Editor’s Note: The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures traded sideways to higher after Monday’s post-options expiration (OPEX) probe lower. Ahead, there are no data releases scheduled.

What To Expect

Fundamental: At what point are monetary tightening and geopolitical tensions priced in?

According to some strategists, such as JPMorgan Chase & Co’s (NYSE: JPM) Marko Kolanovic, the sell-off is overdone and, if anything, Ukraine tensions “would likely prompt a dovish reassessment.”

“Short-term rates markets have likely moved too far vs. what CBs will ultimately deliver in hikes this year,” he adds. “We expect risky asset markets to rebound as they digest these risks and sentiment improves, aided by inflows from systematic investors and corporate buybacks.”

In the worst case, though, pursuant to notes by peers in the industry, Kolanovic nods to the fact that if selling were to continue, there would likely be a point the would Fed reassess tightening.

Basically, in the worst case, there is the potential that further selling invokes the so-called “Fed put,” which is about 15% below current prices.

“[R]isk is being repriced to fit the world where real rates are a lot higher, and the Fed put (is) much lower thanks to the Fed’s need to fight inflation,” says rates strategist Rishi Mishra.

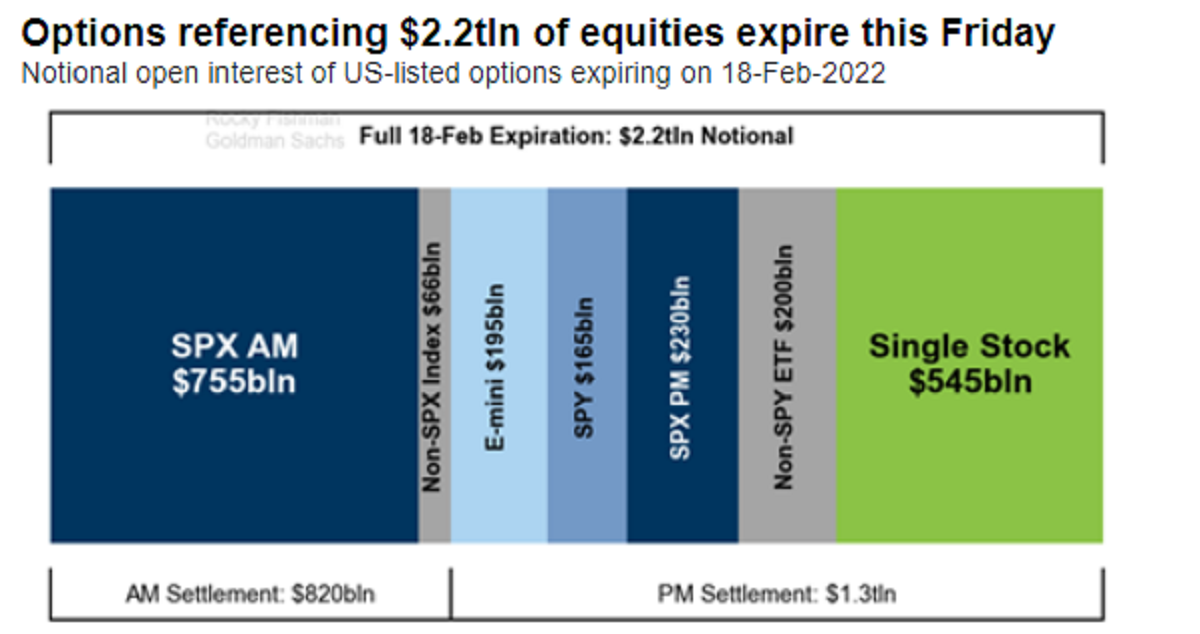

Positioning: Markets stabilize after last week’s large monthly options expiration (OPEX).

Per Bloomberg, that event saw the roll-off of nearly $2.2 trillion in options. In the past, this event had bullish implications (i.e., markets rose into OPEX). That is not the case, really, any longer.

It is participants’ increased awareness of the implications of options and OPEX has resulted in a front running; according to SqueezeMetrics, “People didn’t know about the OpEx week effect (in this case, largely charm). Now everyone and their mother knows about it.”

For context, charm is a measure of an options delta’s change with respect to the passage of time. As time passes, delta “bleeds” as options decay.

As most participants, at least at the index level, own protection, the counterparties to this trade are short protection. These counterparties, therefore, have positive exposure to delta (i.e., as index falls [rises], position loses [makes] money) and negative exposure to gamma, or delta (directional) sensitivity to underlying price changes (i.e., as the index moves against short option exposure, losses are multiplied).

Moreover, given the growth of options volumes, participants’ heavy demand for protection matters more, to put simply. Counterparties, in light of this recent drop, pressured markets with their hedging. The decay (and eventual expiry) of this protection marks options deltas down.

To re-hedge, counterparties buy back short stock and futures hedges. This supportive action is what has been front-run; the bullishness of the event happens days and weeks prior.

The unwind of these hedges now, as seen Friday-Tuesday, often culminates in a post-OPEX low. That “means chase-y accelerant flows from dealer hedging into moves and creating overshoots in both directions,” Nomura Holdings Inc’s (NYSE: NMR) Charlie McElligott wrote.

Taken together, according to SpotGamma, though “post-OPEX, the removal of linear short (-delta) hedges [to put-heavy exposures] may further bolster attempts higher, … [t]he removal of downside (put) protection may also open the door for weakness in a case where some outside (fundamental) event solicits real-money selling and a new demand for protection.”

“The market looks fairly well hedged and it’s why up until today we’ve had little follow-through on the downside despite negative headlines,” Danny Kirsch, head of options at Piper Sandler Companies (NYSE: PIPR), said in an interview.

“We’ll see if things open up after the February expiry.”

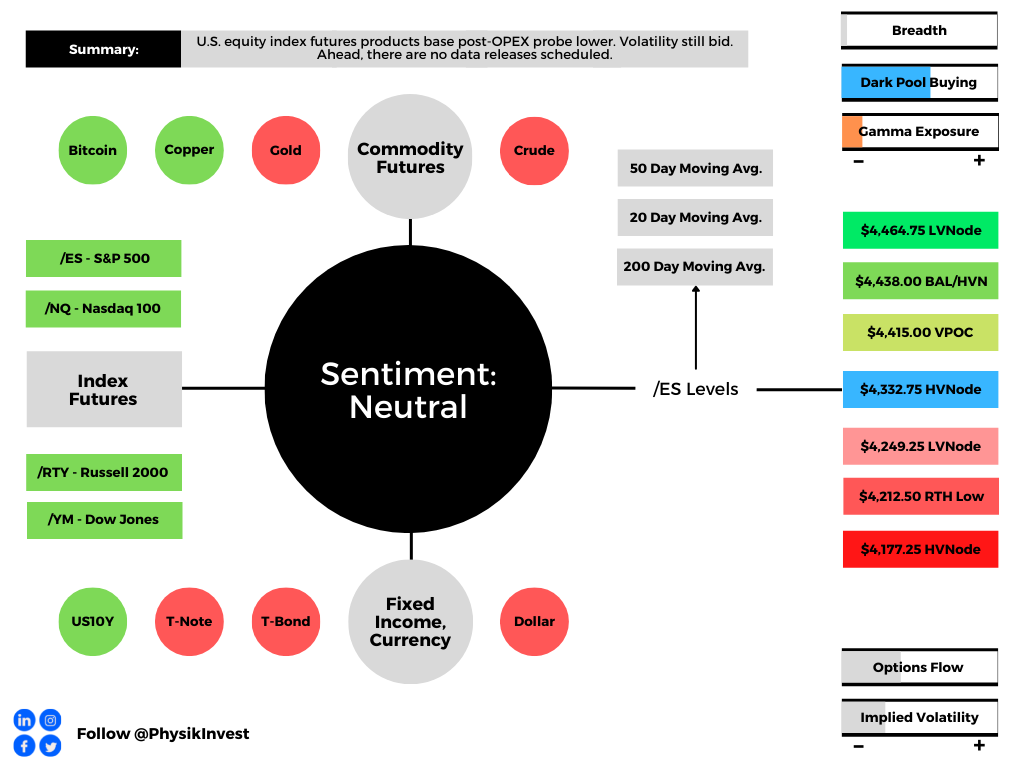

Technical: As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of its overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,332.75 high volume area (HVNode) puts in play the $4,415.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,438.00 key response area and $4,464.00 low volume area (LVNode), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,332.75 HVNode puts in play the $4,249.00 LVNode. Initiative trade beyond the LVNode could reach as low as the $4,212.50 regular trade low (RTH Low) and $4,177.25 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Liquidation Breaks: The profile shape suggests participants were “too” long and had poor

Vanna: The rate at which the delta of an option changes with respect to volatility.

Charm: The rate at which the delta of an option changes with respect to time.

Options: If an option buyer was short (long) stock, he or she would buy a call (put) to hedge upside (downside) exposure. Option buyers can also use options as an efficient way to gain directional exposure.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

One reply on “Daily Brief For February 23, 2022”

[…] the Fed would reassess tightening. At such level of reassessment is the Fed Put, a dynamic we’ve discussed in the […]