Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Administrative

A shorter letter today, so there may be some holes we patch later. Take care!

Fundamental

The Federal Reserve (Fed) bumped its target rate up 25 basis points to 4.75-5.00% and opened the door to more hikes, barring market-induced financial tightening, as this letter put forward yesterday morning.

“The events in the banking system over the past two weeks are likely to result in tighter credit conditions for households and businesses, which would, in turn, affect economic outcomes,” Fed chair Jerome Powell commented, adding that credit tightening significantly means monetary policy “may have less work to do.”

Further, before the recent collapses of a few financial institutions, including SVB Financial Group, the market was pricing a 50 basis point hike.

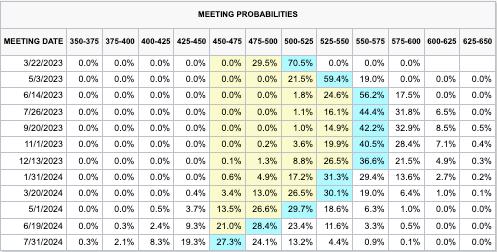

The below CME Group Inc’s (NASDAQ: CME) FedWatch Tool shows the market’s expectations on March 8. Note the 5.50-5.75% terminal (peak) rate.

“Absent SVB, the Fed would have likely raised 50 basis points,” TS Lombard’s Steve Blitz said. “SVB did happen, however, and so this FOMC, ever anxious about facing a recession (rising unemployment), is more than happy to let ‘tighter credit conditions for households and businesses … weigh on economic activity, hiring, and inflation.’ As for financial instability, they believe they have the tools to keep a few poorly managed banks from imploding the whole sector.”

The updated summary of economic projections (SEP) or dot plot shows the FOMC expecting rates to end 2023 above 5.00%.

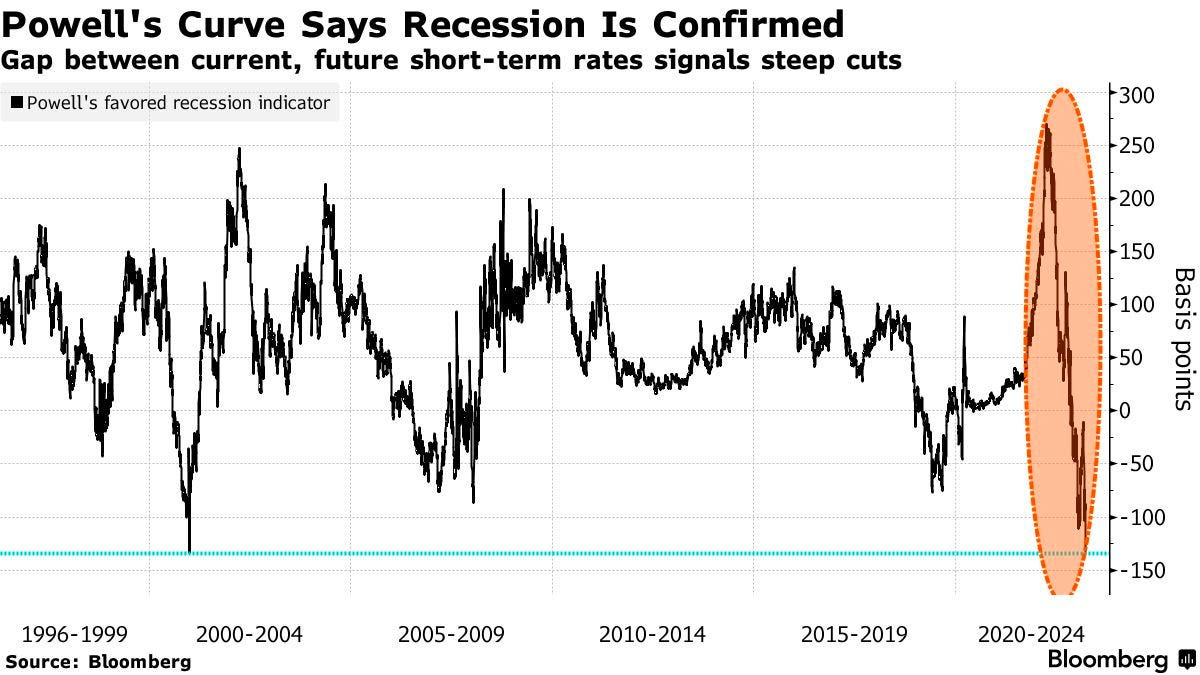

This is far higher than what the markets are pricing. Powell’s go-to measure for spotting economic troubles suggests steep cuts are also coming sooner than later.

Anyways, given that what was expected happened, markets responded positively. If interested in why that is the case following important events as of late, see the Daily Brief for 2/1 and 2/2.

It was Treasury secretary Janet Yellen who took the market lower. Yellen said she has “not considered or discussed anything having to do with blanket insurance of guarantees of deposits,” and markets did not like that.

The likes of Pershing Square’s Bill Ackman responded he “would be surprised if deposit outflows don’t accelerate.” Adding, Federated Hermes’ Steve Chiavarone thought it was “astounding” Yellen and Powell would give contradictory messages.

“Powell essentially said that all deposits are safe; Yellen said, ‘Hold my beer.’ You would have thought that they would have coordinated,” responded Federated Hermes’ Steve Chiavarone.

To keep it brief, we’ll end with references to letters for 3/20 and 3/21, noting that the conditions for weak equity markets are present. The S&P 500 forward earnings are declining, the yield curve is inverted, unemployment is below average, manufacturing PMIs are below 50, and 40% of banks are tightening lending, Morgan Stanley (NYSE: MS) strategists explain.

Technical

As of 8:55 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET) in the S&P 500 will likely open in the middle part of a positively skewed overnight inventory inside the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $3,994.25.

Key levels to the upside include $4,004.25, $4,017.00, and $4,026.75.

Key levels to the downside include $3,977.00, $3,959.25, and $3,946.75.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold, barring an exogenous development.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for some time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future value tests as they offer favorable entry and exit.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

Separately, Capelj is an accredited journalist with past works including interviews with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, North Dakota Governor Doug Burgum, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Connect

Direct queries to renato@physikinvest.com. Find Physik Invest on Twitter, LinkedIn, Facebook, and Instagram. Find Capelj on Twitter, LinkedIn, and Instagram. Only follow the verified profiles.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.