Editor’s Note: The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

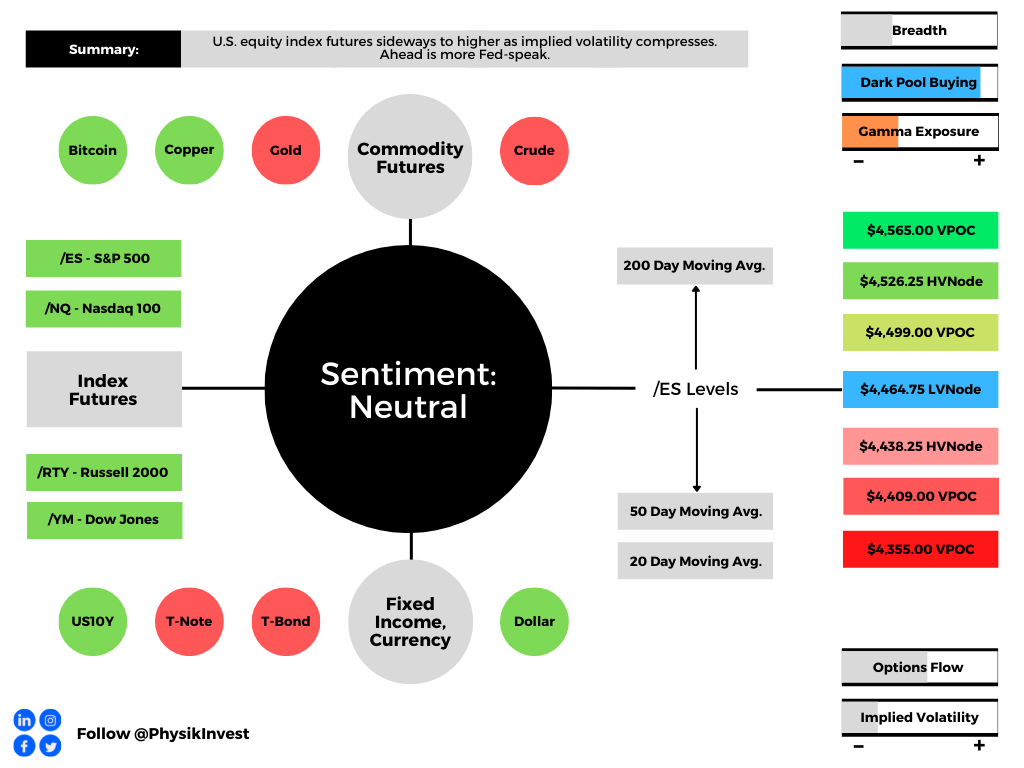

Overnight, equity index futures were sideways to higher, and this validates higher prices, more.

This is as implied volatility metrics – such as the Cboe Volatility Index (INDEX: VIX) – continue to suggest less demand for protection and a potential easing of concern.

As discussed in detail, yesterday, participants are not committing themselves to increased call option (i.e., insurance for shorts or bets on the upside) exposures, a dynamic usually seen at the start of sustained reversals.

Given this, as well as institutional selling in spite of underinvestment (watch a chat), and the Federal Reserve’s (Fed) commitment to reining in inflation via “aggressive” monetary policy (i.e., hike and taper asset purchases) action, there is concern over the sustainability of this rally.

Ahead is Fed-speak. The New York Fed’s John Williams speaks at 10:35 AM ET. San Francisco Fed’s Mary Daly talks at 2:00 PM ET. The Cleveland Fed’s Loretta Mester talks at 5:00 PM ET.

What To Expect

Fundamental: Based on remarks by the Fed’s Jerome Powell, quantitative tightening (QT) will move at a pace of $1 trillion a year. This is a faster pace than that of the prior QT.

Read yesterday’s commentary for more on QE and QT.

According to Joseph Wang’s detailed discussion on the implications of QT, the “[a]nticipation of QT is already widening the spread between Agency MBS and Treasuries but does not yet appear to affect Treasury prices.”

“The supply and demand dynamics suggest that the market may simply be slow to react. In that case, Treasury prices will also have to adjust downward, maybe by a lot.”

Pursuant to that remark, Damped Spring’s Andy Constan explains that quantitative easing (QE), “which decreased risk premiums and increased wealth was inflationary to assets but ineffective in generating inflation of goods and services.”

Essentially, QT is not a good tool to fight inflation.

“Raising rates is the strong tool to fight inflation for the Fed and decreasing the budget deficit growth is the tool for Fiscal policymakers; … the [Fed] will do both QT to reduce the balance sheet and hike rates to fight inflation.”

Moreover, higher bond yields (lower bond prices) are usually not good for stocks. The question is whether participants want to take on the added risk of investing at high valuations?

The QT narrative amplifies the impact of rate hikes.

Lisa Shalett, CIO at Morgan Stanley (NYSE: MS) Wealth Management, discussed recently QT at $80 billion per month (and $500 billion in balance sheet reduction through year-end), as well as how the added risks are to be compensated through lower price-to-earnings multiples in the stock market.

“In tightening terms, that’s the equivalent of another 25-basis-point hike,” Shalett explained. “In contrast, balance sheet run-off totaled $700 billion from 2017 through 2019 before the Fed stopped because markets seized and stocks sold off.”

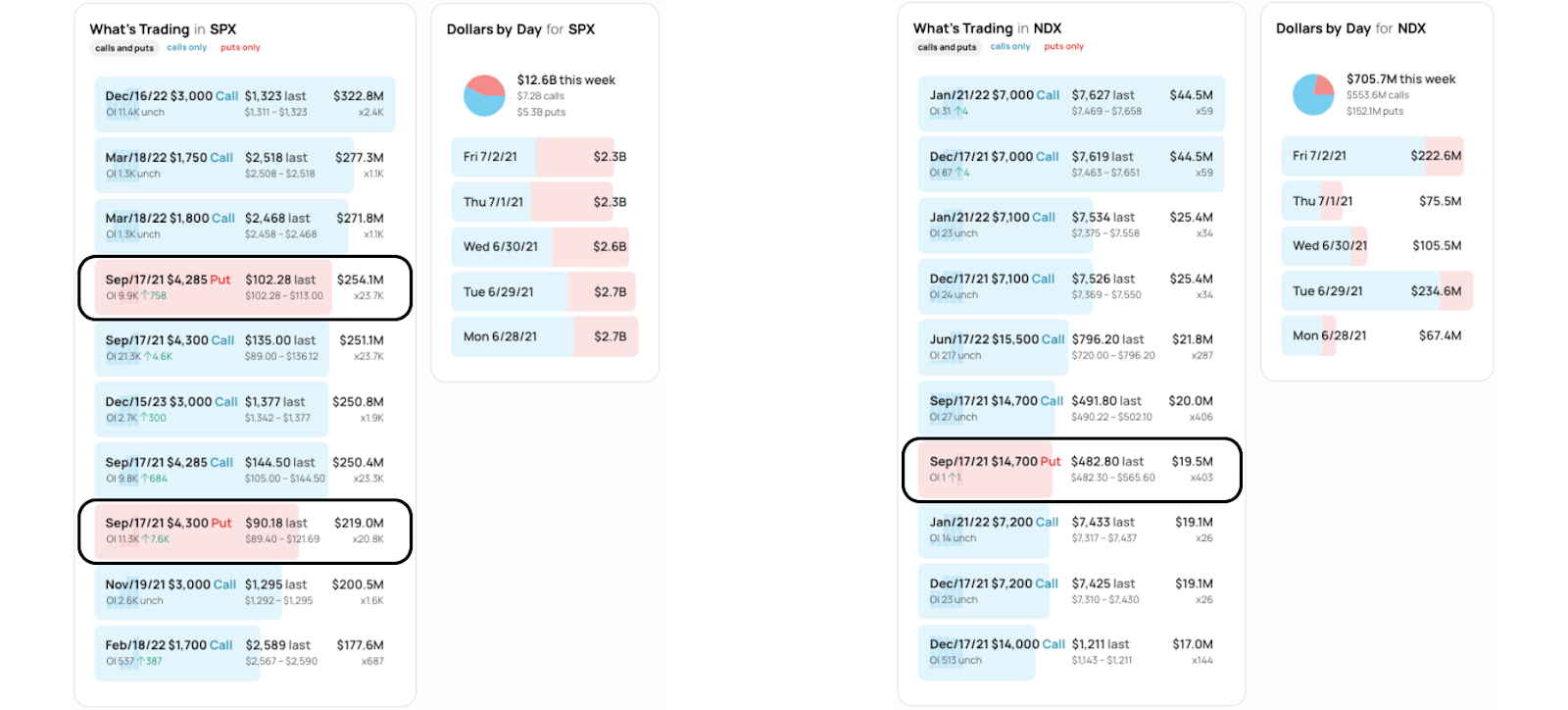

Positioning: As discussed before, a feature of falling markets is the demand for protection.

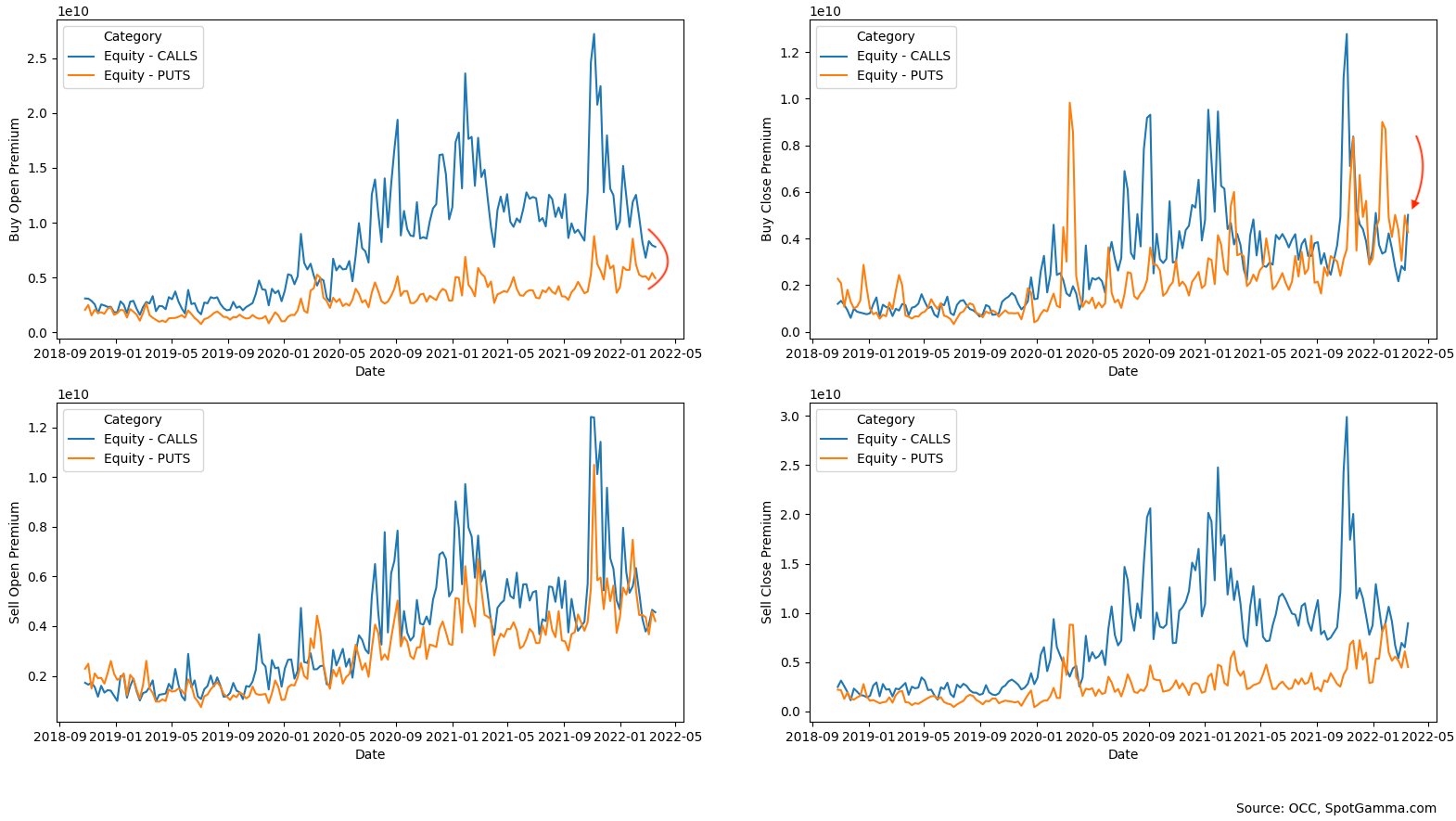

When this protection is monetized (or decay ensues), options counterparties add to the market liquidity (i.e., buying back short futures hedges).

A feature of markets entering a sustainable recovery is the demand for call options.

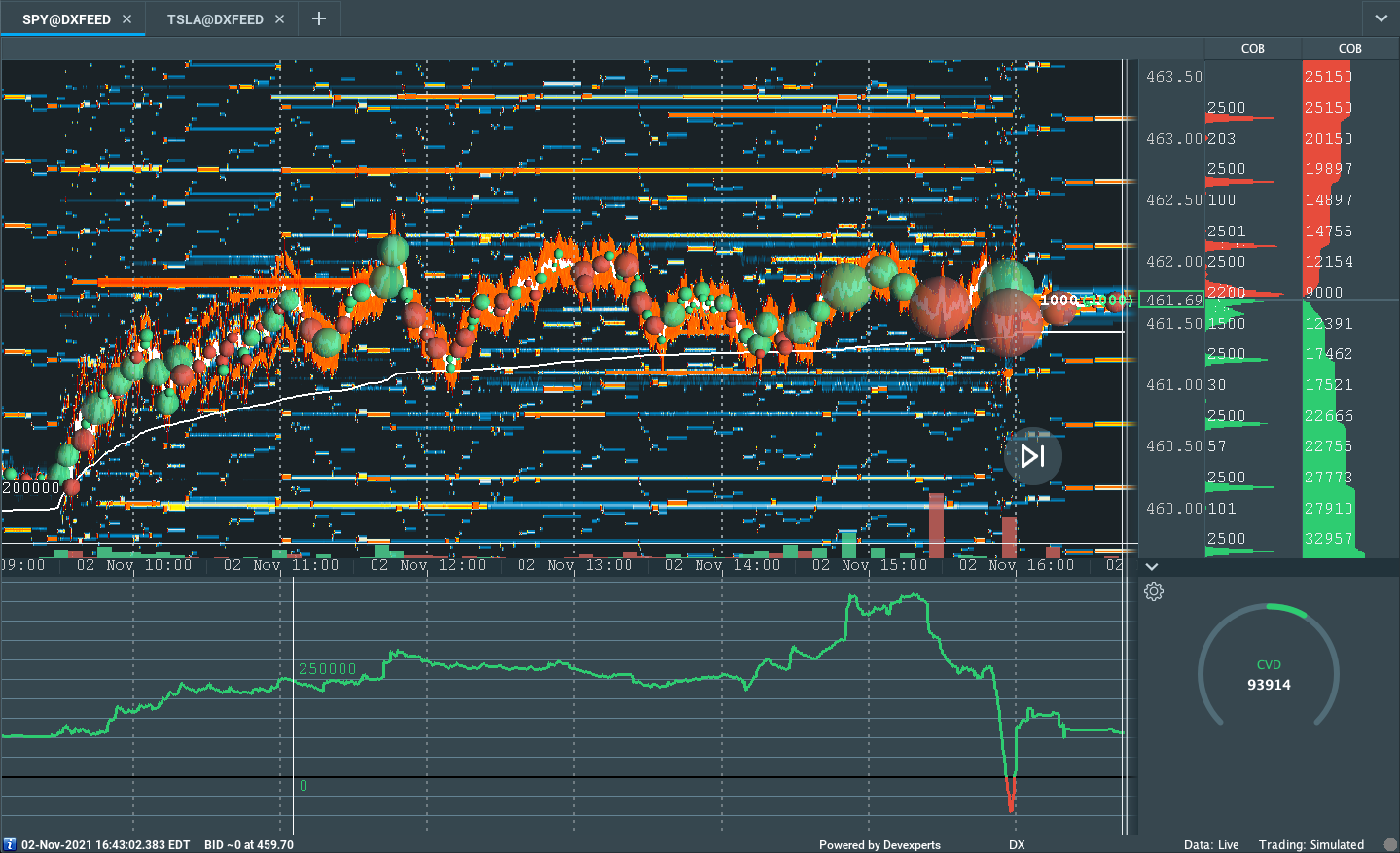

Based on metrics published by SpotGamma, call-buying was near its lows.

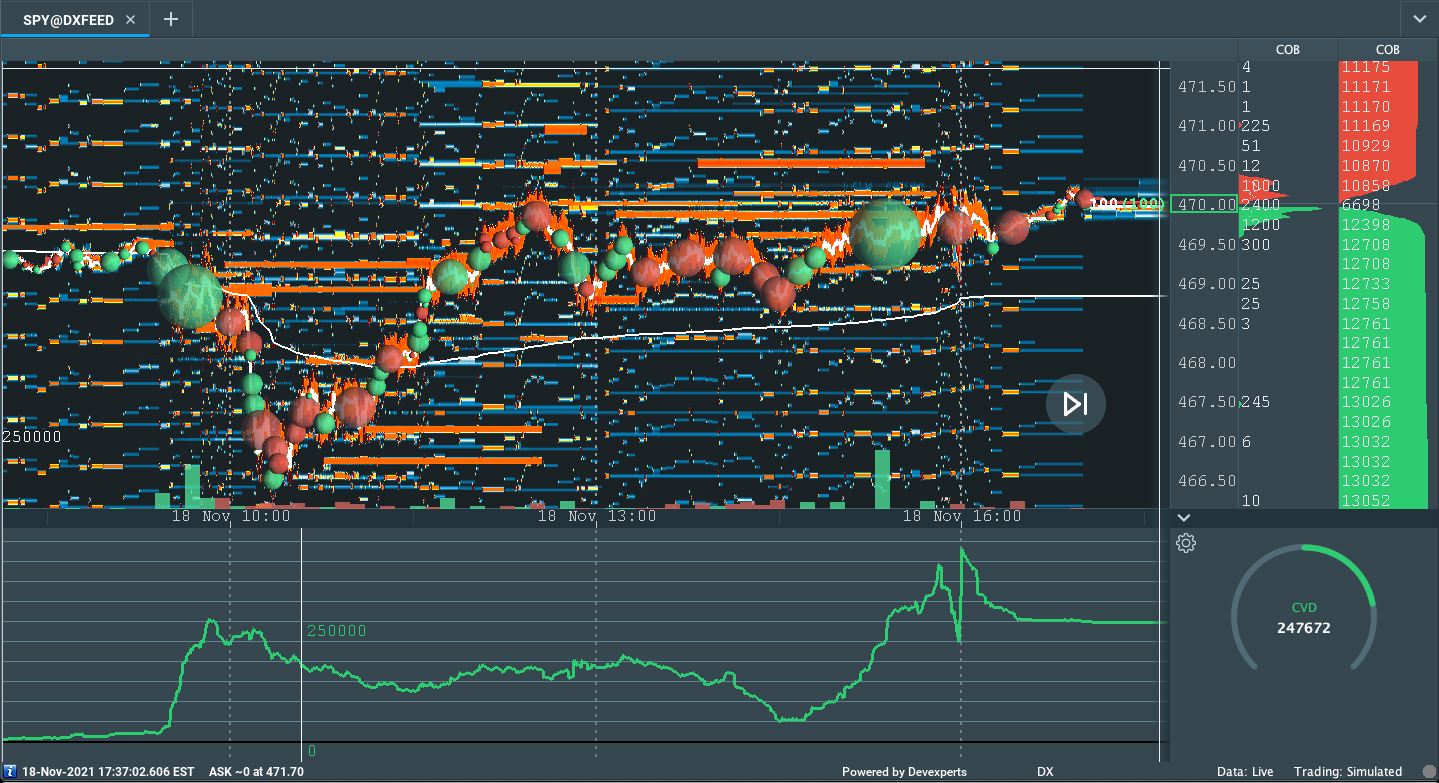

Looking at intraday measures, yesterday, we see that participants’ commitment to a change in direction remains low, still.

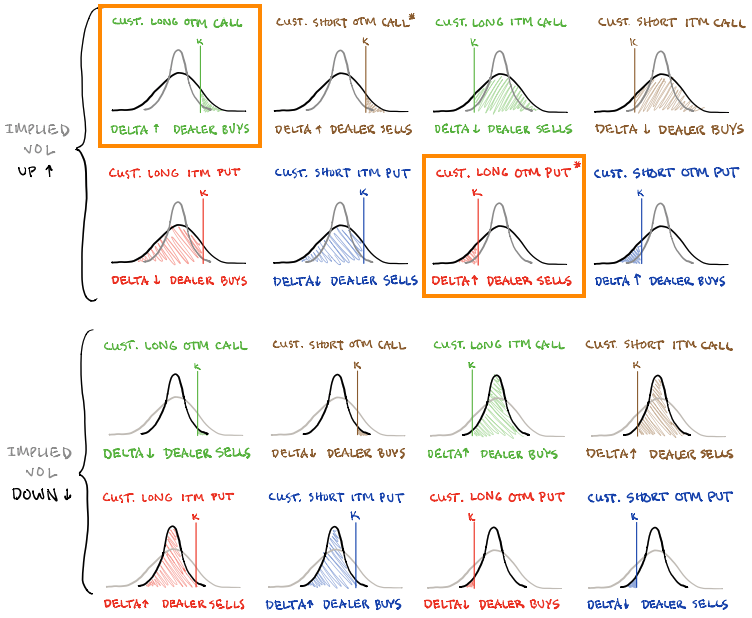

It’s possible that the bottoming process has yet to conclude. Instead, a build of positive options gamma (via the supply of protection – call selling – and more active hedging of call options near the money) may give the market some support.

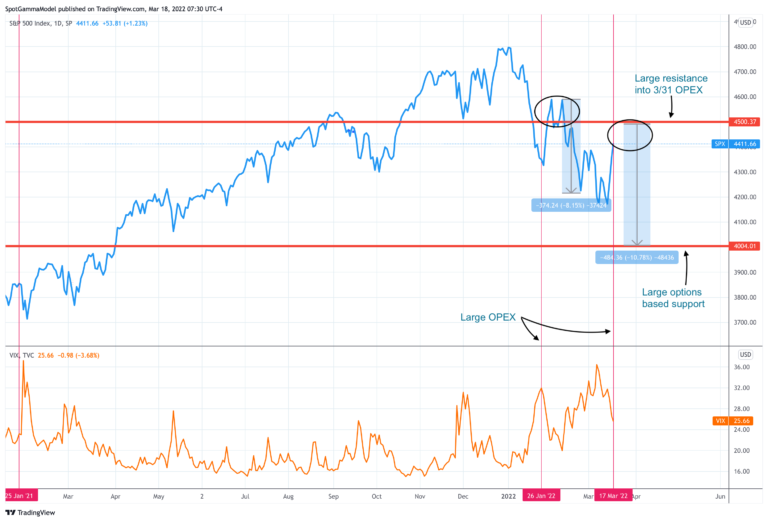

To explain, in accordance with the HIRO graphic above, we surmise counterparties are long calls and therefore tend toward selling into strength (buying into weakness) amid increasing (decreasing) positive delta exposure.

As short-dated activity clusters in the area just north of the most recent price rise, and this protection decays, dealer exposure to positive delta (gamma) falls (rises).”

“Taken together, dealers add to the market liquidity. When there is rising liquidity, volatility (a measure of how ample liquidity is) falls,” SpotGamma adds.

“Was the SPX to liquidate, again, demand for protection and increases in volatility likely have us targeting options-based support.”

In other words, based on the information we have at the moment, the market is prone to sharp drops lower, and the rally is questionable. Caution.

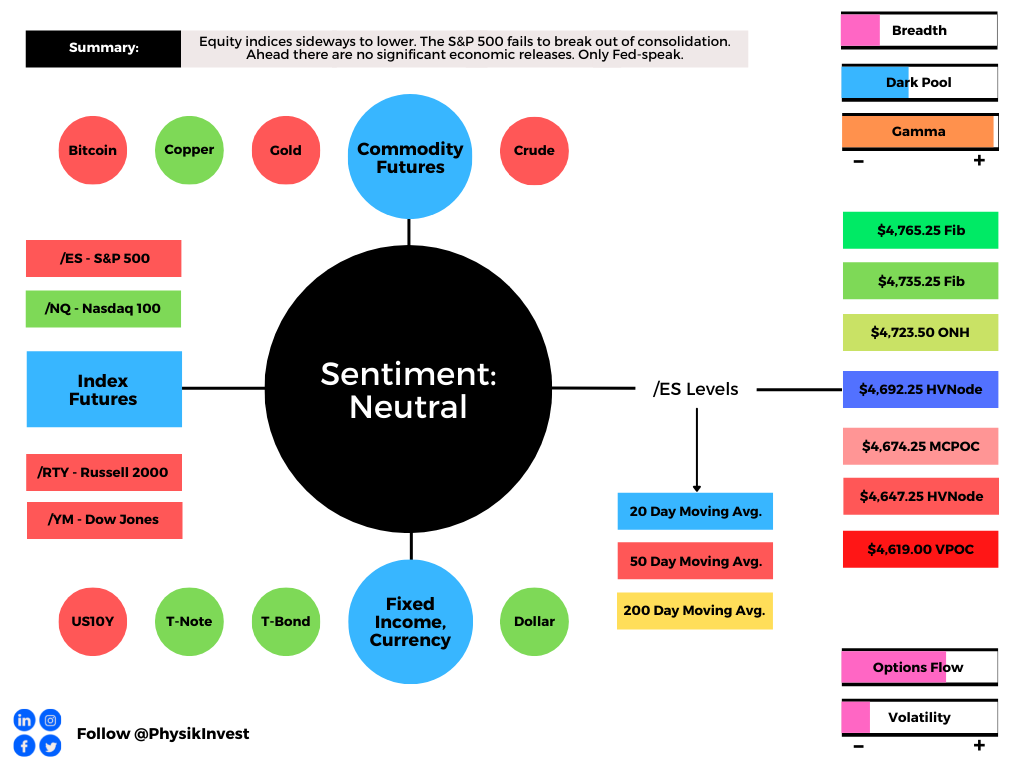

Technical: As of 6:30 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,464.75 low volume area (LVNode) puts in play the $4,499.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,526.25 high volume area (HVNode) and $4,565.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,464.75 LVNode puts in play the $4,438.25 HVNode. Initiative trade beyond the HVNode could reach as low as the $4,409.00 and $4,355.00 VPOC, or lower.

Considerations: Push-and-pull, as well as responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Cave-Fill Process: Widened the area deemed favorable to transact at by an increased share of participants. This is a good development.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Liquidation Breaks: The profile shape suggests participants were “too” long and had poor location.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.