The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 950+ that read this report daily, below!

Fundamental

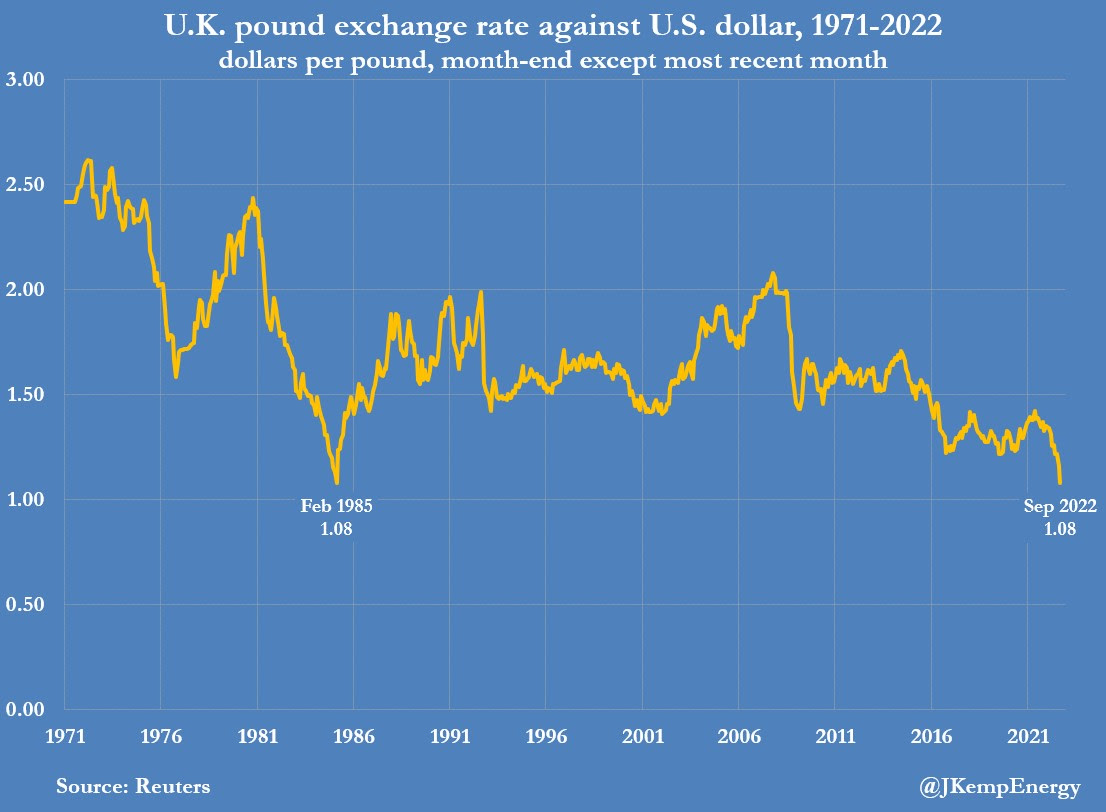

Overnight news was focused on the drop in Britain’s currency and a surge in bond yields. Per Bloomberg, the UK government’s talk about new fiscal plans and pledged tax cuts, alongside moderate interest rate hikes by the Bank of England (BoE), is the source of the weakness.

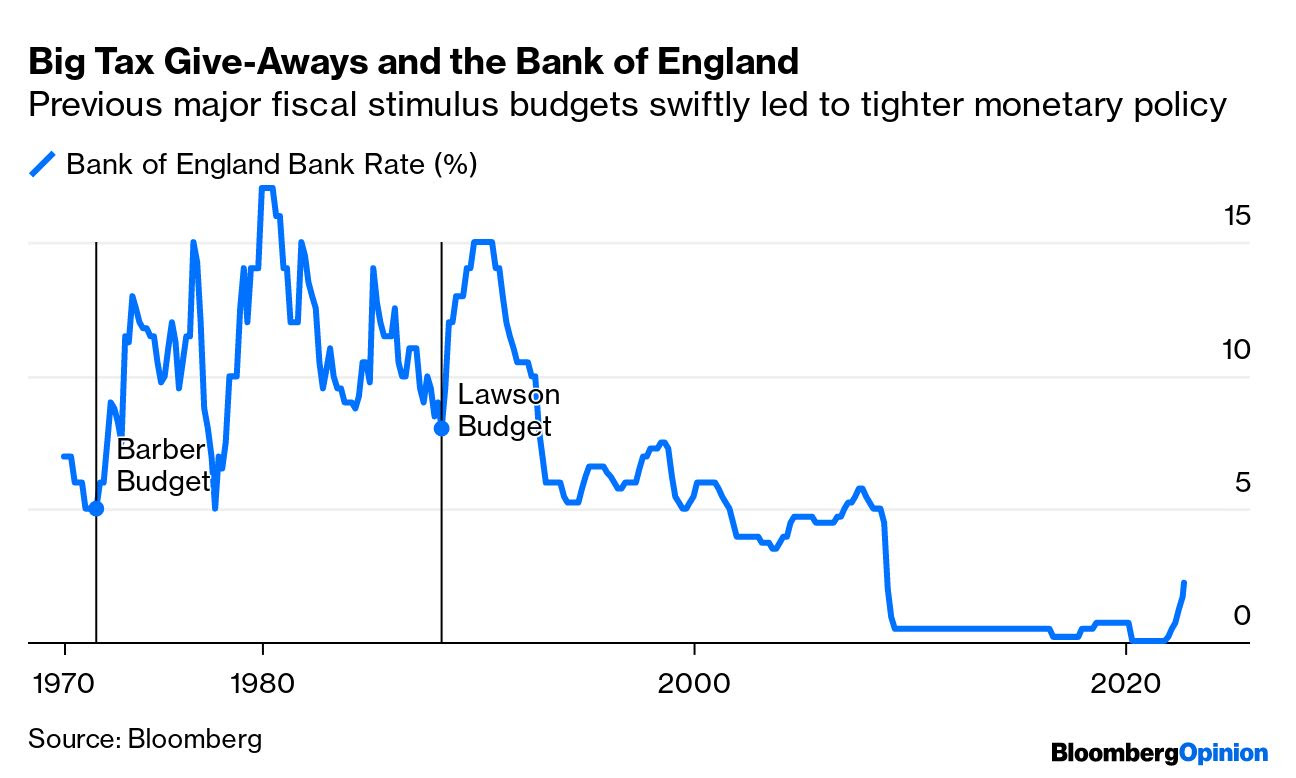

That’s because fiscal stimulus, which is part of a strategy to stoke “all-out” growth now, would add to the inflation already high and sticky from supply chokepoints and an easy-moving BoE.

“An emergency rate hike would be a damning indictment of the government’s strategy, but it will become increasingly likely if markets fail to stabilize,” said Bloomberg economist Dan Hanson.

Adding, traders are pricing increased odds of rate increases (~1.75%) by the BoE’s next policy meeting in November. Looking back, in the wake of previous tax giveaways, interest rates rose by a lot to stem the inflationary shock.

The weekend news, has us looking back to our letters on a “self-reinforcing ‘dollar doom loop,’” as Jon Turek of JST Advisors once put forth. It’s the case that the dominant currency for carry, due to easy monetary policies, was the dollar.

However, “the stronger the dollar gets in comparison, the less tenable it becomes as a global reserve,” and this puts pressure on the longer-term trajectory of the currency.

Knowing that US market liquidity, as well as the dollar’s strong role as a reserve, put the S&P 500 at the center of global carry regimes, an unwinding of carry may compound a market fall affecting nearly all risk assets.

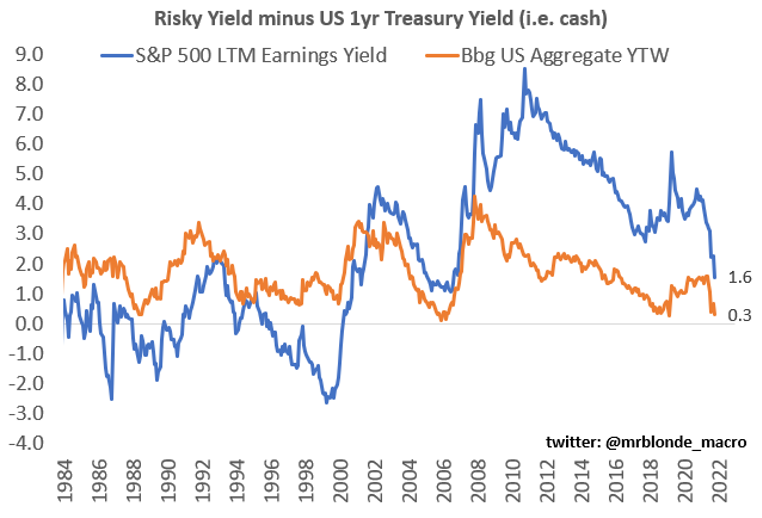

Accordingly, as put forth in Mr. Blonde’s letter, “[e]ven if you are optimistic about growth and the ability of [the] global economy to digest significant financial conditions tightening, you no longer need to be 100% invested in risky, less liquid, assets when you get a competitive return from risk-free cash.”

Positioning

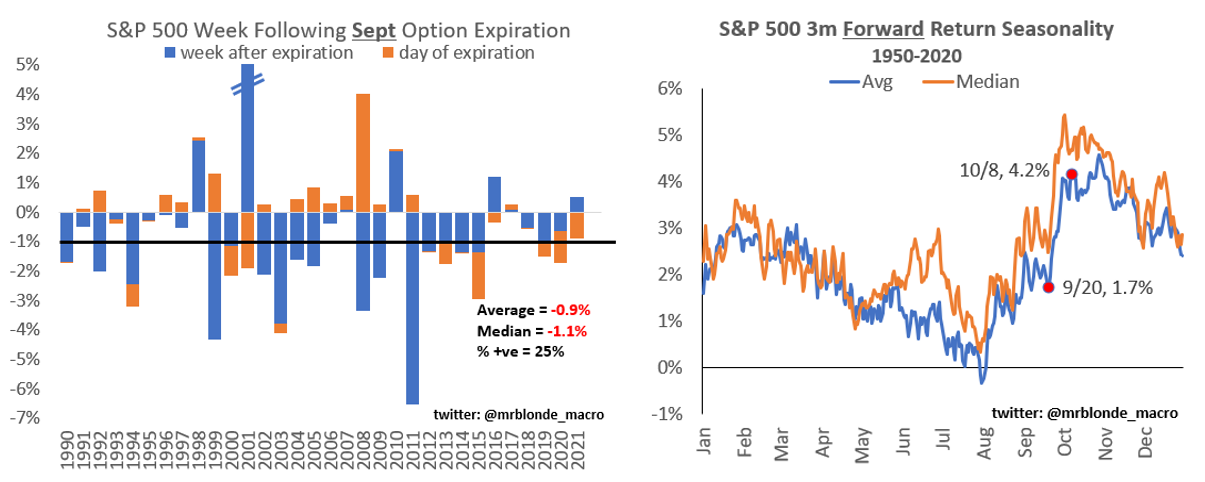

Following the September options expiration (OPEX), markets tend to have their worst week.

From thereon, the weak seasonality tends to persist for about a month, into mid-October. Given this, Kai Volatility’s Cem Karsan explained, “you need to keep selling the rallies, … [as the] war between the structural negative effects, macro flows, and positioning,” is likely to continue.

Dollar strength should feed into margin compression just now “filtering through” and impacting “international dollar-denominated debt.”

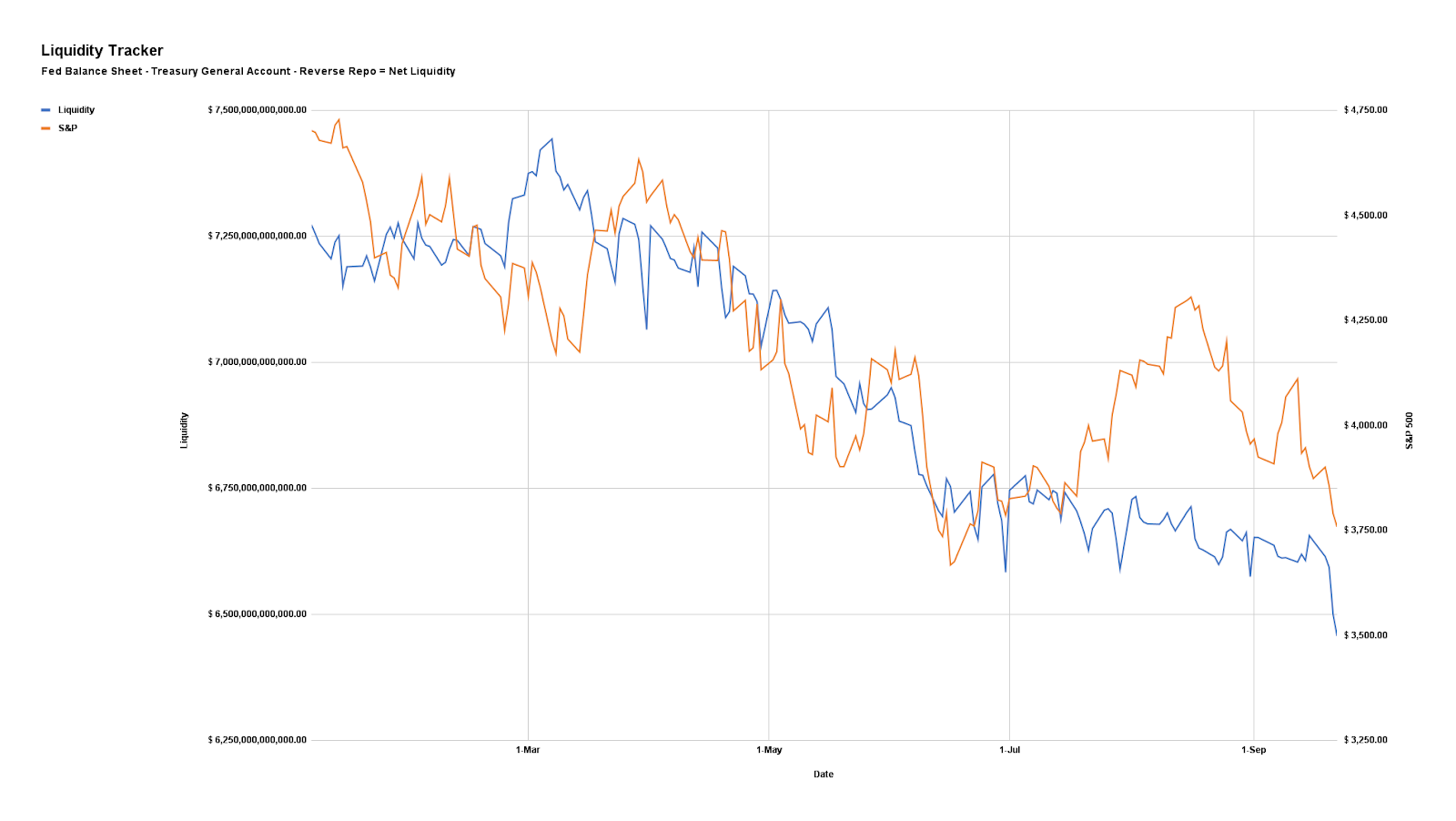

That compounds the impact of quantitative tightening (QT) which is manifesting itself as “$4.5 billion less in demand for assets per day,” as well as the blackout period for buybacks (which were consistently “supporting the market”) and options repositioning.

Read our monetary policy explainers published on September 19 and 20.

At the beginning of the 5-week expiration cycle, Karsan explained, Vanna and Charm flows are reduced; there is “significantly less buyback” of counterparty short stock and futures hedges to “the decay of options which sit at the October monthly expiration.”

So, “less support from Vanna and Charm, less support through QT, and less buyback,” presents a “fragile moment” with the next week representing the most “dangerous period” on record.

Ultimately, “December’s quarterly [OPEX] is now coming into the picture, … [where] volatility is generally highly demanded. When you get a lot of volatility supply in that area, you begin to see people who are short getting back the volatility they were short.”

In other words, equities down, implied volatility down is likely to persist for a little while longer as the risks for a “tail” build; “there’s a window that is opening for long volatility to perform probably starting in about a month or two,” through to “January and March.”

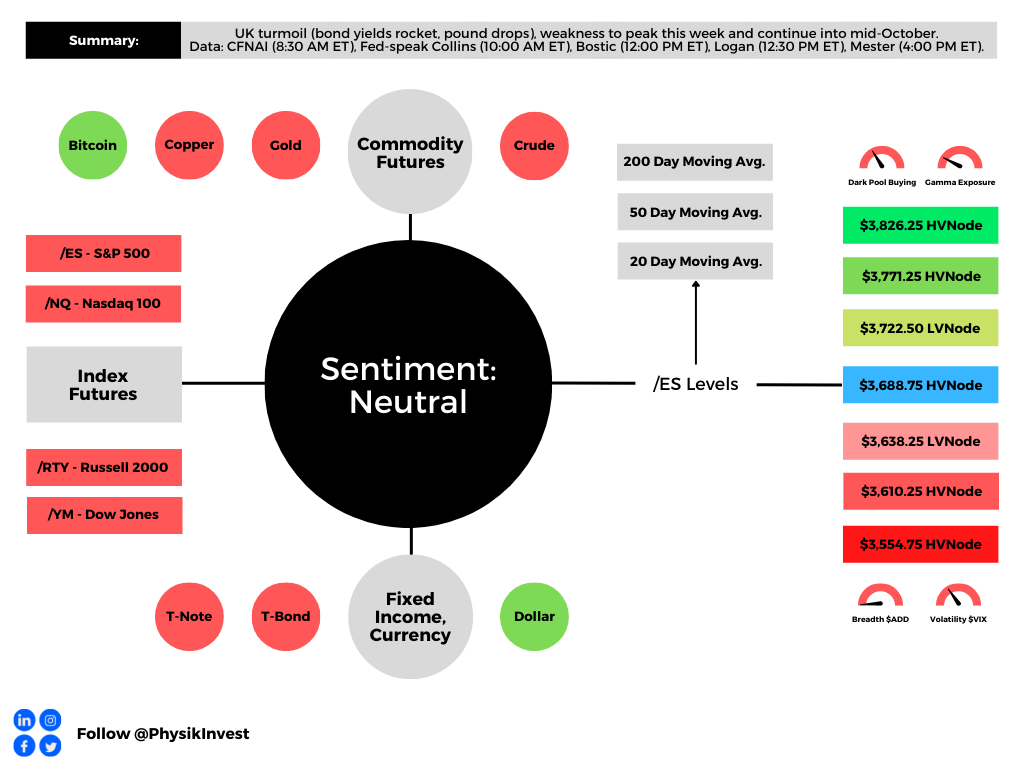

Technical

As of 8:30 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a negatively-skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,688.75 HVNode puts into play the $3,722.50 LVNode. Initiative trade beyond the LVNode could reach as high as the $3,771.25 and $3,826.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,688.75 HVNode puts into play the $3,638.25 LVNode. Initiative trade beyond the LVNode could reach as low as the $3,610.75 and $3,554.75 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

2 replies on “Daily Brief For September 26, 2022”

[…] tax cuts, alongside a more easy pace of interest rate hikes by the Bank of England (BoE). See the Daily Brief for September 26, 2022, for […]

[…] longer-dated government bonds in an attempt to restore stability, which we discussed was at risk on Monday and […]