Notice: To view this week’s big picture outlook, click here.

Key Takeaways For Today:

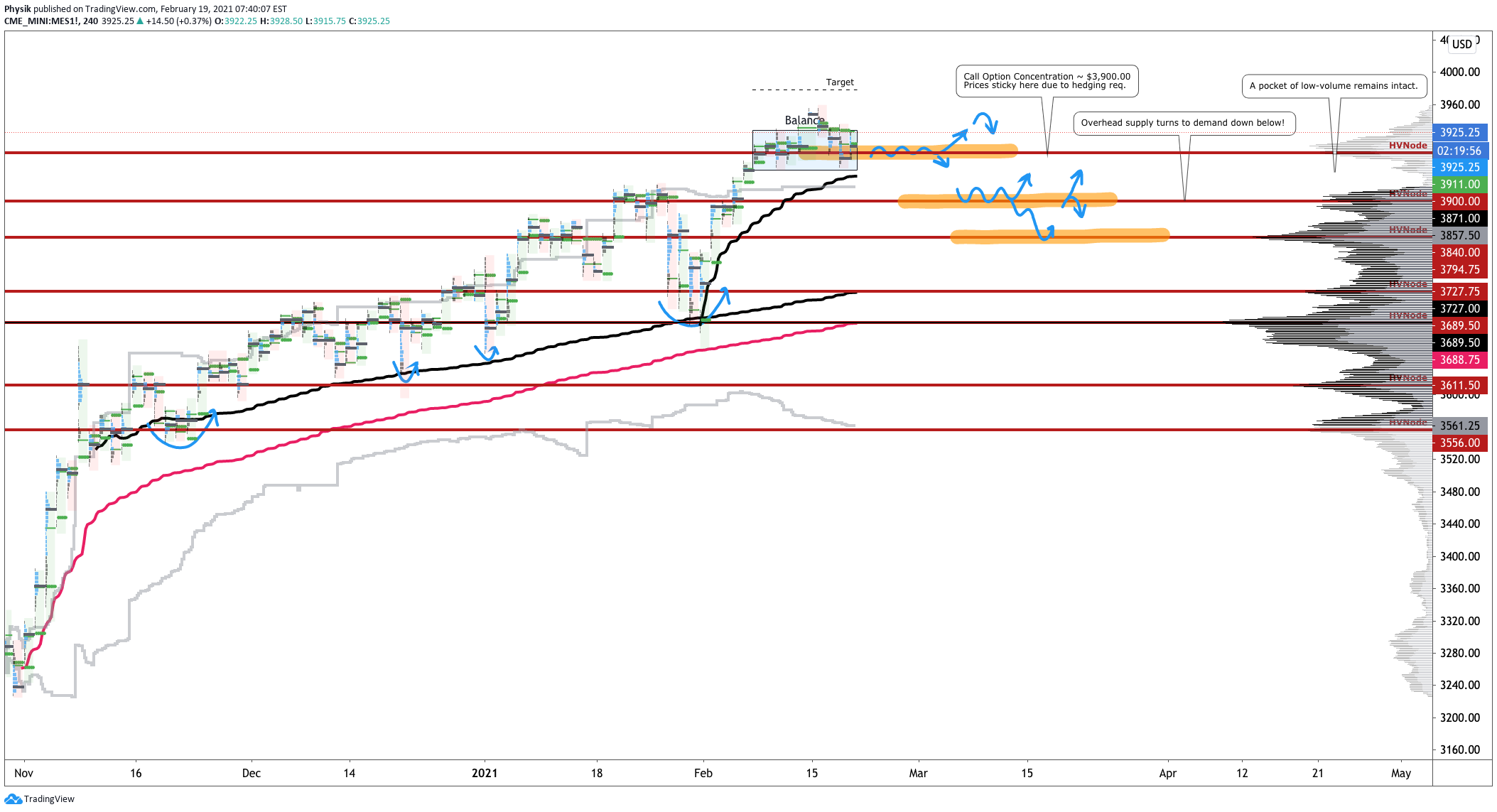

$3,900.00 S&P 500 is sticky, so expect balance.

The longer-term bias remains up until it is not.

Hedge bets when you can, not when you have to.

What Happened: Overnight, U.S. stock index futures auctioned higher, ahead of economic releases on U.S. business activity.

What Does It Mean: The past few weeks have been volatile.

Market participants witnessed a rapid de-risking event, as a result of individual stock volatility, and a subsequent v-pattern recovery, that was later taken back as the February monthly options expiration (OPEX) neared.

Given OPEX, participants have a clue as to why the market has failed to resolve directionally: option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure.

Aside from OPEX, we must talk more on the aforementioned v-pattern recovery and last week’s spike exit from balance, as well as weakening broad market volatility.

More On The V-Pattern: A pattern that forms after a market establishes a high, retests some support, and then breaks above said high. In most cases, this pattern portends continuation.More On Spikes: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

In light of the v-pattern, balance, and spike, the S&P 500’s long-term uptrend remains intact. In support of this uptrend, systematic and hedge fund participants are increasing their long-exposure, given the economic recovery, and a drop in volatility.

Beyond that, speculative activity in the options market and measures of market liquidity fail in offering much information.

SPY Market Liquidity

QQQ Market Liquidity

IWM Market Liquidity

What To Expect: Friday’s regular session (9:30 AM – 4:00 PM ET) will likely open outside of prior-balance and -range, suggesting the potential for immediate directional opportunity.

This comes alongside the acceptance of higher prices (above a prominent high-volume area), and an overnight rally-high at $3,959.25.

More On Overnight Rally Highs: Typically, there is a low historical probability associated with overnight rally-highs ending the upside discovery process.More On Volume Areas: A structurally sound market will build on past areas of high-volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low-volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low-volume, then future discovery ought to be volatile and quick as participants look to areas of high-volume for favorable entry or exit.

Given the above dynamics, the following frameworks ought to be applied.

In the best case, as stated yesterday, the S&P 500 opens and remains above the $3,900.00 confluence zone. Auctioning beneath $3,900.00 turns the high-volume area (HVNode) nearby into supply, offering initiative sellers favorable entry and responsive buyers favorable exit.

Pictured: Profile overlays on a 65-minute candlestick chart of the Micro E-mini S&P 500 Futures.

Notice: To view this week’s big picture outlook, click here.

What Happened: U.S. stock index futures balanced within prior range, ahead of releases on weekly jobless claims.

What Does It Mean: After a v-pattern recovery and sideways trade in the weeks prior, stock index futures auctioned out of prior-balance and -range, via Friday’s end-of-day spike.

More On Spikes: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

Since then, the S&P 500 had difficulty in maintaining higher prices.

At the end of regular trade Wednesday, the aforementioned spike and shift from balance (i.e., the transition from two- to one-time frame trade) was accepted. Overnight, however, the market rotated back into the meat of Wednesday’s range, putting in jeopardy the near-term bullish bias. This is likely the resolve of uninspired buying interest during regular trade (as measured by volume delta).

More On Volume Delta: Buying and selling power as calculated by the difference in volume traded at the bid and offer.

QQQ Market Liquidity

SPY Market Liquidity

IWM Market Liquidity

Noting, as the bid in volatility drops, demand is seen rising.

That’s according to one statement by Goldman Sachs Group Inc‘s (NYSE: GS) trading desk which said: “CTAs [are] purchasing ~$5B of S&P this week, regardless of what the tape does.”

That statement echoes what JPMorgan Chase & Co (NYSE: JPM) Marko Kolanovic’s said last year. Kolanovic suggested equities would rally short-term with the S&P 500 auctioning as high as $4,000 on the basis of low rates, improved fundamentals, buybacks, as well as systematic and hedge fund strategies. Kolanovic has since downgraded growth and suggested the limited potential for further upside despite odds of a sustained economic recovery.

Important to add also is the large February monthly options expiration (OPEX), after which, the interest at the $3,900.00 S&P 500 option strike will roll-off.

Why is this important? Option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure.

What To Expect: Thursday’s regular session (9:30 AM – 4:00 PM ET) will likely open inside of prior-balance and -range, suggesting the limited potential for immediate directional opportunity.

This comes alongside a resumption of balance, acceptance of higher prices (above a prominent high-volume area), and an overnight rally-high at $3,959.25.

More On Overnight Rally Highs: Typically, there is a low historical probability associated with overnight rally-highs ending the upside discovery process.More On Volume Areas: A structurally sound market will build on past areas of high-volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low-volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low-volume, then future discovery ought to be volatile and quick as participants look to areas of high-volume for favorable entry or exit.

Given the above dynamics, and the S&P 500’s move back below the $3,919.75 spike base (i.e., Wednesday’s worst case outcome), the following frameworks ought to be applied.

In the best case, the S&P 500 opens and remains above the $3,900.00 confluence zone. Auctioning beneath $3,900.00 turns the high-volume area (HVNode) nearby into supply, offering initiative sellers favorable entry and responsive buyers favorable exit.

So, above $3,900.00, expect balance-to-higher. Below $3,900.00, expect the potential for downside discovery.

What Happened: U.S. stock indexes resolved a week-long trading range, Friday.

What Does It Mean: As the new administration looked to advance the status of coronavirus relief, U.S. stock index futures established record highs.

This comes as stock indexes, particularly the S&P 500, traded sideways after a rapid de-risking event associated with the GameStop Corporation (NYSE: GME) crisis, and subsequent v-pattern recovery.

More On The V-Pattern: A pattern that forms after a market establishes a high, retests some support, and then breaks above said high. In most cases, this pattern portends continuation.

As stated on Friday, the tight trading range is most likely attributable to the large February monthly options expiration (OPEX), after which, the interest at the $3,900.00 S&P 500 option strike will roll-off.

Graphic 1: Physik Invest maps out the purchase of call and put options in the SPDR S&P 500 ETF Trust (NYSE: SPY), for the week ending February 12, 2021. Activity in the option market was primarily concentrated in short-dated tenors near $390, a strike that corresponds with $3,900.00 in the cash-settled S&P 500 Index (INDEX: SPX).

Why’s this? Most funds are committed to holding long positions. In the interest of lower volatility returns, these funds will collar off their positions, selling calls to finance the purchase of downside put protection.

As a result of this activity, option dealers are long upside and short downside protection.

This exposure must be hedged; dealers will sell into strength as their call (put) positions gain (lose) value and buy into weakness as their call (put) positions lose (gain) value.

Now, unlike theory suggests, dealers will hedge call losses (gains) quicker (slower). This leads to “long-gamma,” a dynamic that crushes volatility and promotes momentum, observed by lengthy sprints, followed by rapid de-risking events as the market transitions into “short-gamma.”

Long-Gamma Visualized

Long-Gamma Evidence

If the interest near $3,900.00 S&P 500 is not rolled up in price and out in time, then option hedging requirements will change.

However, it is important to note that, in recent days, some exposure has been rolled up in price and out in time. This suggests an inclination by participants to maintain long exposure through OPEX, a day that would mark an end to pinning (which we’ve seen over the past weeks).

One such example can be seen below.

Graphic 4: Purchase of call positions higher in price and farther out in time in the cash-settled S&P 500 Index

What To Do: In coming sessions, participants will want to pay attention to the $3,919.75 spike base and $3,928.25 balance-area high.

More On Spikes: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

Balance-areas make it easy to spot change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

Given the spike out of balance, the following frameworks ought to be applied.

In the best case, the S&P 500 opens and remains above the $3,919.75 spike base, confirming last week’s higher prices. In the worst case, the S&P 500 auctions below the $3,919.75 spike base.

Trade below the spike base would be the most negative outcome and may trigger a new wave of downside discovery, repairing some of the poor structures left in the wake of the aforementioned advance.

Graphic 5: Profile overlays on a 30-minute candlestick chart of the Micro E-mini S&P 500 Futures.

Conclusions: The go/no-go level for next week’s shortened holiday trade is $3,919.75. Trade below this level suggests markets are not yet ready to rally.

Notice: To view this week’s big picture outlook, click here.

What Happened: As the new administration pushes approval of a $1.9 trillion coronavirus relief plan, alongside the approval of another $14 billion for pandemic-hit airlines and signs of improve in the labor market, U.S. stock index futures traded sideways, in prior-balance and -range.

What Does It Mean: Market’s were range-bound after a rapid de-risking event associated with the GameStop Corporation (NYSE: GME) crisis, and subsequent v-pattern recovery.

Pictured: 4-hour profile chart of the Micro E-mini S&P 500 Futures

The tight trading range is most attributable to the large February monthly options expiration (OPEX), after which, the interest at the $3,900.00 S&P 500 option strike will roll-off. Why’s this? Most funds are committed to holding long positions. In the interest of lower volatility returns, these funds will collar off their positions, selling calls to finance the purchase of downside put protection.

As a result of this activity, option dealers are long upside and short downside protection.

The exposure must be hedged: dealers sell into strength as their call (put) positions gain (lose) value and buy into weakness as their call (put) positions lose (gain) value.

Now, unlike theory suggests, dealers will hedge call losses (gains) quicker (slower). This leads to “long-gamma,” a dynamic that crushes volatility and promotes momentum, observed by lengthy sprints, followed by rapid de-risking events as the market transitions into “short-gamma.”

Long-Gamma Visualized

Long-Gamma Evidence

If the interest near $3,900.00 S&P 500 is not rolled up in price and out in time, then option hedging requirements will change.

The absence of strong fundamentally-driven buying (as we’ve seen with such things as DIX), can have serious implications on price action.

More On DIX: For every buyer is a seller (usually a market maker). Using DIX — which is derived from short sales (i.e., liquidity provision on the market making side) — we can measure buying pressure.

Pictured: DIX by Squeeze Metrics

However, it is important to note that, in recent days, some exposure has been rolled up in price and out in time.

One such example can be seen below.

Pictured: Purchase of call positions higher in price and farther out in time in the cash-settled S&P 500 Index

What To Expect: Friday’s regular session (9:30 AM – 4:00 PM ET) will likely open inside of prior-balance and -range, suggesting limited potential for immediate directional opportunity.

Given dynamics discussed in the prior section, the odds of substantial change are low, so long as broad market indices, like the S&P 500, remain in balance (i.e., range-bound).

Also, trading in a prominent area of high-volume ($3,900.00) will likely make for a volatile session as such areas denote the market’s most recent perception of value and offer favorable entry and exit, hence the two-sided trade.

More On Volume Areas: A structurally sound market will build on past areas of high-volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low-volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low-volume, then future discovery ought to be volatile and quick as participants look to areas of high-volume for favorable entry or exit.

Going forward, participants will look to the overnight rally-high at $3,928.25, and low-volume structure beneath the $3,880.00 HVNode, which offered responsive buyers favorable entry during Wednesday’s intraday liquidation break.

More On Overnight Rally Highs: Typically, there is a low historical probability associated with overnight rally-highs ending the upside discovery process.More On Liquidation Breaks: The profile shape in the S&P 500 suggests participants were “too” long and had poor location.

That said, the following frameworks apply.

In the best case, the S&P 500 remains rotational, at or above the $3,900.00 HVNode. In the worst case, any break that finds increased involvement (i.e., supportive flows and delta) below the $3,880.00 HVNode, would favor continuation as low as the $3,830.75 HVNode.

As stated yesterday, majorchange will be identified with trade above the $3,928.25 overnight rally-high, and below the $3,878.50 regular-trade low.

Notice: To view this week’s big picture outlook, click here.

What Happened: After a volatile Wednesday, U.S. stock index futures rose alongside fiscal stimulus and vaccine optimism, ahead of releases that would shine light on the labor market recovery.

What Does It Mean: After a gap open, participants sold stock indexes into prior value, yesterday.

This comes ahead of the large February monthly options expiration (OPEX), after which, the interest at the $3,900.00 S&P 500 option strike will roll-off. As a result, stickiness near the $3,900.00 high-volume area (HVNode) will likely cease in the absence of option hedging requirements.

More On Volume Areas: A structurally sound market will build on past areas of high-volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low-volume area which denotes directional conviction and ought to offer support on any test).

If participants were to auction and find acceptance into areas of prior low-volume, then future discovery ought to be volatile and quick as participants look to areas of high-volume for favorable entry or exit.

Pictured: Micro E-mini S&P 500 Future.

Further, we have numerous pieces of context to unpack prior to getting into today’s outlook on trade.

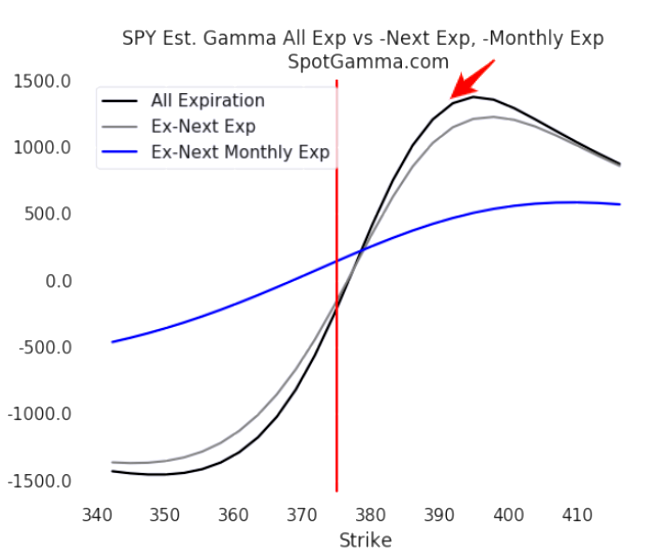

First, the v-pattern recovery after the recent de-risking event suggests room for higher. Second, the market is stuck in a long-gamma environment that favors less volatility (as witnessed during Wednesday’s muted intra-day sell-off and recovery). Third, the S&P 500 is trading just shy of $3,940.00, a primary upside target based on a multi-month balance-area projection.

More On The V-Pattern: A pattern that forms after a market establishes a high, retests some support, and then breaks above said high. In most cases, this pattern portends continuation.

More On Gamma: Gamma is the sensitivity of an option to changes in underlying price. Dealers that take the other side of option trades hedge their exposure to risk by buying and selling the underlying.

When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Graphic 1: SpotGamma data suggests S&P 500 at or above “Long-Gamma” juncture.

What To Expect: Thursday’s regular session (9:30 AM – 4:00 PM ET) will likely open inside of prior-range, suggesting limited potential for immediate directional opportunity.

Adding, given dynamics discussed in the prior section, the odds of substantial change are low, so long as broad market indices, like the S&P 500, remain range bound. Also, trading in a prominent area of high-volume ($3,900.00) will likely make for a volatile session as such areas denote the market’s most recent perception of value and offer favorable entry and exit, hence the two-sided trade.

Going forward, participants will look to the overnight rally-high at $3,928.25, and low-volume structure beneath the $3,880.00 HVNode, which offered responsive buyers favorable entry during Wednesday’s intraday liquidation break.

More On Overnight Rally Highs: Typically, there is a low historical probability associated with overnight rally-highs ending the upside discovery process.More On Liquidation Breaks: The profile shape in the S&P 500 suggests participants were “too” long and had poor location.

Knowing participants are doing a good job of defending their ~7% advance, a non-typical weekly trading range, after taking out the 127.20% price extension, a typical recovery target, and leaving minimal excess (i.e., a proper end to price discovery) at the high, odds point to the increased potential for higher trade or balance in the coming session(s).

That said, the following frameworks apply.

In the best case, the S&P 500 remains rotational, at or above the $3,900.00 HVNode. In the worst case, any break that finds increased involvement (i.e., supportive flows and delta) below the $3,880.00 HVNode, would favor continuation as low as the $3,830.75 HVNode.

Major change will be identified with trade above the $3,928.25 overnight rally-high, and below the $3,878.50 regular-trade low.

What Happened: After prices were advertised below balance in the week prior, responsive buyers in the S&P 500 began a rally that found acceptance back inside a larger balance-area, near the $3,800 high-open interest strike.

Thereafter, initiative buyers extended the S&P 500’s rally, breaking the index above its $3,824.25 balance-area high (BAH), before establishing acceptance near the $3,850.00 price extension, an upside target, and auctioning back into range, repairing poor structures left in the wake of discovery.

What Does It Mean: In light of a failed breakdown in the week prior, U.S. stock indexes were best positioned for further downside discovery. However, after what appears to be aggressive buying in response to prices below value, it was clear that was not the case.

This leads to the following question: why did selling stop on January 15? One answer, aside from a positive start to the earnings season and prospects for further stimulus, may be OPEX, the January 15 option expiry. On expiration days, delta and gamma exposures change — depending on how derivatives exposure is removed or rolled — which causes dealers to adjust hedges.

According to SpotGamma, the January 15 expiry “resulted in a ~50% reduction in single stock gamma … [which] creates volatility because, as large options positions expire[], are closed and/or rolled, dealers have large hedges they need to adjust. There is a trove of data to suggest that the bulk of single stock call activity is long calls, and based on that we believe dealers (who are short calls vs long stock) therefore have long stock positions to sell.”

Put more simply, the price action may have been attributable to the sale of long stock that hedged expiring short derivatives exposure above the market (i.e., call side).

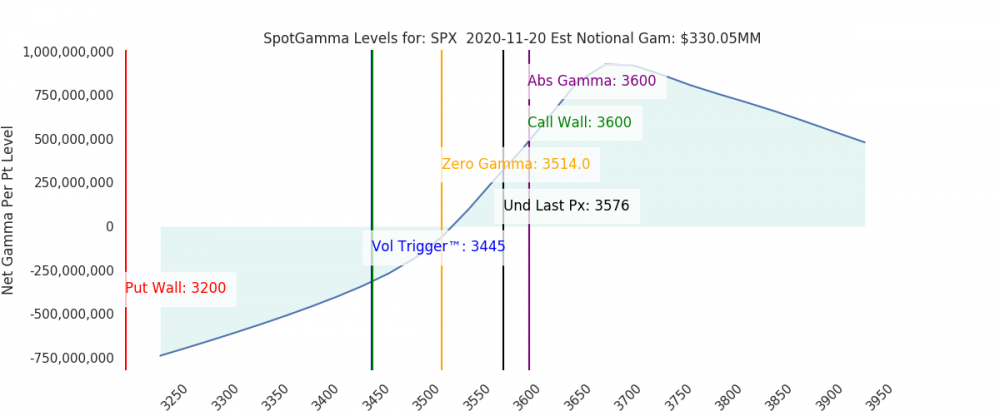

Per the SpotGamma S&P 500 dealer hedging graphic for the January 15 expiry below, “The black line was the mark on Thursday evening, with the red line being the forecasted position on Tuesday. This red line being substantially lower than the black suggests that dealers had to reduce delta exposure as a result of expiration. Note there is a larger shift at overhead prices suggesting this was a ‘call heavy’ expiration.”

Graphic 1: SpotGamma S&P 500 dealer hedging graphic for the January 15 options expiry

After the VIX (i.e., CBOE’s Volatility Index) expiry on January 20, alongside the inauguration of President Joe Biden, the prospects for a rally improved as “event premium in IV dries up … [and] put values drop, which allows dealers (who are short puts) to buy back short hedges … [fueling] a quick rally up to the 3850SPX/385SPY level (green arrow).”

Graphic 2: SpotGamma S&P 500 Gamma Levels

Adding, the number of put options sold to open exceeded the number bought to open, per SpotGamma, suggesting increased confidence in higher prices as market participants look to options for income, and not insurance.

Historically, the returns after such developments are mixed — more often the appearance of strong initiative buying surfaces (e.g., August and January 2020) before a liquidation helps correct excess inventory, and bring sense back into the market.

What To Expect: During Friday’s session in the S&P 500, responsive buying surfaced after a test of the $3,818.25 High-Volume Node (HVNode), above the $3,813.50 ledge (below which is a pocket of low-volume).

In the simplest way, high-volume areas can be thought of as building blocks. A structurally sound market will build on past areas of high-volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low-volume area which denotes directional conviction and ought to offer support on any test).

If participants were to auction and find acceptance into areas of prior low-volume, then future discovery ought to be volatile and quick as participants look to areas of value for favorable entry or exit.

After the S&P 500 found acceptance above the $3,813.50 ledge and $3,824.25 BAH, it encountered responsive selling near the $3,840.75 HVNode, the site of a downtrend line. Since the selling transpired at a visual level, market participants know that technically-driven, short-term traders in control. In other words, institutions (e.g, funds) tend not to transact at exact technical levels.

Given the aforementioned dynamics, participants will come into Monday’s session knowing the following:

The S&P 500’s higher-time frame breakout remains intact, per graphics 7, 8, and 9.

Late last year, JPMorgan Chase & Co. (NYSE: JPM) strategist Marko Kolanovic suggested equities would rally with the S&P 500 auctioning as high as $4,000 on the basis of low rates, improved fundamentals, buybacks, as well as systematic and hedge fund strategies. Since then, Kolanovic downgraded growth and expressed the limited potential for further upside.

The earnings of heavily weighted index constituents suggests participants discount improved speculative flows and delta (e.g., presence of committed buying or selling as measured by volume delta). Please see graphics 4, 5, and 6.

Graphic 4: Supportive order flow in the SPDR S&P 500 ETF Trust (NYSE: SPY), the largest ETF that tracks the S&P 500, on January 20 trend day.Graphic 5: Supportive order flow in the SPDR S&P 500 ETF Trust (NYSE: SPY), the largest ETF that tracks the S&P 500, on January 22.Graphic 6: Speculative derivatives activity for the week ending January 23, 2021.Graphic 7: Daily candlestick chart of the cash S&P 500 Index

Given the above dynamics, the following frameworks apply for next week’s trade.

In the best case, the S&P 500 takes back Friday’s liquidation and auctions above the $3,840.75 HVNode. Expectations thereafter include continued balance or initiative buying to take out the $3,859.75 overnight all-time high (there is a low probability that overnight all-time highs end the upside discovery process). Thereafter buying continues as high as the $3,884.75 price projection, or double the width of the balance-area, the typical target on a balance-area breakout.

In the worst case, any break that finds increased involvement (i.e., supportive flows and delta) below $3,824.25 BAH, would favor continuation as low as the $3,763.75 BAL.

Graphic 8: Profile overlays on a 15-minute candlestick chart of the Micro E-mini S&P 500 Futures

Conclusions: Despite broad-market indices being in a longer-term uptrend, the odds of substantial upside resolve are low. Participants ought to look for favorable areas to transact, such as those high-volume areas in the S&P 500 featured in graphic 8.

All in all, the risk and reward dynamics, at these price levels, are poor.

Graphic 9: 4-hour profile chart of the Micro E-mini S&P 500 Futures

What Happened: U.S. index futures accepted new highs, balancing just above Thursday’s regular trading activity.

What Does It Mean: During Thursday’s regular trade, the S&P 500 confirmed higher prices, with the auction separating and establishing value above prior range.

Overnight, the S&P 500 index future found responsive buyers at the $3,699.75 high-volume area, a valuable price, and initiated up to the $3,720.00 price extension. As of now, ahead of Friday’s derivative expiry, futures have backed off their highs, balancing.

What To Expect: In light of the small overnight gap, the following frameworks apply for today’s trade.

In the best case, buyers maintain conviction and hold the index above the $3,699.75 high-volume node. Holding said reference, and trading into the excess above $3,723.00, would constitute a balance-area breakout. Given the derivative expiry, the odds of sustained directional resolve, today, are low.

In the worst case, if the S&P 500 is brought back into range, participants can expect further balancing. In other words, we’re looking for higher prices, at or above $3,700.00, to facilitate increased trade. A thickening of the composite profile, at the highs, would denote acceptance.

Adding, with any breakout from balance, separation of value is key; such activity would be recognized by range expansion above the aforementioned excess high. A penetration of the $3,699.75 high-volume node, lower, suggests the market is not ready for further upside; less aggressive, responsive trade is the course of action.

Levels Of Interest: The $3,699.75 high-volume node, as well as the excess above $3,723.00.

Sentiment still stretched despite cooling after the vaccine value rotation on news of further lockdowns, which could have a material consequence on the economic recovery.

The pandemic-induced liquidation of businesses not equipped to survive disruption and the accelerated adoption of new technology suggests growth stocks have staying power.

Broad-market equity indices ended in a larger balance area suggesting further acceptance of the positive response to upside earnings surprises, a divided government, and vaccine results.

Friday’s monthly options expiry may mark a decisive move depending on how existing derivatives exposure is rolled forward and the presence of impactful news.

Institutions differ in opinion over the market’s strength into year-end.

What Happened: Following the post-election rally, U.S. index futures remained range-bound as sentiment cooled in the face of new lockdowns and fading stimulus hopes.

What Does It Mean: After Monday’s initiative upside drive on news that another COVID-19 coronavirus vaccine developed by Moderna Inc (NASDAQ: MRNA) was 94.5% effective at preventing cases of the virus, U.S. index futures pared their advance, as participants struggled to maintain higher prices, evidenced by a divergent delta (i.e., the non-presence of committed buying) and mechanical trade (i.e., low-excess at the edges of balance).

Pictured: Profile overlays on a candlestick chart of the Micro E-mini S&P 500 Futures.

What To Expect: On Friday’s end-of-day sell-off away from value, the S&P 500 closed within a prior balance area marked by the $3,580 spike base and $3,506.25 excess low.

Given that Friday’s session failed to retake Wednesday’s spike liquidation, auctioning back into the micro-composite high-volume node at $3,557, the fairest price to do business during the prior week’s balancing activity, initiative sellers remain in control.

As a result, participants come into Monday’s session knowing the following:

Prior end-of-day spikes were the result of weak-handed, short-term buyers liquidating in panic.

The selling did not attract increased participation (i.e., price diverged from value).

Friday’s monthly options expiry may mark a decisive move depending on how existing contracts are rolled forward. Given that $3,600 is the highest gamma strike, the probability of sustained directional resolve, absent material news, is much lower.

Therefore, in light of a weak response to the $3,557 high-volume node and Friday’s options expiry, participants can carry forward the following frameworks for next week’s trade.

If participants manage to spend time and build value in or below the prior selling activity, then initiative sellers remain in control and the liquidation could be the beginning of a new trend to the downside, confirmed by range expansion beyond the $3,506.25 excess low. Otherwise, there is the potential for a failed break-down in which participants manage to rotate back over the $3,580, a balance area boundary.

Conclusion: Friday’s monthly options expiry may mark the beginning of a decisive move. The only thing that’s needed? A catalyst.

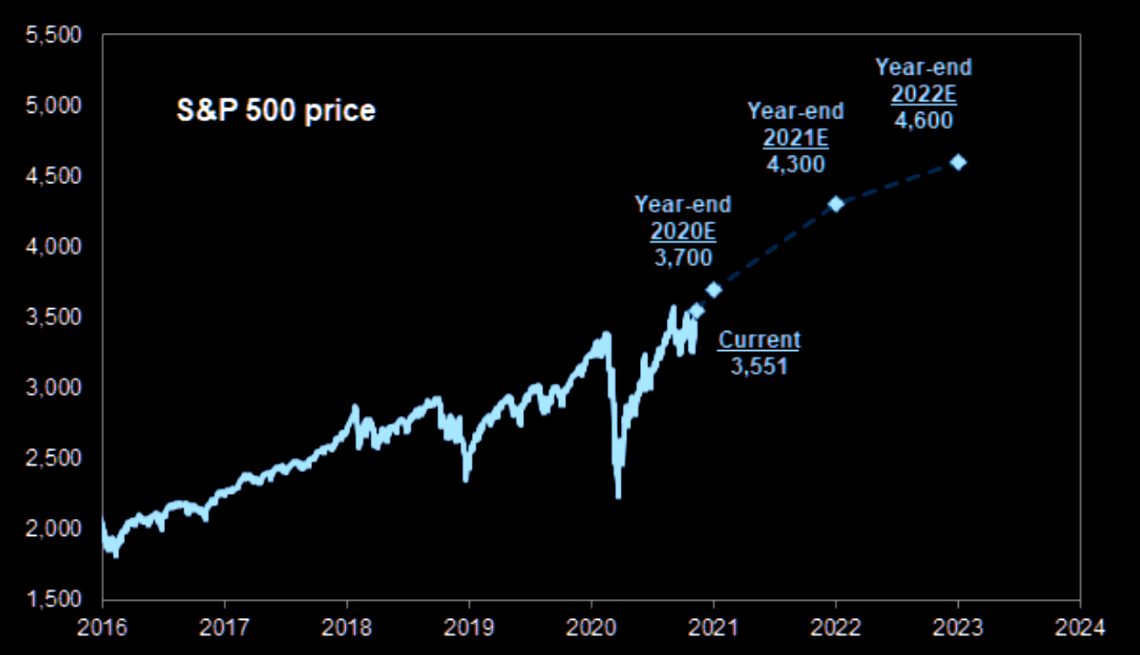

In case of sustained upside, Goldman Sachs Group Inc (NYSE: GS) gives the S&P a $3,700 target on an expectation the v-shape recovery will continue into next year. Contributing factors including a divided government, vaccine administration, rebound in profits, low rates, and a small rise in the yield curve.

Graphic by Goldman Sachs, retrieved from The Market Ear.com.

In case of further balance or selling, JPMorgan Chase & Co (NYSE: JPM) sees vulnerabilities as mutual funds look to sell $160 billion in global equities to revert to their target 60:40 allocation.

Levels Of Interest: Micro-composite HVN at $3,557, the $3,506.25 excess low, as well as the $3,580 balance-area low.

What Happened: Alongside fading stimulus hopes, U.S. index futures remained range bound ahead of Friday’s monthly options expiry, suggesting further acceptance of Wednesday’s spike liquidation.

What Does It Mean: After Thursday’s test of the micro-composite high-volume node at $3,557, the fairest price to do business during last week’s balancing activity, responsive buyers emerged, pushing prices back into Wednesday’s spike liquidation.

Further, the aforementioned liquidation came after participants struggled to maintain higher prices for numerous sessions prior, evidenced by the divergent delta (i.e., non-presence of committed buying) and low-excess at the edges of balance.

As a result, because much of this week’s activity was mechanical, participants come into today’s session knowing that (1) Wednesday’s end-of-day spike was the result of weak-handed, short-term buyers liquidating in panic, (2) the selling did not attract increased participation (i.e., price diverged from value), and (3) Friday’s monthly options expiry could mark a decisive move depending on how existing contracts are rolled forward.

Therefore, in light of Thursday’s response to the $3,557 high-volume node and Friday’s options expiry, participants can carry forward the prior day’s framework for trade.

If participants manage to spend time and build value in or below the prior day’s selling activity, then initiative sellers remain in control and the liquidation could be the beginning of a new trend to the downside, confirmed by range expansion beyond the $3,506.25 excess low. Otherwise, there is the potential for a failed break-down in which participants manage to rotate back over $3,585, the lower boundary of the upper-balance area.

Levels Of Interest: Micro-composite HVN at $3,557, the $3,506.25 excess low, as well as the $3,585 balance-area low.