Editor’s Note: Yesterday, it came to my attention that the top-most graphic quoted outdated levels. Great time for that to happen, knowing that all upside levels came into play, haha!

My apologies for failing to update that graphic, properly. In the future, if you have concerns over levels, scroll to the bottom where you see the text: “Click here to load today’s updated real-time key levels.” By clicking, you will be directed to a real-time, updated TradingView chart.

If any other questions (or you simply want to stay in touch throughout the session), email me at renato@physikinvest.com. Happy trading!

Market Commentary

Equity index futures trade sideways to higher with most commodities. Volatility ebbs.

- Strong balance sheets, investment, labor.

- Ahead: Retail sales, sentiment, and more.

- Positioning for responsive trade, balance.

What Happened: U.S. stock index futures auctioned sideways to higher overnight alongside reports the economy will be supported by consumer balance sheets, business investment, and a healthy labor market.

Ahead is data on retail sales, the Import Price Index, the Empire State Index (8:30 AM ET), University of Michigan consumer sentiment and business inventories (10:00 AM ET), as well as Fed-speak by John Williams (12:20 PM ET).

What To Expect: As of 6:30 AM ET, Friday’s regular session (9:30 AM – 4:00 PM EST) in the S&P 500 will likely open outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator. Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

Adding, during the prior day’s regular trade, on strong intraday breadth and divergent market liquidity metrics, the best case outcome occurred.

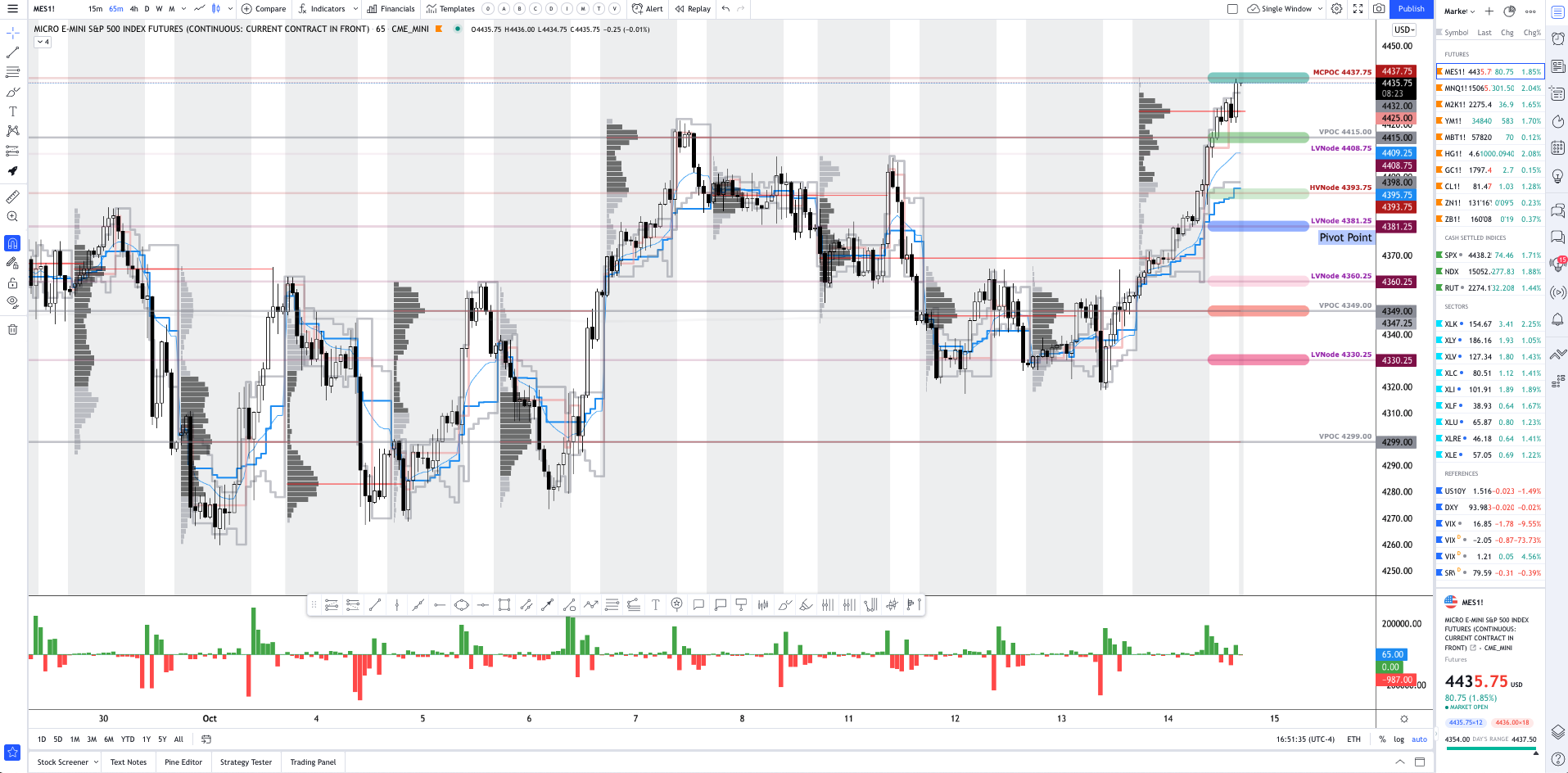

After numerous sessions of a minimum separation in value (i.e., the area where 70% of the day’s volume occurred) failed to support downside price discovery, equity index futures established a rounded bottom before initiative buyers expanded range and value the opposite way.

In light of the recovery process, the S&P 500 – as evidenced by p-shaped emotional, multiple-distribution profile structures – finished, yesterday, just short of the $4,437.75 micro composite point of control (MCPOC) as momentum faded at key areas of resting liquidity.

In other words, the near-vertical price rise was sold responsively. This activity comes after participants saw days of responsive buying into the dip, earlier this week.

Taken together, the status quo remains responsive trade as participants look to balance (i.e., build out a base) ahead of new information. Once new information comes to light, participants will have a base to resolve and build on, directionally, into the end of this year.

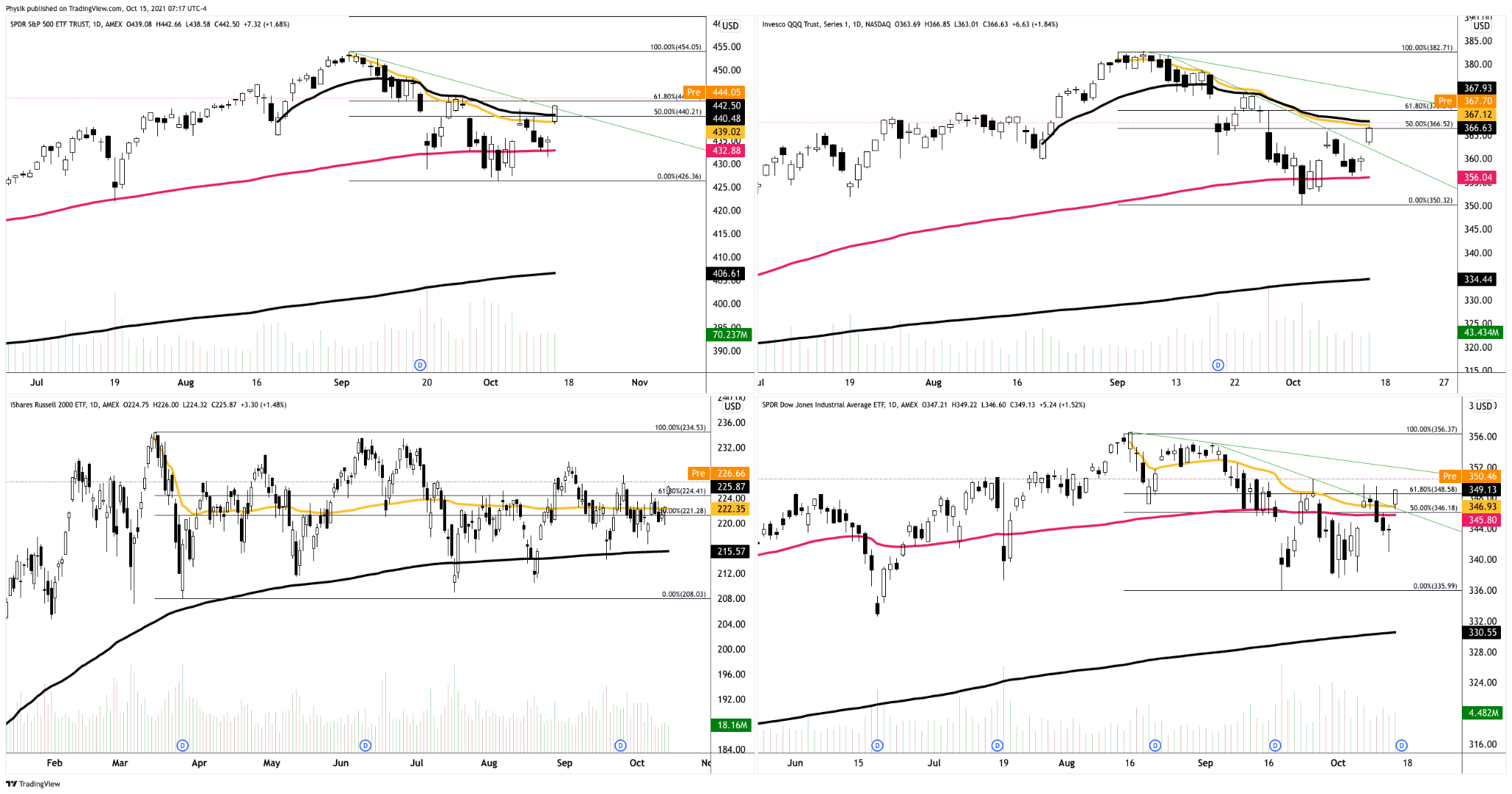

Zooming out, we see the Nasdaq 100 coming into trend, Fibonacci, and volume-weighted average price (VWAP) resistance. This dynamic, alongside poor structure and divergent market liquidity metrics, promotes the responsive trade thesis.

Further, the aforementioned trade is happening in the context of a seasonally bullish cycle of rebalancing and earnings, as well as the risks associated with a taper in asset purchases and a hike in rates.

“The economy is being supported by robust consumer balance sheets, rebounding business investment and a healthy labor market,” adds Hugh Gimber, global strategist at J.P. Morgan Asset Management.

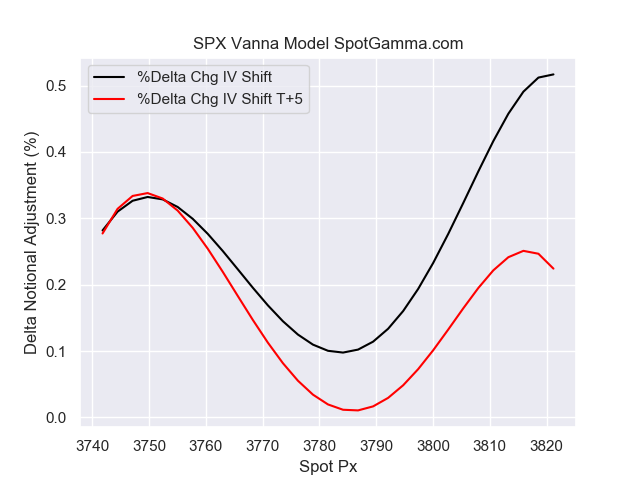

In terms of positioning, coming into October 14, according to SpotGamma, the decay of customers’ long put hedges implied those taking the other side – dealers who warehouse short put risk – would cover their underlying hedges, bolstering the violent move higher.

“[T]his was a vanna/charm type rally back into major resistance. Said another way: we see this as a short cover rally, and the market is unstable.”

Moreover, for today, participants may make use of the following frameworks.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,437.75 MCPOC puts in play the $4,463.75 low volume area (LVNode). Initiative trade beyond the LVNode could reach as high as the $4,481.75 high volume area (HVNode) and $4,510.00 LVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,437.75 MCPOC puts in play the $4,425.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as low as the $4,393.75 HVNode and $4,349.00 VPOC, or lower.

Click here to load today’s updated real-time key levels into the web-based TradingView charting platform. Please note that all levels are derived using the 65-minute timeframe.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Short Covering: The profile shape suggests participants were “too” short and had poor location.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure.

Price Discovery (One-Timeframe Or Trend): Elongation and range expansion denotes a market seeking new prices to establish value, or acceptance (i.e., more than 30-minutes of trade at a particular price level).

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance-areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

Modus operandi is responsive trade (i.e., fade the edges), rather than initiative trade (i.e., play the break).

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

More On Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

Rates: Low rates have to potential to increase the present value of future earnings making stocks, especially those that are high growth, more attractive. To note, inflation and rates move inversely to each other. Low rates stimulate demand for loans (i.e., borrowing money is more attractive). In conjunction with the rapid recovery, lower rates may solicit hawkish commentary as policymakers look to inhibit inflation.

News And Analysis

Upgrades outpace downgrades for second consecutive quarter.

‘Prick this bubble’: Morgan Stanley’s CEO calling for rate hikes.

Bitcoin futures frenzy erupts as day traders pile into ETF plays.

Global energy squeeze triggers unusual decline at U.S. oil hub.

China broke its Evergrande silence and said risks are in check.

JPMorgan Chase suggests more M&A could be on the horizon.

What People Are Saying

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.