What Happened

Overnight, equity index futures diverged as the S&P 500 attempted a breakout, failed, and rotated back into range, leaving some signs of excess (i.e., a proper end to auction) on the composite volume profile. Learn about the profile.

This comes ahead of a weighty options expiration that ought to resolve this market of the dynamics that promoted sideways trade over the past couple of weeks. Attention, after today, shifts to weakening breadth, seasonality, emerging fundamental nuances, and the like, as a result.

Ahead is some Fed-speak and no major economic releases.

What To Expect

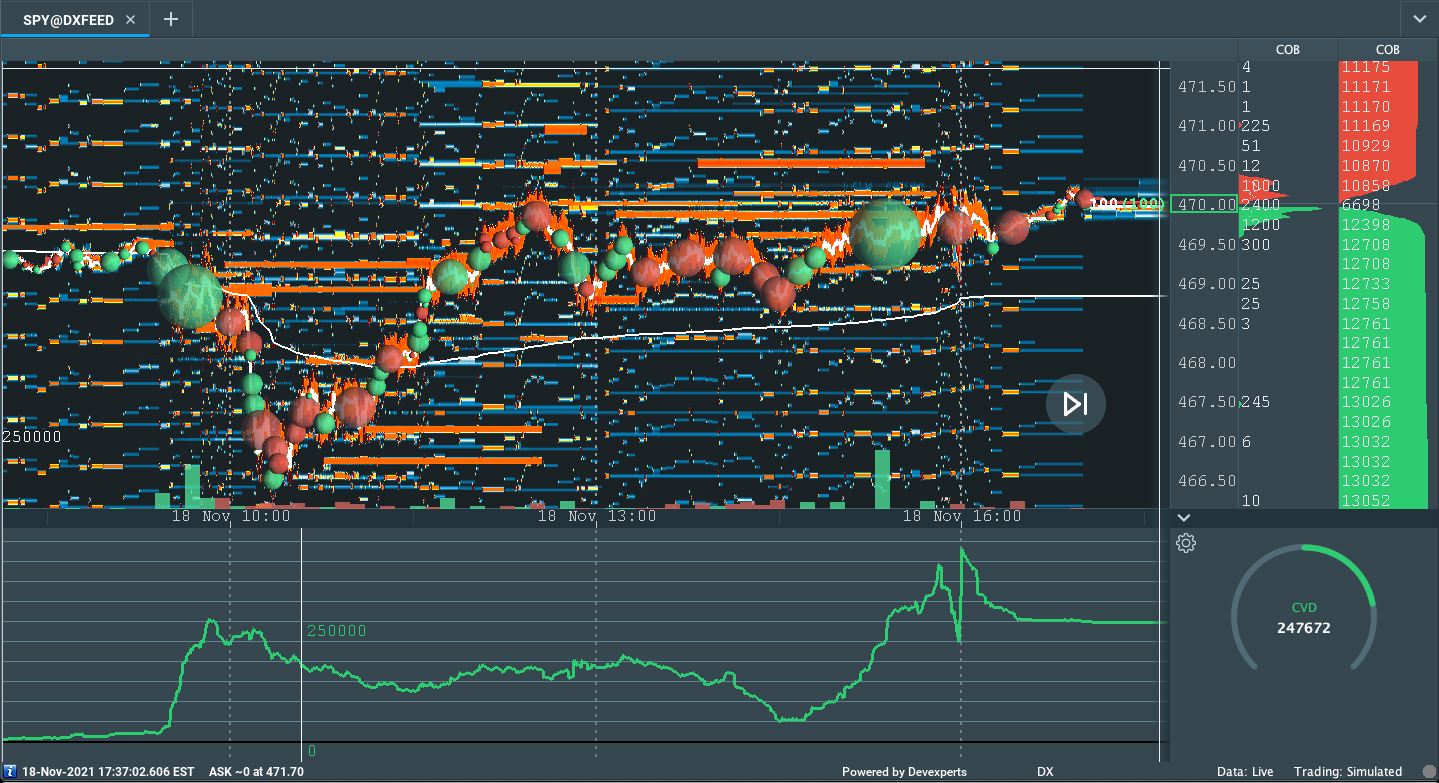

Yesterday, on nonparticipatory intraday breadth and market liquidity metrics, the best case outcome occurred; the S&P 500, after liquidating against a divergent volume delta (i.e., a metric that may reveal participants’ commitment to buying and selling as calculated by the difference in volume traded at the bid and offer) was responsively bought at its lows.

The low-of-day coincided with the $4,674.25 micro-composite point of control, the place at which two-sided trade was most prevalent over numerous day sessions, and the volume-weighted average price (i.e., the place at which liquidity algorithms are benchmarked and programmed to buy and sell) anchored from the Federal Open Market Committee (FOMC) event, weeks ago.

The aforementioned activity left behind a double-distribution profile structure; participants initiated from one area of acceptance to another, closing just beyond what analysis provider SpotGamma sees is the options strike with the highest Absolute Gamma.

As discussed day after day, leading up to today’s monthly options expiration (OPEX), this cluster of options positioning was to restrain (i.e., make it difficult for) directional resolve.

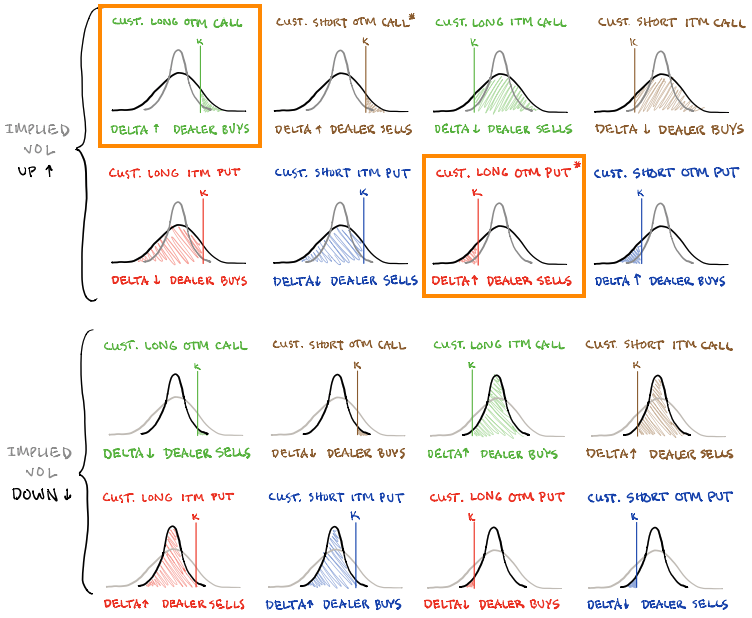

The reason is, as OPEX nears and participants concentrate their activity on shorter-dated expiries (such as the one rolling off today), there’s an increased share who are willing to bet the market won’t move higher. In expressing this bet, participants opt to sell-to-open call exposure, for instance, leaving the counterparty/dealer warehousing exposure to positive options gamma.

As this trend continues (and time to expiry narrows), dealers’ exposure to positive options gamma rises. In offsetting this risk, they sell to open (buy-to-open) the underlying as price rises (declines). This responsive buying and selling are what causes the market to balance (i.e., trade sideways) in a tight range. It ought to end after OPEX, as that options exposure rolls off.

Context: The aforementioned trade is happening in the context of dynamics I touched on in weeks prior, as well as yesterday’s commentary.

This is, specifically, the bond market’s pricing of risk.

According to Bloomberg, based on an “erratic … handling [of] large transfers of risk,” as evidenced by the Merrill Lynch Option Volatility Estimate (INDEX: MOVE), the bond market’s pricing of risk, so to speak, has diverged from the pricing of equity market risk, via the CBOE Volatility Index (INDEX: VIX).

That said, fear in one market tends to feed into the fear of another; regardless of the cause, equity and bond market participants are not on the same page.

What is the fear all about? Well, at its core, the fear coincides with “broad uncertainty about the direction of the economy and monetary policy amid surging prices, labor shortages and yields that are holding well below the rate of inflation,” according to Bloomberg.

As asked, yesterday, in combating high inflation, policymakers ought to raise rates, right?

That’s precisely what economists at institutions like JPMorgan Chase & Co (NYSE: JPM) believe may happen as soon as next September, earlier than once forecasted.

Rising rates, among other factors, have the potential to decrease the present value of future earnings, thereby making stocks, especially those that are high growth, less attractive to own.

As the market is a forward-looking mechanism, the implications of this seem staggering.

Prevailing monetary frameworks and max liquidity promoted a large divergence in price from fundamentals. The growth of passive investing – the effect of increased moneyness among nonmonetary assets – and derivatives trading imply a lot of left-tail risks.

As Kai Volatility’s Cem Karsan once told me: “There’s this constant structural positioning that naturally drives markets higher as long as volatility is compressed,” or there is supply.

“At the end of the day, though, the higher you go, the further off the ground you are and the more tail risk.”

Eventually, fear on the part of bond market participants may feed into equity market positioning.

In rounding out this section, I, again, want to mention the pinning in the broad market, as well as the performance of underlying constituents. If you’ve paid much of any attention, there is some bloodshed going on; breadth is divergent and the indices are sideways to higher, basically.

The concern is that after OPEX, the absence of supportive vanna and charm flows (defined below), for which we can attribute some of the trends in extended day outperformance, alongside that sticky gamma hedging, so to speak, frees the market for directional resolve.

Whether or not that resolve is up or down, we know that (as SpotGamma talks more about), participants are underexposed to downside protection. Should volatility pick up, these participants are likely to reach for that protection forcing dealers to reflexively hedge in a destabilizing manner.

As volatility rises and customers demand out-of-the-money put protection, counterparties are to hedge by selling into weakness. The conditions worsen when much of the activity is in shorter-dated tenors where options gamma is more punchy if we will.

Expectations: As of 6:15 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Balance-Break Failure: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) nearly occurred on a higher time frame. In monitoring for acceptance (i.e., more than 1-hour of trade) outside of the balance area, we saw an overnight rejection (i.e., return inside of balance). This portends a move to the opposite end of the balance. Given OPEX, though, we ought to give more weight to continued balance (i.e., sideways trade).

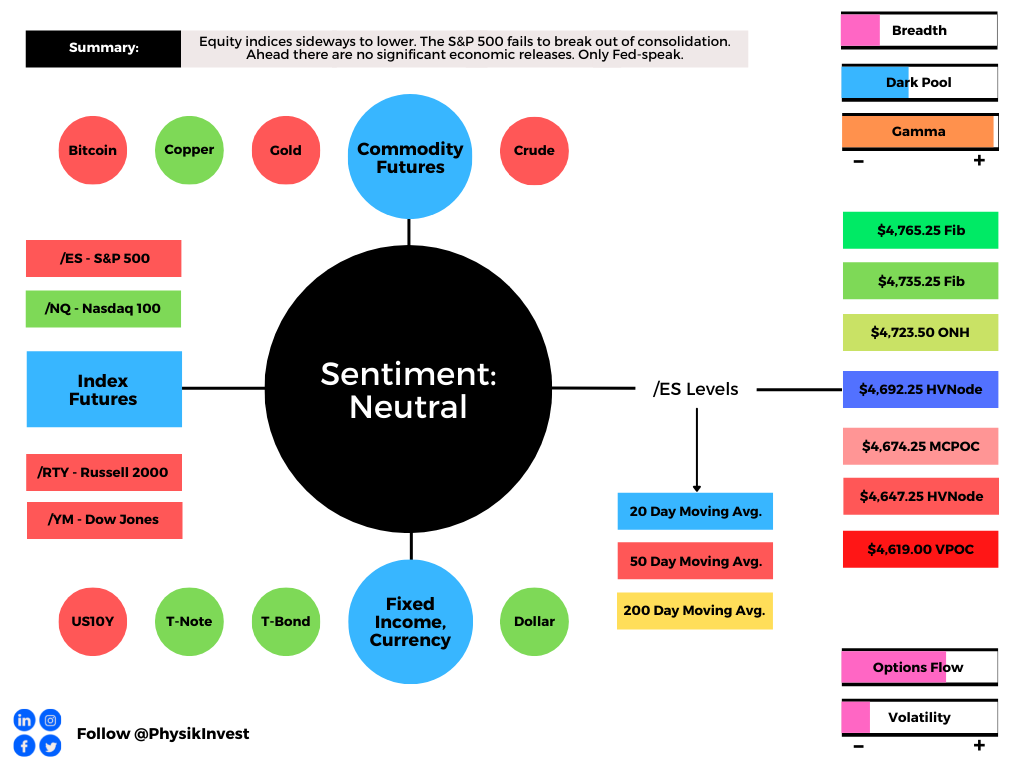

In the best case, the S&P 500 trades sideways or higher; activity above the $4,692.25 high volume area (HVNode) puts in play the $4,723.50 overnight high (ONH). Initiative trade beyond the ONH could reach as high as the $4,735.25 and $4,765.25 Fibonacci, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,692.25 HVNode puts in play the $4,674.25 micro composite point of control (MCPOC). Initiative trade beyond the MCPOC could reach as low as the $4,647.25 HVNode and $4,619.00 VPOC, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Vanna: The rate at which the delta of an option changes with respect to volatility.

Charm: The rate at which the delta of an option changes with respect to time.

Options: If an option buyer was short (long) stock, he or she would buy a call (put) to hedge upside (downside) exposure. Option buyers can also use options as an efficient way to gain directional exposure.

VPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure.

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.