Editor’s Note: Market commentaries to pause until Monday, October 4, 2021, due to travel commitments. As a result, I go in-depth today and offer a strong trade idea for the week ahead.

Also, if you’re in a rush, focus on the bolded text!

Market Commentary

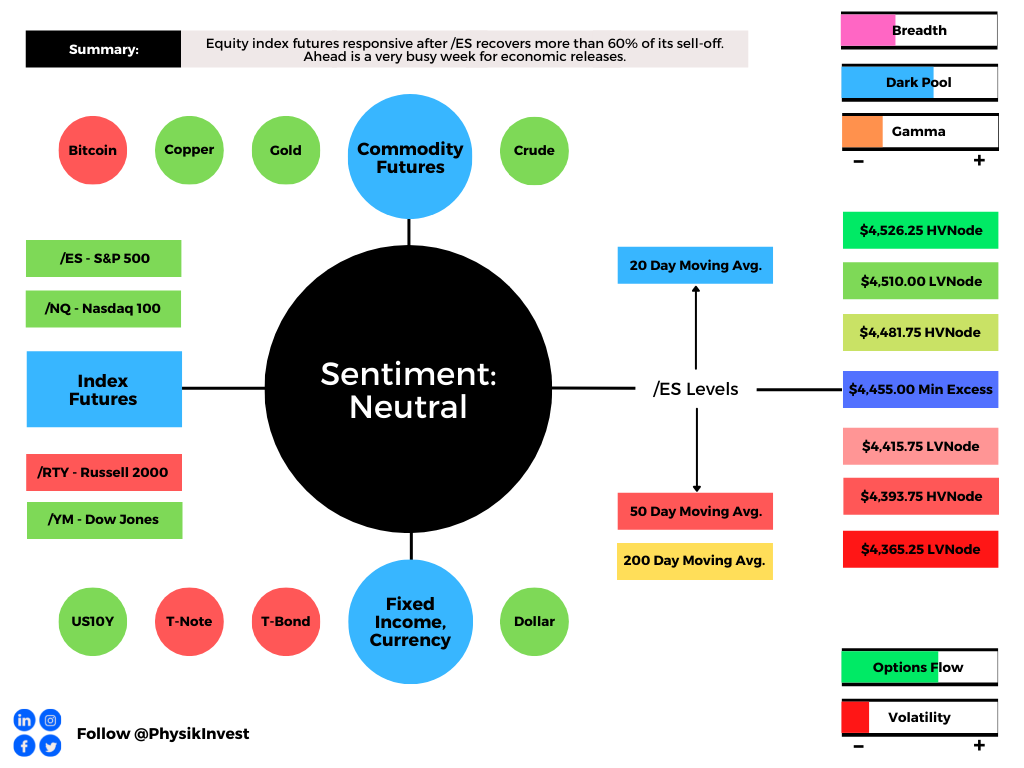

Equity index futures recover. Yields break higher. Volatility implodes.

- Indices have recovered 60% of sell-off.

- Buying-the-dip psychology is breaking.

- Watching: Taper, shutdown, debt risks.

- Fed may stamp out life in the economy.

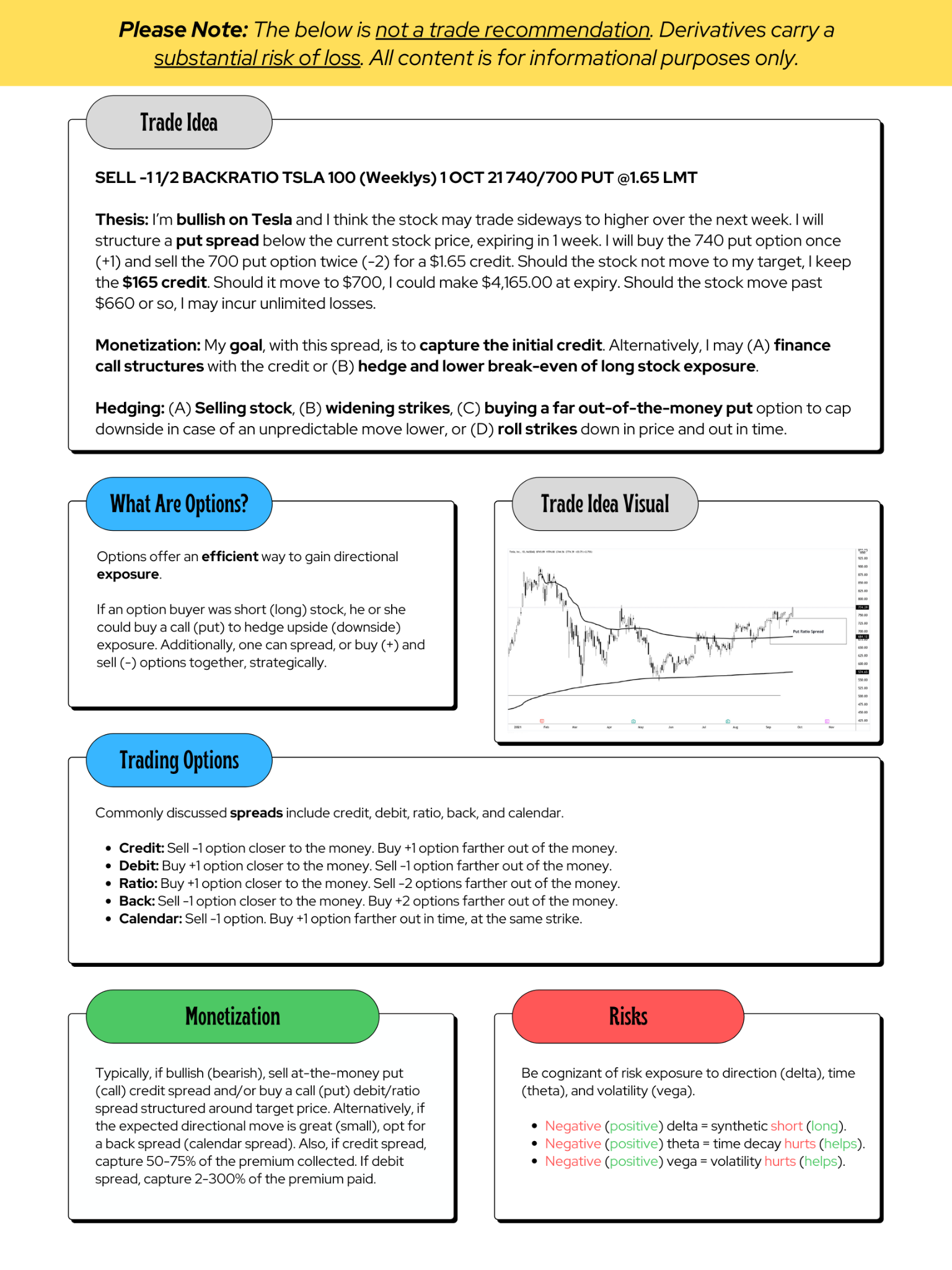

- Trade Idea: Capitalizing on TSLA skew.

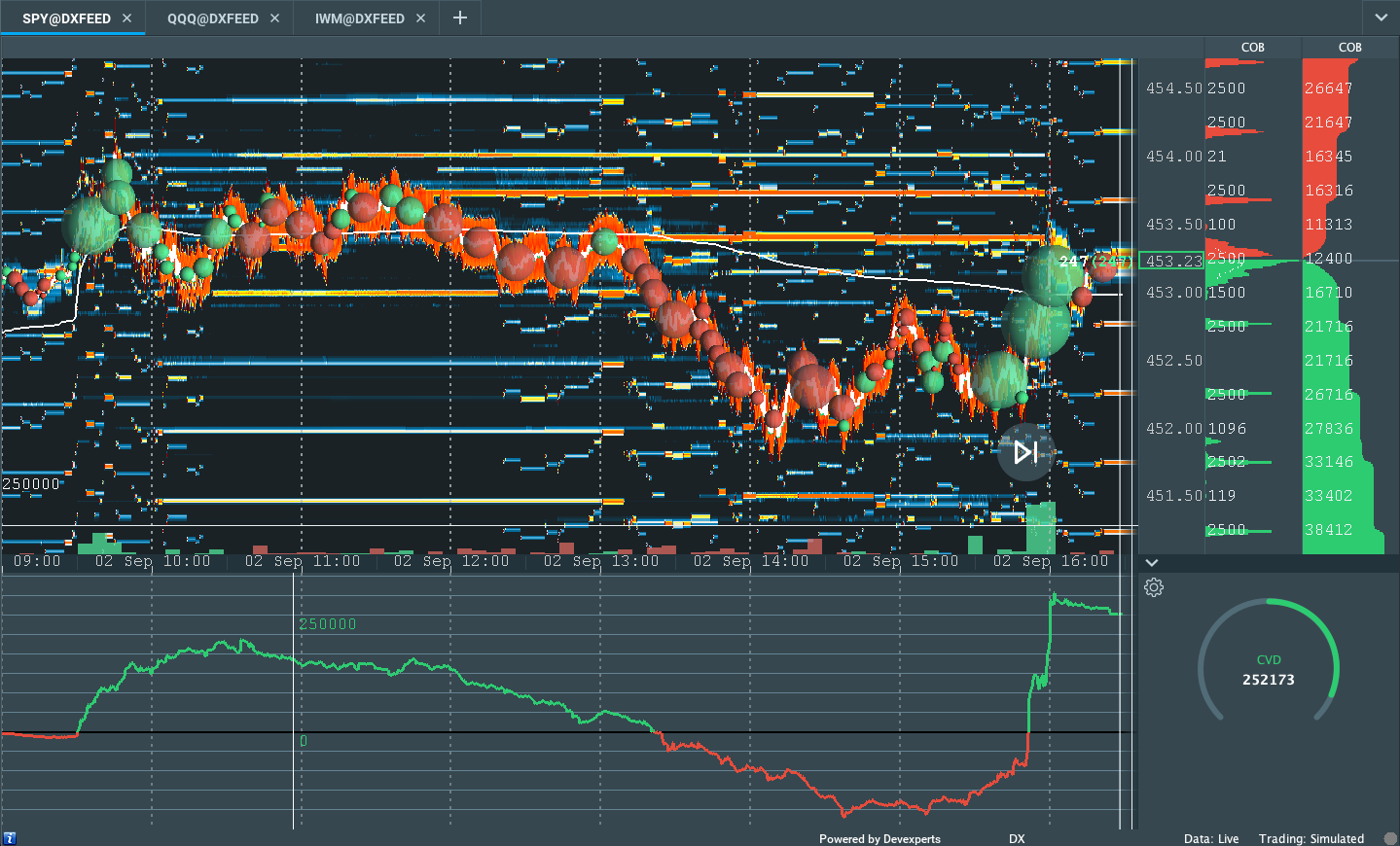

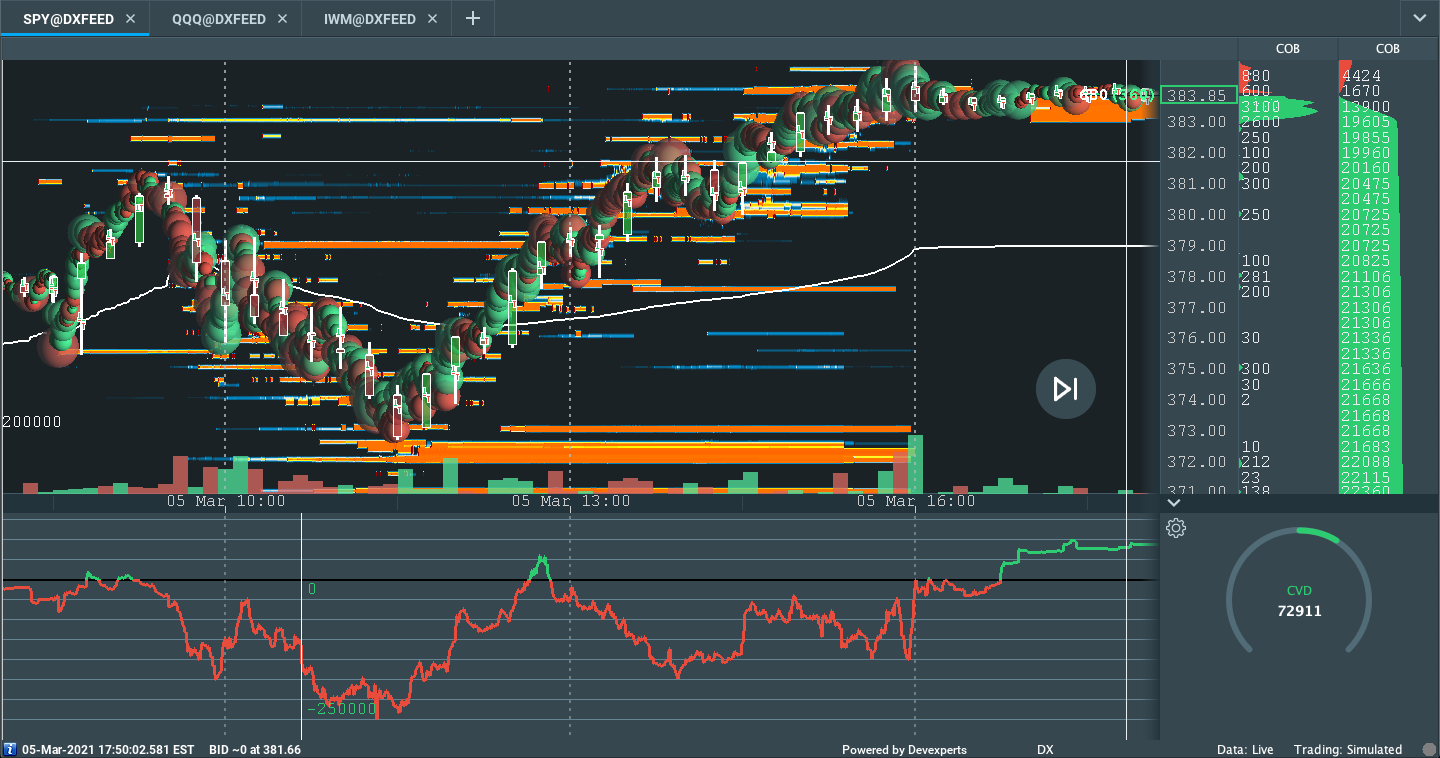

What Happened: After a series of outlier moves, U.S. stock index futures ended the week range-bound when responsive sellers – as confirmed by measures of market liquidity – stepped in at key moving averages and anchored volume-weighted average price levels.

Ahead is a busy week in terms of economic releases; important data on durable goods orders, consumer confidence, home sales, personal income and spending, PCE deflators, as well as manufacturing data are slated to come out.

What To Expect: Be patient with me, there is a lot to condense.

During the prior week’s trade, on mostly strong intraday breadth and divergent market liquidity metrics, equity index futures briefly liquidated; the S&P 500 went as low as $4,300.00.

Then, a swift recovery ensued; participants took back nearly 60% of the most recent sell-off.

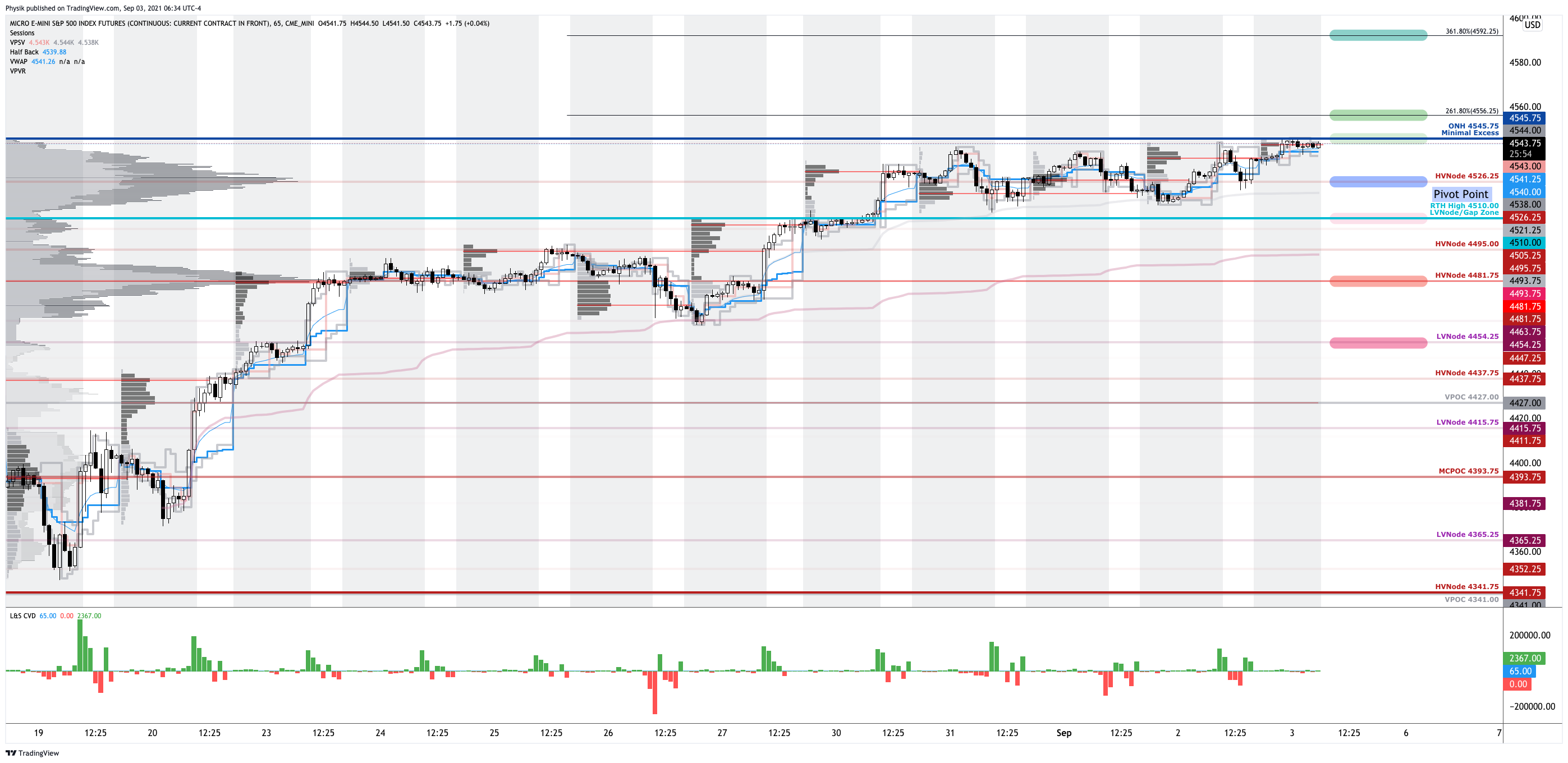

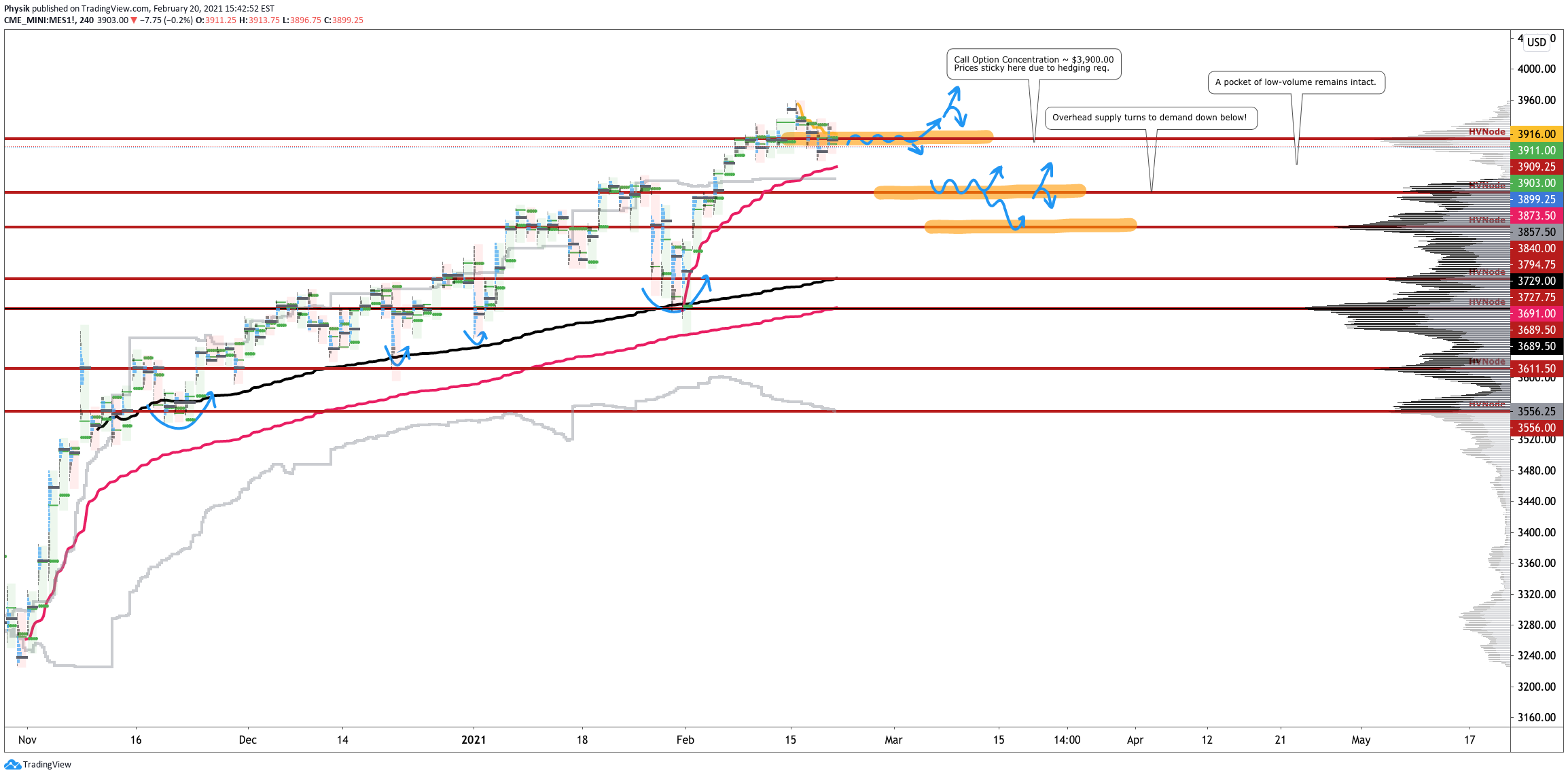

During the recovery process, the S&P 500 – as evidenced by emotional, multiple distribution profile structures – established a minimal excess rally high at $4,455.00 before the momentum from covering shorts was overpowered by responsive selling at key areas of resting liquidity, at and around $4,455.00, or so.

Friday’s session, however, resolved some of the aforementioned emotional structures through what’s called the “cave-fill” process; revisiting, repairing, and strengthening – building out areas of high volume (HVNodes), or value – areas low volume (LVNodes).

To put it simply, the cave-fill process widened the area deemed favorable to transact at by an increased share of participants. This is a good development.

Further, the aforementioned trade is happening in the context of narratives surrounding a taper to Federal Reserve asset purchases, a government shutdown, and the debt ceiling.

The implications of these themes on price are contradictory; to elaborate, in the most recent meeting of the Federal Open Market Committee (FOMC), it was announced that the economy made substantial progress toward the central bank’s goals and, if progress continued as expected, a moderation in the pace of asset purchases was likely.

“Powell said that the tapering process could be wrapped up by mid-2022, which would require either an earlier start or larger reductions,” Moody’s said.

“In other words, as long as September employment isn’t a disaster, the Fed will begin tapering at its November meeting. Therefore, it would skip a formal announcement and a one-meeting delay to dive right into the tapering process. It seems we’re headed for an eight-month taper, or [a] $15 billion reduction per month.”

The Fed’s dot plot saw movement, too; there are increased odds of a rate hike in 2022.

In regards to the debt ceiling, which caused a kink in the Treasury bill curve and may portend financial market volatility if not resolved, Powell voiced concern, noting that it must be raised.

This is a likely development given that “lawmakers know that voting against raising the debt ceiling would have enormous economic costs,” Moody’s noted.

Adding, after the September 17 options expiry which cut S&P 500 dealer gamma in half and opened the window to volatility, alongside threats posed by China’s Evergrande complications, the tone changed markedly, given a fraying in the buy-the-dip psychology.

While strategists at JPMorgan Chase & Co (NYSE: JPM) suggest the selling was knee-jerk and technical, the truth is that, according to Reuters, “global stock funds lost the most since March 2020 as investors moved in [favor] of cash where they [plowed] in $39.6 billion of funds.”

Still, in the face of comments by the Fed, as well as the Evergrande and debt ceiling debacle, the liquidation resolved some fragility with respect to positioning and stocks rallied, affirming the beliefs held by Goldman Sachs Group Inc’s (NYSE: GS) Peter Oppenheimer and HSBC Holdings Plc (NYSE: HSBC) strategists that dip-buying is a go as “we’re still in the relatively early stages of this economic cycle.”

To put it differently, per one Bloomberg article, “the lasting impression … is that for markets the tapir no longer has the power to induce fear in the way that it did eight years ago, … [and] [t]he post-Evergrande bounce has some life in it. It’s no dead cat.” A 4,700 or 5,000 S&P 500, as some strategists see it, could be in the cards.

Moreover, for next week, participants may make use of the following frameworks.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,455.00 minimal excess high puts in play the $4,481.75 HVNode. Initiative trade beyond the HVNode could reach as high as the $4,510.00 LVNode and $4,526.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,455.00 minimal excess high puts in play the $4,415.75 LVNode. Initiative trade beyond the LVNode could reach as low as the $4,393.75 HVNode and $4,365.25 LVNode, or lower.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test. If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit. Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility. Options Expiration (OPEX): Option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure. Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices. More On Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs. Rates: Low rates have to potential to increase the present value of future earnings making stocks, especially those that are high growth, more attractive. To note, inflation and rates move inversely to each other. Low rates stimulate demand for loans (i.e., borrowing money is more attractive). In conjunction with the rapid recovery, lower rates solicit hawkish commentary as policymakers look to inhibit inflation.

Weekly Trade Idea

News And Analysis

Weakening U.S. economy threatens swelling corporate debt mountain.

Ongoing debt limit fight is as much about 2022 politics as fiscal policy.

Alhambra Investments: Next steps to watch for a scarcity of collateral.

From New York To Sydney: See the supply shocks spanning the globe.

Economic Outlooks U.S. Q4 2021: The rocket is beginning to level off.

Nancy Pelosi: The infrastructure plan will likely pass House this week.

Treasuries at risk as Federal Reserve paves way for breakout in yields.

The SEC’s Gary Gensler doesn’t see cryptocurrencies lasting that long.

Bear market is unlikely, but stumble in stocks may lead to a bigger fall.

What People Are Saying

Let’s Hang Out

Salt Lake City, UT September 28-30

Las Vegas, NV October 1-3

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.