Physik Invest’s Daily Brief is read by over 1,200 people. To join this community and learn about the fundamental and technical drivers of markets, subscribe below.

Administrative:

Crazy morning! Coming in really late, today. Not the best letter. I know.

Positioning

To preface, trading is a lonely game and having people to speak with means a lot. So, I call up my trading partner, yesterday, and we chat markets and some other unrelated stuff. During the call, he said something I couldn’t shake. It was along the lines of the following: “Active traders (e.g., directional stock and futures bettors) are getting killed right now, and we are sitting on our hands not getting killed.”

This is a nod to context. We mustn’t look at the market from a single angle, in short.

Starting on the fundamental side of things, the 2022 market de-rate had much to do with participants’ repricing of assets in the context of monetary tightening (to stem structural inflation). As Joseph Wang wrote in one post, the “Fed’s rapid tightening markedly reduced the level of household wealth and thus potential demand.”

It’s “[o]ne of the Fed’s tools to impact aggregate demand [] by adjusting household wealth,” he adds. This “in turn impacts household spending power.”

Adding: “The wealth effect was an explicit rationale for [quantitative easing or QE], where higher asset prices were thought to boost consumer spending. By the same logic, lowering household wealth can potentially lower consumer spending and dampen inflation.”

With “the bulk of asset repricing … behind us,” markets have turned; support is fundamental, for one, and positioning, as we discuss in this letter, has added to market support.

A similar setup occurred late this summer; investors’ supply of protection added to the macro-type flows after elections and CPI. Following the last weeks, the pulling forward of the supportive hedging (linked to the decay of options with respect to the passing of time), in light of the holidays, would keep markets intact.

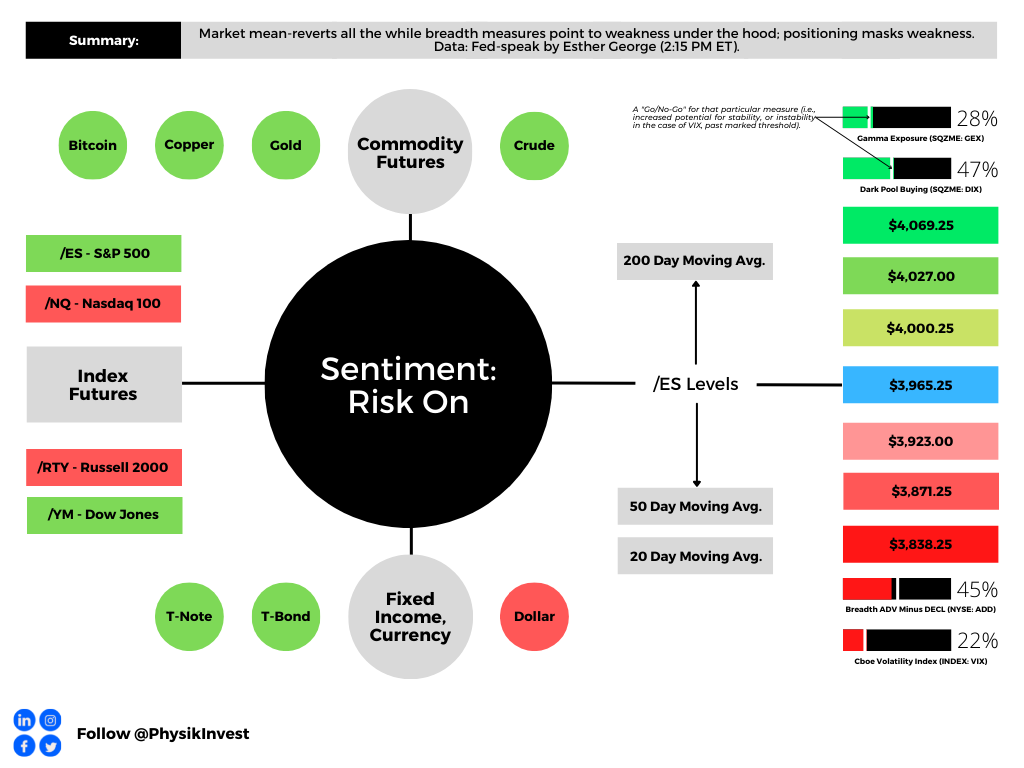

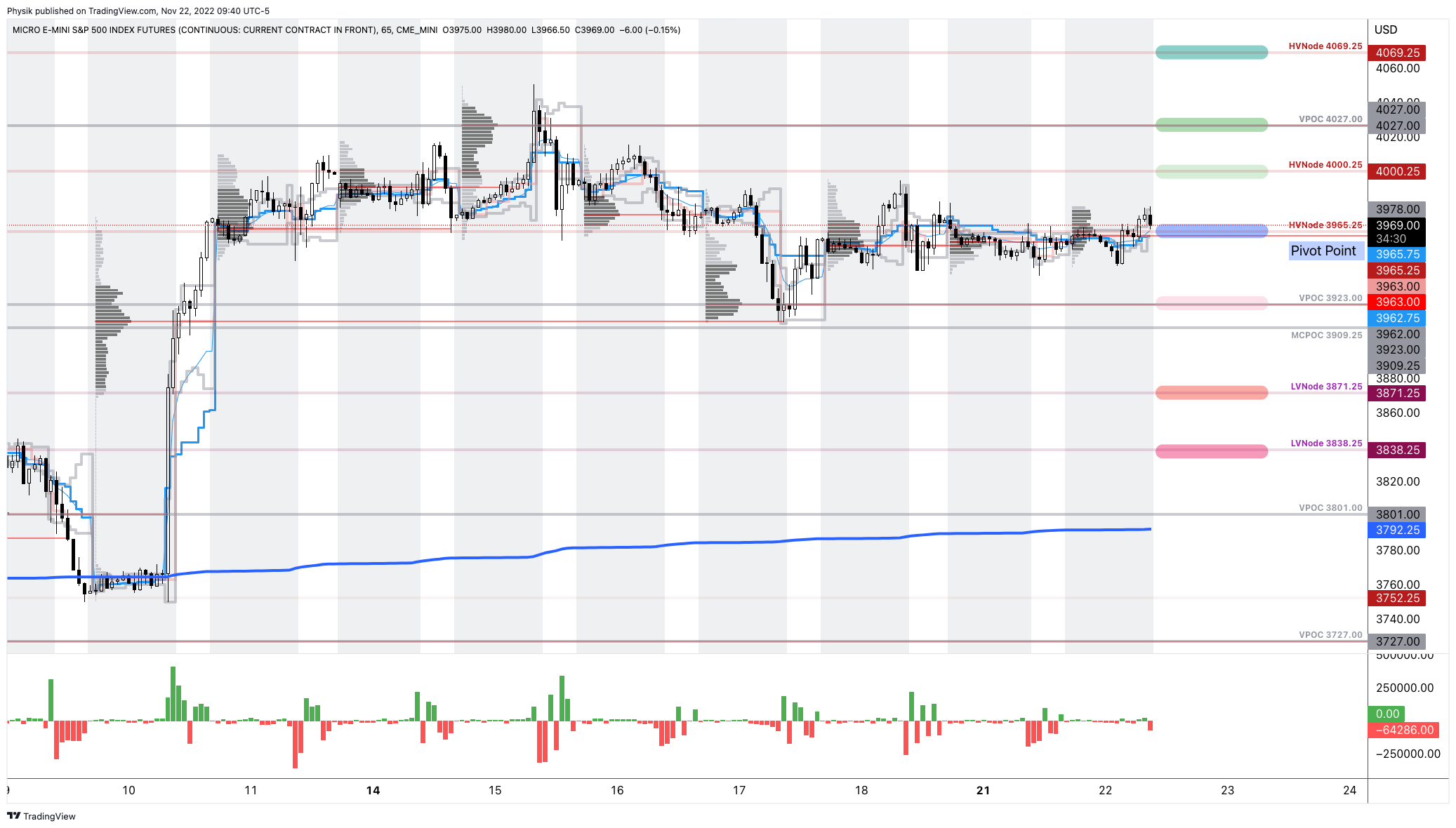

As some evidence, see the below graphic. Yesterday, the S&P 500 (INDEX: SPX) auctioned sideways (the bottom right) while breadth (the top left) was weak.

As SpotGamma put forward yesterday, in addition to the “support coming from the time decay that’s likely being pulled forward due to the holidays, implied volatility compressed and provided the market with that Vanna boost we talk much about.”

Accordingly, “[w]hen investors supply protection,” hence lower IVOL, counterparties “hedge in a manner that reduces market swings,” SpotGamma explained.

How do we capitalize on this information? A few ways stick out.

First, interesting are trades that bet on less whipsaw over the short term (e.g., sell a short-dated option and buy a far-dated option).

You are betting against movement (-Gamma) over a span of time you don’t think the market will move. And, you are betting on movement (+Gamma) over a larger span of time. In theory, using a calendar spread strategy as just described would position you for market movement when the context develops to “catalyze increased whipsaw.”

Second, if you own the S&P 500, sell call skew to fund put skew. By doing so, you will put yourself into a protective collar. For reasons we won’t go into today, according to a recent posting by IPS Strategic Capital’s Pat Hennessy, collars are an “attractive trade for those who are worried about the performance of stocks over the next year but do not want to sell or try timing the market.”

Lastly, if guaranteed returns are desired, box spreads enable you to create “a loan structure similar to a Treasury bill.” Upon maturity, the box spread earns a competitive interest rate. Price some trades at boxtrades.com.

Technical

As of 9:30 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a balanced skewed overnight inventory, just outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Our S&P 500 pivot for today is $3,965.25.

Key levels to the upside include $4,000.25, $4,027.00, and $4,069.25.

Key levels to the downside include $3,923.00, $3,871.25, and $3,838.25.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Bigger participants, some of whom move by a committee and seldom respond to technical nuances, are likely waiting for more information before entering and initiating an expansion of the range. For that reason, our key levels have held to the tick, per the below.

Our Daily Brief for November 18, 2022, went into why this type of push-and-pull occurs in detail.

Definitions:

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also writes options market analyses at SpotGamma and is a Benzinga journalist.

His past works include private discussions with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, the infamous Sam Bankman-Fried of FTX, former Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, the Lithuanian Delegation’s Aušrinė Armonaitė, among many others.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.