Physik Invest’s Daily Brief is read free by thousands of subscribers. Join this community to learn about the fundamental and technical drivers of markets.

Administrative

Time for something inspiring! Separate from his work at Physik Invest, founder Renato Leonard Capelj is a journalist interviewing global leaders in business, government, and finance. In his desire to learn and apply the methods of those others who are far more experienced, Capelj has a long list of interviews you may find helpful in strengthening your understanding of markets. Check out some recent ones!

March 10, 2023: Portfolio Manager Prefers Option, Bond Overlays To Hedge Big Uncertainty Facing Markets

Capelj spoke with Simplify Asset Management’s Michael Green about cutting investors’ portfolio volatility while amplifying profit potential.

In response to uncertainty, Green says investors can park cash in short-term near-risk-free bonds yielding 5% or more, as well as allocate some capital to volatility “to introduce a degree of convexity,” risking only the premium paid. Alternatively, investors can take a more optimistic long view and position in innovations like artificial intelligence or next-generation energy production.

January 8, 2023: Two Major Risks Investors Should Watch Out For In 2023

Capelj spoke with The Ambrus Group’s Kris Sidial about his market perspectives.

Naive measures like the VVIX, which is the volatility of the VIX or the volatility of the S&P 500’s volatility, are printing at levels last seen in 2017, Sidial explains, noting this would suggest “we can get cheap exposure to convexity while a lot of people are worried.”

“Even if inflation continues, the rate at which it rises won’t be the same. Due to this, CTA exposures likely will not perform as well as they did in 2022, and that’s why you may see more opportunities in the volatility space.”

Capelj spoke with Damped Spring Advisors’ Andy Constan about what investors should focus on and how he creates trades that lose him less money.

Constan’s trades are constructed around two- to four-month time horizons and are structured long and short using defined-risk options trades like debit or credit spreads, depending on whether volatility is cheap or expensive.

“I want deltas and leverage. My macro indicators give me an edge on price and in the worst case, the loss is limited to 10%, if everything has to go against me all at once. I can be 100% invested and only risk 10%.”

Capelj spoke with 42 Macro’s Darius Dale about his Wall Street story and perspectives on life and markets.

“We’re tracking at an above-potential level of output in terms of the growth rate of output. We’re also slowing and the pace of that deceleration is likely to pick up steam in the coming quarters.”

By 2023, that process is likely to “catalyze pressure on asset markets through the lens of corporate earnings and valuations you assign to a lower level of growth.”

July 22, 2021: ShadowTrader’s Peter Reznicek On His Early Days, Tips For Success And Evolution

Capelj spoke with ShadowTrader’s Peter Reznicek about his start, perspectives, success tips, and visions for the future.

Reznicek recalled two turning points in his trading career.

The first was learning from expert floor traders involved with the thinkorswim team.

“That was really the genesis of where I started to learn the broken-wing butterfly, ratio spread and things like that,” he shared.

Floor traders, according to Reznicek, had low capital requirements. As a result, they could put on strategies like the 1×2 ratio — a debit spread with an extra short option — for a low cost.

(See parts 1, 2, and 3 of ShadowTrader’s how-to series on ratio spreads.)

“On the floor, it is either go big or go home,” he chuckled, remarking that ratio spreads were the way of the casino. “You either get rich or they take your house. So, why would you put on any other spread?”

The next big turning point was Jim Dalton, who’s been a member of the Chicago Board of Trade, as well as a member of the Chicago Board Options Exchange (CBOE) and senior executive vice president of the CBOE during its formative years.

“I’m still in touch with him on a regular basis and I consider him a friend,” Reznicek said in a discussion on Dalton’s works like Mind Over Markets and Markets in Profile, as well as his use of WindoTrader Market Profile software. “I went to Chicago twice to see him teach live … and I came home from those seminars with five, six, 10 pages of notes. The nuances of profile continue to mold me.”

Capelj spoke with Kai Volatility Advisors’ Cem Karsan about the implications of record valuations and the growth of derivatives markets on policy, the economy, and financial markets.

“It’s not a coincidence that the mid-February to mid-March 2020 downturn literally started the day after February expiration and ended the day of March quarterly expiration. These derivatives are incredibly embedded in how the tail reacts and there’s not enough liquidity, given the leverage, if the Fed were to taper.”

July 13, 2021: Ambrus Group CIO On Taking Advantage Of Volatility Dislocations

Capelj spoke with The Ambrus Group’s Kris Sidial to understand how to capitalize on volatility dislocations.

Unlike standard tail-risk funds which systematically buy equity puts, Ambrus’ approach is bespoke, cutting down on negative dynamics like decay with respect to time.

Given dislocations across single stock skew, term structure, and volatility risk premium, Ambrus will position itself in options with less time to maturity, buying protection up to six weeks out.

“The market will underestimate the distribution,” Sidial said in a conversation on Ambrus’ internal models that spot positional imbalances to determine who is off-sides and in what single asset. “We’re buying things that have happened before and we’re looking for it to carry a heavier beta when the sell-off happens.”

So, by analyzing flow, as well as using internal models to assess the probabilities of deleveraging in a risk-off event, Ambrus is able to venture into individual stocks where there may be excess fragility; “I know if stock XYZ goes down five percent, it’s going to go down 10% because this fund needs to deleverage.”

To aid the cost to carry, Ambrus utilizes defined-risk, short-volatility, absolute return strategies.

“I’m basically giving you a free put on the market – with a ton of convexity – with something that offers a payout that’s just more than a regular put,” Sidial summarized. “If the market doesn’t do anything, and we do an amazing job, we’re flat and you made money on all your long-only equity exposure.”

“You had a free hedge the entire time.”

February 1, 2021: Volatility Arbitrage Trader Talks GameStop, Market Microstructure, Regulation

Capelj spoke with The Ambrus Group’s Kris Sidial about the meme stock debacle of 2021.

“You have distressed debt hedge funds that focus on shorting these types of companies. Melvin Capital is the one that is singled out due to the media, but they aren’t the only ones.”

Market participants added to the crash-up dynamics. Retail investors aggressively bought stock and short-term call options, while institutional investors further took advantage of the momentum and dislocations.

“You have this dynamic in the derivatives market where there is a gamma squeeze when people are buying way far out-of-the-money calls, and dealers reflexively have to hedge off their risk,” Sidial said.

“It causes a cascading reaction, moving the stock price up because dealers are short calls and they have to buy stock when the delta moves a specific way.”

The participation in the stock on the institutional side has not received much attention, he said.

“We’ve noticed that some of the flow is more institutional,” he said in reference to activity on the level two and three order books, which are electronic lists of buy and sell orders for a particular security.

“You have certain prop guys and other hedge funds that understand what’s going on, and they’re trying to take advantage of it, as well.”

This institutional activity disrupted traditional correlations and caused shares of distressed debt assets like GameStop, BlackBerry Ltd, and AMC Entertainment Holdings Inc to trade in-line with each other.

“This was not some WallStreetBet user, … if you look at how some of these things were moving premarket, you would see GME drop like 2%, BB’s best bid would drop and AMC’s best bid would drop. That’s an algo.”

The takeaway: although the WallStreetBets crowd is getting most of the blame, institutions are also at fault for the volatility.

Technical

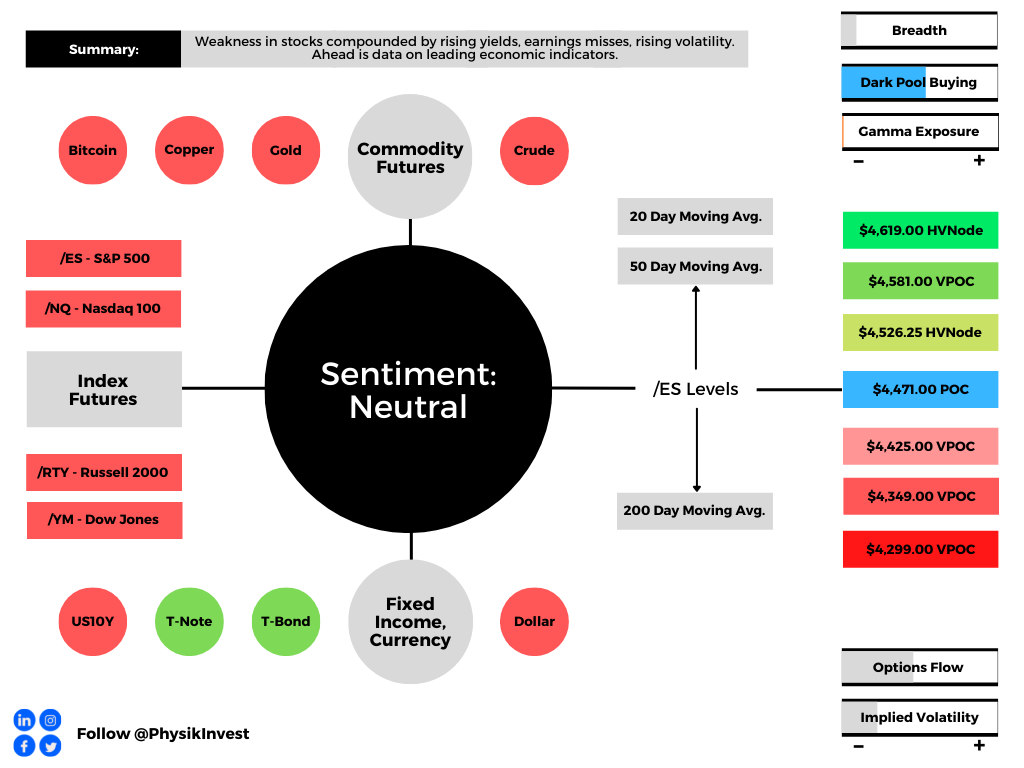

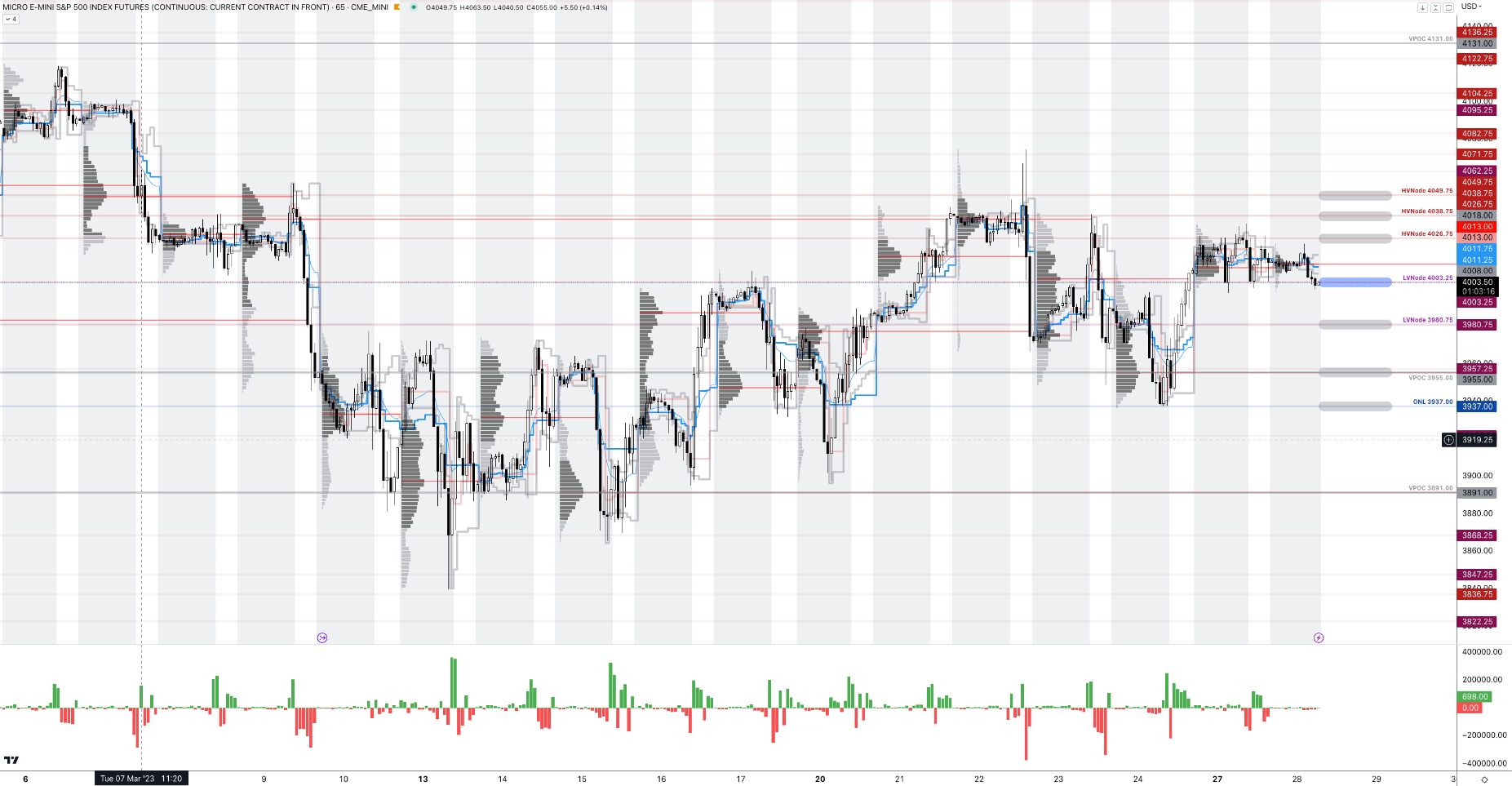

As of 7:00 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET) in the S&P 500 will likely open in the lower part of a balanced overnight inventory, inside the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $4,003.25.

Key levels to the upside include $4,026.75, $4,038.75, and $4,049.75.

Key levels to the downside include $3,980.75, $3,955.00, and $3,937.00.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold, barring an exogenous development.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for some time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

POCs: Areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future value tests as they offer favorable entry and exit.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for some time, this will be identified by a low-volume area (LVNodes). The LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to the nearest HVNodes for more favorable entry or exit.

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

Separately, Capelj is an accredited journalist with past works including interviews with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, North Dakota Governor Doug Burgum, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Connect

Direct queries to renato@physikinvest.com. Find Physik Invest on Twitter, LinkedIn, Facebook, and Instagram. Find Capelj on Twitter, LinkedIn, and Instagram. Only follow the verified profiles.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes. Capelj and Physik Invest manage their own capital and will not solicit others for it.