Notice: Physik Invest’s daily market commentaries will be suspended for the next five regular trading sessions or February 22-26.

Please accept our apologies for the inconvenience and thank you for the support!

Key Takeaways:

- Debt, inflation threatening low-rate regime.

- Markets most complacent in two decades.

- Sentiment turns hot from hotter amid slide.

- Global equity fund net inflows decelerated.

- Markets fret about economic performance.

- Retail sales and industrial production gain.

What Happened: U.S. stock index futures auctioned lower last week.

What Does It Mean: Market participants witnessed a rapid de-risking event, as a result of individual stock volatility, and a subsequent v-pattern recovery, that was later taken back as Friday’s large February monthly options expiration (OPEX) neared.

More On The V-Pattern: A pattern that forms after a market establishes a high, retests some support, and then breaks above said high. In most cases, this pattern portends continuation.

At the same time, bond and equity market volatility diverged, materially.

In other words, a rapid move up in rates — as investors become increasingly concerned over the value of their bonds due to rising debt levels and inflation — has yet to be priced in as an equity market risk.

Adding, the risk of inflation comes alongside a potential for slowing in economic growth, which may have knock-on effects, such as savers protecting their capital by investing in non-productive assets, thus helping form speculative asset bubbles.

Risk Of Monetary Support: The increased moneyness of financial markets; investors look to exchange-traded products (e.g., S&P 500) as savings vehicles, thereby forcing participants, like the Federal Reserve, to backstop market liquidity, and promote market and economic stability in times of turmoil.

Still, as Bloomberg suggests, reasons to not panic include an overreaction by market participants, premature Fed tightening, and a risk asset rout (i.e., rising rates may eventually increase demand for safety assets).

“Typically it’s a good environment for risk assets. Neither the pace nor the extent of the move so far has been unusual relative to other historical moves coming out of a recession,” said Pimco’s Erin Browne. “It would take a significant move in real yields in order to disrupt risk markets broadly.”

Moving on, given OPEX, participants have a clue as to why the market failed to resolve directionally over the past week: option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure.

Aside from OPEX, we must talk more about the v-pattern recovery and a prior week’s spike exit from balance, as well as low broad market volatility.

In light of the v-pattern, balance, and spike, the S&P 500’s long-term uptrend remains intact. In support of this uptrend, systematic and hedge fund participants are increasing their long-exposure, given the economic recovery, and a drop in volatility.

Beyond that, speculative activity in the options market and measures of market liquidity fail in offering much information.

SPY Market Liquidity

QQQ Market Liquidity

IWM Market Liquidity

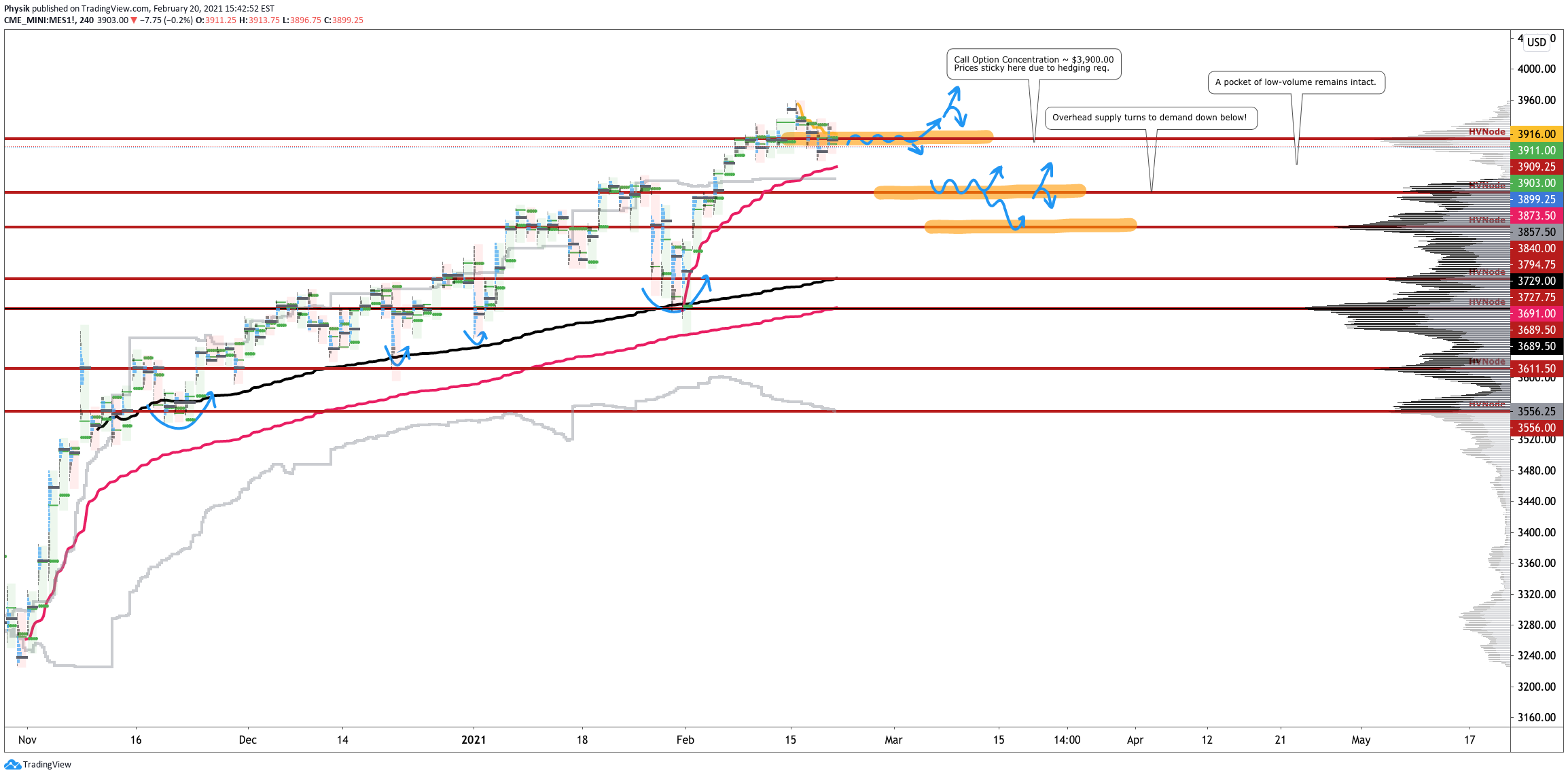

What To Expect: U.S. stock indexes are positioned for directional resolve.

This comes alongside the acceptance of higher prices (inside a prominent high-volume area, or HVNode) and an overnight rally-high at $3,959.25.

More On Overnight Rally Highs: Typically, there is a low historical probability associated with overnight rally-highs ending the upside discovery process. More On Volume Areas: A structurally sound market will build on past areas of high-volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low-volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low-volume, then future discovery ought to be volatile and quick as participants look to areas of high-volume for favorable entry or exit.

What To Do: In the coming sessions, participants will want to pay attention to the VWAP anchored from the $3,959.25 peak and $3,909.25 HVNode.

Volume-Weighted Average Prices (VWAPs): Metrics highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

In the best case, the S&P 500 opens and remains above the $3,909.25 volume area.

Additionally, auctioning above the $3,915.00 VWAP would suggest buyers, on average, are in control and winning, since the February 15 rally high.

Auctioning beneath $3,909.25 turns the HVNode, nearby, into an area of supply, offering initiative sellers favorable entry and responsive buyers favorable exit.

The situation would drastically deteriorate with trade beneath the $3,880.00 HVNode, the last reference before participants find acceptance in an area of low-volume.

In such scenario, future discovery ought to be volatile and quick as participants repair some of the poor structures left in the wake of a prior advance, and look to the next area of high-volume (i.e., $3,830.75) for favorable entry and exit.

Conclusions: The go/no-go level for next week’s trade is $3,909.25.

Any activity at this level suggests market participants are looking for more information to base their next move. Anything above (below) this level increases the potential for higher (lower).

Levels Of Interest: $3,909.25 HVNode.

Photo by Charles Parker from Pexels.

2 replies on “Market Commentary For The Week Ahead: ‘Should I Stay Or Should I Go’”

[…] Outlier risks remain, though; aside from the seasonally weak period, S&P 500 skew – a measure of perceived tail risk and the chances of a black swan event – rose dramatically over the past few weeks. At the same time, sentiment cooled considerably, while individual stock volatility increased the potential for a repeat of the GameStop Corporation (NYSE: GME) de-risking event. […]

[…] Aside from the Fed meeting and OPEX, some outlier risks remain; with VIX spreads at their lows, S&P 500 skew – a measure of perceived tail risk and the chances of a black swan event – rose dramatically over the past few weeks. At the same time, sentiment cooled considerably, while individual stock volatility increased the potential for another meme stock de-risking event. […]