Market Commentary

Out sync with bonds, equity index futures and commodities traded higher. Volatility compressed.

- Monetary uncertainty. Earnings pick up.

- Options positioning may support prices.

- Ahead: Building permits, housing starts.

What Happened: U.S. stock index futures auctioned sideways to higher overnight as participants sought to price in robust earnings against the backdrop of monetary uncertainty and increased pricing pressures.

“The world is watching interest rates more closely than it has for some time — and rightly so, the moves have been emphatic, especially in the short-term maturities,” Chris Weston, head of research at Pepperstone Financial Pty, said. He added it’s “impressive how resilient and calm markets are in the face of the rates repricing.”

Ahead is data on building permits and housing starts (8:30 AM ET).

What To Expect: As of 6:30 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM EST) in the S&P 500 will likely open outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator. Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

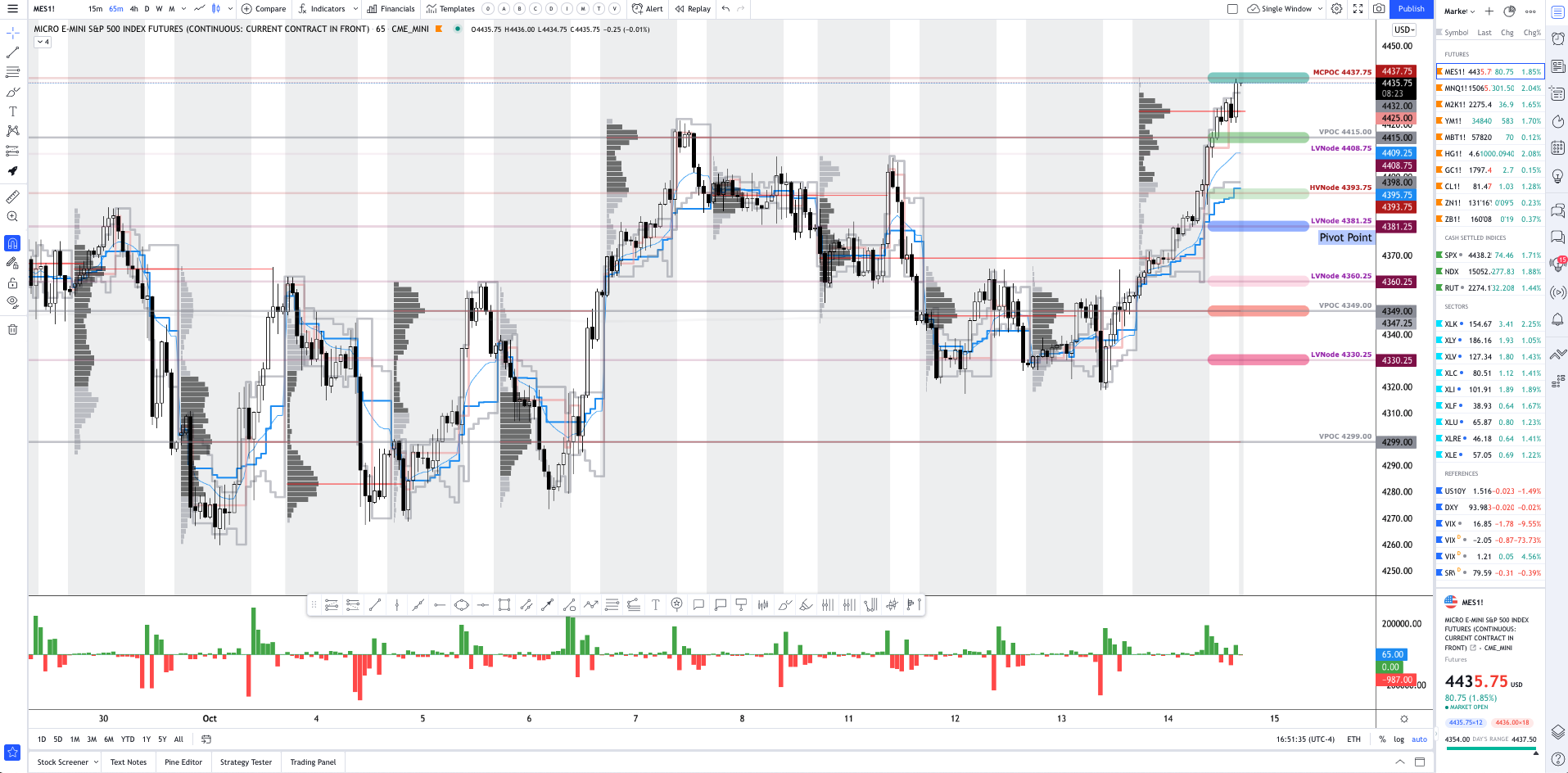

Adding, during the prior day’s regular trade, on non participatory intraday breadth and supportive market liquidity metrics, the best case outcome occurred, evidenced by a response at the $4,437.75 micro composite point of control (MCPOC), which carried into initiative buying, past the $4,469.75 overnight high (ONH).

Coupled with that dynamic is the sustained presence of numerous gaps and p-shaped emotional, multiple-distribution profile structures (i.e., old-money shorts covering); as a result, participants will likely look to revisit, repair, and strengthen – build out areas of high volume (HVNodes) via the cave-fill process – these areas of low volume (LVNodes).

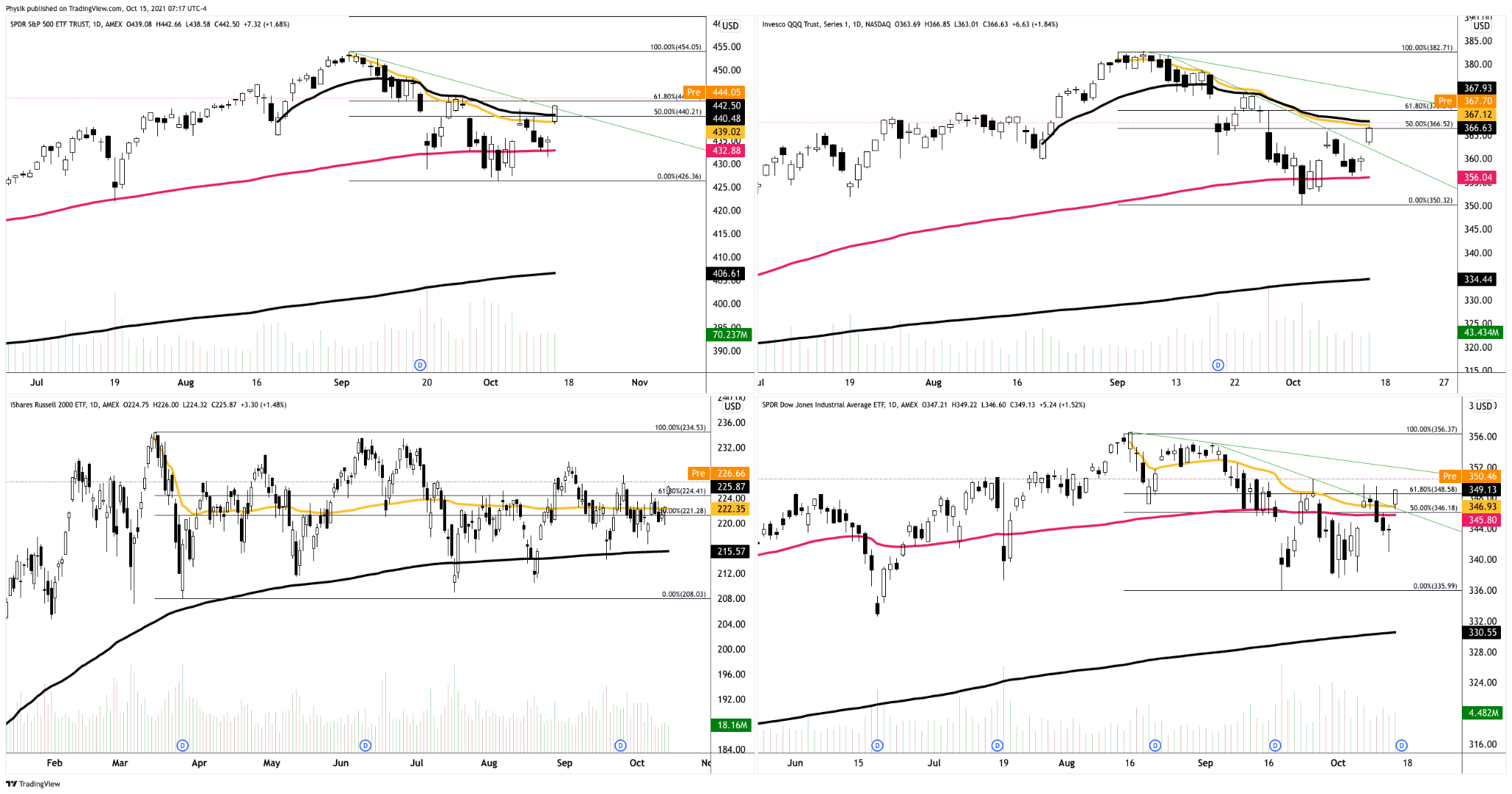

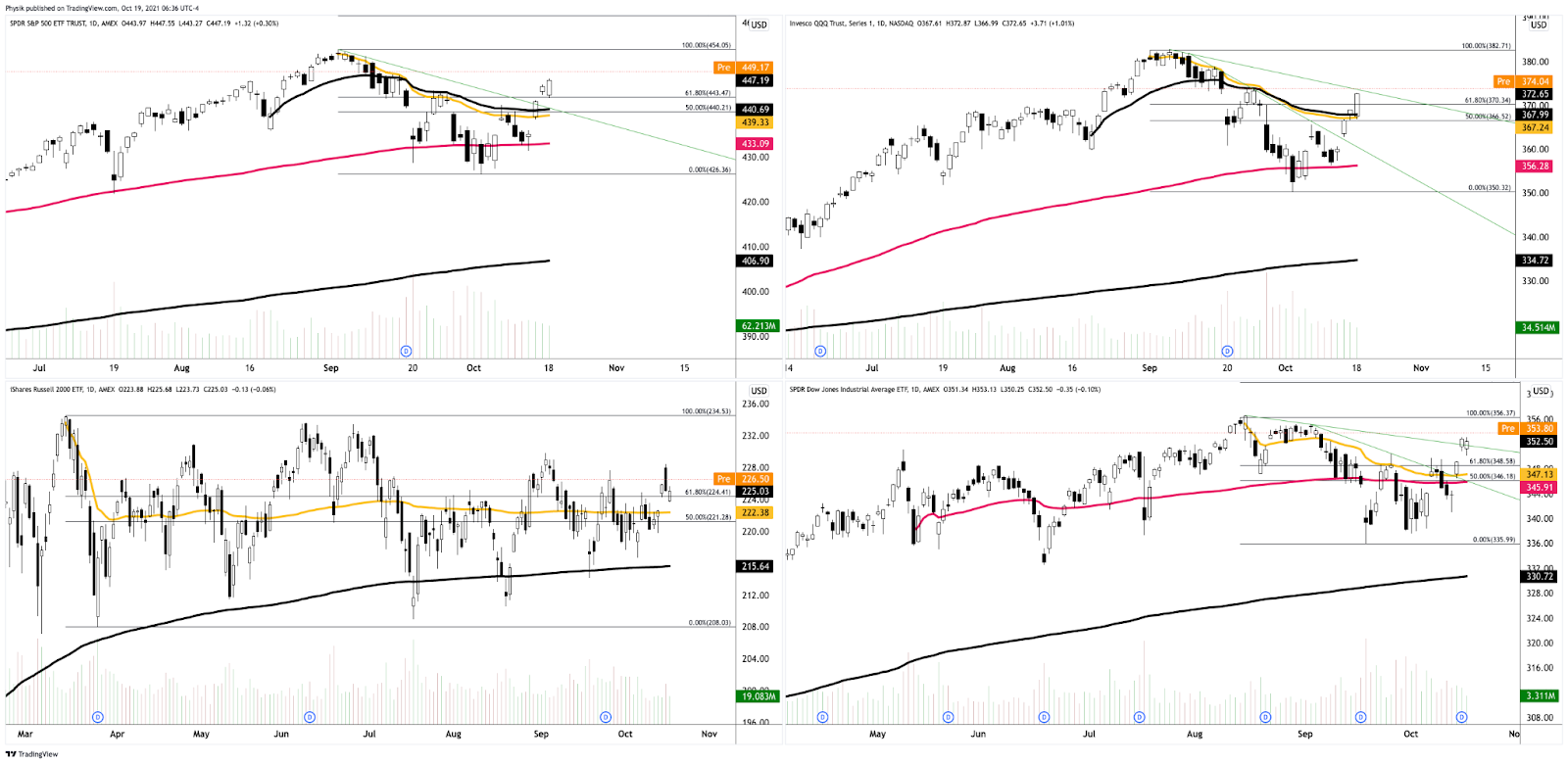

Zooming out, we see the Nasdaq 100 trading relatively strong.

Given where the S&P 500’s price is in relation to the yellow anchored volume-weighted average price (VWAP), below, the average buyer, since the all-time high, holds a winning position; sideways-to-higher trade, above the upward sloping trendline, as well as the 50.00% and 61.8% retracements, likely puts in play a recovery of the all-time high.

Further, the aforementioned trade is happening in the context of improving breadth amidst a seasonally bullish cycle of contributions, rebalancing, and earnings, as well as the risks associated with a taper in asset purchases and a hike in rates.

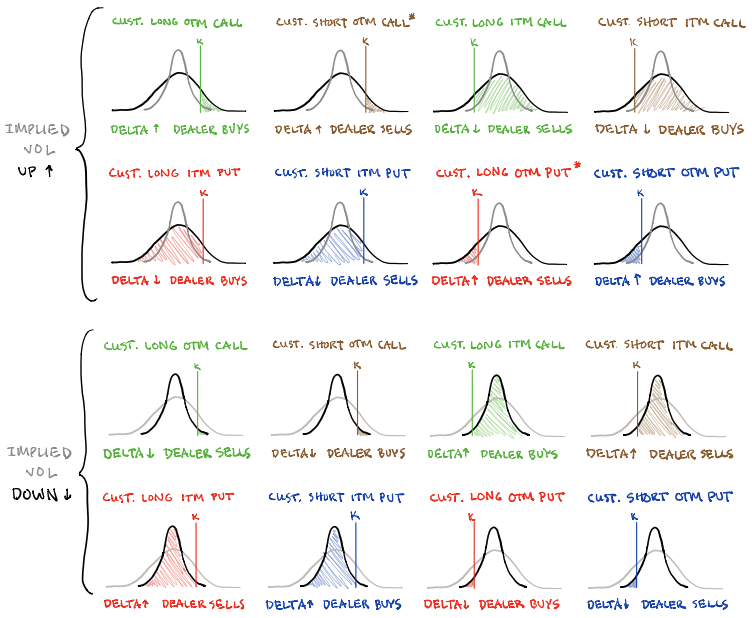

In terms of positioning, the CBOE Volatility Index (INDEX: VIX) was lower, while the VIX futures term structure remained in contango; supply at the front end of the curve, alongside the long-gamma environment, signals a potential for near-term equity market stability.

According to SpotGamma analyses, participants were likely selling puts into yesterday’s price rise; this dynamic may support sideways to higher trade.

In a barebones overview of some of the dynamics at play, here, if implied volatility were to rise, the counterparty to the aforementioned trade would purchase stock (long delta) to hedge their rising long put (short delta) exposure. If implied volatility were to decline, the counterparty would likely sell stock (short delta) as their long put (short delta) exposure declines.

Moreover, for today, participants may make use of the following frameworks.

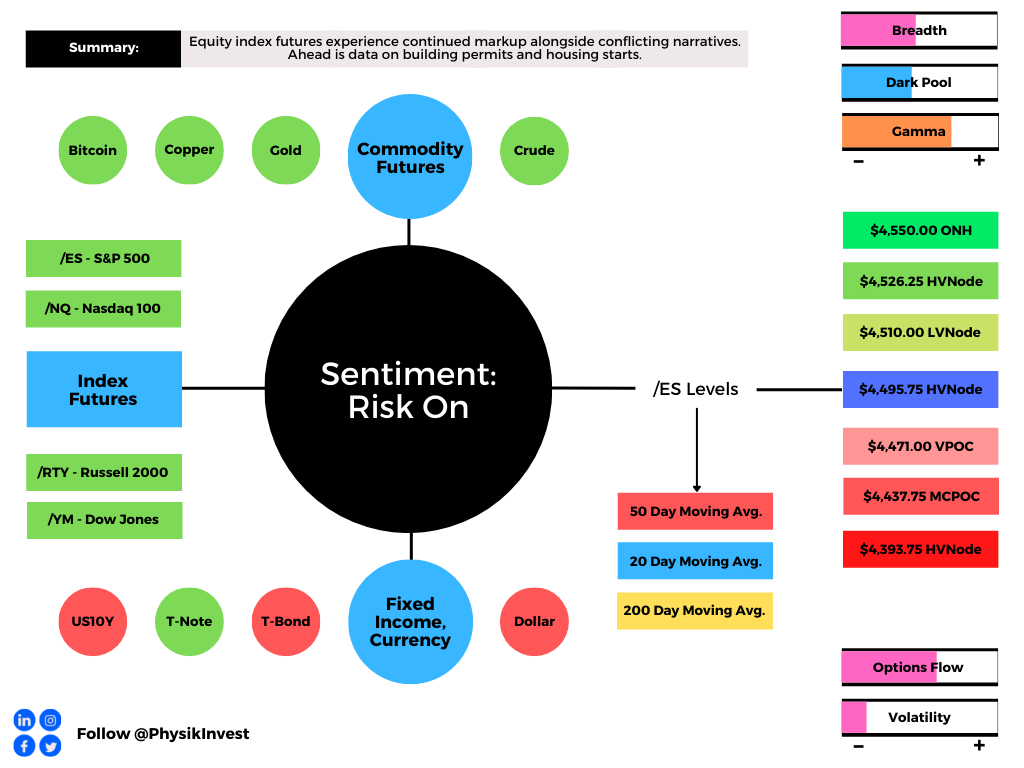

In the best case, the S&P 500 trades sideways or higher; activity above the $4,495.75 high volume area (HVNode) puts in play the $4,510.00 low volume area (LVNode). Initiative trade beyond the LVNode could reach as high as the $4,526.25 HVNode and $4,550.00 overnight high (ONH), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,495.75 HVNode puts in play the $4,471.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as low as the $4,437.75 micro composite point of control (MCPOC) and $4,393.75 HVNode, or lower.

Click here to load today’s updated real-time key levels into the web-based TradingView charting platform. Please note that all levels are derived using the 65-minute timeframe.

Definitions

Cave-Fill Process: Widened the area deemed favorable to transact at by an increased share of participants. This is a good development.

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Short Covering: The profile shape suggests participants were “too” short and had poor location.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Initiative Buying (Selling): Buying (selling) within or above (below) the previous day’s value area.

Responsive Buying (Selling): Buying (selling) in response to prices below (above) an area of recent price acceptance.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

News And Analysis

Nordea: Is permanent inflation now an alarming consensus?

Evergrande unit has remit funds to pay yuan bond coupon.

China’s central bank should cut RRR, one adviser suggests.

World facing fiscal problems much worse than from COVID.

Investing prosperously in light of China’s common prosperity.

Bitcoin pushes toward record before debut of ETF products.

What People Are Saying

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.