Editor’s Note: The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

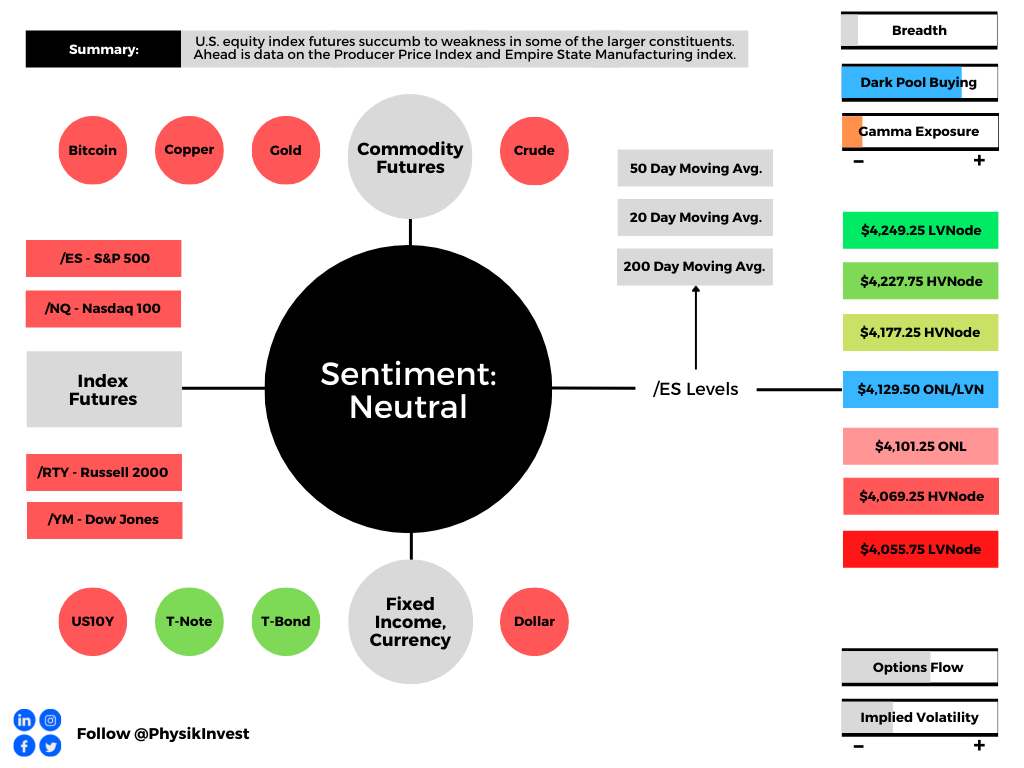

Overnight, equity index futures explored lower prices alongside most commodities. Bonds and implied volatility metrics were bid, also.

The narrative is that this is follow-on selling as participants look to price in the implications of COVID-19 lockdowns in China, as well as the Russia-Ukraine conflict. Arguably, there is some pre-Federal Open Market Committee (FOMC) positioning going on, too.

Ahead is data on the Producer Price Index and Empire State Manufacturing (8:30 AM ET).

What To Expect

Fundamental: Keeping it short, today. Please check out Monday’s commentary, if you haven’t!

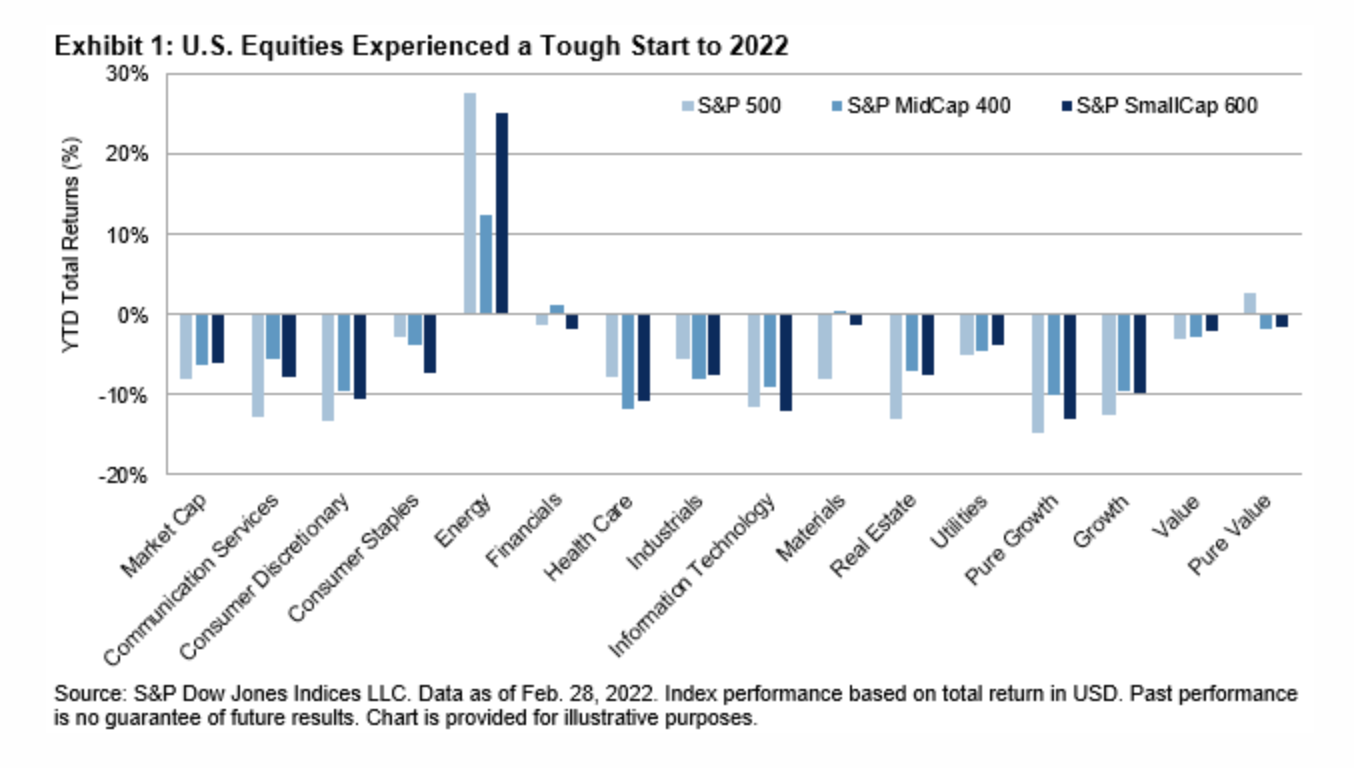

Weak start to 2022 as participants look to price slower growth and inflation, tighter monetary policy, geopolitical tensions, a resurgence in COVID-19, potential Russian defaults, and beyond.

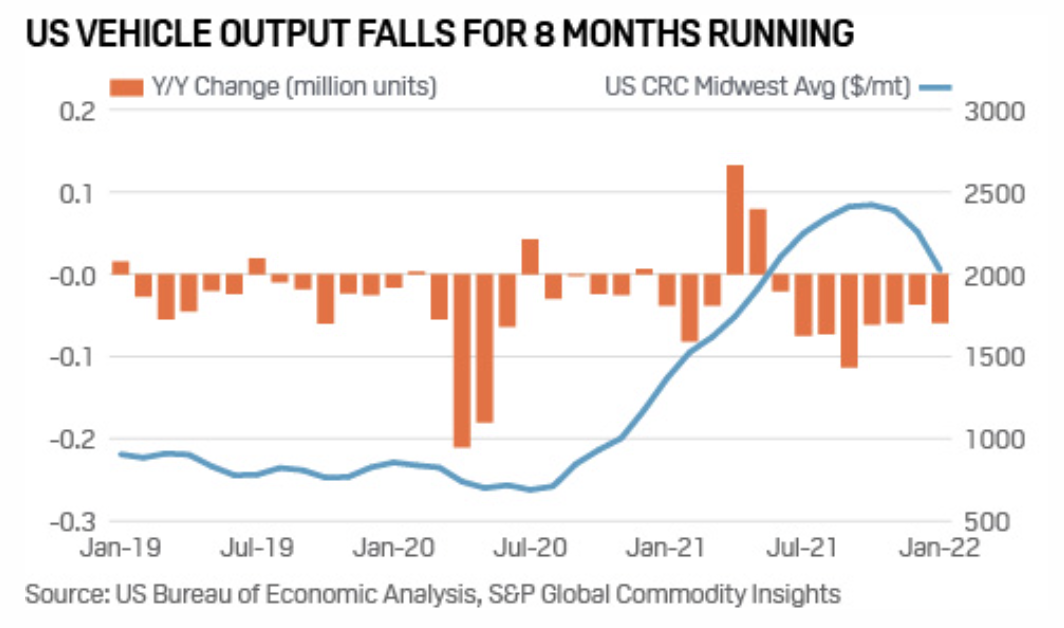

Bolstering inflation pressures are supply-demand challenges. For instance, geopolitical tensions are stifling vehicle production here in the U.S.

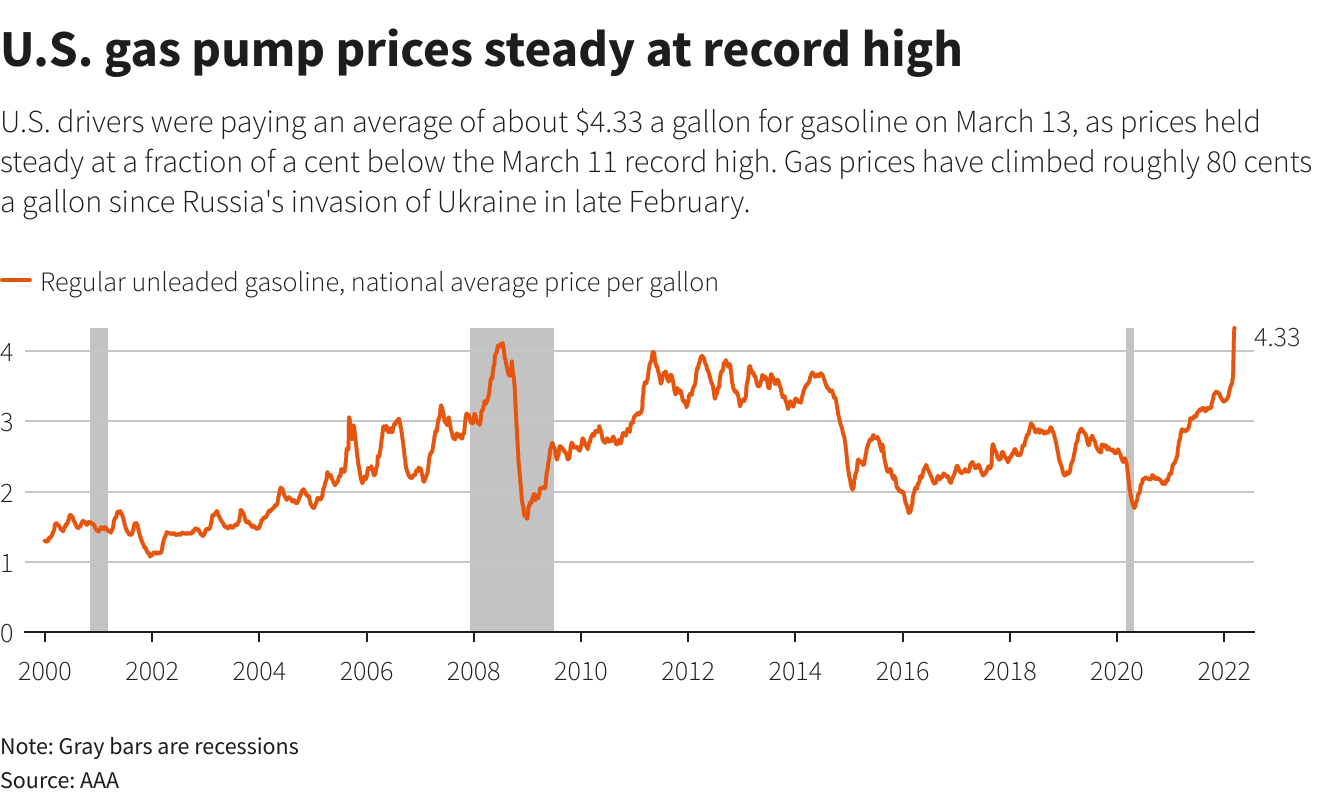

Since Russia’s invasion of Ukraine, gas in the U.S. climbed about $0.80/gallon, also, prompting talk of gas tax holidays.

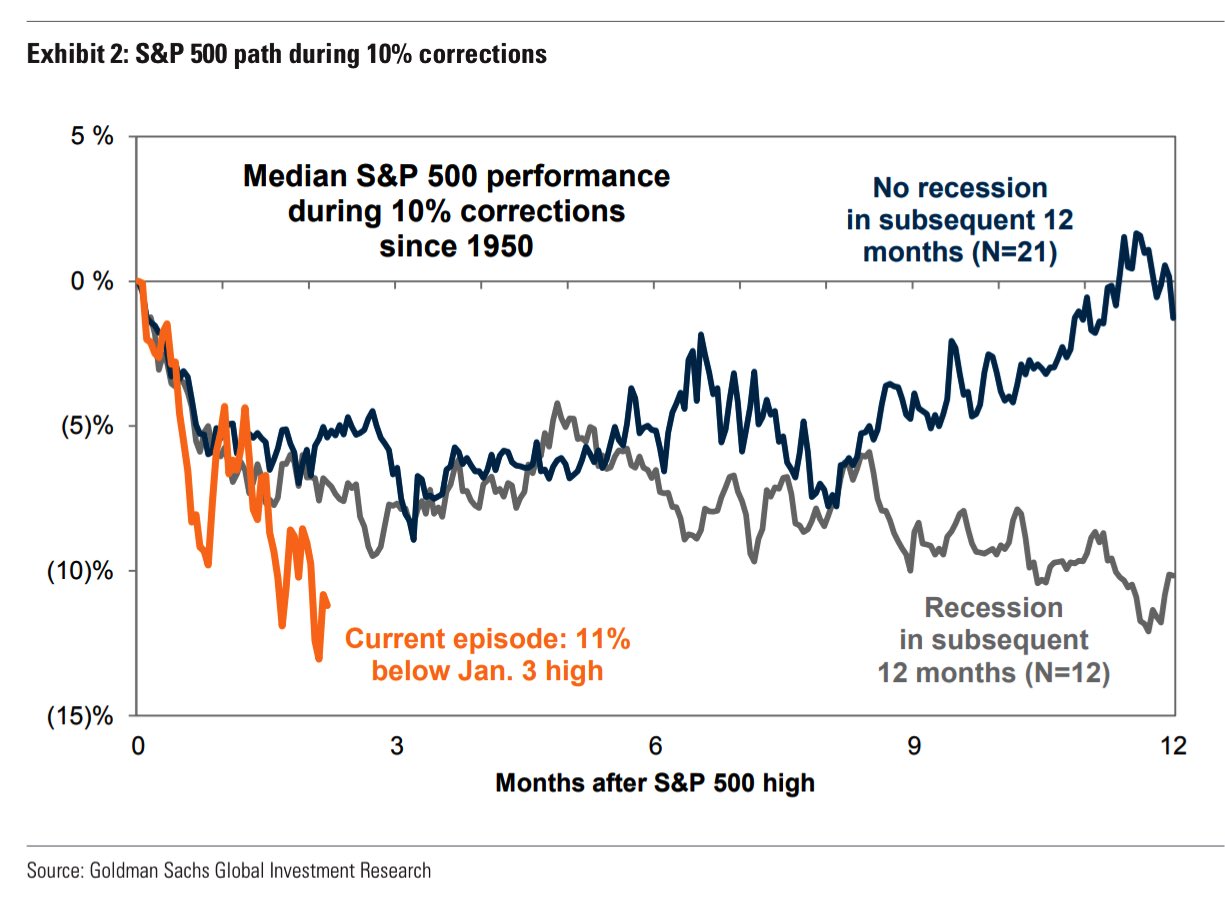

Pursuant to these remarks, Goldman Sachs Group Inc (NYSE: GS) economists suggest the probability of recession in the next year is between 20-35% while Morgan Stanley (NYSE: MS) strategists see equity valuations overshooting to the downside with out of control inflation.

In opposition, JPMorgan Chase & Co’s (NYSE: JPM) Marko Kolanovic suggests there is too much negativity priced in and that investors should add equity risk.

“We believe that the past month’s correction has induced too much negativity in markets, e.g., reflected by our market-implied recession probabilities, on the fear that growth will be severely affected by the war. We stay with a pro-risk stance as we do not believe that we will see a recession or that we have entered a sustained bear market.”

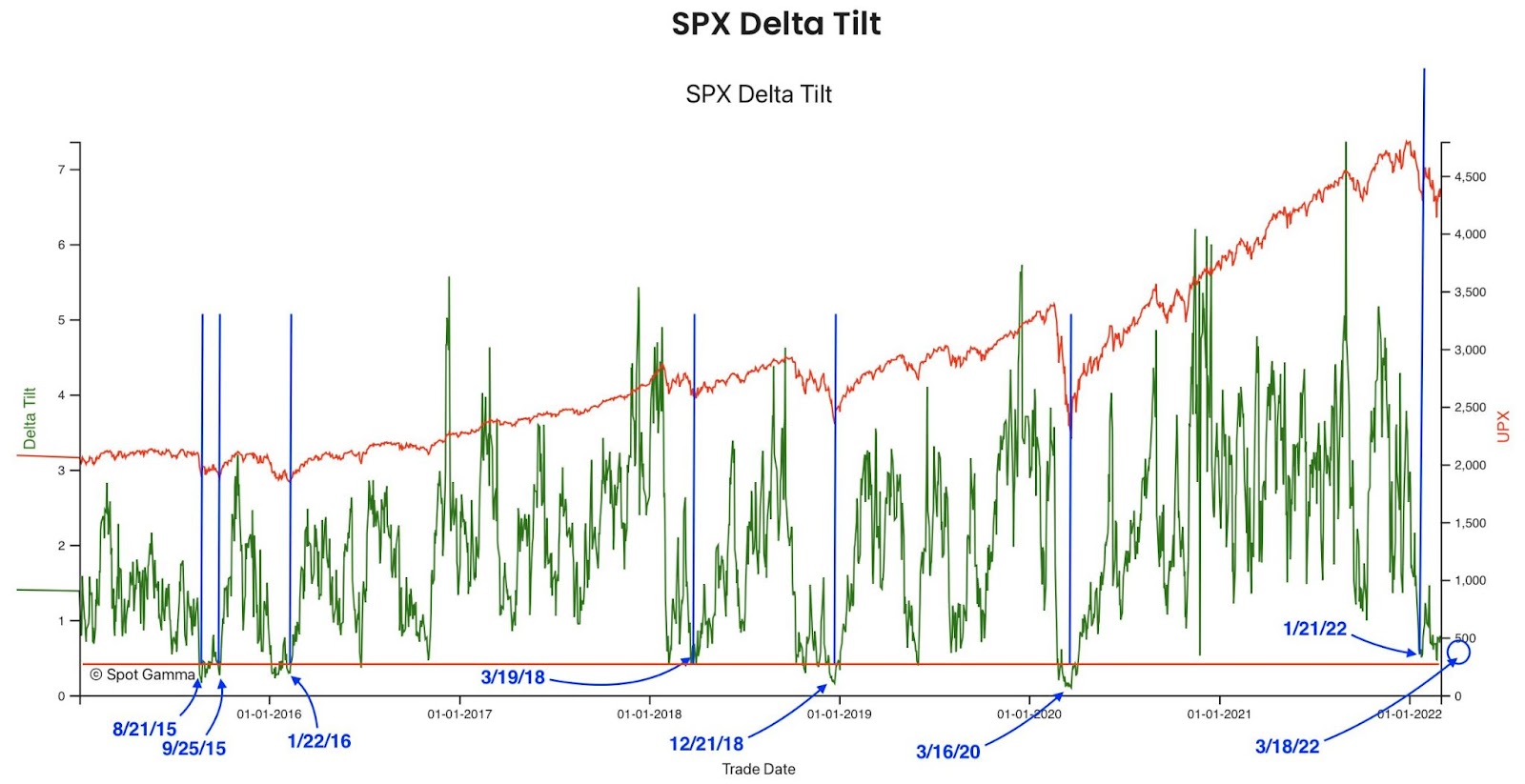

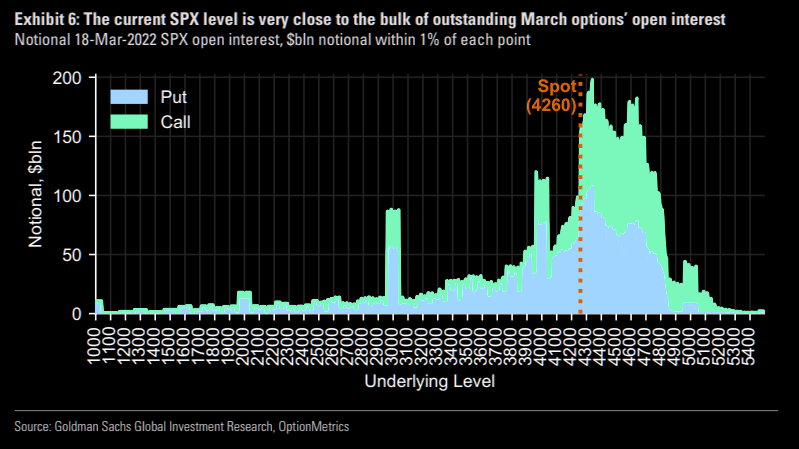

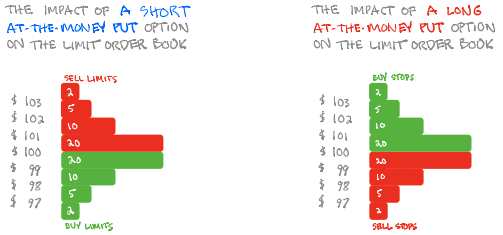

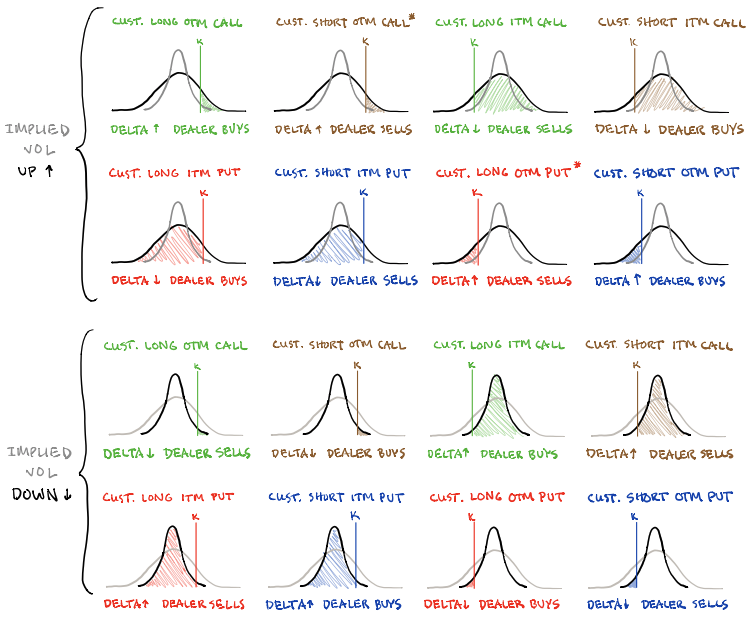

Positioning: Per Goldman Sachs Group Inc’s derivatives team, “puts are more overvalued than any time over the past five years.”

Further, it is expected that the compression of volatility (via passage of FOMC), as well as the removal of customer puts and (accordingly) counterparty negative gamma exposure (OPEX) may serve to alleviate some of this pressure.

In taking the other side of this demand for protection, counterparties carry exposure to positive delta and negative gamma (losses amplified to the downside). In hedging their own exposure, counterparties will sell underlying(s), and this is where the aforementioned pressure arises.

Given present supply and demand conditions (customer hedging in months prior), the incremental pressure counterparties add with each leg lower is less, if you will.

Here’s a good explanation:

“When implied volatility is high, that same 1% move lower is much more ‘expected’ so there generally won’t be the same upward pressure on volatility and in fact it might decline,” said Christopher Jacobson, a strategist at Susquehanna Financial Group LLP.

“Along the same lines, investors at that point have had more opportunity and time to hedge, so those same market moves may not lead to as much hedging activity.”

Adding to that last remark, as Amy Wu Silverman of Royal Bank of Canada’s (NYSE: RY) capital markets group puts it well: “You’re also seeing people selling that volatility and doing some overwriting. That can probably dampen volatility.”

There is the potential, according to SpotGamma, for some “path dependency,” however, as “the expiration and/or covering of a large swath of these put hedges may place the market back into an ‘underhedged’ position.” In such a case, new demand would add fuel to weakness.

Technical: As of 6:15 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator. Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

In the best case, the S&P 500 trades higher; activity above the $4,129.50 overnight low (ONL) puts in play the $4,177.25 high volume area (HVNode). Initiative trade beyond the $4,177.25 HVNode could reach as high as the $4,227.75 HVNode and $4,249.25 LVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,129.50 ONL puts in play the $4,101.25 ONL. Initiative trade beyond the ONL could reach as low as the $4,069.25 HVNode and $4,055.75 LVNode, or lower.

Considerations: Push-and-pull, as well as responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.