The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

Overnight, equity index futures auctioned higher, inside of the prior range, with bonds. Commodities were mixed and implied volatility measures were bid.

Yields fell after comments by Federal Reserve (Fed) Chair Jerome Powell and growth updates in Europe stoked fears of a global downturn, per Bloomberg, as the prospects of a soft-landing look “very challenging.”

“Financial conditions have tightened and priced in a string of rate increases and that’s appropriate,” Powell said. “We need to go ahead and have them.”

Today we’ll dive into positioning – what’s promoting responsive trade – and how to think about the market, accordingly.

Ahead is data on jobless claims and current account (8:30 AM ET), as well as S&P Global Inc (NYSE: SPGI) manufacturing and services PMI (9:45 AM ET), followed by the Federal Reserve (Fed) Chair Jerome Powell’s testimony (10:00 AM ET).

What To Expect

Positioning: Fed Chair Powell added clarity to the central bank’s stance on policy, and its intent to tighten without pushing the economy into a recession, which we’ve argued we’re already in.

“The other risk, though, is that we would not manage to restore price stability and that we would allow this high inflation to get entrenched in the economy,” Powell said. “We can’t fail on that task. We have to get back to 2% inflation.”

The peak of the Fed-rate-hike cycle – terminal rate – now sits at December 2022.

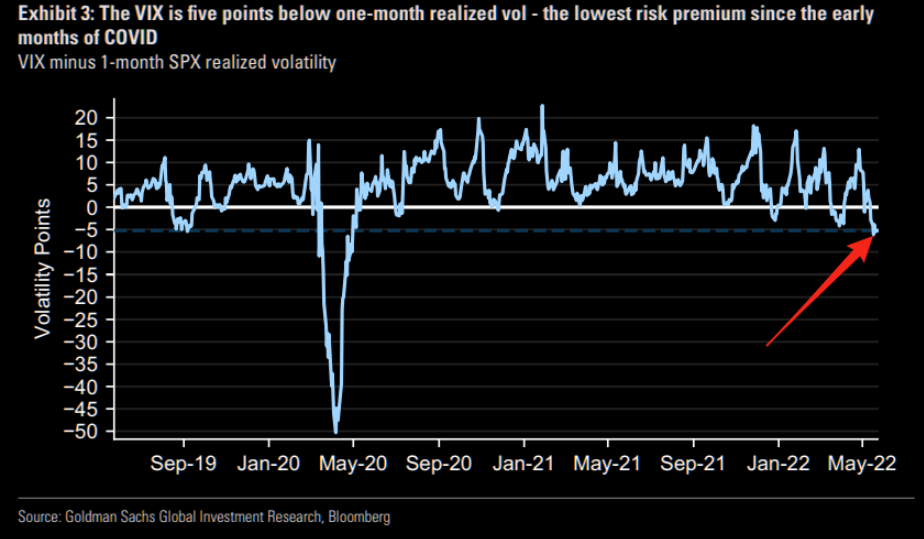

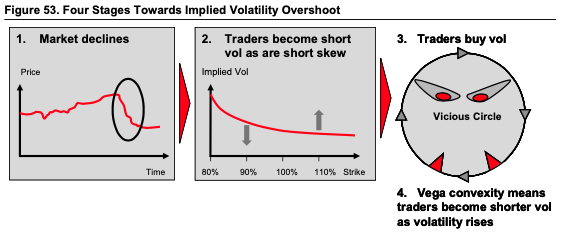

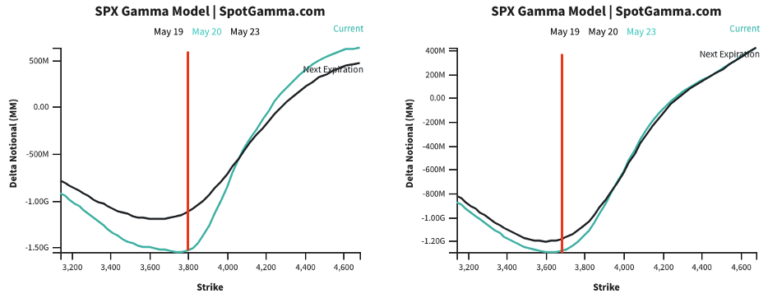

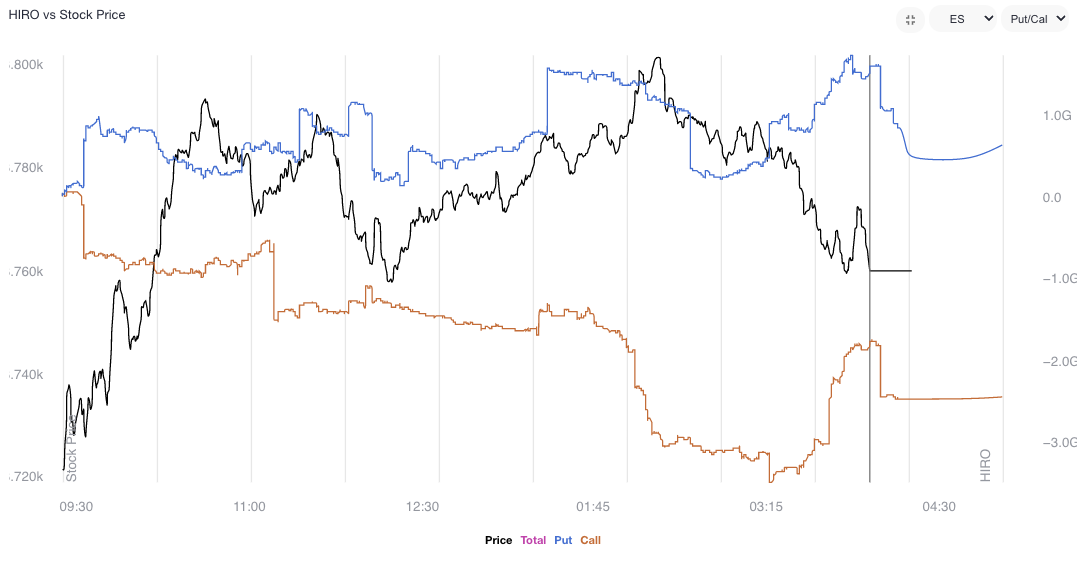

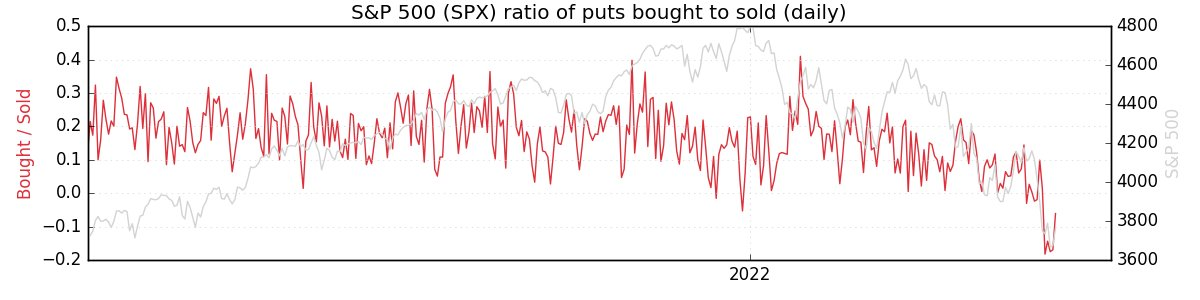

A feature of the equity sell-off is the suppression of implied volatility (IVOL) versus that which the market realizes (RVOL).

As talked about before, participants are hedged and volatility remains in strong supply. Options data and insights platform SqueezeMetrics explains that this is due in part to lower leverage.

“Leveraged long S&P lost favor (understandable), and marginal demand for puts went with it. Creeping into net selling territory is ‘smart’ bear market positioning. Short delta, short skew.”

Accordingly, it remains profitable to own options structures.

“This is the opposite of 2017 where the VIX was at 10% and the realized was 7%,” a trade that leverage poured into and resulted in the spectacular short-volatility ‘Volmageddon’ blow-up in February of 2018,” Dennis Davitt of Millbank Dartmoor Portsmouth explains.

Read: Daily Brief for May 24, 2022.

How to play?

IVOL is bid and at a “higher starting point,” as I described in a SpotGamma note. Noteworthy, too, was the change in tone with respect to the non-linearity and strength of volatility with respect to linear changes in asset prices.

Read: Daily Brief for June 16, 2022.

In the current environment, we have to ask ourselves what would hurt participants the most?

It’d likely be forced selling or demand for protection by a greater share of the market in ways not seen. The associated repricing of IVOL would be a boon for those who own options, particularly in strikes further from current prices where there is a ton more convexity in volatility.

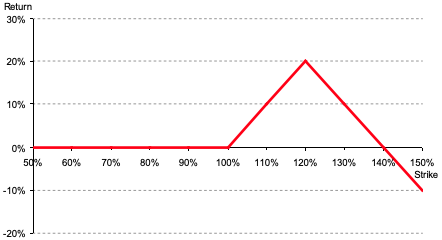

Still, with volatility at that higher starting point, many have exposure to positive delta (options that increase in value if the market goes up, all else equal) and gamma (the amplification of profits as the underlying continues to trade higher).

That (insignificant) demand in the right tail still makes it so we may position, for cheap, in spread structures that still offer attractive and asymmetric payouts (e.g., 500 to 1000 point wide Nasdaq 100 butterflies and ratio spreads maturing up to 20 or 30 days out).

Read: Trading Volatility, Correlation, Term Structure and Skew by Colin Bennett et al. Originally sourced via Academia.edu.

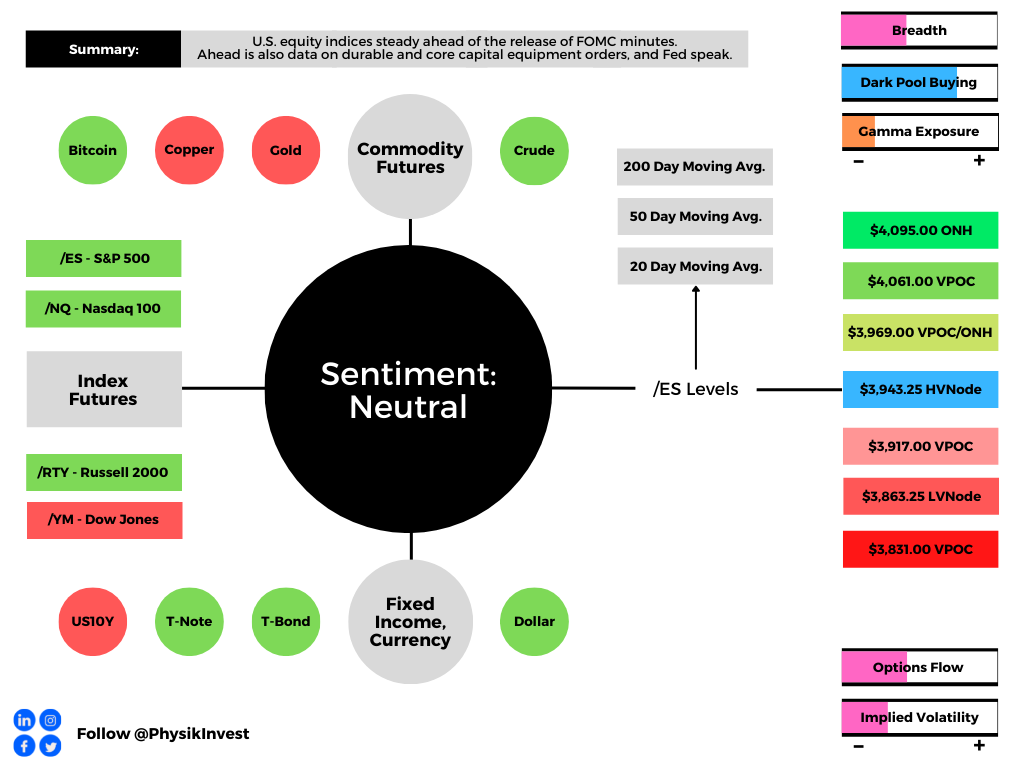

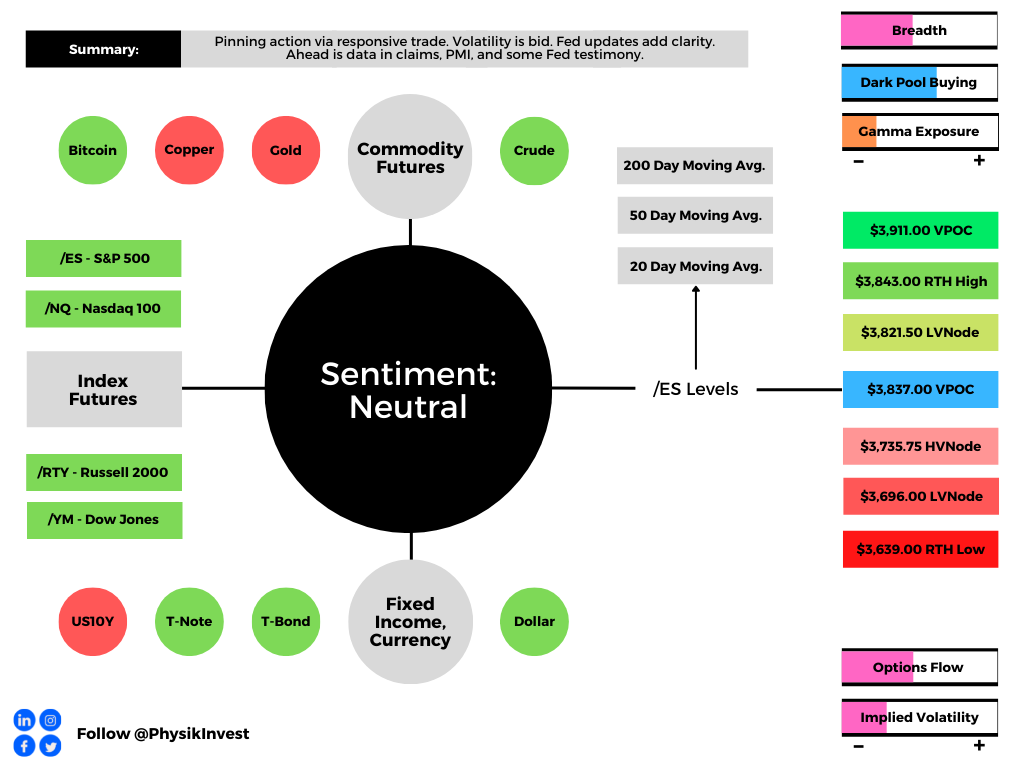

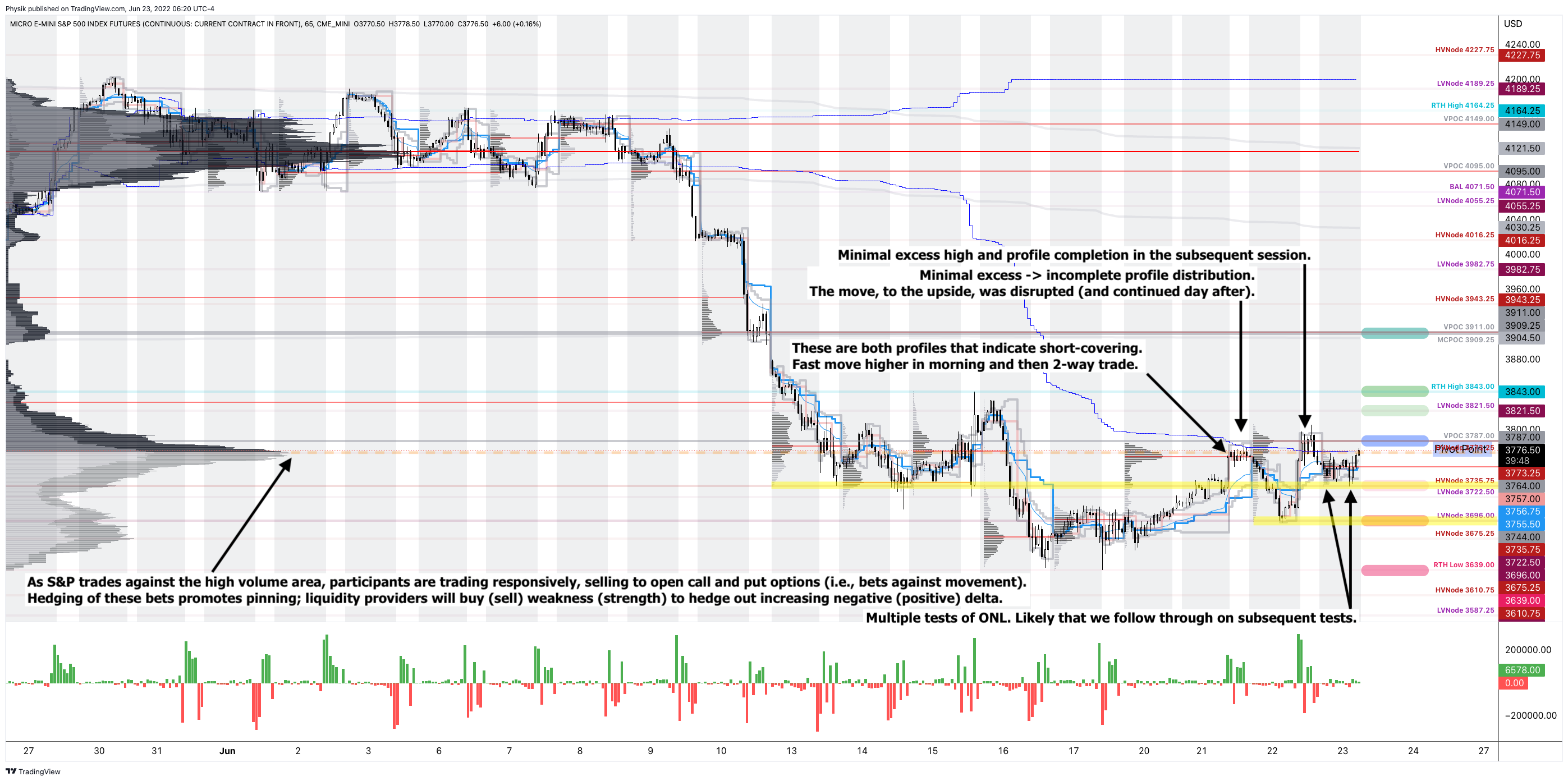

Technical: As of 6:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $3,787.00 VPOC puts in play the $3,821.50 LVNode. Initiative trade beyond the LVNode could reach as high as the $3,843.00 RTH High and $3,911.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower; activity below the $3,787.00 VPOC puts in play the $3,735.75 HVNode. Initiative trade beyond the $3,735.75 HVNode could reach as low as the $3,696.00 LVNode and $3,639.00 RTH Low, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: The SPDR S&P 500 ETF Trust (NYSE: SPY) is above the convergence of a key anchored volume-weighted average price level and retracement.

In the case of a continued downside, that is an area where participants may see a response.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

Modus operandi is responsive trade (i.e., fade the edges), rather than initiative trade (i.e., play the break).

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.