The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures auctioned sideways, mostly, after a weak close, Thursday.

Measures of implied volatility remained bid while bonds rose after yields briefly surpassed 1.9%.

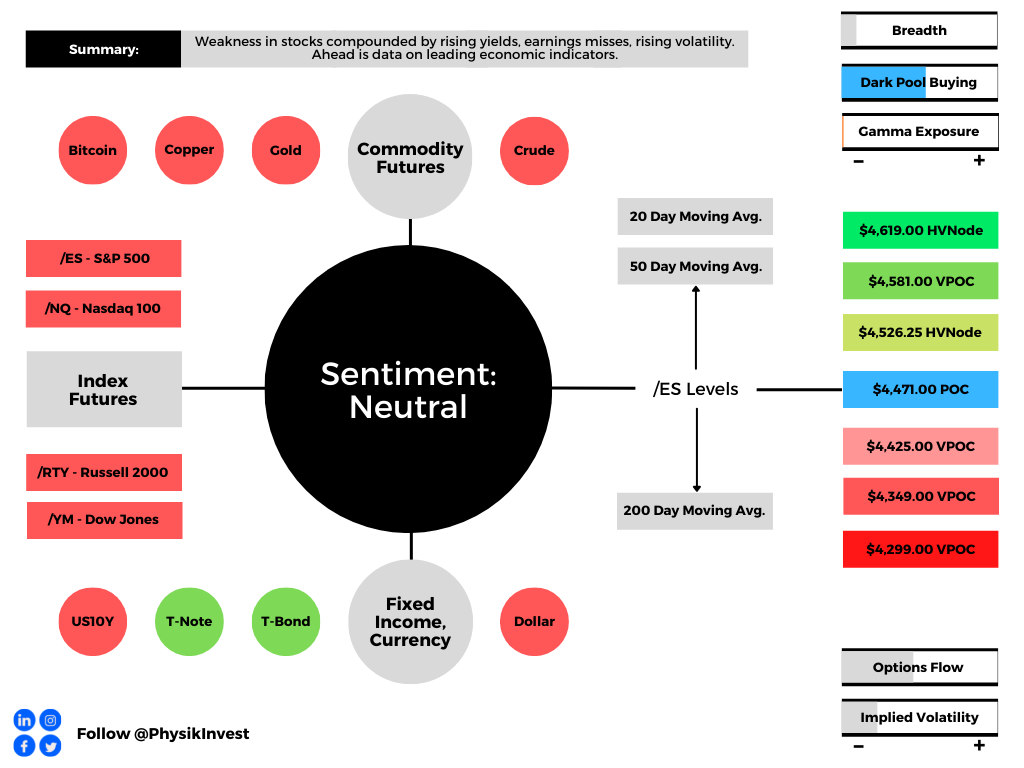

Ahead is data on leading economic indicators (10:00 AM ET).

What To Expect

Fundamental: The Nasdaq dipped into correction territory as stocks extended lower, Thursday.

Weakness was compounded by geopolitical tensions, the prospects of reduced stimulus to combat high inflation, as well as poor responses to earnings results.

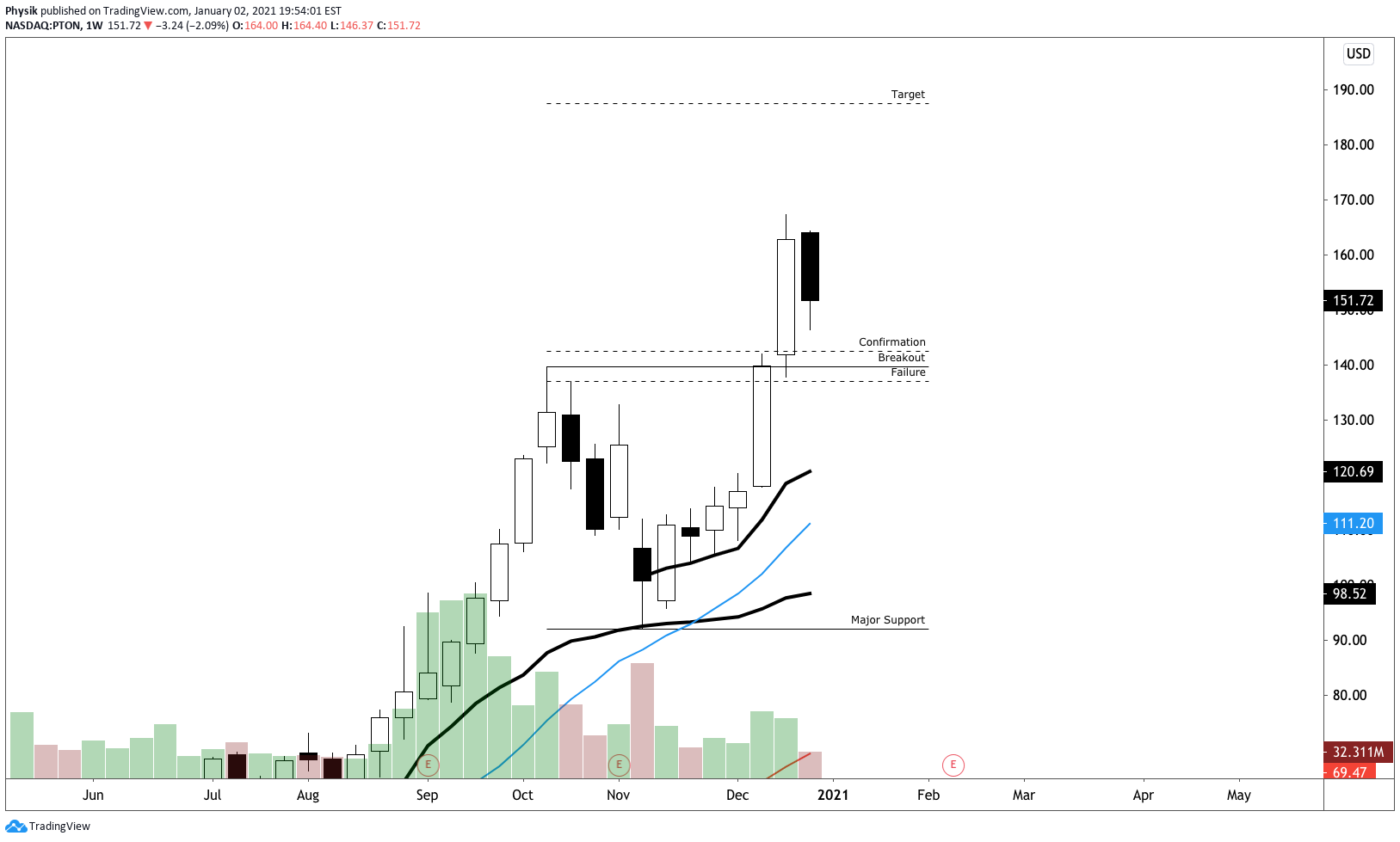

Shares of Amazon Inc (NASDAQ: AMZN) just missed the round $3,000.00 figure and Peloton Interactive Inc (NASDAQ: PTON) fell on waning demand, while Netflix Inc (NASDAQ: NFLX) traded down just over 20.00% on a weak subscriber outlook.

“Thursday’s trading pattern looks exactly like a typical session from the summer of 2007 as the sub-prime crisis was beginning to send the first shock waves through the stock market,” said Bloomberg’s John Authers on wild changes in sentiment exacerbating the volatility.

“Big changes of direction in the last hour, with no obvious news to trigger them, became a fact of life.”

Moreover, with pandemic-era speculation still embedded in prices, Authers adds, the removal of central bank liquidity opens the door to even lower prices as the “process to correct a lot of excess is now underway.”

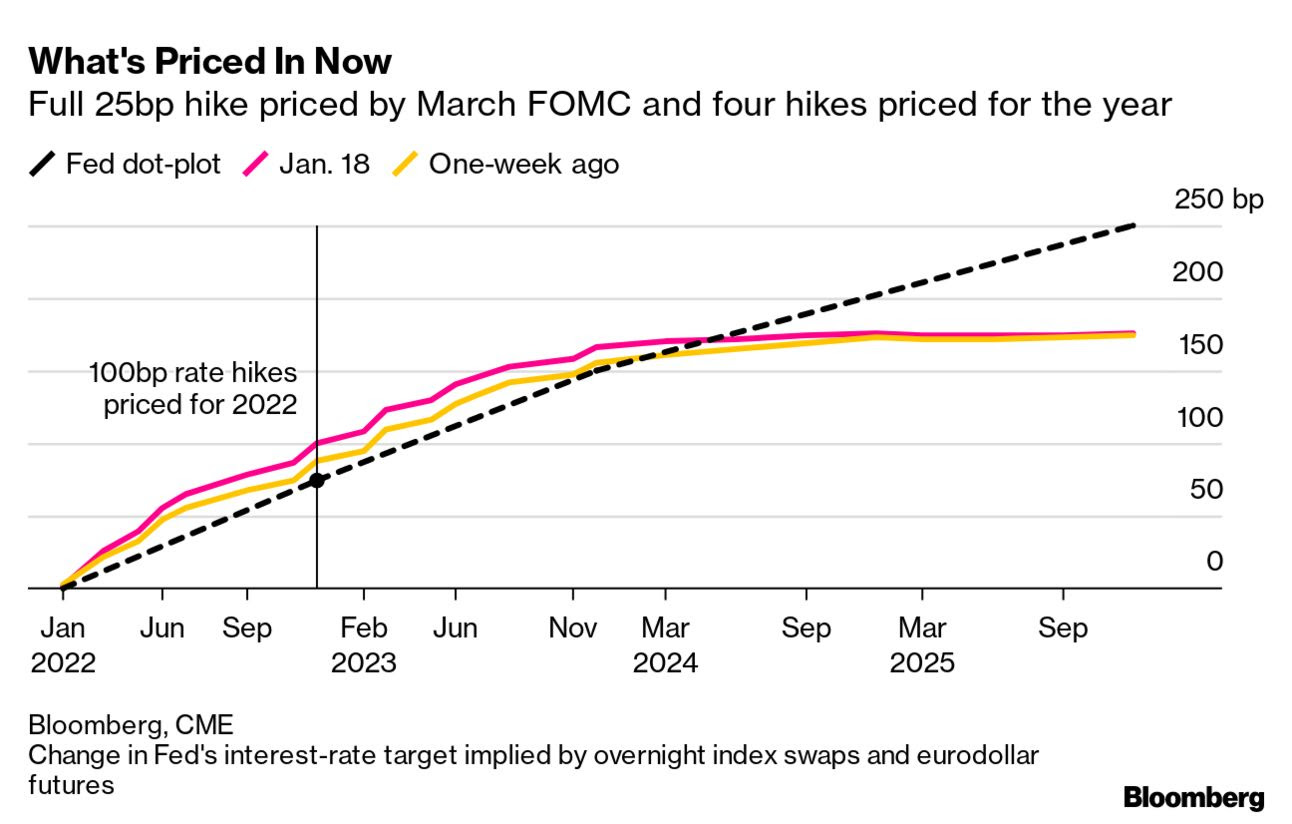

Regardless of how aggressive contractions in monetary policy are, the Federal Reserve will spell out its plans well in advance, Fed Governor Christopher Waller explained.

“I don’t see a 50 basis point hike in March. We have not prepared markets for anything that dramatic. One of our key themes has been not to surprise market, giving well enough advance, in terms of what we’re trying to do.”

At present, a full 25 basis point hike is priced by March.

Per S&P Global Inc (NYSE: SPGI) analyses, these hikes are likely to “cause shorter-term rates, such as the 1- and 2-year Treasury yields, to climb more rapidly than longer-term rates,” potentially pressuring consumer credit, and increasing the costs of loans.

“By launching the reduction in the balance sheet, the Fed could match the rise in short-term rates with a similar rise in longer duration rates,” thus reducing the Fed’s need to hike rates, S&P Global explained.

“Given mortgage rates and corporate borrowing costs are more impacted by movements in 10-year yields than 3-month rates, the Fed funds target rate may not need to be increased as aggressively to get inflation under control,” James Knightley, an ING Groep NV (NYSE: ING) economist, added.

Positioning: Per Morgan Stanley’s (NYSE: MS) prime brokerage data, investors are deploying a more defensive tilt to portfolios in the face of a deceleration in sales and margin compression.

This “stock liquidation played into the large negative gamma position which accelerated selling into the close,” according to options modeling and analysis service SpotGamma.

For context, “when a position’s delta falls (rises) with stock or index price rises (falls), the underlying is in a negative-gamma environment.”

In such an environment, the expansion of volatility as a result of demand for downside (put) protection (a lot of which is short-dated and increasingly sensitive to direction) for instance, leaves dealers compounding weakness.

Therefore, in the case of heightened demand for downside put protection (a negative-delta trade), higher implied volatility increases dealer exposure positive delta.

To offset this positive delta exposure, dealers sell more underlying, exacerbating weakness.

The passage of the monthly options expiration (OPEX) ought to clear some of the put-heavy positioning; “removal of this exposure post-OPEX,” coupled with a reduction in embedded event premiums tied to the approaching Federal Open Market Committee (FOMC) event, “will leave dealers with less positive delta exposure to sell against.”

This opens up a window of strength wherein dealers are to take less liquidity (buy strength and sell weakness) and pressure less the market in hedging put-heavy positioning.

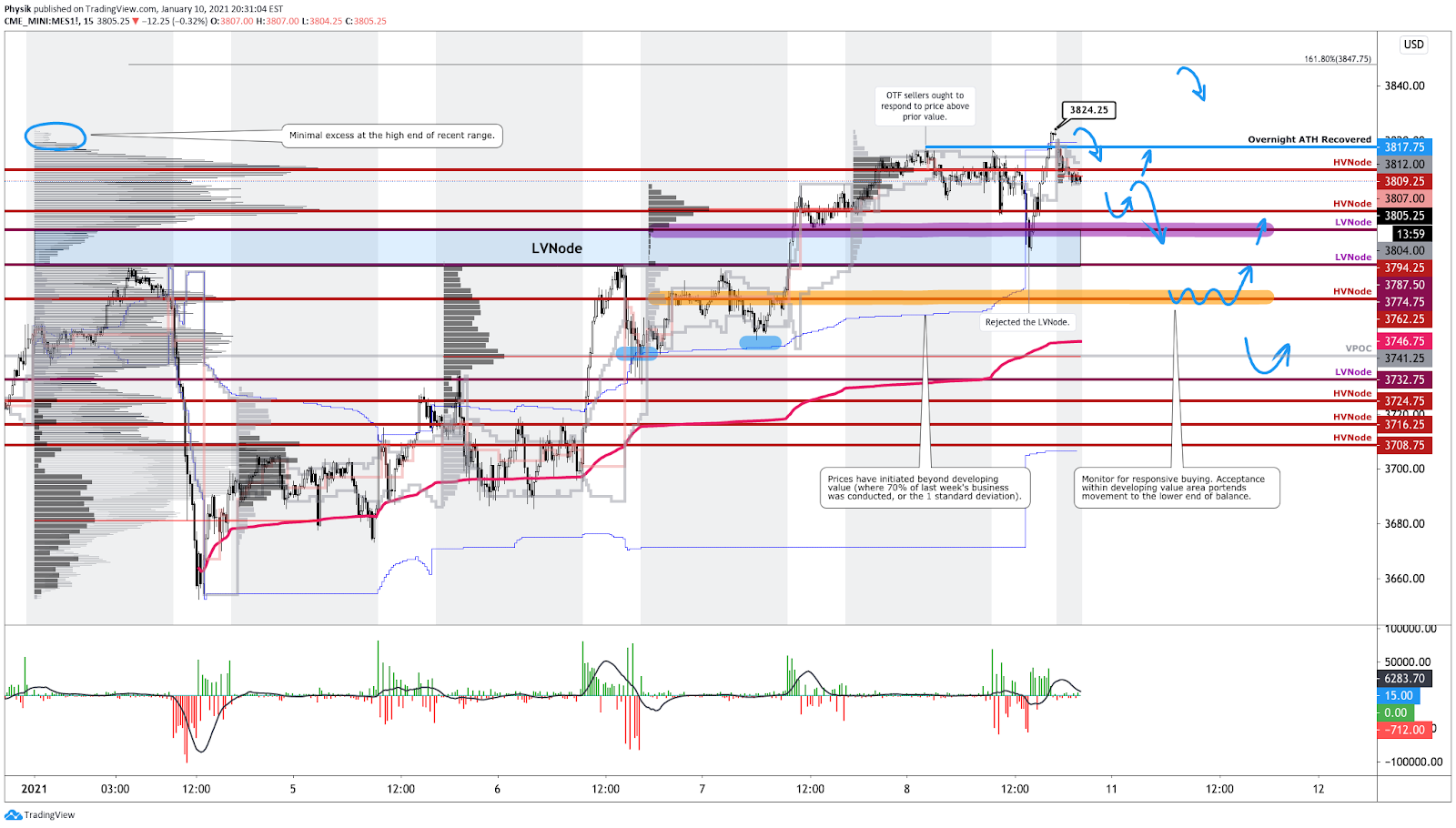

Technical: As of 6:30 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Spikes: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike). The base is $4,549.00.

In the best case, the S&P 500 trades higher; activity above the $4,471.00 point of control (POC) puts in play the $4,526.25 high volume area (HVNode). Initiative trade beyond the HVNode could reach as high as the $4,581.00 untested point of control (VPOC) and $4,619.00 HVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,471.00 POC puts in play the $4,425.00 VPOC. Initiative trade beyond the $4,425.00 VPOC could reach as low as the $4,349.00 and $4,299.00 VPOCs, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.