Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

Fundamental

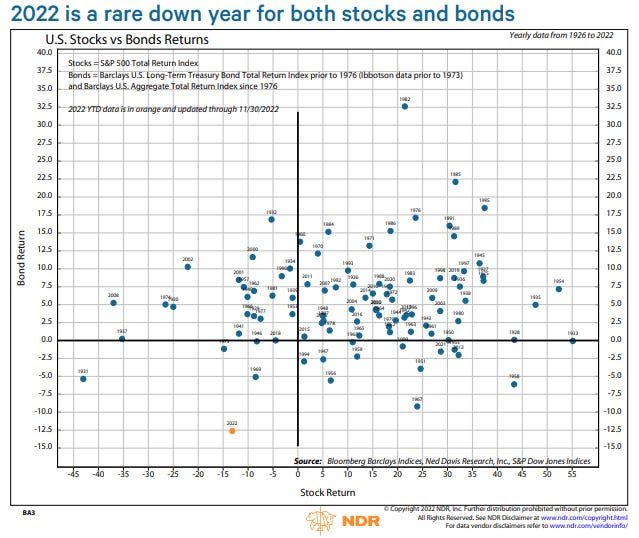

In a well-put statement by Tier1Alpha, “2022 was not a ‘classic’ bear market accompanying an earnings recession and economic slowdown, but rather a ‘rebalancing channel’ bear market.”

Essentially, as the Federal Reserve (Fed) raises interest rates and bond prices fall, equities are sold and “a ‘bear market’ occurs due to portfolio rebalancing,” as Michael Green well explained in a recent interview.

Further, some of the most sensitive (beaten) stocks have been in the technology and innovation sectors and, according to one article by Bloomberg’s John Authers, that’s not surprising.

“These companies are prone to fears of rising interest rates, especially since many of them are valued based on their projected profits far into the future. As the Federal Reserve presses on with its most aggressive tightening of monetary policy in decades, the future profits of tech firms will be worth far less at these higher interest rates. And with recession calls growing louder, it might just spell more trouble ahead for these firms.”

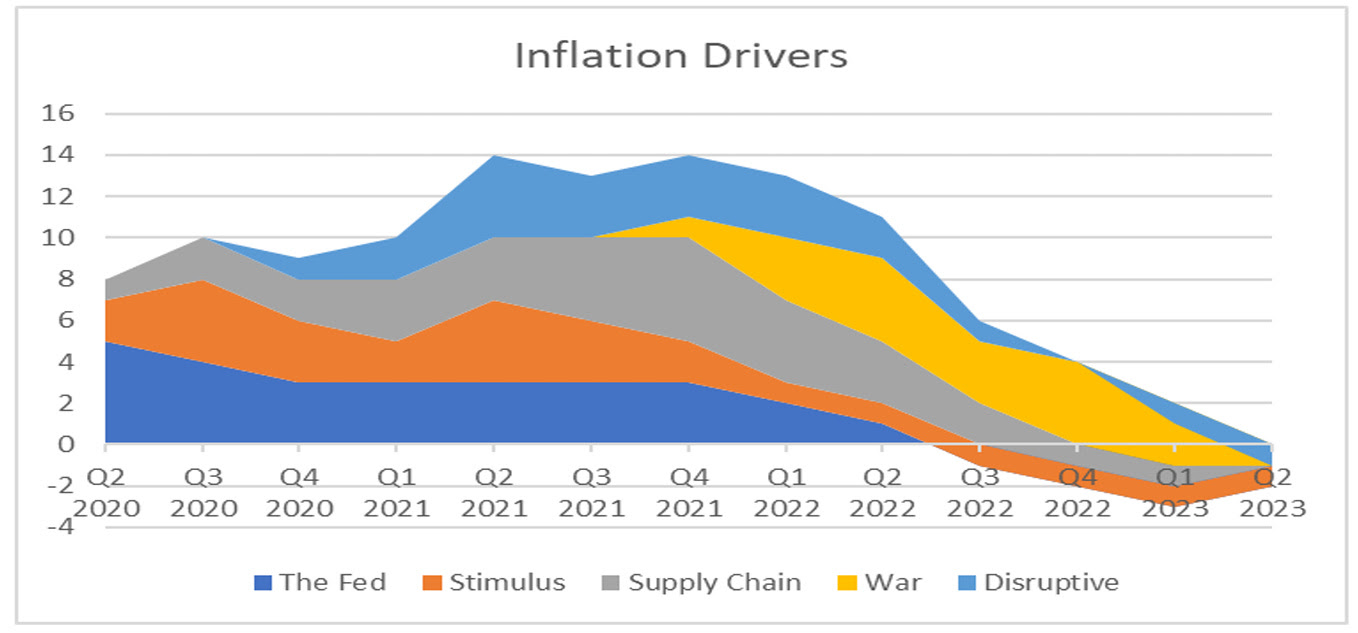

Moving on, given the rule of thumb – “past inflation spikes have never been vanquished until the federal funds rate exceeds the inflation rate” – in the realm of possibilities is a “crash … signaling to the Fed that they have raised rates enough.”

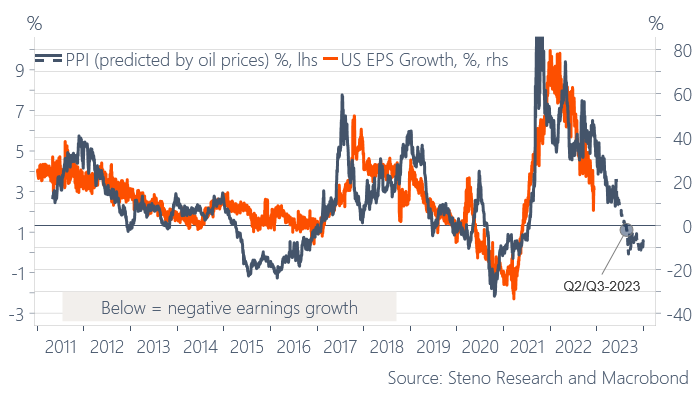

Likewise, per an article by Andreas Steno Larsen making the case for a comeback in deflation, equities have yet to price the negative EPS growth we’re likely to see.

“Those who find a lower inflation print a good opportunity to buy risk assets should look away now,” Steno Larsen said. “Remember that the PPI (and the CPI for that matter) is a leading indicator for EPS … if we allow the oil future to predict PPI, then we are in for negative EPS.”

Adding, Steno Larsen is in the camp that thinks “the 1970s playbook is intact.” When “the disinflation in goods spills over to services through the spring of 2023, … the Fed will pivot,” he explained.

Some come off as less pessimistic, though. The Fed is to ease sooner than expected; quantitative tightening (QT) is not likely to run its course, Joseph Wang said.

To explain, “an ideal QT would drain liquidity in the overall financial system while keeping liquidity in the banking sector above a minimum threshold. That is only possible if the bulk of the liquidity drained is sourced from the $2T RRP, which holds funds owned by money market funds. MMFs could facilitate QT by withdrawing funds from the RRP to invest in the growing supply of Treasury bills, but recent data suggests they have lost interest in bills. Households [which include hedge funds] appear to have replaced MMFs as the marginal buyer of bills and are funding their purchases out of funds held in the banking sector. This suggests QT may lower banking sector liquidity below the Fed’s comfort level much earlier than anticipated.”

Hence, the downside that has yet to happen may prove not to be as material. A potential consequence, as Steno Larsen sees, is “double inflation,” bolstered by inflationary deglobalization trends that may accelerate.

For equities, “a revisit of the $3,500.00-$3,600.00 zone should be on the cards for S&P 500,” he said, while other markets, like housing, may see drawdowns reaching “15-20%” in the base case.

We’ll go into more depth on certain points next week. Hope this was a great way to set the stage for future conversations.

Technical

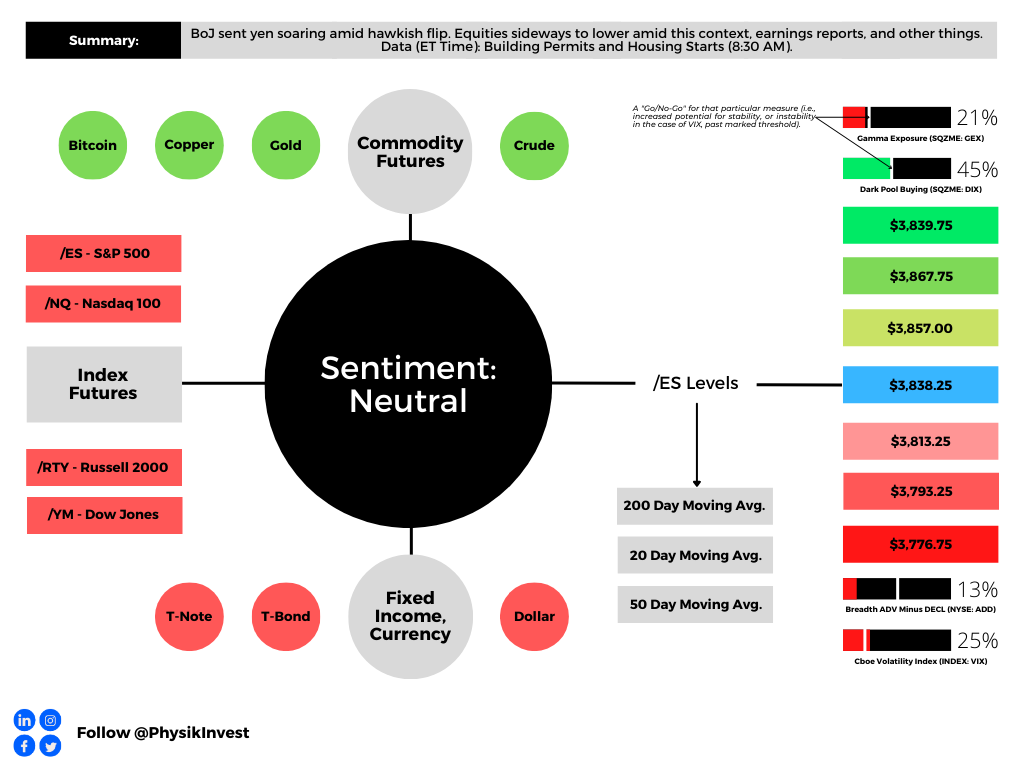

As of 9:25 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Our S&P 500 pivot for today is $3,838.25.

Key levels to the upside include $3,857.00, $3,867.75, and $3,893.75.

Key levels to the downside include $3,813.25, $3,793.25, and $3,776.75.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: Denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

In short, an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.