The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 800+ that read this report daily, below!

Fundamental

The Daily Brief for Monday, August 15, 2022, provided us with a great start to the week. Today, unfortunately, we add only lightly to this narrative, and we will elaborate in later sessions.

In short, markets experienced one of the largest, wide-ranging, short-covering rallies, in years, bolstered by machines “hell-bent on pushing the financial conditions easing trade,” as well put by Dennis DeBusschere, the founder of 22V Research.

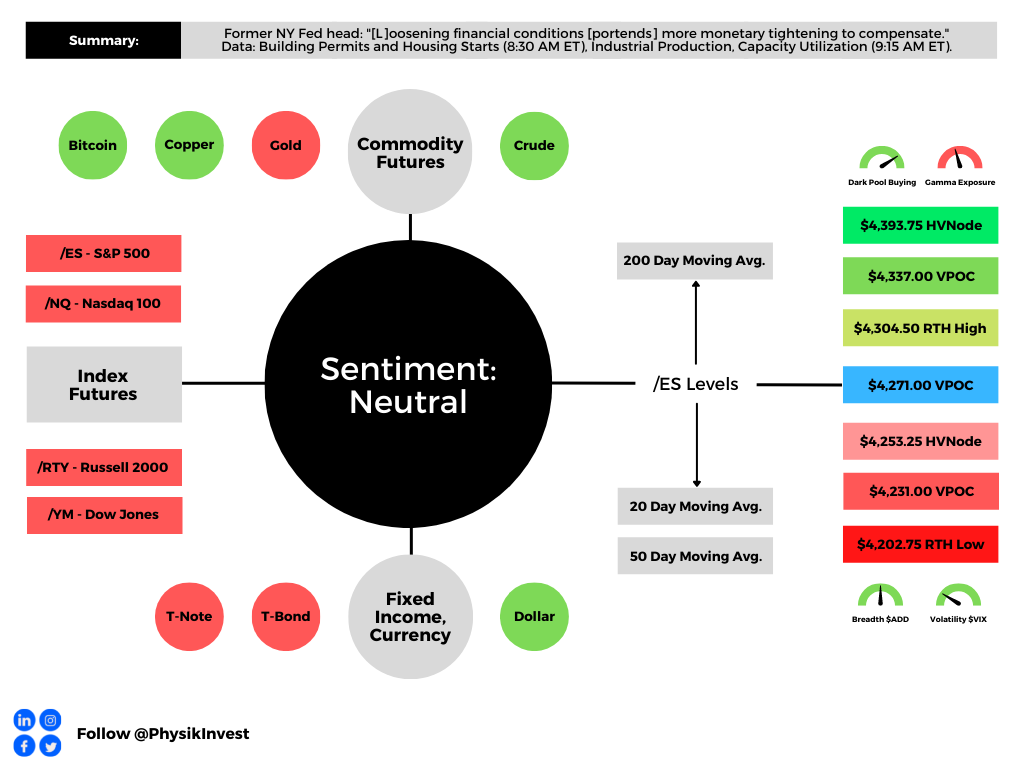

Notwithstanding improving sentiment and data on jobs, as well as cooler inflation figures, former New York Federal Reserve (Fed) President William Dudley, thinks markets have underestimated the Fed’s determination to stem inflation.

To summarize, the Fed will keep hiking until inflation is back to its 2% target and there is more slack in the labor market.

“I think the Fed is going to be higher for longer than what market participants understand at this point,” he explained. This action ought to last at least until the unemployment rate is “well above 4%,” above today’s 3.5%.

Accordingly, “whenever the unemployment rate has risen by a half percentage point or more, the result has been a full-blown recession.”

There is also quantitative tightening (QT), the direct flow of capital from capital markets.

Bank of America Corporation (NYSE: BAC) strategists see the prevailing assumption as if “QT is already priced into the market.”

“The market does not seem to be looking ahead,” the strategists said, suggesting the S&P 500 could print 7% lower, at least. “If financial conditions tighten in a meaningful way, then that could make QT a more important topic.”

Still, Treasury buybacks are among the tools that could be used to strengthen markets against the rising tide of “issuance and potential structural inflation, … [easing] QT by moving liquidity out of the RRP and into the banking sector,” per Joseph Wang.

Positioning

Please refer to our detailed Daily Brief for August 12, 2022. We shall add to this narrative in the coming sessions.

Technical

As of 7:00 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

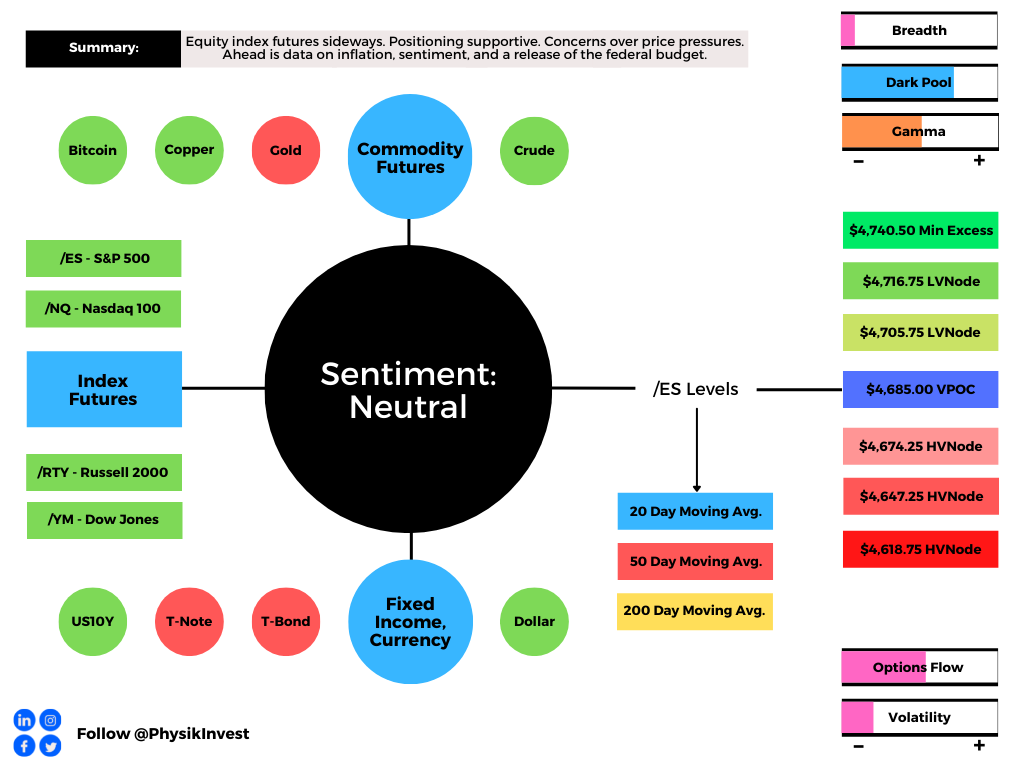

Any activity above the $4,271.00 VPOC puts into play the $4,304.50 RTH High. Initiative trade beyond the RTH High could reach as high as the $4,337.00 VPOC and $4,393.75 HVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $4,271.00 VPOC puts into play the $4,253.25 HVNode. Initiative trade beyond the HVNode could reach as low as the $4,231.00 VPOC and $4,202.75 RTH Low, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.