Abstract

Equity index futures and commodities were mixed. Bonds sideways to higher. Volatility bid.

Ahead is a heavy day of economic releases, in the face of fundamental narratives and positioning metrics that may later support directional resolve.

What Happened

Overnight, equity index futures were flat as participants wait to initiate the next leg – higher or lower – until they are provided clarity on monetary policy frameworks, the pace of the economic recovery, and the like.

Ahead is ADP employment (8:15 AM ET), Markit services PMI (9:45 AM ET), ISM services index and factory orders (10:00 AM ET), as well as Federal Reserve statements (2:00 PM ET).

What To Expect

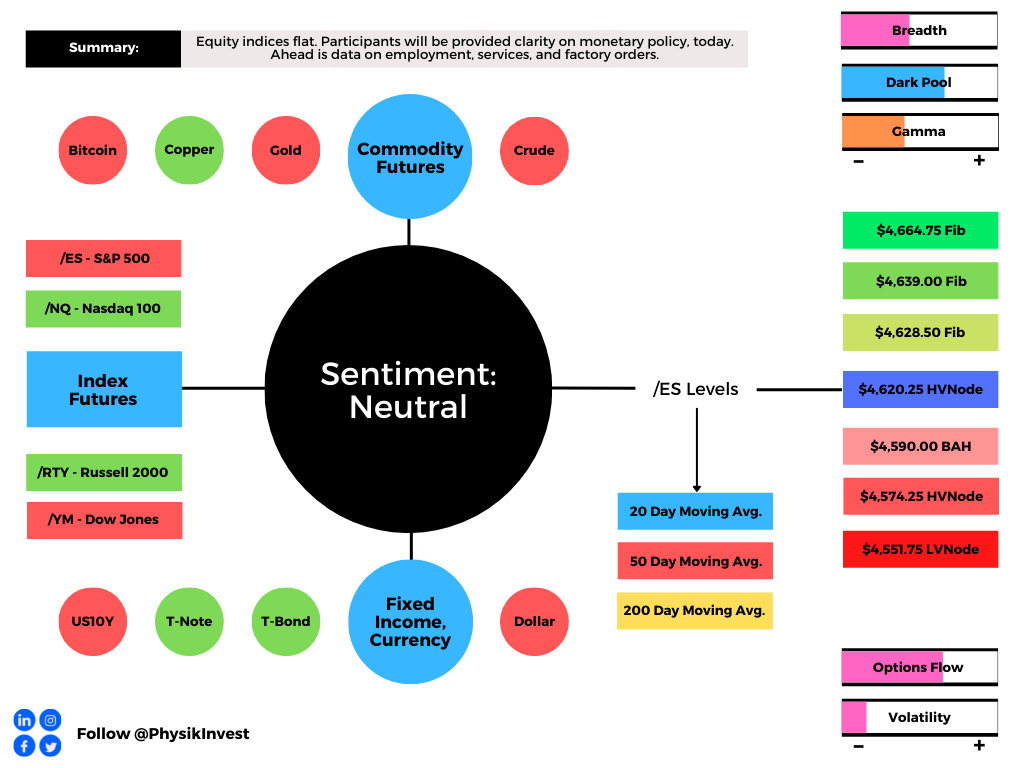

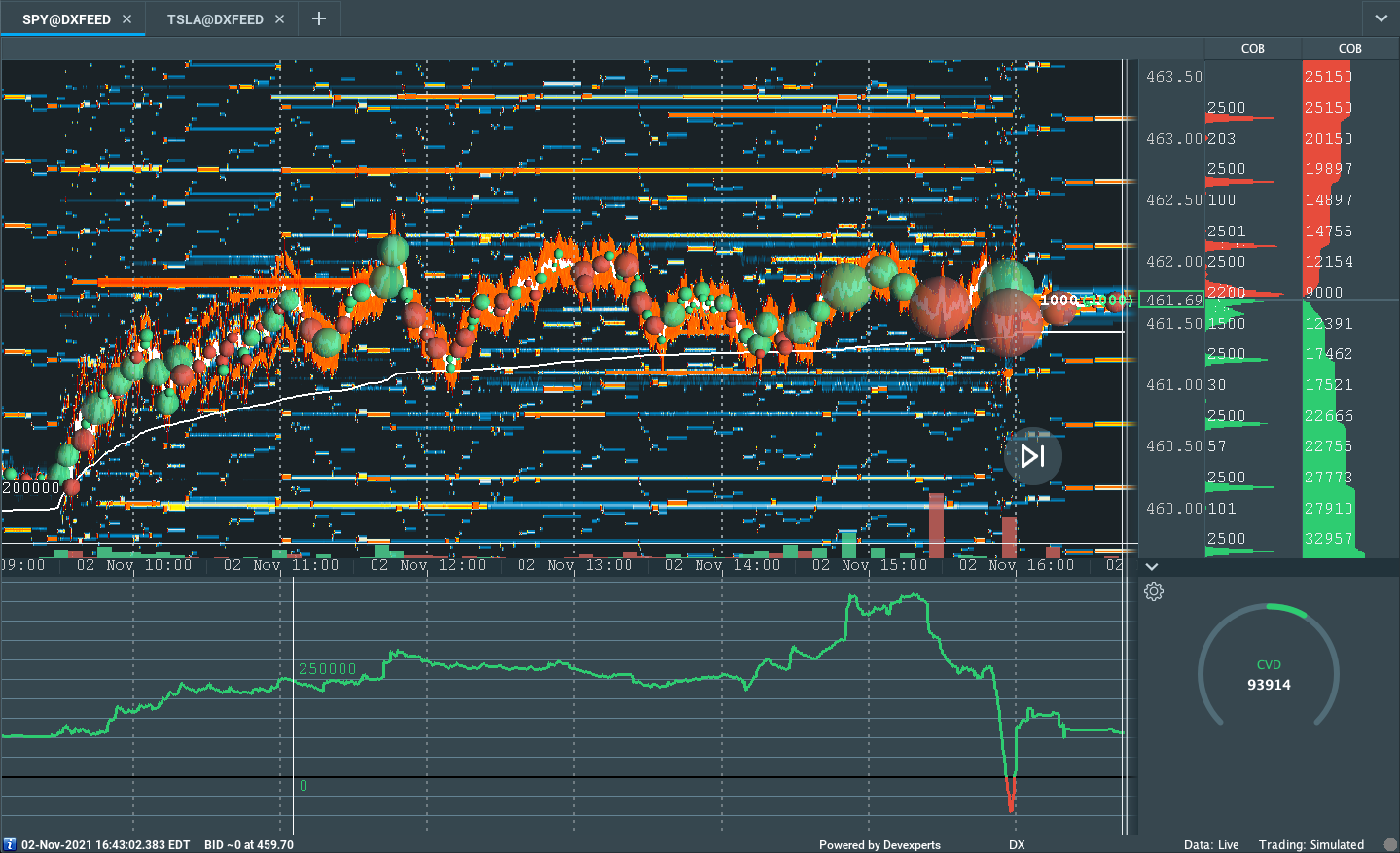

Action: On lackluster breadth and market liquidity metrics, the best case outcome occurred, evidenced by participants’ exploration of new prices in the S&P 500.

Intent: The intraday excess high marks potential exhaustion (or willingness to end trend). Also, the rounding of the composite profile (i.e., developing ledge) suggests participants are either painting themselves into a corner or there is a lack of conviction to take price higher.

Validation: Sideways trade, above the $4,590.00 balance area high (BAH), and overlapping value areas, validates the market’s intent to pause ahead of new information.

Consideration: Poor structure left behind prior initiative trade (as evidenced by the presence of numerous gaps and p-shaped emotional, multiple-distribution profile structures which denote short-covering and a lack of material, new-money buying) adds to technical instability.

Should the market crack, participants will likely look to check old value (i.e., revisit, repair, and strengthen) these pockets of low-volume. This is called the “cave-fill” process, in volume profile terms.

Context: Federal Open Market Committee (FOMC) announcement later today.

The announcement will provide participants with color on the economic recovery and the Federal Reserve’s intent to continue supporting the economy, at the rate it has.

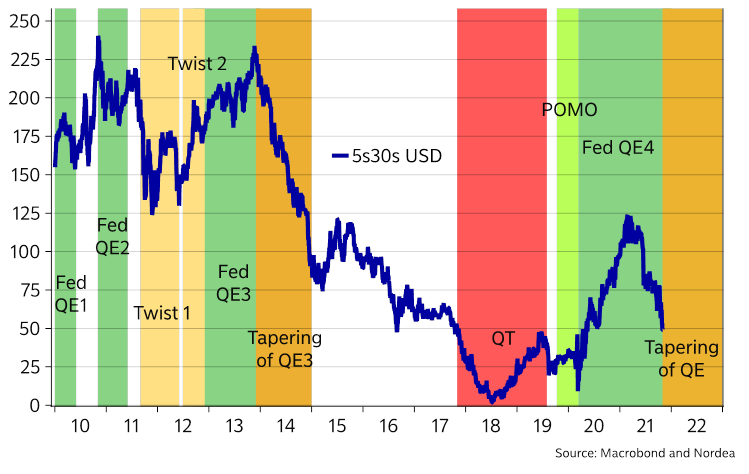

Nordea’s Andreas Steno Larsen states: “Jay Powell will have to walk on eggshells to prevent an acceleration of the front-end of the USD yield curve. Arguments for the Fed to tighten policy keep piling up and hence we see a swift tapering process (30B a meeting) and a first hike in June.”

“The combination of 1) even higher inflation prints during Q4 (with several extremely volatile base effects), 2) a removal of USD liquidity, 3) a historically weak credit impulse into 2022 (due to a massive credit expansion 20/21) sounds like the perfect flattener setup to us,” which may weigh on sentiment and long term investments.

In terms of positioning, the CBOE Volatility Index (INDEX: VIX) was a touch higher, while spreads across the VIX futures term structure widened with demand coming in at the front.

Such a situation, as touched on yesterday, in addition to the long-gamma environment (in which counterparties hedge their warehoused options risk by buying underlying into weakness and selling into strength), has the effect of making it difficult to resolve directionally.

The reasons are: (1) options will slide down their term structure (vanna) and (2) skew decays (charm). When this happens, we expect to see supportive flows as dealers cover their short equity/futures hedges.

With volatility bid, the effect of vanna and charm is dulled. As a result, it is likely that participants see more movement after the FOMC announcement.

To note, the potential for upside resolve comes down to how participants take the FOMC announcement. We know that, according to SpotGamma, there is increased capital being committed to higher and higher options strikes, a development often seen as bullish.

Expectations: As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a neutral overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Balance (Two-Timeframe Or Bracket) Is The Status Quo: Rotational trade that denotes current prices offer favorable entry and exit. Modus operandi is responsive trade (i.e., fade the edges), rather than initiative trade (i.e., play the break).

In the best case, the S&P 500 trades sideways or higher; activity above the $4,620.25 high volume area (HVNode) pivot puts in play the $4,628.50 Fibonacci extension. Initiative trade beyond $4,628.50 could reach the $4,639.00 and $4,664.75 Fibonacci levels, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,620.25 HVNode puts in play the $4,590.00 balance area high (BAH). Initiative trade beyond the BAH could reach as low as the $4,574.25 HVNode and $4,551.75 low volume area (LVNode), or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Cave-Fill Process: Widened the area deemed favorable to transact at by an increased share of participants. This is a good development.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

Ledges: Flattened area on the profile which suggests responsive participants are in control, or initiative participants lack the confidence to continue the discovery process. The ledge will either hold and force participants to liquidate (cover) their positions, or crack and offer support (resistance).

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.