Editor’s Note: Wow, what a month! Looks like there was a ton of volatility we weren’t able to navigate together.

I’m back now and will be making changes to both the quantity and quality of notes sent. In total transparency, I took on way too much work, and quality suffered a tad. I look forward to making things a bit more sustainable and am grateful for your interest in remaining a subscriber.

Interested in getting this free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below, today!

What Happened

Overnight, the equity index and most commodity futures explored lower. Bonds and implied volatility metrics were bid.

This is alongside news that China’s reaction to a local COVID-19 outbreak may feed into global slowdowns just as supply pressures, among other things, are pushing the Federal Reserve (Fed) to adopt a more hawkish policy stance.

Notable is the pace at which China’s yuan is falling.

Per TD Securities, it suggests “the PBOC is utilizing the yuan as another tool to provide stimulus to the economy at a time when they are showing restraint on the monetary policy front.”

Ahead, there are no important economic events scheduled. See who is reporting earnings, here.

What To Expect

Fundamental: A push-and-pull, continues.

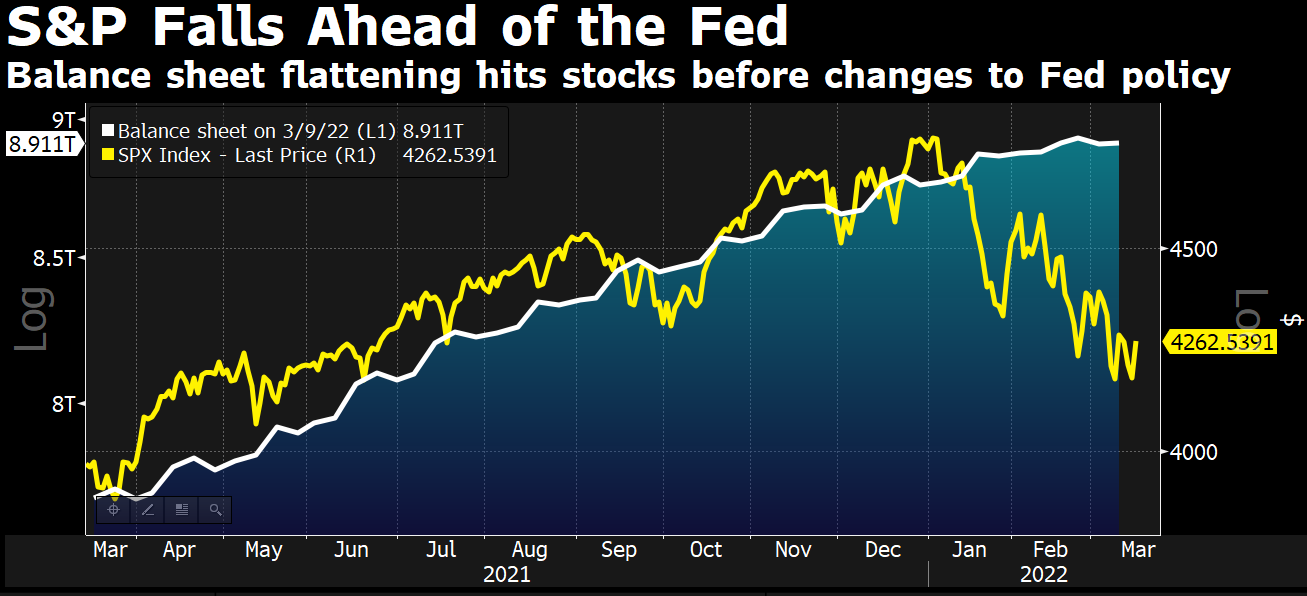

At a high level, it was surmised that many of the responses to geopolitical tension and inflation were priced in. The economy, since early pandemic disruptions, has strengthened and the need for ultra-accommodative policies is no more.

That means low rates and quantitative easing (QE) – easy money so to speak – are on the way out, at least for the time being.

Recall that QE is a policy to expand the Federal Reserve’s balance sheet “to provide monetary accommodation, typically when interest rates are at a zero-lower bound (when nominal interest rates are at, or near, zero),” as JH Investment Management explains.

With QT, central banks remove assets (e.g., government bonds they bought from the private sector) from their balance sheet “either through the sale of assets they had purchased or deciding against reinvesting the principal sum of maturing securities.”

With that, we note that when bonds rise in value, their yields decline; “when the Fed embarks on bond-buying program[s] to support the U.S. economy, … [it nudges] the prices of these assets higher while pushing yields lower, which also has the effect of driving yield-hungry investors into relatively riskier asset categories that promise high returns.”

As a result, participants’ demand for risk assets prompts their divergence from fundamentals. As liquidity is removed and funding costs increase, this may prompt risk assets to converge with fundamentals.

This is because, for investors to take on additional risk for return, they must receive in excess of the risk-free rate (as provided by the Treasury). This excess is the risk premium.

Previously, as the Damped Spring’s Andy Constan had previously commented, “[a]dditional risk premium expansion pressures from these levels is not likely.”

“However, if, in the unlikely event, details of QT do emerge suggesting a start of QT before June and at a greater size than expected, we would no longer be willing to hold [risk] assets as that would cause an end to any risk premium contraction possibilities.”

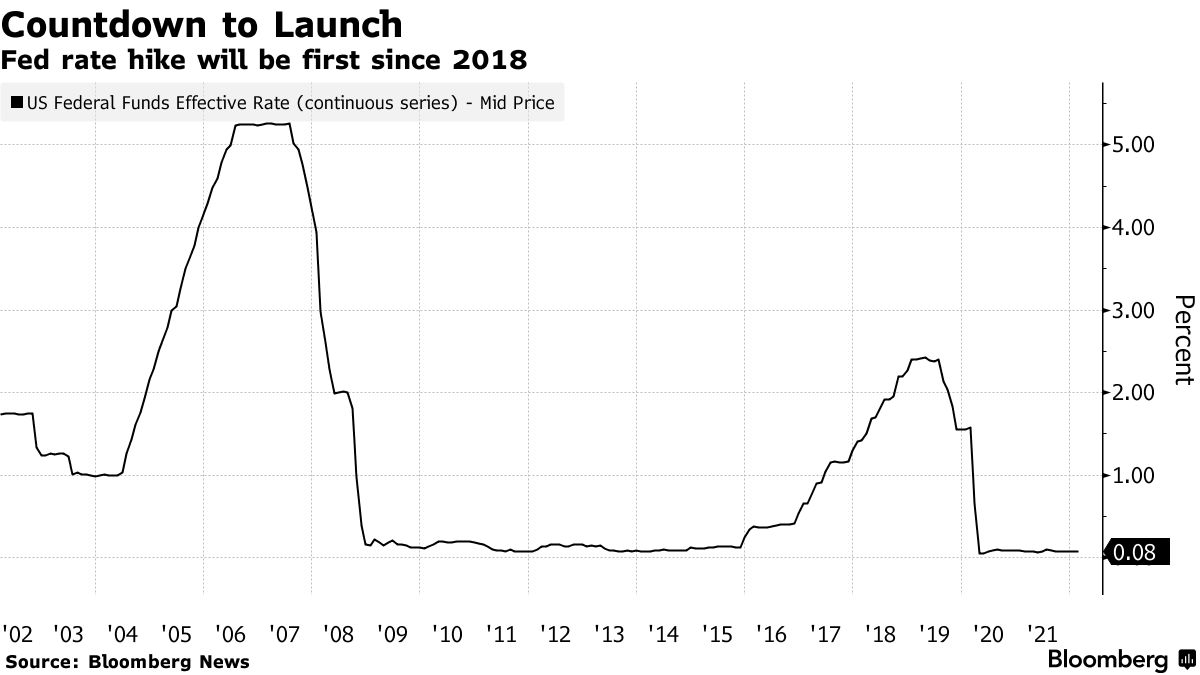

Well, that’s what happened in early April when Fed members said their debt holdings would be reduced “at a rapid pace” as soon as May, as well as hike rates, faster.

“Given that the recovery has been considerably stronger and faster than in the previous cycle, I expect the balance sheet to shrink considerably more rapidly than in the previous recovery,” the Fed’s Lael Brainard said.

The Fed may even raise “caps” on the pace of QT.

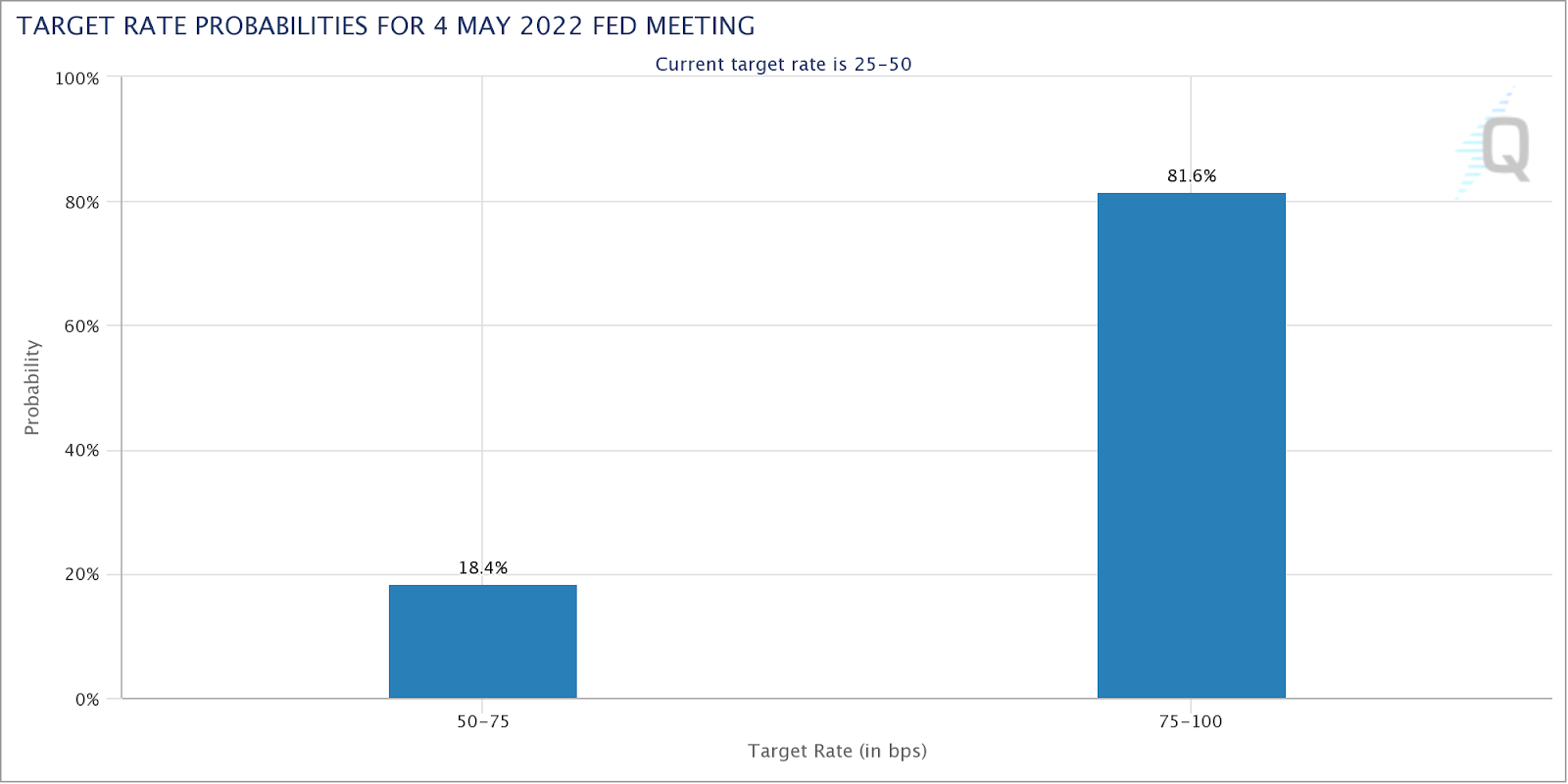

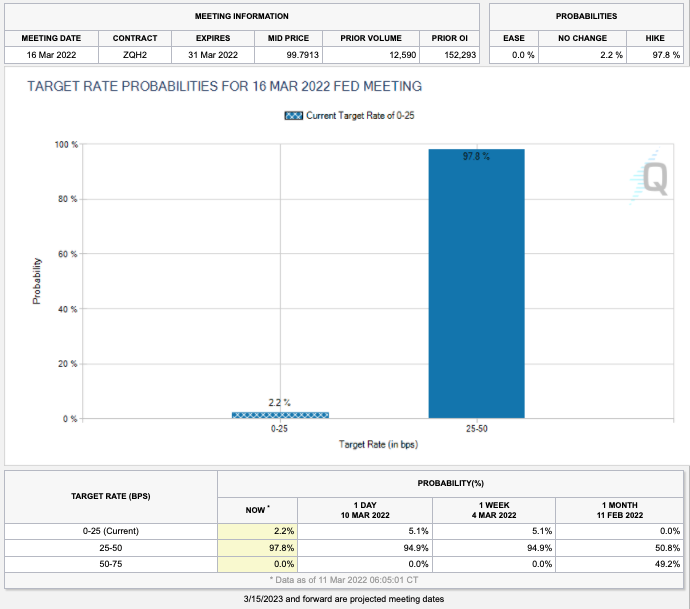

Per CME Group Inc’s (NASDAQ: CME) FedWatch Tool, market participants are pricing a near-100% probability that the Fed will move the target rate to 75-100 bps (+50 or +75 bps).

At a high-level, rates hikes take time to flow through to the economy while “QT is a direct flow of capital to capital markets or flow out of,” according to statements by Kai Volatility’s Cem Karsan.

“An increase in the pace of tightening of QT should mean lower stocks, wider credit spreads and a slight reduction in the need for front-end hikes,” explains Kevin Muir of the MacroTourist.

“Using the balance sheet as a tightening tool represents a large change in the Fed’s attitude, and IS NOT priced into the market.”

As an aside, adding to earlier comments on the yuan’s fall, Bob Parker, a senior adviser at Credit Suisse Group AG (NYSE: CS) explains that “When Chinese investors lose confidence in their own economy/markets, capital outflows from China accelerate, … [and] this, then, leads to a central bank which has to prop up the currency by selling some of the country’s huge reserve piles.”

“Part of their reserves will have been/are in U.S. equities so as the reserves fall, they are natural sellers of the S&P.”

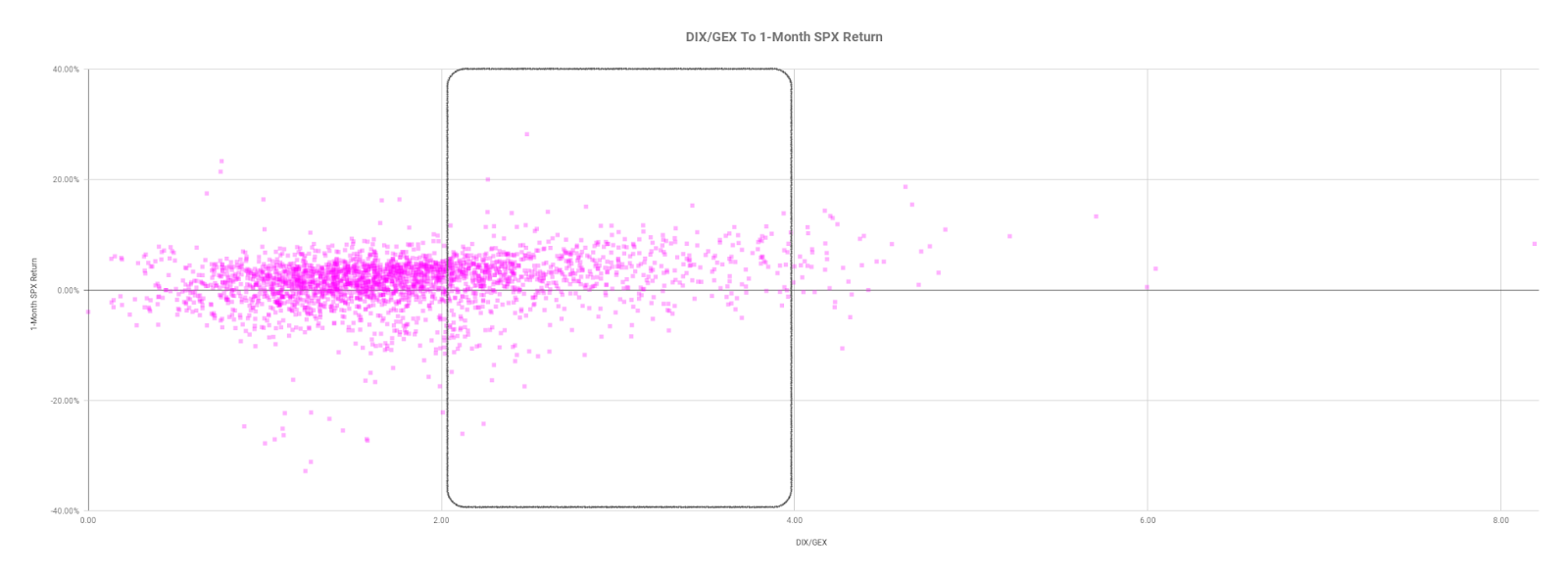

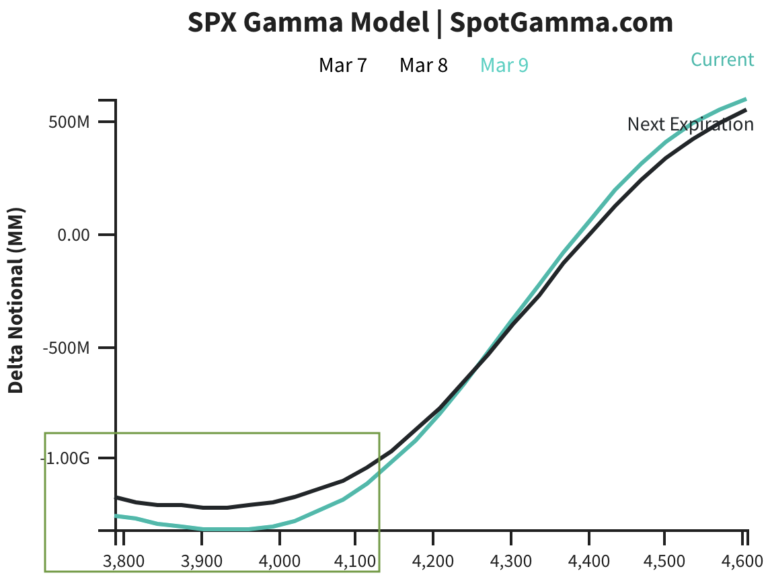

Positioning: In a comparison of options positioning and passive buying support, the returns distribution is skewed positive and points to building support for a potential short-term bounce.

The most recent liquidation resulted in participants reaching for protection and this exacerbated movement to the downside amidst the reflexive hedging.

As this short-dated exposure decays, the counterparts’ hedges are to be tapered and this may assist in the market hammering out a bottom or rallying.

On the contrary, however, as SpotGamma explained in a recent note, “[t]op of mind as we head into new trade on Monday is the likelihood traders will not aggressively sell volatility (i.e., if they sell volatility -> that drives volatility lower -> resulting in hedging flows that support the market) until the FOMC (5/4) and/or some resolution on the geopolitical front.”

“Therefore, [] expect larger trading ranges this upcoming week.”

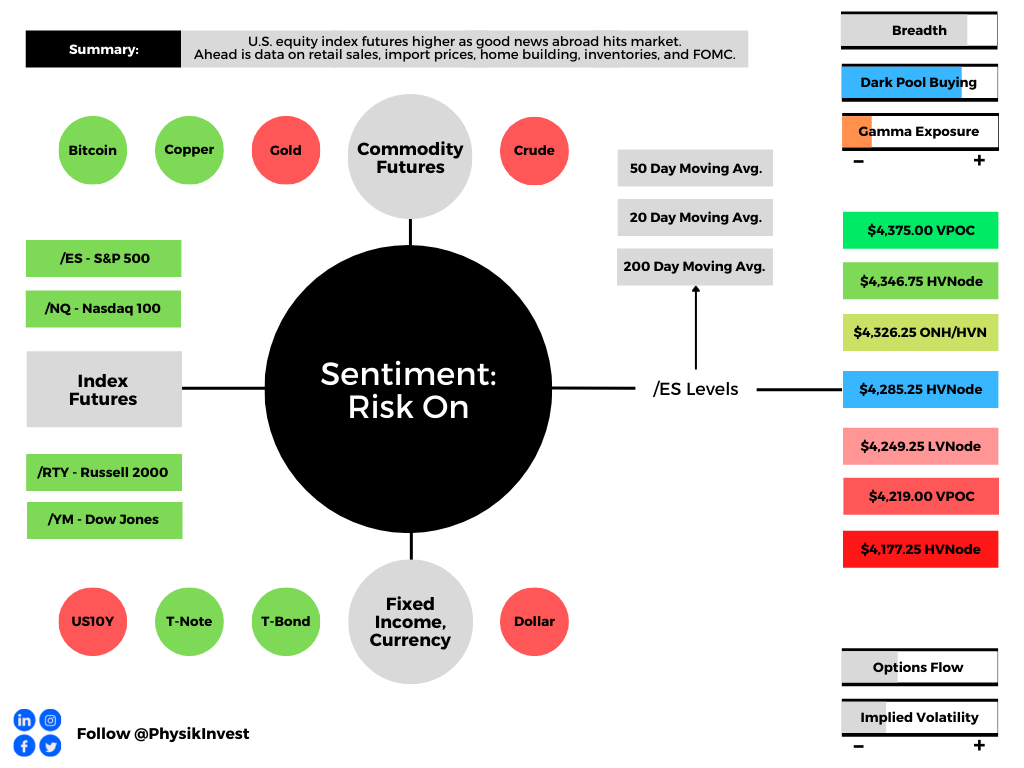

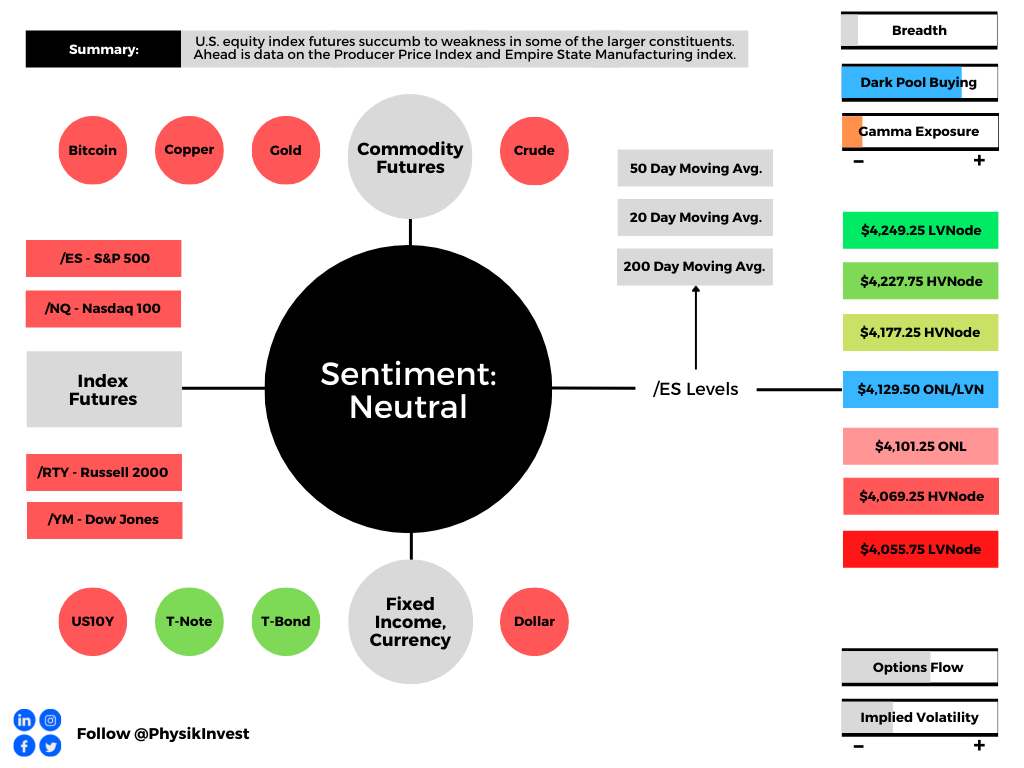

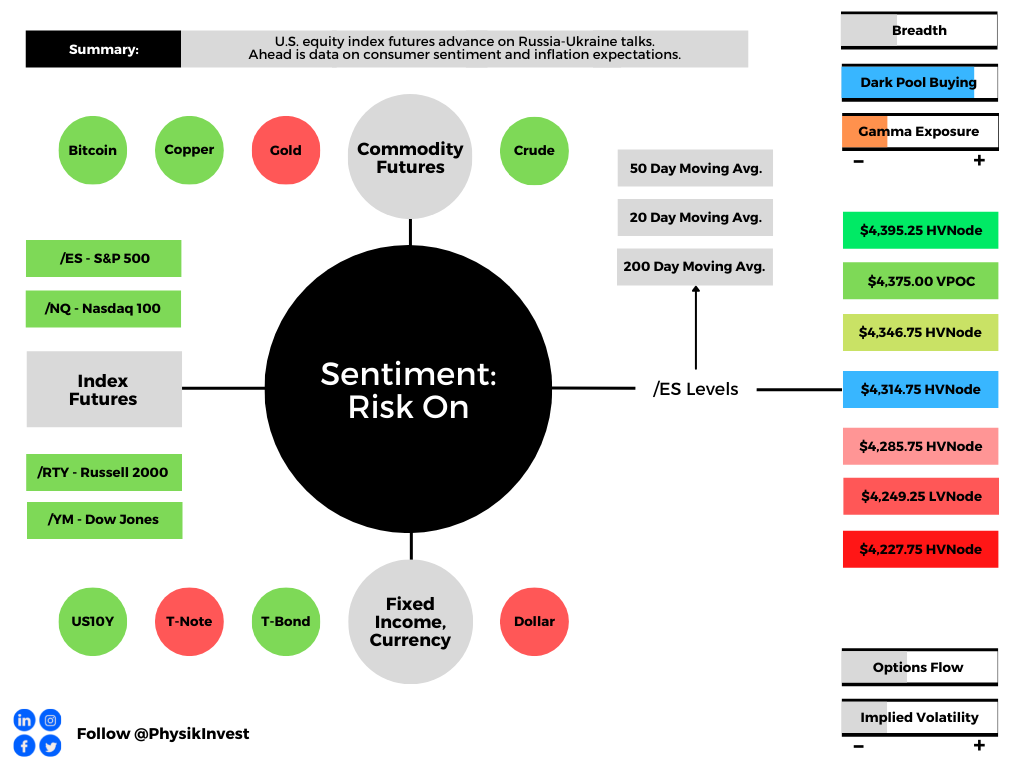

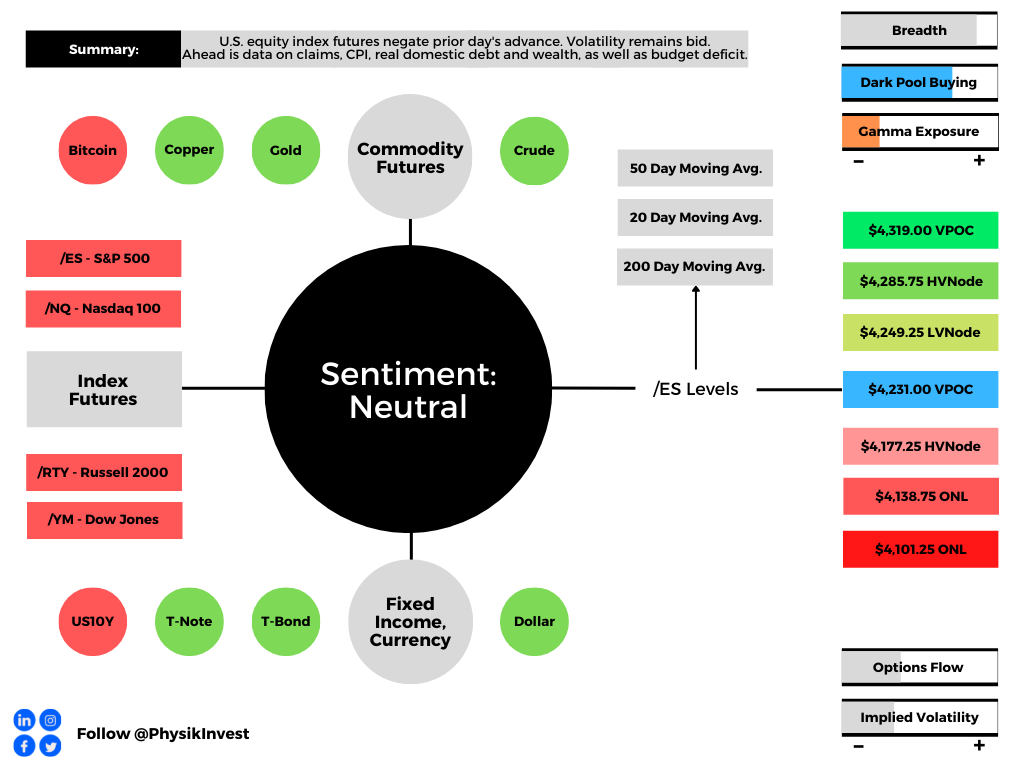

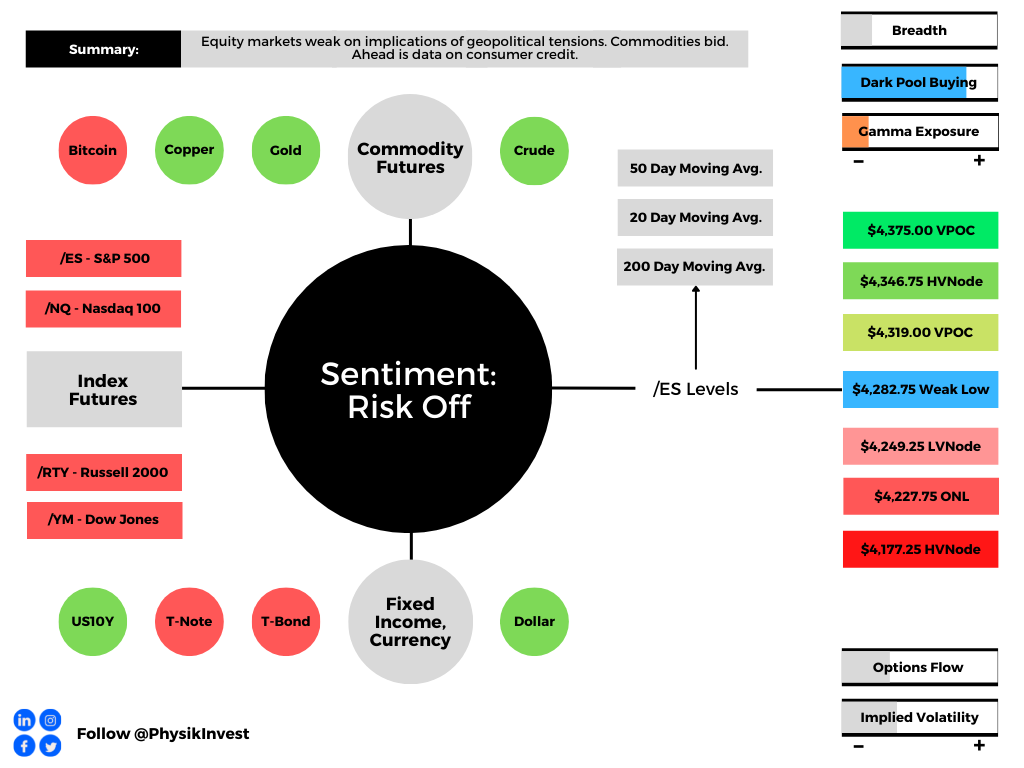

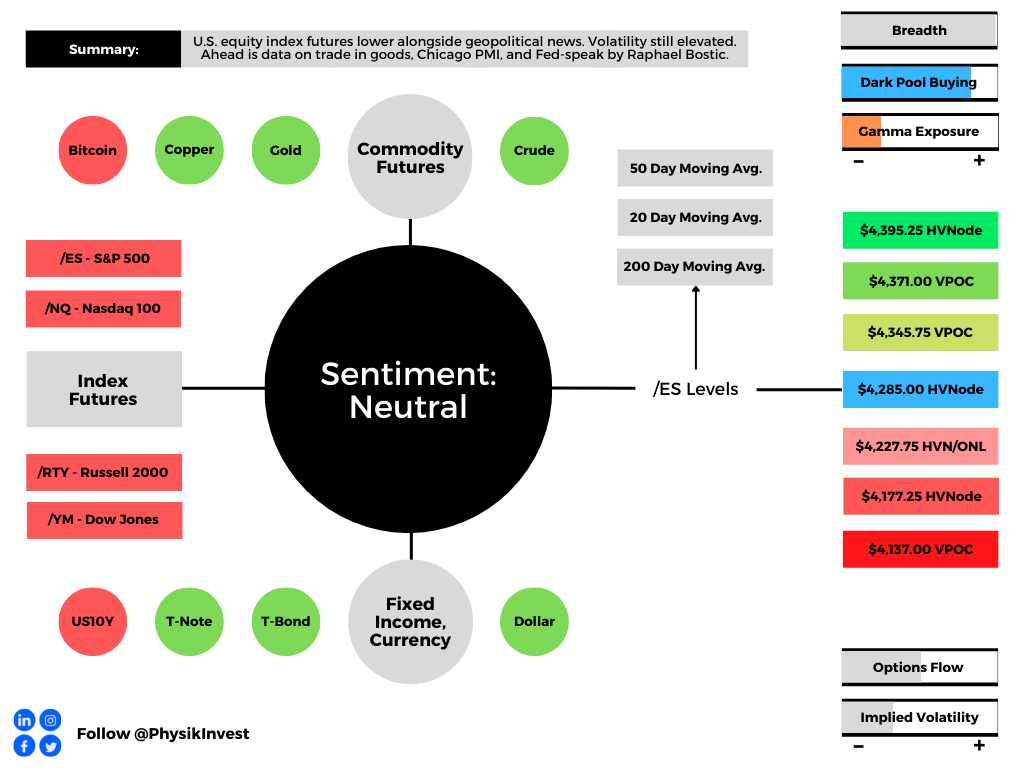

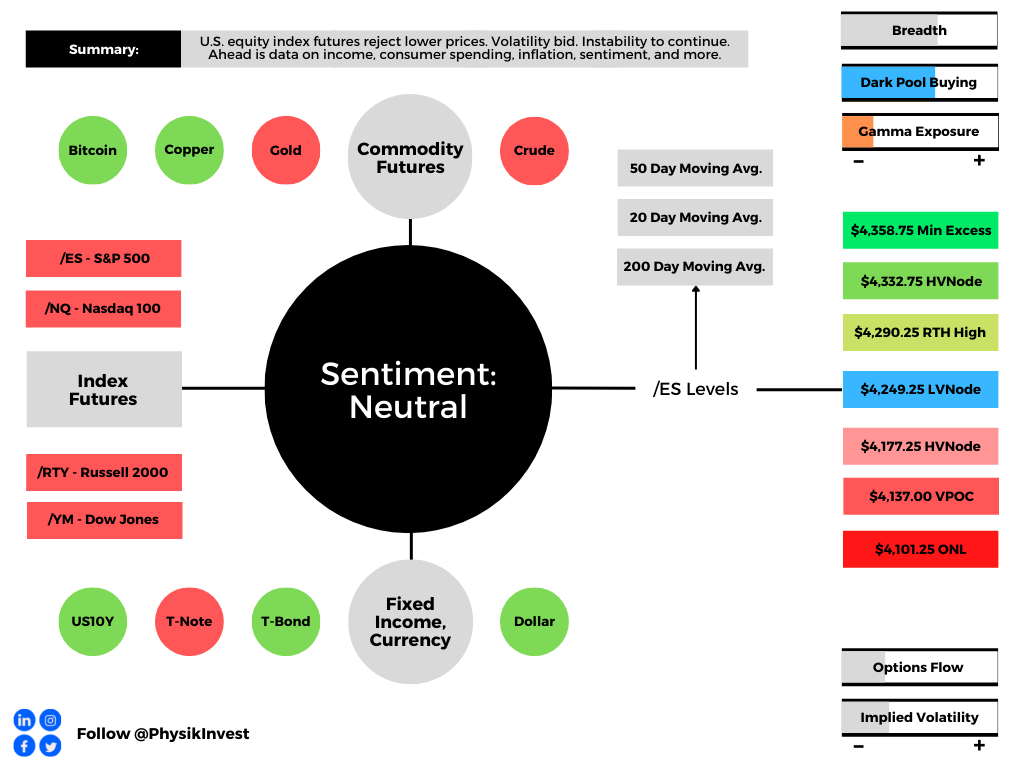

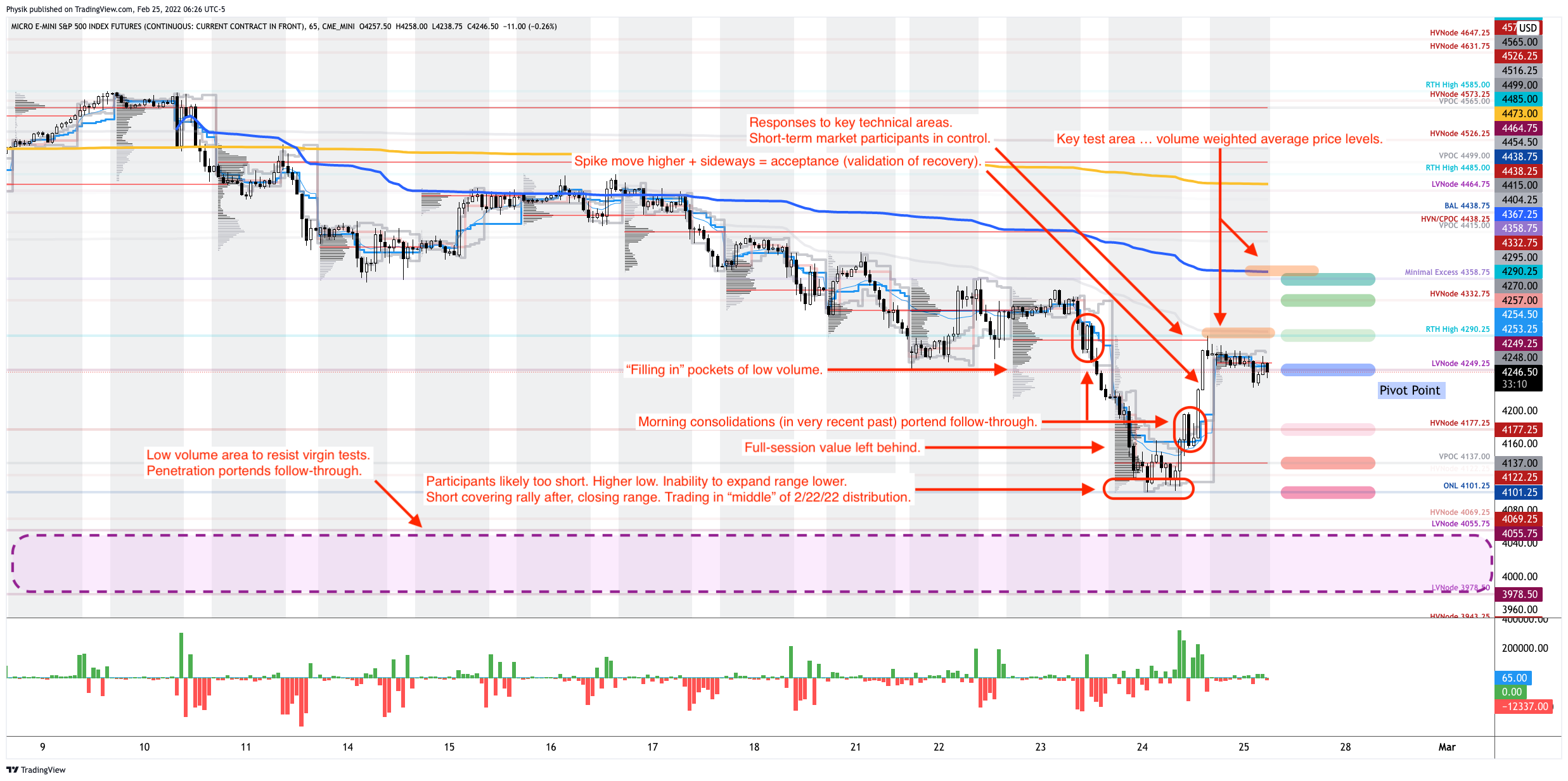

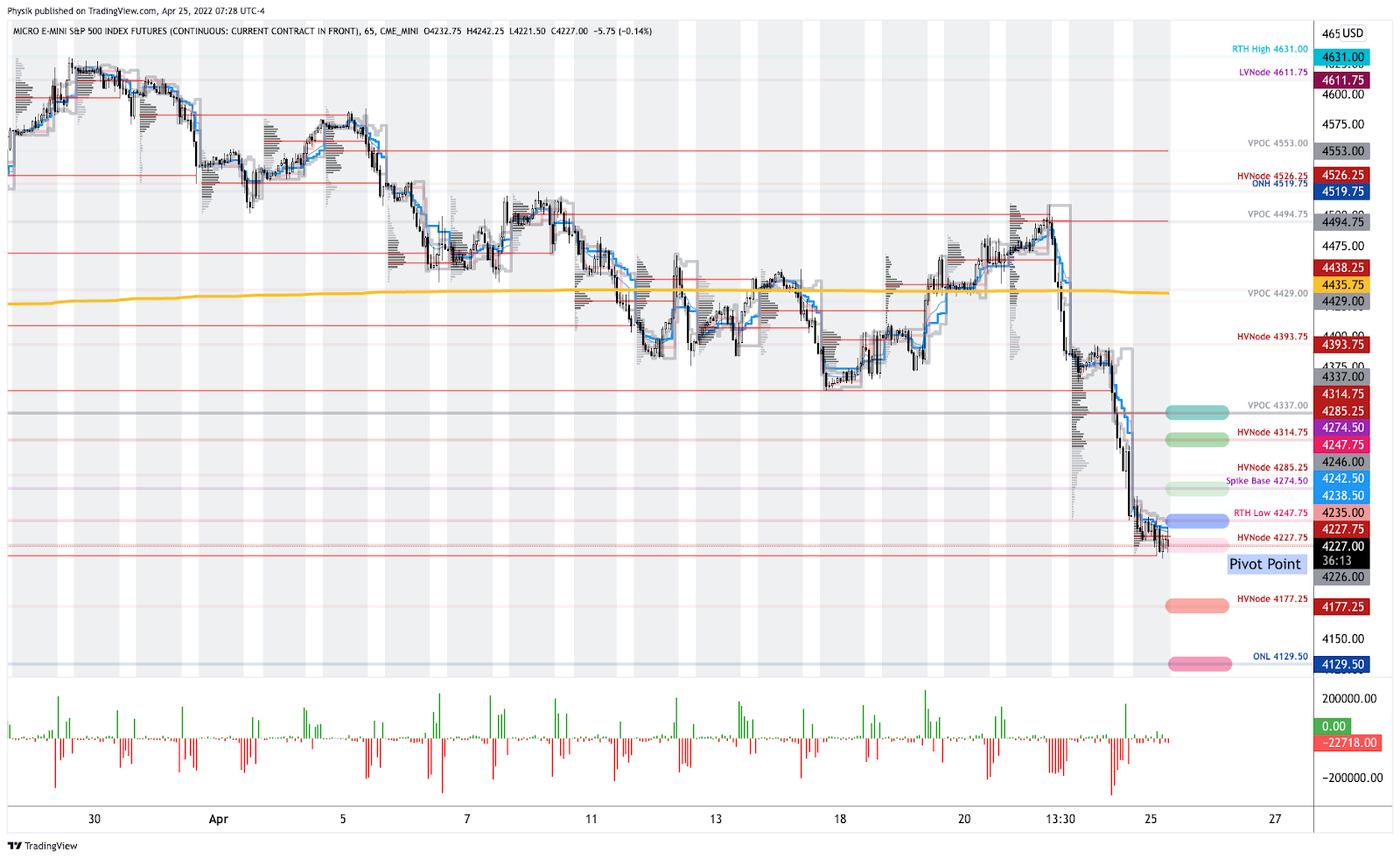

Technical: As of 6:30 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

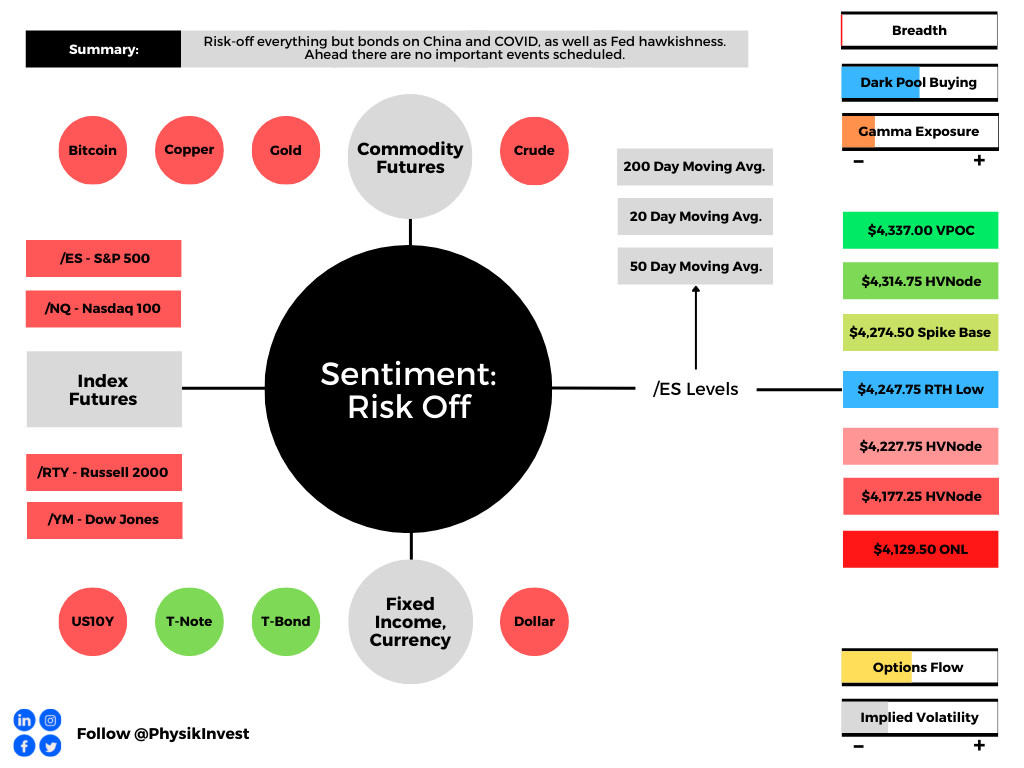

In the best case, the S&P 500 trades higher; activity above the $4,247.75 regular trade low (RTH Low) puts in play the $4,274.50 spike base. Initiative trade beyond the spike base could reach as high as the $4,314.75 high volume area (HVNode) and $4,337.00 untested point of control (VPOC), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,247.75 RTH Low puts in play the $4,227.75 HVNode. Initiative trade beyond the $4,227.75 HVNode could reach as low as the $4,177.25 HVNode and $4,129.50 overnight low (ONL), or lower.

Considerations: Spikes mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

In a spike up (down) situation, trade below (above) the spike base, negates the buying (selling).

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.