The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

Overnight, equity index futures probed outside of the prior day’s large trading range but quickly rotated back inside. Overall, the major indexes and commodities were higher. Volatility was bid.

In the news was President Biden’s remark that the U.S. would intervene with the military to defend Taiwan from a China invasion.

This is just as the administration unveiled a 13-nation economic pact to assert Asia leadership. In response, China’s Foreign Minister Wang Yi said the pact was “doomed to fail.”

In other news, the U.S. got its first 70,000 pounds of baby formula to ease shortages. Beijing saw the most cases of a new COVID-19 outbreak, and Russia may ease key FX limits.

Ahead, there is no data scheduled to be released. Today’s commentary will be lighter.

What To Expect

Fundamental: A shortened commentary to start our Monday.

JPMorgan Chase & Co’s (NYSE: JPM) Chief U.S. economist Michael Feroli notes that as the Federal Reserve gains traction in cutting financial conditions, the U.S. is, indeed, likely to grow slower in 2H22 and 2H23.

“A stronger dollar, lower equity prices, and higher mortgage rates will weigh on demand,” The Market Ear said in their summary of Feroli’s remarks.

“Over time weaker output demand should lead to weaker labor demand.”

Positioning: Wrote an explainer on market weaknesses, from a positioning perspective, via Benzinga. Check out, if interested. Alternatively, read Friday’s in-depth letter, also.

Mainly, we’re in an environment characterized by volatility suppressing activities and an “observed divergence in the volatility realized, versus that which is implied by options activity.”

Moreover, OPEX coincided with the removal of a lot of put delta (i.e., exposure to direction).

Those who are on the other side (e.g., liquidity providers or market makers), who were short these puts (a positive delta trade) protecting investors to the downside, are to buy back their short stock and futures hedges (a negative delta trade, initially) to re-hedge.

That means markets have less pressure (negative delta) to contend with in their attempts up.

Ultimately, options analysis service SpotGamma thinks that “[a]ny ultimate rally off of OPEX [is] subject to swift reversals.”

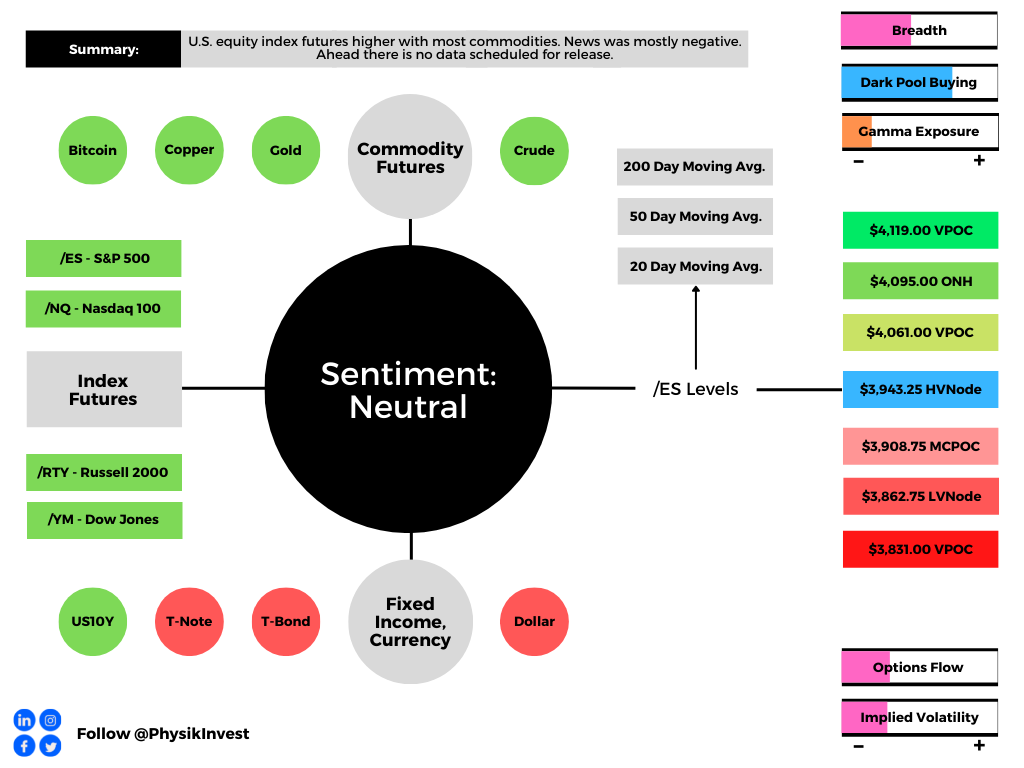

Technical: As of 6:30 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $3,943.25 high volume area (HVNode) puts in play the $4,061.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,095.00 overnight high (ONH) and $4,119.00 VPOC, or higher.

In the worst case, the S&P 500 trades lower; activity below the $3,943.25 HVNode puts in play the $3,908.75 micro composite point of control (MCPOC). Initiative trade beyond the MCPOC could reach as low as the $3,862.75 (low volume area) LVNode and $3,831.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

One reply on “Daily Brief For May 23, 2022”

[…] is as banks UBS Group AG (NYSE: UBS) and JPMorgan Chase & Co cut their expectations for growth here and […]