What Happened

Overnight, equity index futures sideways to higher with bonds. Commodities were mixed.

The purported catalysts include corporate earnings overshadowing fears of hot U.S. inflation.

Ahead is data on the Empire State Manufacturing Index (8:30 AM ET).

What To Expect

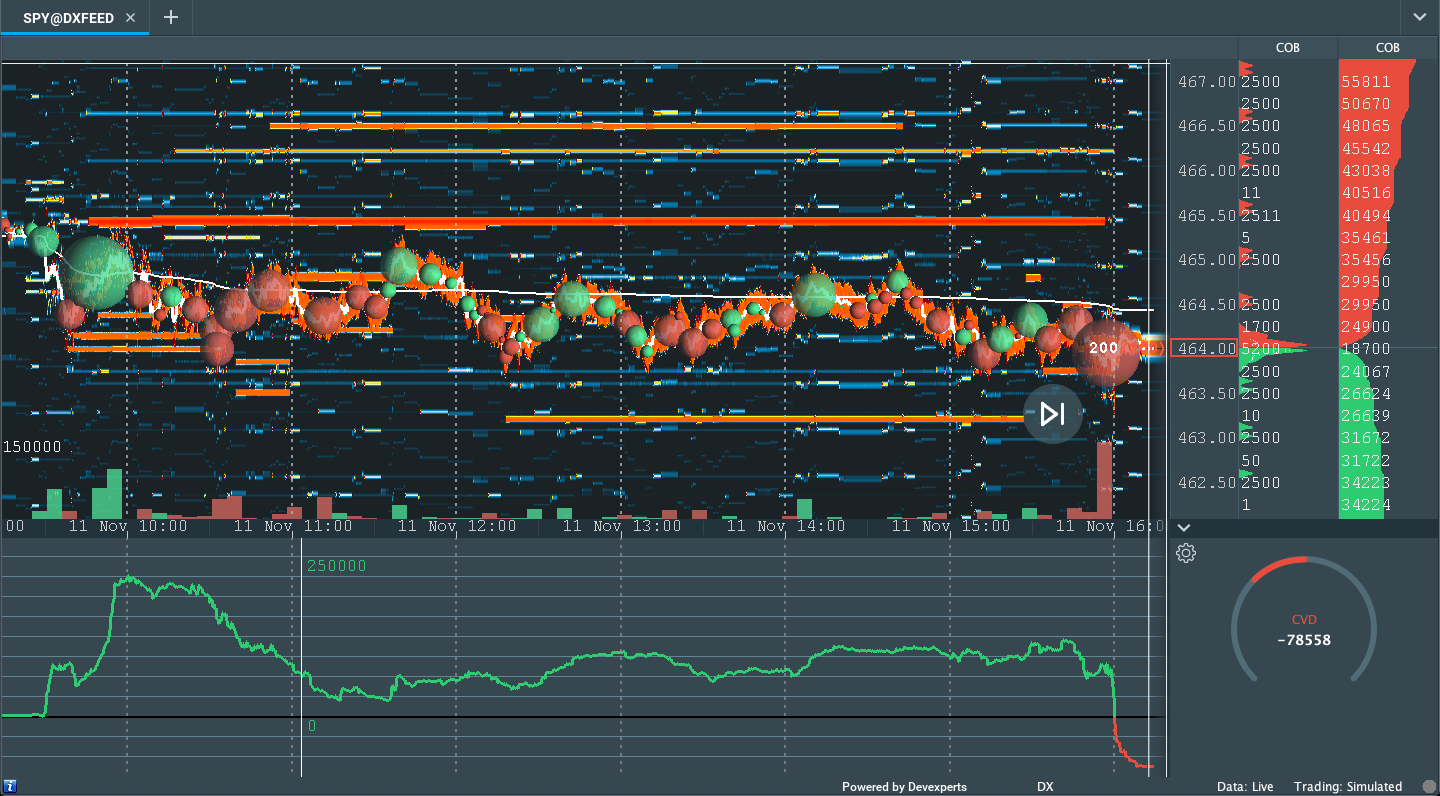

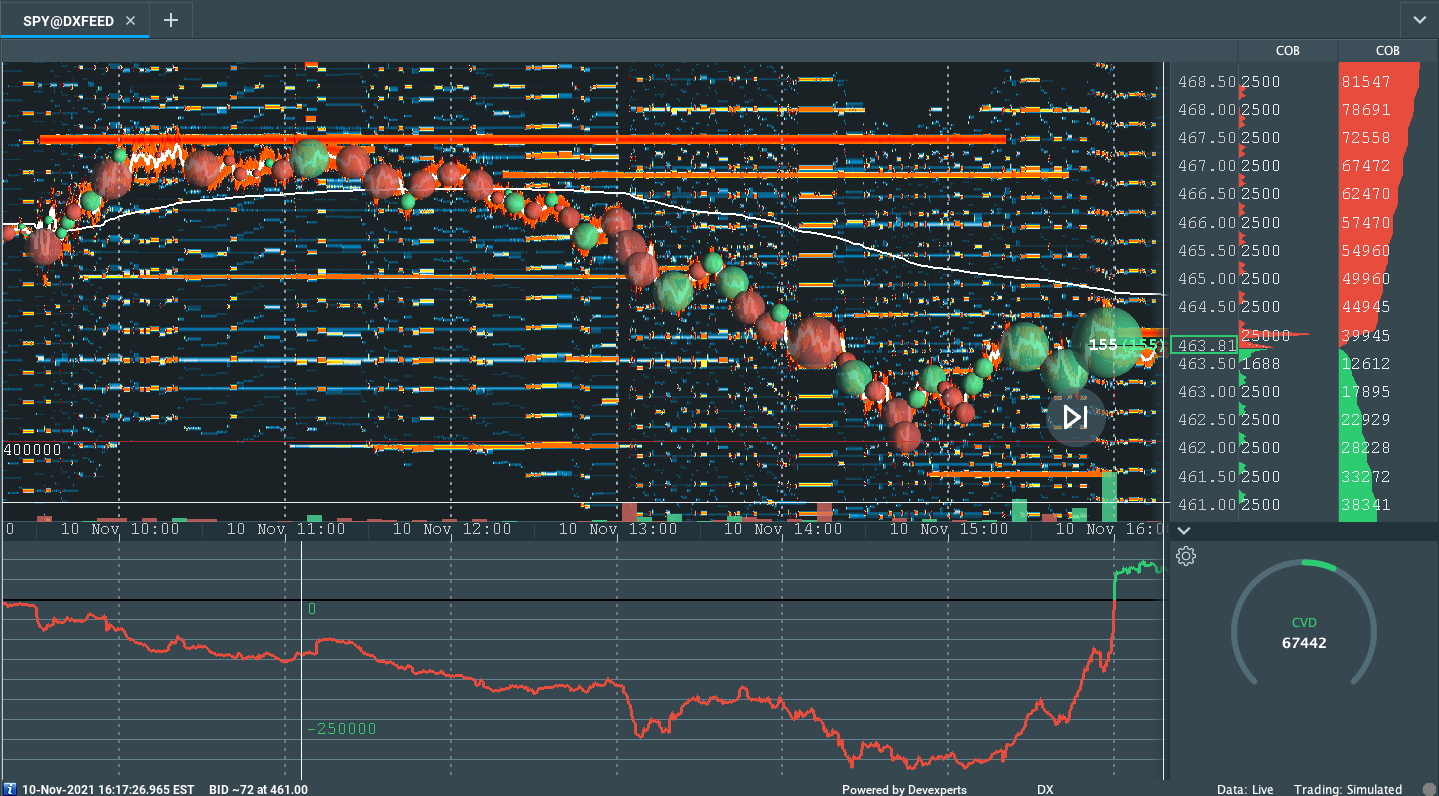

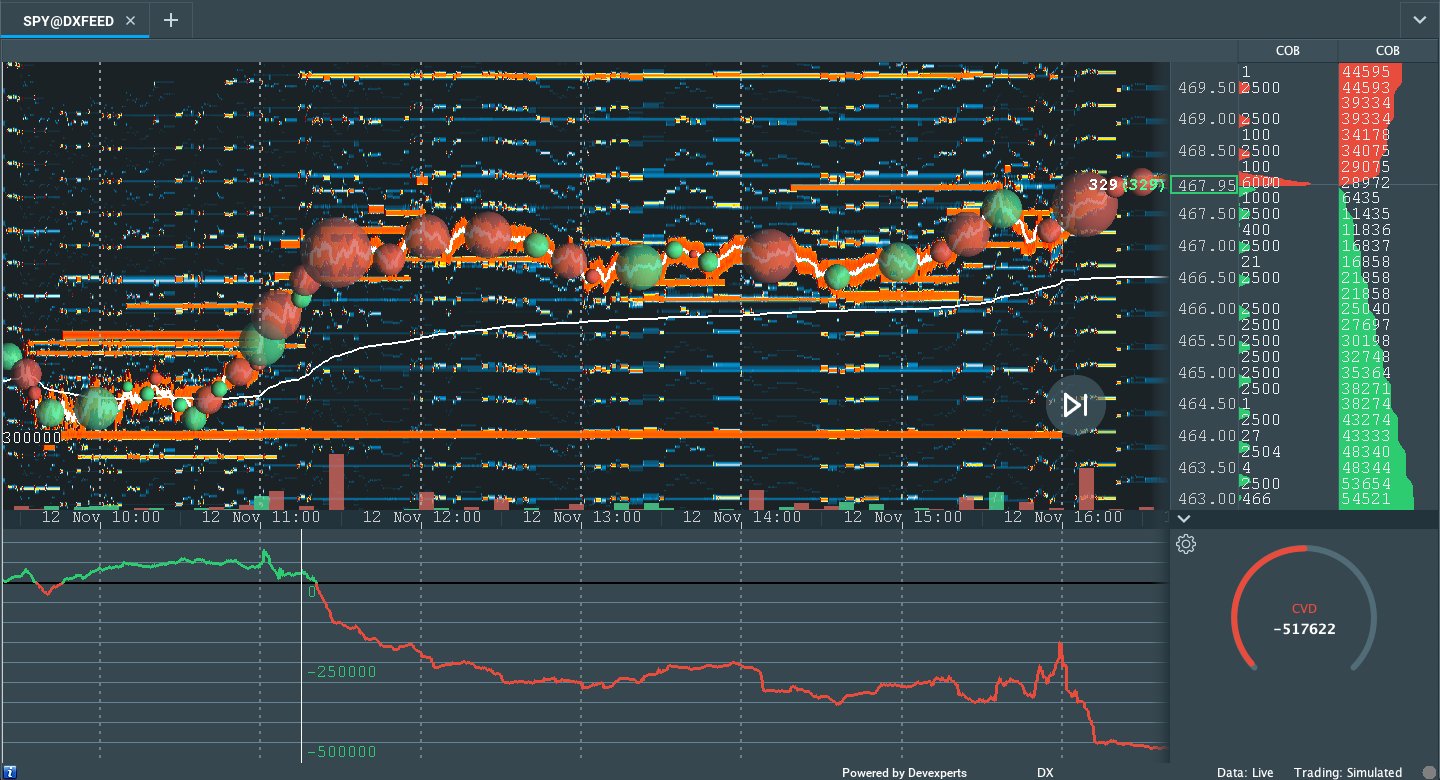

On lackluster intraday breadth and market liquidity metrics, the best case outcome occurred, evidenced by the spike and separation of value, above an area of consolidation in the S&P 500.

This activity, which marks a potential willingness to restart the trend, is built on poor structure, a dynamic that adds to technical instability.

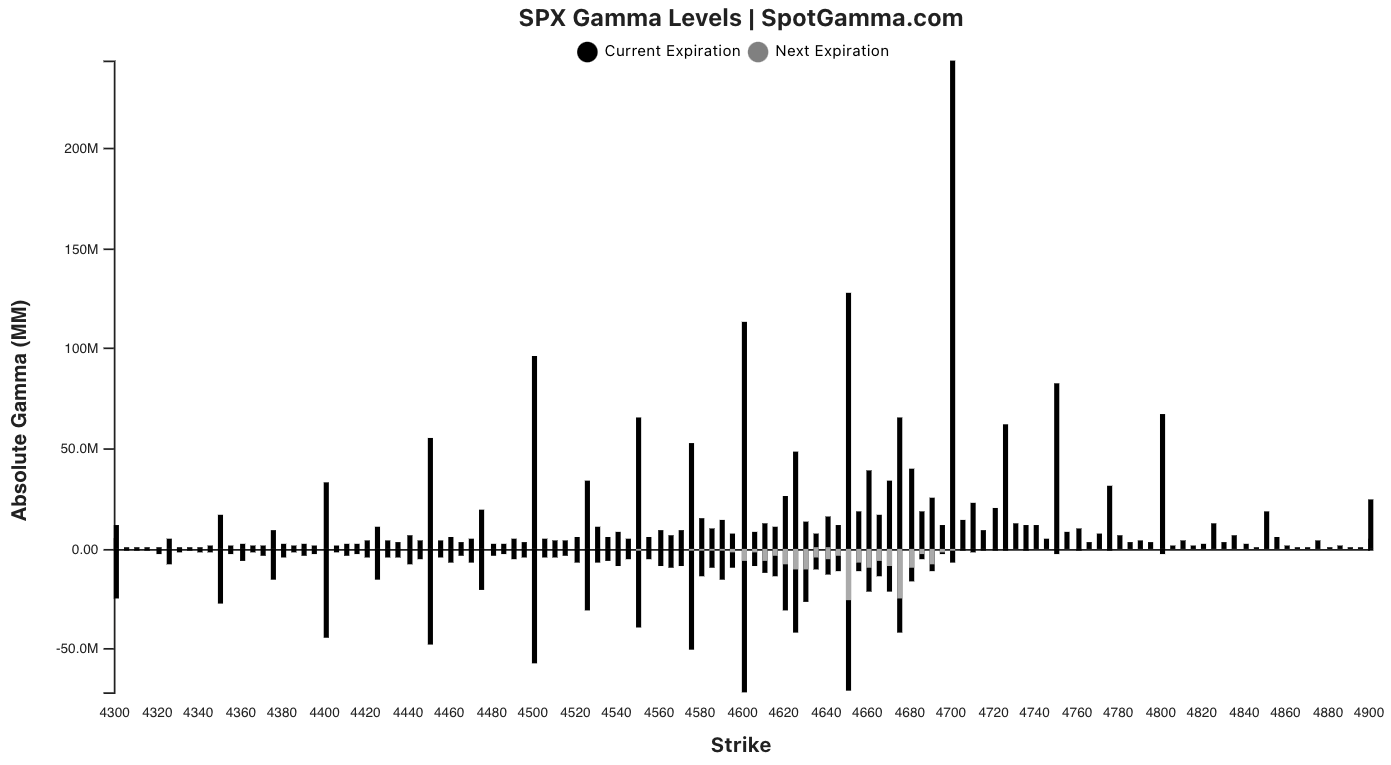

Further, should price feather back into range, participants ought to look for that probe to solicit responsive buying. However, auctioning decisively below Friday’s fairest price to do business – the $4,673.25 untested point of control – puts in play a fast-paced liquidation to $4,647.25 or so.

Context: Lighter than usual. Bear with me.

The purpose of the morning letter is to create a rolling narrative. We try to be as objective as possible in weighing the implications of both headwinds and tailwinds.

More and more, we discuss the apparently weighty implications of the growth of derivatives exposure and tail risk, the heightened moneyness of nonmonetary assets, trends in seasonality, buybacks, earnings growth, inflation, and more.

In light of all these dynamics, the path of least resistance is higher.

Households’ allocation to financial assets, exposure to leveraged products, and the like, is increasing to historic levels in the face of minor erosions in liquidity.

Why? Demand.

As stated, in the face of historic monetary stimulus and inflation, participants are increasingly extending moneyness to nonmonetary assets (e.g., real estate or the equity market) and that dings the velocity of money and typical recovery-tracking metrics like GDP.

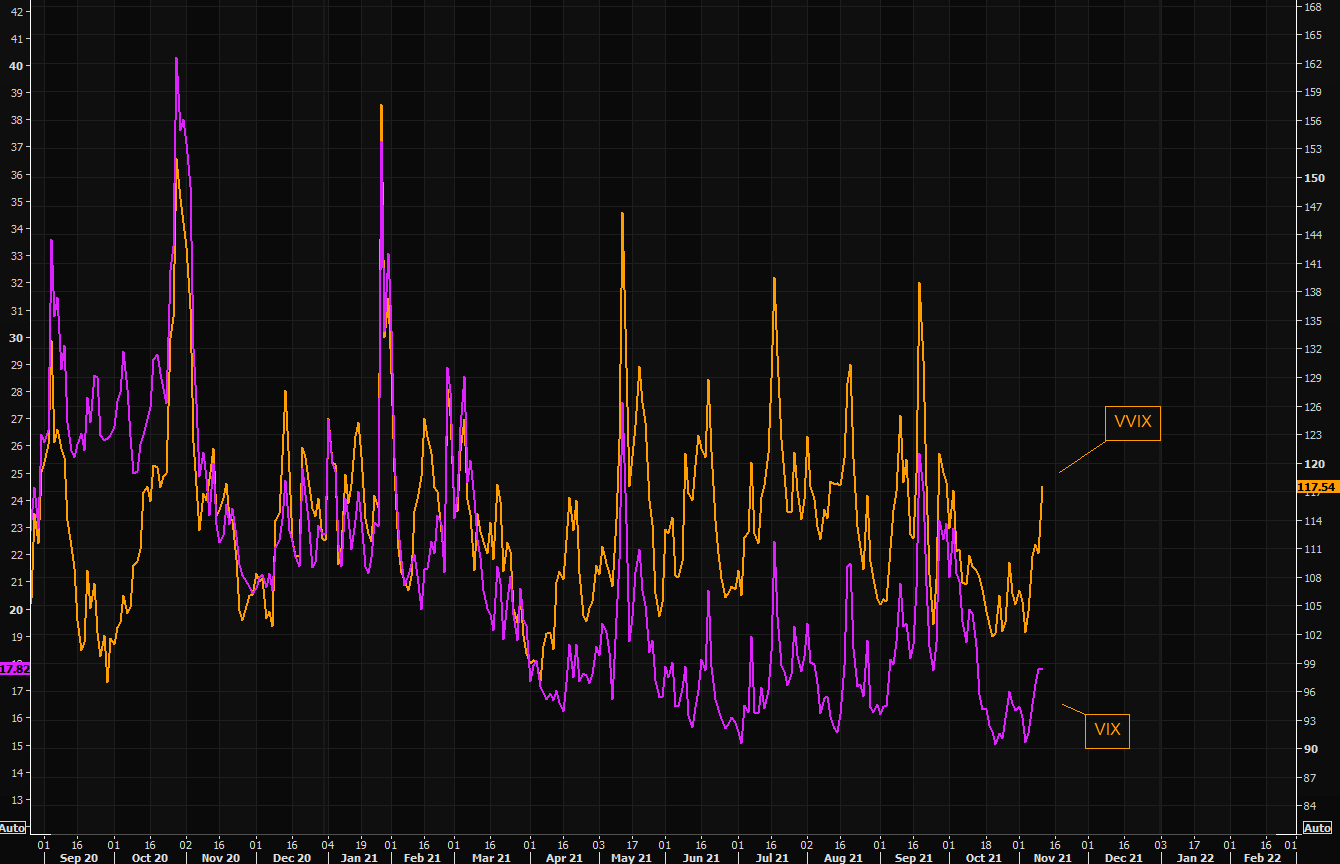

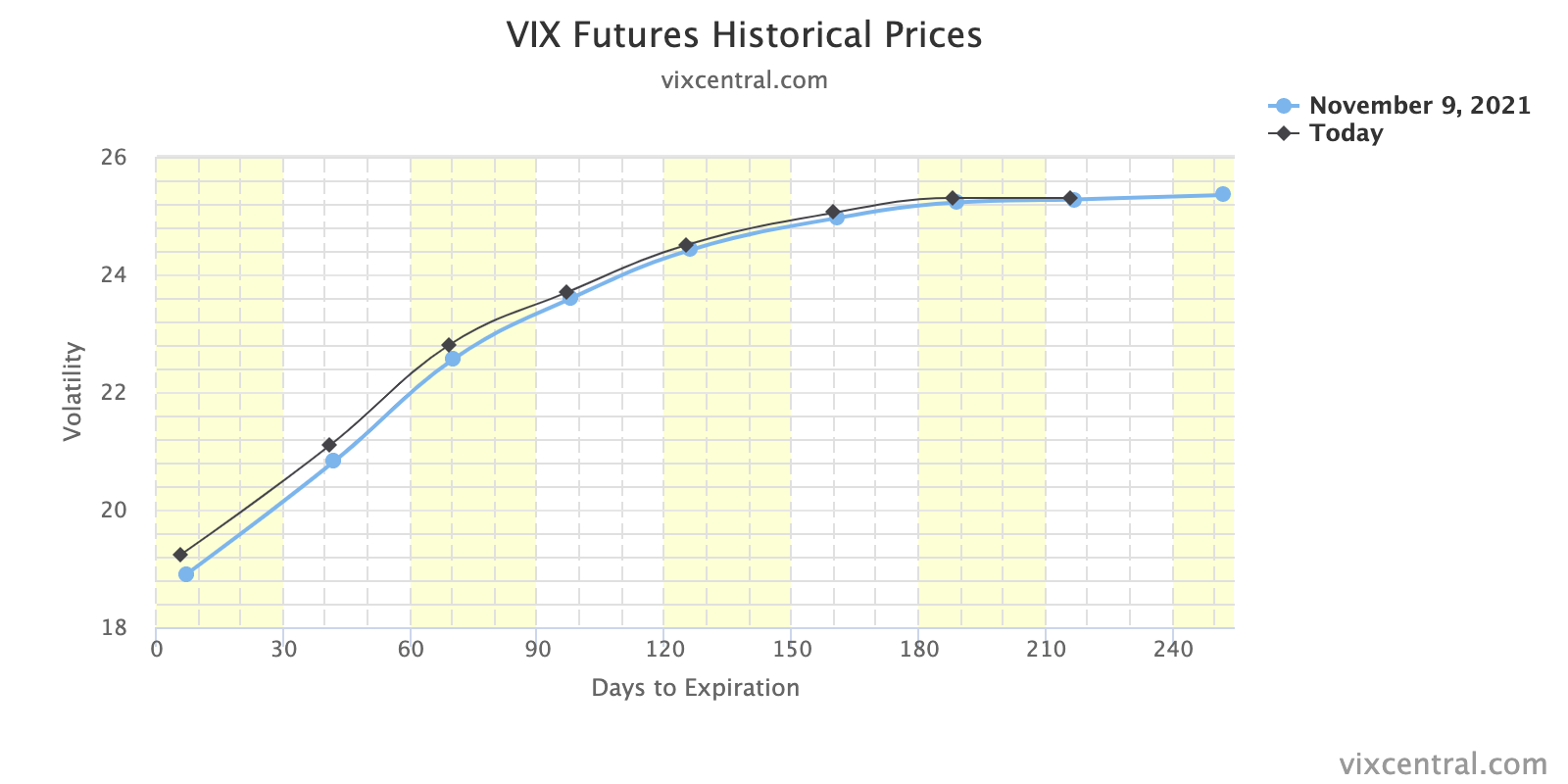

With that, the bond market’s pricing of risk, if we will, based on an “erratic … handling [of] large transfers of risk” – as evidenced by the Merrill Lynch Option Volatility Estimate (INDEX: MOVE) – has diverged from the pricing of equity market risk via the CBOE Volatility Index (INDEX: VIX).

Why are bond market risks being discounted by equity market participants? This isn’t new.

For years, traditional correlations have been breaking and the trend can continue.

Knowing that let’s hone in on the micro. What do we see 1 to 3 weeks out, and how can we best position ourselves to make money?

The first thing is last week’s short but broad downdraft. According to The Market Ear, “[a]t one point, NYSE upticks-downticks hit -1245. Over the past 6mo, there have only been a handful of times selloffs have gotten that broad and each one marked a N-T SPX bottom.”

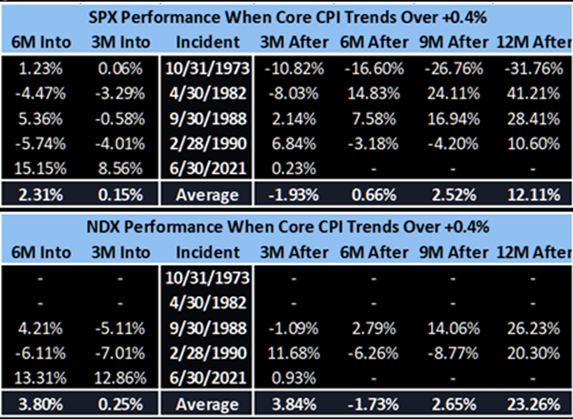

What about the implications of recent consumer price index (CPI) data? “[W]hile we have come into this inflationary environment hotter than typical, as long as it isn’t the 70’s, performance is actually typically pretty good,” The Market Ear explains.

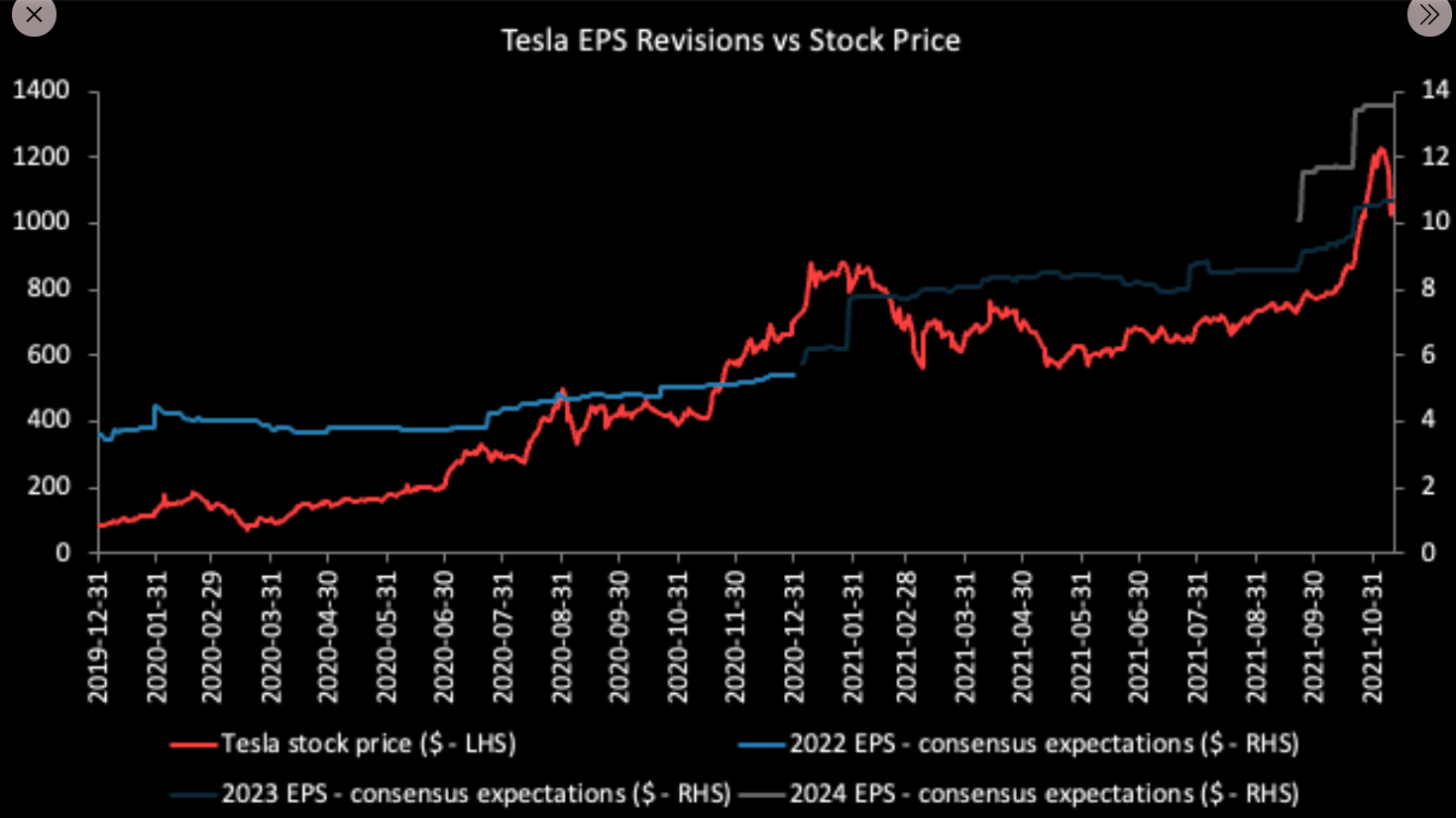

Another key point is strong corporate earnings and the participation of earnings per share expectations in the equity market markup.

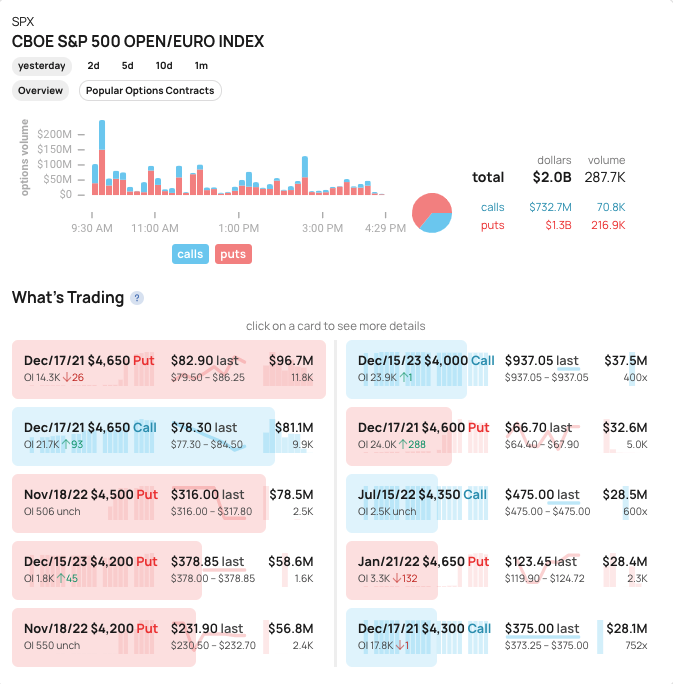

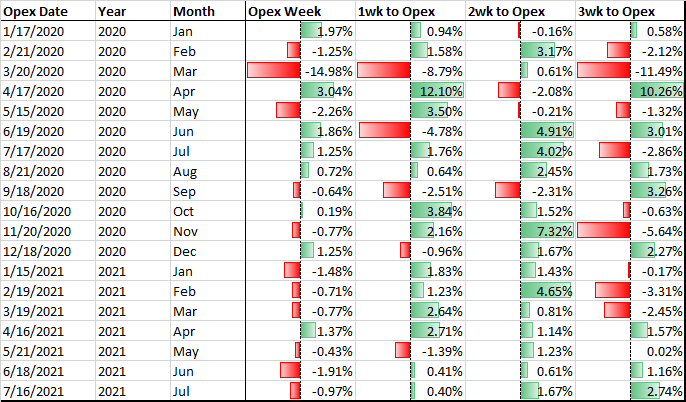

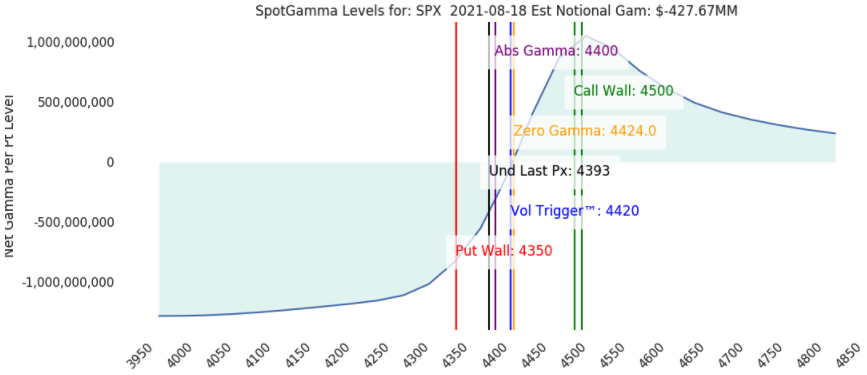

On the other hand, we have weighty VIX and SPX expirations, this week.

With implied volatility coming in at the end of last week, markedly, attention shifts to whether participants can build on that (i.e., commit more capital to higher strike prices), and, potentially, overwhelm post-expiration reductions in gamma exposures and increased volatility.

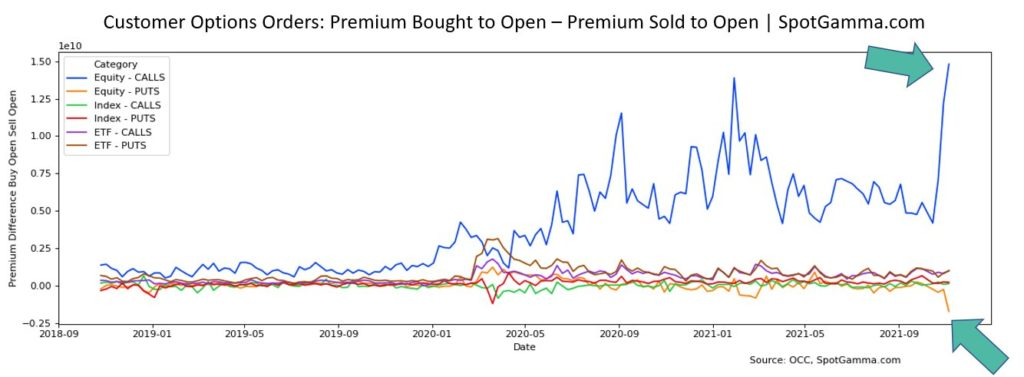

For analysis on the implications of recent derivatives activity, click here to view Friday’s newsletter.

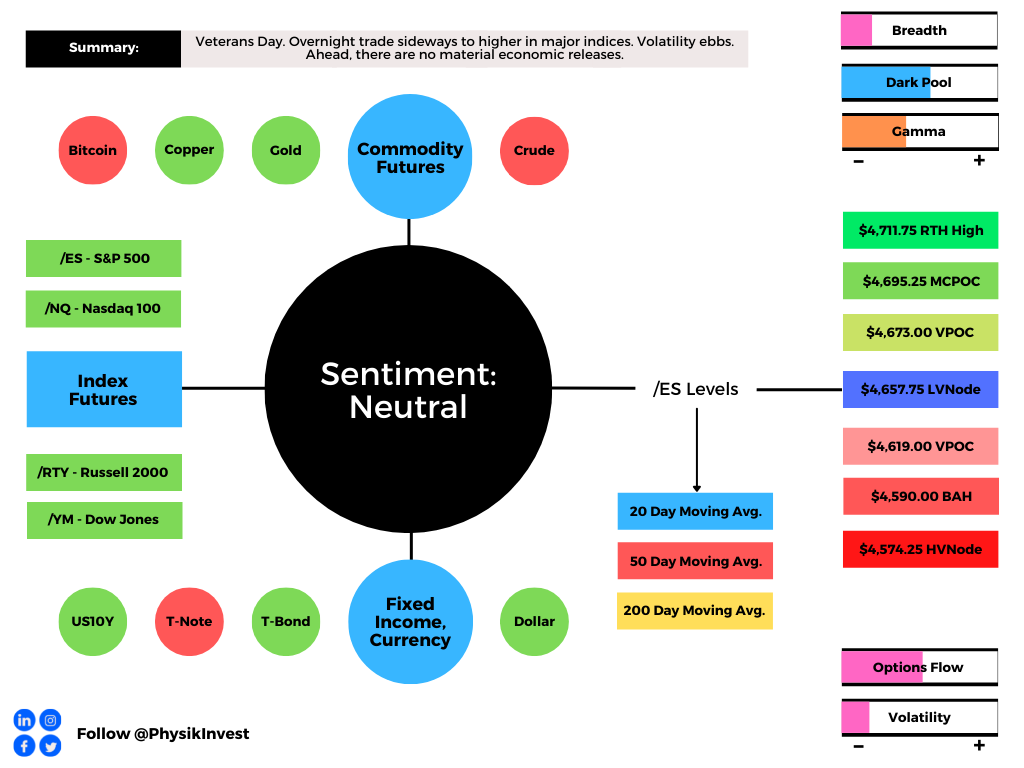

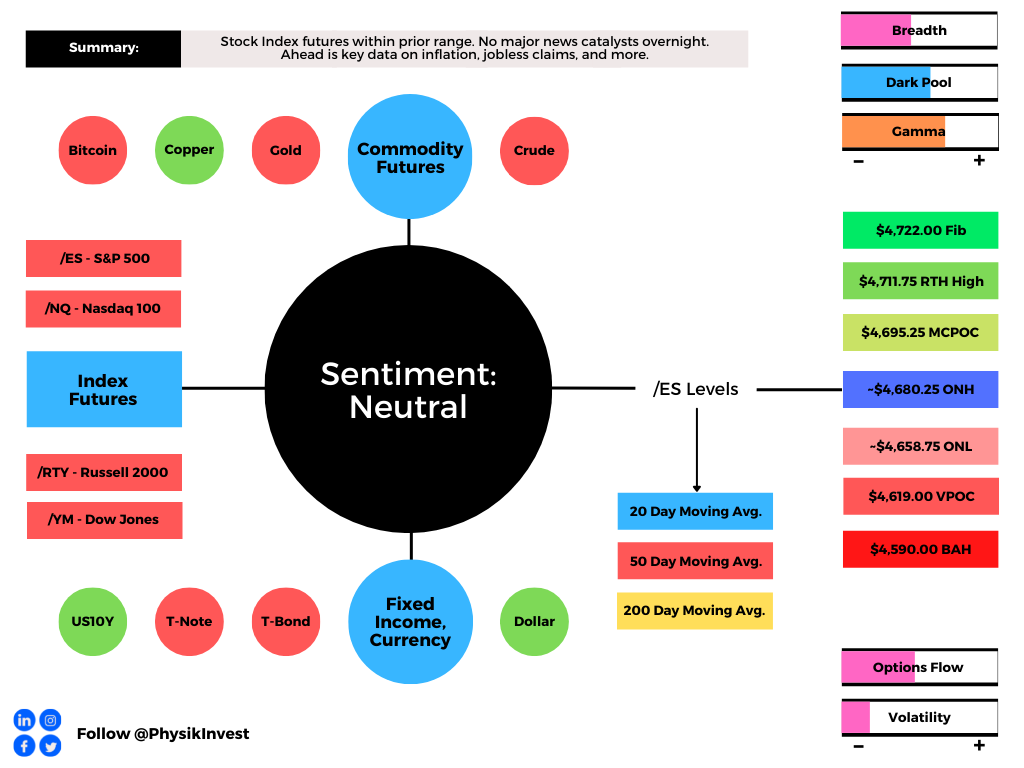

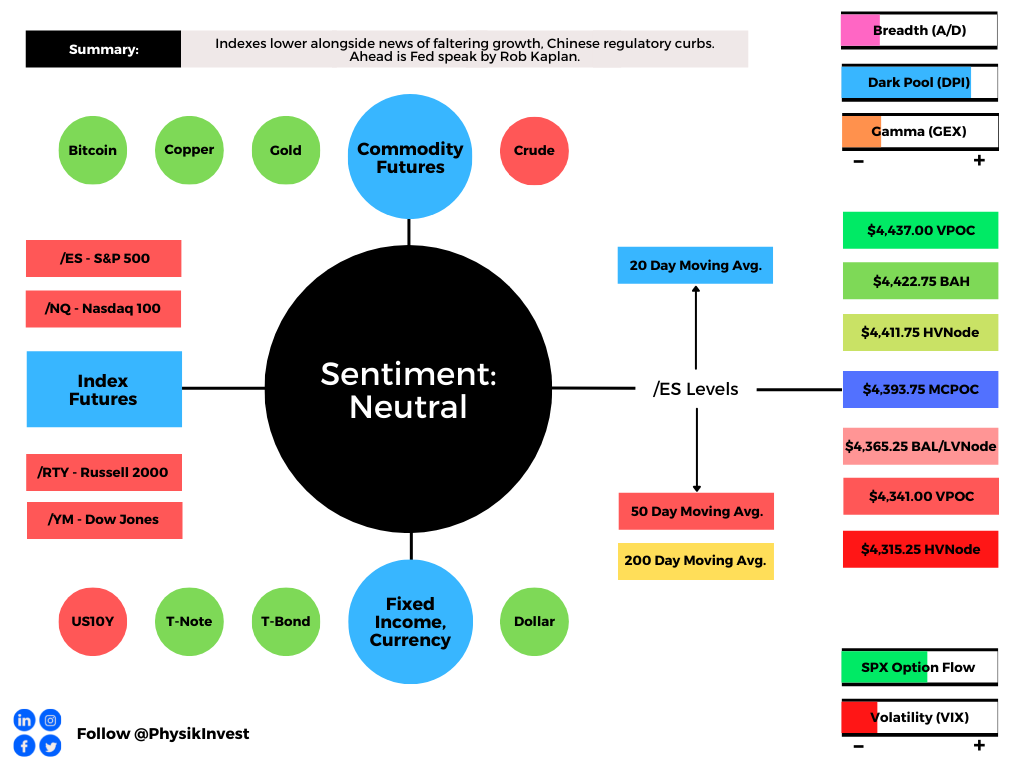

Expectations: As of 5:45 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator. Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

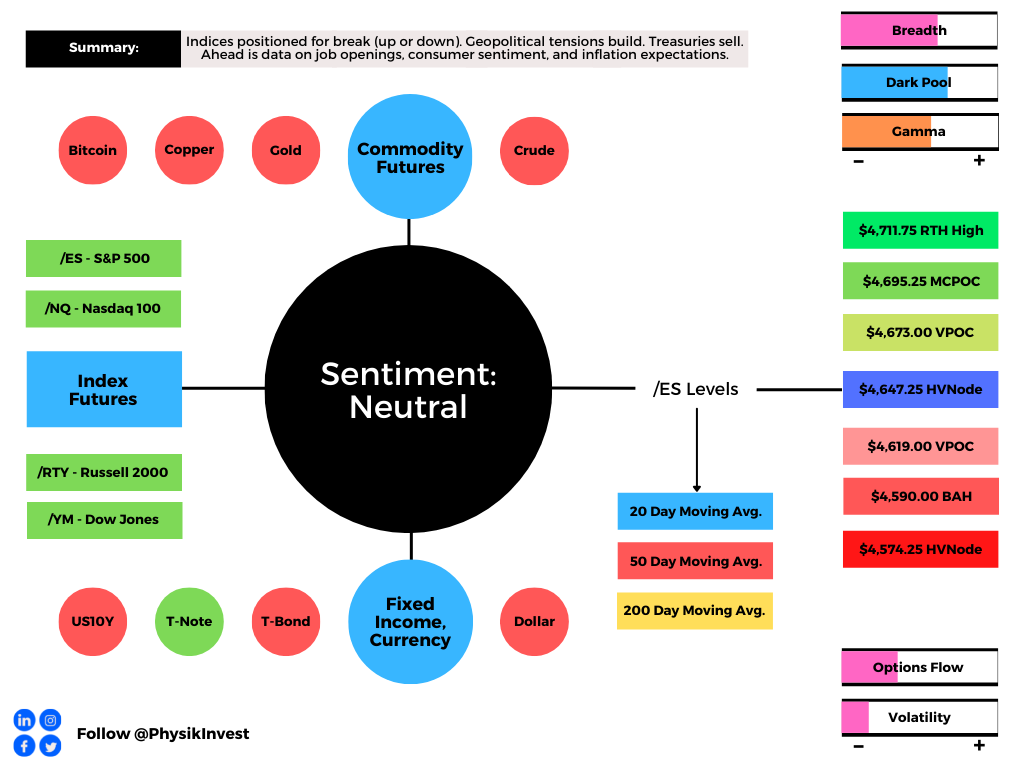

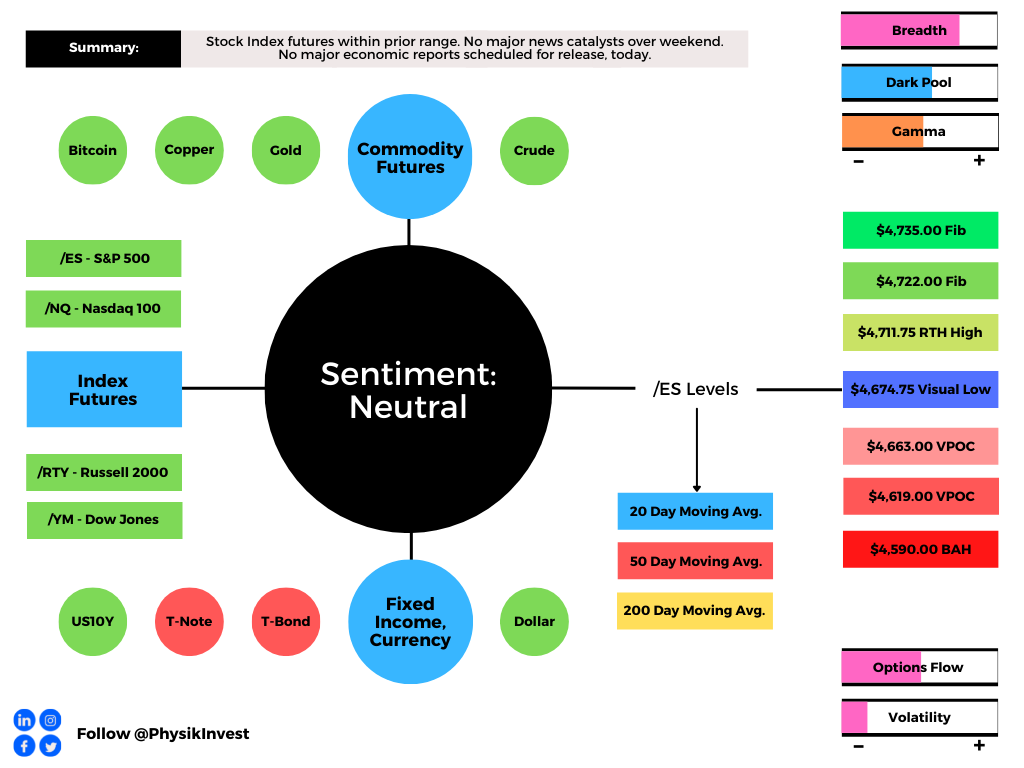

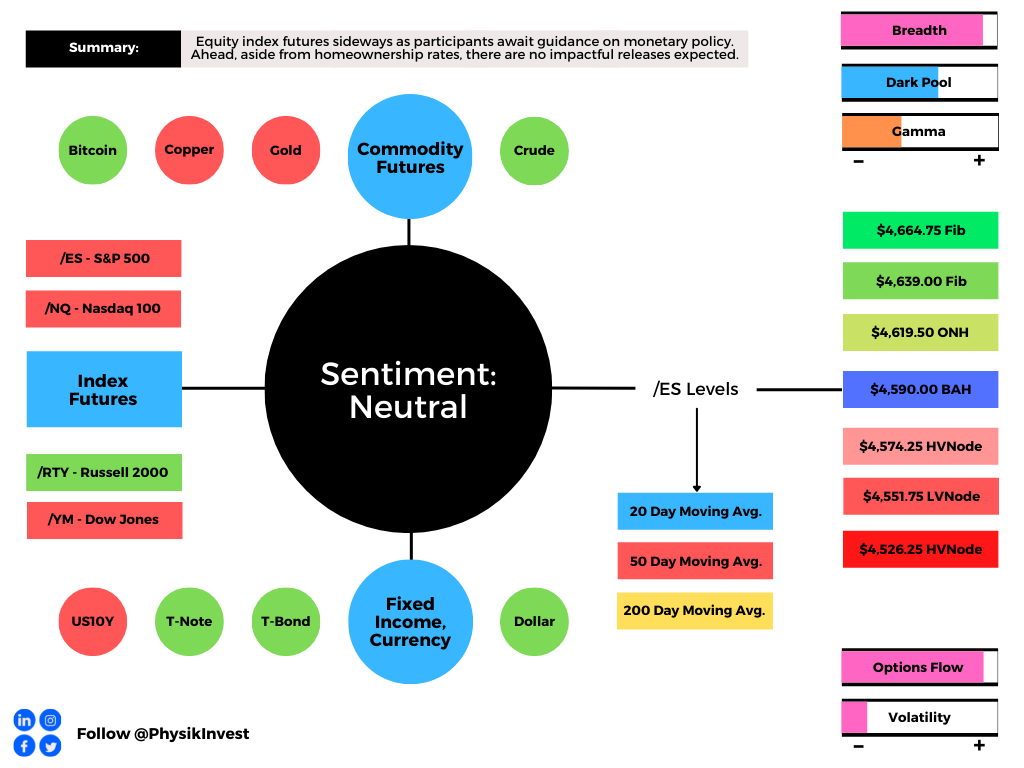

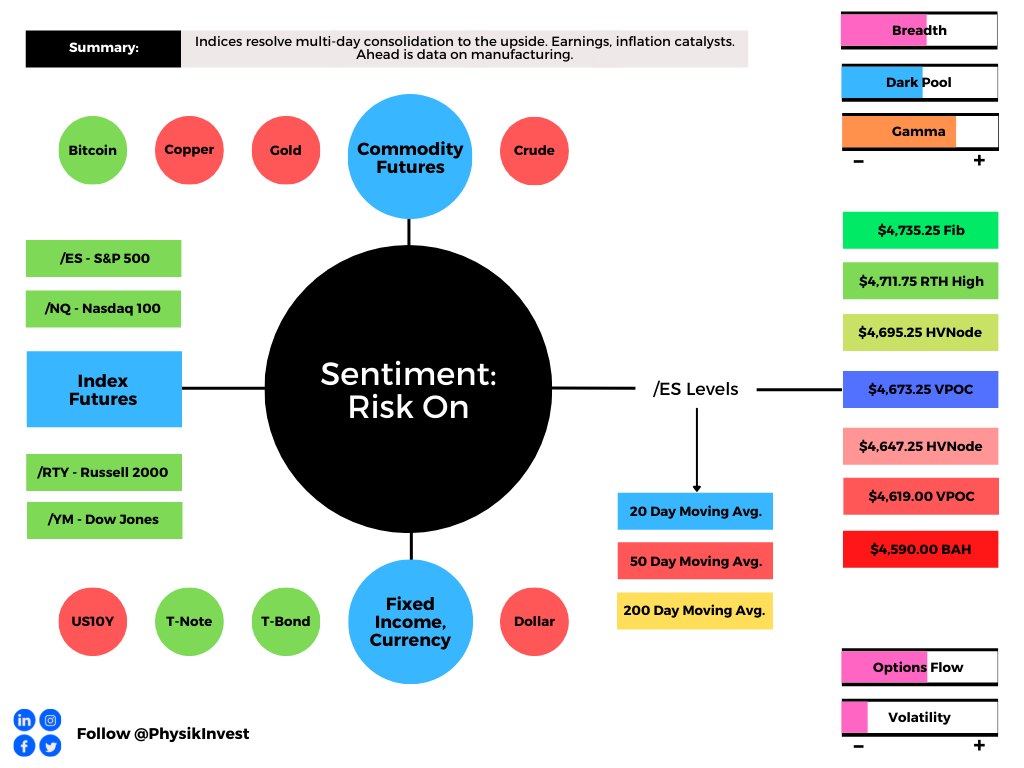

In the best case, the S&P 500 trades sideways or higher; activity above the $4,673.25 untested point of control (VPOC) puts in play the $4,695.25 high volume area (HVNode). Initiative trade beyond the HVNode could reach as high as the $4,711.75 all-time high and $4,735.25 Fibonacci, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,673.25 VPOC puts in play the $4,647.25 VPOC. Initiative trade beyond the $4,647.25 VPOC could reach as low as the $4,619.00 VPOC and $4,590.00 balance area boundary (BAH), or lower.

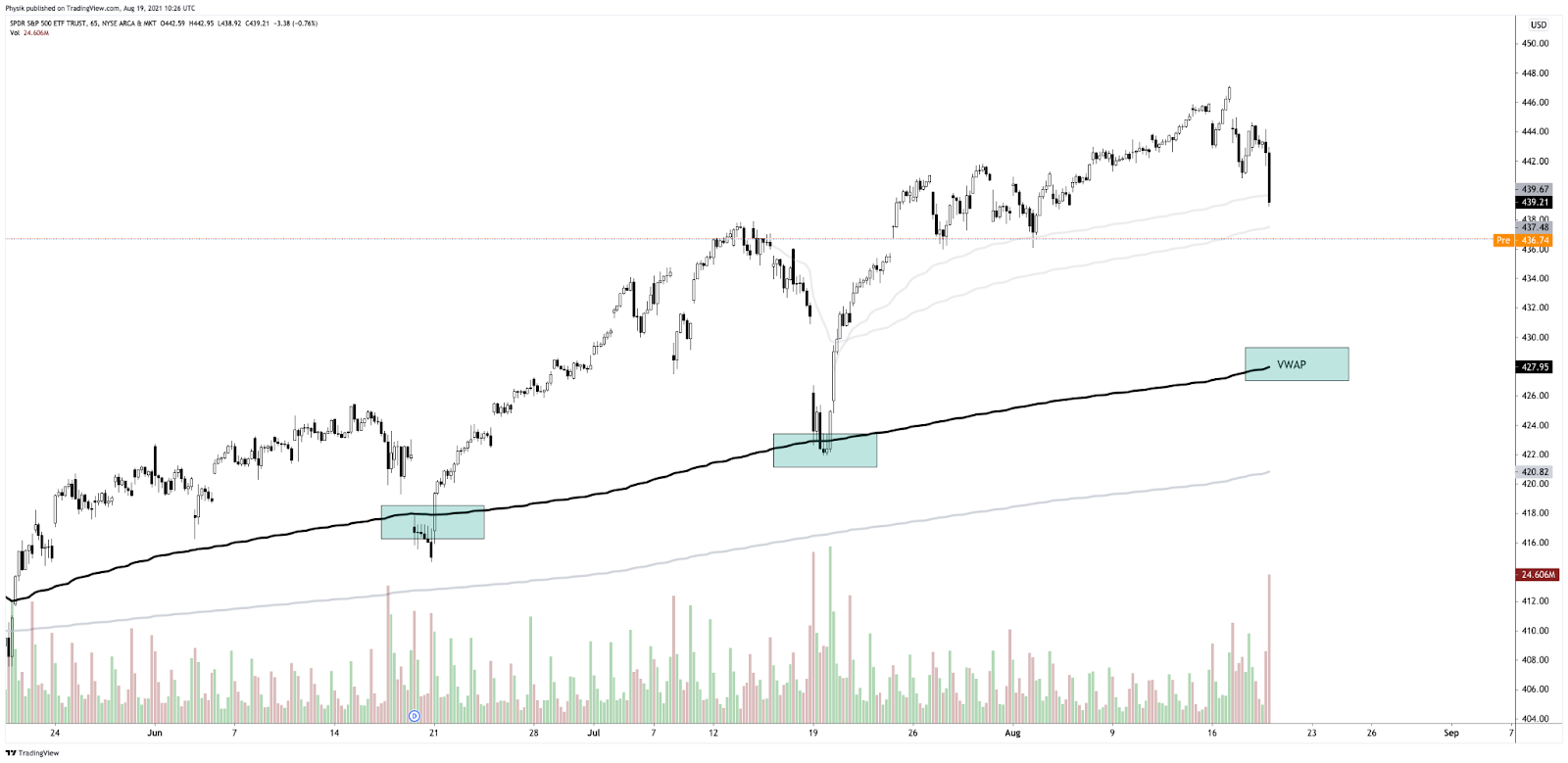

As an aside, participants reclaimed the volume-weighted average price (VWAP) anchored from the all-time high and recent Federal Open Market Committee (FOMC) meeting.

This is a metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

Further, given that this development suggests the average buyer, since the all-time high, is in a winning position, who does this dynamic embolden? The buyer or seller?

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

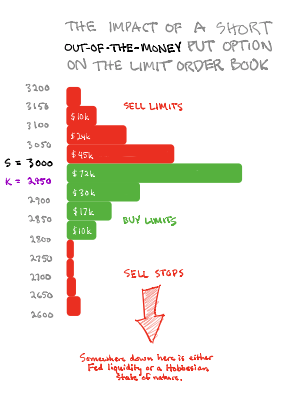

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure. In recent history, this reset in dealer positioning has been front-run; prior, there was an increase in volatility after the removal of large options positions and associated hedging.

Significance Of Prior ATHs, ATLs: Prices often encounter resistance (support) at prior highs (lows) due to the supply (demand) of old business. These areas take time to resolve. Breaking and establishing value (i.e., trading more than 30-minutes beyond this level) portends continuation.

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.