The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

Fundamental

Thanks to all the subscribers who have signed up in the past few days. Not sure how you got here so thank you! Also, thanks to whoever may have shared the letter to make that happen!

From here, you can expect in-depth commentaries on aspects like fundamentals, technicals, and positioning. Insights are actionable as they help me protect and grow my own capital!

Without further delay, below is what you need to know for today!

In the news was Netflix Inc’s (NASDAQ: NFLX) post-earnings jump on better-than-expected subscriber loss numbers, the Russians and Europeans agreeing on gas pipelines, mortgage boycotts spreading across China, tight food supplies, gas prices falling to some of the lowest levels in months, and China warning against a Taiwan visit by the U.S.

View: Earnings calendar.

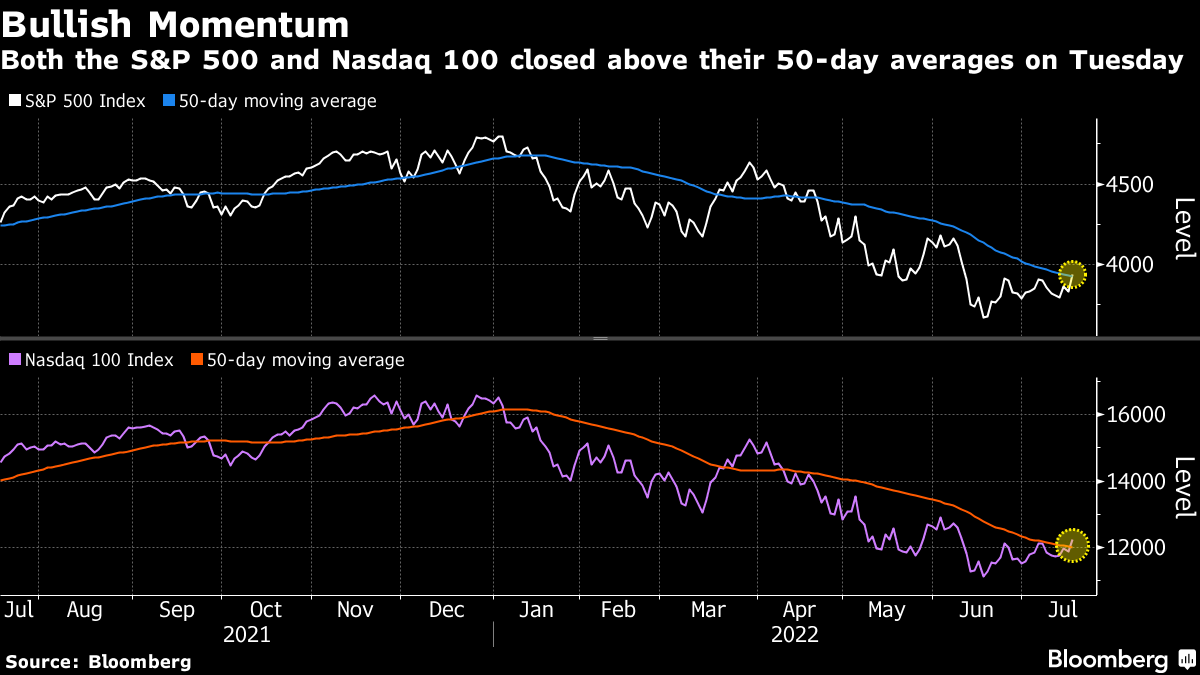

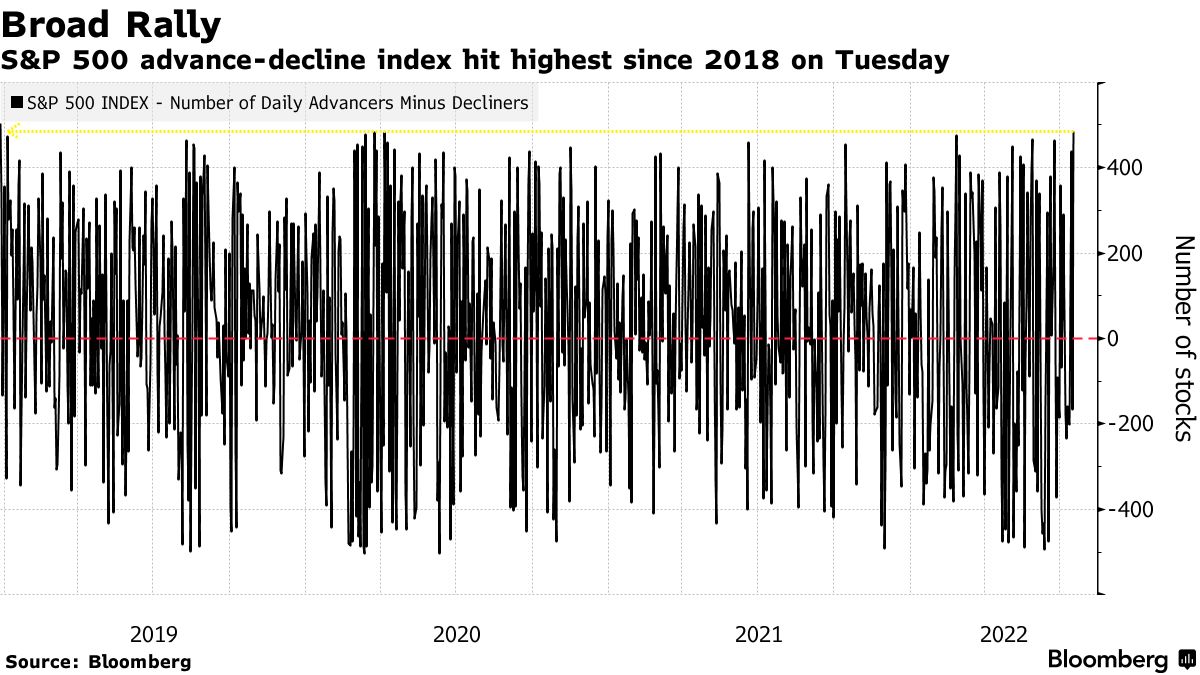

Further, after our July 19 remark on incredibly strong pessimism likely to serve as a contrarian signal, the equity indexes pushed higher, following through key multi-week resistance.

Key levels quoted held nearly to the tick. Now, both the Nasdaq 100 (INDEX: NDX) and S&P 500 (INDEX: SPX) are above their 20- and 50-day moving averages. The Russell 2000, a laggard, made it above the 200-day moving average.

The speed and ferociousness of the rally have more to do with how participants were positioned – in light of what seemed to be a worsening fundamental situation – into the break of some very visual resistances, discussed in prior letters. Read the next section for more on the positioning.

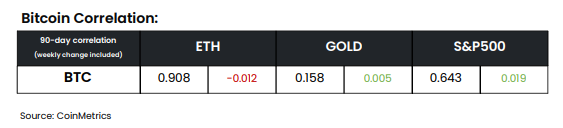

Cryptocurrencies, which were recipients of the same risk-on flows equities saw, too, went higher yesterday. Per CoinMetrics data, Bitcoin’s (CRYPTO: BTC) correlation to equities is positive.

For context, asset volatility had fallen on participants’ extension of moneyness to nonmonetary assets, given easy monetary policies and an environment of ample debt and leverage. These policies made it easier to borrow and make longer-duration bets on ideas with lots of promise.

This had consequences on the real economy and asset prices, accordingly, which rose and kept deflationary pressures at bay. The distinction between economies and financial markets blurred.

When the reverse happens – tighter liquidity and credit – and volatility eventually rises, demand (and competition) for money (or cash) deflates assets (e.g., equities, crypto, and the like).

With U.S. market liquidity, as well as the dollar’s role as a global reserve currency, putting U.S. markets and the S&P 500 at the center of the global carry regime, a U.S. stock market drop is a recession and the direct reflection of the unwinds of carry.

It is the manifestation of a deflationary shock, and today’s sentiment reflects this.

Ultimately, a deflationary pulse manifesting disinflation in consumer prices may prompt the Fed (Federal Reserve) to reverse on rates and quantitative tightening (QT), the (out)flow of capital from capital markets.

Positioning

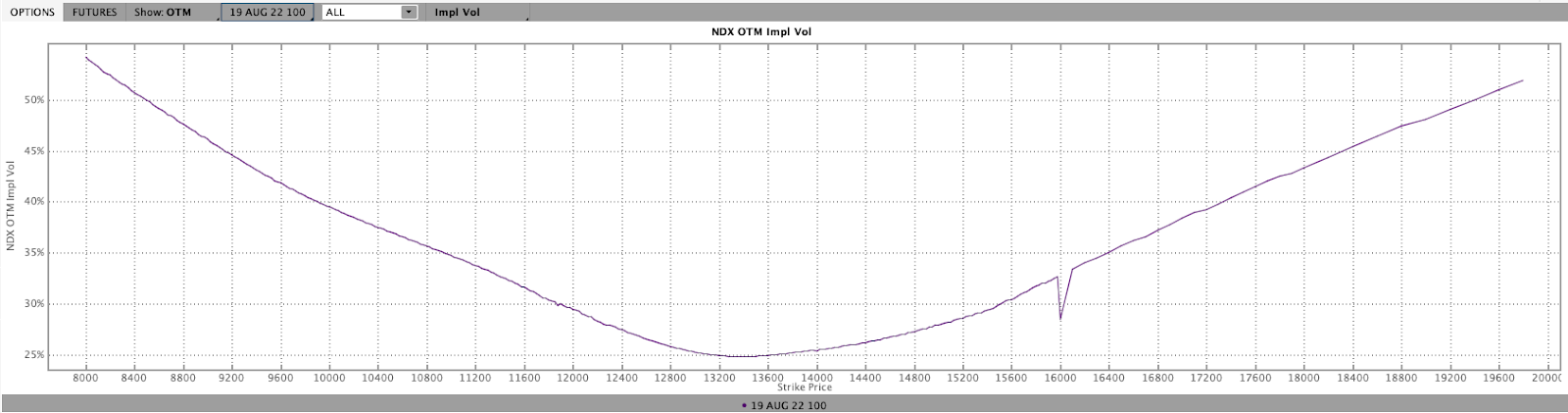

The continued sale of volatility (as long volatility trades have not panned out), particularly across shorter time horizons, left those, on the other side, warehousing long volatility (a sort-of naive thing to say bluntly as we’re discounting customer trades being paired off with each other).

Nonetheless, these liquidity providers’ positions, all else equal, will maintain or increase in value if underlying(s) realize volatility (especially that far in excess of implied). To (re)hedge, those on the other side will do less to add realized (RVOL) volatility and more to suppress implied (IVOL).

Moreover, with RVOL creeping (and exceeding, at times) the IVOL, short volatility structures, particularly if unhedged and across short time horizons, are not doing good. The unwinding of these structures can add fuel to the directional resolve (e.g., if the customer buys back a short call, the liquidity provider sells their long call and buys back their short equity to re-hedge).

Hence, options structures that we said may be good to take advantage of the “smiley” skew (e.g., zero- or low-cost call ratio spreads) are performing much better.

Technical

As of 6:45 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,943.25 HVNode puts into play the $3,982.75 LVNode. Initiative trade beyond the LVNode could reach as high as the $4,016.25 HVNode and $4,055.25 LVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,943.25 HVNode puts into play the $3,909.25 MCPOC. Initiative trade beyond the MCPOC could reach as low as the $3,867.25 LVNode and $3,829.75 MCPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, former Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.