The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 900+ that read this report daily, below!

Fundamental

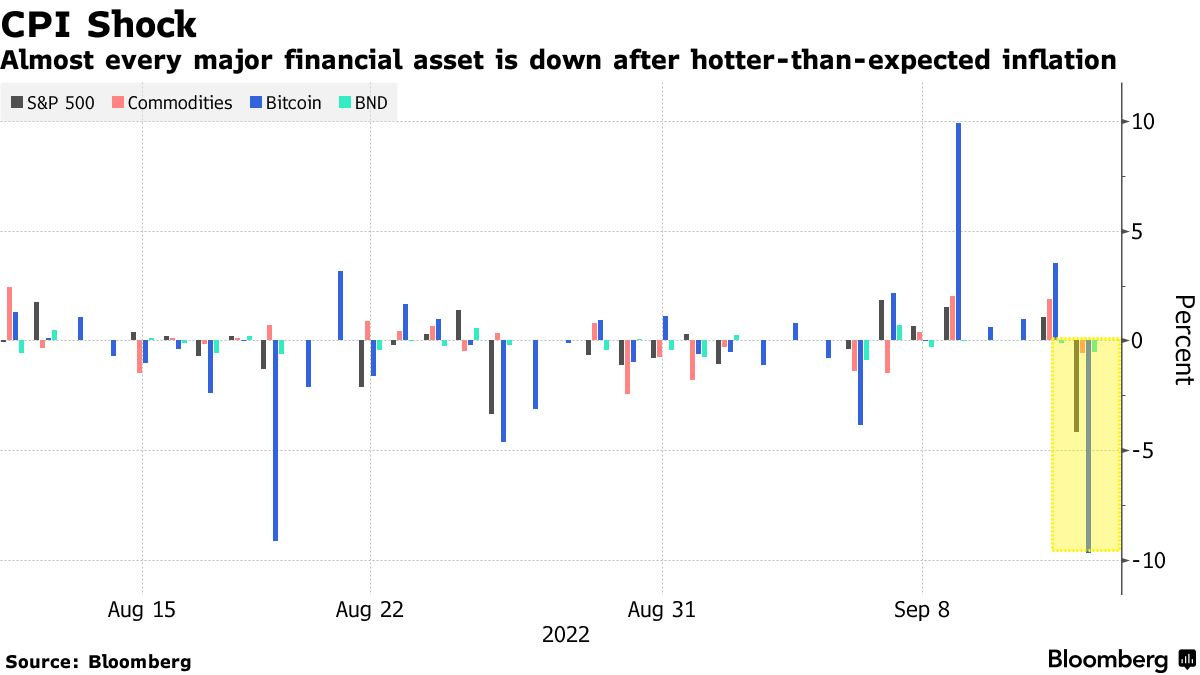

A sell-off spurred by a higher-than-expected Consumer Price Index (CPI) hit nearly all assets.

Expected was an 8.1% rise year-over-year (YoY) and a 0.1% fall month-over-month (MoM). Core CPI (excludes food and energy) was to rise by 6.1% YoY and 0.3% MoM, respectively.

Officially, the headline number rose to 8.3%. The core CPI rose 6.3% YoY and 0.6% MoM, meaning the March peak remains (6.5% YoY, then).

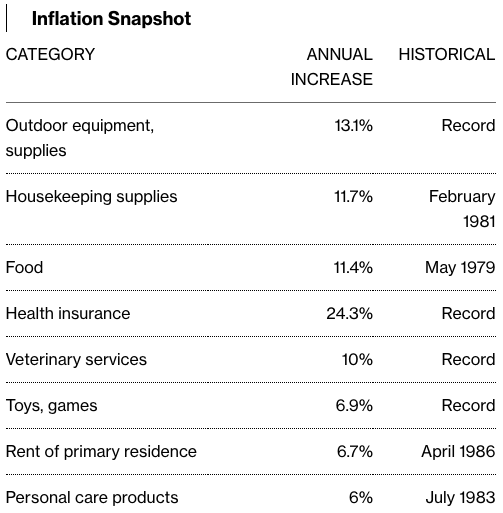

It’s the case, essentially, that “[a]ll measures came in above forecasts. Shelter, food and medical care were among the largest contributors to price growth,” per Bloomberg.

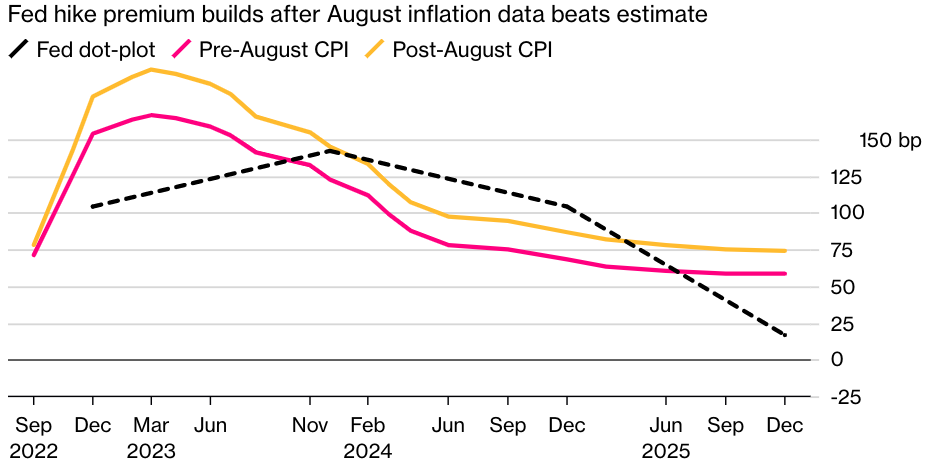

The data, which “illustrates a strong labor market and weakening consumer spending,” in total, bolsters the case for interest rates to rise by “three-quarters of a percentage point.”

Bloomberg’s Anna Wong and Andrew Husby add: “[W]ages have now become the top driver of inflation. With Fed officials already highly concerned about a potential wage-price spiral, the central bank is likely to keep hiking in the first half of 2023.”

The selling hit growth and technology, hard. These areas are far more responsive to changes in rates as there is promise embedded in their stock prices, too. When rates rise, prices are hit as the value of future earnings looks far less attractive versus higher-yielding or less-risky assets.

“Multiple compression will continue as long as we have sticky inflation,” said Marija Veitmane of State Street Corp (NYSE: STT). “Profits will crater. We still see a lot of downside on equities.”

Beyond risk assets, rising interest rates increase the cost of financing leaving households with less money to spend (or more hesitant to spend money), and this leads a decline in demand. Accordingly, business profits and economic growth may decline, too.

A conversation between Joseph Wang and Andy Constan, which we shall unpack in coming letters, deserves a listen. At its core, financial markets sold, primarily, on the “flow” of liquidity this year. Read the coming letters for more.

Positioning

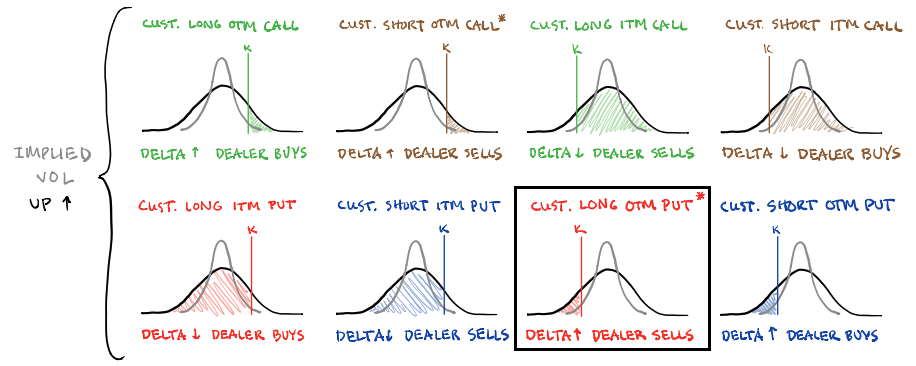

Traders sought shorter-dated equity put (downside) protection, in size, heading into Tuesday’s decline. Prior to the market open, Tuesday, we said that some “‘massive hedging activity’ feels ‘unsettling’” given what the “reaction to that protection entails should markets drop lower and [implied volatility] increase, accordingly.”

From thereon, options were repriced as markets sold and IVOL increased.

As I well put in a SpotGamma note last night, “it’s the case that [out-of-the-money] options went from having very little Delta (exposure to direction) to a lot more Delta. If we maintain the assumption that liquidity providers are short those puts, a positive delta trade, then those liquidity providers sold futures and stock, a negative Delta trade.”

In short, options out of the money are highly sensitive to changes in direction and IVOL, which there was a lot of, yesterday. Those options quickly went from having little value to a lot of value. If you’re short that exposure, and don’t want to lose money, you have to sell something, and the latter is what compounded the selling.

From hereon, as we said, a lot of the exposure demanded is short-dated. Should that exposure not be rolled forward in time, and allowed to expire, “SPX/ES dealers [who] are well hedged,” will unwind their hedges which may drive bullishness “through OpEx (options expiration),” says Kai Volatility Cem Karsan.

Notwithstanding, this “has [the] potential to drive a tail post” OpEx. In [the] tech/meme market melt-up of 2020-2021, positioning was [the] exact opposite.”

Technical

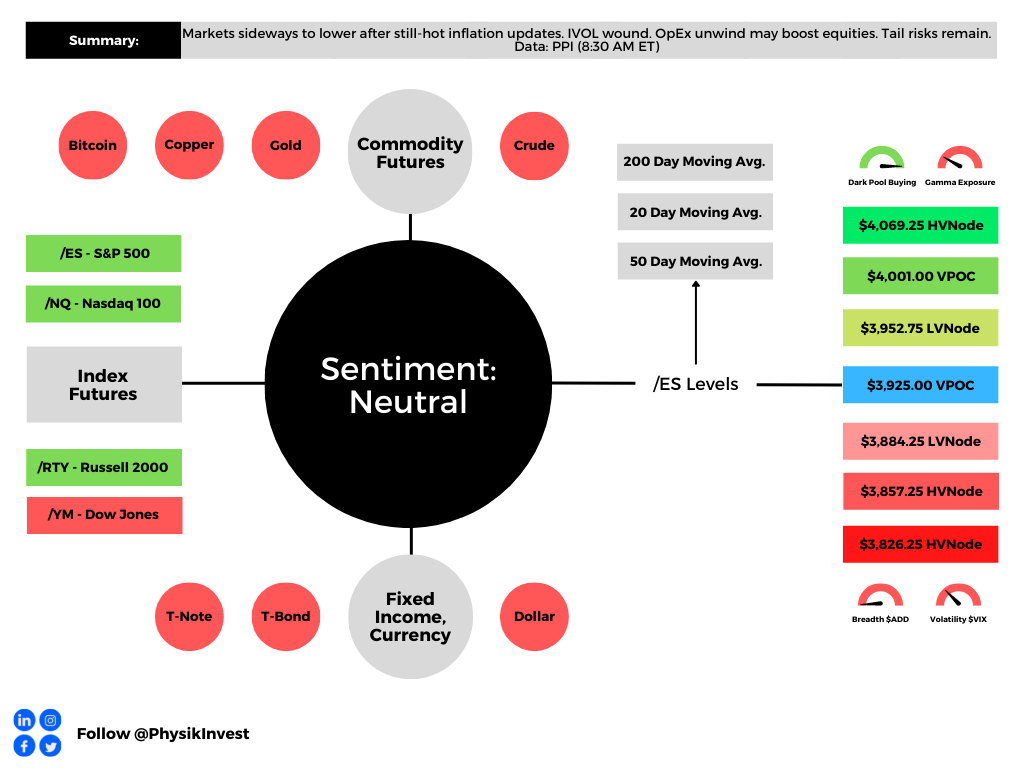

As of 8:10 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,952.00 VPOC puts into play the $3,952.75 LVNode. Initiative trade beyond the LVNode could reach as high as the $4,001.00 VPOC and $4,069.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,952.00 VPOC puts into play the $3,884.25 LVNode. Initiative trade beyond the LVNode could reach as low as the $3,857.25 and $3,826.25 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

One reply on “Daily Brief For September 14, 2022”

[…] – going to refer everyone to yesterday’s letter, a conversation between Joseph Wang and Andy Constan, as well as some updates Cem Karsan of Kai […]