Key Takeaways:

- March dips prior to bullish April.

- World GDP forecasts revised up.

- Manufacturing sentiment soars.

- Risk appetite elevated, but lower.

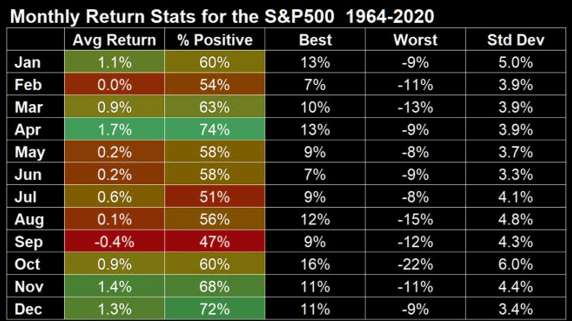

- Historical Perspective: Economy.

- $1.1T in student debt still paused.

- Consumers spend 40% stimulus.

- Delinquency rates are near highs.

- Financial conditions tighten up.

- Retail tempered its bullishness.

- $2T infrastructure plan unveiled.

- 1970s-like inflation very unlikely.

- Hedge funds not that levered up.

What Happened: U.S. stock index futures closed higher, last week.

What Does It Mean: The S&P 500 closed above $4,000.00 for the first time.

This comes as investors shifted their focus from the risks of rapidly rising inflation to the increasing pace of COVID-19 coronavirus vaccinations and a rebound in economic activity.

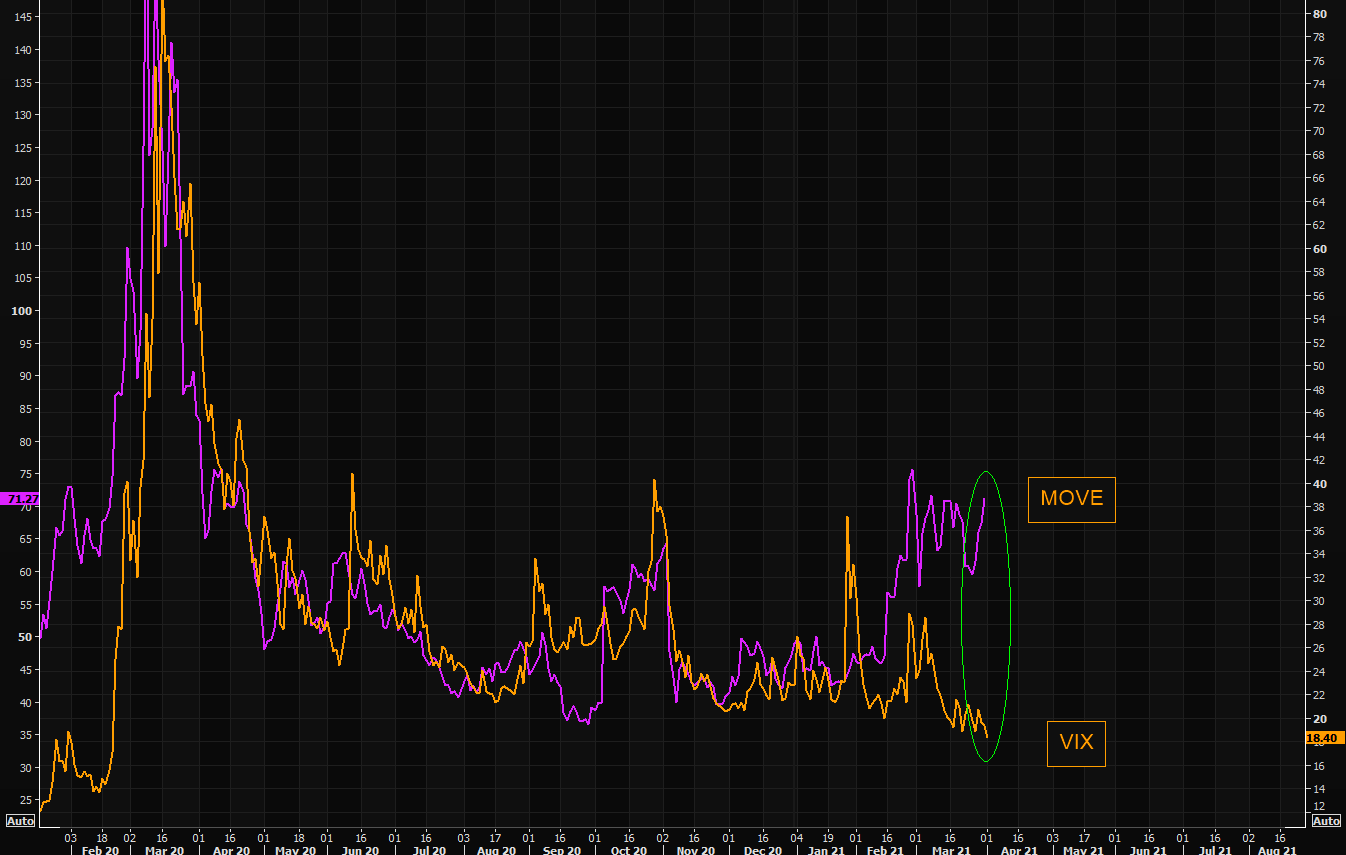

At the time, the CBOE Volatility Index (INDEX: VIX), a measure of the stock market’s expectation of volatility based on S&P 500 (INDEX: SPX) options, hit the lowest level since February of 2020. This was likely the result of an oversupply in volatility due to contract rolling, signaling a shift in the demand for volatility and options-based hedging.

Adding, the market is entering into a historically bullish period, ahead of the upcoming corporate earnings season, with structural flows supporting the ongoing narrative, also, at least until mid-April. The reason being, most funds are committed to holding long positions. In the interest of lower volatility returns, these funds will collar off their positions, selling calls to finance the purchase of downside put protection.

As a result of this activity, options dealers are long upside and short downside protection.

This exposure must be hedged; dealers will sell into strength as their call (put) positions gain (lose) value and buy into weakness as their call (put) positions lose (gain) value.

Now, unlike theory suggests, dealers will hedge call losses (gains) quicker (slower). This leads to “long-gamma,” a dynamic that crushes volatility and promotes momentum, observed by lengthy sprints — like the one the market is currently in — followed by rapid de-risking events as the market transitions into “short-gamma.”

What To Expect: Balance-to-higher into mid-April.

Why? One last hurrah before the reopening accelerates and flows turn.

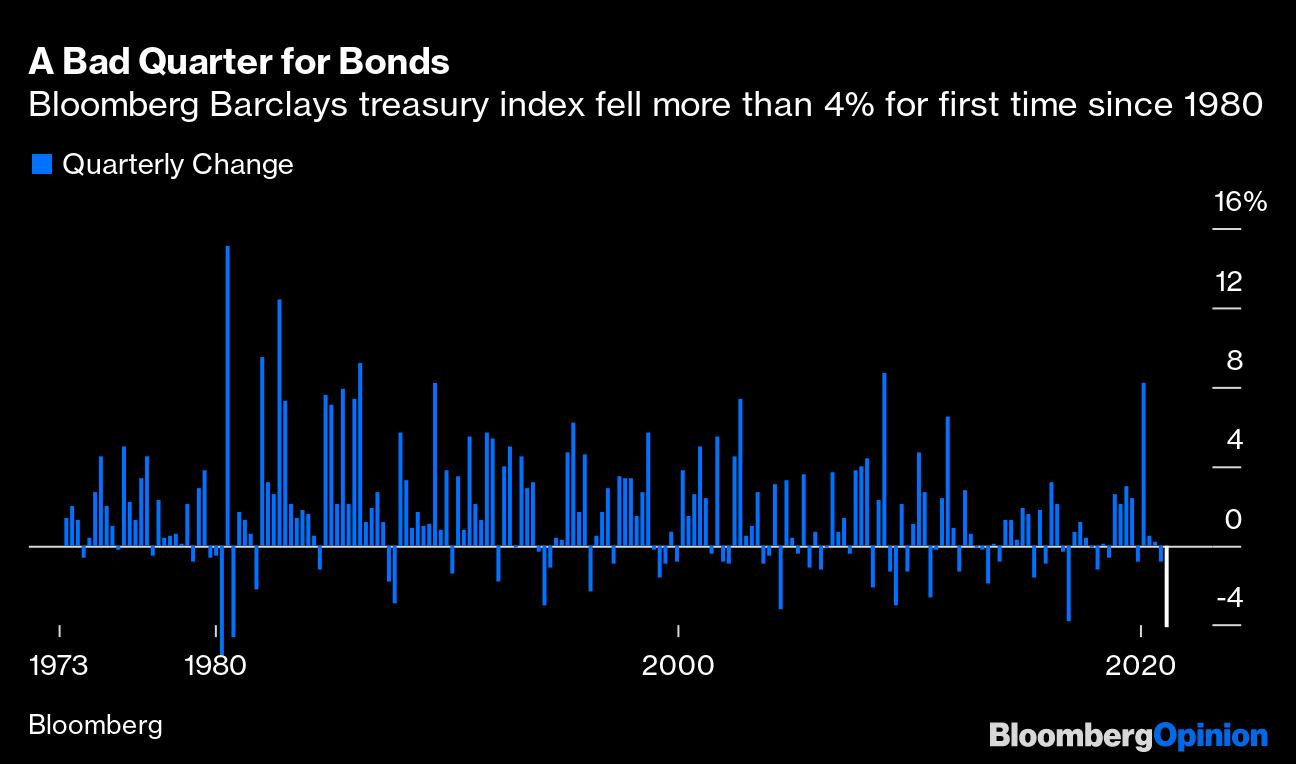

When flows turn, it is likely that equity and bond market volatility converge; the ongoing divergence comes alongside an attempt, by market participants, to price in rising debt levels and inflation. As consumers shift their preferences from saving and investing to spending, this divergence ought to disappear.

Adding, metrics, like DIX, confirm increased buying pressure while divergences in options activity and volume delta suggest opportunistic selling.

More On DIX: For every buyer is a seller (usually a market maker). Using DIX — which is derived from short sales (i.e., liquidity provision on the market-making side) — we can measure buying pressure. Volume Delta: Buying and selling power as calculated by the difference in volume traded at the bid and offer.

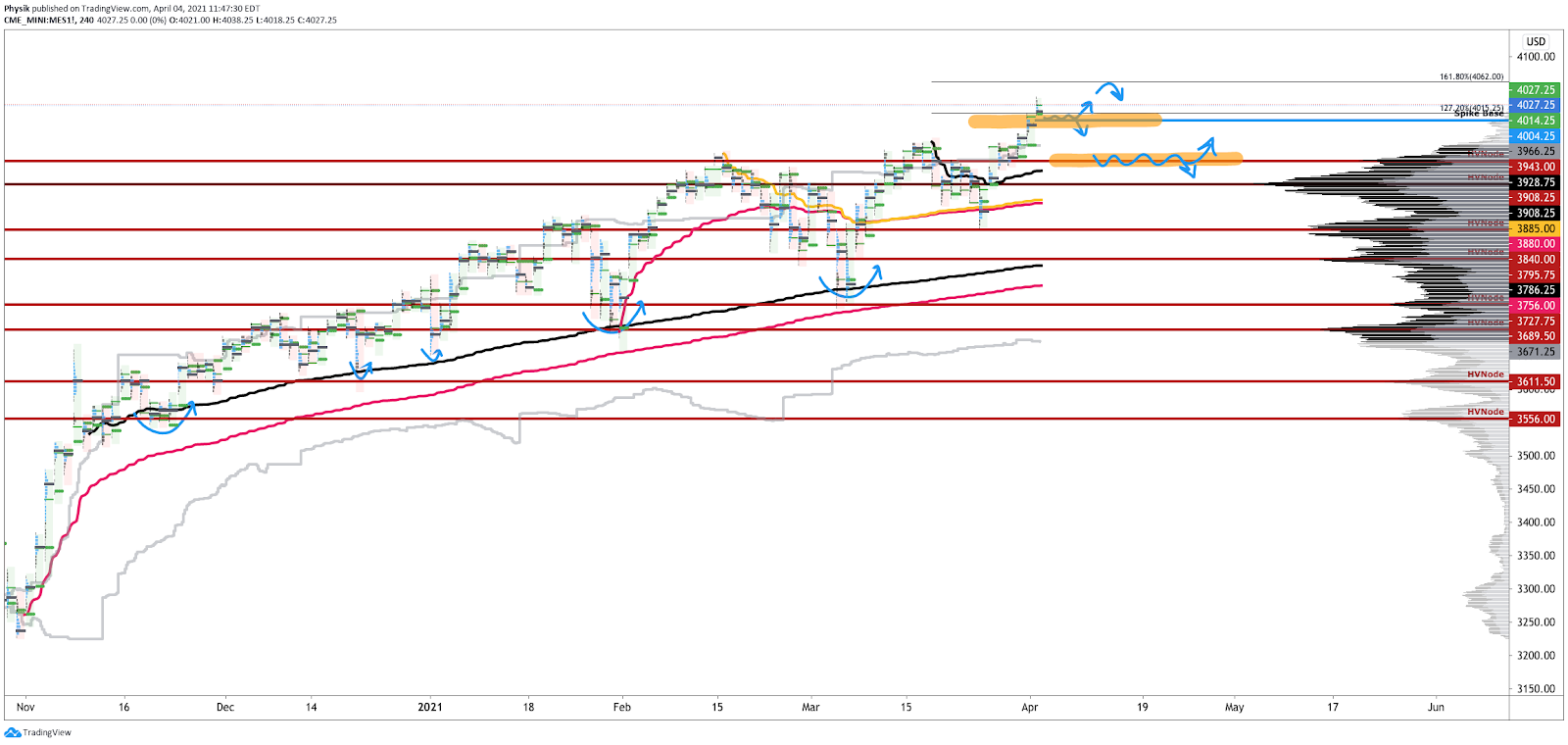

What To Do: In the coming sessions, participants will want to pay attention to where the S&P 500 trades in relation to Thursday’s end-of-day spike higher.

More On Spikes: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

In the best case, the S&P 500 remains above the $4,004.25 spike base. Doing so means that the participants are finding higher prices, above the VWAP anchored from the March 17 rally-high, valuable (i.e., buyers, on average, are in control and winning since the March 17 rally-high).

More On Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

In the case of higher prices, given that the $4,015.25 price extension was achieved in after-market trade that established an overnight high at $4,038.25, participants can target the $4,062.00 extension.

More On Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Any activity below the $4,004.25 spike base puts the rally on hold and calls for balance or digestion of higher prices.

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance-areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

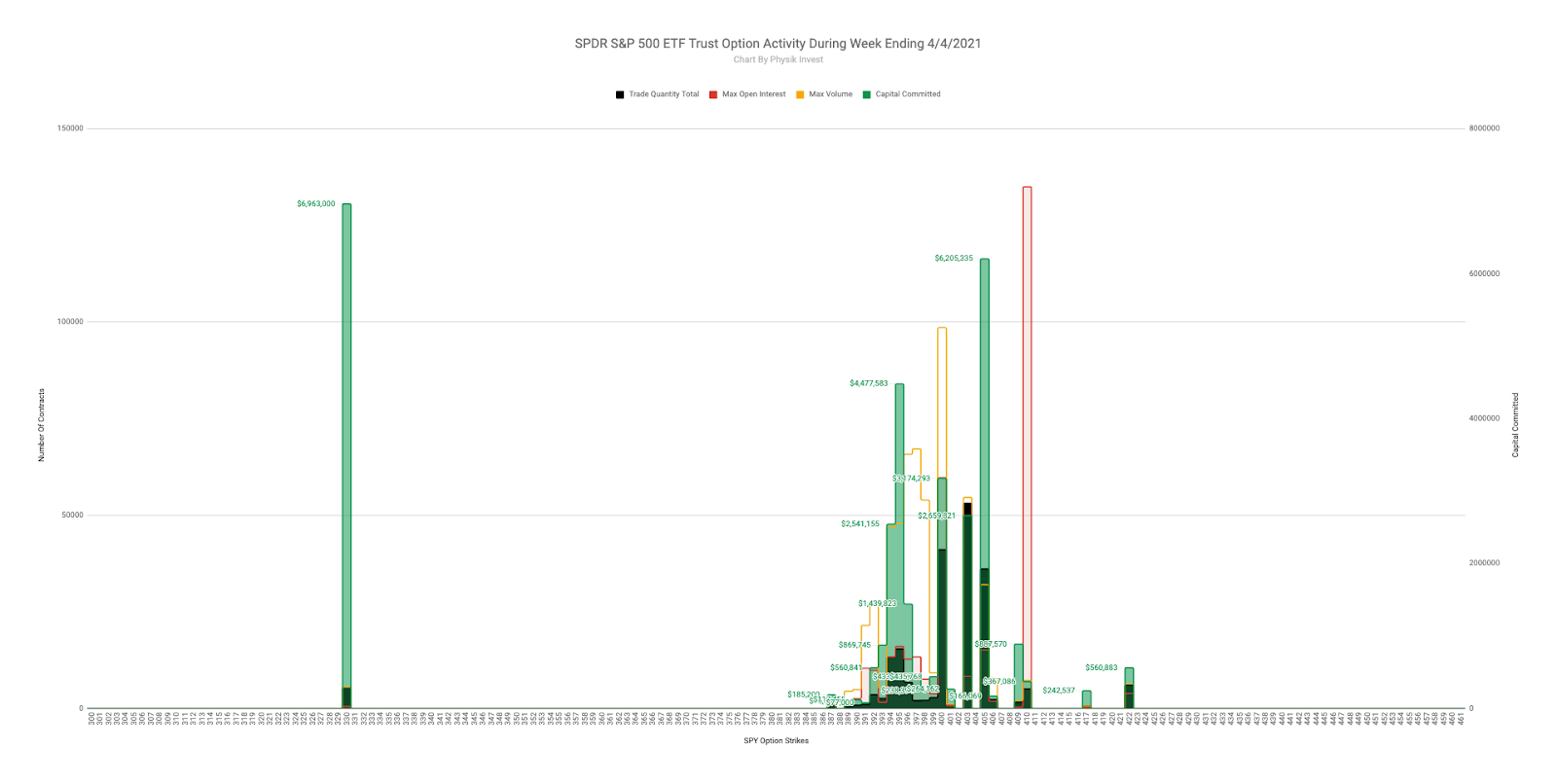

In the case of lower prices, participants can look to whether a test of the $3,943.00 and $3,908.25 high-volume areas (HVNodes) solicit a response.

More On Volume Areas: A structurally sound market will build on past areas of high-volume (HVNode). Should the market trend for long periods of time, it will lack sound structure (identified as a low-volume area (LVNode) which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low-volume, then future discovery ought to be volatile and quick as participants look to areas of high volume for favorable entry or exit.

Conclusions: The go/no-go level for next week’s trade is $4,004.25.

Any activity above this level confirms the bullishness of last Thursday’s end-of-day spike.

Levels Of Interest: $4,004.25 Spike Base.

Cover photo by Taryn Elliott from Pexels.