Market Commentary

Key Takeaways: Index futures in balance.

- Best to assume the taper tantrum happened.

- Ahead: Fed speak and data on employment.

- Indices traded sideways-to-higher last week.

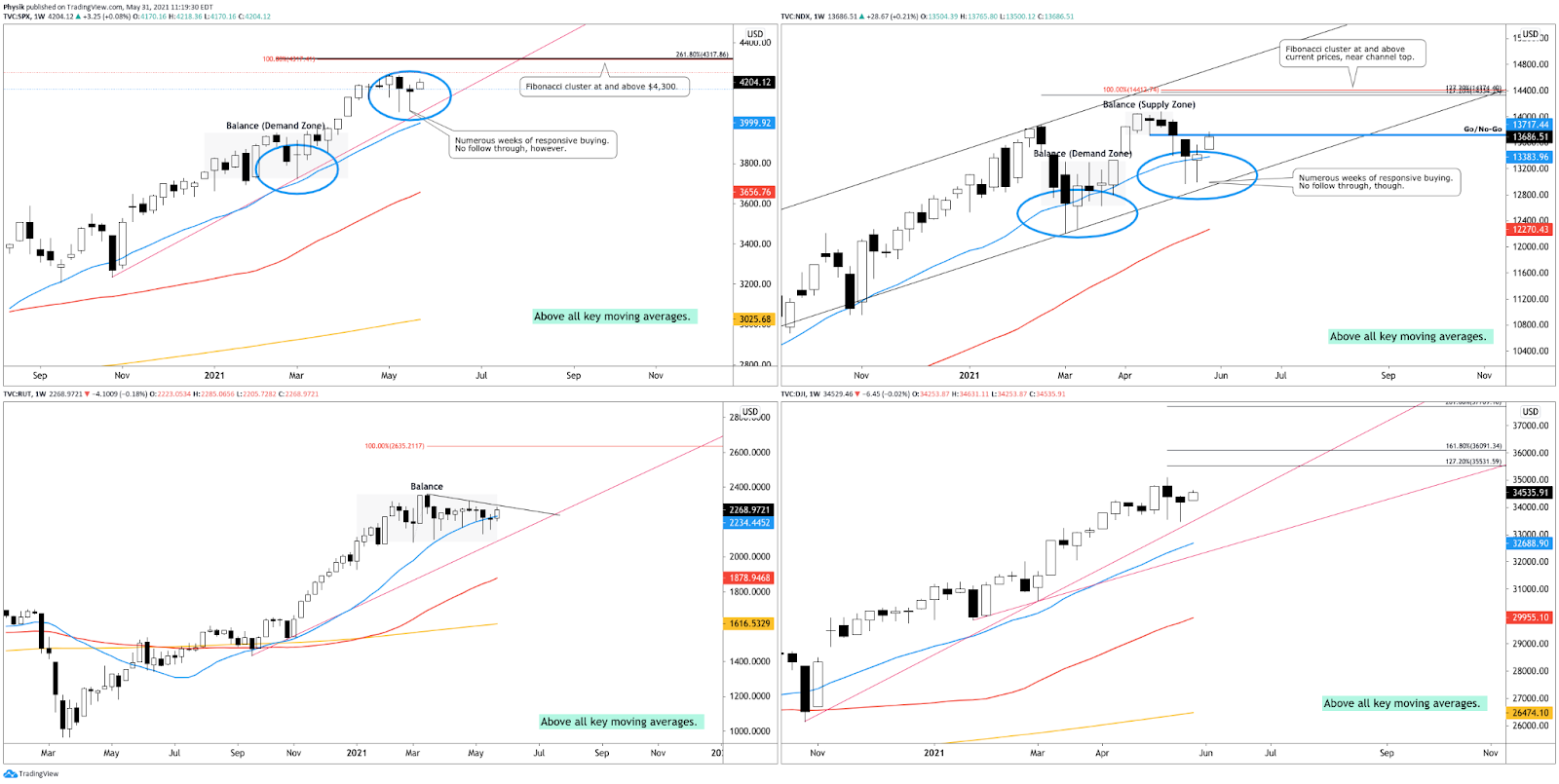

What Happened: Coming into the large May monthly options expiration (OPEX) and extended holiday weekend, U.S. stock index futures pinned, trading sideways-to-higher.

Options: If an option buyer was short (long) stock, he or she would buy a call (put) to hedge upside (downside) exposure. Option buyers can also use options as an efficient way to gain directional exposure. Options Expiration (OPEX): Option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure. Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Furthermore, looking back, the movement in price was both volatile and mechanical.

After a short covering-like rally toward $4,200.00, the S&P 500 was responsively bought and sold at key visual references, suggesting a dominance by short-term participants.

Responsive Buying (Selling): Buying (selling) in response to prices below (above) areas of recent price acceptance.

The technically-driven trade denotes a lack of interest by institutional participants, at record highs; supply chain uncertainties and rising inflation, fiscal and monetary tightening, COVID-19 concerns, political risks, and the like, are some of the emerging concerns larger participants are looking to price in.

Of all the above risks, inflation remains the hottest topic.

Generally speaking, inflation and rates move inversely to each other. Low rates stimulate demand for loans (i.e., borrowing money is more attractive). With the rapid recovery, though, market participants fear that rates will rise to protect the economy from overheating.

Higher rates have the potential to reduce the present value of future earnings, making stocks, especially those that are high growth, less attractive.

To note, however, rates remain range-bound; rates on the 10 Year T-Note sit below their March high and are likely to continue higher, which the market may absorb.

How may the market absorb a rise in rates? During the so-called Taper Tantrum, in the early 2010s, rates settled in a wide range, and equities rallied big. Adding, some strategists, like Kit Juckes of Societe Generale SA (OTC: SCGLY) suggest it may be best to assume a tantrum has already happened.

“U.S. 10-year yields rose from a low of 1.4% in 2012 to 3% during their tantrum. In this cycle, the rise has been from 0.5% to a high just below 1.8%. That’s comparable in relative terms. The eventual peak in U.S. yields in 2018 was 3.25%. Can’t we accept that the taper tantrum has already happened? The important difference is that in the tantrum cycle, core CPI never got above 2 ½%. A bet on further bond weakness is a bet on inflation proving to be stickier than the Fed can cope with.”

Adding, research by JPMorgan Chase & Co (NYSE: JPM), as well as Goldman Sachs Group Inc (NYSE: GS), suggests equities may be getting cheap with reflationary themes being the go-to play. This sentiment would help explain the increased interest in S&P 500 and Nasdaq 100 call options.

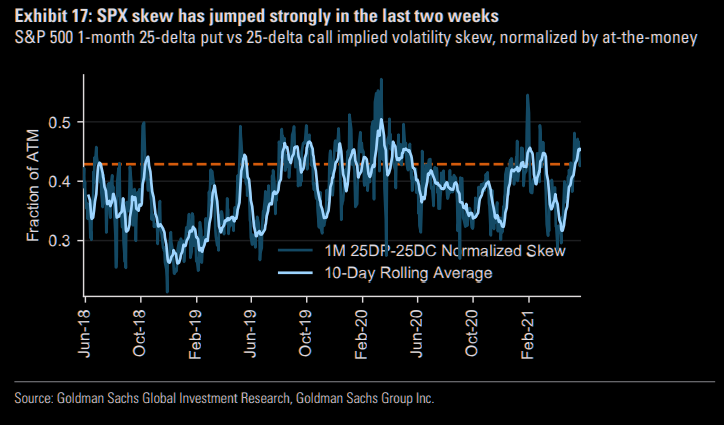

Outlier risks remain, though; aside from the seasonally weak period, S&P 500 skew – a measure of perceived tail risk and the chances of a black swan event – rose dramatically over the past few weeks. At the same time, sentiment cooled considerably, while individual stock volatility increased the potential for a repeat of the GameStop Corporation (NYSE: GME) de-risking event.

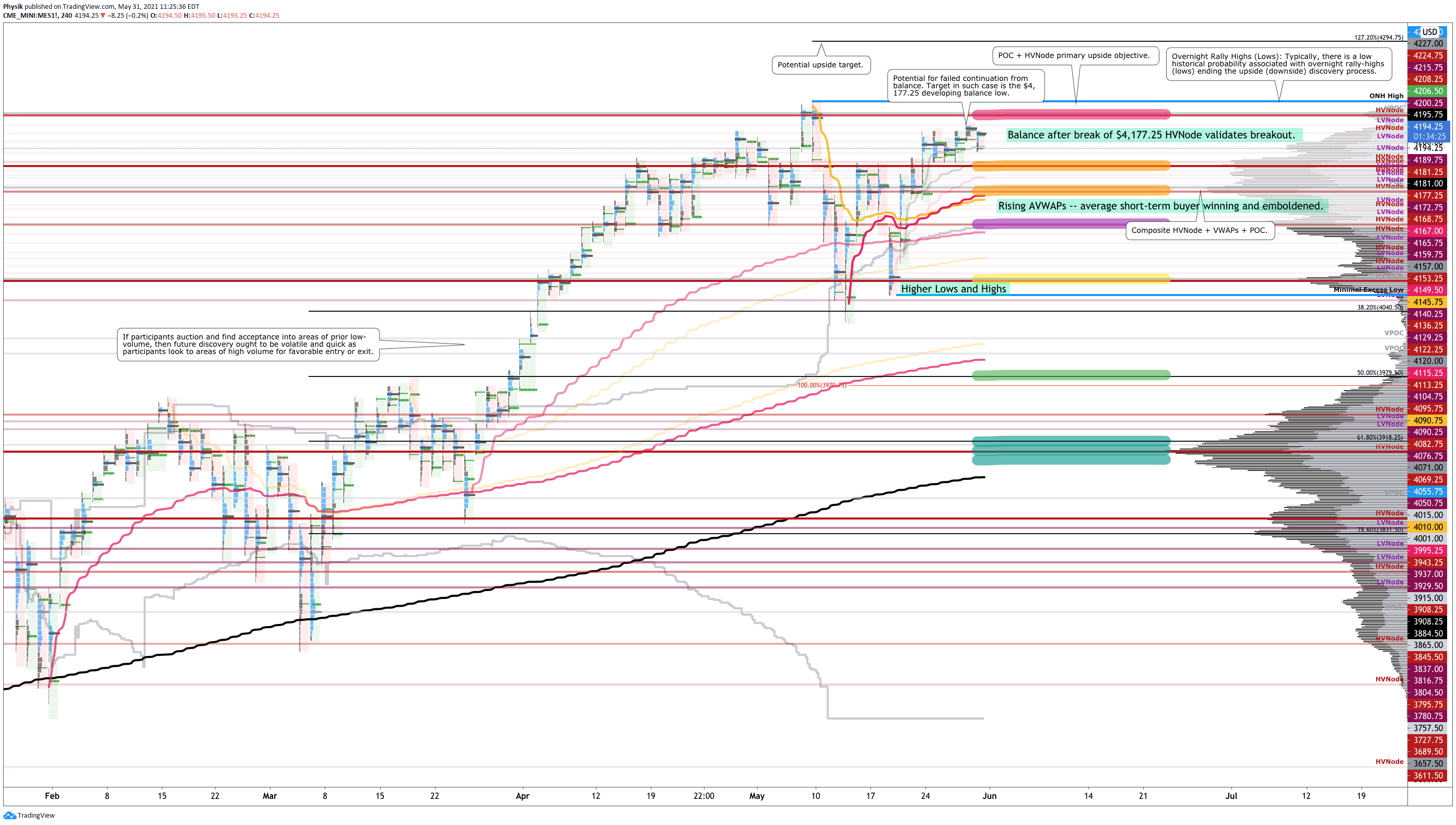

What To Expect: In the coming sessions, participants will want to focus their attention on where the S&P 500 trades in relation to the $4,197.25 high volume area (HVNode).

Volume Areas: A structurally sound market will build on past areas of high volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low volume, then future discovery ought to be volatile and quick as participants look to areas of high volume for favorable entry or exit.

That said, participants can trade from the following frameworks.

In the best case, the index trades sideways or higher; activity above $4,197.25 has the potential to reach the $4,227.00 point of control (POC). Initiative trade beyond the POC could reach as high as first the $4,238.00 overnight all-time high (ONH) and then, the $4,294.75 Fibonacci-derived price extension, a typical recovery target.

POCs: POCs (like HVNodes described above) are valuable as they denote areas where two-sided trade was most prevalent. Participants will respond to future tests of value as they offer favorable entry and exit. Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

In the worst case, the index trades lower; activity below the $4,177.25 HVNode puts in play the $4,153.25 HVNode, first. Thereafter, if lower, the $4,122.25 HVNode and $4,071.00 POC come into play.

On a cross through the $4,050.75 low volume area (LVNode), long-biased traders should beware of a rapid liquidation, as low as first the $4,015.00 and $4,001.00 POCs. In such a liquidation, odds favor a test of ~$3,970.00 50.00% retracement, as well as the $3,918.00 61.80% retracement and HVNode.

News And Analysis

Trade | One of the world’s top ports expects delays on an outbreak. (BBG)

Markets | PBOC raises reserve ratio for foreign exchange holdings. (BBG)

Economy | Recovery solidifies in U.S., Europe, while EM faces risks. (Moody’s)

Markets | China bars banks from selling commodity-linked products. (REU)

Economy | Fed security purchases draw fire in hot U.S. housing market. (S&P)

Energy | Global oil demand is seen eclipsing India, Iran’s uncertainty. (S&P)

Economy | U.S. won’t experience stagflation over next few years. (Moody’s)

Economy | Non-government loans seeing a jump in forbearances. (MND)

Economy | U.S. speculative-grade corporate default rate to fall to 4%. (S&P)

Markets | Inflation, higher oil, stronger yuan point in same direction. (BBG)

Economy | U.S. retailers face headwinds from slowing sales, inflation. (S&P)

Markets | Everyone with bonds to liquidate had ample time to do so. (BBG)

What People Are Saying

Innovation And Emerging Trends

Markets | How recent growth in leveraged finance affects investors. (BZ)

Politics | Tech growth overshadowed by regulatory risks, challenges. (S&P)

Markets | Chamath: SPACs need more oversight and regulation. (BBG)

Politics | China moves to a three-child policy to boost its birthrate. (BBG)

Markets | Shakeout stirs debate over ether’s long-term potential. (BBG)

FinTech | Which banks are positioned for low rates, digital adoption. (S&P)

About

Renato founded Physik Invest after going through years of self-education, strategy development, and trial-and-error. His work reporting in the finance and technology space, interviewing leaders such as John Chambers, founder, and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others, afforded him the perspective and know-how very few come by.

Having worked in engineering and majored in economics, Renato is very detailed and analytical. His approach to the markets isn’t built on hope or guessing. Instead, he leverages the unique dynamics of time and volatility to efficiently act on opportunity.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.