The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

Fundamental

Adding fuel to the fire – dollar strength, crypto bankruptcies, China contagion fears – was a hot consumer price index (CPI) report released Wednesday.

Expected was an 8.8% rise year-over-year (YoY) and 1.1% month-over-month (MoM). Core CPI (which excludes food and energy) was to rise by 5.7% YoY and 0.5% MoM, respectively.

Officially, the headline number rose to 9.1%. The core CPI rose 5.9% YoY and 0.7% MoM, meaning a peak was established in March (6.5% YoY, then).

“Though CPI’s spike is led by energy and food prices, which are largely global problems, prices continue to mount for domestic goods and services, from shelter to autos to apparel,” says Robert Frick of the Navy Federal Credit Union.

Accordingly, expectations regarding the Federal Reserve’s (Fed) response to hot inflation prints have changed. Participants now are pricing an increased potential for a 100 basis point hike in interest rates, something the Bank of Canada implemented, yesterday.

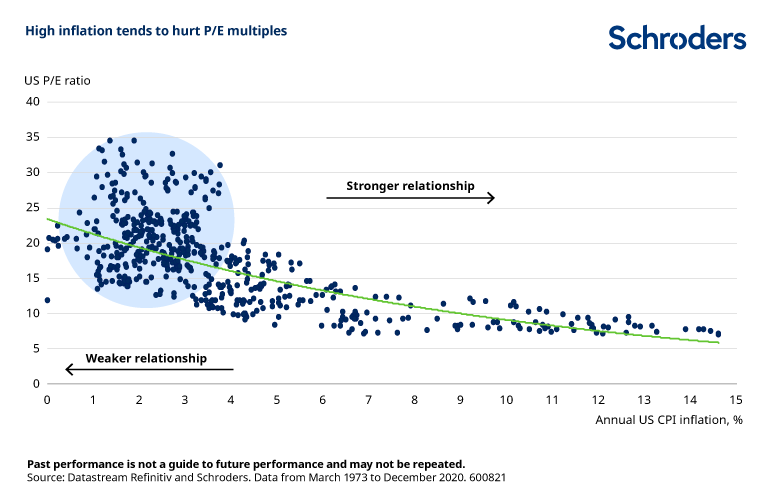

This is a negative for stocks, at the surface. High inflation, and the response to it, tends to hurt multiples (which has been the principal driver of this year’s de-rate, already).

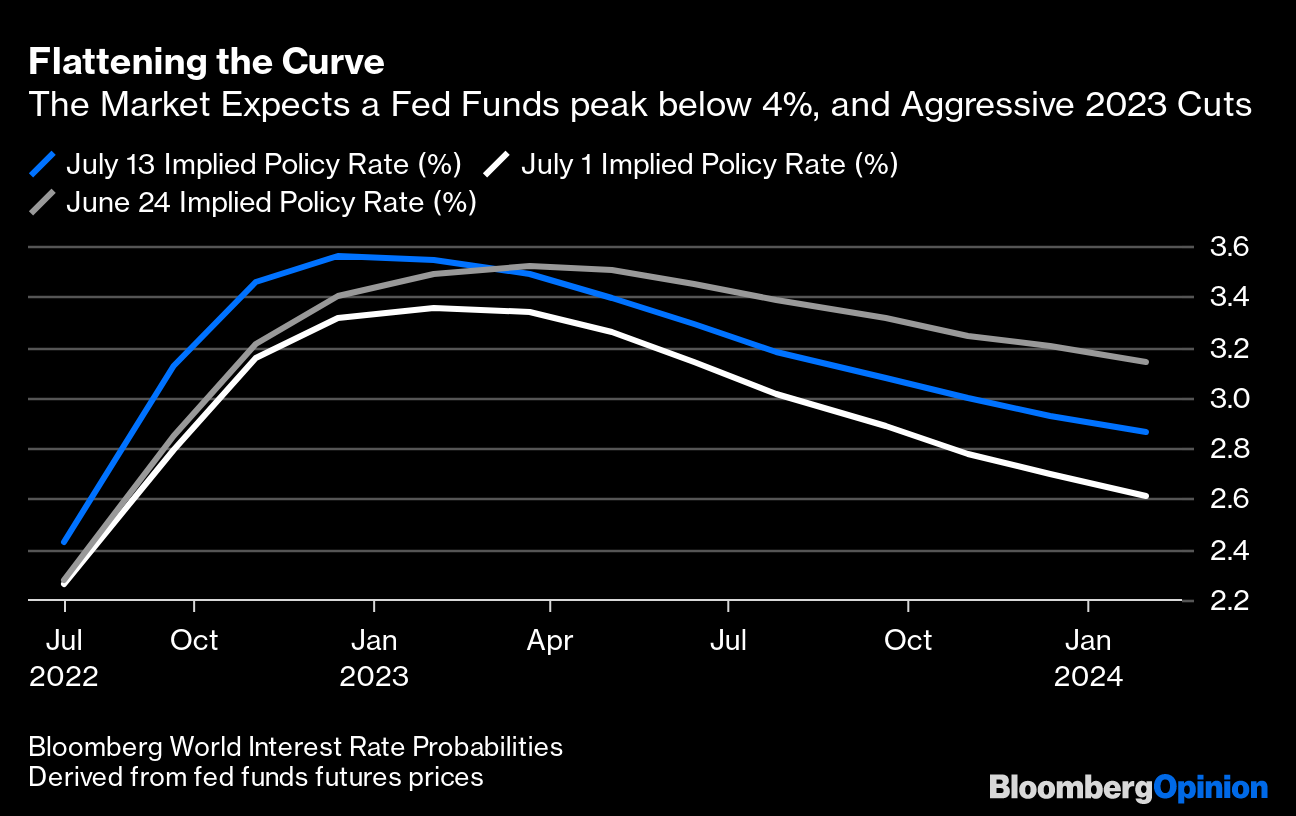

The market expects a Fed Funds peak below 4%, followed by aggressive easing. This is as the Fed’s Beige Book showed signs that inflation is (or soon will be) peaking, amid slowing demand and recession worries.

Positioning

Little change in the dynamics talked about in past letters. Therefore, we continue rolling forward our positioning narratives.

Post-CPI, the market moved lower, first, and higher, later. This was, in part, the result of dealer inventory rebalancing, as Kai Volatility’s Cem Karsan has explained well many times before.

The subsequent move is likely to be “tied to the incremental effects on liquidity (QE/QT).”

Rising inflation probably bolsters the Fed’s backing of a 75 to 100 basis point rate hike. So, don’t fight the Fed. Rising rates and the withdrawal of liquidity, coupled with the impact of inflation and an economic slowing, may prompt continued pressure on equity markets.

Check out The Ambrus Group’s Kris Sidial speak on implied volatility (IVOL) suppression and the implications of a dash for cash (investor exit) and reach for protection.

Technical

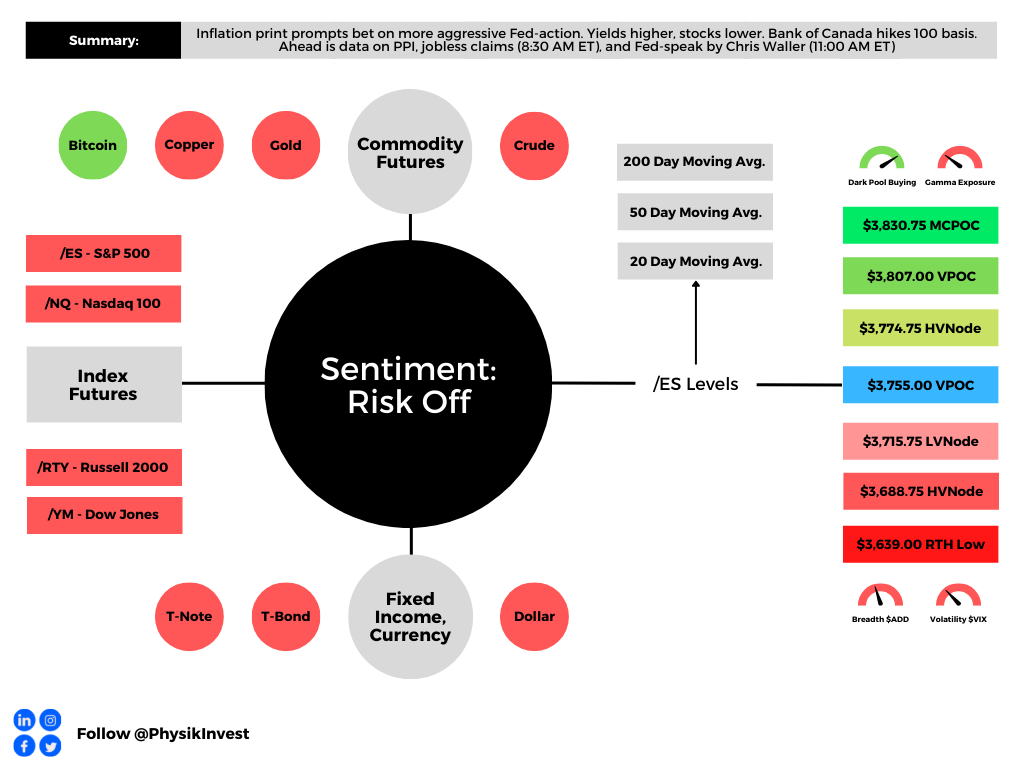

As of 6:45 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a negatively skewed overnight inventory, just beyond prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,755.00 VPOC puts into play the $3,774.75 HVNode. Initiative trade beyond the HVNode could reach as high as the $3,807.00 VPOC and $3,830.75 MCPOC, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,755.00 VPOC puts into play the $3,715.75 LVNode. Initiative trade beyond the LVNode could reach as low as the $3,688.75 HVNode and $3,639.00 RTH Low, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, former Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.