Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

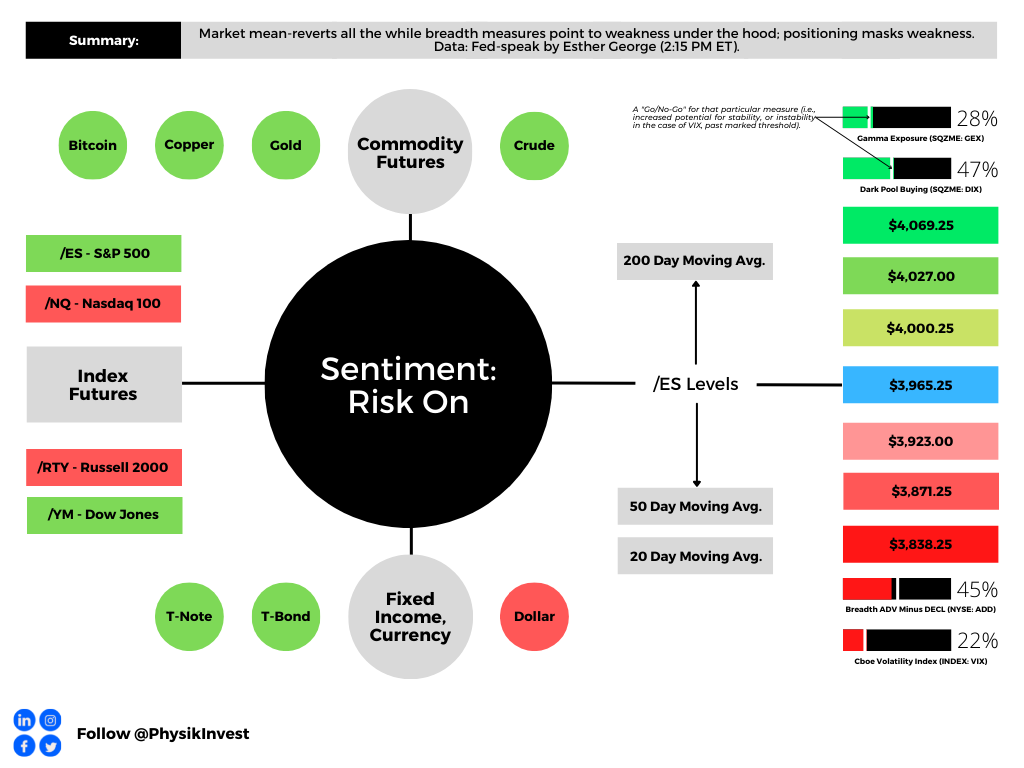

Positioning

The Federal Reserve’s (Fed) decision to increase its benchmark interest rate by 25 basis points kicked off a bout of strength, boosted by the compression of wound implied volatility (IVOL). This volatility compression we observed with a shift lower in the IV term structure in the S&P 500 (INDEX: SPX). Follow-on strength surfaced on Thursday and, based on an analysis of top-line IVOL measures such as the Cboe Volatility Index (INDEX: VIX) trending higher with the SPX, it was, in part, from traders’ demands for call options, hence high call option volumes.

Recall our detailed letter published prior to February 2, 2023 (e.g., February 1, 2023, January 26, 2023, and beyond). The context was set for the SPX and VIX to trend higher; traders bidding up call options due to their fear of missing out, in the context of less liquidity to absorb those demands, would be beneficial to owners of structures like call option butterflies and ratio spreads. Additionally, owning such structures would help dampen the impact of potential SPX downside on portfolios.

For instance, on January 25, 2023, this letter said trades structured in the indexes such as the Nasdaq 100 (INDEX: NDX), where there was a steeper skew that would enable us to collect more credit in the options we are short, thereby lowering the cost of the spread we own, looked attractive, given the likelihood that the index would stay strong after the earnings reports of some big movers like Tesla Inc (NASDAQ: TSLA).

In yesterday’s letter update, we said that such trades were working spectacularly. In fact, your letter writer’s trading partner, who “initiated some +1 x -2 (17 FEB 23 13500/14000) [NDX] call ratio spreads for free (i.e., $0.00 debit or better to enter),” saw his spreads price in excess of a $40.00 credit to close, yesterday. That structure went from a $0 debit to open to a $4,000.00 credit to close. Again, nice job Justin. I’m expecting that case study, soon!

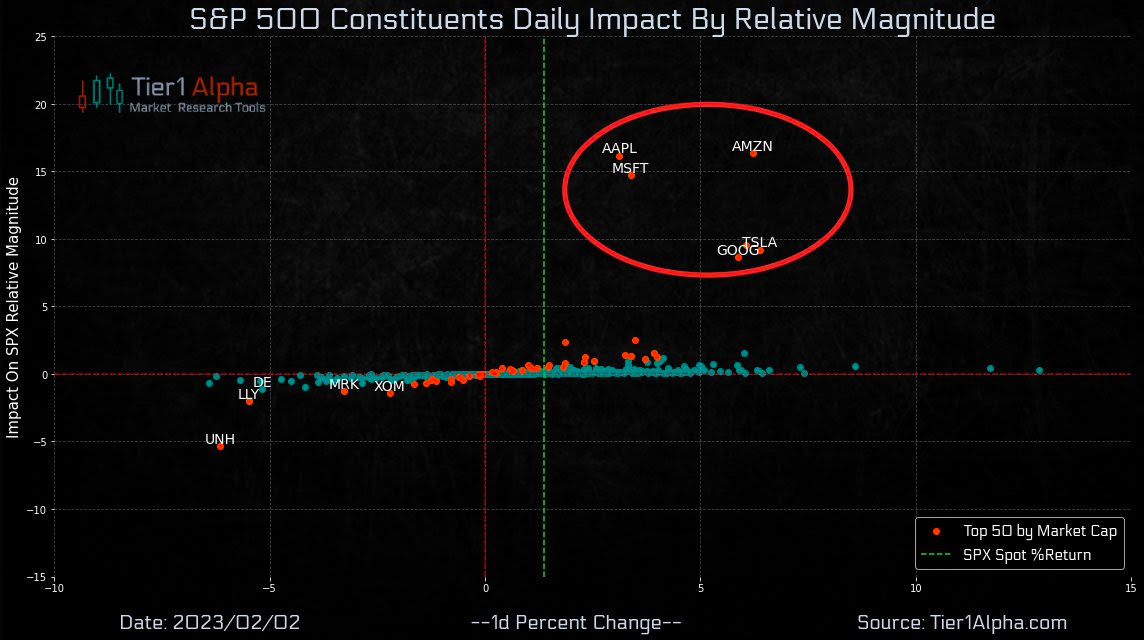

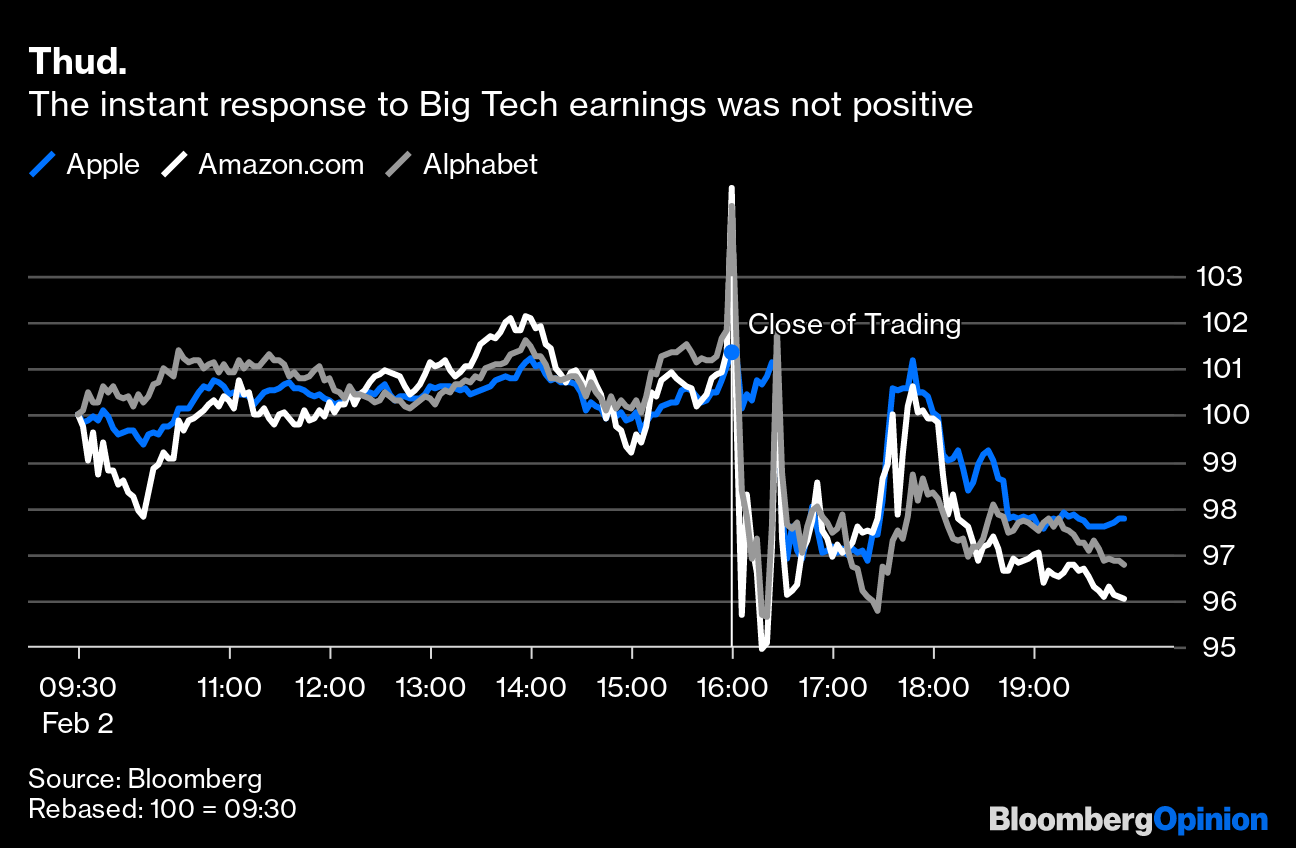

The NDX was probably the best place to be, yesterday, looking at the magnitude of movement in some of the heavyweights in the SPX, yesterday.

Noteworthy is that many of the strongest performers (e.g., Google, Amazon, Apple) weakened considerably in the after-market when their earnings, and the speeches associated, pointed to some challenges ahead.

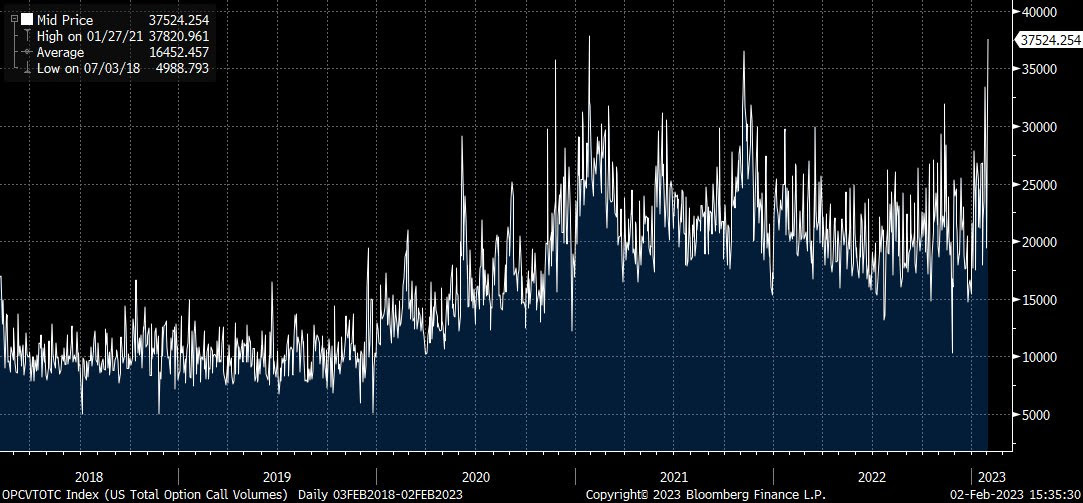

Breadth was, generally, not that strong, to add. This validates your letter writer’s belief the market is in a precarious position. Notwithstanding the market’s potential to stay strong into the mid-February timeframe as some strategists believe, the data seems to suggest that “whenever there are two million or more call contracts that exchange hands on the Cboe, future 5- and 10-day returns tend toward being negative (about -1.37% and -2.12% respectively),” SpotGamma said.

SpotGamma added: “This is, in part, because the bullish hedging impact of short-dated call options activity is not long-lasting. Also, IV compressing from a relatively low starting point also does little to bolster long-lasting rallies.”

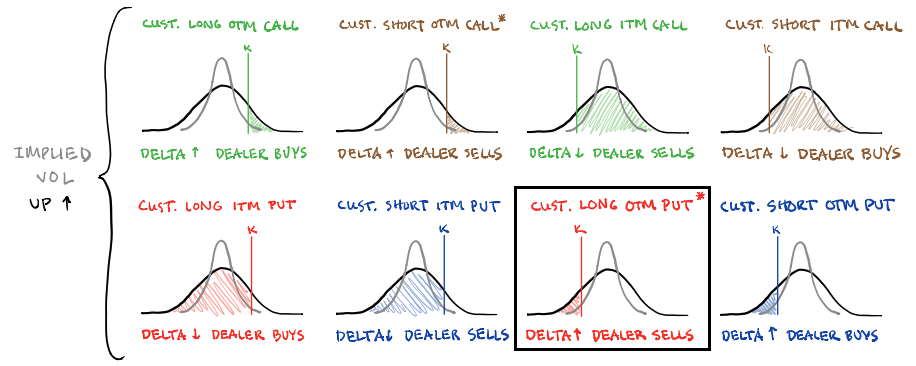

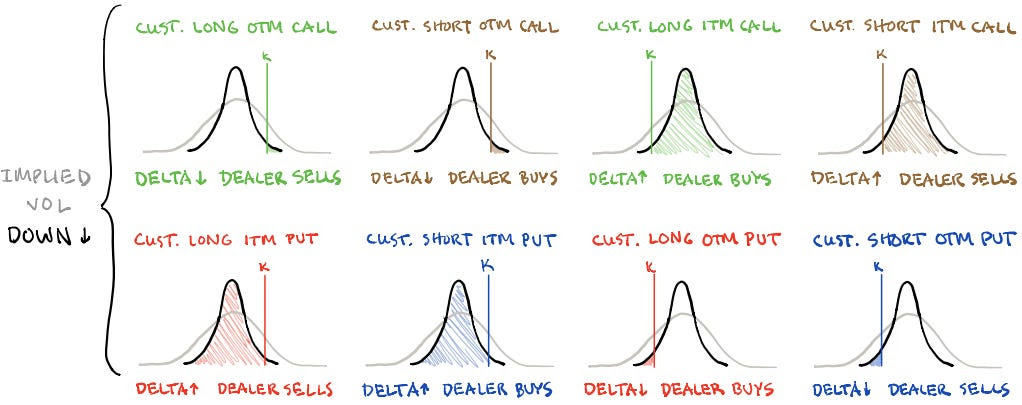

As further validation for the precariousness the market is in, “[t]he most prominent feature of the 0DTE landscape is actually customer-bought calls way out at $4,200.00 (which would ramp up buying from dealer long-gamma if SPX were to rise to ~$4,170.00.” Per SpotGamma, should “traders’ interest build at or slightly above current SPX prices, then dealers’ hedging may actually result in range suppression or pressure” as time passes and volatility falls. That’s because if a long call option’s probability of finishing in the money at expiration falls, the dealer’s risk falls as well and, so, the dealer can sell some of their hedges. This is market pressure.

As this letter stated, yesterday, knowing that longer-dated SPX IVOL “is cheap, now attractive trades include selling rich call verticals to finance put verticals.”

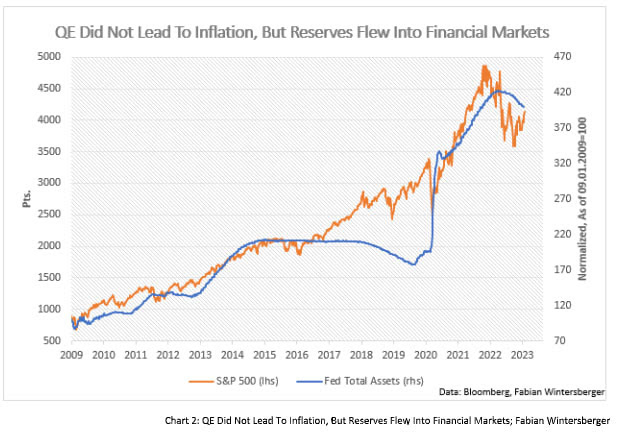

Per Joseph Wang, the “increasing probability of a second bout of inflation, an issue in the 1970s that the Fed is keen to avoid … [by] retighten[ing] financial conditions … through its balance sheet,” the flow of capital out of capital markets presents more pressure on the financial economy (not necessarily the real economy). Cheap put protection may help hedge the realization of further macro-type market pressure.

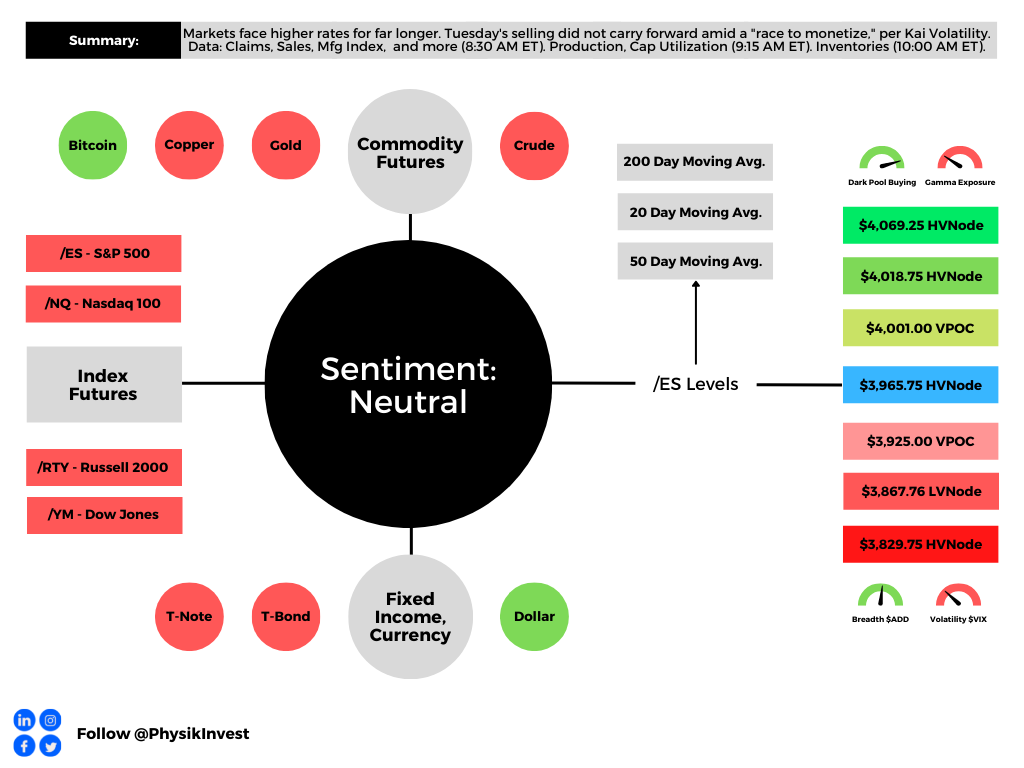

Technical

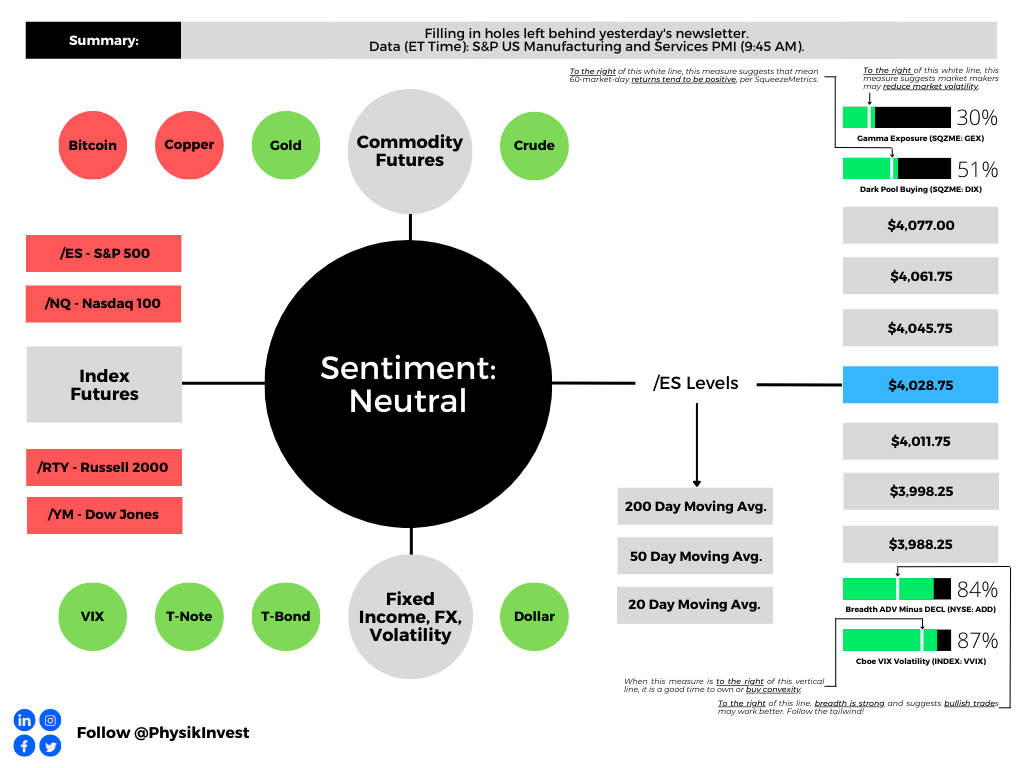

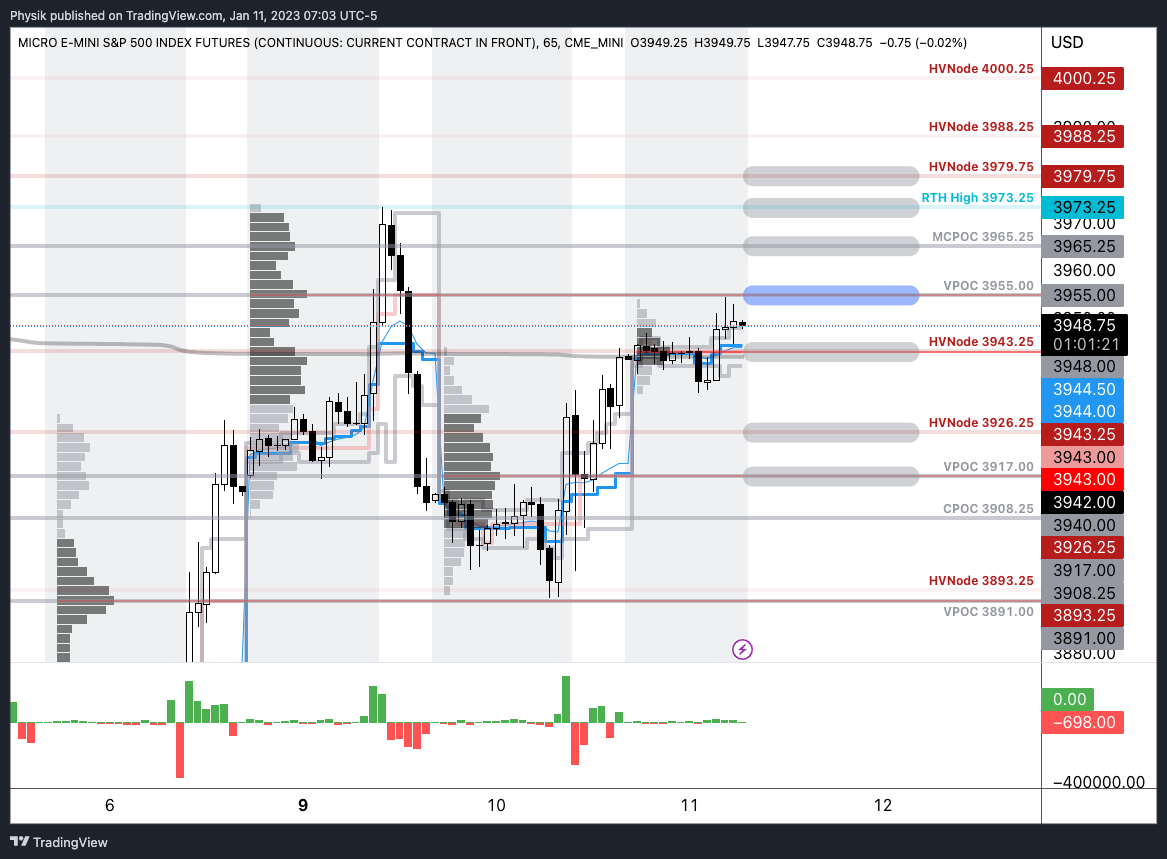

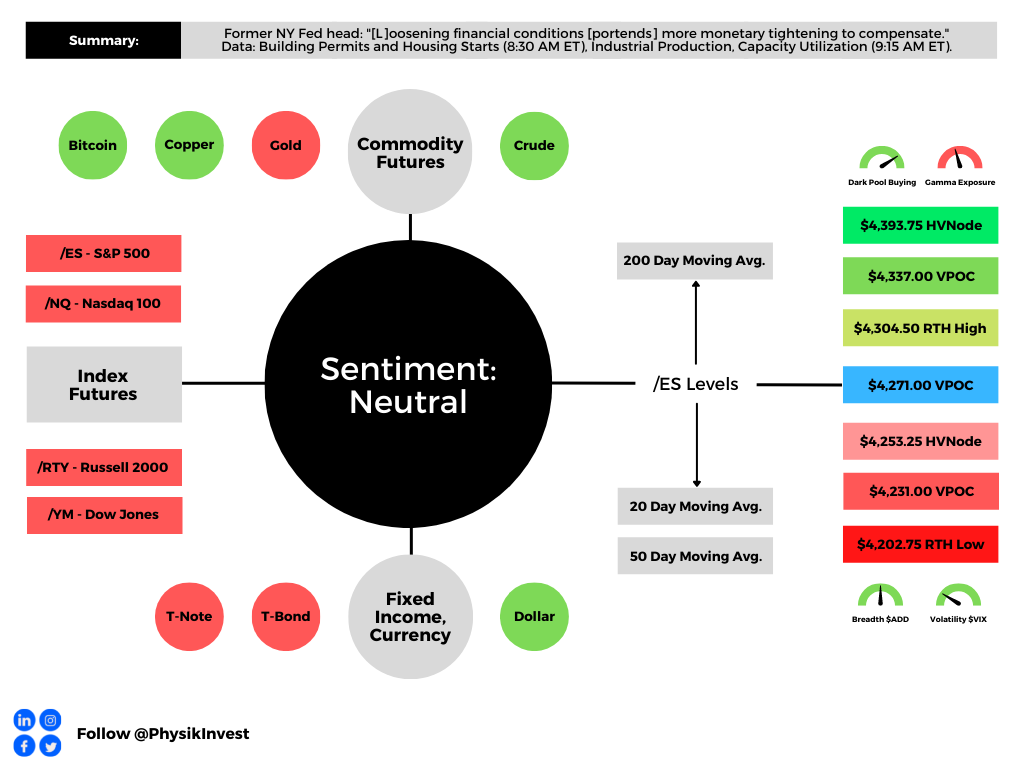

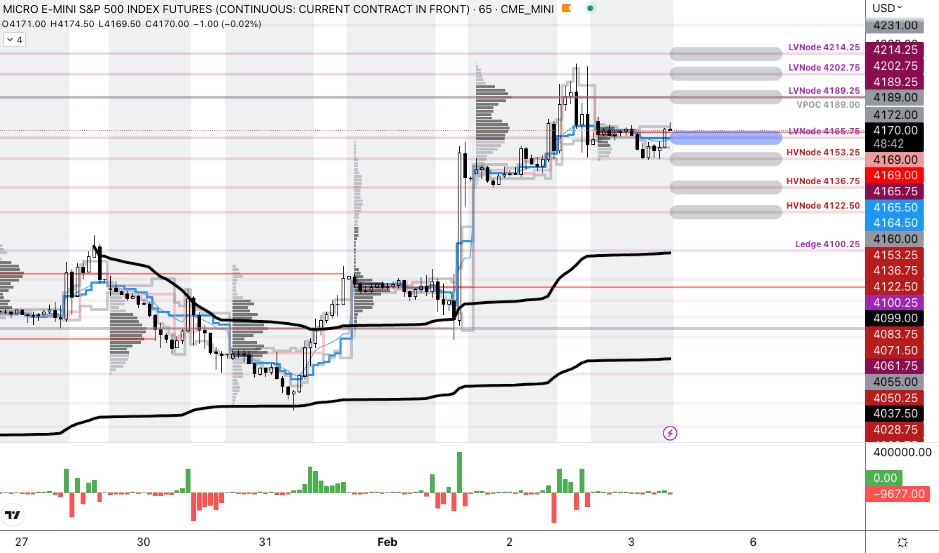

As of 8:15 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a negatively skewed overnight inventory, inside of the prior range, suggesting a limited potential for immediate directional opportunity.

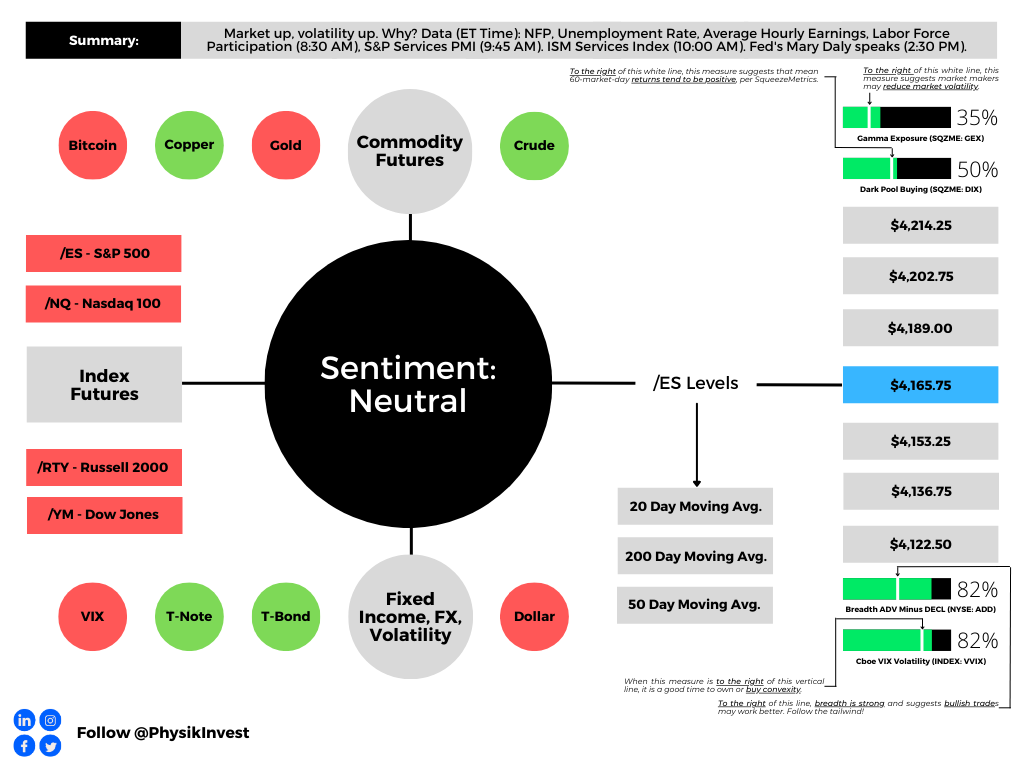

The S&P 500 pivot for today is $4,165.75.

Key levels to the upside include $4,189.00, $4,202.75, and $4,214.25.

Key levels to the downside include $4,153.25, $4,136.75, and $4,122.50.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels hold weight barring an exogenous development.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for a period of time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

In short, Renato Leonard Capelj is an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.