The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 850+ that read this report daily, below!

Fundamental

Working on a detailed fundamental write-up this week. Report back, soon.

Positioning

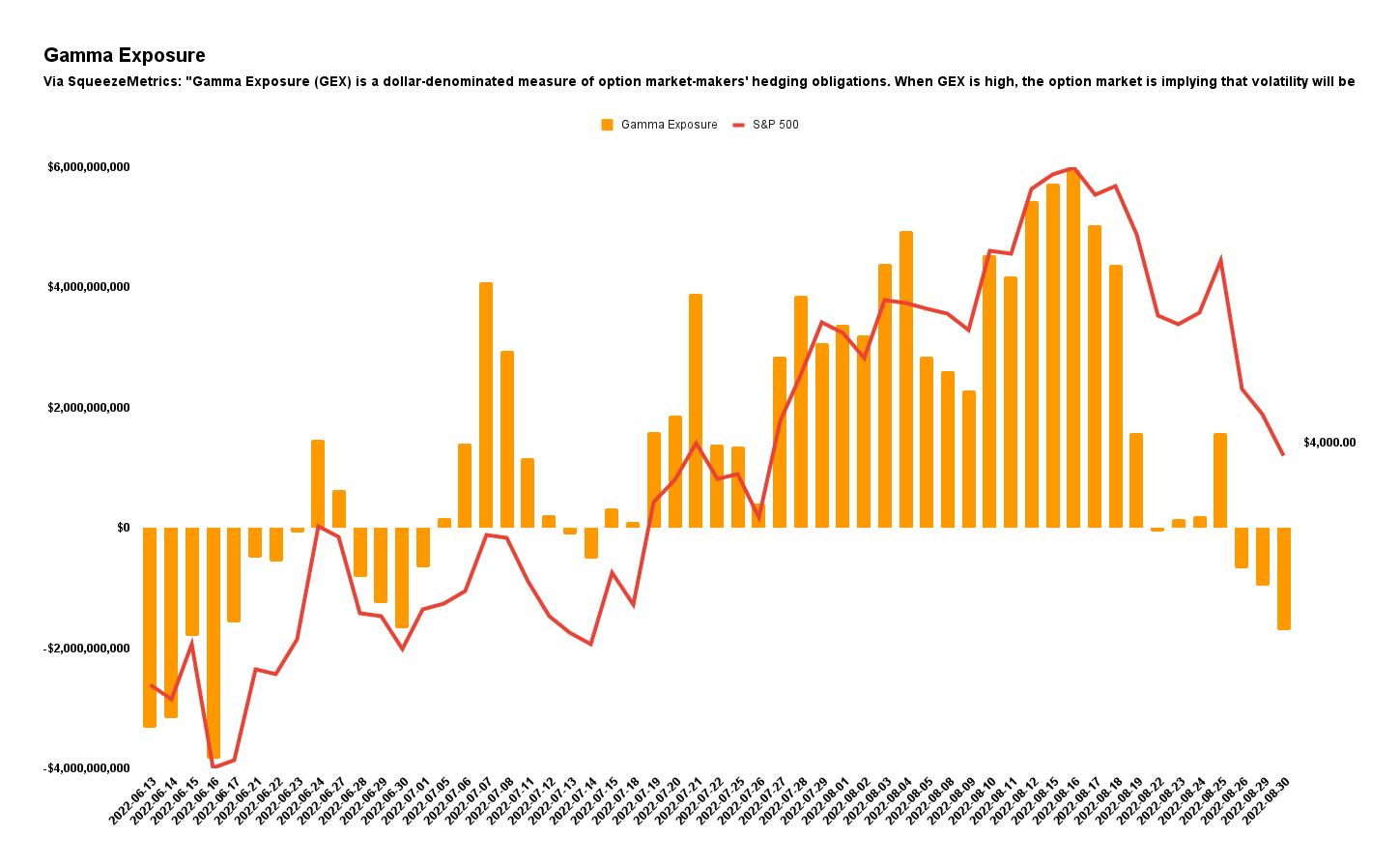

As of 6:30 AM ET, Wednesday’s expected volatility, via the Cboe Volatility Index (INDEX: VIX), sits at ~1.38%. After the August monthly options expiration (OPEX) date, gamma exposures have trended (and continue to trend) lower which does more to take from market stability.

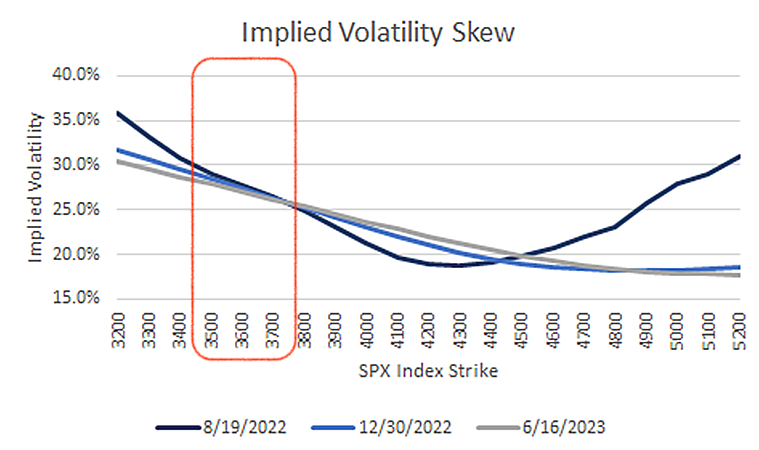

Previously, based on our reads of realized (RVOL) and implied (IVOL) volatility, as well as skew, it was beneficial to be structurer of complex options structures like the Short Ratio Put Spread, down at S&P 500 prices between $3,700.00 and $3,500.00, to play contexts we (think we) have a solid read on.

To quote the August 18 letter, “it is beneficial to be a buyer of options structures to protect against (potential) downside (e.g., S&P 500 [INDEX: SPX] +1 x -2 Short Ratio Put Spread | 200+ Points Wide | 15-30 DTE | @ $0.00 or better).”

Into the decline, those structures expanded and, now, the time has come to monetize. Though the decline (or increases in demand for options protection) may not be over, the trades are ripe for monetization (i.e., closing and converting a position to cash).

We buy (sell) when others are sellers (buyers), in short. Despite a bid in IVOL, personally, the concern is that the passage of time may do more to impact the trades negatively, all the while the trade’s exposure to changes in direction is very sensitive.

In other words, the trade has a lot to lose on a move higher while a lot of big and unrealistic things have to happen for the trade expand much further.

So now, it is beneficial to be a seller of those options structures to monetize downside (e.g., S&P 500 [INDEX: SPX] -1 x +2 Ratio Put Spread | 200+ Points Wide | 15-30 DTE).

Note: Trades Renato has personally taken will be unpacked in subsequent commentaries. Both the mistakes and successes, as well as what to do better.

Technical

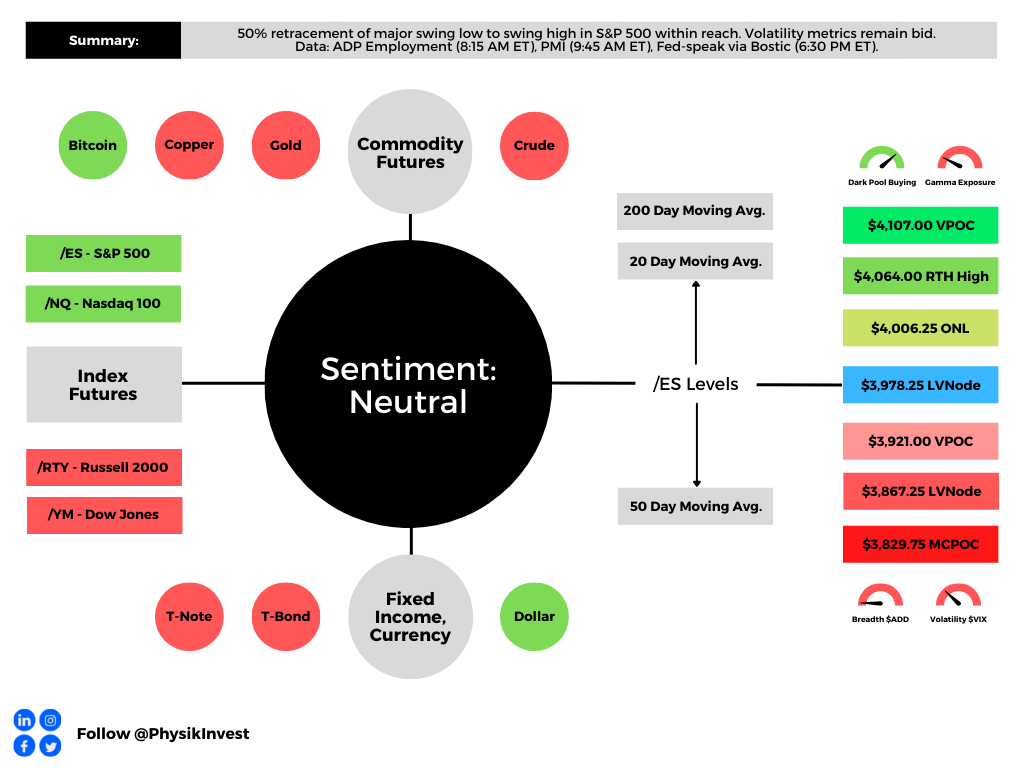

As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,978.25 LVNode puts into play the $4,006.25 ONL. Initiative trade beyond the ONL could reach as high as the $4,064.00 RTH High and $4,107.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,978.25 LVNode puts into play the $3,921.00 VPOC. Initiative trade beyond the $3,921.00 VPOC could reach as low as the $3,867.25 LVNode and $3,829.75 MCPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

2 replies on “Daily Brief For August 31, 2022”

[…] discussed thoroughly in our August 31 (HERE) and August 18 (HERE) letters, our analyses had us structuring spreads against the […]

[…] structured, as well as the reasons we had to take them off, which we dissected a bit on August 31 [HERE] and September 1 […]