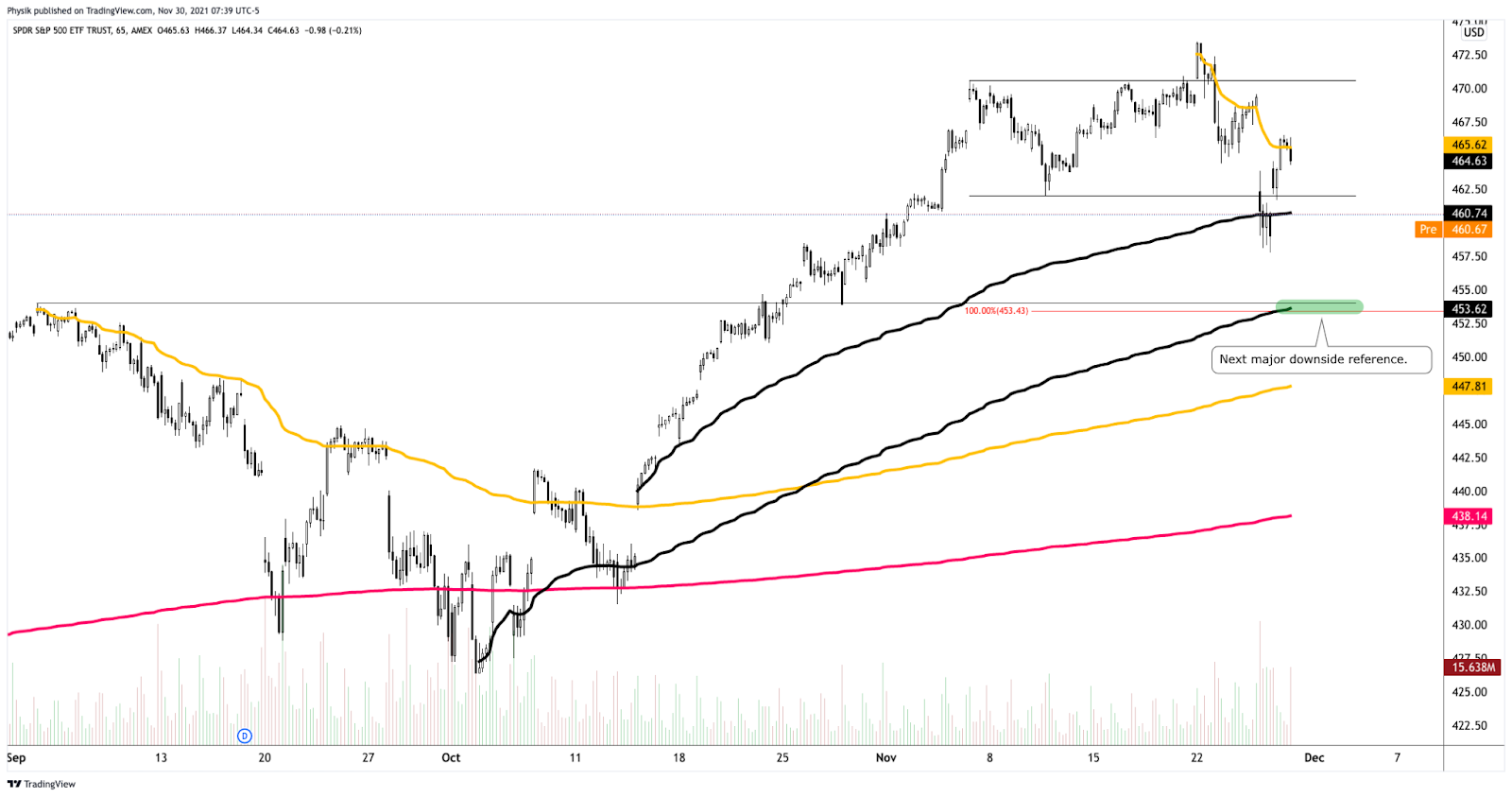

Graphic: (NYSE: SPY). (S~$453, R~$465). S is for support. R is for resistance.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Responsive Buying (Selling): Buying (selling) in response to prices below (above) an area of recent price acceptance.

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance-areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

Modus operandi is responsive trade (i.e., fade the edges), rather than initiative trade (i.e., play the break).

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

Rates: Low rates have to potential to increase the present value of future earnings making stocks, especially those that are high growth, more attractive. To note, inflation and rates move inversely to each other. Low rates stimulate demand for loans (i.e., borrowing money is more attractive).

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

Overnight, equity index futures auctioned sideways to higher as participants looked to take back nearly all of Friday’s shortened holiday trading range.

According to some metrics, the SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, experienced one of its most illiquid days, Friday.

At the same time, the CBOE Volatility Index (INDEX: VIX) closed up nearly 50% while the VIX futures term structure settled in backwardation amidst a re-pricing of tail-risk, so to speak.

Moreover, ahead is data on Pending Home Sales (10:00 AM ET).

Graphic updated 5:50 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

Despite the lackluster intraday breadth and divergent market liquidity metrics, the worst-case outcome occurred, Friday, evidenced by downside expansion of range and separation of value.

Coming into the session, the experiences associated with ‘Volmageddon’ came to mind; the VIX was up nearly 40.00%, a concern given the exuberance of past weeks and options positioning, as well as a decline in correlations, and unsupportive breadth.

Tempering the fall were divergences; the Russell 2000 was down nearly 4.00% before Friday’s U.S. open while the S&P 500 was off about 2.00% or so, buoyed by the Nasdaq 100 which was only down about 1.00% amidst an 8% dip in the ten-year yield.

The divergence persisted with the S&P 500 closing firmly below its 20-day simple moving average, a visual level often acted on by short-term, technically-driven participants who generally are unable to defend retests.

Graphic: Divergent delta (i.e., non-committed selling as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index.

Context: A resurgence in the COVID-19 coronavirus as an improvement in macroeconomic conditions prompts a hawkish shift from the Federal Reserve (Fed).

“Many risky asset tailwinds in 2021 are turning into at least mild headwinds in 2022,” Nordea says. “Economic growth should decelerate, liquidity conditions are deteriorating, profit margins should be under pressure from rising costs and question marks regarding the Fed/ECB put will arise due to elevated inflation indicators. To us, this spells higher volatility.”

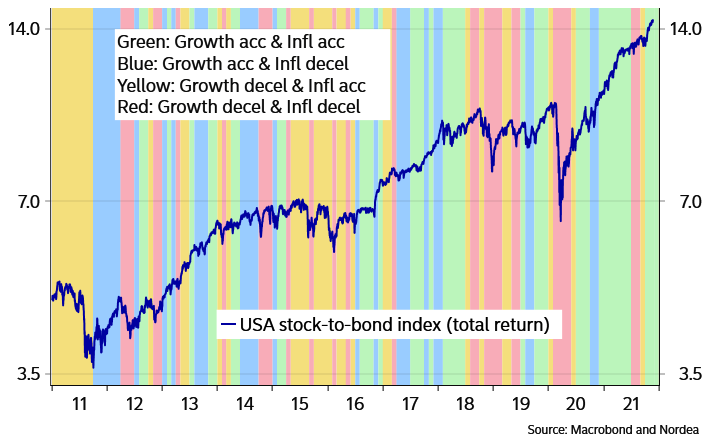

Moreover, for the past two years, almost, equities rallied amidst an acceleration in growth, which is typically correlated with equity outperformance over bonds.

Graphic: Accelerating growth correlates with equity outperformance over bonds.

At the same time, there’s been an insatiable appetite for stocks, according to Bloomberg, with investors pouring “almost $900 billion into equity exchange-traded and long-only funds in 2021 — exceeding the combined total from the past 19 years.”

This appetite for risk fed into the activity of some high-flyers like Tesla Inc (NASDAQ: TSLA) with customers, at least in the past weeks, opting to aggressively sell puts and buy calls heading into the November monthly options expiration (OPEX).

Graphic: Per The Market Ear, participants were hating on downside protection for weeks.

Unfortunately, (1) after OPEX, the absence of sticky and supportive hedging flows freed the broader market for directional resolve, and (2) according to SpotGamma, in light of recent exuberance, “participants [were] underexposed to downside put protection.”

Graphic: Customers took on significant leverage in their purchase and sale of options, via SpotGamma.

What this meant was that after OPEX’s unpinning and increase in correlation, fundamental contexts were to matter more.

Therefore, the Fed’s “increased openness to accelerat[e] the taper pace” and hike rates, alongside fresh travel restrictions on a new COVID-19 variant, as well as holiday illiquidity, resulted in a rough re-pricing of tail risk as participants sought after those highly “convex” options which had counterparties exacerbating underlying price movement.

Graphic: According to Bloomberg, markets price “a full quarter-point rate hike into the June Fed meeting with a second by September and a third by December.”

To elaborate, in short, was volatility to pick up, those participants (who were once exuberant) were likely to reach for protection forcing dealers to reflexively hedge in a destabilizing manner.

Dealers is the term used to describe those participants that take the other side and warehouse customer options risk, at least in the case where orders can’t be matched between customers.

With that, as volatility rose and customers demanded protection, counterparties hedged by selling into weakness. The conditions worsened when much of the activity was concentrated in shorter-dated tenors where the sensitivity of options to direction is higher if we will.

Graphic: VIX term structure. Backwardation signals an entry into an unstable environment.

Once that short-dated protection rolls off the table (and/or is monetized), dealers will reverse and support the market, buying to close their existing stock/futures hedges.

This flow is stabilizing and may play into a seasonally-aligned rally into Christmas as participants see defenses rolled out against the new COVID-19 variant, and the positive effects of pro-cyclical inflation and economic growth, improvements in global trade, and continuity at the Fed, among other dynamics, play out.

We see participants opportunistically buying the dip, already, via metrics like DIX that’s derived from liquidity provision on the market-making side.

Expectations: As of 6:00 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,618.75 high volume area (HVNode) puts in play the $4,647.25 HVNode. Initiative trade beyond the latter HVNode could reach as high as the $4,674.25 micro composite point of control (MCPOC) and $4,691.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,618.75 HVNode puts in play the $4,590.00 balance boundary (BAH). Initiative trade beyond the BAH could reach as low as the $4,574.25 HVNode and $4,551.75 LVNode, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

Charts To Watch

Graphic: (NYSE: SPY). (S~$460 and $453). S is for support.Graphic: (NASDAQ: QQQ). (S~$389 and $381). S is for support.Graphic: (NYSE: IWM). (S~$222 and $216). S is for support.

What People Are Saying

On Friday the SPY had a fire lit underneath it, it was the most illiquid day in a very long time. 332 of the 504 the S&P500 components printed 200 day Illiquidity Ranks above 90%. So what does it mean. pic.twitter.com/KB94QiIPGB

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure.

Rates: Low rates have to potential to increase the present value of future earnings making stocks, especially those that are high growth, more attractive. To note, inflation and rates move inversely to each other. Low rates stimulate demand for loans (i.e., borrowing money is more attractive).

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

Overnight, equity index futures auctioned within the confines of Tuesday’s range, unable to follow through on attempts higher or lower. This comes as there was a clear validation of Monday’s knee-jerk selling.

This sideways-to-lower price action in the index products is happening alongside a sell-off in new issues and richly priced technology stocks. Part of the weakness may have something to do with investors booking capital losses to lower their capital gains.

The other part of it, according to Bloomberg, is an exodus among professional investors who were counting on high-flyers to salvage their year.

“There was a desire to kind of keep up with the broader index. And there was definitely a view that those are higher-beta assets and that’s a way to try and play a little bit of catch-up,” Barclays Plc’s (NYSE: BCS) Todd Sandoz said. “When the market turns and it’s not working, you need to take risks down. And everybody’s in those names, so you also probably have a view to try to cut things faster.”

With indices pinned and heavily weighted constituents sideways to higher, there is only one form of reconciliation – a decline in correlation. Nonetheless, fundamentals are no different; investors may be able to buy quality stocks at a discount amidst the market’s entry into a seasonally bullish period.

Buybacks and increased retail engagement, resilient activity, and macro metrics, as well as excess liquidity, in the face of central bank cautiousness, suggest “dips should be bought,” according to Barclays.

Ahead is data on jobless claims, GDP, durable and core capital goods orders, and trade in goods (8:30 AM ET). Thereafter is data on personal and disposable income, consumer spending, core inflation, home sales, sentiment, and 5-year inflation expectations (10:00 AM ET). FOMC minutes come later (2:00 PM ET).

Graphic updated 6:00 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

On divergent intraday breadth and market liquidity metrics, the worst-case outcome occurred, evidenced by an acceptance of Monday’s knee-jerk, high-tempo selling.

Though this activity marks a potential willingness to start trending lower, the nature of Monday’s liquidation, as well as the failure to follow-through (i.e., expand the range to the downside) forces us to question whether participants have it in them to push indices lower.

In light of the activity we’re seeing, it’s tough to pick a direction and stick with it; the higher odds play, in light of the divergences we’re seeing in breadth metrics between exchanges, as well as market liquidity (below), is to responsively buy dips and sell rips.

Key levels to trade against are the high volume areas (HVNodes) at $4,691.25 and $4,647.25. The latter level corresponds with the 20-day simple moving average.

These levels are the clearest ways to measure risk, given the mechanical responses in prior trade. Should participants manage to break past either level, then conditions have changed. Follow-through is likely. Reason being? Those visual levels are acted on by short-term, technically-driven market participants who generally are unable to defend retests.

Graphic: Divergent delta (i.e., non-committed selling as measured by volume delta or buying and selling power as calculated by the difference in volume traded at the bid and offer) in SPDR S&P 500 ETF Trust (NYSE: SPY), one of the largest ETFs that track the S&P 500 index, via Bookmap. The readings are supportive of responsive trade (i.e., rotational trade that suggests current prices offer favorable entry and exit; the market is in balance).

Context: Keeping this section very short.

We saw the CBOE Volatility Index (INDEX: VIX) end higher, yesterday.

However, supply came in across the entire area of the VIX futures term structure. That, with the long-gamma environment (defined below), suggests participants are not reaching for hedges.

For the time being, that’s stabilizing, cognizant of the fact that exuberance in individual stocks, over the past weeks, fed into the stock indices themselves.

Further, the price action we’re seeing is likely the resolve of some of that weak breadth we were seeing, recently, in addition to some of the topics discussed at the beginning of this newsletter.

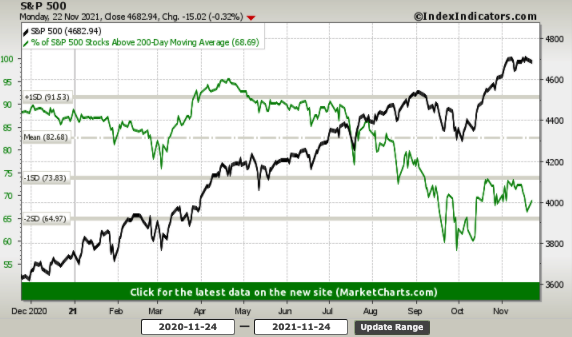

Graphic: Divergences in breadth. SPX versus % of SPX stocks above the 200-day average.

In short, however, should volatility continue to pick up, those participants (who were once exuberant) may reach for protection forcing dealers to reflexively hedge in a destabilizing manner.

Once that protection rolls off the table (expires and/or is monetized), dealers will reverse and support the market, buying-to-close existing stock/futures hedges to negative gamma positions.

This flow is stabilizing and may support a seasonally-aligned rally into Christmas.

400 is the key strike in $QQQ with put gamma (and high volatility) prevailing below, and call gamma above.

Not sure what happens next, but if you wanted to setup a Santa Claus rally pulling back the slingshot before firing works best. pic.twitter.com/lgmq1vxviC

Expectations: As of 6:00 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Spike Scenario In Play: A spike marks the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

The spike may also be looked at as a pivot; in today’s case, the spike base is $4,697.50.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,691.25 high volume area (HVNode) puts in play the $4,711.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,740.50 minimal excess high and $4,765.25 Fibonacci, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,691.25 HVNode puts in play the $4,674.25 micro composite point of control (MCPOC). Initiative trade beyond the MCPOC could reach as low as the $4,647.25 HVNode and $4,619.00 VPOC, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures. Learn about the profile.

Charts To Watch

What People Are Saying

S&P500, $SPY short-term (10-day) Sector Correlations are ultra low closing at .06. In 2021 this condition has preceded sell-offs. pic.twitter.com/KB1H7vITqR

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.