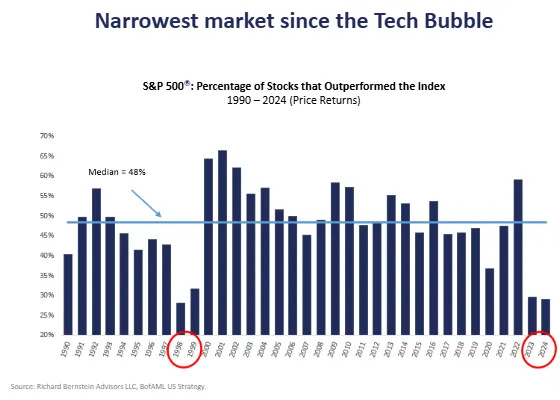

Leading up to the recent decline, market breadth (measuring how many stocks participate in a market move) had weakened. While a handful of dominant stocks masked the weakness, the underlying market was thinning out. Such dispersion [1] [2] [3], where some stocks surge while others lag, can create an illusion of stability in some market environments.

At the same time, liquidity—cash and credit availability—steadily drained from the system. Mechanisms like the reverse repo facility (where banks park excess cash with the Federal Reserve), the Treasury General Account (the government’s cash balance), and money market flows help offset [1] shortfalls. However, this time, they offered little cushion.

New policies—such as tariffs and trade restrictions—reinforce market trends and drive investors toward safer assets like bonds. There is a growing preference for lower bond yields over short-term stock market gains.

While the Federal Reserve controls short-term interest rates, long-term rates are more influenced by broader factors such as inflation expectations, economic growth, and investor sentiment.

Although lower long-term rates can support risk assets, their more immediate and significant impact is on the broader economy. Lowering them reduces borrowing costs for homeowners and businesses, encouraging investment and consumption. Additionally, lowering these yields helps with servicing government debt burdens and improving fiscal stability.

The shifts are intentional. Policymakers are transitioning the economy from dependence on government stimulus, but this adjustment comes with growing pains. Policy narratives and actions may weaken markets and slow economic activity in the short term. One reason receiving attention is the wealth effect—wealthier households, who drive a significant share of consumer spending, tend to spend more when stocks rise. Conversely, market drops can curb this effect and feed an economic slowdown.

Graphic: Retrieved from Bloomberg via @amitisinvesting.

Positioning Context: Setting Up For A Rip

History doesn’t repeat, but it often rhymes. Today’s setup echoes late summer 2024, albeit without the sharp volatility repricing. The difference? This time, investors were prepared, with hedges to act as insurance against market turmoil. The selling has been orderly, creating an illusion of stability and sustaining optimism.

Graphic: Retrieved from JPMorgan Chase via @Marlin_Capital.

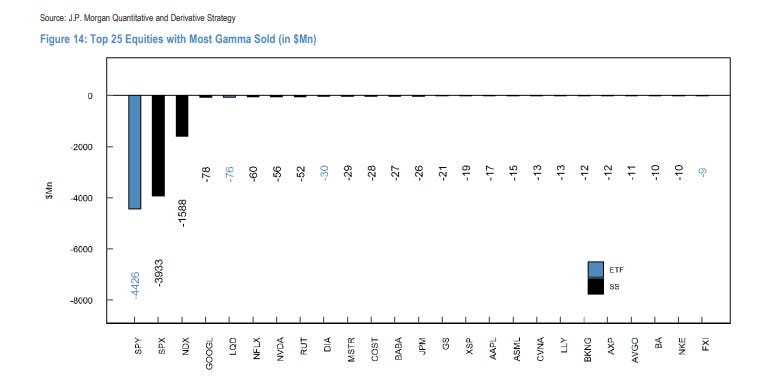

This ongoing decline began in mid-February, coinciding with the unwinding of significant amounts of call options—contracts to buy stocks at a set price. This added indirect pressure on the market through hedging-related flows.

SpotGamma expresses this view, highlighting that the February expiration was “call-weighted” due to strong stock performance leading up to it. This increased the likelihood of a pullback, as call sellers unwound their long stock hedges—a simplified explanation, as other offsetting positions may also be in play.

Graphic: Retrieved from SpotGamma.

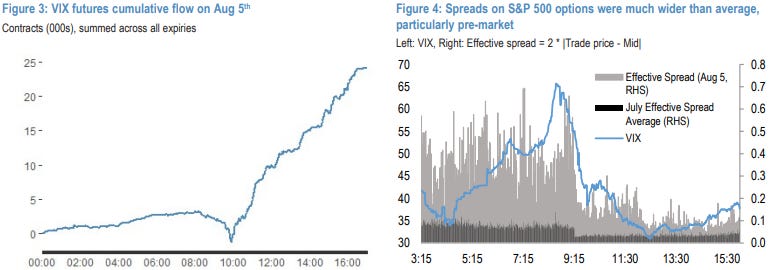

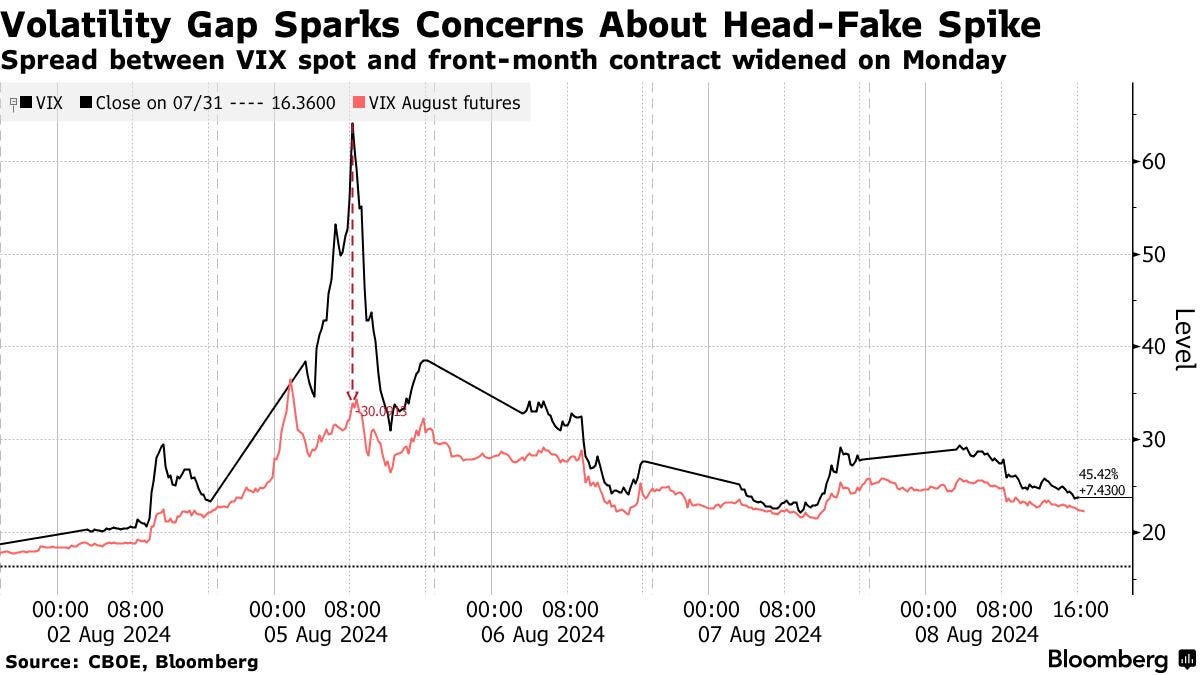

At the same time, after market shocks in August and December 2024, investors focused more on guarding against sudden volatility spikes rather than hedging against a broader market downturn. This pattern is familiar—the S&P 500 and the Cboe Volatility Index (VIX), which measures expected market volatility, sometimes rise together ahead of market peaks.

Meanwhile, within market supply dynamics, this activity has effectively set a floor under VIX pricing, as reflected in the VVIX trending higher since the volatility of late last summer.

Graphic: Retrieved from TradingView.

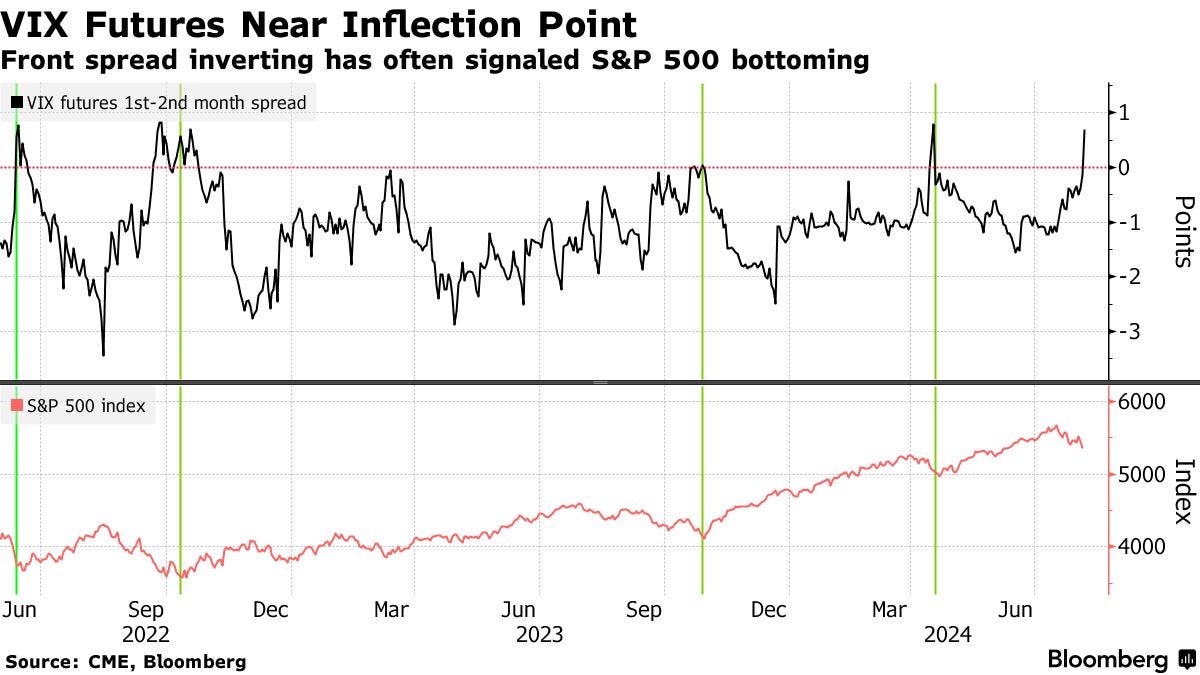

The result? Despite preparations for increased volatility, it hasn’t materialized, frustrating hedge holders and making it harder to identify a market bottom typically marked by extreme volatility spikes. Even with a backwardated implied volatility term structure (where short-term volatility is priced higher than longer-term volatility), anxiety and market movements remain out of sync.

Graphic: Retrieved from TradingView. 1-month VIX less 3-month VIX.

Over time, some traders might shift to longer-dated options, while others might drop their hedges altogether, which could amplify volatility-selling behavior. Ironically, this could create the conditions for shocks they were trying to hedge against.

Given this environment, 2022’s playbook becomes relevant. Back then, investors—rattled by the COVID crash—were prepared, monetizing hedges into declines and keeping a lid on volatility. We may see parallels now. After last week’s economic data, hedgers have been supplying volatility back to the market, offering brief relief as we potentially enter a seasonally stronger period.

Graphic: Retrieved from SpotGamma.

The main takeaway? Current positioning dynamics indicate that investors have effectively managed and responded to the downside. While markets will be volatile, significant shocks may be delayed or avoided.

Graphic: Retrieved from SpotGamma and for illustrative purposes only. SPX prices X-axis. Option delta Y-axis. When the factors of implied volatility (Vanna) and time change (Charm), hedging ratios change. If investors hedge by selling stock to offset long put options, falling implied volatility (as seen in the skew chart above) leads them to buy back the stock, which can support markets.

Context Applied: Trade Structuring

We adapted previously shared structuring guides. Given volatility’s failure to perform, we opted for downside ratios and flies. This worked, and we plan on developing some case studies.

A potential cyclical rebound within a broader period of weakness could be expressed via low-cost positive-delta (bullish) structures, including buying calls while proportionately hedging with stocks or futures, where potential gains from the calls can outweigh hedge-related losses. Additionally, as we prefer, one can deploy verticals and flies, buying options closer to the current market prices while selling more options further out (with an extra far-out option bought to reduce margin requirements if needed).

We and others agree that the Nasdaq 100 (NDX) and higher beta stocks are appealing. For one, relative strength pockets emerge in the NDX versus the SPX, potentially attributable to tariffs disproportionately impacting non-tech sectors. Checking options skews, and NDX options farther away in price may be underpriced for the eventually realized volatility.

Graphic: Retrieved from Bloomberg via Nicholas Smith.

For more on structuring across different products, be they gold or Bitcoin, see our Mar-a-LagoAccords letter published last month.

Disclaimer

By viewing our content, you agree to be bound by the terms and conditions outlined in this disclaimer. Consume our content only if you agree to the terms and conditions below.

Physik Invest is not registered with the US Securities and Exchange Commission or any other securities regulatory authority. Our content is for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any security or other investment. The information provided is not tailored to your financial situation or investment objectives.

We do not guarantee the accuracy, completeness, or timeliness of any information. Please do not rely solely on our content to make investment decisions or undertake any investment strategy. Trading is risky, and investors can lose all or more than their initial investment. Hypothetical performance results have limitations and may not reflect actual trading results. Other factors related to the markets and specific trading programs can adversely affect actual trading results. We recommend seeking independent financial advice from a licensed professional before making investment decisions.

We don’t make any claims, representations, or warranties about the accuracy, completeness, timeliness, or reliability of any information we provide. We are not liable for any loss or damage caused by reliance on any information we provide. We are not liable for direct, indirect, incidental, consequential, or damages from the information provided. We do not have a professional relationship with you and are not your financial advisor. We do not provide personalized investment advice.

Our content is provided without warranties, is the property of our company, and is protected by copyright and other intellectual property laws. You may not be able to reproduce, distribute, or use any content provided through our services without our prior written consent. Please email renato@physikinvest for consent.

We reserve the right to modify these terms and conditions at any time. Following any such modification, your continued consumption of our content means you accept the modified terms. This disclaimer is governed by the laws of the jurisdiction in which our company is located.

“Good investing doesn’t come from buying good things, but from buying things well.” – Howard Marks

There is a lot of noise—it’s exhausting. Today, we will sift through the noise and focus on how we can protect and potentially grow our portfolios this year. This is a follow-up to our Market Tremors letter. But first, let’s clarify the context for our approach. This is a long newsletter, so you may have to view it in another window.

Inflation is back in focus, gold is soaring, and investors are optimistic about stocks. Correlations remain low, dispersion is high, and the market’s volatility pricing/positioning obscures potential risks lurking beneath the surface. The macro landscape is shifting rapidly, yet when we zoom out, we’re confronted with something we’ve discussed before: inflation is here to stay!

For a long time, the expectation was that inflation would take a particular shape—a transitory spike and a manageable trend. Instead, structurally, we’re dealing with a world that is moving away from the low-inflation paradigms of the past. The pillars supporting cheap capital and abundant liquidity—globalization and dovish monetary policy—are shifting.

These shifts are neither sudden nor unexpected. In 2023, we wrote much about the narrative of the ideological struggle between the West and East, particularly with the Russia-Ukraine conflict sparking. Historically, whenever Eastern economies prosper, the West adjusts the rules. Now, it’s more about who controls what. Control over assets, inflation, and interest rates define economic power. Folks like Zoltan Pozsar have warned that the fundamental drivers of the low-inflation era—globalization and financialization—are unraveling, leaving policymakers with little choice.

The well-respected Kai Volatility’s Cem Karsan, a mentor to many, has pointed out in excruciating, albeit digestible detail that the trends favoring high-beta portfolios over the past four decades are reversing. Monetary authorities, particularly the Federal Reserve, have been constrained in their ability to address the widening wealth divide. Their response to inflation in the early 2020s—from creating demand to absorb surplus supplies of low-priced items to structurally restricting demand in response to shortages—was intended to guide the economy along a path of managed declines in activity while maneuvering interest rates to prevent another inflationary flare. Rising populism is a byproduct manifesting as shifts in public demand and political sentiment.

Thus, today’s Mar-a-LagoAccords and the broader economic overhaul signify a significant trade, monetary policy, and financial stability restructuring. Tariffs, a U.S. sovereign wealth fund, and global security restructuring are the key issues at this forefront. The implications of this shift are profound, and markets have yet to adjust. A portfolio for this new environment could creatively layer exposure to stocks, bonds, commodities, and volatility. Understanding the pieces herein will be critical for structuring trades and managing risk. Let’s dive in.

Macro Context: A New Economic Framework

#1 – Tariffs

One significant component of this broader economic overhaul is tariffs. Economist Stephen Miran, nominated by the U.S. President to be Chairman of the Council of Economic Advisers, has outlined how tariffs, historically used to influence trade flows, are being retooled as protectionist instruments and an alternative revenue source.

According to Miran’s AUser’sGuidetoRestructuringtheGlobalTradingSystem and fantastic explanations by Bianco Research founder Jim Bianco, a core issue is a persistently strong dollar distorting global trade balances. If paired with currency adjustments, tariffs could redistribute the costs away from U.S. consumers, “present[ing] minimal inflationary or otherwise adverse side effects, consistent with the [U.S.-China trade war] experience in 2018-2019.” However, this approach risks retaliation or distancing from key trading partners, further fracturing global supply chains.

To mitigate these risks, policymakers consider implementing tariffs in phases, gradually increasing rates to address inflationary pressures and market volatility. Even during the 2018-2019 trade war, tariff rate increases were implemented over time. Additionally, tariffs will be driven by national security concerns, targeting industries essential to defense and technological innovation. From this perspective, policymakers view access to the U.S. market as a privilege.

#2 – Sovereign Wealth Fund

A significant consideration is a U.S. sovereign wealth fund leaning on undervalued national assets to restore fiscal stability. Unlike traditional sovereign wealth funds built on surpluses, this fund would operate by revaluing and monetizing domestic reserves.

Key assets under consideration include undervalued gold reserves and billions in government-possessed bitcoin, which could be integrated into this fund. Bianco says these could total nearly $1 trillion.

This strategy introduces volatility concerns. Those concerned say government exposure and potential speculation on financial assets could lead to instability. Should we invest now for later?

#3 – Global Security Agreements

Beyond trade and monetary policy, a core element of the broader economic overhaul is linking military alliances to economic policy. The longstanding framework in which the U.S. provided security to allies without direct compensation is being rethought. The warnings are explicit; note the President’s Davos remarks and the Vice President’s Munich Security Conference speech.

Under a new paradigm, Bianco summarizes that NATO members may be required to contribute more to defense (say ~5% of GDP), foreign-held U.S. Treasury bonds may be converted into 100-year zero-coupon bonds, reducing short-term debt burdens, and tariff structures may be adjusted based on a country’s alignment with U.S. security interests.

“What Miran said in his paper is: you owe us so much for the last 80 years that what we want to do is a debt swap,” Bianco explains how the U.S. can be paid for being the world’s protector. “Those NATO countries have trillions of dollars of debt. [You’ll] swap it for 100-year or perpetual zero coupon non-marketable Treasury securit[ies]. So, you’re going to swap $10 billion worth of Treasuries for a $10 billion coupon century bond [that] won’t mature for 100 years, [and] won’t get any interest.”

In short, this is a fundamental shift that requires allies to bear a more significant share of security and costs. It’s the Mar-a-LagoAccords, a new financial order and policy framework akin to past agreements that reshaped the global economy, such as the Bretton Woods Agreement of 1944, which established the U.S. dollar as the international reserve currency, and the Plaza Accord of 1985, which coordinated currency adjustments to correct trade imbalances.

The proposed Mar-a-LagoAccords aim to reprice U.S. debt through asset monetization, weaken the dollar to improve U.S. export competitiveness and enforce tariff structures to rebalance global trade.

Positioning Context: Market Positioning Obscures

Tariff-driven price pressures, a weaker dollar, and a floor under interest rates raise bond yields, corporate borrowing costs, and strain leveraged players. This backdrop favors debasement plays and perceived safe havens like bitcoin and gold, which have been climbing for reasons discussed in the past and present.

Graphic: Retrieved from Bloomberg via @convertbond.

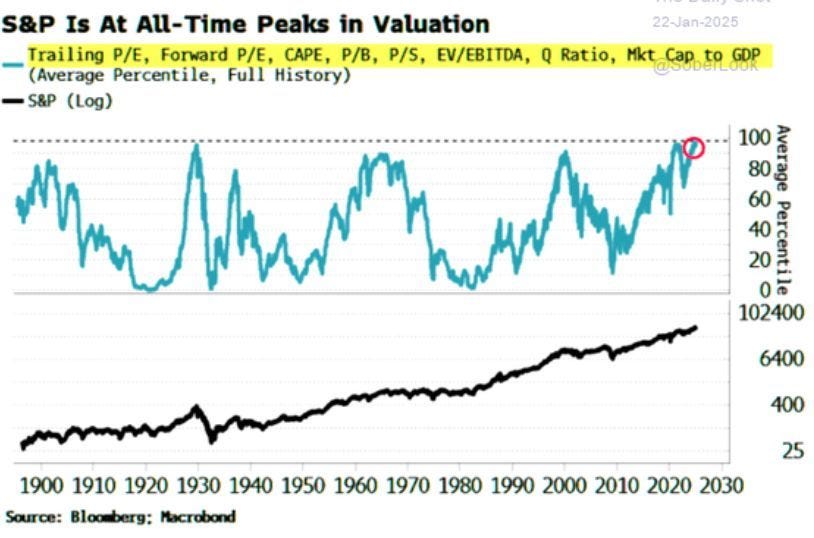

Equities face a less promising outlook. Oaktree Capital highlights that decade-long returns have historically been lackluster when investors bought the S&P 500 at today’s multiples. As Howard Marks puts it, earning +/-2% annually isn’t disastrous—but the real risk lies in a sharp valuation reset, compressed into just a few years, much like the brutal selloffs of the 1970s and 2000s.

Graphic: Retrieved from Bloomberg via Bob Elliott.

While the current market environment may feel frothy, with stretched valuations and narrow leadership, we’re not in an imbalanced 1970s scenario. Also, the possibility of a dollar devaluation serves as a tailwind for S&P 500 earnings, potentially boosting stock prices, Fallacy Alarm explains. Markets are not irrational; instead, they could face modest returns of around 5-6% annually for stocks and bonds over the next decade. Such sanguine sentiment is evident in the options/volatility market, reflecting the distribution of future possible outcomes; the trading and hedging of options make them a robust gauge of future outcomes—offering a view of where markets stand and where they might be headed.

Graphic: Retrieved from Bank of America via Bloomberg.

We observe several key happenings:

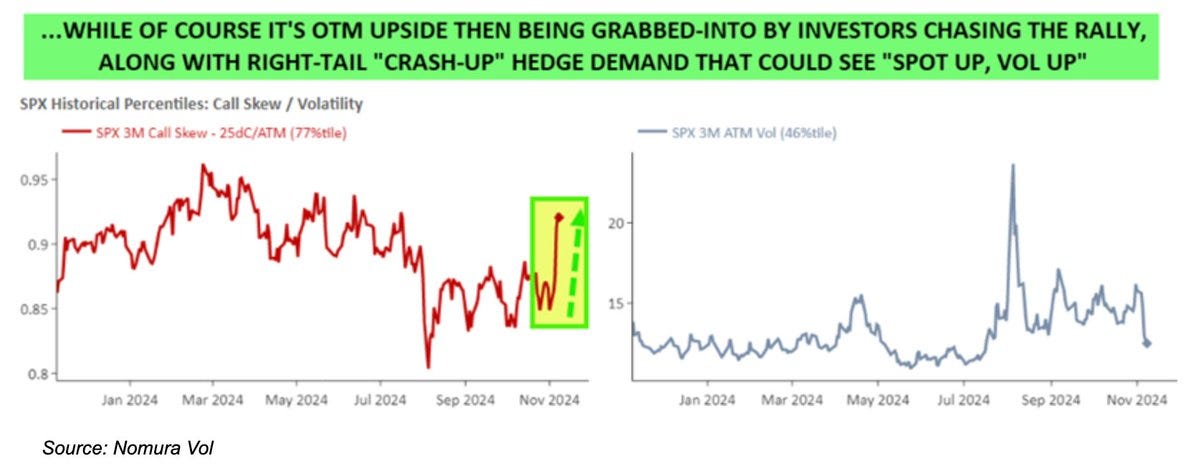

#1 – Hedging Volatility Spikes, Not Market Crashes

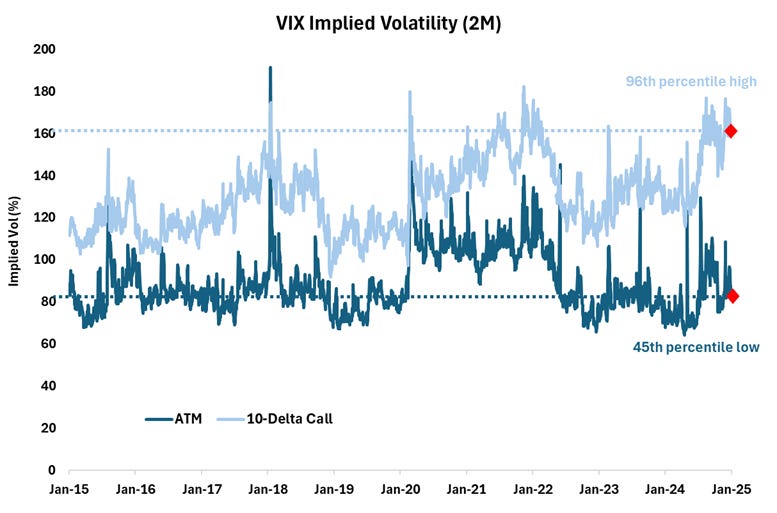

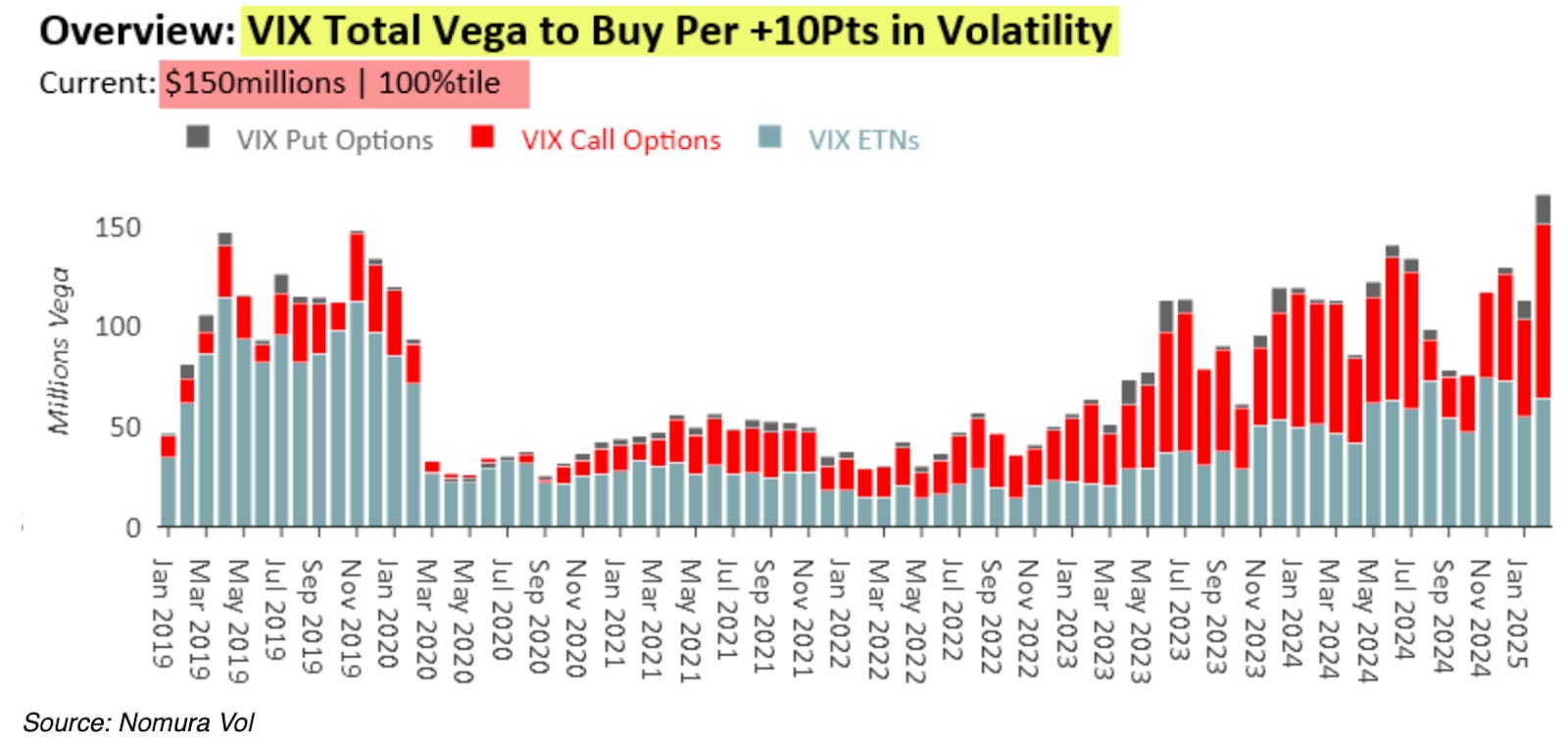

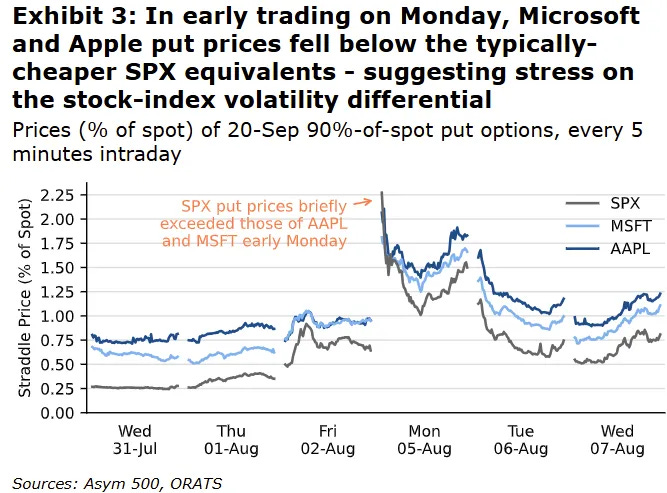

Investors are hedging against potential volatility spikes like those seen on August 5, 2024, when the VIX exploded higher. While the S&P 500 grinds upward and the VIX drifts lower and appears cheap (<16), the VVIX—“VIX of the VIX”—remains elevated. This unusual divergence manifests from demand for VIX calls, suggesting the market worries sharp repricings of risk are more likely than broad equity selloffs. The dynamic boils down to supply and demand; SPX options remain underappreciated—why protect when the market seems stable—meanwhile, VIX options are in demand, bolstering VVIX.

SpotGamma highlights this massive VIX call buying, noting dealer short convexity positioning suggests that, should volatility “wake up,” there could be significant downside pressure on equities and upside pressure on volatility, reinforcing the view that the VVIX’s elevated levels could signal a potential volatility spike, rather than a broad market crash.

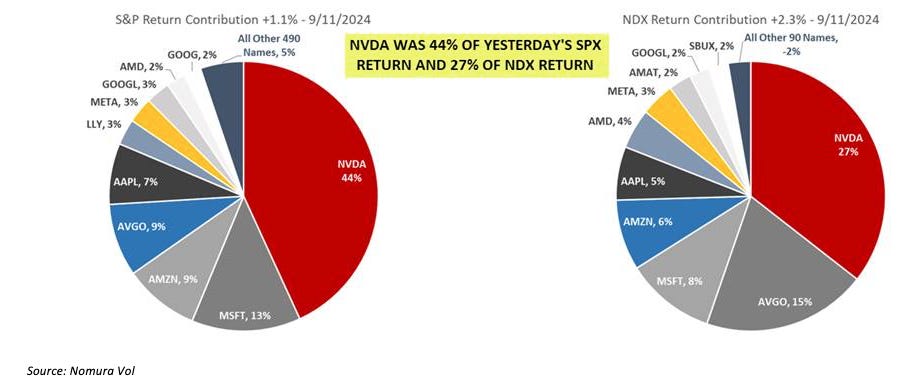

“The aforementioned vega supply is indeed large, but it is innocuous unless provoked,” SpotGamma’s founder Brent Kochuba explains. Still, “with correlation stretched and IVs at lows, there is the potential for an SPX index short vol cover/single stock spasm to push into this upside vega convexity – something that we think a sharp NVDA [earnings] miss could spark.”

#2 – Options Selling and the ‘Buy My Course’ Gurus

Investors are leaning toward short-dated options selling (sometimes packaged within an ETF structure, without regard for price and thoroughly assessing broader market positioning) and structured products.

Graphic: Retrieved from JPMorgan via @jaredhstocks.

As QVR Advisors’ Benn Eifert explains, dynamic creates opportunity: deep out-of-the-money, long-dated volatility in single stocks looks attractive for tail-risk hedging. But there’s a catch—the persistence of this activity reinforces spot-vol covariance (i.e., the relationship between the underlying movements or spot and its volatility or vol). If the market shifts and volatility rises as the underlying asset moves up/down (the usual pattern flips), long volatility positions could become highly profitable, as it is then they would benefit from this reversal in spot-vol dynamics (e.g., 2020).

Graphic: Retrieved from Bloomberg via Kris Sidial. Volatility is fair in indexes; “much better opportunities in singles right now.”

As SpotGamma elaborated, if strength through earnings persists, “it will supply a final equity vol and correlation drop (a ‘final vol squeeze’), ushering in a blow-off equity top. At the same time, these metrics are low enough to justify owning 3-6 month downside protection, as bad things usually happen from these vol levels.”

Graphic: Correlation via TradingView. Stocks are expected to move more independently. Peep the pre-2018 Volmageddon levels.

As an aside, implied correlation measures the degree to which the prices of the assets in the basket are expected to move together (positively correlated) or in opposite directions (negatively correlated). Low correlation, in this case, indicates that the stocks are expected to move independently or in opposite directions; hence, dispersion trades betting on this have performed well.

#4 – The Changing Narrative of Bitcoin and Its Maximalists

Similar patterns emerge in bitcoin. As countries face currency debasement and economic stresses, bitcoin stands out as a hedge to some. Like equities, bitcoin options are underappreciated.

For example, implied volatility has traded under 50% for one-month options, representing an attractive entry point for those looking to position themselves for a surge. This low volatility environment in Bitcoin mirrors the opportunities in equities. Here, bitcoin benefits from any volatility reversal, presenting a compelling case for those looking to participate in a big market move.

Graphic: Retrieved from SpotGamma. Higher skew and IV rank suggest calls are expensive and moves are stretched.

Context Applied: Trade Structuring

Trade structuring this year is all about creativity. We’ve added the following to our portfolios.

#1 – Rates

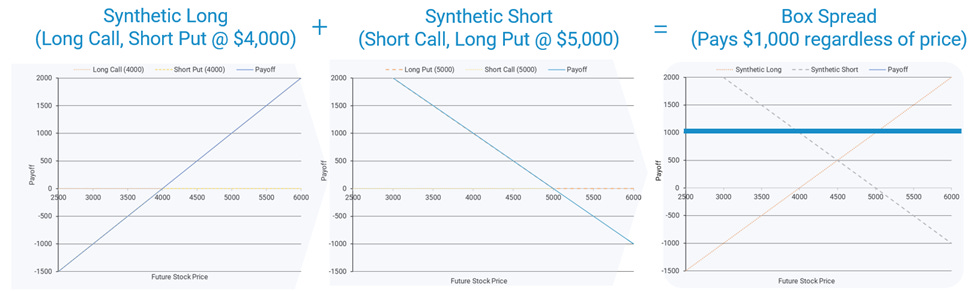

One efficient structure for safeguarding cash is the box spread, which offers several key benefits: a convenience yield, capital efficiency (especially for users of portfolio margin), easy execution via most retail brokers, and favorable tax treatment—60% long-term and 40% short-term if executed using cash-settled index options (e.g., SPX). This strategy combines a bull call spread and a bear put spread, matching lower and higher strikes and the same expiration date.

We frequently trade such structures. For instance, here’s one we purchased at the beginning of this year: BOT +1 IRON CONDOR SPX 100 (Quarterlys) 31 DEC 25 4000/7100/7100/4000 CALL/PUT @2964.25 CBOE

In this case, we invest $296,425 now to receive $310,000 in a year. This represents an implied interest rate of 5.32% or ((3100-2964.25)/2964.25)*(365/314)=0.053234. Note that there is a convenience yield, and that’s due to counterparty risk, as box spreads depend on the Options Clearing Corporation (OCC) to guarantee the transaction.

Tools like boxtrades.com help with tracking yields and finding attractive box structures.

Box trades unlock the power of yield stacking, enhancing returns by layering multiple exposures without increasing capital outlay. They preserve full buying power with portfolio margin for margin-intensive trades like synthetic longs.

For non-portfolio margin traders, yield stacking is less applicable. Instead, you can allocate ~95% of cash to box spreads, locking in your principal at maturity while risking only ~5% (the interest you stand to make), with limited downside.

Low correlation and subdued implied volatility signal stability, but any disruption could spark sharp moves.

As we explained better in Reality Is Path-Dependent, Cem Karsan notes that a slow grind higher cheapens options, fueled by continued volatility selling. Eventually, realized upside volatility will surpass implied, prompting smart money to buy options at these discounts. If the VIX holds steady or rises, it suggests fixed-strike volatility is creeping up, potentially forcing options counterparties to cut exposure or hedge, boosting markets higher; increased call demand could push counterparties to hedge by buying the underlying asset, reinforcing stability and giving a floor to options prices and the market by that token.

The play here? Replace stock exposure with options. You can buy calls outright and hedge them by selling stock—gains on the calls should outpace hedge losses. Karsan has talked about this a lot. One of our moves is to structure broken-wing butterflies or similar: buy an option near the money, sell a larger number of options further out, and cap risk with an even farther out option. In this environment, you can often put on these trades for little cost and exit at multiples higher if the market drifts sideways or up. Please see our website for case studies and example trades.

Don’t overlook crypto, either. Implied volatility remains underappreciated in bitcoin, making synthetic exposures compelling. Swapping spot for synthetic alternatives is a play on these opportunities. Though we haven’t touched them, check out Cboe’s cash-settled options on spot bitcoin: the Cboe Bitcoin US ETF Index (CBTX) and Cboe Mini Bitcoin US ETF Index (MBTX).

#3 – Hedging

Though less attractive now, VIX calls and call spreads remain a powerful tool for hedging tail risks. In our RealityIsPath-Dependent letter, we explore this topic further.

There are more compelling structures within the S&P 500 complex, particularly back spreads. For example, a put back spread involves selling a higher strike put option and buying a larger number of lower strike put options, positioning you to profit from substantial volatility shifts—similar to what we saw on August 5, 2024.

Although this structure takes advantage of the market’s unappealing volatility skew, drift presents challenges; if volatility fails to perform well during a downturn, you risk losing more money than you initially invested in the spread. Caution!

Graphic: Retrieved from Bloomberg via Goldman Sachs.

Bonus: From the White House to Wall Street

We had the opportunity to catch up with Steven Orr, founder of Quasar Markets. We discussed his career and the future of fintech and trading technology. Before Quasar Markets, Orr worked as an executive at Money.net and Benzinga. He also serves on the board of the American Blockchain and Cryptocurrency Association. His diverse background includes positions with the White House, the U.S. State Department, the PGA Tour, the NBA, and various professional sports leagues. Orr frequently shares his insights on TV and appears at events like the World Economic Forum. Check it out, and thank you, Steven!

Disclaimer

By viewing our content, you agree to be bound by the terms and conditions outlined in this disclaimer. Consume our content only if you agree to the terms and conditions below.

Physik Invest is not registered with the US Securities and Exchange Commission or any other securities regulatory authority. Our content is for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any security or other investment. The information provided is not tailored to your financial situation or investment objectives.

We do not guarantee the accuracy, completeness, or timeliness of any information. Please do not rely solely on our content to make investment decisions or undertake any investment strategy. Trading is risky, and investors can lose all or more than their initial investment. Hypothetical performance results have limitations and may not reflect actual trading results. Other factors related to the markets and specific trading programs can adversely affect actual trading results. We recommend seeking independent financial advice from a licensed professional before making investment decisions.

We don’t make any claims, representations, or warranties about the accuracy, completeness, timeliness, or reliability of any information we provide. We are not liable for any loss or damage caused by reliance on any information we provide. We are not liable for direct, indirect, incidental, consequential, or damages from the information provided. We do not have a professional relationship with you and are not your financial advisor. We do not provide personalized investment advice.

Our content is provided without warranties, is the property of our company, and is protected by copyright and other intellectual property laws. You may not be able to reproduce, distribute, or use any content provided through our services without our prior written consent. Please email renato@physikinvest for consent.

We reserve the right to modify these terms and conditions at any time. Following any such modification, your continued consumption of our content means you accept the modified terms. This disclaimer is governed by the laws of the jurisdiction in which our company is located.

In this newsletter, we interview David Aferiat, co-founder of Trade Ideas, about his entrepreneurial journey and the future of fintech and trading technology.

From building Trade Ideas—a well-known name in self-directed investing—to advising startups, Aferiat has worked at the intersection of finance and technology for about two decades.

Our conversation explored the evolution of self-directed investing, including the recent introduction of commission-free trades and the implications of AI and automation. Also, Aferiat shared a few insights on building businesses and partnerships.

You can watch the video at this link and below. An edited transcript offering key context follows. We hope you enjoy this lighthearted conversation and some of our other recent newsletters, which are a nice break from the usual. Cheers!

Thanks for joining me, David. You’re based in Atlanta, Georgia, right?

I’ve been here for about 24–25 years. I raised a family, started several businesses, and moved here as a consultant after getting my MBA in Dallas. Atlanta has been great—it connects you to the world with direct flights and is a great place to raise a family.

I’ve known you since 2019 when I was at Benzinga. You were one of my first interviews, and we talked about how retail trading was evolving. You discussed AI before it became the hot narrative it is today. But before we dive into that, I’d love to hear more about your background—your heritage, upbringing, and early career. Can you take me back?

Absolutely. I love how our conversations have come full circle, especially with AI as a recurring theme.

I’m the son of an immigrant from North Africa, part of France before gaining independence. Half of my family went to France, and the other half went to the U.S. My grandfather was an entrepreneur, but my father took a different path, building a successful career in the hospitality industry.

My grandfather introduced me to the stock market. We used to pull out graph paper and manually track stocks using point-and-figure charts. That early exposure sparked my fascination with markets, which I later channeled into Trade Ideas—something much bigger than myself, helping people make better trading decisions.

Given your family’s history, you could have been risk-averse but took an entrepreneurial path instead. Why is that?

It is a generational ricochet effect.

My grandfather was entrepreneurial, but my father was more conservative—out of necessity. He had to adapt, assimilate, and establish financial security. I respect that, but I also felt a pull toward entrepreneurship, like my grandfather.

I relate to that. My grandfather was entrepreneurial overseas, but my dad was more conservative after immigrating to the U.S. It seems we take the best of both worlds. What did you study in school, and what was your early career like?

I graduated from the University of Texas and earned my MBA at Kraft Foods; Kraft paid for my MBA, and after that, I worked in consulting, which brought me to Atlanta. Consulting felt like an extension of my MBA—applying models, engaging teams, and managing projects, which proved valuable in building a startup like Trade Ideas.

Tell me about the early days of Trade Ideas. What problem were you solving?

It started as a web-based tool displaying market data. Over time, we refined it to help traders make better decisions.

We gained traction when major brokerages like E*Trade, Scottrade, Interactive Brokers, and TD Ameritrade integrated our tools. This helped us scale and reach more traders. Today, I apply the lessons I learned at Trade Ideas to assist fintech companies in growing, whether they are building indicators, execution tools, or enhancing market infrastructure.

What did it take to secure those partnerships?

It’s about identifying champions within organizations—decision-makers with budget control and internal advocates who can push your product forward. We built a compelling case, showing how our technology improved engagement and retention.

Where do you see trading technology evolving?

Technology, especially AI, transforms how people interact with financial markets, driving a convergence where platforms like Robinhood and Fidelity adopt each other’s features. The emergence of 24-hour trading in equities appears inevitable, with crypto setting a standard for continuous market access. Traditionally, equities led in financial innovation, but in recent years, they have fallen behind. Also, the number of publicly traded companies has nearly halved since the 1990s, resulting in the dominance of larger firms and a growing need for fractional trading.

How did you stay committed to Trade Ideas for so long in this age of instant gratification?

Purpose and customer experience are key to me.

Joey Coleman’s book, NeverLoseaCustomerAgain:TurnAnySaleintoLifelongLoyaltyin100Days, emphasizes mapping customer touchpoints and delivering value from the first interaction. When engaging with customers, the first impression is crucial. It should demonstrate the long-term value, allowing them to instantly envision an ongoing relationship where they continue to benefit from the experience. That philosophy has been applied to Trade Ideas and continues influencing my work today.

How did you handle delegation as Trade Ideas grew?

Surrounding yourself with the right people is essential. For example, I am involved with organizations like the Entrepreneurs’ Organization (EO) and connect with other leaders who face similar challenges.

Generally, successful teams combine strategic thinkers, executors, relators, and communicators. If there are too many strategists, nothing gets done; too many executors, and there is no long-term vision.

You’re also involved in Avid Vines and Advintro. Can you share more about those ventures?

Avid Vines is an organic champagne import business rooted in my French heritage. It’s been a journey of learning and assembling the right team.

Advintro keeps me connected to fintech, where I advise startups and established companies on everything from scaling to customer experience.

What’s a key lesson you pass on to clients?

One big one is the power of experience and, within those experiences, intentionally moving people to create and connect themselves. A book called The Art of Gathering: How We Meet and Why It Matters helped me refine how I view and create impactful events, whether for fintech or entrepreneurs.

Last year, I co-led a conference on perseverance that brought together about 500 entrepreneurs. We spent over 18 months and had a $1 million budget to create this event, featuring speakers like Peter Diamandis and former Senator Martha McSally. The theme was perseverance and building routines that lead to a better future self.

Again, success isn’t just about KPIs; it’s about ensuring each team member is in the proper role, leveraging the collective strengths, and working toward a shared goal.

What daily habits keep you focused?

Self-care is essential. I follow GAMER: Gratitude, Affirmations, Meditation, Exercise, and Rest/Reading. It keeps me balanced and focused on the next version of myself.

Final question—what are the underrated characteristics of successful founders?

Empathy, humility, and integrity are essential for success. They come from relying on others, keeping promises, and staying true to one’s values. Those lacking these qualities may struggle with inner conflict, which can ultimately hold them back.

Disclaimer

By viewing our content, you agree to be bound by the terms and conditions outlined in this disclaimer. Consume our content only if you agree to the terms and conditions below.

Physik Invest is not registered with the US Securities and Exchange Commission or any other securities regulatory authority. Our content is for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any security or other investment. The information provided is not tailored to your financial situation or investment objectives.

We do not guarantee the accuracy, completeness, or timeliness of any information. Please do not rely solely on our content to make investment decisions or undertake any investment strategy. Trading is risky, and investors can lose all or more than their initial investment. Hypothetical performance results have limitations and may not reflect actual trading results. Other factors related to the markets and specific trading programs can adversely affect actual trading results. We recommend seeking independent financial advice from a licensed professional before making investment decisions.

We don’t make any claims, representations, or warranties about the accuracy, completeness, timeliness, or reliability of any information we provide. We are not liable for any loss or damage caused by reliance on any information we provide. We are not liable for direct, indirect, incidental, consequential, or damages from the information provided. We do not have a professional relationship with you and are not your financial advisor. We do not provide personalized investment advice.

Our content is provided without warranties, is the property of our company, and is protected by copyright and other intellectual property laws. You may not be able to reproduce, distribute, or use any content provided through our services without our prior written consent. Please email renato@physikinvest for consent.

We reserve the right to modify these terms and conditions at any time. Following any such modification, your continued consumption of our content means you accept the modified terms. This disclaimer is governed by the laws of the jurisdiction in which our company is located.

Editor’sNote: In pursuing quality, we want to emphasize that we presented an inadequate definition in the haste to publish this letter. The Volume-Weighted Average Price (VWAP) reflects the average price at which an asset has traded over a specific period, weighted by volume. It is calculated by multiplying the price of each trade by the number of shares traded at that price, summing these products, and dividing by the total shares traded during that timeframe. We sincerely apologize for that!

Our technical analysis toolkit is streamlined to prevent analysis paralysis. The primary indicator we rely on is the Volume-Weighted Average Price (VWAP), which combines price and volume to provide a clearer view of an asset’s traded price over time.

Firms like Citadel use VWAP to execute trades, minimizing market impact and achieving better prices. VWAP can be applied to various strategies, including trend identification, mean reversion, and support/resistance trading.

Below, we explain VWAP and recommend following experts on the topic, like Brian Shannon of AlphaTrends. Additionally, platforms like TradingView offer this tool free.

What is Anchoring?

Anchoring is a psychological bias where people rely heavily on the first piece of information they encounter when making decisions. In financial markets, price levels often act as anchors that influence trading behavior. For example:

“If the price hits this level, I’ll take profit.”

“If it drops below this level, I’ll cut my losses.”

These anchor points serve as the basis for support and resistance levels in technical analysis. At support, there is buying interest (demand); at resistance, there is selling interest (supply). When these levels are breached, their roles can reverse: previous resistance can turn into new support, and vice versa.

Why Anchoring Matters?

Think of the average price people pay to enter a trade. Future decisions, like selling or holding, are often based on this price. If the price breaks a significant support level, traders who bought at higher prices may rush to sell to avoid further losses, creating resistance at those levels.

What are VWAPs?

Volume-Weighted Average Price (VWAP) is calculated by multiplying the price of each trade by the number of shares traded at that price, summing these values, and then dividing by the total shares traded during the period.

The Anchored VWAP (AVWAP) extends this concept by incorporating time, price, and volume to determine the average price participants have paid since a specific starting point. This starting point could be a pivotal event, such as:

A significant announcement (e.g., earnings, Federal Reserve decisions).

The start of a new trading period (e.g., month-to-date, year-to-date).

A considerable price movement (e.g., swing highs or lows).

AVWAP helps answer:

Have most traders been in a winning or losing position since the anchor date?

Where might support or resistance form based on trading activity?

AVWAP in Action

Above AVWAP: Most participants are profitable if the price exceeds the AVWAP line.

Below AVWAP: Most participants are likely at a loss if the price is below the AVWAP line.

Clusters of AVWAPs: Multiple AVWAP lines close together often create strong support or resistance zones.

Sample Uses

Intraday Support: In short-term trading (e.g., 2-minute charts), a rising AVWAP often acts as support. Prices may repeatedly bounce off the AVWAP line during the trading session.

Breaking Trends: In this example with Shopify Inc (NYSE: SHOP), the stock broke an uptrend, and the AVWAP line from earlier highs acted as resistance. Traders could use this to decide where to sell or avoid buying.

MomentumTrading: Expanding on breaking trends, when trading stocks with strong prior momentum, the AVWAP from the latest spike high can serve as a dependable level to take profits. Here’s an example from Brian Shannon himself.

Why AVWAP Works

AVWAP is popular because Chief Investment Officers use it to evaluate trade quality, and liquidity algorithms are frequently designed to buy or sell near the VWAP, establishing it as a benchmark for institutional trading.

A Practical Application

When AVWAP lines from previous peaks and troughs come together, the stock often breaks out decisively above or below this “pinch” zone. For a depressed stock, pairing an AVWAP pinch with a rising short interest can prepare us for a squeeze! Below is an excellent example from Brian Shannon.

Combining AVWAP with Other Indicators

To enhance decision-making, we can pair AVWAP with:

Simple Moving Averages: A rising moving average signals buying interest.

Volume Data: To confirm whether trading activity supports the price levels.

Key Takeaways

The AVWAP provides a more customized view by anchoring the VWAP calculation to a specific point in time (e.g., a significant price level or event), which helps view price, volume, and time factors more dynamically. It is most effective alongside other tools like market profiles, volume profiles, and moving averages.

Disclaimer

By viewing our content, you agree to be bound by the terms and conditions outlined in this disclaimer. Consume our content only if you agree to the terms and conditions below.

Physik Invest is not registered with the US Securities and Exchange Commission or any other securities regulatory authority. Our content is for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any security or other investment. The information provided is not tailored to your financial situation or investment objectives.

We do not guarantee the accuracy, completeness, or timeliness of any information. Please do not rely solely on our content to make investment decisions or undertake any investment strategy. Trading is risky, and investors can lose all or more than their initial investment. Hypothetical performance results have limitations and may not reflect actual trading results. Other factors related to the markets and specific trading programs can adversely affect actual trading results. We recommend seeking independent financial advice from a licensed professional before making investment decisions.

We don’t make any claims, representations, or warranties about the accuracy, completeness, timeliness, or reliability of any information we provide. We are not liable for any loss or damage caused by reliance on any information we provide. We are not liable for direct, indirect, incidental, consequential, or damages from the information provided. We do not have a professional relationship with you and are not your financial advisor. We do not provide personalized investment advice.

Our content is provided without warranties, is the property of our company, and is protected by copyright and other intellectual property laws. You may not be able to reproduce, distribute, or use any content provided through our services without our prior written consent. Please email renato@physikinvest for consent.

We reserve the right to modify these terms and conditions at any time. Following any such modification, your continued consumption of our content means you accept the modified terms. This disclaimer is governed by the laws of the jurisdiction in which our company is located.

Hedge fund week just wrapped up here in Miami, and I had the chance to catch up with some industry friends like fellow Croatian and former podcast guest Vuk Vukovic. A big shoutout to Vuk and the incredible success of Oraclum Capital, his NYC-based hedge fund! Beyond motivation, these conversations always get us thinking—about how far we’ve come, the lessons learned, and the market patterns emerging. So, today, we’re switching things up a bit.

Breaking Down Thinking vs. Acting in Real-Time

These newsletters often dive deeply into trade theory—how to form opinions, identify dislocations, and structure trades to take advantage of them. Thinking critically about market context is just as important, if not more so, than taking action, as outlined in the case study linked here. But let’s be honest: we don’t always have the luxury of testing every idea before committing capital. Sometimes, decisions must be made on the spot, and more often than not, they’re more straightforward than they appear—they have to be.

To illustrate this, I share a slightly refined diary entry from a year ago, offering reflection and motivation. Market highs, uncertainty, and the fear of missing out create a lot of noise—but they also spark new ways of thinking. I hope this record and perspective spark new ideas on when and how to engage in markets this year ahead.

Take your time, enjoy the read, and try to focus on the bigger picture rather than getting lost in the details. Stay tuned for upcoming podcasts, explainers, and part two of the Market Tremors newsletter. Cheers, and let’s make some money.

On February 16, 2024, my trading partner Justin pointed out a rich, elevated call skew in Super Micro Computer Inc. (NASDAQ: SMCI). This occurs when out-of-the-money call options carry higher implied volatility than at-the-money or in-the-money options, often signaling strong demand for upside exposure. At that point, SMCI had been climbing steadily for weeks, with the charts suggesting a parabolic advance and an imminent climax.

I spotted 200-wide 1×2 ratio spreads that could be opened for credit. Simply put, a ratio spread is an options structure in which you buy a contract at one strike and sell two (or more) at another, further away. I often use such a structure when volatility is more steeply skewed, meaning certain strikes—like deep out-of-the-money (OTM) calls—have much higher implied volatility (IV) because traders expect more risk or extreme moves in that direction.

IV is the amount of movement traders anticipate. A higher IV means the market expects more significant price swings, leading to more expensive options, while a lower IV suggests less expected movement, making options cheaper—factors like earnings reports, economic data, or overall market uncertainty influence IV.

In this case, using Schwab’s thinkorswim lookback feature, implied volatility on the call side ranged from the mid-100s near the current market price to over 200% at the furthest strike. On the put side, things got even wilder—volatility climbed from the mid-100s near the market price to several hundred percent at the farthest strike, as pictured below. When volatility is this high in far-out-of-the-money options, traders are piling in—either looking for protection or betting on a big, unexpected move.

As the stock was pulled back from its highs, we observed that the excitement in call-side volatility had begun to diminish—it wasn’t as intense as it had been a month earlier, according to SpotGamma data. This served as a key signal for us. A declining enthusiasm for calls indicates that traders are less inclined to chase the stock higher. We were prepared to act on this shift, betting that the stock had reached an interim peak; this was great news for us, as our options structures tend to perform best when volatility stabilizes and the stock drifts rather than making significant, protracted moves.

Right after the market opened, the 23 FEB 24 1300/1500 spread flipped from a 0.50 debit to over a 1.00 credit to open. I didn’t catch it right at the start, but about an hour later, I spotted the opportunity. The pricing looked solid—it offered a credit to close at the money—and everything checked out risk-wise according to my rules. So, I decided to dip my toes in with five units, keeping it on the smaller side for this trade. This all went down on February 16.

SOLD -1 1/2 BACKRATIO SMCI 100 (Weeklys) 23 FEB 24 1300/1500 CALL @1.10

All else equal, if the trade were entirely in the money (ITM), meaning the short strikes are right around the current market price, it would price for about 40.00 credit to close. At the money (ATM), right around the current market price, the structures traded for around 12.00 credit to close. This quick check suggests we’re good to move forward. Here are the orders for one account. You can find a summary screenshot of all orders at the end of this letter.

Given the risk involved in this trade, the abovementioned account could take on a maximum of 8 units. As we’ll see later in this entry, I pushed those limits, possibly going beyond what’s typical for me. However, I justified this by considering the distance between the stock price and the strikes used in the trades, which felt like a safe cushion to work with.

$320,000 (Net Liquidation Value) / $38,000 (Daily Loss at +1 EPR if the Spread’s Long Strike is ATM) = 8.4 units. EPR represents the brokerage firm’s estimate of the maximum expected one-day price range for an underlying security. Net Liquidation Value refers to the total value of a portfolio if all positions were liquidated at current market prices. Here are more details.

A few hours later, implied volatility dropped across the board, with the further out-of-the-money (OTM) options seeing the most significant decline. The implied volatility of the options closest to the stock price fell moderately, while the farther OTM strikes experienced a more substantial drop. This shift worked in our favor and helped make the trade profitable.

The long strike I owned (1300) had an implied volatility of ~190% before, which dropped to ~165% after.

The short strike I sold (1500) had an implied volatility of ~215% before, which dropped to ~180% after.

The trades were closed on the consolidation following the sharp morning liquidation. Here are the trade tickets.

From the panicked price movement, it looked like people late to the party were just selling off existing positions, not necessarily big new sellers entering the market; the stock might eventually retest those higher levels again. Even with the drop, implied volatility stayed high, which is crucial because it suggests continued uncertainty and anticipation of significant movement.

Given how sharp the sell-off was and how many traders were probably surprised by it, I decided to jump back into the trade on February 20—this time with a bigger position, especially after the long weekend when the market had some time to settle. Strikes and trade tickets follow.

SOLD -1 1/2 BACKRATIO SMCI 100 (Weeklys) 1 MAR 24 1300/1500 CALL @1.10

SOLD -1 1/2 BACKRATIO SMCI 100 (Weeklys) 1 MAR 24 1400/1600 CALL @1.10

SOLD -1 1/2 BACKRATIO SMCI 100 (Weeklys) 1 MAR 24 1350/1550 CALL @1.05

With the liquidation, the trade above was farther away from current prices than the last. Additionally, we moved it to next week’s expiry after the long weekend since it was no longer present for the 23 FEB 24 expiry. The lookback feature on Schwab’s thinkorswim shows implied volatility at the 1300 strike was ~180%, while at the short strikes, it was ~200%.

A quick check of SpotGamma’s implied volatility skew tool reveals a still-elevated call skew. Awesome!

Soon after, despite minor volatility shifts, we added similar trades with strikes that were further from the current price.

Gauging implied volatility accurately using the lookback feature can be tricky, but we observed that the difference in implied volatility between the strikes was narrowing. This indicated that the volatility skew was “flattening.” In simpler terms, the implied volatility between different strikes was becoming more similar, unlike a steeper skew where the farther strikes have much higher implied volatility. This can be good for the trade.

Here’s a chart that illustrates this “flattening” volatility skew. While this example shows the S&P 500, the concept is the same. Pay attention to the blue versus green line!

Anyways, back to the charts. So, here’s the price action. Straight down!

On February 22, we rotated more into similar structures we started working on February 20.

SOLD -1 1/2 BACKRATIO SMCI 100 (Weeklys) 8 MAR 24 1400/1600 CALL @1.10

At the time of entry, lookback showed the implied volatility of the 8 MAR 24 spreads was around 145% for the long and 155% for the short strikes. At the second entry, the volatility spread between the strikes started narrowing. Overall volatility came down, but the difference between the strikes was about the same.

Here’s what the volatility skew looked like at this point. This is a 30-day look back (the shadow).

I ended up closing the 1 MAR 24 spreads on February 22 for up to a 1.00 cr.

Here’s the implied volatility for the 1 MAR 24 options chain. Again, while a bit lower than when we started, the difference between the two is roughly the same. The passage of time is definitely working in our favor, here!

I’ll note that I closed prematurely because underlying price action suggested we could trend higher, with the upper VWAP band as an upside target. The spreads ended up pricing for $1.00 more in credit. Take what you can get, Renato!

The challenge we faced was deciding whether closing and rotating the trade early would lead to additional profits. Ultimately, we rolled the position and made money either way, but this was the thought at the time. In other words, are we doing too much?

After closing the 1 MAR structure, we added 8 MAR structures on February 22. Trade tickets for one account below. These additions made the position larger than I wanted, so I bought cheaper crash options to manage the margin (the amount of money required to maintain the position) first and foremost. It was a tense moment! Thankfully, with these additions, we stayed within our limits and didn’t breach any safety thresholds.

SOLD -12 1/2 BACKRATIO SMCI 100 (Weeklys) 8 MAR 24 1400/1600 CALL @1.05

At this point, the lookback showed implied volatility for the short strikes was around 160%, while the long strikes were at 150%. The difference between the two was around 10%.

Again, IV refers to the market’s expectations of future price movement expressed as a percentage. A higher IV suggests more movement, while a lower IV suggests less movement.

This is what the chart looked like at that time.

Around 2 PM, the market struggled but recovered, finishing higher by the close. The trades moved against me slightly, but the ATM and ITM entry and holding criteria (i.e., credit to close) mentioned above were still met, so I stuck with it.

Regarding having to hedge, I just focused on the spread’s sensitivity to price movements. Despite intense price action, the Greeks were okay. I remained in the position for about a week and a half. After the first week, the spread moved in my favor, but not to the extent I had hoped.

To explain, implied volatility remained higher on the short strike but dropped more on the long strike. Had the volatility on the short strikes dropped significantly more, the spreads would have likely come off sooner. Pricing the 15 MAR 24 spreads, those were trading for a debit to close, and it did not make sense to do anything other than sit on my hands and wait. If the stock continued to rise, which eventually occurred, the spread had more potential. Here’s the lookback at the time.

This is the price chart at month-end. It felt like there was more room to go up.

After the weekend, there was a big overnight move. Traders caught the news that SMCI would be included in the S&P 500.

I used the gap as a gift and sold into it, monetizing spreads from 3.00 to 5.05 cr to close. Trade tickets for one account follow.

5.05 marked the top in the structure’s pricing despite the stock moving higher after 10:00 AM. It took me years of watching these structures to spot softening sensitivity in the spread, prompting such closure. Had this gap not happened, the spreads likely would have been closed for small credits (0.05 cr). Again, the gap was a gift. Take it, Renato!

At this point, I am already considering rinsing and repeating this trade. The 15 MAR 24 200-point spread fully ITM traded for a small credit to close, which was unsafe. I widened accordingly to a 250-wide spread, priced for a very thick credit to close—the lookback shows about 44.00 cr. Here’s the lookback.

So, we went out to 1300/1550. There, I saw 1x2s pricing for thick credits to open.

SOLD -1 1/2 BACKRATIO SMCI 100 15 MAR 24 1350/1600 CALL @3.05

The implied volatility at the 1300 strike was ~150%, and at the 1550 strike, it was ~175%. We entered an hour early without regard for the stock chart (above), which was a costly mistake. The stock ripped higher, resulting in a ~$2.00 loss per spread.

Notably, the implied volatility skew steepened on the day of entry. Here’s a visual.

However, later that day, the spreads settled down. At 1:40 PM, the stock peaked, and the pricing of the 1300/1550 we put on declined slightly. To manage risk, I closed some units there. In any case, the spread narrowed, owing to a flattening and stickiness of the skew; 1300/1550 = 150/175% (~25% spread) → 140/160% (~20% spread). If I waited longer, the additional units would have gone massively in my favor. Oh, well!

Over the next few days, the stock moved down and then up; overall, the stock stayed flat. During this time, the spread increased in value, working in my favor. With these spreads, you want drift, not protracted movement!

My targets were at 5.00 and 10.00 cr to close, as I got over the next day or so. Implied volatility didn’t budge much. Based on thinkorswim’s lookback feature, it rose in the long strike more than the short strikes, which is what you want to see. Decay helped!

I wanted to hold longer because the spread 50 points closer to the money was pricing at 10.00 cr to close, about 3-5.00 cr more than I had my pricing for. Based on the stock price chart, we were peaking, but these moves tend to go sideways or higher for a bit longer. Candle shadows tend to get tested!

If we fast forward, the session was quiet, with SMCI trading sideways to lower from the open. The pricing of the spread went as high as 10.00 cr (at which point I started to monetize).

Here’s what implied volatility looked like (i.e., a rise in the long strike, whereas the short strike stayed about the same).

After the close, I started thinking, “Man, I should have closed that last spread.” It went to my target, but I kept holding (correctly), as you want to maintain some runners. However, the price action was weak into the evening, after the market closed, and I was now concerned I would lose all or most of the profit in my remaining spread. Mental games, here. Patience, Renato!

The market opened sideways the next day. I monetized my last spread for 11.00 cr, close to its peak.

Here are the implied volatilities at the exit (i.e., noticing the more significant drops in short strikes relative to the long ones).

There’s a critical factor that helped the trade keep its value. The stock went sideways, and a day or so passed, allowing some of the decay to kick in. The decay disproportionately affected the further OTM strikes (i.e., there’s more to decay than usual), with the lookback showing implied volatility dropped to 135% long / 150% short a few minutes after I closed my position. The market was attempting to go higher, volume was low on the 1300 strike, and the spread ended up pricing higher than what I closed it for. Bummer! Here’s what it looked like.

On March 8, the market peaked, hitting the 1200 figure I had envisioned. 1200 was a target for me due to the amount of interest (open interest and volume) at that strike, as well as the trend of the market. The March 4 shadow would also be taken based on the March 5-7 price action. Essentially, we traded up to and held short of the March 4 high, and the spread increased in value by $10.00 cr. I could have doubled my profits for the trade, but at the risk of losing it if things had gone the other way. Remember February 22, when the extreme volume was at the 1000 strike and above? We failed there. This was a blow to options buyers!

On March 8, 10-15 minutes after the market opened, implied volatility for 1300/1550 per thinkorswim’s lookback showed a much more significant drop in further OTM strike as the stock went up by $33 in that one day. Vol down, stock up, weekend decay, and that’s how a spread that priced 5.00 cr to close two days before ended up trading to 25.00 cr to close. Here’s the lookback.

On March 11, the stock traded much weaker. Implied volatility on the 1300/1550 went to 150/170%. Despite this, the trade lost a lot of delta, which the implied volatility bump couldn’t make up. The lookback shows the trade went to a 7.00 cr, a ~70% loss. This is what I say you’re up against. There’s not a lot of give to work with at times.

At this point, I realized I was doing what I was supposed to: take what I could get. Sometimes, the risk of losing what you made is not worth the potential reward. The trade was done after the stock hit 1200 (a location where I struck a bunch of Fibonacci extensions, too).

Finally, this is what the implied volatility skew looked like on March 8, the peak day.

In conclusion, this trade demonstrated one of my better executions. Over the month, SMCI traded sideways, and I captured about $24,000 in premiums across a couple of accounts. As I told my trading partner, the execution felt “divine”; there were plenty of moments where we could have made big mistakes—being too greedy, sizing too large and having to delta hedge in response, entering or exiting at the wrong times, or letting fears take over. However, the SMCI trades show improved thinking and acting quickly. Continuous improvement is all this is about—and that’s all I can ask for!

Some thoughts from this experience include waiting for market capitulation when the excitement fades, which helps spot better opportunities to trade the above structures. I identify these trades by scanning for high implied volatility, tracking a watchlist daily, sizing trades appropriately, and monitoring them closely; I size appropriately when I spot potential trades and save those trades (i.e., keep them in my monitor tab). I also suggest tracking implied volatility at specific strikes and keeping detailed notes; if you see a pattern, note it and decide whether adding or reducing the position is worth it. Additionally, holding onto “runners” (remaining positions) can significantly boost profits, as seen with the trades expiring on 15 MAR. Also, consider what may happen if the underlying moves toward the spreads and how you’ll react, adding, hedging, or reducing size.

What’s your favorite engagement trade when the fear of missing out is so great? Let’s discuss.

Disclaimer

By viewing our content, you agree to be bound by the terms and conditions outlined in this disclaimer. Consume our content only if you agree to the terms and conditions below.

Physik Invest is not registered with the US Securities and Exchange Commission or any other securities regulatory authority. Our content is for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any security or other investment. The information provided is not tailored to your financial situation or investment objectives.

We do not guarantee the accuracy, completeness, or timeliness of any information. Please do not rely solely on our content to make investment decisions or undertake any investment strategy. Trading is risky, and investors can lose all or more than their initial investment. Hypothetical performance results have limitations and may not reflect actual trading results. Other factors related to the markets and specific trading programs can adversely affect actual trading results. We recommend seeking independent financial advice from a licensed professional before making investment decisions.

We don’t make any claims, representations, or warranties about the accuracy, completeness, timeliness, or reliability of any information we provide. We are not liable for any loss or damage caused by reliance on any information we provide. We are not liable for direct, indirect, incidental, consequential, or damages from the information provided. We do not have a professional relationship with you and are not your financial advisor. We do not provide personalized investment advice.

Our content is provided without warranties, is the property of our company, and is protected by copyright and other intellectual property laws. You may not be able to reproduce, distribute, or use any content provided through our services without our prior written consent. Please email renato@physikinvest for consent.

We reserve the right to modify these terms and conditions at any time. Following any such modification, your continued consumption of our content means you accept the modified terms. This disclaimer is governed by the laws of the jurisdiction in which our company is located.

Financial markets tend to oscillate like a pendulum, but recently, the fluctuations have intensified. For example, interest rates rapidly climbed from zero to 5%, and markets often alternate dramatically between despair and euphoria.

Decades-long policies concentrating wealth and incentivizing risk-taking are at the heart of these fluctuations. Central bank interventions, passive investing, and regulatory quirks have created fertile ground for dislocations and headline-grabbing events like the GameStop saga in 2021. For younger generations, these dynamics have been particularly tough. Millennials and Gen Z face delayed milestones, diminishing wealth, and growing skepticism about traditional, centralized financial structures.

Jannick Malling, co-founder and co-CEO of Public.com, aims to help investors adapt and thrive in this evolving landscape. In our latest podcast, Malling explains how Public engages a newer, active generation of investors.

You can watch the linked full video and/or read about some key points below.

Who is Jannick Malling?

Malling, of Danish descent, began his entrepreneurial journey in Copenhagen. His childhood curiosity about technology led him to build computers and explore the digital world. What started as a simple interest soon became a passion, as he began creating websites to organize video game meetups and help small businesses increase their visibility.

“You spend a lot of time in front of the computer, and you can’t be gaming 24/7,” he reflects. “So, when you’re not gaming, you’re just hanging out online, and I started to get excited about building websites. I wanted to design to solve problems, and this led to finding the design process so incredibly rewarding, interesting, and fulfilling that I just stayed with it my whole life.”

Unconventional for a 17-year-old, Malling later entered the professional world by joining Saxo Bank, a fintech that radically transformed investing in Europe. The experience was incredibly formative, teaching Malling about work ethic and the importance of speed, adaptability, and user-centric design—principles that continue to guide him at Public today.

Malling parallels his experience after Saxo Bank with that of the PayPal Mafia, a group of former PayPal employees who went on to shape the tech and venture capital worlds. Like PayPal’s Peter Thiel, Reid Hoffman, and Elon Musk, Malling and his Saxo Bank colleagues stayed connected, collaborating on new ventures after leaving the company.

Why build Public.com?

After co-founding and building several companies, Malling took a break and moved to New York City. Frustrated with managing his portfolio as a retail investor, he realized fractional shares could ease rebalancing and dollar-cost averaging for everyday investors. Inspired by this insight, he designed mockups for an app with a Venmo-like user experience. This ultimately became Public.com.

“I think there’s always been this overarching trend of leveling the playing field between institutions and individual investors,” Malling explains, highlighting Public’s focus on providing better information, community, and access at a lower cost. “Now, the question is what they should buy and why, which is where the research comes in.”

Retail brokerage platforms usually offer research, which can be challenging for investors without financial expertise. However, thanks to recent AI advancements, Public has enhanced its offerings, introducing products like Alpha.

“When ChatGPT came out, our imaginations were captured, and we started tinkering with this intersection of research and LLM interfaces,” he says. “Now, you can go to a stock on Public and ask any question. It’ll answer immediately, scanning the earnings files, financials, and analyst ratings. The process of researching a company is so much higher quality, and we’ve been able to drive AI hallucinations to basically zero, improving trust.”

Alpha has proven so effective in answering investor questions that Public launched it as a standalone platform. Those with a Public account can access Alpha for free, while those without can subscribe for just $1 weekly.

“Just screenshot your Apple Stocks, and Alpha auto-follows all those stocks, constantly scanning and telling you not just if they’re moving, but why they’re moving. That’s a great example of how AI can enhance the research experience without requiring people to dig too deep, creating more informed investors.”

Why did Public ditch PFOF?

In 2021, Public discontinued payments for order flow (PFOF). This decision underscores a more significant concern: the shortcomings of the National Best Bid and Offer (NBBO) system, which represents the best available bid and offer prices for equities across U.S. exchanges, serving as a benchmark for order execution.

The NBBO was created long before retail investing and zero-commission trading rocketed. Malling notes that it is based on market volumes of 100 shares or more, leaving out much of the current retail trading activity, like fractional and smaller trades. Although retail trading now accounts for a substantial share of market volume—sometimes over 40%—the NBBO does not adjust to this; firms complying with NBBO standards may provide prices that are not the best available.

“Retail makes up a much larger part of the market, but the NBBO doesn’t consider that in its reference price,” Malling explains. “So, sort of the hurdle that you have to clear is a little broken, which means that some firms can say, ‘Hey, we gave you the NBBO,’ but there may be a price that nobody else sees that’s lower than that.”

However, Public continues using the PFOF model in options trading, which works differently.

“In the options world, orders must be posted to an exchange, which creates more competition and drives better customer outcomes,” Malling explains. Public also shares up to 50% of its order flow rebates with customers. “You make what we make on your flow, so for those customers, it’s just incredibly transparent.

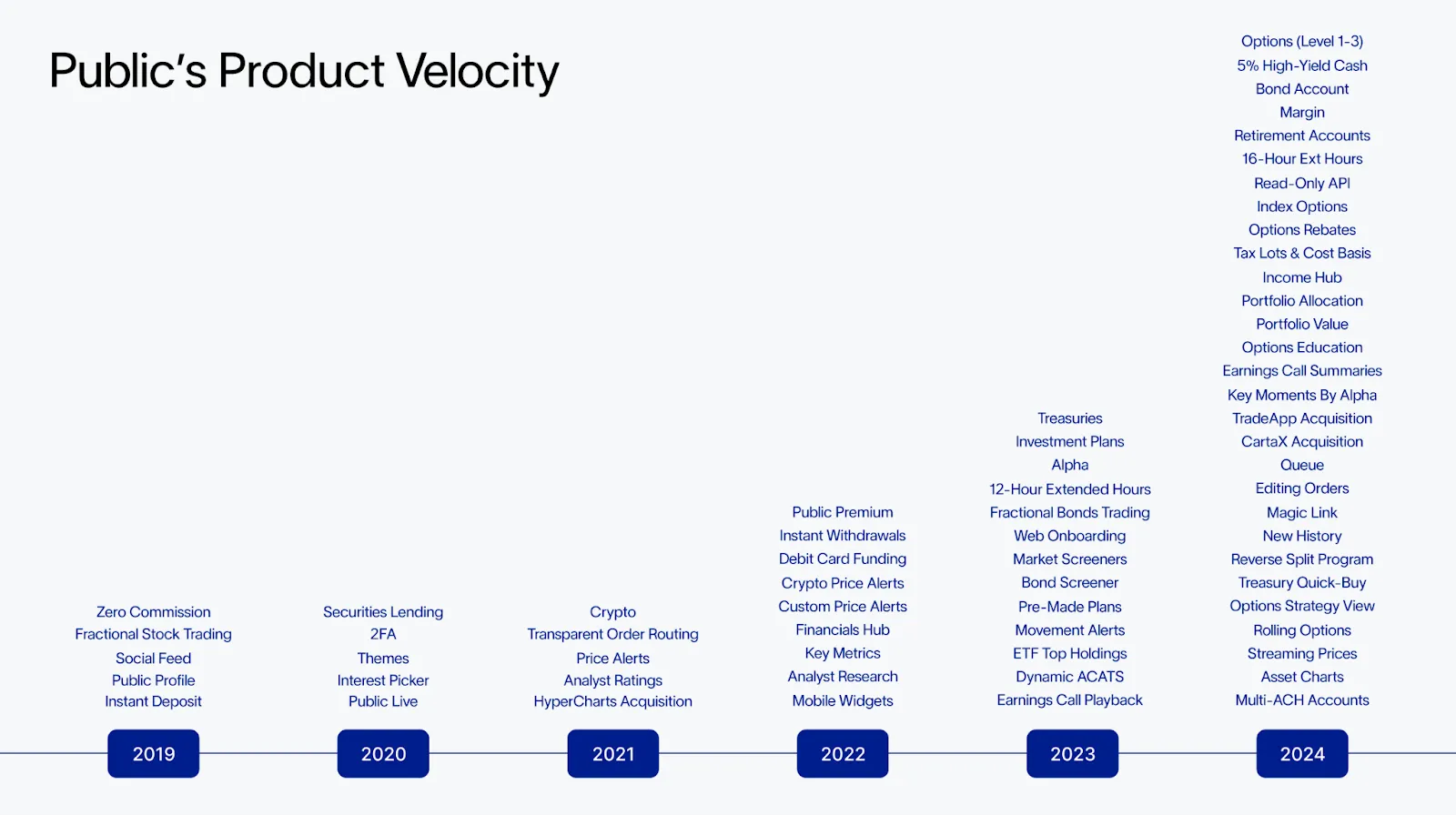

How does Public launch quicker?

Last year, Public launched a significant new feature roughly every ten days. Malling attributes this speed and adaptability—such as launching options on cash-settled indexes and Bitcoin in just over two weeks—to the company’s horizontal tech stack, lean team, and commitment to minimizing technical debt.

“Most big players in the space rack up technical debt, which happens when code is written in a way that makes it hard to maintain or further develop,” Malling elaborates. “To add new products, you’re forced to rewrite entire features, which slows down product velocity. Our engineers are allergic to that. By building a horizontal stack, we can move much more quickly.”

Partnerships that mitigate risks in everything from clearing to custody bolster this adaptability, enabling Public to concentrate on providing valuable features like seamless, real-time money transfers across asset classes, unified performance reporting, and tax optimization tools—all accessible via a single login for multiple account types, including cash, margin, IRA, and trust accounts.

What’s Public positioning for?

Looking ahead, Malling sees enormous opportunity in the ~$100 trillion wealth transfer from Baby Boomers to Millennials and Gen Z. These generations grew up with information at their fingertips and distrust in traditional financial structures. Accordingly, they seek alternatives like DIY investing, which, as was discussed, Public is making easier.

“This shift will redefine how wealth is managed. Younger generations are fundamentally different in how they approach investing, prioritizing transparency, technology, and self-direction,” he says. “Now, I have all the tools in the world to do it myself, which is the simple one-two punch that puts this generation on a fundamentally different path.”

For more, please consider watching the YouTube interview. Jannick Malling can be followed on LinkedIn and Twitter/X. Thank you!

Disclaimer

By viewing our content, you agree to be bound by the terms and conditions outlined in this disclaimer. Consume our content only if you agree to the terms and conditions below.

Physik Invest is not registered with the US Securities and Exchange Commission or any other securities regulatory authority. Our content is for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any security or other investment. The information provided is not tailored to your financial situation or investment objectives.

We do not guarantee the accuracy, completeness, or timeliness of any information. Please do not rely solely on our content to make investment decisions or undertake any investment strategy. Trading is risky, and investors can lose all or more than their initial investment. Hypothetical performance results have limitations and may not reflect actual trading results. Other factors related to the markets and specific trading programs can adversely affect actual trading results. We recommend seeking independent financial advice from a licensed professional before making investment decisions.

We don’t make any claims, representations, or warranties about the accuracy, completeness, timeliness, or reliability of any information we provide. We are not liable for any loss or damage caused by reliance on any information we provide. We are not liable for direct, indirect, incidental, consequential, or damages from the information provided. We do not have a professional relationship with you and are not your financial advisor. We do not provide personalized investment advice.

Our content is provided without warranties, is the property of our company, and is protected by copyright and other intellectual property laws. You may not be able to reproduce, distribute, or use any content provided through our services without our prior written consent. Please email renato@physikinvest for consent.

We reserve the right to modify these terms and conditions at any time. Following any such modification, your continued consumption of our content means you accept the modified terms. This disclaimer is governed by the laws of the jurisdiction in which our company is located.

This edition shouts out Public.com, a multi-asset investing platform built for those who take investing seriously. Public recently launched Alpha, an AI investment exploration tool, in the app store. We’re excited to host co-founder and co-CEO Jannick Malling on the next podcast to discuss the market and how AI levels the playing field. Stay tuned!

When market expectations drift too far from underlying fundamentals, they eventually become unsustainable. This sometimes leads to corrections that can trigger cascading effects across the broader market.