Investors foresaw weakness before the 2022 equity market decline in response to the coming monetary tightening. They repositioned and hedged their equity downside with allocations to commodities and options, colloquially referred to as volatility.

The commodity exposure worked well, while the volatility exposure did not. Consequently, the 2022 equity market decline was unlike many before. The monetization and counterparty hedging of existing customer options hedges and the sale of short-dated options, particularly in some single names where implied volatility or IVOL was rich, lent to lackluster volatility performance. Some may have observed tameness among IVOL measures such as the Cboe Volatility Index or VIX.

“One-year variance swaps or implied volatility on an at-the-money S&P 500 put option would trade somewhere in the neighborhood of 25 to 30%,” said Michael Green of Simplify Asset Management. “That implies a level of daily price movement that is difficult to achieve.”

Eventually, entering August 2022, entities were getting squeezed out of these trades that did not work. The market advanced as participants rotated out of options and commodities; a macro-type re-leveraging ensued on improvements in inflation data, an earnings season that was better than expected, and “crazy tax receipts,” among other things. In August 2022, the advance climaxed the week of monthly options expiry or OpEx, as shown below.

Why did the advance climax the week of OpEx? Well, heading into that particular week of OpEx, markets were rising quickly, and call options (i.e., bets on the market upside) were highly demanded.

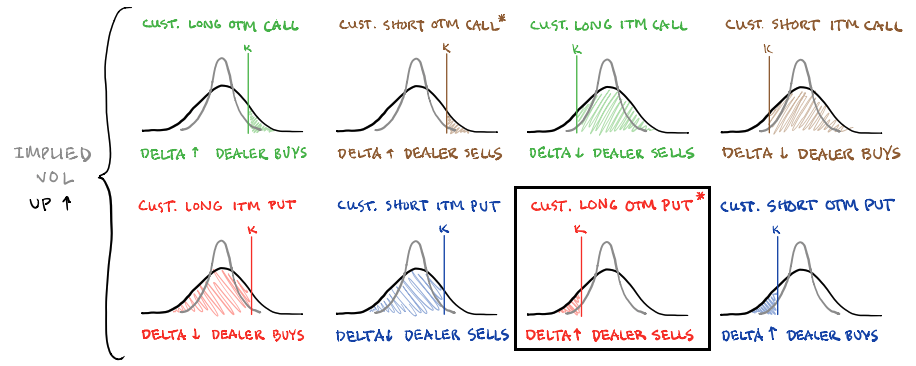

Those on the other side of the call option trades (i.e., counterparties) thus hedged in a supportive manner (i.e., counterparties sell calls to customers and buy underlying to hedge exposure).

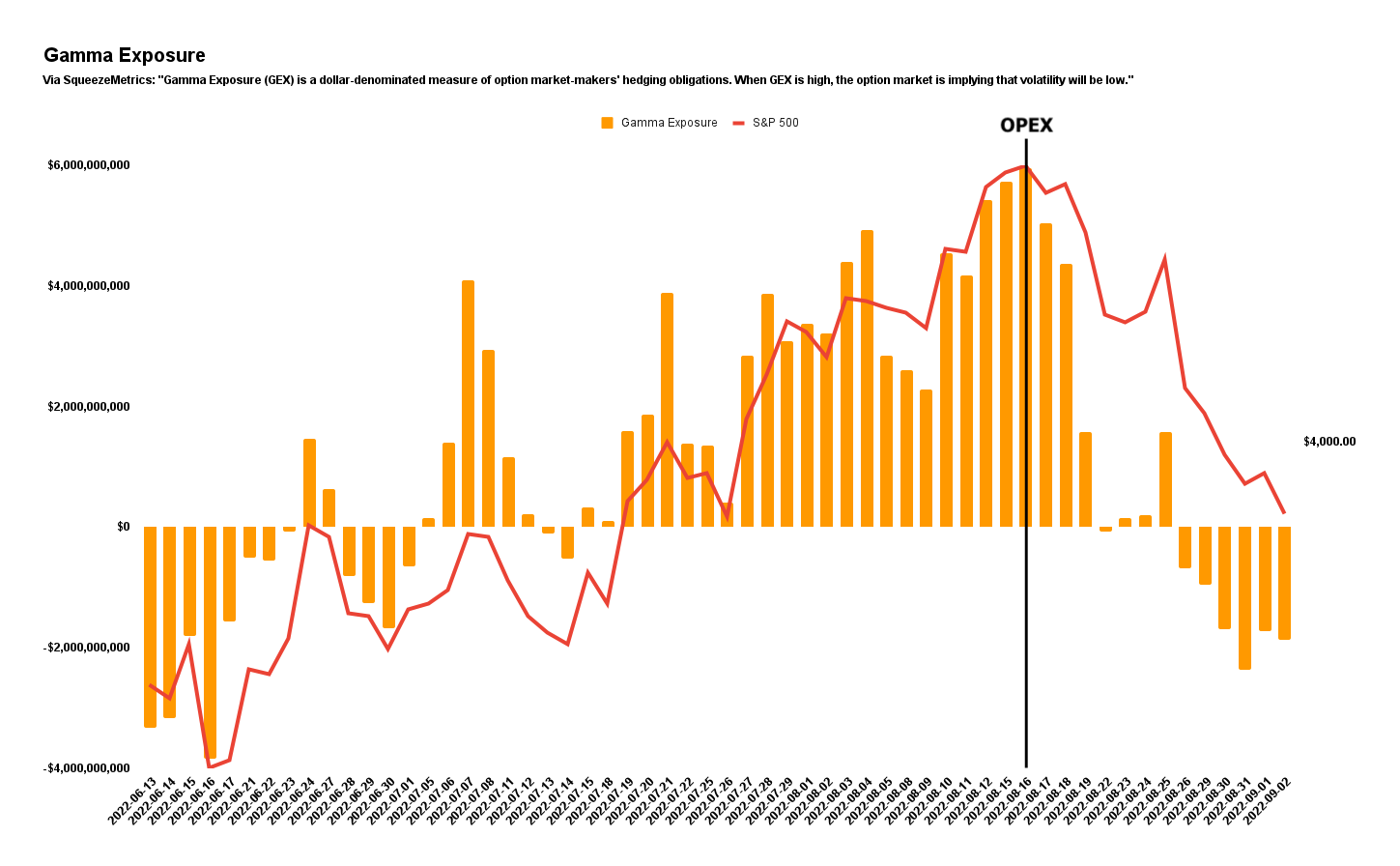

Eventually, traders’ activity in soon-to-expire options concentrated at specific strikes – particularly $4,300.00 in the S&P 500 – while IVOL trended lower. The counterparty’s response, then, did more to support prices and reduce movement. That is because, with time passing and volatility declining, options Gamma (i.e., the sensitivity of an option to direction) became more positive; the range of spot prices across which Delta (i.e., options exposure to direction) shifts rapidly shrunk. When options Gamma exposure is more positive, market movements may positively impact the counterparty’s position (i.e., movement benefits them). However, if the counterparty is not interested in realizing that benefit, it may hedge in a manner that dulls the market’s movement. This is partly what happened in the late stages of the August rally. After the S&P 500 hit $4,300.00, the near-vertical price rise sputtered. Soon, follow-on support, from a fundamental (e.g., liquidity) and volatility perspective, would worsen following OpEx.

Why the removal/weakening of support? OpEx would trigger “a big shift in market positioning,” Nomura Holdings Inc’s (NYSE: NMR) Charlie McElligott explained at the time.

In short, participants’ failure to roll forward their expiring bets on market upside coincided with a message that the Federal Reserve (Fed) would stay tough on inflation. After OpEx, those same bets prompting counterparties to stem volatility and bolster equity upside were removed (i.e., expire). We can visualize this by the drop in Gamma exposures post-OpEx, as shown below.

Accordingly, August OpEx, combined with technical and fundamental contexts prompting funds to “reload[] on short sales,” shocked the market into a higher volatility and negative Gamma environment. In this negative Gamma environment, put options, through which the vast majority of participants speculate on lower prices and protect their downside, solicited far more pressure from counterparties. If markets continued trading lower, traders would likely continue rotating into those put options, further bolstering pressure from counterparties. This happened, as shown below.

Demand for put options protection was bid IVOL. To hedge against this demand for protection and rising IVOL, counterparties sold underlying, compounding bearish fundamental flows.

In late August, new data suggested September would have “a very large options position as it is a quarterly OpEx,” SpotGamma said. With positioning “put heavy,” a slide lower, and an increase in IVOL was likely to drive continued counterparty “shorting” with little “relief until Jackson Hole.”

Based on this information, Physik Invest sought to initiate trades, expecting markets to trade lower and more volatile.

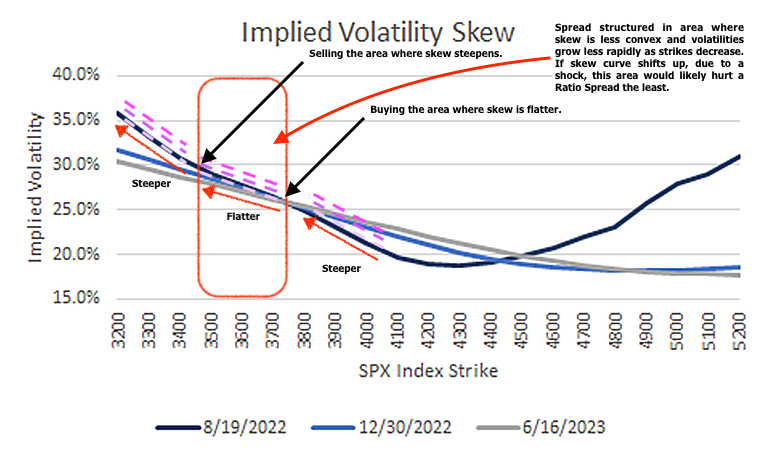

Call option premiums appeared attractive in mid-August, partly due to interest rates, while IVOL metrics seemingly hit a lower bound. This was observable via a quick check of skew, a plot of IVOL for options across different strike prices. Usually, skew, on the S&P 500, shows a smirk, not a smile. This meant it was likely that short-dated, wide Put Ratio Spreads had little to lose in a sideways-to-higher market environment. Additionally, call Vertical Spreads above the market were relatively more expensive.

Given the above context, the following analysis unpacks how Physik Invest traded options tied to the S&P 500 leading up to and through the August 19 OpEx into the Jackson Hole Economic Symposium.

Note: Click here to view all transactions for all accounts involved.

Sequence 1:

Through August 12, 2022, after a volatility skew smile was observed, the following positions were initiated while the S&P 500 was still trending higher for a net $7,616.68 credit.

Positions were structured in a way that would potentially net higher credits had the index moved lower.

- SOLD 10 1/2 BACKRATIO SPX 100 (Weeklys) 26 AUG 22 3700/3500 PUT @ ~$0.13 Credit

- SOLD 3 VERTICAL SPX 100 21 OCT 22 [AM] 4300/4350 CALL @ ~$25.10 Credit

Sequence 2:

While the S&P 500 was trading near $4,300.00 resistance, by 8/19/2022, all aforementioned Ratio Put Spread positions were rolled forward for a $452.26 credit.

The resulting position was as follows:

- -17 1/2 BACKRATIO SPX 100 (Weeklys) 16 SEP 22 3700/3500 PUT

- -3 VERTICAL SPX 100 21 OCT 22 [AM] 4300/4350 CALL

From thereon, the market declined, and by 9/1/2022, all positions were exited for a $6,963.84 credit.

- BOT 17 1/2 BACKRATIO SPX 100 (Weeklys) 16 SEP 22 3700/3500 PUT @ ~$4.94 Credit

- BOT 3 VERTICAL SPX 100 21 OCT 22 [AM] 4300/4350 CALL @ ~$4.57 Debit

Summary:

The trades netted a $15,032.78 profit after commissions and fees.

The max loss (absent some unforeseen events) sat at ~$6,790.00 if the S&P 500 closed above $4,350.00 in October. Because the Ratio Put Spreads were initiated at no cost, any loss would have resulted from the trade’s Vertical Spread component if the market went higher.

Overall, this trade netted more than a 200% return; its profit was more than two times the initial debit risk, making it a multi-bagger.

Reflection:

Heading into the trades, it was the case that IVOL performed poorly during much of the 2022 decline. This would likely remain the case on any subsequent drop; hence, the ultra-wide and short-dated Ratio Put Spread.

Despite the Ratio Put Spread exposing the position to negative Delta and positive Gamma (i.e., the trade makes money if the market moves lower, all else equal), if implied skew became more convex (i.e., implied volatilities grow more rapidly as strike prices decrease), the position could have been a giant loser. So, if the flatter part of the skew curve (where the position was structured) became more convex (i.e., rose), which is not something that was anticipated would happen, then the only recourse would have been to (1) close the position or (2) sell (i.e., add static negative Delta in) futures and correlated ETFs. In the second case, the trade would have allowed time to work (i.e., let Theta work) and become a potential winner.

Additionally, under Physik Invest’s risk protocol, more Short Put Ratio Spread units could have been initiated on the transition into Sequence 2. These units could have been held through Labor Day and monetized for up to an additional ~$4.00 credit per unit.

Though additional units of the Vertical Spreads could not have been added due to the strict limits to debit risks, there were still months left to that particular trade component. With lower prices expected, there was little reason the Verticals should have been removed fast.

In the future, should the context from a fundamental and volatility perspective remain the same, Physik Invest could potentially re-enter a similar position only on a rally.

6 replies on “Case Study: How A Bearish S&P 500 Trade Turned Into A Multibagger”

[…] and markets are in an environment characterized by two-way ranges that are larger. Yesterday, we unpacked one way traders could have played the entry into this […]

[…] traders to a recent case study (HERE) on how to play this market environment, as well as the impacts of implied volatility (IVOL) […]

[…] This made for some attractive trade opportunities seen here. […]

[…] may be far riskier to employ into the end of this year and the middle half of next year. For context, this was a trade to have on this […]

[…] go into more detail and discuss how to structure a new trade on this information, such as the one unpacked in a recent case study of […]

[…] here’s an in-depth Ratio Spread case study published a few months […]